Financial Guarantees

38

FINANCIAL GUARANTEES TEAM MEMBERS : HARJEET SINGH SAKSHAM AGARWAL J. SUPRIYA IVNEET KAUR KARAN ARORA KANIKA AGARWAL

-

Upload

parulnigam -

Category

Documents

-

view

533 -

download

3

Transcript of Financial Guarantees

FINANCIAL GUARANTEES

TEAM MEMBERS:

HARJEET SINGHSAKSHAM AGARWALJ. SUPRIYAIVNEET KAURKARAN ARORAKANIKA AGARWAL

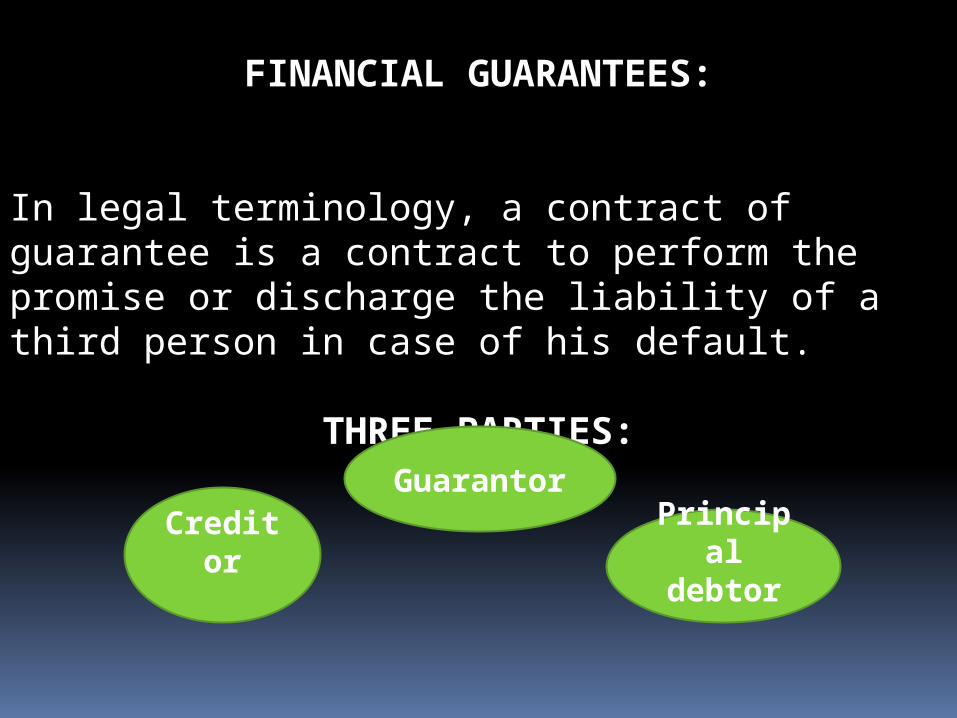

FINANCIAL GUARANTEES:

In legal terminology, a contract of guarantee is a contract to perform the promise or discharge the liability of a third person in case of his default.

THREE PARTIES:

Creditor Principal debtor

Guarantor

Guarantor

CreditorPrincipal

debtorDefaulter

Debtor

ADVANTAGES OF FINANCIAL GUARANTEES

Minimizes risk of lender

Help the debtor to secure a more attractive interest rate on the loan or other debt instrument

Improves Credit rating of the borrower

Offers financial protection to the exporter

Encourage the flow of credit to small borrowers

CLASSIFICATION OF FINANCIAL GUARANTEES:

CONTINUING

IMPLICIT

UNSECURED

PERFORMANCE

SECURED

EXPLICIT

FINANCIAL

SPECIFIC

SUPPLIERS OF GUARANTEES:

GOVERNMENT

FINANCIAL INSTITUTIONS LIKE BANKS,

INSURANCE Cos

PERSONAL

FINANCIAL INSTITUTIONS

LIKE IDBI,ICICI

SPECIALISED PUBLIC

GUARANTEE INSTITUTIONS: DICGC, ECGC

PERSONAL GUARANTEES

A personal guarantee is a pledge, by someone other than the named borrower, that he or she promises to pay any deficiencies on a specific loan.It is considered as the oldest form of guarantee service. It represents an unorganized and therefore, scattered and decentralized method of rendering the service.

