Financial Statement Analysis / Entrepreneurial Finance.

54

Financial Statement Analysis / Entrepreneurial Finance

-

Upload

marsha-lyons -

Category

Documents

-

view

218 -

download

0

Transcript of Financial Statement Analysis / Entrepreneurial Finance.

Financial Statement Analysis / Entrepreneurial

Finance

Financial Analysis Overview

• An assessment of a company’s past, present and future financial condition

• Purpose is to diagnose company’s financial strengths and weaknesses

• Primary tools– Financial Statements– Ratios

Financial Statements

Main Financial Statements

• Balance Sheet

• Income Statement

• Statement of Cash Flows

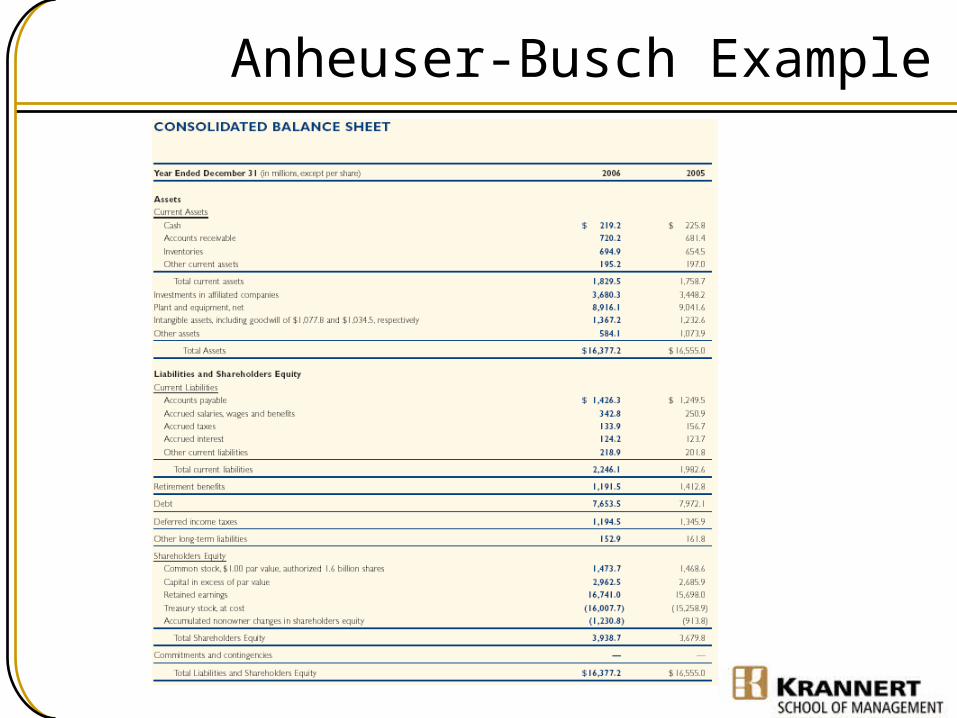

The Balance Sheet

• The balance sheet shows a firm’s assets (what it owns) and liabilities (what it owes)

• The difference between a firm’s assets and liabilities is the firm’s net worth

• A snapshot in time

Balance Sheet Items

Assets• Current assets:

– Cash & securities– Accounts Receivable– Inventories

• Fixed assets:– Tangible assets like

PPE– Intangible assets

Liabilities and Equity• Current liabilities:

– Accounts payable– Short-term debt

• Long-term liabilities• Shareholders' equity

Anheuser-Busch Example

Income Statement

• The income statement summarizes revenues and expenses for the business

• Covers an interval of time (monthly, quarterly, annually)

• Major components:– Revenues– Expenses– Taxes– Extraordinary Items

Income Statement Format

Sales revenue- Cost of goods sold= Gross profit margin- Operating expenses= EBITDA- Depreciation & Amortization= EBIT (Operating income)- Interest payments= Taxable income- Taxes= Net Income

Anheuser-Busch Example

Accounting vs. Economic Earnings

• Accounting definition of earnings ignores unrealized changes in market value of assets and liabilities

• Accounting profit does not recognize cost of equity capital

• Accounting profit may not contain all relevant costs– e.g., opportunity cost of entrepreneur’s time

Cash Flow Statement

• Summarizes the levels of cash being generated or consumed by the business

• Covers an interval of time (monthly, quarterly, annually)

Cash Flow Statement Format

Cash flow from operationsNet income

+ Depreciation- Increase in accounts receivable- Increase in inventories+ Increase in accounts payable

Total cash flow from operations

Cash flow from investing activities- Investment in plant and equipment

Cash flow from financing activities- Dividends paid+ Increase in short-term debt

= Change in cash

Anheuser-Busch Example

Statement Connections

• Excel example

Ratio Analysis

Why do ratio analysis?

