Financial Stability and Central Banks - Semantic Scholar€¦ · vis-à-vis smaller banks. Section...

132

Financial Stability and Central Banks SELECTED ISSUES FOR FINANCIAL SAFETY NETS AND MARKET DISCIPLINE Liisa Halme, Christian Hawkesby, Juliette Healey, Indrek Saapar and Farouk Soussa Issued by the Centre for Central Banking Studies, Bank of England, London, EC2R 8AH Telephone 020 7601 3892, Fax 020 7601 5860 May 2000 © Bank of England 2000 ISBN 1 85730 162 5

Transcript of Financial Stability and Central Banks - Semantic Scholar€¦ · vis-à-vis smaller banks. Section...

Financial Stability and Central Banks

SELECTED ISSUES FOR FINANCIALSAFETY NETS AND MARKETDISCIPLINE

Liisa Halme, Christian Hawkesby, Juliette Healey,Indrek Saapar and Farouk Soussa

Issued by the Centre for Central Banking Studies,Bank of England, London, EC2R 8AHTelephone 020 7601 3892, Fax 020 7601 5860May 2000

© Bank of England 2000ISBN 1 85730 162 5

Contents Page

Foreword 1

Authors and Acknowledgements 3

Too Big to Fail: Moral Hazard and Unfair Competition? 5Farouk Soussa, Bank of England

Bank Corporate Governance and Financial Stability 32Liisa Halme, Bank of Finland

Financial Conglomerates: Implications for the Financial Safety Net 71Indrek Saapar, Bank of Estonia, and Farouk Soussa, Bank of England

Central Banks and Supervisors: The Question of Institutional Structure 95and ResponsibilitiesChristian Hawkesby, Reserve Bank of New Zealand

List of attendees at the conference on 10 December 1999 129

1

Foreword

In 1998, the Bank of England’s Centre for Central Banking Studies (CCBS)under its then Director, Professor Maxwell Fry, began a programme ofAcademic Workshops. These workshops aim to explore a topic of relevanceto central banking by inviting around 20-25 central bankers for discussionswith academics, international policy makers and fellow participants over aperiod of a week. Following a workshop three or four of the participatingcentral bankers stay on at CCBS to take part in a related project, usuallylasting around ten weeks.

In 1999 the CCBS hosted three academic workshops. The first, in January,looked at “Financial Market Data for International Financial Stability” andthe second, in April, studied “Lessons for Central Bankers from RecentFinancial Crises”. The final academic workshop of the year, and the onewhich prompted this volume, took place in September under the title“Central Bank Responsibility for Financial Stability”.

It is a daunting task to do justice to such a title, given the wide range oftopics that it encompasses. And financial stability is not like monetarypolicy – there is no single measurable indicator that the authorities canbenchmark their activities against. Look at central banks around the worldand you will find a spectrum of responsibilities in this area.

What all central banks do have in common is an interest in financial stabilityas a public policy objective, as a key factor influencing macroeconomicperformance and the potential for systemic disturbances. Various structuralfactors can affect financial stability, and public authorities have a range oftools they can use to influence these structural factors and to address crisissituations when they occur. Many of these factors and tools were discussedduring the September workshop, but not all the issues raised could befollowed up by the subsequent project team.

Given the scope of potential topics and the short timetable, the project teamhad to narrow down their focus. In doing so, the team have attempted toaddress topical issues while trying to avoid overlap with recent andprospective work by international financial committees and working groups.The theme linking all four papers is that of the provision of safety nets(lender of last resort (LOLR) and deposit insurance) and the promotion of

2

market discipline. The papers have focused on developed countries but theissues raised are relevant to all countries in varying degrees and the papershave attempted to draw out the relevance for different types of economies.

Farouk Soussa’s paper focuses on “too big to fail” institutions and whetherthey take on additional risk and whether they have a competitive advantage.Liisa Halme’s paper looks at bank corporate governance as a way ofpromoting market discipline. Indrek Saapar and Farouk Soussa’s paperlooks at conglomerisation and the issues raised for the provision of LOLRand deposit protection. And Christian Hawkesby’s paper looks atinstitutional arrangements and in particular how one might assess the prosand cons of establishing a consolidated supervisor outside of the centralbank.

Juliette HealeyAdviser, Financial Stability

Centre for Central Banking Studies

3

Authors

Liisa Halme is a lawyer by training and a Senior Adviser in the financialMarkets Department at the Bank of Finland. Christian Hawkesby is aneconomist in the Financial Markets area of the Reserve Bank of NewZealand. Indrek Saapar is a banking supervisor by training and works asan expert in the Policy Division of the Bank of Estonia. Farouk Soussa isan economist working in the Regulatory Policy Division within the FinancialStability wing of the Bank of England. The project was undertaken, andthese papers produced, under the guidance of Juliette Healey, Adviser,Financial Stability, at the Centre for Central Banking Studies, Bank ofEngland.

Acknowledgements

First and foremost, our thanks go to the central banks who collaborated inthis project by kindly agreeing to release the authors to spend nearly threemonths at the Centre for Central Banking Studies in London. With theirsupport this was a truly international collaborative effort. We are alsoparticularly grateful to Professor David Llewellyn of the EconomicsDepartment at Loughborough University and to Bill Allen, Deputy Directorof the Financial Market Operations area of the Bank of England. They actedas discussants at the conference held on 10 December 1999 where thesepapers were presented, and their comments were invaluable. The conferencediscussion was lively and generated additional useful suggestions andobservations - we are grateful to all those who attended. Many othersprovided additional comments on earlier drafts of the papers, to whom eachauthor has given their own personal thanks in their papers.

As part of this project, Chang Shu provided research support, Karen Corbinadministrative support and Lucy Clary secretarial support. Our thanks go toall of them.

During the September 1999 workshop, Bill Allen (Bank of England),Alastair Clarke (Executive Director, Bank of England), Phil Davis (Bank ofEngland), Asli Demirguc-Kunt (World Bank), Peter Fisher (Federal ReserveBank of New York), Michael Foot (Managing Director, Financial Services

4

Authority), Professor Charles Goodhart (Monetary Policy Committee, Bankof England), Peter Hayward (International Monetary Fund), Andy Haldane(Bank of England), Glenn Hoggarth (Bank of England), Dr Rosa Lastra(University of London), Carl-Johan Lindgren (International Monetary Fund),Professor Peter Sinclair (Birmingham University, and now Director ofCCBS), Paul Tucker (Bank of England), Sushil Wadhwani (Monetary PolicyCommittee, Bank of England), Steve Weisbrod and Professor GeoffreyWood (City University and Bank of England) gave insightful presentationson specific financial stability issues that set the stage for our follow-upproject. At the Bank of England Professor Charles Goodhart and ProfessorRichard Brealey gave helpful guidance during the early stages of the project.

We are also grateful to the other central bank participants attending the oneweek workshop from whose views and experiences we benefited; AhmadHizzad Baharuddin (Bank Negara Malaysia), Charity Dhliwayo (ReserveBank of Zimbabwe), Olcay Emir (Central Bank of the Republic of Turkey),Andrea Enria (European Central Bank), Ibrahim Ghobrial (Central Bank ofEgypt), Marianne Gizycki (Reserve Bank of Australia), Pauline Green (Bankof Jamaica), Reint Gropp (European Central Bank), Nicolas Karydas(Central Bank of Cyprus), Tomas Kvapil (Czech National Bank), NicholasKwan (Hong Kong Monetary Authority), Per Lilja (Bank of Sweden),Katalin Mero (Bank of Hungary), Michael Patra (Reserve Bank of India),Roelf du Plooy (South African Reserve Bank), Henriette Prast (DeNederlandsche Bank NV), Yutaka Soejima (Bank of Japan), Tomaz Toplak(Bank of Slovenia) and Lenore Wade (Eastern Caribbean Central Bank).

The views expressed in this book do not necessarily reflect those of the Bankof England or any individual acknowledged within. All errors remain thesole responsibility of the authors.

5

Too Big To Fail:Moral Hazard and Unfair Competition?

Farouk Soussa, Bank of England*

Contents

1. Introduction2. Are some banks too big to fail (TBTF)? 2.1 The rationale for TBTF 2.2 TBTF – evidence from the markets3. Do TBTF banks have an unfair competitive advantage? 3.1 The arguments 3.2 The evidence4. Do TBTF banks take more risk? 4.1 The arguments for and against 4.2 The evidence5. Policy issues and conclusions 5.1 Levelling the playing field No bailouts Extend TBTF for all Systemic ‘tax’ on TBTF banks

Appendix I Further evidence of bank risk from the UKReferencesTable 1. Fitch IBCA bank ratings from selected countries (June 1999)Table 2. Regression results – spreads between ratingsTable 3. Implied ratings subsidyTable 4. Dependent variable: standaloneTable 5. Dependent variable: loan loss provisions/loans *This paper was written while at the Centre for Central Banking Studies, Bank of England. The authorwould like to thank David Llewellyn, Glenn Hoggarth, Simone Varotto and Bill Allen for helpfulcomments and suggestions. The opinions in this paper are those of the author and not necessarily those ofthe Bank of England.

