Financial reporting in the utilities industry* · PDF file · 2015-06-031.3.1...

72

Energy, Utilities & Mining Financial reporting in the utilities industry* International Financial Reporting Standards April 2008 *connectedthinking

Transcript of Financial reporting in the utilities industry* · PDF file · 2015-06-031.3.1...

Energy, Utilities & Mining

Financial reporting in theutilities industry*International Financial Reporting Standards

April 2008

*connectedthinking

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 1

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 2

The move to International Financial ReportingStandards (IFRS) is advancing the transparencyand comparability of financial statements aroundthe world. Many countries now requirecompanies to prepare their financial statementsin accordance with IFRS. National standards inother countries are being converged with IFRS.The global trend towards IFRS has gainedsignificant further momentum with the USSecurities and Exchange Commission’s (SEC)commitment to the standards, beginning with itsdecision to drop the requirement for foreign-listed companies in the US to reconcile to USGAAP.

The utilities industry is key to the world economy, and an increasing number of companies are nowoperating on an international and, sometimes,global scale. The development of IFRS offersconsiderable long-term advantages for manyutilities companies but, along the way, it bringsconsiderable challenges. The utilities industry ischaracterised, for example, by the need forsignificant upfront investment, often withuncertainty about outcomes over a long-termtime horizon. Its geopolitical, environmental,energy and natural resource supply and tradingchallenges, combined with often complex

stakeholder and business relationships, hasmeant that the transition to IFRS has requiredsome complex judgements about how toimplement the new standards.

This edition of ‘Financial reporting in the utilities industry’ describes the financial reportingimplications of IFRS across a number of areasselected for their particular relevance to utilitiescompanies. It provides insights into howcompanies are responding to the variouschallenges, and includes examples of accountingpolicies and other disclosures from publishedfinancial statements. It examines keydevelopments in the evolution of IFRS in theindustry.

This publication does not describe all IFRSs applicable to utilities entities. The ever-changinglandscape means that management shouldconduct further research and seek specificadvice before acting on any of the more complexmatters raised. PricewaterhouseCoopers has adeep level of insight into and commitment tohelping companies in the sector reporteffectively. For more information or assistance,please do not hesitate to contact your local officeor one of our specialist utilities partners.

Manfred WiegandGlobal Utilities Leader

Foreword

Foreword

1Financial reporting in the utilities industry

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 3

Contents

Introduction 5

1 Utilities Value Chain & Significant Accounting Issues 7

1.1 Generation 9

1.1.1 Fixed assets & components 9

1.1.2 Borrowing costs 9

1.1.3 Decommissioning obligations 10

1.1.4 Impairment 11

1.1.5 Arrangements that may contain a lease 12

1.1.6 Emission Trading Scheme and Certified Emission Reductions 13

1.2 Transmission & Distribution 15

1.2.1 Fixed assets & components 15

1.2.2 Customer contributions 16

1.2.3 Regulatory assets & liabilities 16

1.3 Retail 18

1.3.1 Customer acquisition costs 18

1.3.2 Customer discounts 18

1.4 Company-wide Issues 18

1.4.1 Service concession arrangements 18

1.4.2 Business combinations 19

1.4.3 Financial instruments 21

1.4.4 Trading and risk management 25

2 Developments from the IASB 29

2.1 Borrowing costs 30

2.2 Emissions Trading Schemes 30

2.3 Revenue recognition project 30

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 4

Contents

3Financial reporting in the utilities industry

2.4 IFRS 3, Business Combinations (revised) and IAS 27, Consolidated and Separate Financial Statements (revised) 31

2.5 ED 9 Joint Arrangements 32

3 IFRS/US GAAP Differences 35

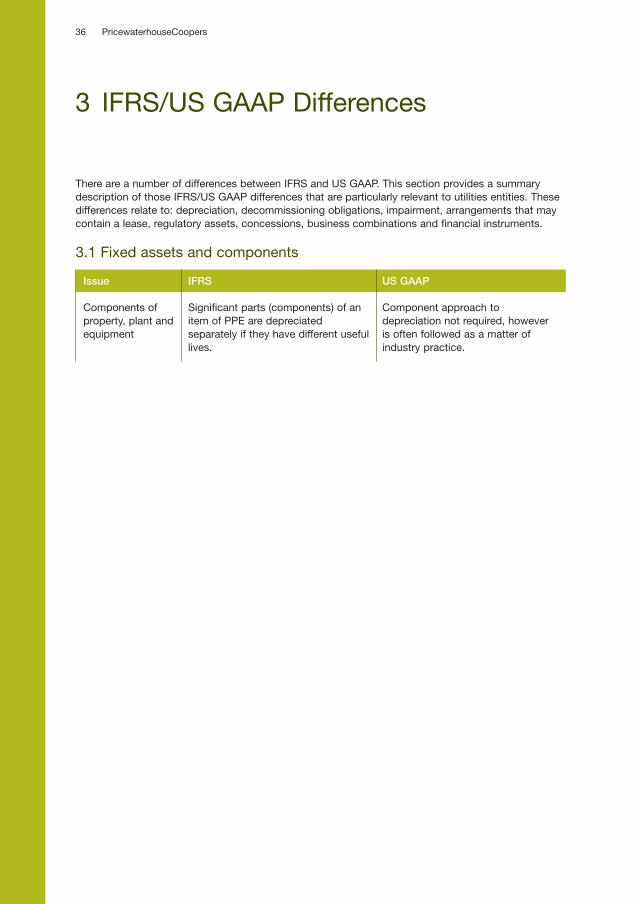

3.1 Fixed assets and components 36

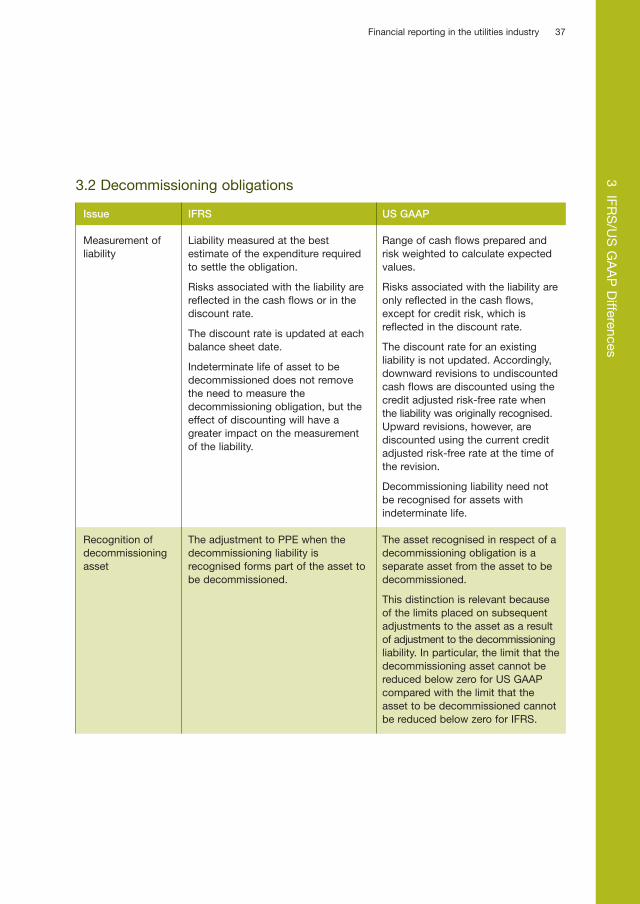

3.2 Decommissioning obligations 37

3.3 Impairment 38

3.4 Arrangements that may contain a lease 39

3.5 Regulatory Assets and Liabilities 39

3.6 Business combinations 40

3.7 Concession arrangements 41

3.8 Financial instruments and trading & risk management 43

4 Financial disclosure examples 45

4.1 Decommissioning obligations 46

4.2 Impairment 48

4.3 Arrangements that may contain a lease 51

4.4 Emission Trading Scheme and Certified Emission Reductions 51

4.5 Customer contributions 52

4.6 Regulatory assets & liabilities 53

4.7 Business combinations 53

4.8 Concession arrangements 54

4.9 Financial instruments 54

Contact us 66

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 5

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 6

What is the focus of this publication?

