Financial Repression in Transition Output Reduction and Hyperinflation in the Formerly Soviet...

23

Financial Repression in Transition Output Reduction and Hyperinflation in the Formerly Soviet Economies UNC-MGIMO Seminar, 27 April 2001

-

Upload

jasmine-jennings -

Category

Documents

-

view

217 -

download

1

Transcript of Financial Repression in Transition Output Reduction and Hyperinflation in the Formerly Soviet...

Financial Repression in Transition

Output Reduction and Hyperinflation in the Formerly

Soviet Economies

UNC-MGIMO Seminar, 27 April 2001

Thesis Financial Repression contributed to the

output reduction and hyperinflation observed in the former Soviet economies in the 1990s.

Sustainable recovery from this depression requires governments in these economies to follow policies that eliminate financial repression.

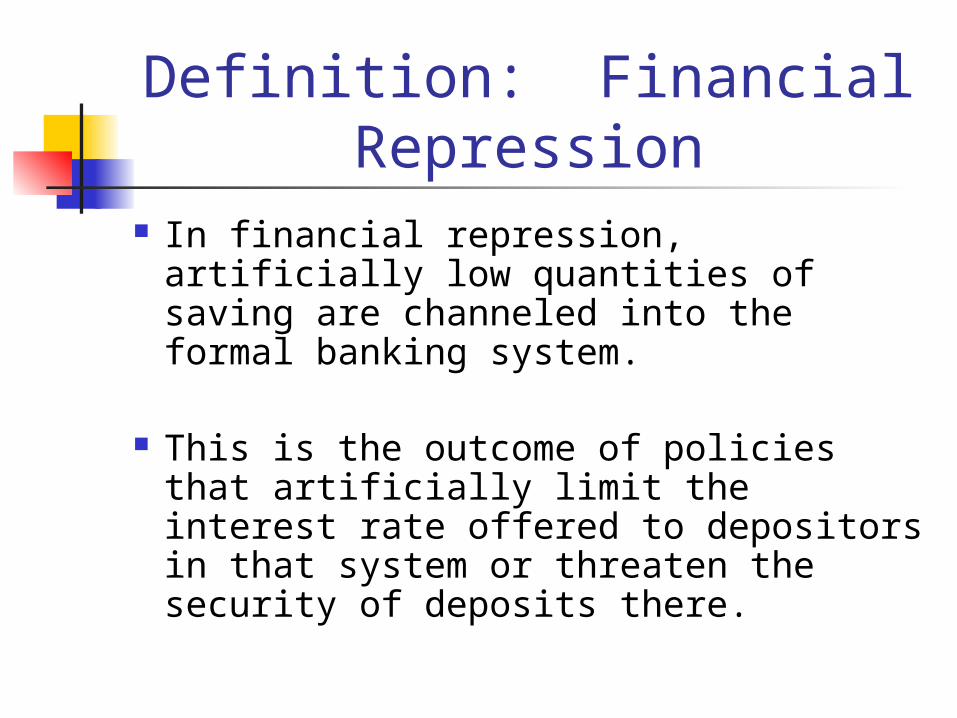

Definition: Financial Repression

In financial repression, artificially low quantities of saving are channeled into the formal banking system.

This is the outcome of policies that artificially limit the interest rate offered to depositors in that system or threaten the security of deposits there.