6

Table A-1. Selected ratios for small and big banks

Figure 1. The effect of a funding subsidy on bank profitFigure 2. Individual ratings and long term credit rating for small and big

banksFigure 3. Implied yields for different ratings categories and maturitiesFigure A-1. Composition of total risk weighted assets by risk weightFigure A-2. Provisions against bad or doubtful debt for large and small

banks as a percentage of total loans and total assets

Appendix 1. Further evidence of bank risk from the UK

7

1. Introduction

The term ‘Too Big To Fail’ (TBTF) was coined by the United StatesComptroller of the Currency to describe the eleven largest US banks in thewake of the Continental Illinois crisis in 1984. It put into words the beliefthat the failure of certain large banks would have a sufficiently significant(negative) impact on the financial system and the economy as a whole suchthat these failures would be intolerable to the authorities. The result is animplicit guarantee by the authorities on the continued survival of certainlarge banks.

Many observers have criticised this guarantee on the basis that it createsmoral hazard that results in perverse incentives for large banks to takegreater risk. This is because if risk is not costly to the bank (i.e. the downsideof risk is not present) banks will take on risk in order to capture the upside(higher reward). Another criticism of this guarantee is that it gives largebanks an unfair advantage over their competitors. This may be because largebanks can afford to pursue a higher risk/reward strategy than their smallercompetitors as they are implicitly insured against the downside of any riskthey assume. Furthermore, the advantage may come from the implicitguarantee given to the creditors of large banks, lowering their cost offunding relative to that of smaller banks.1

While these arguments are intuitively appealing, there is little empiricalevidence on the subject. Nonetheless, fears of greater risk taking in banksthat receive official assistance have partly motivated such policies as‘constructive ambiguity’ and limits in the scope of official assistance (e.g.,the Federal Deposit Insurance Corporation Improvement Act – FDICIA1991).

This paper evaluates these arguments conceptually and empirically. Section2 provides the theoretical rationale for the TBTF doctrine and evidence that,despite efforts by the authorities to create uncertainty over whether officialsupport would be forthcoming, certain banks are perceived by the markets tobe TBTF. Section 3 examines the funding subsidy that TBTF banks havevis-à-vis smaller banks. Section 4 addresses the question ‘do TBTF bankstake more risk?’ The moral hazard argument is presented in favour of theproposition, while arguments such as diversification and investmentopportunities are presented against it. Some evidence on bank risk taking 1 This also lowers the cost of funding of large banks relative to non-banks who are typically not subject tosuch guarantees.

8

and size is presented. Finally, section 5 provides some conclusions andpolicy implications.

2. Are some banks TBTF?

2.1 The rationale for TBTF

The doctrine of TBTF reflects the recognition that sufficient disruption tothe smooth operation of the financial system can be triggered by the failureof a single bank, as opposed to a group of banks or some macro-economicshock. In other words, a bank that is TBTF is one whose failure, due to someidiosyncratic problem, would disrupt the financial system in the absence ofany other adverse shock. These disruptions are costly as they prevent theeconomy from benefiting from functions provided by the financial system,which include the efficient allocation of resources, the provision of thepayment system, and the efficient pricing of financial risk (De Bandt andHartmann, 1998). The question is, therefore, how can the failure of a singlebank create systemic disturbances?2

One channel by which systemic disruptions can be generated by the failureof a large bank is through the bilateral exposures that other banks wouldhave to it. Under normal circumstances, the larger a bank is, the greater theexposure of other banks to it. Empirical evidence supporting this hypothesisis limited by a lack of data, but Michael (1998) finds that interbank lendingexposures are significant in the United Kingdom, particularly for the largebanks that provide payment and settlement services.3

Another channel increasingly recognised as a source of systemic risk is thatof exposures via financial markets. The failure of a large bank with asignificant presence in a given market may cause liquidity to dry up in thatmarket if the failed bank is forced to unwind its substantial position rapidly.Other financial institutions with exposures to that market will consequentlyexperience liquidity problems. This source of exposure is not unique tobanks, as the LTCM crisis illustrates, but is likely to become increasinglysignificant in the banking industry as banks become more involved intrading activity.

2 In reality, some of the arguments that follow apply to the failure of a large non-bank financial institutionas well. However, this paper will concern itself with banks only.3 Risks arising from bilateral exposures via payment and settlement systems, while significant in the past,have been largely mitigated with the advent of Real Time Gross Settlement (RTGS) systems (see Bank ofEngland (1989) and Hills and Rule (1999)).

9

The failure of a large bank may also hamper the smooth functioning of thefinancial system by disrupting the credit creation process. As Diamond(1984) argues, banks extend credit based on private information and thiscontributes to the development of relationships between the bank andborrower.4 If that relationship is broken, it will take time for borrowers tobuild relationships with alternative banks. This is especially true ofborrowers for whom public information is not readily available, such assmall firms and individuals, and who therefore cannot turn to capital marketsas an alternative source of funding. Because larger banks are likely to have agreater number of borrowers than small banks, and thus a greater percentageof the credit market, the failure of large banks will cause significantdisruptions to the credit creation process.

Finally, systemic disruptions can be generated by the failure of a large bankif it raises doubts in the minds of depositors at other banks over thesoundness of those banks, causing them to run. These doubts may bejustified, with depositors perceiving similarities between the failed bank andtheir own (Chari and Jaganathan, 1988; Kaufman, 1994)). Alternatively,they may be sparked by pure panic (Diamond and Dybvig, 1983). In anycase, given that the failure of large banks would be more visible to thepublic, the likelihood of contagious runs on other banks, and panics inparticular, may be higher for large banks than small banks.

All these are ways in which the failure of a single large bank may potentiallyresult in significant disruption to the financial system and provide a rationalefor the TBTF doctrine. However, authorities do not announce theirwillingness to support insolvent banks that they consider TBTF. Rather, theynormally pursue a policy of ex ante ‘constructive ambiguity’ about whichbanks, if any, would receive support if they got into trouble. Althoughambiguity may create uncertainty about the likelihood of support formedium to small-sized banks, it does little to deter markets from perceivingthe largest banks as being TBTF. Evidence of this is presented below.

2.2 TBTF – evidence from the markets

Evidence that certain banks are expected to be bailed out by the authoritiesshould they run into trouble is quite easy to find. Fitch IBCA, the rating

4 For more on relationship banking, see, for example, Greenbaum and Venezia (1985), Diamond, (1989),Greenbaum, Kanatas, and Venezia (1989), Sharpe (1990), Rajan (1992) and Greenbaum and Thakor(1995).

10

agency, explicitly expresses the likelihood of official support for the banksit rates. It does so by assigning a ‘support rating’, which has a numericalvalue between 1 and 5, 1 being the highest probability of support and 5 thelowest.5 Table 1 summarises Fitch IBCA’s bank ratings for selectedcountries.

Note that countries in which ‘supported’ banks’ assets make up the highestpercentage of the total banking system’s assets (>70% in Australia, Canada,Finland, Japan, Netherlands and Sweden – these are highlighted in the table)are countries with highly concentrated banking systems.6 The exception tothis pattern is Japan in which, despite a relatively low concentration ratio,‘supported’ banks hold almost three quarters of the total assets in thebanking system. This may reflect the Japanese authorities generoustreatment of troubled banks in recent times, although there are insufficientdata to test this proposition.

Overall, since Fitch-IBCA rates mainly those banks that issue securities, andsince these tend to be the larger banks, it is perhaps unsurprising that aparticularly high percentage of rated banks received support ratings of 1 or 2(i.e., they were expected to be bailed out by authorities). All the same, thesedata demonstrate, despite efforts by the authorities to be ‘constructivelyambiguous’, markets do nevertheless have expectations that official supportwould be forthcoming for certain institutions.

5 A support rating of 3 is assigned to receive those banks who are likely to ‘unofficial’ support, e.g. from aparent bank or affiliate.6 Although no data are available for Australia and Finland from this source, these are both countries knownto have highly concentrated banking systems.

11

Table 1.7 Fitch IBCA bank ratings from selected countries (June 1999)Country Number of

BanksThought tobeSupported(supportrating of 1or 2)

Numberof RatedBanks

(%supported)

Totalnumberof Banks

( %supported)

Supportedbanks’assets as %of all assetsin bankingsystem

Concentrationratios (share oftop five (ten)financialinstitutions oftotal financialassets)

Australia 9 12 (75) 83 (11) 82 -Belgium 7 8 (88) 119 (6) - 57(74)Canada 6 6 (100) 80 (8) 85 78(93)Germany 23 28 (82) 2337 (1) 55 17(28)Denmark 3 4 (75) 210 (1) 34 -Spain 13 32 (41) 172 (8) 60 -Finland 4 4 (100) 12 (25) 96 -France 12 32 (31) 618 (2) 53 57(73)Ireland 2 7 (29) 55 (4) 64 -Italy 9 36 (25) 710 (13) (<38) 25(38)Japan 31 35 (89) 198 (16) 74 31(50)Netherlands 7 8 (88) 80 (9) 82 79(88)Norway 6 7 (86) 43 (14) 60 -Sweden 6 6 (100) 26 (23) (>90) 90(93)UnitedKingdom

9 57 (16) 313 (3) 65 47(68)

Source: Fitch-IBCA and BIS (1999)

3. Do TBTF banks have an unfair competitive advantage?

3.1 The arguments

One criticism of TBTF is that it gives large banks an unfair advantage overtheir competitors for two possible reasons. First, because TBTF banks canafford to be more risky, they will achieve higher returns. Whether or not thisis true is examined in the next section and discussion of this argument istherefore reserved until later.