This publication considers the major accountingpractices adopted by the utility industry underInternational Financial Reporting Standards(IFRS).

The need for this publication has arisen due to:

• the adoption of IFRS by utility entities across a number of jurisdictions, with overwhelming acceptance that applying IFRS in this industry will be a continual challenge; and

• ongoing transition projects in a number of other jurisdictions, for which companies can draw on the existing interpretations of the industry.

Who should use this publication?

This publication is intended for:

• executives and financial managers in the utility industry, who are often faced with alternative accounting practices;

• investors and other users of utility industry financial statements, so they can identify some of the accounting practices adopted to reflect unusual features unique to the industry; and

• accounting bodies, standard-setting agencies and governments throughout the world interested in accounting and reporting practices and responsible for establishing financial reporting requirements.

What is included?

Included in this publication are issues that webelieve are of financial reporting interest due to:

• their particular relevance to utility entities; and/or

• historical varying international practice.

The utility industry has not only experienced the transition to IFRS, it has also seen:

• significant growth in corporate acquisition activity;

• increased globalisation;

• continued increase in its exposure to sophisticated financial instruments and transactions; and

• an increased focus on environmental and restoration liabilities.

This publication has a number of chapters designed to cover the main issues raised.

PricewaterhouseCoopers’ experience

This publication is based on the experiencegained from the worldwide leadership position of PricewaterhouseCoopers in the provision of accounting services to the utility industry. This leadership position enablesPricewaterhouseCoopers’ Global Utility IndustryGroup to make recommendations and leaddiscussions on international standards andpractice.

We hope you find this publication useful.

Introduction

Introduction

5Financial reporting in the utilities industry

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 7

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 8

1 Utilities Value Chain & Significant Accounting Issues

7Financial reporting in the utilities industry1 U

tilities Value Chain &

Significant A

ccounting Issues

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 9

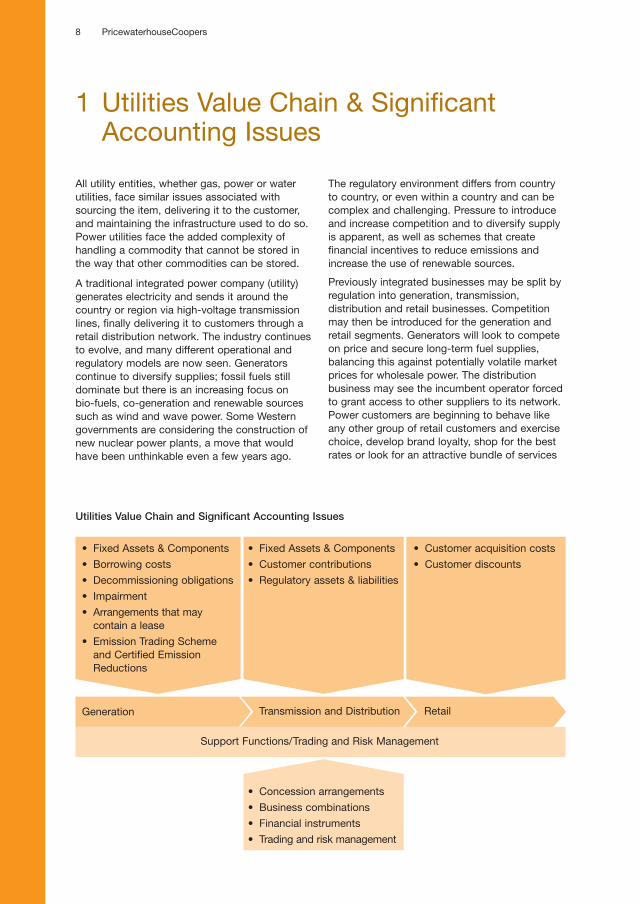

• Fixed Assets & Components

• Borrowing costs

• Decommissioning obligations

• Impairment

• Arrangements that may contain a lease

• Emission Trading Scheme and Certified Emission Reductions

Support Functions/Trading and Risk Management

Generation Transmission and Distribution Retail

All utility entities, whether gas, power or waterutilities, face similar issues associated withsourcing the item, delivering it to the customer,and maintaining the infrastructure used to do so.Power utilities face the added complexity ofhandling a commodity that cannot be stored inthe way that other commodities can be stored.

A traditional integrated power company (utility) generates electricity and sends it around thecountry or region via high-voltage transmissionlines, finally delivering it to customers through aretail distribution network. The industry continuesto evolve, and many different operational andregulatory models are now seen. Generatorscontinue to diversify supplies; fossil fuels stilldominate but there is an increasing focus on bio-fuels, co-generation and renewable sourcessuch as wind and wave power. Some Westerngovernments are considering the construction ofnew nuclear power plants, a move that wouldhave been unthinkable even a few years ago.

The regulatory environment differs from country to country, or even within a country and can becomplex and challenging. Pressure to introduceand increase competition and to diversify supplyis apparent, as well as schemes that createfinancial incentives to reduce emissions andincrease the use of renewable sources.

Previously integrated businesses may be split by regulation into generation, transmission,distribution and retail businesses. Competitionmay then be introduced for the generation andretail segments. Generators will look to competeon price and secure long-term fuel supplies,balancing this against potentially volatile marketprices for wholesale power. The distributionbusiness may see the incumbent operator forcedto grant access to other suppliers to its network.Power customers are beginning to behave likeany other group of retail customers and exercisechoice, develop brand loyalty, shop for the bestrates or look for an attractive bundle of services

1 Utilities Value Chain & Significant Accounting Issues

8 PricewaterhouseCoopers

Utilities Value Chain and Significant Accounting Issues

• Fixed Assets & Components

• Customer contributions

• Regulatory assets & liabilities

• Concession arrangements

• Business combinations

• Financial instruments

• Trading and risk management

• Customer acquisition costs

• Customer discounts

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 10

that might include gas, phone, water and internetservices as well as power.

The regulatory environment with continuing government involvement in pricing, security ofsupply, pressure to reduce emissions and otherpollutants and increasing competition all impacton how business is conducted, and give rise tosome difficult accounting issues. This publicationexamines the accounting issues that are mostsignificant for the utilities industry. The issues areaddressed following the utilities value chain:generation, transmission & distribution, retail andissues that impact on the entire entity.

For published financial disclosure examples, seeSection 4 on page 45.

1.1 Generation

1.1.1 Fixed assets & components

IFRS has a specific requirement for ‘component’ depreciation, as described in IAS 16 Property,plant and equipment. Each significant part of anitem of property, plant and equipment isdepreciated separately. Significant parts of anasset that have similar useful lives and pattern ofconsumption can be grouped together. Thisrequirement can create complications for utilitiesentities, as there are many assets that includecomponents with a shorter useful life than theasset as a whole.

Identification of components of an asset

Generating assets are often large and complex installations. They are expensive to construct,tend to be exposed to harsh operating conditionsand require periodic replacement or repair.Generating assets might comprise a significantnumber of components, many of which will havediffering useful lives. The significant componentsof these types of assets must be separatelyidentified. It can be a complex process,particularly on transition to IFRS, as the detailedrecordkeeping may not have been required tocomply with national GAAP. This can particularlybe an issue for old power-generating plants.However, some regulators may require detailedasset records, which can be useful for IFRScomponent identification purposes.

An entity might look to its operating data if the necessary information for components is notreadily identified by the accounting records.Some components can be identified byconsidering the routine shutdown or overhaulschedules for power stations and thereplacement and maintenance routinesassociated with these. Consideration should alsobe given to those components that are prone totechnological obsolescence, corrosion or wearand tear more severe than that of the otherportions of the larger asset.

Depreciation of components

Those identified components that have a shorter useful life than the remainder of the asset shouldbe depreciated to their recoverable amount overthat shorter useful life. The remaining carryingamount of the component is derecognised onreplacement and the cost of the replacement partis capitalised.

The costs of performing a turnaround/overhaul are capitalised as a component of the plant,provided this provides access to future economicbenefits, but turnaround/overhaul costs that donot relate to the replacement of components orthe installation of new assets should beexpensed when incurred. Turnaround/overhaulcosts should not be accrued over the periodbetween the turnarounds/overhauls becausethere is no legal or constructive obligation toperform the turnaround/overhaul – the entitycould choose to cease operations at the plantand hence avoid the turnaround/overhaul costs.