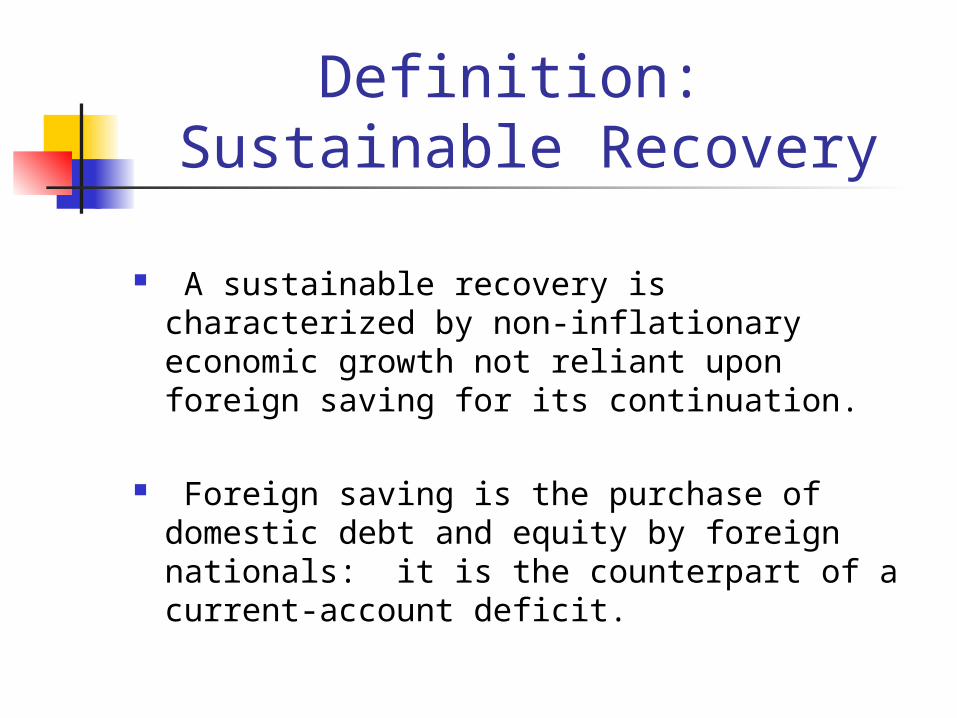

Definition: Sustainable Recovery

A sustainable recovery is characterized by non-inflationary economic growth not reliant upon foreign saving for its continuation.

Foreign saving is the purchase of domestic debt and equity by foreign nationals: it is the counterpart of a current-account deficit.

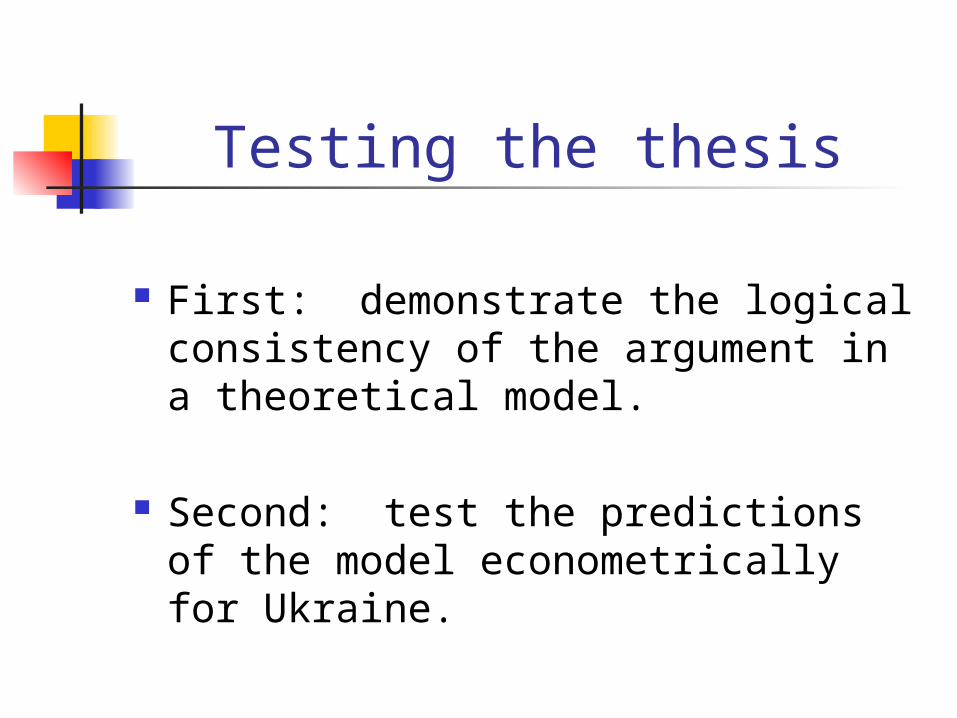

Testing the thesis

First: demonstrate the logical consistency of the argument in a theoretical model.