The second possible reason is that the unfair advantage comes from theimplicit guarantee given to the creditors of large banks, lowering the cost offunding relative to that of small banks, and thus increasing their profits.Figure 1 illustrates this. SL and SD1 are the supply of loans and depositsrespectively in a perfectly competitive (subsidy-free) banking industry,while D is the demand for funds. Under such conditions, the equilibriumsupply of loans and deposits is M, with a lending rate of i1 and a deposit rateof i0. The difference between these two rates, π, is the profit of the bank. The 7 All figures are taken from Fitch-IBCA and are only indicative.

12

effect of a TBTF subsidy, according to the above argument, is that it lowersthe cost of funding, shifting the supply of deposits outwards to SD2. This, asthe figure shows, means that firms with a lower cost of funding will have an‘abnormal’ profit of π*.

Figure 1. The effect of a Funding Subsidy on Bank Profit

3.2 The evidence

A few studies in the United States have examined the ‘wealth effects’ ofTBTF (see, for example, Angbazo and Saunders (1996)). They test thehypothesis that TBTF is reflected in the value of the banks (share price) as itreduces the cost of funding and therefore increases the profitability of thebank. These studies have found a positive relationship between bank sizeand share price, providing indirect evidence that TBTF does indeed raiseprofitability by lowering funding costs. O’Hara and Shaw (1990), forexample, find that the largest US banks experienced positive adjustments intheir share-price immediately after the announcement by the Comptroller of

D

SD2

SD1

SL

i1

i0

i2

π

π*

Interest Rate

QuantityM

13

the Currency in 1984 that certain banks were too big to fail. There is littleliterature, however, which directly measures the alleged funding subsidyimplied by TBTF, particularly for European banking industries.

Here, we attempt to provide such evidence using a sample of 120 banks fromsix countries: France, Italy, the United Kingdom, Germany, Spain and Japan.We compare two Fitch-IBCA measures of bank credit risk: ‘IndividualRatings’ and ‘Long-Term Credit Ratings’.

According to Fitch-IBCA’s definitions, ‘Individual Ratings’ assess how abank would be viewed if it were entirely independent and could not rely onexternal support. They are designed to assess a bank’s exposure to, appetitefor, and management of risk, and thus represent Fitch-IBCA’s view on thelikelihood that it would run into significant difficulties such that it wouldrequire support. They analyse a bank’s profitability and balance sheetintegrity, franchise, management, operating environment, and prospects.Individual ratings are thus a proxy measure of the market’s perception of therisk an individual bank takes on. Individual ratings are herein referred to asstandalone ratings.

‘Long-Term Credit Ratings’ are an overall indicator of the likelihood that aninvestor will get his or her money back in accordance with the terms inwhich he or she invested. They are thus a measure of overall credit risk, andinclude both individual risk and the likelihood that a bank will get support inthe event of a crisis. Long-term credit ratings will be referred to as inclusiveratings in the remainder of this paper.

In principle, therefore, the difference between a bank’s standalone ratings(which, by definition, excludes the possibility of support) and inclusiverating should reflect the value of official support.

Within the overall data set consisting of 120 banks, we examine two groups:TBTF banks (with a support rating of 1 or 2 – there are 76 such banks in thesample) and ‘small banks’ (with a support rating of 4 or 5 – there are 44 ofthese in the sample).8 Figure 2 shows the relationship between standaloneratings and inclusive ratings for these two groups of banks. A regression line(using ordinary least squares) has been drawn separately for each group.

8 To ensure that the difference reflects the value of official support, banks with support ratings of 3(reflecting the possibility of support from a parent company etc.) were excluded from the sample.

14

Figure 2. Individual ratings and Long Term Credit rating for Smalland Big Banks

The regression lines are significant and take the form:

Small Coefficients Standard Error t StatIntercept 2.546763 0.618384 4.118414X Variable1

0.748201 0.155818 4.801759

TBTFIntercept 0.883379 0.369231 2.392485X Variable1

0.597811 0.060064 9.952948

What Figure 2 and these regressions show is that for a given level of bankrisk (standalone rating), TBTF banks receive a higher inclusive rating andthus, in principle, a lower cost of funding. For example, a small bank with astandalone rating of C would, on average, receive an inclusive rating ofBBB+, while a TBTF bank of the same standalone rating would receive ahigher inclusive rating of A+. Based on this rough calculation, the impliedsubsidy for a TBTF bank over a small bank of a standalone rating of C isthree credit notches. 9

9 For example, one notch is equivalent to the difference between AA+ and AA or AA and AA-.

Inclusive and StandandaloneRatings for TBTF and Small Banks

D/E

D

C/D

C

B/C

B

A/B

A

BBB BBB+ A- A A+ AA- AA AA+ AAA

Inclusive Rating

Stan

dalo

ne R

atin

g

TBTF Banks

EBBB-

Small Banks

15

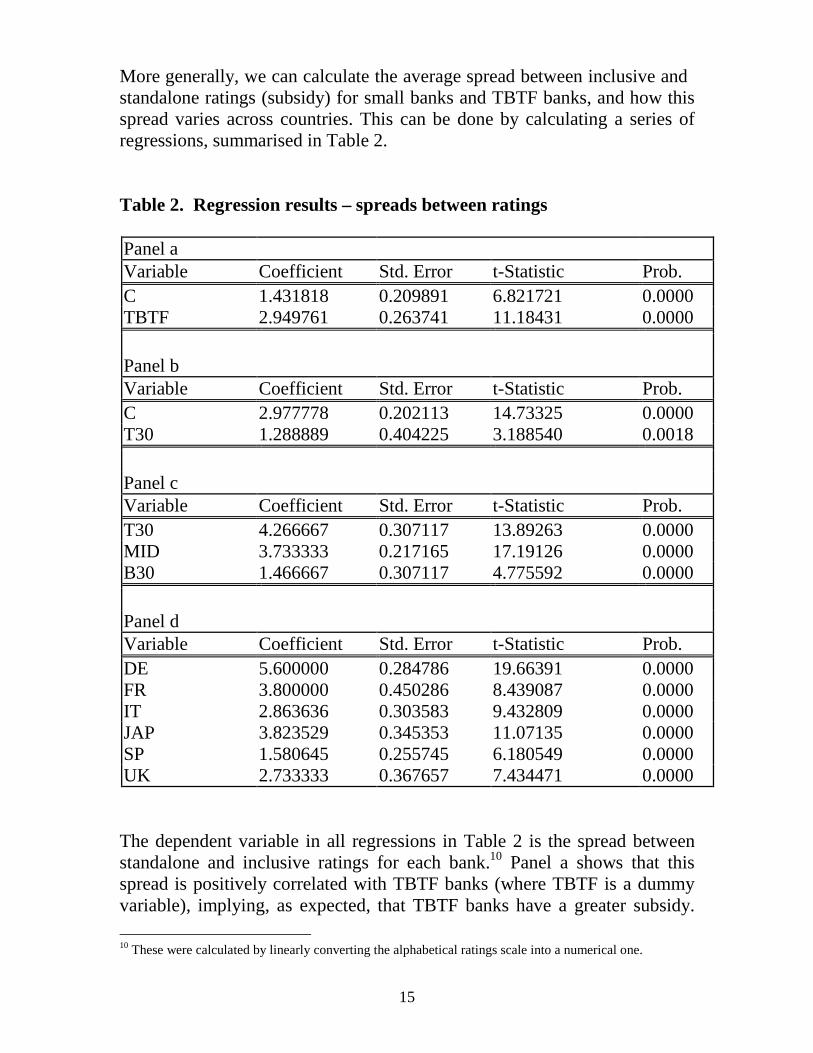

More generally, we can calculate the average spread between inclusive andstandalone ratings (subsidy) for small banks and TBTF banks, and how thisspread varies across countries. This can be done by calculating a series ofregressions, summarised in Table 2.

Table 2. Regression results – spreads between ratings

Panel aVariable Coefficient Std. Error t-Statistic Prob.C 1.431818 0.209891 6.821721 0.0000TBTF 2.949761 0.263741 11.18431 0.0000

Panel bVariable Coefficient Std. Error t-Statistic Prob.C 2.977778 0.202113 14.73325 0.0000T30 1.288889 0.404225 3.188540 0.0018

Panel cVariable Coefficient Std. Error t-Statistic Prob.T30 4.266667 0.307117 13.89263 0.0000MID 3.733333 0.217165 17.19126 0.0000B30 1.466667 0.307117 4.775592 0.0000

Panel dVariable Coefficient Std. Error t-Statistic Prob.DE 5.600000 0.284786 19.66391 0.0000FR 3.800000 0.450286 8.439087 0.0000IT 2.863636 0.303583 9.432809 0.0000JAP 3.823529 0.345353 11.07135 0.0000SP 1.580645 0.255745 6.180549 0.0000UK 2.733333 0.367657 7.434471 0.0000

The dependent variable in all regressions in Table 2 is the spread betweenstandalone and inclusive ratings for each bank.10 Panel a shows that thisspread is positively correlated with TBTF banks (where TBTF is a dummyvariable), implying, as expected, that TBTF banks have a greater subsidy. 10 These were calculated by linearly converting the alphabetical ratings scale into a numerical one.