1.1.2 Borrowing costs

The cost of an item of property, plant and equipment may include borrowing costs incurredfor the purpose of acquiring or constructing it.Such borrowing costs may be capitalised if theasset takes a substantial period of time to getready for its intended use. The capitalisation ofborrowing costs under IAS 23 Borrowing Costs(Issued 1993) is an option, but one which mustbe applied consistently to all qualifying assets.However, amendments to IAS 23 that werepublished in 2007 and become effective from 1 January 2009 will require that all applicableborrowing costs be capitalised.

9Financial reporting in the utilities industry1 U

tilities Value Chain &

Significant A

ccounting Issues

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 11

Borrowing costs should be capitalised while acquisition or construction is actively underway.These costs include the costs of specific fundsborrowed for the purpose of financing theconstruction of the asset, and those generalborrowings that would have been avoided if theexpenditure on the qualifying asset had not beenmade. The general borrowing costs attributableto an asset’s construction should be calculatedby reference to the entity’s weighted averagecost of general borrowings.

1.1.3 Decommissioning obligations

The utilities industry can have a significantimpact on the environment. Decommissioning orenvironmental restoration work at the end of theuseful life of a plant or other installation may berequired by law, the terms of operating licencesor an entity’s stated policy and past practice. An entity that promises to remediate damage,even when there is no legal requirement, mayhave created a constructive obligation and thus a liability under IFRS. There may also beenvironmental clean-up obligations forcontamination of land that arises during theoperating life of a power plant or otherinstallation. The associated costs ofremediation/restoration can be significant. The accounting treatment for decommissioningcosts is therefore critical.

Decommissioning provisions

A provision is recognised when an obligation exists to remediate or restore. The local legalregulations should be taken into account whendetermining the existence and extent of theobligation. Obligations to decommission orremove an asset are created at the time the asset is placed in service. Entities recognisedecommissioning provisions at the present value of the expected future cash flows that willbe required to perform the decommissioning.The cost of the provision is recognised as part ofthe cost of the asset when it is placed in serviceand depreciated over the asset’s useful life. Thetotal cost of the fixed asset, including the cost ofdecommissioning, is depreciated on the basisthat best reflects the consumption of theeconomic benefits of the asset: generally time-based for a power station.

Provisions for decommissioning and restoration are recognised even if the decommissioning isnot expected to be performed for a long time, forexample 80 to 100 years. The effect of the timeto expected decommissioning will be reflected inthe discounting of the provision. The discountrate used is the pre-tax rate that reflects currentmarket assessments of the time value of money.Entities also need to reflect the specific risksassociated with the decommissioning liability.Different decommissioning obligations will,naturally, have different inherent risks, forexample different uncertainties associated withthe methods, the costs and the timing ofdecommissioning. The risks specific to theliability can be reflected either in the pre-tax cashflow forecasts prepared or in the discount rateused.

A similar accounting approach is taken for nuclear fuel rods. These rods are classified asinventory, and an obligation to reprocess them istriggered when the rods are placed into thereactor. A liability is recognised for thereprocessing obligation when the rods are placedinto the reactor, and the cost of reprocessingadded to the cost of the fuel rods.

Revisions to decommissioning provisions

Decommissioning provisions are updated at each balance sheet date for changes in the estimatesof the amount or timing of future cash flows andchanges in the discount rate. Changes toprovisions that relate to the removal of an assetare added to or deducted from the carryingamount of the related asset in the current period.The adjustments to the asset are restricted,however. The asset cannot decrease below zeroand cannot increase above its recoverableamount:

• if the decrease of provision exceeds thecarrying amount of the asset, the excess is recognised immediately in profit or loss;

• adjustments that result in an addition to thecost of the asset are assessed to determine if the new carrying amount is fully recoverable or not. An impairment test is required if there is an indication that the asset may not be fully recoverable.

10 PricewaterhouseCoopers

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 12

The accretion of the discount on adecommissioning liability is recognised as part offinance expense in the income statement.

1.1.4 Impairment

The power industry is distinguished by the significant capital investment required, exposureto commodity prices and heavy regulation. The required investment in fixed assets leavesthe industry exposed to adverse economicconditions and therefore impairment charges.Utilities assets should be tested for impairmentwhenever indicators of impairment exist. Thenormal measurement rules for impairment apply.

Impairment indicators

External impairment triggers relevant for the utilities industry include falling retail prices, risingfuel costs, overcapacity and increased or adverseregulation or tax changes.

Impairment indicators can also be internal in nature. Evidence that an asset or CashGenerating Unit (CGU) has been damaged orbecome obsolete is an impairment indicator; forexample a power plant destroyed by fire is, inaccounting terms, an impaired asset. Otherindicators of impairment are a decision to sell orrestructure a CGU or evidence that businessperformance is less than expected. Performanceof an asset or group of assets that is below thatexpected by management in operational andfinancial plans is also an indicator of impairment.

Management should be alert to indicators on a CGU basis; for example learning of a fire at anindividual generating station would be anindicator of impairment for that station as aseparate CGU. However, generally managementis likely to identify impairment indicators on aregional, country or other asset grouping basis,reflective of how they manage their business.Once an impairment indicator has beenidentified, the impairment test must be performedat the individual CGU level, even if the indicatorwas identified at a regional level.

Cash generating units

A CGU is the smallest group of assets that generates cash inflows largely independent ofother assets or groups of assets.

Power generation assets will form CGUs by location or possibly by single generating facilityon a multiple turbine site. The determination ofhow many CGUs will depend on the extent ofshared infrastructure and the ability to generatelargely separate cash inflows. The determinationof CGUs is not driven by how managementchooses to use its assets. For example, an entitymay have three generating stations in a largemetropolitan area, which can be runindependently. Management makes the decisionto produce based on expected prices, demandand efficiency. It uses the three stations to meetdemand in a most efficient to least efficient basis.The three stations remain separate CGUs.

Calculation of recoverable amount

Impairments are recognised if the carrying amount of a CGU exceeds its recoverableamount. Recoverable amount is the higher of fairvalue less costs to sell (FVLCTS) and value in use(VIU).

Fair value less costs to sell (FVLCTS)

Fair value less costs to sell is the amount that a market participant would pay for the asset orCGU, less the costs of sale. The use ofdiscounted cash flows for FVLCTS is permittedwhere there is no readily available market pricefor the asset or where there are no recent markettransactions for the fair value to be determinedthrough a comparison between the asset beingtested for impairment and a recent markettransaction. However, where discounted cashflows are used, the inputs must be based onexternal, market-based data.

The projected cash flows for FVLCTS therefore include the assumptions that a potentialpurchaser would include in determining the priceof the asset. Thus industry expectations for thedevelopment of the asset may be taken intoaccount, which may not be permitted under VIU.However the assumptions and resulting valuemust be based on recent market data andtransactions.

Post-tax cash flows are used when calculating FVLCTS using a discounted cash flow model.The discount rate applied in FVLCTS will be apost-tax market rate based on a typical industryparticipant’s cost of capital.

11Financial reporting in the utilities industry1 U

tilities Value Chain &

Significant A

ccounting Issues

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 13

balance sheet at fair value as a derivative.Including the contracted prices of such acontract would double count the effects of thecontract. Impairment of financial instruments thatare within the scope of IAS 39 FinancialInstruments: Recognition and Measurement isaddressed by IAS 39 and not IAS 36.

The cash flow effects of hedging instruments such as caps and collars for commoditypurchases and sales are also excluded from the VIU cash flows. These contracts are alsoaccounted for in accordance with IAS 39.

1.1.5 Arrangements that may contain alease

IFRS requires that arrangements that convey the right to use an asset in return for a payment orseries of payments be accounted for as a leaseeven if the arrangement does not take the legalform of a lease. Some common examples ofsuch arrangements might include a series ofpower plants built to exclusively supply the railnetwork; a generator located on the site of analuminium smelter or a generator constructed ona build–own–operate–transfer arrangement with anational utility. Tolling arrangements may alsoconvey the use of the asset to the party thatsupplies the fuel.