Personal guarantees are more in use for consumption and social transactions and when the loan amount is small, in many cases they are in the oral rather than written form.

Personal guarantees play an important role in the agricultural sector where loans are given by cooperative institutions, agro-industries corporations on the basis of guarantees given by big land-owners .

Personal guarantees are mainly for short term credit and are estimated to account for 6% of total borrowings.

Personal guarantees are also used in organized sector but it has been seen that over a period of time the volume of these guarantees has been reducing.Earlier banks and lending institutions used to give loans on the basis of guarantees from managing agents, directors and managerial personnel. But this has declined due to change in the institutional set-up.

The two major reasons for the reduction in this practice have been: -

1. Abolition of the managing agency system led to the disappearance of reputed , prestigious and credit- worthy personal guarantors.

2. Rise of a new entrepreneurial class, professionalism of managerial cadres, and improvement in the technique of financial and technical appraisal of proposals for assistance, the need to obtain guarantees has declined.

GUARANTEES BY GOVERNMENT

Central and state government cooperative banks face problems like• Shortage of resources • High rate of default on loans

to deal with these challenges the banks rely on RBI and commercial banks by issuing them debentures or keeping deposits etc.But these commercial banks do these operations only on the basis of guarantees provided by the state and central government

The governments also provide guarantees on behalf of public sector enterprises to cover their borrowings they also provide counter guarantees in respect of bank guarantees extended on behalf of public corporations and other bodies.

GUARANTEES BY FINANCIAL INSTITUTIONS

The market for credit guarantees in India can be considered as well developed because commercial banks, insurance companies and statutory financial institutions at both state and central level provide guarantees.

The diversification of the credit guarantee markets has taken place in the last few decades.

While these institutions do provide guarantees it can be considered as a side business for most of them . Often the work of credit guarantee is related to their other business.

Guarantee business is done on a significant scale by commercial banks. The banks provide guarantees on behalf of their customers for the fulfillment of obligations undertaken by them.

Banks provide two types of guarantees:• performance guarantees.• financial guarantees.

Performance guarantees are those where the banks undertake to guarantee the performance of contracts entered into by their customers in respect of construction work, supply – purchase of goods etc . They also guarantee export performance in case of import of machinery, etc.

COMMERCIAL BANKS

Financial guarantees are of several types: -

a) Those in the nature of service facility.

b) Guarantees to cover import of goods or purchase of indigenous machinery.

c) Guarantees to cover loan payments.

d) Guarantees in lieu of inland letters of credit.

The maturity period of loans guaranteed by the banks is majorly short term. The guarantee commission charged by them is usually 1 percent p.a.. Generally banks provide these services to large well-established businesses.

The main agenda of banks in any case is to reduce their risk in the guarantee business. To do so the banks issue secure guarantees whenever possible.

These guarantees are secured by deposit of cash, lodgment of securities, or tangible assets, and a reduction in the drawing power of the debtor.

The banks also provide unsecured guarantees depending on the status of the customer, his standing with the bank, the purpose etc.

Insurance companies issue four types of guarantees:a) Related to performance of non-financial contracts.b) On behalf of hire-purchase companies.c) Guarantees to cover deferred payments.d) Guarantees to cover term loans from banks.

While guaranteeing loans from one company to other companies, or dealers, insurance companies do not follow the practice of issuing blanket guarantees.

The concerned company has to obtain a credit guarantee for each dealer or each debtor company, separately.

INSURANCE COMPANIES

The maturity period of guarantees ranges from 6 months to 1 year, however, it may be longer in case of deferred payment guarantees.

The guarantee commission charged by them is usually 1% p.a. and a significant part of their guarantee business covers medium and long term loans.

A significant portion of guarantees issued by insurance companies is given to banks or financial institutions like IDBI, ICICI, etc. who, in turn, give guarantees to creditors, suppliers or contract giving parties.

The availability of guarantee service in India has increased significantly since 1950 because of the creation of many new statutory financial institutions and their expansion.