• A means of evaluating and diagnosing performance• Ratios standardize numbers and facilitate comparisons

– Comparing performance to competitors or industry standards (horizontal comparison)

– Comparing performance to prior history (vertical comparison)

• Examine a variety of areas– Liquidity– Solvency– Efficiency– Profitability

• Remember that ratios are meaningless unless you have something to compare

Major Ratio Categories

• Liquidity– ability to cover short-term obligations

• Solvency– ability to cover long-term obligations; examines mix of debt and

equity

• Efficiency– amount of activity generated by resources deployed

• Profitability– amount of profit generated by resources deployed

• Market value (if applicable)– some of these ratios (e.g. price-earnings ratio, market-to-book

ratio) are useful in valuation analysis, such as valuing private firms

Liquidity Ratios

• Current Ratio– The ratio between all current assets and all current liabilities.– Formula:

• Current Assets Current Liabilities

• Quick Ratio – The ratio between all assets quickly convertible into cash (this

excludes inventory) and all current liabilities. – Formula:

• Cash + Accounts Receivable + Short-Term Investments Current Liabilities

Anheuser-Busch Example

Current Ratio:

1829.5 / 2246.1 = 0.81

Quick Ratio:

(219.2 + 720.1 + 195.2) / 2246.1 = 0.51

Solvency Ratios

• Debt to Equity – Shows the ratio between capital invested by the owners and the

funds provided by lenders.– Formula:

• Total Liabilities Total Equity

• Interest coverage ratio – A measurement of the number of times a company could make

its interest payments with its earnings before interest and taxes; the lower the ratio, the higher the company’s debt burden.

– Formula:• Pretax Operating Income + Interest Expense Interest Expense

Anheuser-Busch Example

Debt to Equity:

(2246.1 + 1191.5 + 7653.5 + 1194.5 + 152.9) / 3938.7 = 3.16

Anheuser-Busch Example

Interest Coverage Ratio:

(2719.6) / 451.3 = 6.03

Profitability

• Gross Profit Margin – Indicator of how much profit is earned on products

without consideration of selling and administration costs.– Formula:

• Sales - COGS Sales

• Net Profit Margin / Return on Sales (ROS)– Shows how much profit comes from every dollar of

sales.– Formula:

• Net Income Sales

Anheuser-Busch Example

Gross Profit Margin:

5552.1 / 15717.1 = 35.3%

Net Profit Margin:

1965.2 / 15717.1 = 12.5%

Profitability

• Return on Equity (ROE) – Determines the rate of return on the investment in the business. – Formula:

• Net Income Equity

• Return on Assets (ROA) – Considered a measure of how effectively assets are used to

generate a return. – Formula:

• Net Income Total Assets

• Return on Invested Capital (ROIC) – Formula:

• Net Income Total Liabilities + Stockholder’s Equity – Current Liabilities

Anheuser-Busch Example

Return on Equity:

1965.2 / 3938.7 = 49.9%

Return on Assets:

1965.2 / 16377.2 = 12.0%

Return on Invested Capital:

1965.2 / (12438.5 + 3938.7 – 2246.1) = 13.9%

Info from income statement and balance sheet

Info from income statement and balance sheet

Info from income statement and balance sheet

Efficiency

• Days in Receivables – This calculation shows the average number of days it takes to

collect accounts receivable (number of days of sales in receivables).

– Formula:• Accounts Receivable

Sales / 365 days• Compare to industry standards.