IFRIC 4 Determining whether an Arrangement contains a Lease sets out guidelines to determinewhen an arrangement might contain a lease.Once a determination is reached that anarrangement contains a lease, the leasearrangement must be classified as either financeor operating. The principles in IAS 17 Leasesapply: a lease that conveys the majority of therisks and rewards of operation is a finance lease.A lease other than a finance lease is an operatinglease.

The classification has significant implications; a lessor in a finance lease would find itselfderecognising its generating assets andrecognising a finance lease receivable in return. A lessee in a finance lease would recognise fixedassets and a corresponding lease liability ratherthan an executory contract, as in the past.

Classification as an operating lease leaves the lessor with the fixed assets on the balance sheetand the lessee with an executory contract.

12 PricewaterhouseCoopers

Value in use (VIU)

VIU is the present value of the future cash flows expected to be derived from an asset or CGU inits current condition. Determination of VIU issubject to the explicit requirements of IAS 36Impairment of Assets. The cash flows are basedon the asset that the entity has now and mustexclude any plans to enhance the asset or itsoutput in the future but includes expenditurenecessary to maintain the current performance ofthe asset. The VIU cash flows for assets that areunder construction and not yet complete shouldinclude the cash flows necessary for theircompletion and the associated additional cashinflows or reduced cash outflows.

Any foreign currency cash flows are projected in the currency in which they will be earned anddiscounted at a rate appropriate for thatcurrency. The resulting value is translated to theentity’s functional currency using the spot rate atthe date of the impairment test.

The discount rate used for VIU is always pre-tax and applied to pre-tax cash flows. This is oftenthe most difficult element of the impairment test,as pre-tax rates are not available in the marketplace. Grossing up the post tax rate does notgive the correct answer unless no deferred tax isinvolved. Arriving at the correct pre-tax rate is acomplex mathematical exercise.

Contracted cash flows in VIU

The cash flows prepared for a VIU calculation should reflect management’s best estimate of thefuture cash flows expected to be generated fromthe assets concerned. Purchases and sales ofcommodities are included in the VIU calculationat the spot price at the date of the impairmenttest, or if appropriate, prices obtained from theforward price curve at the date of the impairmenttest.

There may be commodities – both fuel and the resultant electricity output – covered by purchaseand sales contracts. Management should use thecontracted price in its VIU calculation for anycommodities unless the contract is already onthe balance sheet at fair value. A commoditycontract that can be settled net in cash and forwhich the own use exception cannot be claimed,for example, is recognised separately on the

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 14

Operating lease classification might be achievedwhere the utility has other customers and most ofthe capacity production is sold to third parties.

Power purchase agreements

Power purchase agreements where the purchaser controls the dispatch of power, takesall of the output and has guaranteed a return tothe operator or provides a de facto guarantee ofthe obligation assumed to finance the facility arenot difficult to classify as a finance lease.Difficulties tend to arise where there is a powerpurchase agreement (PPA) for substantially all, orall, of the output of a wind farm or hydro facilitybecause the amount of generation is determinedby an uncontrollable factor, in this case the windor the amount of rain/snowfall.

For example, a typical wind farm contract would be:

• for 100% of the output of the wind farm;

• for substantially all of the asset’s life;

• guarantees a level of availability when the wind is blowing;

• allows the purchaser to agree the timing ofmaintenance outages;

• has pricing which is fixed per unit of output rather than a time-based payment.

Government requirements or incentives for the production of power from renewable sourceshave led to the development of many wind farms and other green generating sources. The developer and owner of the wind farmtypically agrees to sell 100% of the output of thewind farm to a single purchaser, allowing thedeveloper to recover its operating costs, debtservice cost and a development premium.Available wind studies are used to help site windfarms and assess the economic viability early inthe development stage of the project.

A PPA for 100% of the output of a wind farm with a guaranteed minimum production maymeet the requirement for finance leaseaccounting. The developer may establish thecontract so that it will get its full return from asingle contract, even though the generation ofelectricity is contingent on the wind.

Co-located assets

Power companies may construct generating facilities at customer locations on propertyowned or controlled by a customer. This mayoccur where a customer is a heavy user of powerand steam. These arrangements may also befound where the customer produces waste by-products that can be burned to produceelectricity.

These arrangements may have the substance of a finance lease under IAS 17 where the customerhas the majority of the risks and rewardsincidental to ownership of the asset. Some of the characteristics consistent with a financelease are where the customer takes most of theoutput and makes payments for the asset to‘stand ready’ in addition to payments for outputreceived. A common indicator of a finance leaseis that the customer provides a de factoguarantee of obligations assumed to finance thefacility. The guarantee may take the form of atake or pay contract or an outright guarantee ofindebtedness.

1.1.6 Emission Trading Scheme andCertified Emission Reductions

The ratification of the Kyoto Protocol by the EU required total emissions of greenhouse gaseswithin the EU member states to fall to 92% oftheir 1990 levels in the period between 2008 and2012. The introduction of the EU EmissionsTrading Scheme (EU ETS) on 1 January 2005represents a significant EU policy response to thechallenge. Under the scheme, EU member stateshave set limits on carbon dioxide emissions fromenergy intensive companies. The scheme workson a ‘cap’ and ‘trade’ basis, and each memberstate of the EU is required to set an emissionscap covering all installations covered by thescheme.

The EU cap and trade scheme is expected to serve as a model for other governments seekingto reduce emissions.

There are also several non-Kyoto carbon marketsin existence. These include the New South WalesGreenhouse Gas Abatement Scheme, theRegional Greenhouse Gas Initiative and WesternClimate Initiative in the United States and theChicago Climate Exchange in North America.

13Financial reporting in the utilities industry1 U

tilities Value Chain &

Significant A

ccounting Issues

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 15

Accounting for ETS

The emission rights permit an entity to emit pollutants up to a specified level. The emissionrights are either given or sold by the governmentto the emitter for a defined compliance period.

Schemes in which the emission rights are tradable allow an entity to:

• emit fewer pollutants than it has allowances for and sell the excess allowances;

• emit pollutants to the level that it holds allowances for; or

• emit pollutants above the level that it holds allowances for and either purchase additional allowances or pay a fine.

IFRIC 3 Emission Rights was published in December 2004 to provide guidance on how toaccount for cap and trade emission schemes.The interpretation proved controversial and waswithdrawn in June 2005 due to concerns over theconsequences of the required accountingbecause it introduced significant incomestatement volatility. The withdrawal of IFRIC 3means there is no specific comprehensiveaccounting for cap and trade schemes.

The guidance in IFRIC 3 remains valid but entities are free to apply variations provided that therequirements of all relevant IFRS standards aremet. Several approaches have emerged inpractice under IFRS. The scheme can result inthe recognition of assets (allowances), expenseof emissions, a liability (obligation to submitallowances) and potentially a government grant.

The allowances are intangible assets and are recognised at cost if separately acquired.Allowances that are received free of charge fromthe government are recognised either at fair valuewith a corresponding deferred income (liability),or at cost (nil) as allowed by IAS 20 Accountingfor Government Grants and Disclosure ofGovernment Assistance.

The allowances recognised are not amortised provided residual value is at least equal tocarrying value. The cost of allowances isrecognised in the income statement in line withthe profile of the emissions produced.

The government grant (if initial recognition at fair value under IAS 20 is chosen) is amortised to theincome statement on a straight line basis overthe compliance period. An alternative to thestraight line basis can be used if it is a betterreflection of the consumption of the economicbenefits of the government grant.

The entity may choose to apply the revaluation model in IAS 38 Intangible Assets for thesubsequent measurement of the emissionsallowances. The revaluation model requires thatthe carrying amount of the allowances is restatedto fair value at each balance sheet date, withchanges to fair value recognised directly in equityexcept for impairment, which is recognised in theincome statement. This is the accounting that isrequired by IFRIC 3 and is seldom used inpractice.

A provision is recognised for the obligation todeliver allowances or pay a fine to the extent thatpollutants have been emitted. The allowancesreduce the provision when they are used tosatisfy the entity’s obligations through delivery tothe government at the end of the scheme year.However, the carrying amount of the allowancescannot reduce the liability balance until theallowances are delivered.