These financial institutions extend guarantees for different purposes like: - IFC extends guarantees for loans raised by industrial concerns from scheduled banks or state co-operative banks. The ICICI guarantees loans from other private investment sources. The IDBI guarantees deferred payments due from industrial concerns, loans raised by them in the stock market or from scheduled banks.The NSIC guarantees loans from banks and similar institutions to small industrial units.

OTHER FINANCIAL INSTITUTIONS

SPECIALIZED PUBLIC GUARANTEE INSTITUTIONS

These institutions was set up by the Government during the past

three decades.

The Objective behind creating these institutions was to :

Provide direct credit to priority sectors

Provide them with specific clients and purposes

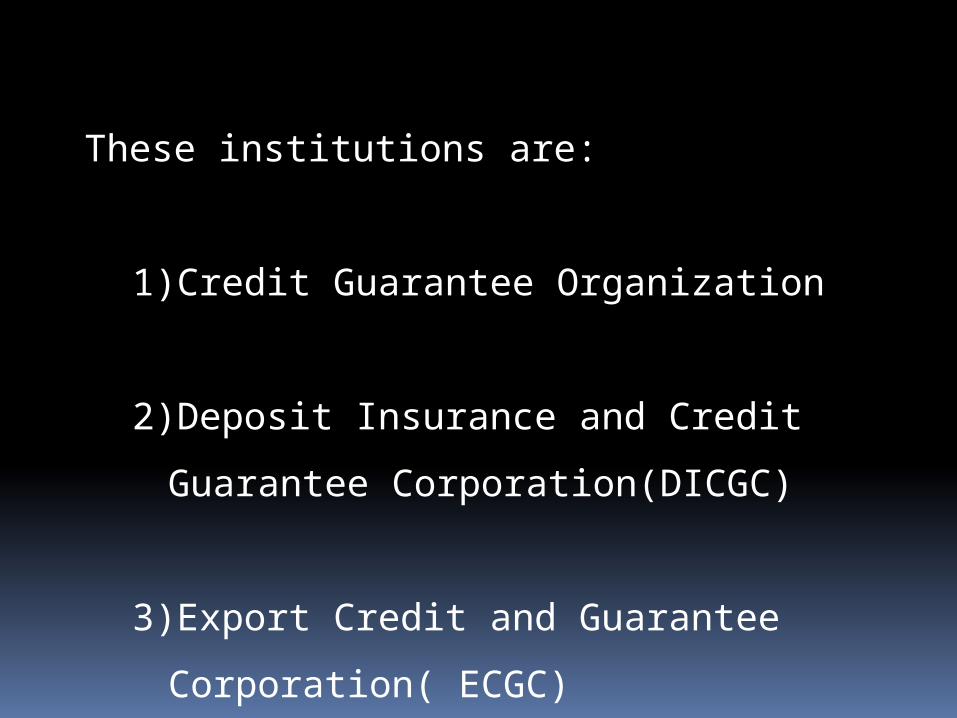

These institutions are:

1) Credit Guarantee Organization

2) Deposit Insurance and Credit Guarantee

Corporation(DICGC)

3) Export Credit and Guarantee

Corporation( ECGC)