16

The coefficient on the TBTF dummy is interpreted as the average spread forTBTF banks over small banks i.e., all other banks in the sample. This spreadis roughly three credit notches. This supports the earlier observation that a‘small’ and TBTF bank of standalone rating of C would get an inclusiverating of BBB+ and A+ respectively.

Panels b and c examine whether size is a factor in determining the subsidyreceived. Panel b shows that the top 30 banks (by scaled asset size11) receivea subsidy over and above the rest of the banks, equivalent to approximatelyone credit notch. However, panel c shows that this subsidy relative to thesmallest 30 banks in the sample (b30) is closer to three credit notches. Theseresults imply that ‘size matters’.

Panel d looks at the average spread by country using a series of countrydummies. The coefficients on the dummies are interpreted as the averagesubsidy in notches. It is interesting to note that the greatest subsidy isexpected in Germany. This is perhaps unsurprising given the high proportionof German banks that are state-owned. Also high in terms of subsidy areFrance and Japan, possibly reflecting these countries’ lower threshold oftolerance for bank failure.

The above is evidence of how spreads between standalone and inclusiveratings vary according to various factors. But how does one interpret thesubsidy of three credit notches that TBTF banks have over small banks, forexample? In other words, what does it mean, in terms of cost of funding, tohave an inclusive rating three notches higher than a competitor? To answerthis question, we calculate the yields on bonds implied by the historicaldefault probabilities of different ratings classes, based on the approachdeveloped by Jarrow, Lando and Turnbull (1997).

That is, we assume the value of a bond to bePresent Value of Bond = (p)(δ)(1/RBn) + (1-p)( 1/RBn)Where p is the probability of default, δ is the recovery rate of assets givendefault, RB is the return on risk-free debt, and n is the maturity. We use thehistorical probabilities of default12 for each of the inclusive ratingscategories, holding δ and RB at 50% and 7% respectively, and calculate thevalue of the bond (also interpreted as the discounted value of 1 unit of

11 To account for differences in country size, assets of banks were scaled such that the largest bank in eachcountry were given the same nominal asset size.12 Using the average cumulative default rates (percent) for 1920-1999 calculated by Moody’s.

17

investment), from which we can then calculate the implied yield. Theresults are summarised in Table 3.

Table 3. Implied ratings subsidy

Rating DefaultProbability-5yr

DefaultProbability-10yr

DefaultProbability-15yr

DefaultProbability-20yr

AAA 0.002 0.0109 0.0189 0.0238AA 0.0097 0.031 0.0561 0.0675A 0.0137 0.0361 0.0613 0.0747BBB 0.0351 0.0792 0.1146 0.1395BB 0.1004 0.1905 0.2595 0.3082B 0.2089 0.319 0.3917 0.437

Discounted value of 1 pound ofinvestment

AAA 0.712 0.506 0.359 0.255AA 0.710 0.500 0.352 0.250A 0.708 0.499 0.351 0.249BBB 0.700 0.488 0.342 0.240BB 0.677 0.460 0.315 0.219B 0.639 0.427 0.291 0.202

Annual interestrate

AAA 7.02% 7.06% 7.07% 7.06%AA 7.10% 7.17% 7.20% 7.18%A 7.15% 7.20% 7.22% 7.20%BBB 7.38% 7.43% 7.42% 7.39%BB 8.11% 8.08% 8.00% 7.90%B 9.39% 8.88% 8.57% 8.33%

The lower panel allows us to convert credit notches into actual interest rates.In particular, it allows us to interpret the subsidy of three credit notches thatTBTF banks have over small banks. Three credit notches is the differencebetween a letter rating category, for example, a small and TBTF bank of agiven standalone ratings could expect an inclusive rating of BBB and Arespectively. If such banks were issuing debt of a 5-year maturity, the small

18

bank would be paying 23 basis points more in interest than the large bank(7.38%-7.15%). This is the nominal value of the TBTF subsidy.

Figure 3 shows the yields for the different maturities graphically. It is clearfrom this figure that the subsidy received by TBTF banks is greater for lowermaturity debts than for longer maturity.

Figure 3. Implied Yields for Different Ratings Categories andMaturities

4. Do TBTF banks take more risk?

4.1 The arguments for and against

It is often argued that TBTF encourages moral hazard for large banks,leading to perverse incentives for such banks to take greater risk. Thesearguments are twofold.

First, large banks take advantage of the implicit elimination of downside riskimplied by TBTF. As argued by the former Deputy Governor of the Bank ofEngland, and now Chairman of the UK Financial Services Authority,Howard Davies, “If the state guarantees the existence of individual banks,that can create incentives which encourage irresponsible behaviour. The

7.00%

7.50%

8.00%

8.50%

9.00%

9.50%

10.00%

5yr 10yr 15yr 20yr

Maturity

Yiel

d

AAAAAABBBBBB

19

prize for taking excessive risk may – if things go well – be excess returns(and telephone number bonuses) while, if things turn out badly, the statesteps in and picks up the tab. This is known as a one-way bet” (Davies,1997).

Second, TBTF implicitly insures depositors (those which are not explicitlyinsured by deposit insurance) thereby eliminating their incentive to monitorthe bank. This allows banks, it is argued, to take advantage of the one-waybet described in the preceding paragraph.

To assess these arguments, it is first important to clarify for whom the moralhazard is allegedly created. In other words, which person or persons are bothgiven incentives to take on more risk and have the ability to do so. These areclearly those people who control the bank: bank managers. When speakingof moral hazard and TBTF, therefore, one must bear in mind that thequestion is whether bank management has the inclination or ability to takeexcessive risk.

The above arguments, while suggesting that managers at big banks maychoose riskier portfolios than small banks ceteris paribus, do not necessarilyimply that big banks in practice have greater portfolio risk than small banks.This is because big banks, by virtue of their size, benefit from factors thatreduce the level of their portfolio risk vis-à-vis small banks. The mostobvious of these is that bigger banks are likely to be better diversified thansmall banks due to economies of scale. In addition to this, big banks benefitfrom better investment opportunities: small banks, with limited funds toinvest, may have investment opportunities that are limited to smallbusinesses and individuals (see, for example, Strahan and Weston (1998)and Jayaratne and Wolken (1998)) . Since such lending is typically morerisky than that to larger corporations (which big banks have the funds to lendto) this suggests that small banks may have inherently riskier portfolios.

Given identical diversification and investment opportunities, however, it isstill not obvious that large banks will behave in the way suggested by theabove arguments. If regulators price risk, so that greater risk is reflected inhigher required capital for example, the incentive to take greater risk may bereduced. Monitoring of risk by the authorities (supervision) also limits theability of banks to take greater risk.

Failing this, if a large bank encounters problems arising from poormanagement of risk, the authorities would normally intervene in favour of

20

the bank only on the condition that management and shareholders arepunished, the former often being barred from working in the financialservices industry for a certain period. An analogy could be made to adrunken taxi driver: rather than impounding the taxicab – reducing thewelfare of all taxi patrons – the authorities punish the driver while puttingthe taxicab into another’s more competent hands. The incentives for bankmanagers to take excessive risk are thus reduced, despite their bank’sguaranteed survival.

The effect of TBTF on the riskiness of large banks will depend, therefore, onthe significance of the risk-reduction benefits of diversification and betterinvestment opportunities, and whether or not the authorities are able toimplement policies that could counter the incentives to take greater risk.

4.2 The evidence

Although a considerable amount has been written on the moral hazardeffects of lender of last resort (LOLR) and TBTF, little empirical work hasbeen carried out on the subject. What literature does exist suggests that thereis no apparent correlation between bank size and overall risk, although thereis a correlation between bank size and the composition of risk. There is atendency for larger banks to have higher risk components in their portfolio,but these risks are neutralised through diversification benefits. Large banksthus capture gains in diversification through higher reward rather than lowerrisk (see Berger, Demsetz and Strahan (1999), Demsetz and Strahan (1997,1995a, 1995b)).

Market observations appear to be consistent with the view that, despite beingmore likely to be bailed out than smaller banks, large banks do not takegreater risk. Panel A of Table 4 below shows the results of a regressionexamining the relationship between TBTF banks and standalone ratings, theproxy for market perception of individual risk. A positive correlation wasfound, meaning TBTF banks have a lower standalone rating on average.However, there was a problem with the sample in the sense that all Japanesebanks have a support rating of 1 or 2 (TBTF) and all have a low standalonerating due to the current state of the Japanese banking system. This biasesthe sample, and to correct for this we include in the regression in panel B aJapan dummy. This has the effect of making the relationship between TBTFbanks and standalone ratings statistically insignificant. While this isinteresting, Fitch IBCA’s assessment of individual risk is made privately andis partly subjective and it would be prudent to examine a more objective

21

measure of bank risk-taking to assess whether or not this is consistent withFitch IBCA’s view.