Second: test the predictions of the model econometrically for Ukraine.

Theoretical building blocks Output depends upon the cost and

availability of credit. The saving (non-consumption) choice

depends upon the real interest rate on saving instruments and the real value of accumulated wealth.

Financial repression reduces desired saving and credit availability: output falls as firms are rationed, hyperinflation follows as saving is induced.

PE

FE

nn*

*

Equilibrium without Financial Repression

Inflationary Consequences of Financial Repression

With excess demand for saving, the real interest rate will rise.

The government has another tool to raise saving. It can induce saving by lowering the value of accumulated wealth. Inflation does this.

Financial Equilibrium for Earmarked Instruments

HH

at-1/(1+ t)

DD

t*

0 at-1/(1+ t)*

Inflation/Output Dynamics

HH

at-1/(1+ t)

DD

o= v

0

ii

Bv

ao

i

iii

Bii

Bi

Biii

i

rii

rv

B

DRri

ii

’

Financial Fragmentation: the Foreign Exchange

Market

HH

q

*

v

0

’

SS

qvq*

45o

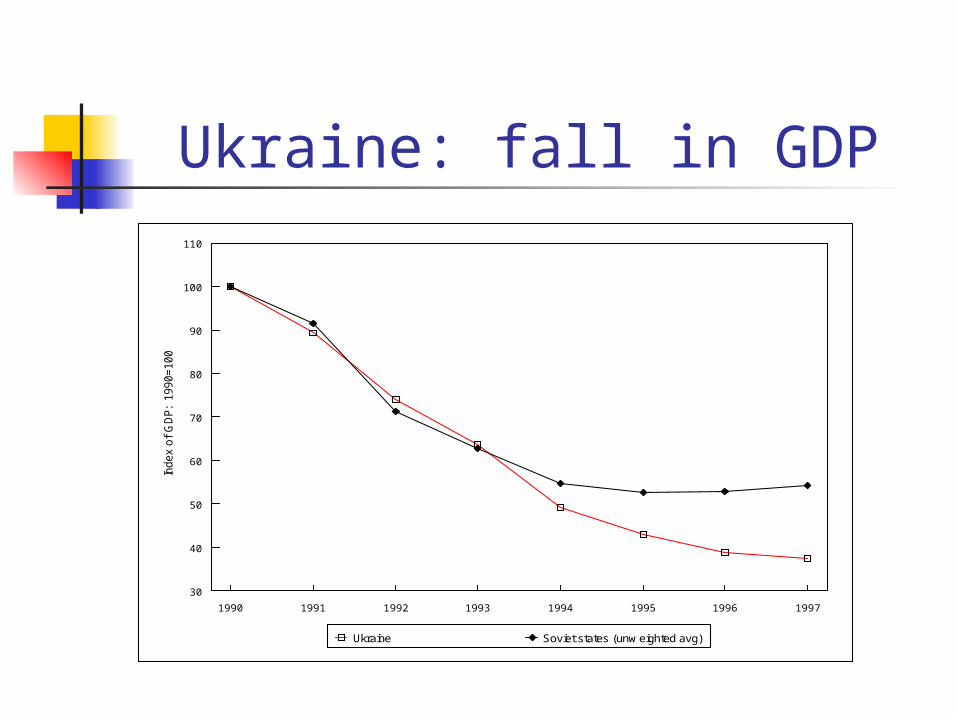

Ukraine: fall in GDP

30

40

50

60

70

80

90

100

110

Index o

f G

DP: 1

990=100

1990 1991 1992 1993 1994 1995 1996 1997

Ukraine Soviet states (unw eighted avg)