• Accounts Receivable Turnover – Number of times that trade receivables turnover during the year.– Formula:

• Net Sales Accounts Receivable

Efficiency

• Days in Inventory – This calculation shows the average number of days it will take to

sell inventory – Formula:

• Average Inventory Cost of Goods Sold / 365 days

• Inventory Turnover – Number of times that inventory is turned over (sold) during the

year.– Formula:

• Cost of Goods SoldAverage Inventory

Efficiency

• Asset Turnover– Indicates how efficiently business generates sales on each dollar of

assets.– Formula:

• Sales Total Assets

• Days in Accounts Payable – This calculation shows the average length of time trade payables are

outstanding before they are paid.– Formula:

• Accounts Payable COGS / 365 days

• Accounts Payable Turnover – The number of times trade payables turnover during the year.– Formula:

• COGS Accounts Payable

Anheuser-Busch Example

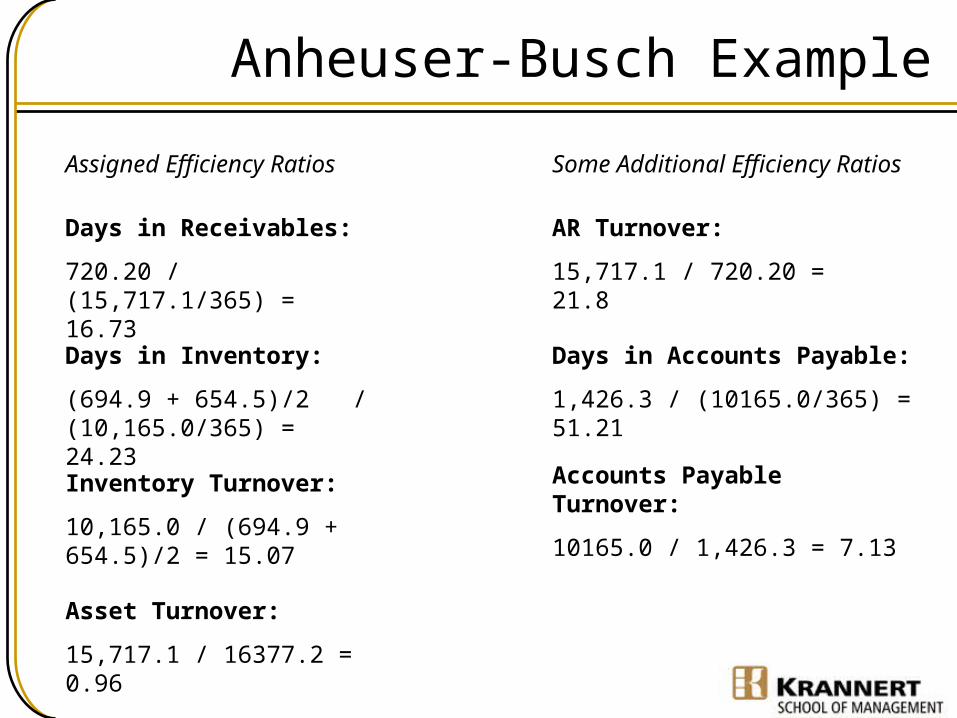

Days in Inventory:

(694.9 + 654.5)/2 / (10,165.0/365) = 24.23

Inventory Turnover:

10,165.0 / (694.9 + 654.5)/2 = 15.07

Days in Accounts Payable:

1,426.3 / (10165.0/365) = 51.21

Days in Receivables:

720.20 / (15,717.1/365) = 16.73

AR Turnover:

15,717.1 / 720.20 = 21.8

Asset Turnover:

15,717.1 / 16377.2 = 0.96

Some Additional Efficiency Ratios

Accounts Payable Turnover:

10165.0 / 1,426.3 = 7.13

Assigned Efficiency Ratios

The DuPont Equation

• ROE = (Net Income/Sales) x (Sales/Total Assets) x (Total Assets/Equity

= profit margin x asset turnover x leverage multiplier• DuPont equation shows how three different areas combine to determine

ROE– expense management (measured by the profit margin)– asset management (measured by asset turnover)– debt management (represented by the debt ratio or leverage

multiplier)

Using Ratio Analysis to Better Understand Profitability

Seemingly Similar Companies

Outback Steakhouses, Inc.

NASDAQ: OSI

Brinker International, Inc.

NYSE: EAT

Darden Restaurants, Inc.