Table 4Dependentvariable:

Standalone

Panel AVariable Coefficient Std. Error t-Statistic Prob.C 3.545455 0.253314 13.99631 0.0000TBTF 1.204545 0.318304 3.784259 0.0002Panel BVariable Coefficient Std. Error t-Statistic Prob.C 3.545455 0.189462 18.71329 0.0000JAP 3.352941 0.345943 9.692183 0.0000TBTF 0.454545 0.250331 1.815779 0.0720

To arrive at a more objective measure of bank risk taking, the ratio of loanloss provisions over total loans was considered for the sample above. Thisratio gives a good approximation of bank portfolio risk for two reasons.First, loan losses, although partly reflecting a bank’s investmentopportunities, also reflect a bank’s investment decisions and risk appetite(Walter, 1991). Second, the ratio picks up changes in the profitability of thebanks, so that a measure of earnings is included. Panel A of Table 5 belowshows that the relationship between whether a Bank is TBTF and the ratio ofloan loss provisions over loans is statistically insignificant. When the Japandummy is included, for reasons mentioned earlier, the relationship becomeseven less statistically insignificant.

Table 5Dependent Variable: Loan Loss Provisions / LoansPanel AVariable Coefficient Std. Error t-Statistic Prob.C 0.504437 0.729347 0.691627 0.4909TBTF 1.716361 0.944940 1.816370 0.0726Panel BVariable Coefficient Std. Error t-Statistic Prob.C 0.504437 0.662746 0.761131 0.4485JAP 5.460952 1.208490 4.518824 0.0000TBTF 0.156089 0.925475 0.168658 0.8664

22

Finally, evidence on loan losses of banks in the United Kingdom based onquarterly supervisory reports between 1989-1995 (see appendix) confirmsthe view that asset quality in large banks is at least no worse than that insmall banks.

Overall, the evidence presented in this section is intended to show that, inpractice, large banks do not appear to take on more risk than small banks.However, it is not intended to refute the claim that there is a moral hazardproblem with respect to the TBTF doctrine.

First, the evidence does not show that large banks take on less risk than theywould in the absence of TBTF. It could be that in the absence of TBTF,large banks would be less risky than small banks because of diversificationetc. but this is impossible to verify.

Second, the behaviour of large banks implied by the evidence abovesuggests that the mitigating factors to the theoretical threat of greater risktaking (described in section 4.1) are significant. Moral hazard may yet be aproblem in the absence of such policies.

5. Policy issues and conclusions

In most countries, the threat of moral hazard arising from a TBTF policy hasbeen heeded by the authorities, who try to minimise the reach of the safetynet while maintaining a degree of ‘constructive ambiguity’ in its use. Theevidence presented above suggests that such policies may be motivated byan over-emphasis on the negative incentive effects for large banks thatTBTF may have, while not taking enough account of mitigating factors suchas economies of scale and measures that the authorities may take to counterthese incentives.

To begin with, constructive ambiguity does not appear to work – marketsstill believe that support would be forthcoming for certain large banksshould they encounter difficulties. Moreover, constructive ambiguity appearsto be unnecessary, since despite there being a general belief that certainbanks will be supported, these banks do not behave in the feared manner oftaking on excessive risk. However, while this suggests that the authoritiescould, in principle, do away with constructive ambiguity and state theirwillingness to support certain banks, in practice this would be difficult. Thisis because the notion of a systemically important bank is context-dependent:

23

a bank that is important in one set of circumstances may not be in another.This is especially true of ‘medium-sized’ banks, whose systemic importanceis marginal (Goodhart and Huang, 1999). Ambiguity over precisely whichbanks will be supported, therefore, may be a result of uncertainty on the partof the authorities themselves and not their deliberate desire to createuncertainty.

5.1 Levelling the playing field

Be this as it may, TBTF does appear to lower the funding cost for largerbanks and thus creates an uneven playing field in banking. TBTF thereforereduces competition and thus efficiency, exemplifying the general trade-offofficial intervention in the financial sector presents between efficiency andfinancial stability.

To level the playing field, one of three policies can be adopted. First,authorities can commit to a policy of not bailing out any banks, regardless oftheir size or systemic importance. Second, the safety net can be extended toall banks. Finally, large banks could be charged a tax that would reflect theirsystemic importance and compensate for the subsidy they receive because ofthis.

No bailouts

If authorities believes that bank failures may have systemic consequences, apolicy of a priori commitment to not bailing out any banks indicates thatauthorities have placed a great deal of weight on competitiveness andefficiency within the financial system, and less weight on stability.

Of course the premise that bank failures create instability is oftenquestioned. The ‘free banking’ school, which argues for a completecessation of official intervention in the financial sector, would argue thatbank failures do not create externalities or knock-on effects over and abovethose created by the failure of any non-financial firm of similar size.Moreover, they argue that market mechanisms for effectively discipliningbanks would have evolved that would have reduced the likelihood of bankfailure vis-à-vis the usual current system of intervention.13

However, arguments such as those outlined earlier in Section 4.1, whichmaintain that bank failures can lead to financial instability, are more 13 See Dowd (1996) for some views on free banking.

24

generally accepted. In this context, the desire to eliminate bailouts isnormally balanced with measures that would likewise eliminate the need todo so. In other words, ending a policy of TBTF would require that theauthorities ensure the following: (i) all banks, particularly large banks, areprudently managed; (ii) their financial health is monitored at all times; (iii)should their financial health deteriorate, corrective measures be takenpromptly; and (iv) if corrective measures are unsuccessful, the bank shouldbe closed before it ‘fails’ (i.e., defaults on obligations). One regime thatincorporates these requirements is that of the United States, post the FederalDeposit Insurance Corporation Improvement Act (FDICIA) (1991).

Unfortunately, not all bank failures can be avoided through regulation andsupervision and, given the financial instability created by bank failures, anysuch system would face a time-consistency problem: authorities would findit difficult to adhere to their pre-stated commitment of not bailing out banks.FDICIA (1991), in an attempt to avoid this problem, has incorporated aclause that exempts systemically important banks from mandatory closure(see appendix).

The evidence presented in this paper questions the necessity of such aregime. Although FDICIA is also partly motivated by the desire to limit thedirect financial costs of bailouts to the authorities, an important objective ofits PCA provisions, and any other scheme that aims to eliminate bailouts, isto limit their moral hazard effects. Given we find no evidence of greater risktaking in large banks, and given the downside of such policies – i.e. greaterrisk of financial instability and/or time consistency problems in theirimplementation – their effectiveness and desirability is questionable.

Extend TBTF for all

If TBTF does not lead to greater risk taking, why not extend it to all banks?This would level the playing field in raising funds.

The caveat to such an approach is that, as argued earlier, there are threereasons why TBTF does not induce greater risk taking: (i) regulation thatlimits the ability of banks to take on excessive risk and/or makes risk morecostly; (ii) supervision, which monitors and enforces prudentialrequirements; and (iii) punishment of management and shareholders shouldofficial intervention be required. Large banks, in the absence of thesemeasures, may behave in the way predicted by the moral hazard theory. It

25

therefore follows that if TBTF were to be extended to all banks, thesemeasures would have to be as well.

This requirement will not affect the first and third measures listed in thepreceding paragraph. Prudential regulation applies, in principle, to all banks,regardless of their size and therefore would not need to be extended.Punishment of managers and shareholders is relatively cost less and thuswould not act as a barrier to extension of the safety net. It is the secondmeasure, supervision, which would provide an argument against allowingaccess to the safety net to all banks.

Supervision is costly, and recent trends suggest that best practice involvesfocussing supervisory efforts on those institutions whose failure would posethe greatest systemic threat. Indeed, in the United States, supervisors followthe philosophy of ‘risk-focussed supervision’, and in the United Kingdomtoo, large banks are monitored and supervised more closely than smallbanks. If the safety net was extended to all banks, without extending thecloser supervision larger banks receive, smaller banks may be able tocapitalise on the implicit guarantee by taking more risk. Because, in general,such close scrutiny of all banks would be extremely costly, extension of thesafety net to all banks would be impractical, particularly for banking systemswith a large number of small banks.

Systemic ‘tax’ on TBTF banks

The option of limiting the safety net to only those banks that aresystemically important, in effect the TBTF doctrine currently practised in anumber of countries, has advantages over the previous two options. First, itavoids the risk of systemic crises and, potentially, the time consistencyproblem of a policy that commits to not bailing out any banks. Second, itallows resources to be focussed on the closer supervision of large banks vis-à-vis small banks, which is the drawback of a comprehensive safety net.What can be done, therefore, to reduce the unfair competitive advantage bigbanks enjoy over small banks in such a regime?

The funding subsidy that big banks enjoy could, in principle, be neutralisedby imposing greater costs on banks deemed TBTF. TBTF banks could berequired, for example, to hold higher capital reserves. Since capital is bothcostly and a buffer to losses, such requirements would both increase largebanks’ costs in line with small banks, and also decrease the likelihood thatlarge banks would require official assistance. Alternatively, a ‘systemic tax’

26

on large banks could be levied, which would increase their costs as well asprovide funds from which intervention costs may be recouped. The actualdesign of the costs imposed on large banks is an important issue that is thesubject of ongoing research.

The drawback of this scheme is that it would necessitate the identification ofa precise group of TBTF banks. As mentioned earlier, the notion of anygiven bank being TBTF is context-dependent which would make such a taskdifficult.

