Implementing Financial Management Information System Projects

Upload

kofi-quansahCategory

view

430download

4

CBE Financial Management Training for Implementing Partners

Presented by: Benjamin Kofi Quansah (Grants & Finance Manager)

Purpose of Orientation

Provide guidance on the CBE fund management procedures.

The Fund Management Procedures aim to ensure that:

The CBE Programme achieves: its ultimate outcome,

DFID’s fiduciary requirements,

value for money and results.

TEAM=Together Everyone Achieves More

CBE Team

CBE Team ◦ Four levels of Programme Financial Management Support

(a) DFID

◦

◦ Provides the Funding

(b) Management and Support Team

◦ Provides oversight support

◦ Provides strategic guidance and advice to the Management Unit, and

◦ Manages resource requirements across the programme.

(c) Management Unit/MoE/GES

Manages the daily operations of the CBE

programme and administers the fund. The MU is to work with the MoE/GES and the

IPs to ensure that the CBE is fully institutionalized at the end of the 3 year period.

The unit comprises

Team Leader Senior Education Advisor Finance & Grants Manager M&E Manager M&E Officer Project Administrator.

(d) Implementing Partners ◦ Implements the CBE Programme to ensure the programme achieves its objectives.

Financial Management Procedures

To ensure: ◦ Efficient and effective financial management system.

◦ Timely execution and completion of the CBE programme

◦ Ensuring availability of adequate funds as per the approved programme plan.

(a) CBE Financial year

Follows the same timeframe as DFID’s financial year

Shall run from 1st April to 31st March.

Accordingly, the four quarters within each year shall be: ◦ 1. April – June

◦ 2. July – September

◦ 3. October – December

◦ 4. January – March

(b)Disbursement Request Forms

◦ All IPs shall request for funds by submitting Disbursement Request Forms(DRFs).

◦ (DRFs) shall form part of a summary quarterly financial report to be submitted according to the appropriate template, with guidance provided by the Finance & Grants Manager.

◦ The DRF is considered as an official invoicing document received from the IP so long as it is appropriately signed by a responsible officer of the IP.

(c)Financial Monitoring of IPs

A risk-based approach will underpin CBE financial monitoring, identifying those contracts (or contractors) where there may be greater scope for misuse or abuse, and focusing resources accordingly. Financial monitoring will include the following elements:

i. Budget vrs Actual Comparison

An individual set of records will be maintained for each IP and each separate grant they may have under the CBE programme.

As part of that data an Ms Excel Grant Tracker will be held for each project, holding records of:

◦ (a) All annual budgets,

◦ (b) Actual reported expenditures,

◦ (c) Claimed amounts,

◦ (d) payments made,

◦ (d) variations and deviations etc.

ii. Budget Virements

Virement between budget lines permitted up to 10% of the value of the respective budget line.

Virements greater than 10% require prior approval from Finance & Grants Manager in writing.

iii. Annual Audited Accounts IPs required to provide a copy of Annual Audited

Accounts. The key purpose of monitoring the IP annual account is to assess the financial health of the organisation and identify any compliance issues which might have been highlighted in the report by the auditors.

iv. Regular Surprise Financial Reviews

Finance & Grants Manager will, at least once in each half of a year, carry out surprise on-the-spot visits to IP offices.

v. Audited Annual Financial Accounts ◦ As a condition of funding, all IPs are required to

maintain books of accounts that can identify CBE programme funds and expenditures to facilitate reconciliation and provide an audit trail.

◦ All funded IPs are required to have their annual financial reports audited by an independent auditor contracted by Crown Agents and reporting to Crown Agents and the CBE MU. Audits will be scheduled twice a financial year; the first audit will be conducted after 6 months, in October, and the second audit will be conducted at final year, in April.

The audit should include:

An assessment of the adequacy of the accounting and internal controls system for financial reporting, safeguarding of assets and to monitor expenditures and financial transactions.

A determination of whether proper financial records have been kept for all relevant transactions.

An identification that the expenditures incurred are eligible for CBE financing and identify all ineligible expenses.

A determination of whether the cash and bank balance indicated as being on hand in the financial statements is represented by cash in the bank account.