NYSE: DRI

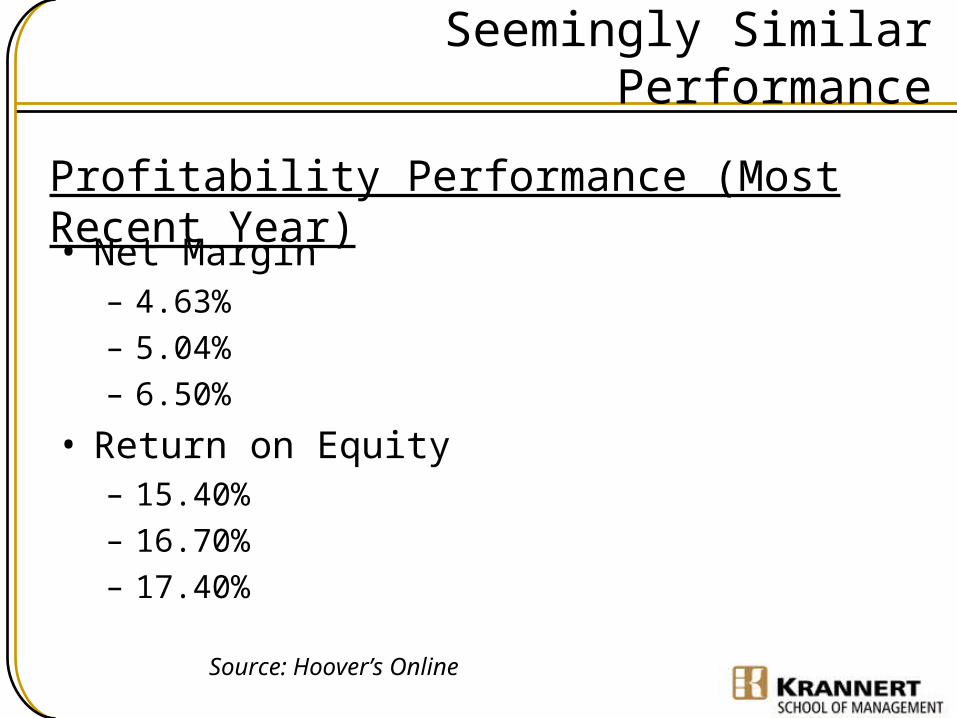

Seemingly Similar Performance

• Net Margin– 4.63%– 5.04%– 6.50%

• Return on Equity– 15.40%– 16.70%– 17.40%

Source: Hoover’s Online

Profitability Performance (Most Recent Year)

Potential Paths to Performance

• High Margins

• High Efficiency

• High Leverage

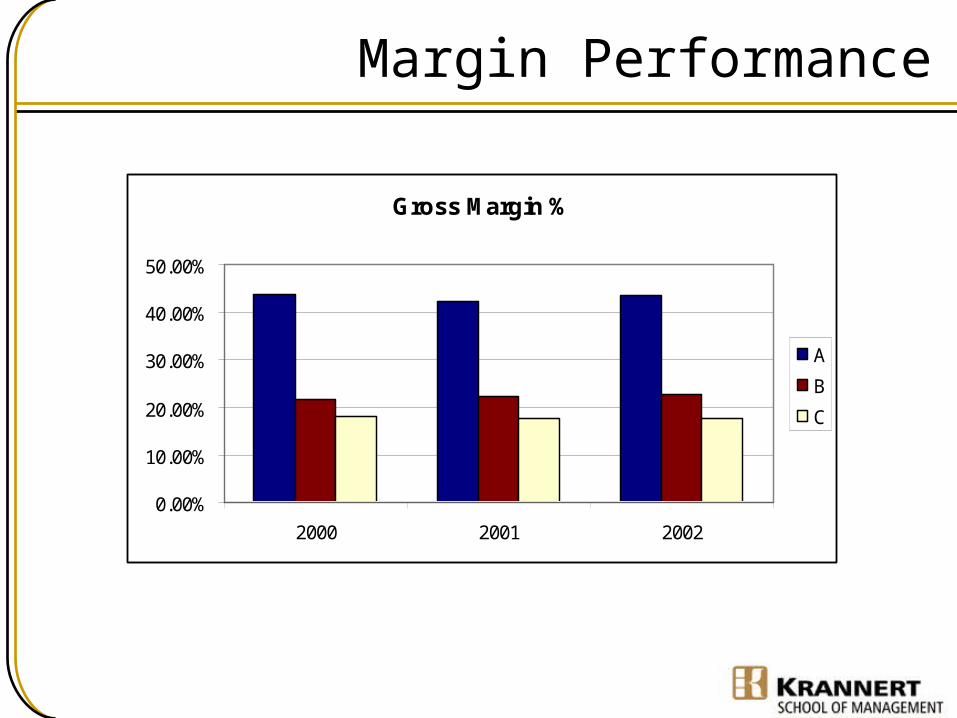

Beginning the Investigation

• Use company’s financial statements– Income Statement and Balance Sheet

• Examine and compare common ratios– Across time– Across companies

• Use three year period (2000 – 2002)