Certified Emission Reductions (CERs)

There is another scheme under the Kyoto Protocol for fast-growing countries and countriesin transition that are not subject to a Kyoto targeton emissions reduction. Entities in thesecountries can generate Certified EmissionsReductions (CERs). CERs represent a unit ofgreenhouse gas reduction that has beengenerated and certified by the United Nationsunder the Clean Development Mechanism (CDM)provisions of the Kyoto Protocol. The CDMallows industrialised countries that are committedto reducing their greenhouse gas emissionsunder the Kyoto protocol to earn emissionsreductions credits towards Kyoto targets throughinvestment in ‘green’ projects. Examples ofprojects include reforestation schemes andinvestment in clean energy technologies. Oncereceived, the CERs have value because they areexchangeable for EU ETS allowances and hencecan be used to meet obligations under thatparticular scheme.

14 PricewaterhouseCoopers

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 16

An entity that acquires CERs accounts for these as described under ETS; they are accounted forat cost at initial recognition and then subsequentlyin accordance with the accounting policy chosenby the entity. There is no specific accountingguidance under IFRS that covers the generationof CERs. Entities that generate CERs shoulddevelop an appropriate accounting policy. Most entities that need CERs are likely to acquirethem from third parties and account for them asseparately acquired assets.

The key question that drives the accounting for self-generated CERs by ‘green’ entities is: whatis the nature of the CERs? The answer to thisquestion lies in the specific circumstances of thegreen entity’s core business and processes. If theCERs generated are held for sale in the entity’sordinary course of business, CERs are within thescope of IAS 2 Inventories. If they are not theyshould be considered as identifiable non-monetary assets without physical substance ie,intangible assets.

The accounting for CERs is also driven by the applicability of IAS 20. If CERs are granted bygovernment the accounting would be as follows:

• recognition when there is a reasonable assurance that the entity will comply with the conditions attached to the CERs and the grant will be received;

• initial measurement at nominal amount or fair value, depending on the policy choice;

• subsequent measurement depends on the classification of CERs and should follow the relevant standard ie, IAS 2 for inventory, IAS 38 for intangible assets, IFRS 5 for non-current assets held for sale.

1.2 Transmission & Distribution

1.2.1 Fixed assets & components

Some network companies applied renewals accounting for expenditure related to theirnetworks under national GAAP. Expenditure wasfully expensed and no depreciation was chargedagainst the network assets. This accountingtreatment is not acceptable under IFRS as thenormal fixed asset accounting and depreciationrequirements apply. This may be a significant

change for network companies and introducessome application challenges.

Network assets such as an electricity transmission system or a gas pipeline comprise manyseparate components. Many individualcomponents may not be significant. A practicalapproach to identifying components is toconsider the entity’s mid/long-term capitalbudget, which should identify significant capitalexpenditures and pinpoint major components ofthe network that will need replacement over thenext few years. The entity’s engineering staffshould also be involved in identification ofcomponents based on repairs and maintenanceschedules and planned major renovations orreplacements.

A network must be broken down into its significant parts that have different useful lives.The determination of the number of parts and thesplit is specific to the circumstances of the entity.A number of factors might be considered indoing the analysis; the cost of different parts,how the asset is split for operational purposes,physical location of the asset and technicaldesign considerations.

An entity that has a history of expensing all current expenditure may struggle initially toreinstate what should have been capitalised andwhat should have been expensed. Materiality is auseful guide; if replacement costs are material tothe asset then, provided recognition criteria aremet (cost can be reliably measured and futureeconomic benefits are probable), these costsshould be capitalised.

Network companies may be used to a working assumption that assets have an indefinite usefullife. All significant assets under IAS 16 Property,Plant and Equipment will have a finite life to bedetermined, being the time remaining before theasset needs to be replaced. Maintenance andrepair activities may extend this life, butultimately the asset will need to be replaced.

A residual value must be determined for all significant components. This value in many casesis likely to be scrap only or zero, since IAS 16defines it as the disposal proceeds if the assetwere already of an age and in the conditionexpected at the end of its useful life. An entity is

15Financial reporting in the utilities industry1 U

tilities Value Chain &

Significant A

ccounting Issues

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 17

required to allocate costs at initial recognition toits significant parts. Each part is then depreciatedseparately over its useful life. Separate parts thathave the same useful life and depreciationmethod can be grouped together to determinethe depreciation charge.

1.2.2 Customer contributions

The provision of utility services to customers requires some form of physical connection,whether the service is gas, water or power. The investment required to provide thatconnection to the customer from the national orregional network may be significant. This is likelywhen the customer is located far from thenetwork or when the volume of the utility that will be purchased requires substantial equipment.An example may be the provision of power to aremote location where the construction of asubstation is required to connect the user to thenational network.

Many utility entities require the customer to contribute to the cost of the connection, and inreturn the customer receives the right to accessthe utility services. The utility entity constructsthe connecting infrastructure and retainsresponsibility for maintaining it. Commonaccounting practice is for the utility entity tocapitalise the connection equipment as property,plant and equipment (PPE) and recognise thecontribution as deferred income, which isamortised to the income statement over anappropriate period – usually over the life of thePPE.

Major connection expenditures, such as substations or network spurs, will often benefitmore than one customer and contributions maybe received from several of these. However, whenmajor connection equipment is constructed forthe sole benefit of one customer and can bedistinguished from the general network,consideration should be given to whether theequipment has, in substance, been leased to thecustomer. IFRIC 4 and IAS 17 should be appliedto determine whether the arrangement is insubstance a lease and whether it should beclassified as an operating or finance lease.

A recent draft interpretation published by the IFRIC, D24 Customer Contributions, is broadlyconsistent with the approach described above,

although some detailed requirements may needto be considered when the interpretation isfinalised.

1.2.3 Regulatory assets & liabilities

Complete liberalisation of utilities is not practical because of the physical infrastructure requiredfor the transmission and distribution of thecommodity. Privatisation and the introduction ofcompetition is often balanced by price-regulation. Some utilities continue as monopolysuppliers with prices limited to a version of costplus margin overseen by the regulator.

The regulatory regime is often unique to each country. The two most common types ofregulation are incentive-based regulation andrate-based regulation. The regulator governing anincentive-based regulatory regime usually setsthe ‘allowable revenues’ for a period with theintention of encouraging cost efficiency from theutility. A utility entity operating under rate-basedregulation is usually permitted the recovery of anagreed level of operating costs, together with areturn on assets employed.

An entity’s accounting policies should take account of the regulatory regime and therequirements of IFRS. Any regulatory type assetor liability recognised under IFRS needs to be afinancial asset, an intangible asset or a financialliability in its own right, as there are no specialrecognition requirements for regulatory assets orliabilities under IFRS.

Future price increases

A common feature of price-regulated markets is the agreement of the regulator to allow future price increases in compensation for certainidentified past costs. These price increases areabove those that otherwise might have beenpermitted by the regulator in normal cost pluscalculations.

The costs associated with these price increases can be considered in two broad categories: thosethat are operating in nature and those that arecapital. Examples of operating costs mightinclude previously unbudgeted employee costs(for example, pension cost increases) andincreased fuel costs in volatile market conditions.These costs are expensed as incurred under

16 PricewaterhouseCoopers

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 18

IFRS and included in cost of sales in the periodin which the employee service is rendered or thefuel is consumed. These costs have beenincurred directly in generating the power sold inthat period.

Examples of capital costs include damage to fixed assets from extreme weather, such ashurricanes and ice storms, or from otherunexpected and uninsured events. An impairmentcharge is recognised under IFRS for anydamaged assets. The cost of replacement assetsare capitalised as appropriate as PPE.

The regulator may grant the utility permission to add an additional charge per unit to futurebillings to customers. This gives rise to a financialreceivable only as the power, water or gas isdelivered to the customer, not when the rateagreement is reached. The rate agreement doesnot give rise to the recognition of an intangibleasset as it does not change the nature of theexisting licence. Any ‘compensation’ receivablethrough an increased future price is notrecognised until that amount becomesreceivable, which is when the future electricity,water, or gas is delivered. A regulatoryadjustment, billable to identifiable existingcustomers with no further obligation to deliverservices, might meet the recognition criteria as afinancial asset. Few regulatory regimes allow thiskind of retroactive pricing adjustment.