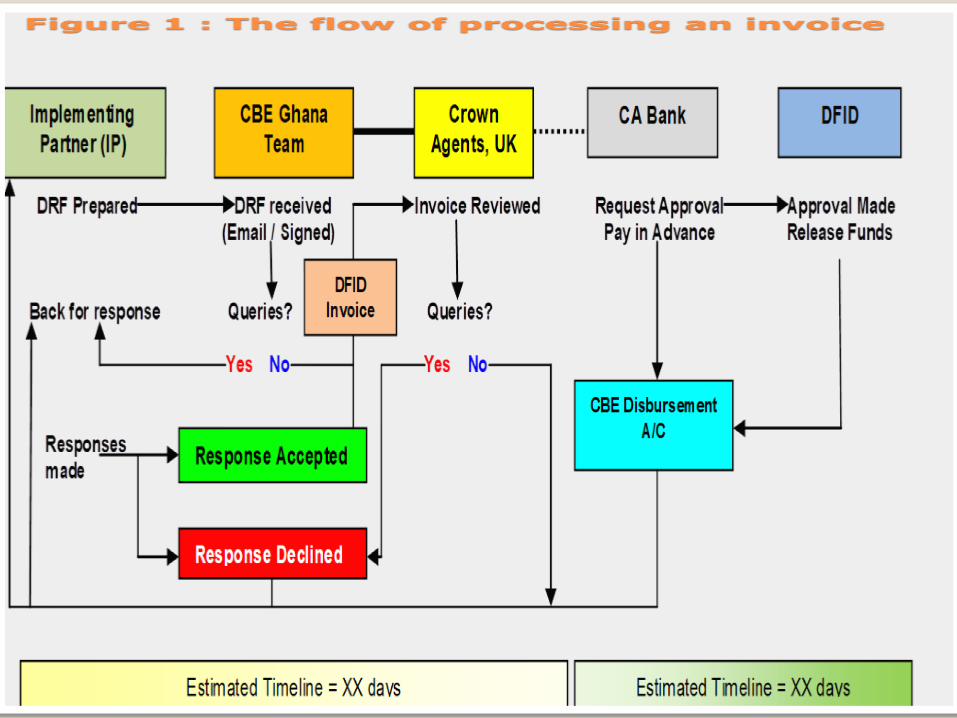

vi. Payment Procedures

Funds will be disbursed to IPs on quarterly basis in advance/arrears

Any funding disbursement will be made following the receipt of a Disbursement Request Form and each shall cover a quarter’s worth of financial needs.

Coverage of Disbursements:

All payments submitted by and made to IPs shall cover a specific quarter i.e. Apr-Jun, Jul-Sep, Oct-Dec, or Jan-Mar. It shall be made in no other format than on the Disbursement Request Form.

Frequency of DFID Invoicing: ◦ The MU will batch and process only one invoice to DFID each quarter.

◦ All IPs to submit their Disbursement Request Form to reach the Finance & Grants Manager no later than the 15th of the last month of each quarter. Requests received after 15th will NOT be processed until the next quarter. The DRF shall cover:

◦ Budget approved for the cycle

◦ Budget approved for the financial year

◦ Actual funds released by DFIF/Crown Agents

◦ Actual expenditure incurred( quarterly expenditure and cumulative)

◦ Forecast for the next quarter

Detailed review of invoices:

Once the invoice meets the initial administrative checks, it will be carefully reviewed by the Finance & Grants Manager.

The review of invoices will be done with input from the M&E team, who will provide evidence on what degree of completion the project has achieved. This will then be matched against expenditures being claimed. If queries are raised this will be promptly communicated to the IP until a satisfactory review is achieved.

Consolidated invoice record:

The Finance & Grants Manager prepares a DFID invoice spreadsheet listing all the DRFs received and that includes the following details: ◦ Name of IP;

◦ The CBE Reference No.;

◦ Contract value for the IP;

◦ Total Disbursements made to date to the IP;

◦ Total CBE Amounts reported as spent by the IP;

◦ Amount of funding being claimed during the specific

quarter; and

◦ The period covered by the current disbursement.

Financial Reporting Templates

Sample Budget Template

Sample Disbursement Request Form

Sample Financial Report- Quarterly and Annual

Variance Report