Margin Performance

Gross Margin %

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

2000 2001 2002

A

B

C

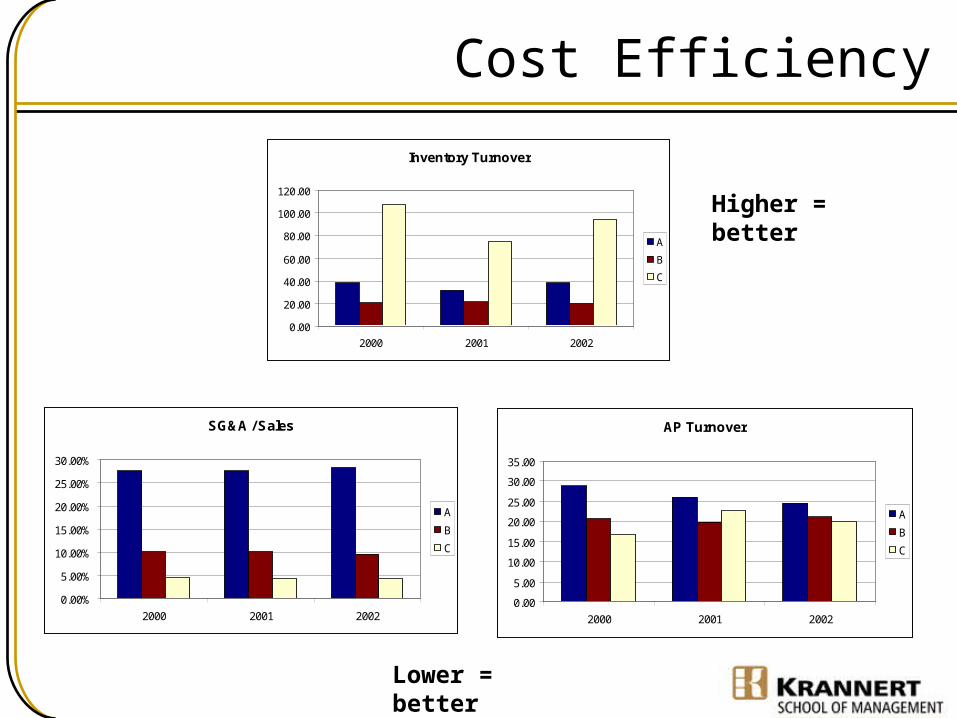

Cost Efficiency

SG&A / Sales

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

2000 2001 2002

A

B

C

Inventory Turnover

0.00

20.00

40.00

60.00

80.00

100.00

120.00

2000 2001 2002

A

B

C

AP Turnover

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

2000 2001 2002

A

B

C

Higher = better

Lower = better

Leverage

Long-Term Debt / Equity

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

2000 2001 2002

A

B

C

Interest Coverage Ratio

0.005.00

10.0015.0020.0025.0030.0035.0040.0045.0050.00

2000 2001 2002

A

B

C

Higher = more levered

Lower = more levered

Summary

• Company A– High margins– Less efficient– Low leverage

• Company B– Moderate margins– Moderate efficiency– High leverage

• Company C– Low margins– High efficiency– Moderate leverage

They run very similar businesses and deliver similar results, but the paths are very different.