Appendix I. Further evidence of bank risk from the UK

In order to provide further evidence that large banks are no more risky thansmall banks, the balance sheets of 6 large UK banks (with average assets ofapproximately £100bn in June, 1995) and a sample of 62 small banks (withaverage assets of just over £200 million in June, 1995) were examined.14

Table A-1 lists some selected ratios. These results are consistent with theabove evidence and contradict the notion that large banks take on more riskthan small banks.

The table shows, as does Figure 5, that while both large and small bankshave a bias towards holding assets in the 100% risk-weighted category(which are more risky), this bias is marginally stronger for small banks. Butthe more telling results are in the last four columns of Table A-1 and aregraphically presented in Figure 6. These show that provisions against bad ordoubtful debt (as a proportion of total loans or assets) were, on average,almost five times higher for small banks than they were for large banks inthe sample period.

At first glance, the fact that these provisions were so much higher for smallbanks than for large banks appears to be contradictory to the resultspresented in Figures 3 and 4 (main text). However, one must bear in mindthat the small banks examined in this last exercise are much smaller thanthose from the Fitch IBCA sample. It may thus be that the ‘investmentopportunity’ component of loan loss provisions is more significant in Figure6 – the banks in this sample may be so small that their lack of diversificationopportunities and investment opportunities renders their assets more risky.

14 The data are based on biannual and quarterly reports for the period 1989-1995.

27

Unfortunately, data on banks of a similar size to those used in the FitchIBCA sample were difficult to find.

Nevertheless, if moral hazard is as significant as much of the theoreticalliterature suggests, one would expect that large banks would, in pursuinghigher risk loans at higher rates, have a higher proportion of bad loans intheir portfolio than small banks. The evidence presented in this sectionsuggests that this is clearly not the case.

28

Table A-1. Selected ratios for small and big banks%age of 10%rwa /total rwa

%age of 20%rwa /total rwa

%age of 50%rwa /total rwa

%age of 100%rwa /total rwa

Provisions /loans

Provisions /assets

Small Big Small big small Big small big Small big Small bigDec-89 0.08 0.44 4.09 6.53 3.67 6.43 92.17 86.60 7.81 3.01 6.67 2.63Jun-90 0.06 0.52 4.36 6.33 3.17 6.65 92.41 86.50 8.78 2.68 7.52 2.33Dec-90 0.07 0.53 4.84 6.41 3.38 7.09 91.72 85.98 10.78 2.69 9.33 2.33Jun-91 0.06 0.53 4.94 6.37 2.97 7.05 92.03 86.05 11.76 2.96 9.96 2.56Dec-91 0.05 0.55 4.55 6.93 2.63 7.68 92.77 84.84 11.65 3.05 9.81 2.63Jun-92 0.06 0.58 4.67 7.22 2.78 8.17 92.49 84.03 12.38 3.05 10.32 2.60Dec-92 0.03 0.58 4.81 8.19 2.63 8.59 92.54 82.64 11.27 3.17 9.51 2.71Jun-93 0.07 0.67 5.16 8.60 2.75 8.85 92.02 81.89 12.40 2.73 10.42 2.22Dec-93 0.05 0.78 5.41 9.38 2.63 9.57 91.90 80.27 12.28 2.62 10.20 2.06Jun-94 0.07 0.76 5.67 10.17 2.48 9.99 91.78 79.07 11.61 2.26 9.56 1.75Dec-94 0.06 0.89 5.39 9.83 2.27 10.35 92.28 78.93 9.78 1.97 8.01 1.54Jun-95 0.07 0.99 4.96 10.23 2.09 10.50 92.88 78.28 9.01 1.68 7.34 1.286 yearaverage 0.06 0.65 4.90 8.01 2.79 8.41 92.25 82.92 10.79 2.66 9.05 2.22

Figure A-1 Composition of total risk weighted assets by risk

Figure A-2 Provisions against bad or doubtful debt for large and

small banks as a %age of total loans and total assets

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

10% 20% 50% 100%

small banksbig banks

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

Dec-89

Mar-90

Jun-9

0

Sep-90

Dec-90

Mar-91

Jun-9

1

Sep-91

Dec-91

Mar-92

Jun-9

2

Sep-92

Dec-92

Mar-93

Jun-9

3

Sep-93

Dec-93

Mar-94

Jun-9

4

Sep-94

Dec-94

Mar-95

Jun-9

5

smallprov/loansbig prov/loans

small prov/ass

big prov/ass

Risk Weighting

% or risk-weightedassets

Date

% oftotalassets

30

References

Angbazo, L and A. Saunders (1996) "The effects of TBTF on BankCost of Funds", New York University Salomon Center Working Paper,s/96/39.Bank of England (1989) “Payment and Settlement Systems Risk andEfficiency: A Discussion Paper", mimeo.Berger, A., Demstez, R. and P. Strahan (1999) “The Consolidation ofthe Financial Services Industry,” forthcoming, Journal of Banking andFinance, Vol. 23.Chari, V and R Jagannathan (1988) “Banking Panics, Information, andRational Expectations Equilibrium”, Journal of Finance, Vol. 43, pp.749-61.Davies, H (1997) “Financial Regulation: Why, How and by Whom?”Bank of England Quarterly Bulletin, February, pp. 107-12.De Bandt, O and P Hartmann (1998) “What is Systemic Risk Today?”,Risk Measurement and Systemic Risk: Proceedings of the Second JointCentral Bank Research Conference, Bank of Japan, November, pp 37-84.Demsetz, R. and P. Strahan (1997) “Diversification, Size, and Risk atBank Holding Companies”, Journal of Money, Credit and Banking, Vol.29.Demsetz, R. and P. Strahan, (1995a) “Size, Diversification and Risk atBank Holding Companies”, FRBNY Research Paper no. 9506.Demsetz, R. and P. Strahan (1995b) “Historical Patterns and RecentChanges in the Relationship Between Bank Holding Company Size andRisk,” FRBNY Economic Policy Review.Diamond, D (1984) “Financial Intermediation and DelegatedMonitoring”, Review of Economics Studies, July, pp. 393-414.Diamond, D (1989) “Reputation Acquisition in Debt Markets”, Reviewof Economic Studies, Vol. 99, pp. 689-721.Diamond, D and P Dybvig (1983) “Bank Runs, Deposit Insurance, andLiquidity”, Journal of Political Economy, Vol. 91, pp. 401-19.Dowd, K. (1996) Laissez-Faire Banking. Routledge, New York.Freixas, X, C. Giannnini, G. Hoggarth and F. Soussa (1999) “Lenderof Last Resort: a Review of the Literature,” Financial Stability Review,Bank of England, Issue 7, November.Goodhart, C A E and H Huang (1999) “A Model of the Lender of LastResort”, LSE Financial Markets Group Discussion Paper, dp0131Greenbaum, S I and A Thakor (1995) Contemporary FinancialIntermediation, The Dryden Press, Orlando, Fl.

31

Greenbaum, S I and I Venezia (1985) “Partial Exercise of LoanCommitments Under Adaptive Pricing”, Journal of Financial Research,Vol. 8, pp. 251-63.Greenbaum, S I, Kanatas, G and I Venezia (1989) “Equilibrium LoanPricing Under the Bank-Client Relationship”, Journal of Banking andFinance, Vol. 13, pp. 221-35Hills, R and D Rule (1999) “Counterparty Credit Risk in WholesalePayment and Settlement Systems”, Financial Stability Review, Bank ofEngland, Issue 7, November, pp. 98-114.Jarrow, R, D Lando and S. Turnbull (1997) "A Markov Model for theTerm Structure of Credit Risk Spreads", Review of Financial Studies, pp.481-523.Jayaratne, J and J Wolken (1998) “How Important are Small Banks toSmall Business Lending: New Evidence from a Survey of Small Firms,”Journal of Banking and Finance, Vol. 22, Issue 6-8, pp. 427-58.Kaufman, G (1994) “Bank Contagion: A Review of the Theory andEvidence”, Journal of Financial Services Research, pp. 123-150.Michael, I (1998) “Financial Interlinkages and Systemic Risk”, Bank ofEngland Financial Stability Review, Issue 4, Spring, pp 26-33.O’Hara M. and W. Shaw (1990) "Deposit Insurance and WealthEffects: The Value of Being 'Too Big To Fail'", Journal of Finance, pp.1987-1600.Rajan, G (1992) “Insiders and Outsiders: The Choice Between Informedand Arm’s-length Debt”, Journal of Finance, Vol. 47, pp. 1367-1400.Sharpe, A (1990) “Asymmetric Information, Bank Lending, and ImplicitContracts – A Stylised Model of Customer Relationships”, Journal ofFinance, Vol. 45, pp. 1069-87.Strahan, P and J Weston (1998) “Small Business Lending and theChanging Structure of the Banking Industry”, Journal of Banking andFinance, Vol. 22, Issue 6-8, 821-45.Walter, J (1991) “Loan Loss Reserves”, Federal Reserve Bank ofRichmond Economic Review, Vol. 77, Issue 4, pp. 22-30.

