Financial Statements Economics 98 / 198 Fall 2007 Copyright 2007 Jason Lee.

34

Financial Statements Economics 98 / 198 Fall 2007 Copyright 2007 Jason Lee

-

date post

21-Dec-2015 -

Category

Documents

-

view

220 -

download

0

Transcript of Financial Statements Economics 98 / 198 Fall 2007 Copyright 2007 Jason Lee.

Financial StatementsEconomics 98 / 198

Fall 2007Copyright 2007 Jason Lee

Announcements

• Oct 31 versus Nov 31 lecture?

• Simulation Exercise - Money

CURRENT EVENT / NEWS

LECTURE CONTENT

Today’s Lecture

• Trading Psychology• Financial Statements introduction

– Income Statement– Balance Sheet– Cash Flow Statement– Earning Season

• Ratio Analysis

TRADING PSYCHOLOGY

Trading Psychology

Emotions severely impair your judgment in deciding whether to buy or sells tocks

HOPEFEARGREEDPRIDE

Psychology & The Stock Market

•Emotions can wreak havoc on your results and decisions

•Need to take emotion out of investing

•Do this by developing a system with rules to follow with discipline

Trading Psychology

“Your biggest enemy, when trading, is within yourself. Success will only come when you learn to control your emotions”

- Edwin Lefevre

Accounting 101:

Financial Statements

Reporting Financial Statements

•Public co. required to publish 10K and 10Q– 10K = Annual financial reports– 10Q = Quarterly financial reports

Income StatementBalance SheetStatement of Cash Flows

• Why do we care about these reports?

The Income Statement

•Shows how much a company earned or lost during that specific period

•Considered the most analyzed statement for investors

•Divulges into a company’s profitability

IS THE COMPANY MAKING PROFIT?

Income Statements

•Generally, 3 Major Parts– Revenues– Expenses– Net Income

•Earnings Per Share (EPS)= Profits / Shares Outstanding

•Investors pay very close attention to profits (earnings) and revenue (sales)

Income = Revenues - Expenses

Balance Sheet

•Summarizes company’s assets, liabilities, and shareholders’ equities at specific time

Assets = Liabilities + Shareholder’s Equity

•How do we analyze this statement?• We use ratios and changes in trends to analyze

the information

Balance Sheet

Assets– Current Assets: life span of 1 year or less– Non-Current assets

Liabilities– Current Liabilities– Non-current liabilities

Shareholder’s Equity– Common / Preferred Stock– Retained Earnings

Statement of Cash Flows

• Shows how much money coming in (inflows) and going out (outflows)– Cash flow from operations – Cash flow from investing– Cash flow from financing

• Shows if company having trouble with cash– Profitable companies can struggle cash flows. Why?

• Cash is king! Pays for bills and funds

operations!

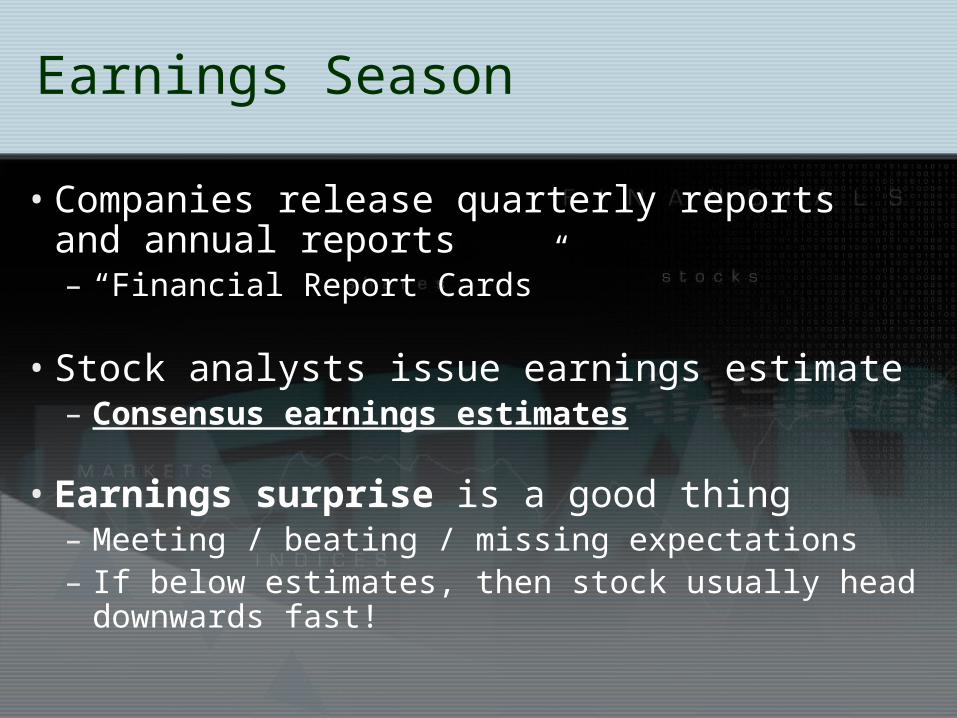

Earnings Season

• Companies release quarterly reports and annual reports– “Financial Report Cards”

• Stock analysts issue earnings estimate– Consensus earnings estimates

• Earnings surprise is a good thing– Meeting / beating / missing expectations– If below estimates, then stock usually head

downwards fast!

Understanding Earnings

•Actual earnings value is important, but so is the growth of these earnings

•Compare EPS / Revenue?– Do we compare them to last quarter?– Do we compare them to the same quarter

last year?

EPS % Growth: Google Q2 2007Source: MSN Money Stock Quotes

EPS growth calculated comparing Q2 2007 to Q2 2006

Q2 2007EPS Growth

2007 Q2 EPS

2006 Q2 EPS

$2.98 / sh

$2.39 / sh

=25%

Why do Investors Care About Earnings?