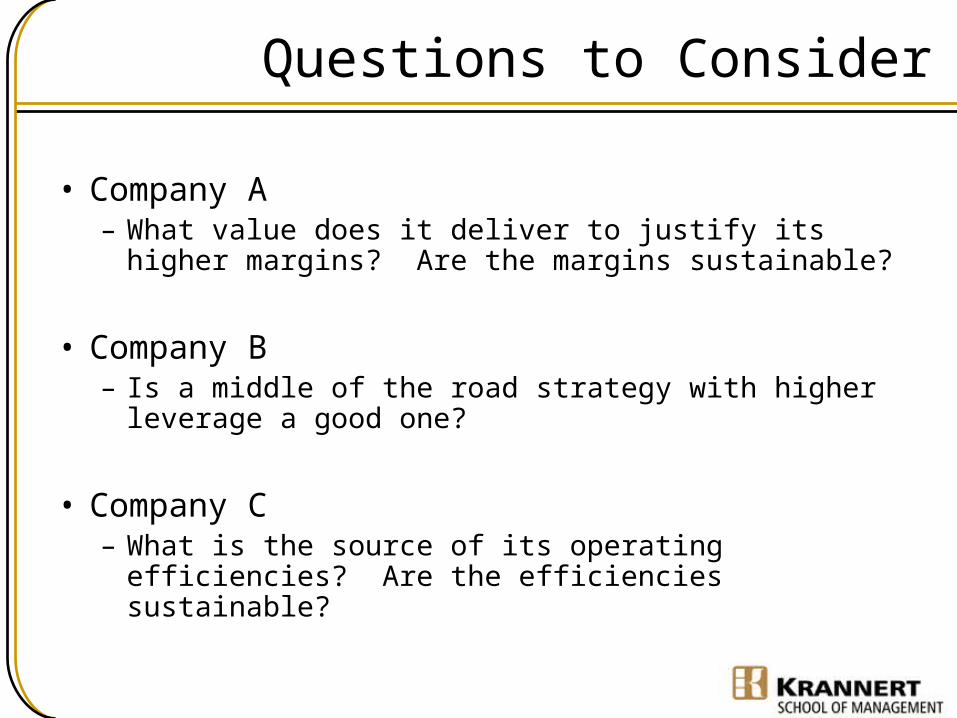

Questions to Consider

• Company A– What value does it deliver to justify its higher

margins? Are the margins sustainable?

• Company B– Is a middle of the road strategy with higher leverage a

good one?

• Company C– What is the source of its operating efficiencies? Are

the efficiencies sustainable?

Who is Who?

• A few additional clues– 2002 sales ($millions)

• A: 2,362• B: 4,369• C: 2,887

– Sales growth (2002 – 2003)• A: 14.4%• B: 6.4%• C: 13.5%

Using Financial in New Ventures

How to use financial ratios in new ventures?

• Remember, financial statements are pro-forma (expectations about what financial position will be)

• Could use average industry ratios as a starting point for generating pro-forma statements

• Pro-forma statements should reflect the underlying strategy of the firm

Adjusting ratios according to your strategy

Key restaurant ratios

Low Cost Strategy

Differentiation strategy

Inventory turnover

(Wages & benefits) / sales

Liquidity

Gross profit margin

Operating costs / sales

Limitations of Ratios

• They are outcome measures; if you have a problem with a ratio, you still have to figure out what’s causing the problem

• Choosing the right comparison data is sometimes difficult– What’s the right industry?– Published industry averages are just rough guidelines– Who are the competitors? – Accounting practices can differ across firms

• Seasonality may affect ratios

• We have only discussed ratios generated from financial statements– These are based on historical data; we would like something that helps predict

future performance– Operational / marketing measures may be more critical– Recall the Balanced Scorecard

Other Values to Consider

• SG&A to Sales– Is company controlling overhead expenses?

• Direct labor utilization– Often critical in professional services companies

• Customer acquisition cost– Compare to lifetime value of a customer

• Others (company-specific)