Future price decreases

Price regulation can also lead to the requirement from a regulator for a utility entity to reduce itsprices in a future period. A decrease in pricesseldom leads to the recognition of a liability, as itdoes not constitute a refund of past amountscollected. The benefit of reduced prices is onlyreceived by customers if they continue topurchase the commodity. This is not sufficient tocause the recognition of a liability. It might beappropriate to recognise a liability if the entitywas obliged to repay cash to the customers (orperhaps to the government) or if the reduction inprices was so significant that it represented anonerous contract. An obligation to pay cash tocustomers or the government would berecognised as a financial liability. An onerouscontract would be recognised as a provision. It isextremely rare that the recognition of a liability

under IAS 39 or IAS 37 Provisions, ContingentLiabilities and Contingent Assets is met in thecontext of price regulation because the customermust purchase future services or commodity toreceive the benefits.

The IFRIC has considered the topic of regulatory assets and liabilities twice; once when dealingwith service concessions and a second time inresponse to a question about whether FAS 71could be applied under IAS 8 AccountingPolicies, Changes in Accounting Estimates andErrors. The IFRIC concluded on both occasionsthat the recognition criteria in FAS 71 were notfully consistent with IFRS and that any assets orliabilities recognised in relation to rate-regulatedutilities needed to meet the normal recognitioncriteria in the IFRS standards.

Regulatory assets and business combinations

The acquisition of a utility in a business combination requires the recognition of all of theutility’s identifiable assets and liabilities at theirfair values. A utility’s rights to charge a highertariff in the future or to reduce future pricesprovides additional information about the value of the licence. The tariff value will usually bereflected in the fair value of the licencerecognised on acquisition rather than therecognition of a separate regulatory asset.

Stranded costs

Stranded costs are a particular type of regulatory asset that are not associated with a utility’snormal day-to-day operations. They arise as aresult of a regulator requiring a utility to disposeof capital assets at a loss in order to achievegreater liberalisation of the utility. The lossincurred is known as a stranded cost, andtypically the regulator allows the utility entity tocharge a higher tariff to customers in the future inorder to compensate it for the loss incurred ondisposal of the capital assets. There may beunusual circumstances in which recognising suchstranded costs as an asset could be justified; forexample, if the entity had a substantial change tothe terms of its operating licence such that it hadexchanged its existing licence (an intangibleasset under IAS 38) for a new operating licence.

17Financial reporting in the utilities industry1 U

tilities Value Chain &

Significant A

ccounting Issues

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 19

1.3 Retail

1.3.1 Customer acquisition costs

Deregulation of markets and the introduction of competition often provides customers with theability to switch from one supplier to another.Utility entities invest in winning and developingtheir relationships with their customers. The costsof acquiring and developing these customerrelationships are capitalised if certain conditionsare met. The costs directly attributable toconcluding a contractual agreement with acustomer are capitalised and amortised over thelife of the contract. These costs includecommissions or bonuses paid to sign the utilitycustomers where the utility entity has thesystems to separately record and assess thecustomer contract for future economic benefits.

However, expenditure relating to the general development of the business, such as providingservice in a new location or an advertisingcampaign for new customers, represents thedevelopment of internally-generated goodwill andcannot be capitalised. Such general expenditureis not capitalised because the specific costsassociated with individual customers cannot beseparately identified or because the entity hasinsufficient control over the new relationship for itto meet the definition of an asset.

However, customer relationships must be recognised when they are acquired through abusiness combination. Customer-related intangiblessuch as customer lists, customer contracts andcustomer relationships are recognised by theacquirer at fair value at the acquisition date.

1.3.2 Customer discounts

Utility entities may offer discounts and other incentives to customers to encourage them tosign up to certain tariffs or payment plans. The costs associated with these programmesneed to be identified carefully to ensure that theyare appropriately separated from the salesrevenue. For example, when customers receive a lower tariff for paying monthly compared withother customers who pay quarterly, considerationshould be given to whether separation of thesales revenue from the finance income that isembedded in the price charged to the customerswho pay quarterly is required.

1.4 Company-wide Issues

1.4.1 Service concession arrangements

Public/private partnerships are one method whereby governments attract private sectorparticipation in the provision of infrastructureservices. These services might include, amongothers, toll roads, prisons, hospitals, publictransportation facilities and water and powerdistribution. These types of arrangements areoften described as concessions and many fallwith the scope of IFRIC 12 Service ConcessionArrangements. Arrangements within the scope ofthe standard are those where a private sectorentity may construct the infrastructure, maintain itand provide the service to the public. The entitywill be paid for its services in different ways.Many concessions require that the relatedinfrastructure assets are returned or transferredto the government at the end of the concession.

IFRIC 12 applies to arrangements where the grantor (the government or its agents) controls orregulates what services the operator provideswith the infrastructure, to whom it must providethem and at what price. The grantor also controlsany significant residual interest in theinfrastructure at the end of the term of thearrangement.

Water distribution facilities and energy supply networks are examples of infrastructure thatmight be the subject of service concessionarrangements. The government may haveauthorised the building of a new town. It maygrant a concession to a power distributioncompany to construct the distribution network,maintain it and operate it for a period of 25 years.The distribution network is transferred to thegovernment at the end of the concession periodwith a specified level of functionality for noconsideration. The national regulator sets priceson a cost-plus basis. The concession agreementhas base-line service commitments that willtrigger substantial penalties if service isinterrupted. The government requires that thepower company provide universal access toelectricity for all residents of the town andregulates the prices at which it is supplied.Customers can be disconnected for non-payment subject to hardship provisions for thepoor and elderly.

18 PricewaterhouseCoopers

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 20

This arrangement would fall with in the scope of IFRIC 12, as it has many of the common featuresof a service concession arrangement:

• The grantor of the service agreement is a public sector entity or a private sector entity to which the responsibility for the service is delegated (in this case the government has authorised the new town and granted the licence).

• The operator is not an agent acting on behalf of the grantor but responsible for at least some of the management of the infrastructure (the operator has an obligation to maintain the network and deliver electricity).

• The arrangement is governed by a contract (or by the local law, as applicable) that sets outperformance standards, mechanisms foradjusting prices and arrangements forarbitrating disputes (there are financialpenalties for poor operating performance anda cost-plus tariff).

• The operator is obliged to hand over the infrastructure to the grantor in a specified condition at the end of the period of the arrangement (transfer with no consideration from the government at the end of the concession period).

There are two accounting models under IFRIC 12 that an operator applies to recognise the rightsreceived under a service concessionarrangement:

• Financial asset – an operator with a contractual and unconditional right to receive specified or determinable amounts of cash (or other financial asset) from the grantor recognises a financial asset. The financial asset is within the scope of IAS 32 Financial Instruments: Presentation, IAS 39 and IFRS 7 Financial Instruments: Disclosures.

• Intangible asset – an operator with a right to charge the users of the public service recognises an intangible asset. There is no contractual right to receive cash when payments are contingent on usage. The licence is within the scope of IAS 38.

IFRIC 12 is a new interpretation, applicable for the first time in 2008. Arrangements betweengovernments and service providers are complex,and seldom will the conclusion be as obvious asthe example above. Once within the scope ofIFRIC 12, the appropriate accounting model may not always be obvious. Entities should beanalysing arrangements in detail to conclude onwhether these are within the scope of theinterpretation and whether the arrangement fallsunder the financial asset or intangible assetmodels. Some complex arrangements may have elements of both models for the differentphases. It may be appropriate to separatelyaccount for each element of the consideration.Applying IFRIC 12 for the first time will require aretrospective application, ie, comparatives will berestated for those concessions within its scope.

1.4.2 Business combinations

Acquisitions of assets and businesses are common in the utility industry. These may bebusiness combinations or acquisitions of groupsof assets. IFRS 3 Business Combinationsprovides guidance on both types of transactions,and the accounting can differ significantly.

All business combinations are accounted for by applying the purchase method. The purchasemethod is summarised as follows:

(a) identify the acquirer;

(b) measure the cost of the combination; and

(c) record the fair value of assets acquired and liabilities assumed.

Issues commonly encountered in the utility industry include making the judgement aboutwhether a transaction is a business combinationor an asset deal, recognition and valuation ofintangible assets, goodwill and deferred tax.