Ukraine: Hyperinflation

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

Perc

ent A

nnua

l Inf

latio

n R

ate

1991 1992 1993 1994 1995 1996 1997

Ukraine Soviet states (unw eighted avg)

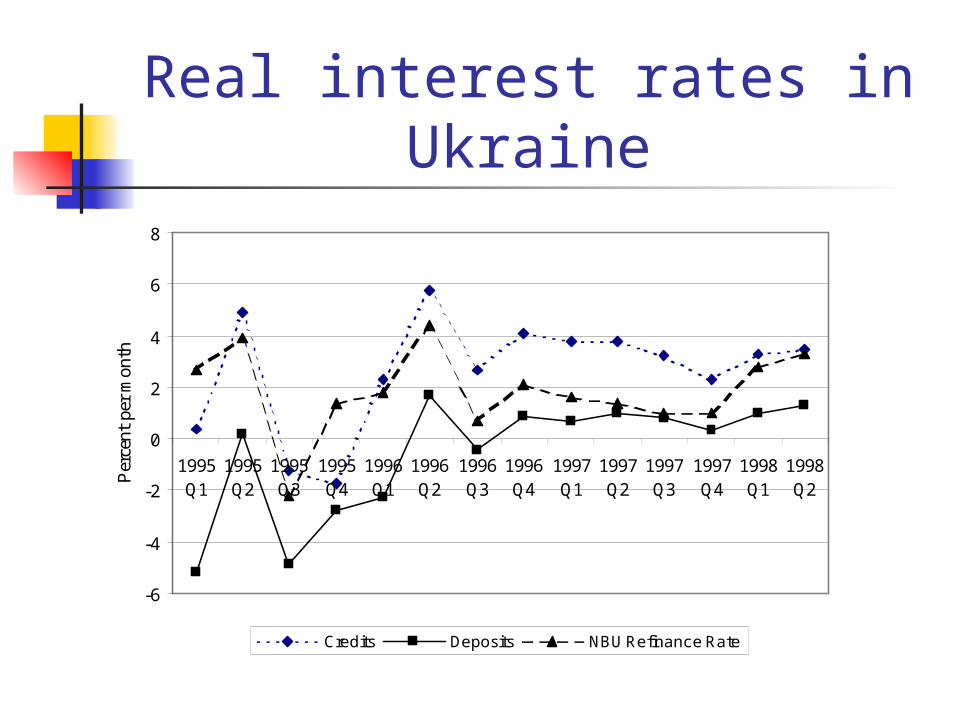

Real interest rates in Ukraine

-6

-4

-2

0

2

4

6

8

1995Q1

1995Q2

1995Q3

1995Q4

1996Q1

1996Q2

1996Q3

1996Q4

1997Q1

1997Q2

1997Q3

1997Q4

1998Q1

1998Q2P

erce

nt p

er m

onth

Credits Deposits NBU Refinance Rate

Output depends on credit availability

GDP Function Regression Results

(Quarterly data, 1993/1 to 1998/3)

Dependent variable: ln(yt)

Intercept -4.14 -1.71

(0.88) (0.72)

ln(Wt-1/Pt-1) 0.60 0.44

(0.10) (0.14)

ln(Ryt) 0.90 0.62

(0.12) (0.14)

ln(CRt)* 0.24(0.10)

ln(CRt-1/PBt-1) 0.11

(0.03)

R2 0.85 0.92

F(.) 30.32 59.65

N 19 19

* – Treated as simultaneously determined variable. Instruments include lagged endogenous variables, budget deficit, and exogenous regressors in these equations.

Inflation to induce saving

Dependent variable: t

Intercept -118.04 -106.20

(50.17) (49.93)

t-1 -4.53 -4.35

(3.27) (3.21)

at-1 3.19 2.51

(1.04) (1.13)

µt ---- 0.50

(0.36)

R2 0.36 0.41

F(x,23-x) 5.88 4.70

N 23 23

For the F statistic, x=2 for the first equation and x=3 in the second equation. Standard errors

in parentheses.