•Strong earnings or expectations of strong earnings drive stock prices. Why?

– Potential for greater reinvestment, and greater earnings

– Passing the money to shareholders in various forms (dividends, buybacks, etc.)

•Ultimately, earnings provide a return on the investment for shareholders

Ratio Analysis

Ratio Analysis

• Used to gain idea of valuation and financial performance

• Compared to competitors and historical values to gain understanding about company’s value– Is it undervalued? Overvalued?– How is it performing?

Profit Margins

Profit Margins• = net income / net sales (revenue)

– Measures how much out of every dollar of sales a company actually keeps in earnings

• High profit margins indicates that management efficient at controlling costs– Increased earnings are good, but if costs are increasing

faster than sales, leads to lower profit per sale

• Good sign if company has growing profit margins

Profit Margins: Example

Company has a net income of $10 million from sales of $100 million, giving it a profit margin of 10% ($10 million/$100 million)

If in the next year net income rose to $15 million on sales of $200 million.

Would its profit margins be growing or diminishing? What does this mean?

Price to Earnings Ratio (P/E)

P/E Ratio• = Price per share / Earnings per share

– Look at company’s earnings relative to its price

• Most basic valuation method of company– How do you we use it?

• Ex. If BIG OIL co. has P/E ratio of 15 and has solid fundamentals, and the industry average is 40, then the BIG OIL would be considered undervalued

Price to Earnings Ratio (P/E)

• Use as a guide, not a guarantee in your analysis

• Sometimes, there is a reason for high or low P/E ratios (understanding business and industry is important)

– High P/E ratios: investors may be willing to pay more for less earnings because its expect higher growth rates in the future

– Low P/E ratios: may seem like a bargain, but low ratio may signal questionable future prospects

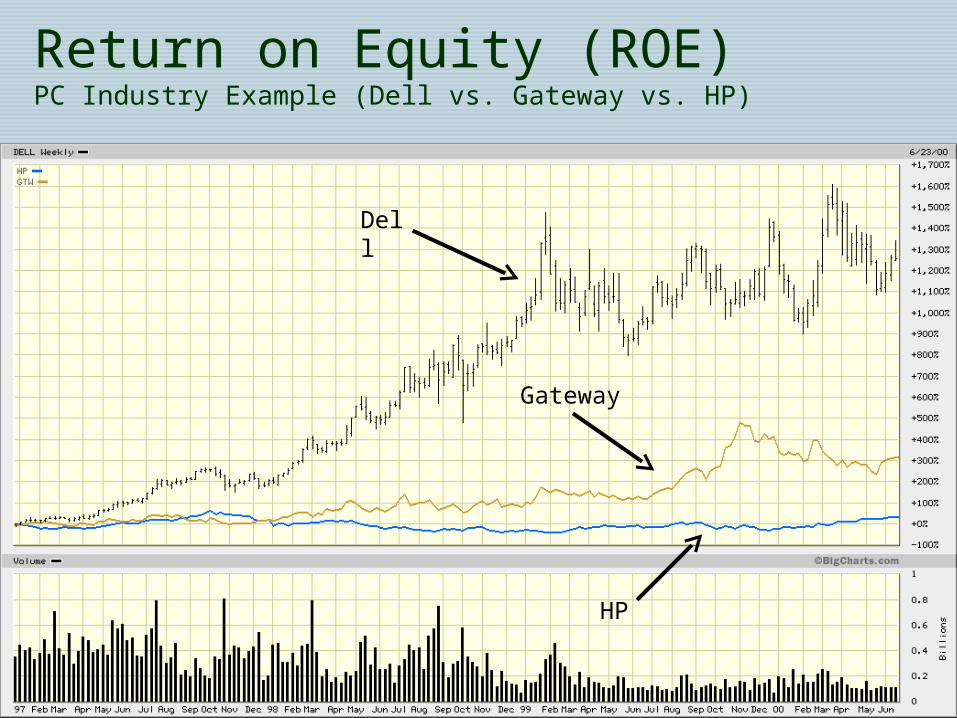

Return on Equity (ROE)

Return on Equity (ROE)• = Net Income / Shareholder’s Equity

– how much profit a company can generate with the money shareholders have invested

– Is it a profit-making machine or an inefficient clunker?

• Useful for comparing profitability and efficiency of a company to other firms in same industry– can indicate whether a company is growing without pouring

new capital into business

• Growing ROE also shows management making better use of money invested by shareholders

Return on Equity (ROE)PC Industry Example (Dell vs. Gateway vs. HP)

Dell

HP

Gateway

Debt-to-Equity Ratios

Debt / Equity Ratio• = Total Liabilities / Shareholder’s Equity

– Proportion of equity and debt to finance assets

• High ratio: aggressive debt, potential for higher earnings per share but at more risk– More volatile earnings and larger interest expenses

• Compare this similar companies• Warren Buffet preferred to see lower ratio so that

earnings growth is generated by investors rather than borrowed money

Google Example

2004 2005 2006Profit Margin 13% 24% 29%

ROE 14% 16% 18%

Debt / Equity 0.13 0.09 0.08

EPS Growth 344% 198%

Other Relevant Ratios

• Current Ratio• Return on Assets• Inventory Turnover• Interest Coverage

More on Ratio Analysis / Financial Statement Analysis:

http://www.investopedia.com/university/ratios/ratios1.asphttp://www.investopedia.com/university/financialstatements/

UGBA 102A: Introduction to Financial Accounting

Reading

• Motley Fool. “Analyzing Stocks”

• Recommended:Investopedia. “Valuation”