• Create a Balanced Scorecard

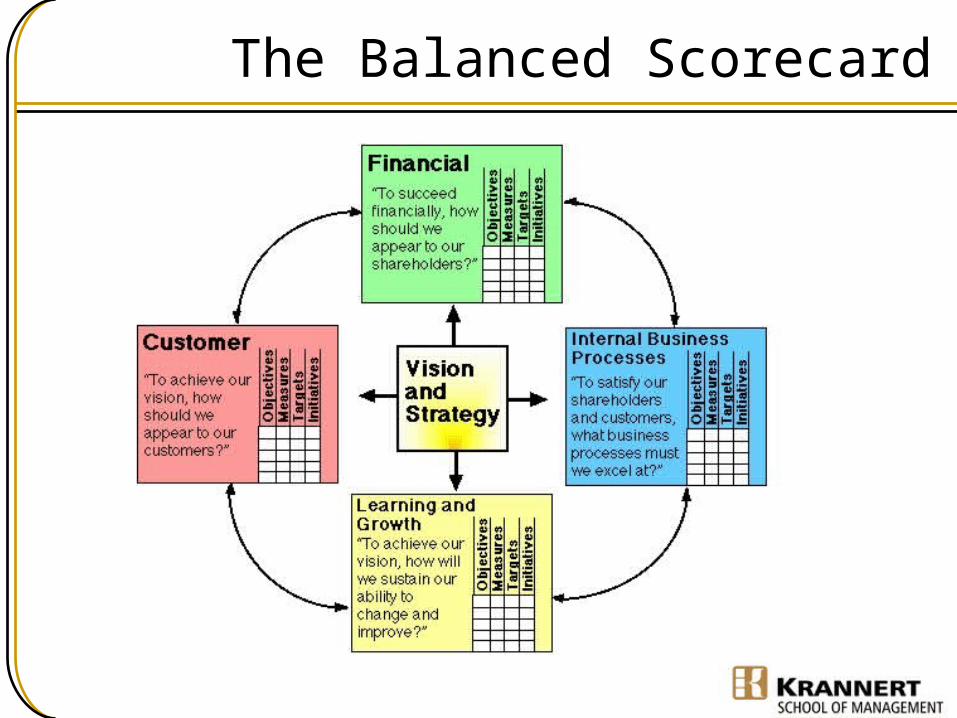

The Balanced Scorecard

Kaplan and Norton (1992)

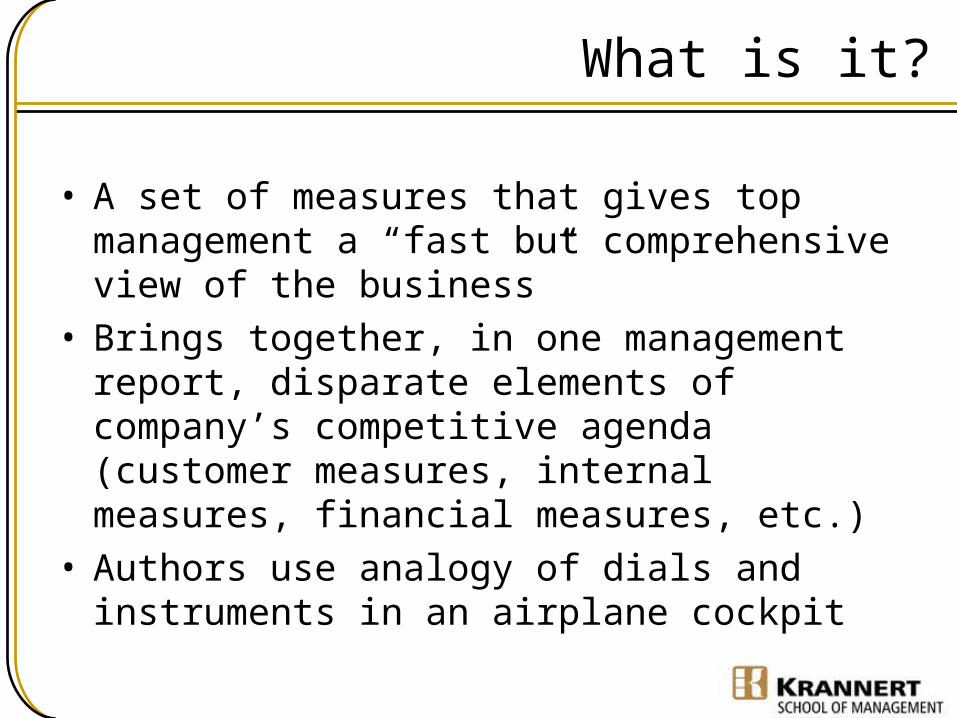

What is it?

• A set of measures that gives top management a “fast but comprehensive view of the business”

• Brings together, in one management report, disparate elements of company’s competitive agenda (customer measures, internal measures, financial measures, etc.)

• Authors use analogy of dials and instruments in an airplane cockpit

Why do it?

• No single measure is adequate

• It’s important to examine the means used to achieve financial outcomes

• Many operational measures translate into future financial results

• Traditional measures might give misleading signals regarding continuous improvement and innovation (focus on short-term results)

The Four Perspectives

• Customer Perspective: How do customers see us?

• Internal Business Perspective: What must we excel at?

• Innovation and Learning Perspective: Can we continue to improve and create value?

• Financial Perspective: How do we look to shareholders?

The Balanced Scorecard

Next Time

• Zipcar case on Monday– This requires some financial thinking /

analysis– Think about what key measures / ratios

should be for the business