32

Bank Corporate Governance andFinancial Stability

Liisa Halme, Bank of Finland*

Contents

1. Introduction2. A theoretical background3. Basic features of an incentive-based legal, regulatoryand supervisory framework4. Corporate Governance and the implementation ofan incentive-based framework

4.1 Definitions of corporate governance4.2 Studies related to corporate governance4.3 Different practical approaches to corporate governance4.4 How to set incentives for bank management

4.4.1 Responsibility and power4.4.2 Responsibility and sanctions

4.5 How to set incentives for shareholders4.6 How to set incentives for supervisors

5. The applicability of incentive-based corporate governance for differentcountries6. The role and responsibility of the central bank7. Summary

ReferencesTable 1. Key elements of efficient regulation

* This paper was written while at the Centre for Central Banking Studies, Bank of England. The authorwould like to thank Bill Allen, Richard Brealey, Charles Goodhart, Juliette Healey, Rosa Lastra,Paula Launiainen, David Llewellyn, David Mayes and David Swanney for their helpful comments.The opinions in this paper are those of the author and not necessarily those of the Bank of Finland orthe Bank of England.

33

1. Introduction

The fundamental premise of this paper is that the legal and supervisoryframework of the financial industry matter as a precondition for stability.An effective and workable regulatory and supervisory regime is basicallyforward-looking and anticipatory, so that those responsible for financialsystem stability ensure that the regime is adapted to forthcoming, or atleast current, changes in the surrounding economy. This is the aspect,which has often been given too little weight – if not forgotten entirely -during the regime shift periods that preceded banking crises in manycountries.

An analysis of how the financial infrastructure may have contributed tobanking crises is complicated and politically unattractive to domesticpolicy makers. However, while the state of a country’s financialinfrastructure may not be the trigger for a banking crisis it is clear frompast experience that it may affect the scope, depth and length of a crisis.

But what constitutes an effective regulatory and supervisory framework?Increasingly, global integration and the development of financial marketshave put pressure on supervisors to focus their attention on the role ofincentives alongside rules, as supervisory authorities struggle to keep upwith the financial world they are supposed to safeguard. It is today quitewidely accepted that the regulatory and supervisory framework should bebased on incentives that make banks and supervisors act in a way thatsupports both the stability of the financial system as a whole and theinterests of banks. However, there are different views on the practicalfeatures of such a framework.

The aim of this paper is to highlight possible features of an incentive-based legal, regulatory and supervisory framework that would minimiseincentives for excessive risk-taking in the business of banking andcompensate for moral hazard generated by the existence of safety nets. Icome to the topic as a lawyer who works with economists. Much of thediscussion referred to in this paper is based on developed countries, inparticular Scandinavian countries and to some degree the UK.

Section 2 explains very briefly the theoretical background for incentive-based regulation, showing the link between the assumption of rationalityin an individual’s behaviour and legal rules. Section 3 highlights keyelements of an incentive-based approach for a legal, regulatory andsupervisory framework. Section 4 introduces corporate governance as aconcept for concrete policy suggestions to increase the commitment ofbank management, shareholders and supervisors to their duties. Section 5

34

briefly explores whether and how an incentive-based corporategovernance framework can be applied to less developed countries.Finally, section 6 raises the question of the role of central banks inpromoting good corporate governance as part of their role in financialstability.

2. A theoretical background

In the field of law-and-economics, economics provides assumptions onthe economic effects of legal rules. A normative viewpoint goes beyondthe positive analysis of economic effects and takes a view in favour oragainst various legal rules, giving recommendations for the most effectivelegislation.

The paper uses the assumptions of neo-classical economic theory toexplain and assess the links between the three dimensions of law: ethical,normative and realistic/factual.15 Thus, as regards the first dimension,economics provides assumptions on the legal structure supporting thefunctioning of ideal markets. These are the assumptions of natural law,which is the legal counterpart of neo-classical economics. To clarify,natural law assumes that legal rules are defined in a hypothetical situationin which no one knows which individual will be subject to which legalrule. This ensures that legislation is just, acceptable to all members of asociety and in harmony with the interests of individuals and society. Thecounterpart to this in banking legislation is the assumption that thecontents of laws should not be influenced by notions of who will besubject to the legal rule being enacted and in what way. Similarly, the aimshould be to enact legal rules that are consistent with the overallobjectives of banking legislation, not just with the interests of, forexample, one particular banking group.

As for the second dimension, we can use economics to control thefunctioning of the normative level, that is the effects of current legalrules. Finally, as regards the third dimension - and most importantly fromthe point of view of this paper - economics provides assumptions on howthose subject to regulation actually behave and what is the incentiveimpact of legal rules on their behaviour. The drafting of legal rules shouldtake into account that individuals behave rationally, i.e. in their self-interest. Under perfect market conditions this kind of behaviour leads toefficient outcomes (pareto-optimality) which are in harmony with theobjects of a society. In addition, this behaviour is also acceptable from anethical point of view, but only under assumptions of ideal markets. Thisview can be linked to natural law and the concept of a social contract, 15 See Halme (1999a and 1999b).

35

which has been dealt with in depth by various contractarian schools ofthought (moral, social and constitutional contractarians).

However, the real world is not ideal. One of the most analyseddeficiencies is the lack of perfect information and the issue of how thisaffects the actions and outcomes of rationally behaving agents. This fieldof economic theories is called principal-agent theory. It is important tonote that the assumption of rationality prevails even in the real world withinformation problems, but rationality now leads to outcomes that can bedetrimental from a financial stability point of view. The key issue is howto build the regulatory and supervisory framework so that it allowsmarkets to become as efficient as possible and – because conditions ofideal markets cannot be achieved – how to correct distortions caused bynon-ideal conditions, such as asymmetric information and moral hazard.

The answer stems from the idea of legal rules as incentives16 for bringingabout desired behaviour. However, the problem is that an individual maynot automatically obey the rules, particularly if they are not in line withhis self-interest and failure to comply elicits only a minor sanction. Thisgives rise to an obvious tension between an obligation to obey legitimaterules and rationality-based behaviour (agent as law-taker). It is alsopossible that the agent, for example banks, will attempt to direct thecourse of legal amendments (agent as lawmaker). In the latter case, if alegislator does not act ‘behind the veil of ignorance’, i.e. he does not treatall parties on an equal basis, there is a danger that particular parts of thelegislation may be amended in a way that is contradictory to theobjectives of the entire piece of legislation.

For the legislator, this means that in drafting law he must take intoaccount the rationality-based behaviour of individuals. It also means thatin a ‘proper’ legal framework the pursuit of self-interest can be consistentwith the interests of society, or public good. In other words, the idea ofcomplete contracts should be transferred to legal rules so that the agents17

are responsible for their actions, receive the benefits of them and take partin risk sharing. This gives us rules that are based on a clear and explicitdivision of responsibilities, but also explicit and exercisable rules onsanctions. This is how to maximise the agent’s commitment tocompliance with the rules, and minimise the distorting effects of 16 See Kornhauser (1989).17 The concept of agent refers to principal – agent theory. In this theory, a principal engages an agentto act on his/her behalf. Due to asymmetric information, however, the principal is unable to observe theactions of the agent entirely, and there is scope for the agent to deviate from the principal’s wishes.There are various agent–principal relations in the field of banking regulation and supervision.Legislator can act as a principal and supervisor as an agent, depositor as a principal and bank as anagent, supervisor as a principal and bank as an agent, shareholders as principals and bank managementas an agent, non-executive board as a principal and management as an agent.

36

asymmetric information and moral hazard. This is the basis of legal rulesas incentives.

However, it is worth pointing out that not all economists – let alonelawyers – share the above view on legal rules as incentives, andespecially its origins in neo-classical economic theory with its concepts ofrationality and individual welfare maximisation. They argue that theconcept of rationality aimed at the maximisation of self-interest of anagent is about the rationality of greed. They suggest that in order to limitthe pursuit of self-interest, agents must take into account moral andethical principles. Thus, for example, incentives together with ethics forma sound basis for financial market stability.

The link between ethics (the approach of equality, justice and fairness)and financial market legislation can also be viewed from the perspectiveof depositor protection (consumer protection) and financial stability.These two aspects form the basic rationale for the whole of bankinglegislation. Thus it is also the responsibility of the banks themselves,when pursuing their self-interest, to take into account the interests ofother stakeholders and the stability of financial markets as a whole, notjust the interests of the shareholders. Or, as the EU Council has noted,well-functioning financial markets must strike a balance between theinterests of market players, consumer protection and the need to maintaina reliable regulatory framework that has the capacity to ensure thestability of financial markets while adapting to new developments.18

Conclusions from theory

The key conclusion is that neo-classical economic theory can providesome guidelines for structuring an incentive-based legal, regulatory andsupervisory system. The problem is that the theory does not tell you muchabout how to implement an institutional, legal or supervisory framework.Neither does it tell us much about the actual behaviour of particularagents because the theory itself is too rough to model individualpreferences. Rather it just gives a general prediction of the behaviour ofagents, taking into account the intrinsic rationality and self-interestassumption in various principal – agent relations. However, for example,Friedman defends the relevance of assumptions of neo-classicaleconomics and emphasises the differences between a description andprescription.19

18 See Journal of Financial Regulation, June 1999.19 See Friedman (1953)

37

What we can take from the basis of the theory is that, when structuringthe legal and supervisory framework, we have to mimic completecontracts in rule setting, and mimic ideal market conditions by exploitingmarket discipline. Rules and incentives need not be seen as separate anddistinct tools, which is the point of view quite often taken in economic orregulatory literature. Rules should also be based on incentives. Even so,the more market discipline there is in practice, the more we can count onan endogenous (self-imposed) governance system.20 However, untilperfect market conditions can be achieved with a self-imposedgovernance system – as the proponents of the free banking school havesuggested – we need ex ante and externally prescribed rules by thelegislator, regulator or supervisor. And we need an enforcement systemfor both legally binding and self-imposed rules.