Definition of a business

A business is an integrated set of activities managed together to provide a return toinvestors or other economic benefits. Two keyelements of the definition are ‘integration’ and‘return to investors’. The accounting for abusiness combination and a group of assets canbe substantially different. A business combinationwill usually result in the recognition of goodwill

19Financial reporting in the utilities industry1 U

tilities Value Chain &

Significant A

ccounting Issues

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 21

and deferred tax. An asset transaction qualifiesfor the initial recognition exemption and thereforethere is usually no deferred tax. The considerationin an asset transaction is allocated to individualassets acquired and liabilities assumed based onrelative fair values.

Acquisition of an integrated utility or a group of generators located in a country will fall squarelyinto the scope of IFRS 3 as a businesscombination. The classification of the acquisitionof a single generating facility, or a portion of atransmission network, may not be so clear cut. The acquisition of a generating facility that iscontracted out and is within the scope of IFRIC 4and classified as a finance lease may not be abusiness combination because often theoperator’s return is fixed or guaranteed by thecontract, and any variability in costs is passedthrough to the purchaser of the power.

Allocation of the cost of the combination toassets and liabilities acquired

IFRS 3 requires all identifiable assets and liabilities (including contingent liabilities) acquiredto be recorded at their fair value. These includeassets and liabilities that may not have beenpreviously recorded by the entity acquired, forexample customer relationships.

IFRS 3 also requires recognition separately of intangible assets if they arise from contractual orlegal rights, or are separable from the business.The standard includes a list of items that arepresumed to satisfy the recognition criteria. The intangible assets that might be identified inthe acquisition of a utility may differ dependingon the regulatory regime. Brand names andcustomer relationships might be significantassets of a utility in a less regulated and morecompetitive market. A utility in a monopolymarket might have a brand name and a logo, butthis would have much less value as customershave no choice of supplier. The transmissionnetwork might be a separate business and tradewith a number of generators and distributioncompanies. If it has a monopoly position it hascustomer relationships, but these again are likelyto be of little value. Existing contracts andarrangements, however, might give rise to assetsor liabilities for favourable or unfavourablepricing. This could include operating leases, fuel

purchase arrangements and contracts thatqualify for own-use that might otherwise bederivatives under IAS 39.

The utility usually has a licence or a series of licences to operate. These licences are almostalways included in the value of the fixed assets,as the two can seldom be separated. The licenceto operate a nuclear power plant is specific tothe location, assets and often the current entity(not freely transferable). The licence and fixedassets are usually valued on the basis ofexpected cash flows and will incorporate anyexisting rate agreements that will survive thebusiness combination. The regulator, in somecountries, may seek to re-negotiate existing rateagreements perhaps as part of agreeing to achange in control.

Fair values of assets are often determined using discounted cash flow models. These modelsshould include the tax amortisation benefit (TAB)available to the typical market participant. The TAB represents the value associated with the tax deductibility for an asset. Asset valuesobtained through direct market observationsrather than the use of discounted cash flows(DCFs) already reflect the general tax benefitassociated with the asset. Differences betweenthe general tax benefit of each asset and thespecific tax benefits for the acquirer are includedwithin goodwill because these are entity-specific.

Goodwill

IFRS 3 requires that the fair value of the assets acquired and liabilities assumed are recognised.The difference between consideration and the fairvalue of net assets gives rise to positive ornegative goodwill. This residual approach to thecalculation of goodwill required by IFRS 3 is likelyto result in the recognition of goodwill in businesscombinations. Any goodwill is likely to representthe value paid for assets that do not qualify forseparate recognition on the balance sheet (suchas an assembled workforce), synergies paid forby the acquirer, ‘development premium’ reflectinguncertainty of the completion of the project and,occasionally, overpayments.

However, IFRS 3 requires certain assets and liabilities acquired in a business combination tobe recognised on a basis other than fair value.Examples include pension liabilities and deferred

20 PricewaterhouseCoopers

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 22

tax. Deferred tax is calculated after the fair valuesof the other identifiable assets and liabilities havebeen determined by comparing the fair valuerecognised for accounting purposes with the taxbase of each asset and liability. Consequently,the mechanics of the deferred tax calculation andthe goodwill calculation might result in goodwillbeing recognised solely as a result of therecognition of the deferred tax. That is, goodwillmight be recognised when there is no expectationof goodwill because there are no unrecognisedassets, no synergies and no overpayments. This anomaly will persist until the IASB revisesthe deferred tax standard, expected in 2009.

1.4.3 Financial instruments

The accounting for financial instruments can have a major impact on a utility entity’s financialstatements. Many use a range of derivatives tomanage the commodity, currency and interestrate risks to which they are operationallyexposed. Other, less obvious, sources of financialinstruments issues arise through both the scopeof IAS 39 and the rules around accounting forembedded derivatives. Many entities that areengaged in generation, transmission anddistribution of electricity may be party tocommercial contracts that are either wholly withinthe scope of IAS 39 or contain embeddedderivatives from pricing formulas or currency.Other entities may have active energy tradingprogrammes that go far beyond mitigation of risk.This section looks at two broad categories offinancial instruments: those that may arise fromthe scope of IAS 39 and those that arise fromactive trading and treasury management activity.Separately, it addresses accounting for weatherderivatives.

Scope of IAS 39

Contracts to buy or sell a non-financial item, such as a commodity, that can be settled net incash or another financial instrument, or byexchanging financial instruments, are within thescope of IAS 39. They are treated as derivativesand are marked to market through the incomestatement. Contracts that are for an entity’s‘own-use’ are exempt from the requirements ofIAS 39 but these ‘own-use’ contracts mayinclude embedded derivatives, which may berequired to be separately accounted for. An ‘own-

use’ contract is one that was entered into andcontinues to be held for the purpose of thereceipt or delivery of the non-financial item inaccordance with the entity’s expected purchase,sale or usage requirements. In other words, it willresult in physical delivery of the commodity. The ‘net settlement’ notion in IAS 39 is quitebroad. A contract to buy or sell a non-financialitem can be net settled in any of the followingways:

(a) the terms of the contract permit either party to settle it net in cash or another financial instrument;

(b) the entity has a practice of settling similar contracts net, whether:• with the counterparty; • by entering into offsetting contracts; or • by selling the contract before its exercise or

lapse;

(c) the entity has a practice, for similar items, of taking delivery of the underlying and selling it within a short period after delivery for the purpose of generating a profit from short-term fluctuations in price or a dealer’s margin; or

(d) the commodity that is the subject of the contract is readily convertible to cash.

Application of ‘own-use’

Own-use applies to those contracts that were entered into and continue to be held for thepurpose of the receipt or delivery of a non-financial item. The practice of settling similarcontracts net prevents an entire category ofcontracts from qualifying for the own-usetreatment (ie, all similar contracts must then berecognised as derivatives at fair value).

A contract that falls into category (b) or (c) above cannot qualify for own-use treatment. Thesecontracts must be accounted for as derivativesat fair value. Contracts subject to the criteriadescribed in (a) or (d) above are evaluated to seeif they qualify for own-use treatment.

Many contracts for commodities such as oil, gas and electricity meet criterion (d) above (ie, readilyconvertible to cash) when there is an activemarket for the commodity. An active marketexists when prices are publicly available on aregular basis and those prices represent regularly

21Financial reporting in the utilities industry1 U

tilities Value Chain &

Significant A

ccounting Issues

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 23

occurring arm’s length transactions betweenwilling buyers and willing sellers. Consequently,sale and purchase contracts for commodities inlocations where an active market exists must beaccounted for at fair value unless own-usetreatment can be evidenced. An entity’s policies,procedures and internal controls are thereforecritical in determining the appropriate treatmentof its commodity contracts.

Own-use is not an election. A contract that meets the own-use criteria cannot be selectivelyfair-valued unless it otherwise falls into the scopeof IAS 39.

If an own-use contract contains one or more embedded derivatives, an entity may designatethe entire hybrid contract as a financial asset orfinancial liability at fair value through profit or lossunless:

(a) the embedded derivative(s) does not significantly modify the cash flows of the contract; and

(b) it is clear with little or no analysis that separation of the embedded derivative is prohibited.

However, the IASB has proposed to restrict the ability to designate the entire hybrid instrumentas a financial asset or financial liability at fairvalue through profit or loss. The proposal to beincluded in the IASB’s 2008 Annual Improvementsproject will restrict this designation to hostcontracts that are financial instruments in thescope of IAS 39.

