Financial Reporting on the Internet Andrew Lymer Lymer & Associates and The University of Birmingham...

23

Financial Reporting on the Internet Andrew Lymer Lymer & Associates and The University of Birmingham [email protected]

-

Upload

kimberly-campbell -

Category

Documents

-

view

214 -

download

0

Transcript of Financial Reporting on the Internet Andrew Lymer Lymer & Associates and The University of Birmingham...

Financial Reporting on the Internet

Andrew LymerLymer & Associates and The University of [email protected]

Outline

BackgroundCurrent Technologies &

TrendsInternational activityBest practice quick guideDemise of annual reporting?Conclusion

Background

Internet History - the bits that still matter Developed in USA No central governing body Statistics? - big enough to matter!

Estimated 850 million indexable web pages

High penetration amongst companiesRecent global survey of large co.s - 62% 100% in Germany, Sweden, Canada and USALowest - Chile at 52%

Current Technologies

The Technologies CD-ROM - largely bypassed Electronic Paper - e.g. Adobe Acrobat HTML + plug-ins, multimedia, 3D Dynamic media - database driven, Java Push technologies XML - the future? Intelligent Agents ….

International Activity

Online Reporting Current ‘Hot Topic’ AICPA -

Jenkins Report (94), Elliott Report (96), Vision Project, Continuous Auditing Report (99), XFRML

FASB - ‘Top 4’ strategy itemBusiness Reporting Research Project (99)Faux com Inc. (98)

ICAEW & ICAS21st Century Company Reporting (98)Business Reporting - An Inevitable

Change? (99)

International Activity

CICA - ‘Impact of Technology on Financial and Business Reporting’ November 1999

‘..the WWW is beginning to challenge the very nature of financial reporting, its boundaries, its frameworks, even its fundamental role in society’

International Activity

IASC - ‘Business Reporting on the Internet’ (Nov 1999) Purpose

to examine the nature of change occurring in business reporting and the dissemination of accounting and business information.

to identify the effects the change may have on the future of accounting standard setting.

to recommend a set of measures to deal with the varied forms of electronic business reporting.

International Activity

Examination of top 30 companies in Dow Jones Global Index (22 countries)

16% had no website22% had website but no financials96% provide Income Statement95% provide Balance Sheet52% provide full Notes to Accounts45% provide ‘Audit Report’

International Activity

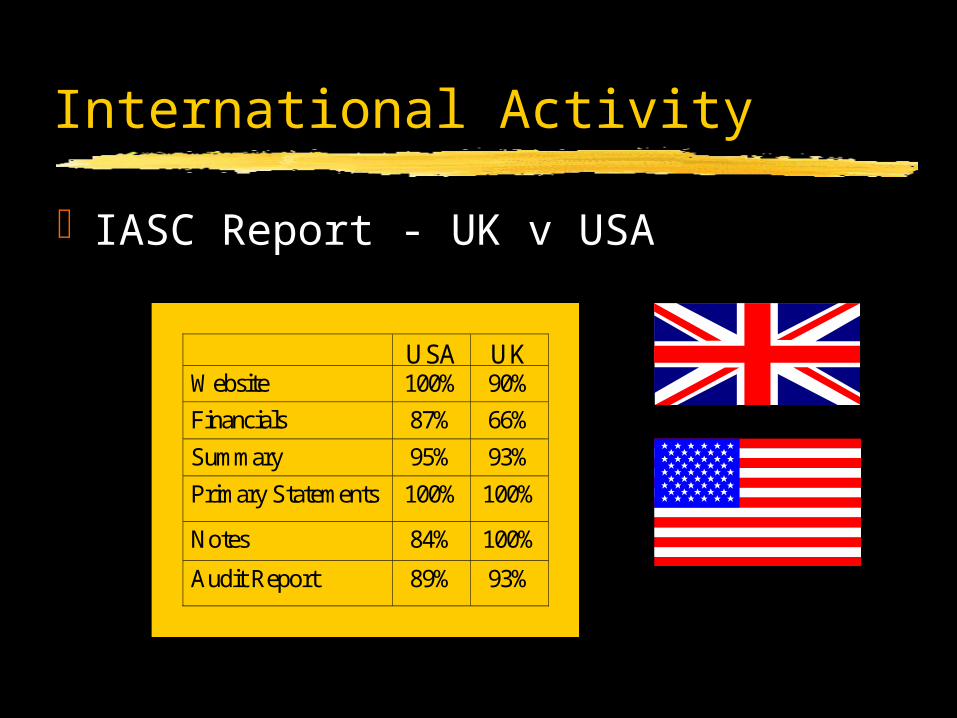

IASC Report - UK v USA

USA UK Website 100% 90%

Financials 87% 66%

Summary 95% 93%

Primary Statements 100% 100%

Notes 84% 100%

Audit Report 89% 93%

International Activity

IASC Report Recommendations Short Term proposal

‘Code of Conduct’

Longer Term issuesThe ‘Business Reporting Language’

International Activity

IASC Report - Short Term Proposal Example areas covered by code :

clear foundation of responsibilitiesdeparture point from financials

indicatedcomparison of paper and online

versions possibleclear labelling of GAAP used &

reconciliation between GAAPs

International Activity

Short Term Proposal continued..data should be placed online

immediately availableinformation should be

stable/accessible over timeaudit reports to be made available for

audited dataall supplementary data should be

available online

International Activity

Longer Term Issues HTML is presentation language

limited usefulness

Need data description ‘language’favoured example = XML

Allows for ‘combined reporting’ without overloade.g. company financials, news, share details etc

Requires co-operation to make work

International Activity

Where next? AICPA etc proposal for

XFRML?What does it mean?Extensible Financial Reporting

Mark up Language

What does it ACTUALLY mean?

International Activity

XFRML ‘Framework which allows companies,

accountants, investors, bankers, industry analysts, regulators and others involved in the financial reporting supply chain, a standard way to prepare publish, exchange and analyze financial reports and the information they contain and allow financial information prepared to be reliably and automatically extracted or exchanged between computer applications’

International Activity

XFRML: text based information

At December 31: 1998 1997

Finished Goods £1,088 £1,090

Work in process and 4,112 4,049

raw materials

£5,200 £5,139

International Activity

XFRML: XML based information

<Type>stock</type><Label>STOCK</label><table columns=“3” ID=“stock”> <columnheaders>

<columnheader>At December 31:</columnheader> <columnheader>1998</columnheader> <columnheader>1997</columnheader> </columnheaders> <LineItem>

<Label>Finished Goods</label><amount period=”1998”>1088</amount><amount period=“1997”>1090</amount>

</LineItem>

……..

International Activity

Is the future XFRML? Problems are BIG

role of auditor/attestation?who sets the standards?who monitors and enforces?data integrity?

Current Best Practice

Microsoft - http://www.microsoft.com/msft

Report as pdf & Financial Review Webcasts of events such as earnings

announcements Live stock activity link History in excel spreadsheets & graphs Excel PivotTables for financials analysis Online speeches and meetings in video &

audio Statutory filings & Press Releases Non-financial data

Demise of the annual report?

Key issue to be addressed what do people really want?

e.g. cost v timeliness

who is best placed to deliver it?

Demise of the annual report?

By 2005 - the ‘crystal ball’ globally focused companies the norm interactive investor relations online reporting normal means of

corporate communication single GAAP as only workable solution monthly reporting continuous audit for all listed companies far greater access to historical and forward

looking data for all intelligent software for data analysis

Conclusion

Internet developing rapidly as investor relations tool

Lots of opportunity to use innovatively

Future solutions to overload problems in hand

Globalisation will make online reporting required