3. Key elements of an incentive-based legal, regulatory andsupervisory framework

To begin with, the lawmaking process should be such that it leads to asensible and well-reasoned division of responsibilities and to sound ruleson disclosure of information and competition. Furthermore, the contentsof legislation should not be affected by the interests of the parties subjectto regulation, unless this can be justified on stability grounds. Similarly,considerations relating to the interests of banks should not influencesupervision or the decisions of regulators, if they are not compatible withthe stability of the financial system as a whole.

The requirement of perfect information cannot be satisfied in the realworld. For example, bank management is always better aware of thebank’s financial situation than the supervisor, shareholders, depositors orcreditors. It is the ’mission’ of the legislator to correct distortions causedby asymmetric information.

When emphasising the importance of transparency in the business ofbanking, we normally consider the rules concerning disclosure ofinformation on the financial status and risk exposures of the bank. Fromthe supervisor’s point of view transparency and disclosure requirementsmean, above all, the minimisation of private information. Transparency

20 See e.g, Goodhart et al (1998). He concludes the following: ‘One of the key questions that arises isthe extent to which behaviour is to be altered by externally imposed rules, or through creatingincentives for firms to behave in a particular way. Regulation can be endogenous to financial firm (i.e.self-control) as well as exogenous. A major issue, therefore, is whether regulation should proceedthrough externally imposed, prescriptive and detailed rules, or by the regulator creating incentives forappropriate behaviour.’ See also Llewellyn (1999).

38

may also be improved by disclosing supervisory decisions and actions -positive and negative. This is discussed in section 4.6.

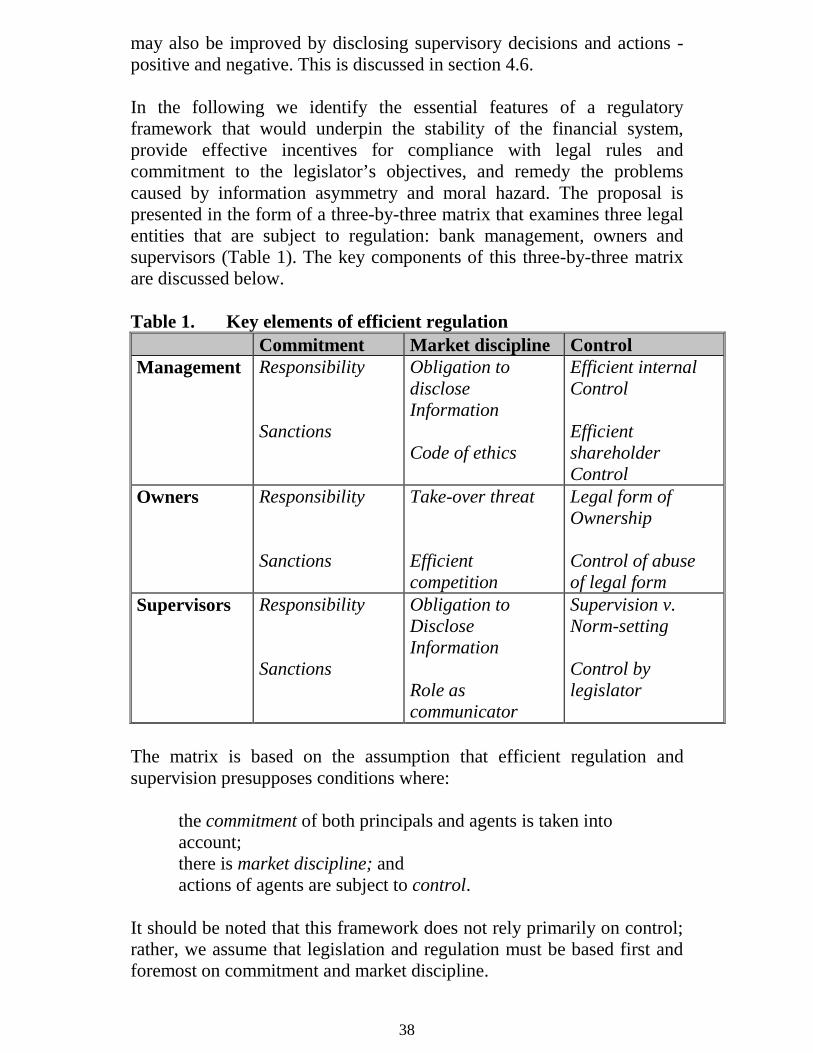

In the following we identify the essential features of a regulatoryframework that would underpin the stability of the financial system,provide effective incentives for compliance with legal rules andcommitment to the legislator’s objectives, and remedy the problemscaused by information asymmetry and moral hazard. The proposal ispresented in the form of a three-by-three matrix that examines three legalentities that are subject to regulation: bank management, owners andsupervisors (Table 1). The key components of this three-by-three matrixare discussed below.

Table 1. Key elements of efficient regulationCommitment Market discipline Control

Management Responsibility

Sanctions

Obligation todiscloseInformation

Code of ethics

Efficient internalControl

EfficientshareholderControl

Owners Responsibility

Sanctions

Take-over threat

Efficientcompetition

Legal form ofOwnership

Control of abuseof legal form

Supervisors Responsibility

Sanctions

Obligation toDiscloseInformation

Role ascommunicator

Supervision v.Norm-setting

Control bylegislator

The matrix is based on the assumption that efficient regulation andsupervision presupposes conditions where:

the commitment of both principals and agents is taken intoaccount;there is market discipline; andactions of agents are subject to control.

It should be noted that this framework does not rely primarily on control;rather, we assume that legislation and regulation must be based first andforemost on commitment and market discipline.

39

Commitment refers to the existence of explicit rules concerningresponsibility and sanctions in the event of non-compliance. Commitmentis linked to the law-and-economics viewpoint that sees legal rules asincentives and the assumption of economic theory regarding the rationalbehaviour of individuals. Legal rules should pursue the ideal of perfectcontracts in which the agent bears full responsibility for performing thetask specified in the contract, and an effective sanction is imposed for thebreach of the contract.

Market discipline refers mainly to obligations to disclose information,which depositors, investors, regulators and the markets in general can useas a reliable basis for assessing the activities of a bank and thusoverseeing e.g. bank management. Here market discipline is associatedwith first-best solutions, by which it is endeavoured to eliminate theunderlying causes of problems encountered in banking and bankingregulation. The smaller the amount of private information a particularagent has, the less that agent can act in a way that is at variance with theprincipal’s objectives and the less is excessive risk taking. Disclosure ofinformation imposes discipline but it is only effective if there iscompetition. In the absence of competition there is also a need forcontrol.

Control is needed to support commitment and market discipline. Controlwould not be needed at all if a state of perfect information, one of therequirements for perfect markets, could be achieved in the real world. Asthis objective can never be fully met, the actions of agents must besupervised. However, control itself suffers from the very shortcomingthat it is needed to deal with, namely imperfect information. Since theagent always knows more about his own actions than does the principalor his representative who exercises control, the potential for control aloneto reduce moral hazard and excessive risk taking is limited.

4. Corporate governance and the implementation of anincentive-based framework

Corporate governance has become a topical issue worldwide inconnection with efforts to structure and implement an efficient legal,regulatory and supervisory framework for financial markets. The bankingcrises of recent decades have highlighted the importance of a well-functioning legal, regulatory and supervisory framework in ex anteprevention of massive banking crises and the reduction of the resultingpain. The crises have clearly demonstrated that there can be seriousnegative outcomes in situations where the incentives influencing the

40

behaviour of legislators, regulators, supervisors or banks (management,board, shareholders) are inappropriate. Corporate governance as part of alegal and regulatory infrastructure has been seen as a device to mitigatemoral hazard problems and make bank management accountable toshareholders and other stakeholders, including supervisors. The need foraccountability and for appropriate incentives also applies to regulatorsand supervisors.

This paper looks at corporate governance from the agency perspective,seeking answers to the question of how to increase the commitment ofmanagement, owners and supervisors. However, before drawingconclusions, we shed some light on the definitions of the concept and keyfeatures of studies and concrete work on the issue of corporategovernance (sections 4.1 – 4.3). I also give some concrete country-specific examples, mostly from Scandinavian countries, and exploreproblems related to managerial discretion, shareholder control andsupervisory discretion (sections 4.4–4.6).

The view of corporate governance in this paper goes beyond just therelationship between management, board and shareholders. I am alsomore inclined towards the view of the likes of Jean Tirole, who arguesthat focusing on shareholder value alone generates biased decision-making although it is better founded, say with regard to incomegeneration and the clear mission of management.21 He sees corporategovernance as an arrangement by which institutions induce or forcemanagement to internalise the welfare of all stakeholders, not justshareholders. Supervisors implement rules and regulations and representdispersed depositors. Thus they play the role of one important stakeholderin banks’ corporate governance.

4.1 Definitions of corporate governance