Further discussion on embedded derivatives is presented in the following section.

Measurement of long-term contracts that donot qualify for ‘own-use’

Long-term commodity contracts are not uncommon, particularly for purchase of fuel andsales of electricity. Some of these contracts maybe within the scope of IAS 39 if they contain netsettlement provisions and do not get own-usetreatment. These contracts are measured at fairvalue using the valuation guidance in IAS 39 withchanges recorded in the income statement.There may not be market prices for the entireperiod of the contract. For example, there maybe prices available for the next three years andthen some prices for specific dates further out.

This is described as having illiquid periods in thecontract. These contracts are valued usingvaluation techniques in the absence of an activemarket for the entire contract term.

Valuation is complex and is intended to establish what the transaction price would have been onthe measurement date in an arm’s lengthexchange motivated by normal businessconsiderations. Therefore it:

(a) incorporates all factors that market participants would consider in setting a price, making maximum use of market inputs and relying as little as possible on entity-specific inputs;

(b) is consistent with accepted economic methodologies for pricing financial instruments; and

(c) is tested for validity using prices from any observable current market transactions in the same instrument or based on any available observable market data.

The assumptions used to value long-term contracts are updated at each balance sheetdate to reflect changes in market prices, theavailability of additional market data and changes in management’s estimates of prices for any remaining illiquid periods of the contract.Clear disclosure of the policy and approach,including significant assumptions, are crucial toensure users understand the entity’s financialstatements.

Day-one profits

Commodity contracts that fall within the scope of IAS 39 and fail to qualify for own-use treatmenthave the potential to create day-one gains. Aday-one gain is the difference between the fairvalue of the contract at inception as calculatedby a valuation model and the amount paid toenter the contract. The contracts are initiallyrecognised under IAS 39 at fair value. Any suchprofits or losses can only be recognised if the fairvalue of the contract:

(1) is evidenced by other observable market transactions in the same instrument; or

(2) is based on valuation techniques whose variables include only data from observable markets.

22 PricewaterhouseCoopers

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 24

Thus, the profit must be supported by objective market-based evidence. Observable markettransactions must be in the same instrument (ie,without modification or repackaging and in thesame market where the contract was originated).Prices must be established for transactions withdifferent counterparties for the same commodityand for the same duration at the same deliverypoint.

Any day-one profit or loss that is not recognised at initial recognition is recognised subsequentlyonly to the extent that it arises from a change ina factor (including time) that market participantswould consider in setting a price. Commoditycontracts include a volume component, andutility entities are likely to recognise the deferredgain/loss and release it to profit or loss on asystematic basis as the volumes are delivered, oras observable market prices become availablefor the remaining delivery period.

The recognition of the day-one gain/losses may change as the result of the IASB project on theFair Value Measurements.

Take or pay contracts

Generators may enter into long-term take-or-pay contracts with key fuel suppliers. Theseagreements give rise to an obligation for thegenerator to purchase a minimum quantity orvalue of the relevant fuel. The actual quantity orvalue of fuel the generator requires may be lessthan the minimum agreed amount in any onemeasurement period. The generator may berequired to pay the supplier the equivalentmonetary value of the shortfall. The shortfallamount may also be carried forward and used insatisfaction of supply in subsequent periods.

A long-term take-or-pay contract might not qualifyfor own-use treatment. The inherent variability inamount and the ability to ‘net settle’ may putsuch a contract outside the exemption because itwill not meet the criteria for own-use.

Volume flexibility (optionality)

Many contracts for the supply of commodities usually give the buyer the right to take either aminimum quantity or any amount based on thebuyer’s requirements. A minimum annualcommitment does not create a derivative as longas the entity expects to purchase all the

guaranteed volume for its own-use. However, if itbecomes likely that the entity will not take thecommodity, and instead pay a penalty under thecontract based on the market value of thecommodity or some other variable, a derivativeor an embedded derivative may well arise. In thissituation, since physical delivery is no longerprobable, the derivative would be recorded at theamount of the penalty payable. Changes inmarket price will affect the penalty’s carryingvalue until the penalty is paid. On the other hand,if the amount of the penalty payable is fixed orpre-determined, there is no derivative becausethe penalty’s value remains fixed irrespective ofchanges in the product’s market value. In otherwords, the entity will need to provide for thepenalty payable once it becomes clear that non-performance is likely.

On the other hand, if the quantity specified in the contract is more than the entity’s normal usagerequirement and the entity intends to net settlepart of the contract that it does not need in thenormal course of the business, the contract willfail the own-use exemption. For example, theentity could take all the quantities specified in thecontract and sell on the excess, or it could enterinto an offsetting contract for the excess quantity.In such situations, the entire contract falls withinIAS 39’s scope and should be marked-to-market.

Embedded derivatives

Long-term commodity purchase and sale contracts frequently contain a pricing clause (ie,indexation) based on a commodity other than the commodity deliverable under the contract.Such contracts contain embedded derivativesthat may have to be separated and accounted forunder IAS 39 as a derivative. Examples are fuelprices that are linked to the electricity price orother products or a pricing formula that includesan inflation component.

An embedded derivative is a derivative instrument that is combined with a non-derivativehost contract (the ‘host’ contract) to form a singlehybrid instrument. An embedded derivativecauses some or all of the cash flows of the hostcontract to be modified, based on a specifiedvariable. An embedded derivative can arisethrough market practices or common contractingarrangements.

23Financial reporting in the utilities industry1 U

tilities Value Chain &

Significant A

ccounting Issues

08PwC0291 - IFRS Utilities final edit 10.04.2008 11:54 Uhr Seite 25

An embedded derivative is separated from the host contract and accounted for as a derivativeif:

(a) the economic characteristics and risks of the embedded derivative are not closely related to the economic characteristics and risks of the host contract;

(b) a separate instrument with the same terms as the embedded derivative would meet the definition of a derivative; and

(c) the hybrid (combined) instrument is not measured at fair value with changes in fair value recognised in the profit or loss (ie, a derivative that is embedded in a financial asset or financial liability at fair value through profit or loss is not separated).

Embedded derivatives that are not closely related must be separated from the host contract andaccounted for at fair value, with changes in fairvalue recognised in the income statement. It maynot be possible to measure the embeddedderivative. Therefore, the entire combinedcontract must be measured at fair value, withchanges in fair value recognised in the incomestatement.

An embedded derivative that is required to be separated may be designated as a hedginginstrument, in which case the hedge accountingrules are applied.

A contract that contains one or more embedded derivatives can be designated as acontract at fair value through profit or loss atinception, unless:

(a) the embedded derivative(s) does not significantly modify the cash flows of the contract; and

(b) it is clear with little or no analysis that separation of the embedded derivative(s) is prohibited.

Assessing whether embedded derivatives areclosely related

All embedded derivatives must be assessed to determine if they are ‘closely related’ to the hostcontract at the inception of the contract. Apricing formula that is indexed to somethingother than the commodity delivered under the

contract could introduce a new risk to thecontract. Some common embedded derivativesthat routinely fail the closely related test areindexation to an unrelated published market priceand denomination in a foreign currency that isnot the functional currency of either party and nota currency in which such contracts are routinelydenominated in transactions around the world.

The assessment of whether an embedded derivative is closely related is both qualitative andquantitative, and requires an understanding ofthe economic characteristics and risks of bothinstruments.

In the absence of an active market price for a particular commodity, management shouldconsider how other contracts for that particularcommodity are normally priced. It is common fora pricing formula to be developed as a proxy formarket prices. When it can be demonstrated thata commodity contract is priced by reference toan identifiable industry ‘norm’ and contracts areregularly priced in that market according to thatnorm, the pricing mechanism does not modifythe cash flows under the contract and is notconsidered an embedded derivative.

Timing of assessment of embedded derivatives

All contracts need to be assessed for embedded derivatives at the date when the entity firstbecomes a party to the contract. Subsequentreassessment of embedded derivatives isprohibited unless there is a significant change inthe terms of the contract, in which casereassessment is required. A significant change inthe terms of the contract has occurred when theexpected future cash flows associated with theembedded derivative, host contract, or hybridcontract have significantly changed relative to thepreviously expected cash flows under thecontract.