Saving Allocation Responded to Real-interest-rate movements

Household portfolio decisions show significant support for theory. (Table 4)

Enterprise portfolio decisions follow quite different incentives.

The role of foreign-currency denominated instruments is also in line with theory. (Table 5)

Sustainable Growth?

-1000

-750

-500

-250

0

250

500

750

1000

1/1995

3/1995

1/1996

3/1996

1/1997

3/1997

1/1998

3/1998

1/1999

3/1999

mill

ions

USD

Net foreign investment Net increase in FX reserves

Conclusions to paper Financial repression is

demonstrated as a logically consistent cause of both output reduction and hyperinflation.

Evidence from Ukraine supports this thesis.

Financial Repression and the Financial Crisis of 1998 Was the non-inflationary growth in

Russia and Ukraine prior to August 1998 sustainable?

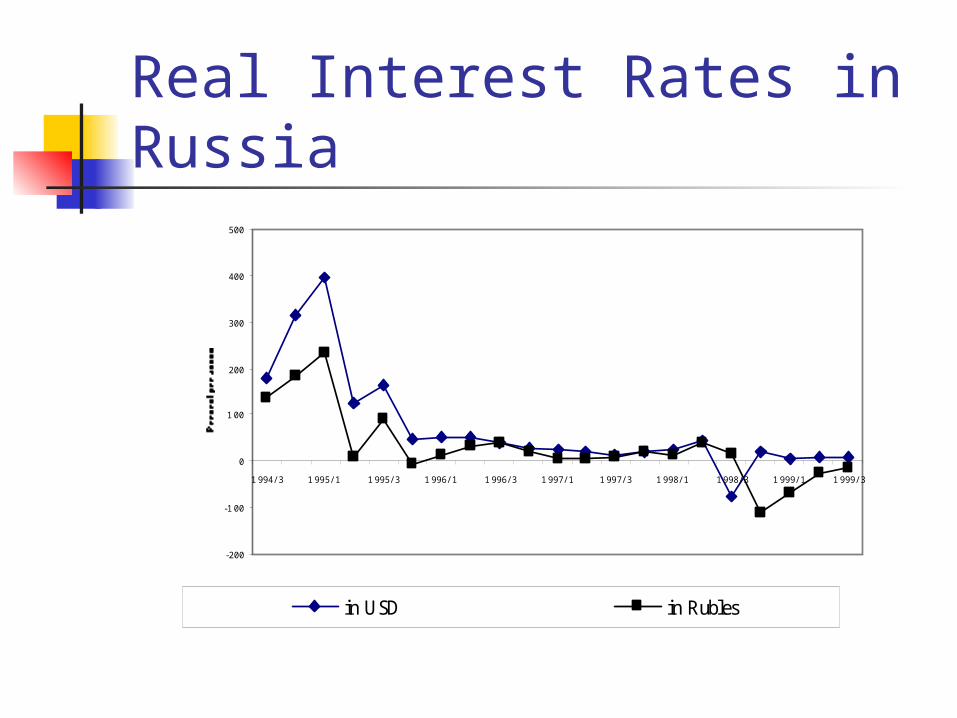

Real Interest Rates in Russia

-200

-100

0

1 00

200

300

400

500

1 994/ 3 1 995/ 1 1 995/ 3 1 996/ 1 1 996/ 3 1 997/ 1 1 997/ 3 1 998/ 1 1 998/ 3 1 999/ 1 1 999/ 3

in USD in Rubles

Sustainable Growth in Russia?

0

5000

10000

15000

20000

25000

1993/ 4 1994/ 2 1994/ 4 1995/ 2 1995/ 4 1996/ 2 1996/ 4 1997/ 2 1997/ 4 1998/ 2 1998/ 4 1999/ 2 1999/ 4

Total FX reserves IMF Credit/Loans Outstanding

Russian Borrowing at the IMF

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

1992 1993 1994 1995 1996 1997 1998 1999 2000

mill

ion

s o

f S

DR

s

Disbursed by IMF Russian repurchases