CREDIT GUARANTEE ORGANIZATION

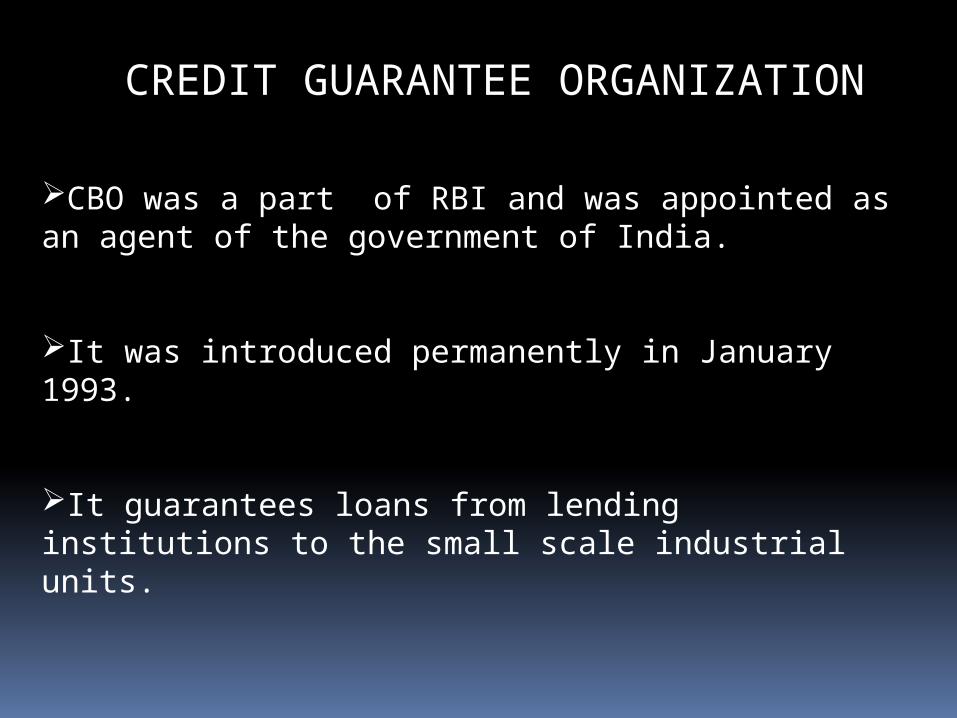

CBO was a part of RBI and was appointed as an agent of the government of India.

It was introduced permanently in January 1993.

It guarantees loans from lending institutions to the small scale industrial units.

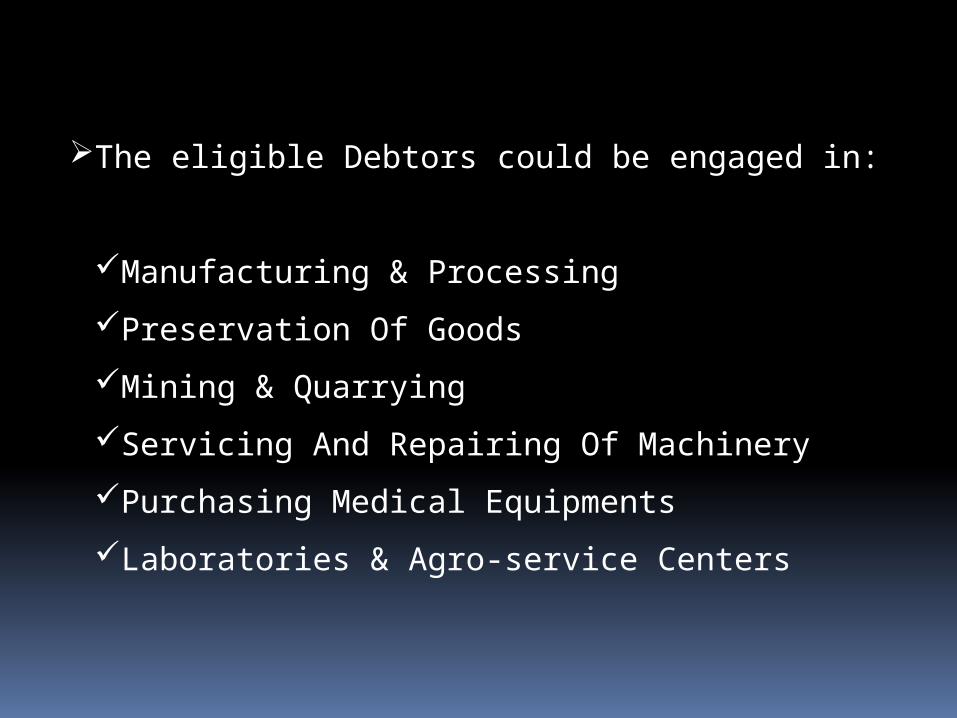

The eligible Debtors could be engaged in:

Manufacturing & Processing

Preservation Of Goods

Mining & Quarrying

Servicing And Repairing Of Machinery

Purchasing Medical Equipments

Laboratories & Agro-service Centers

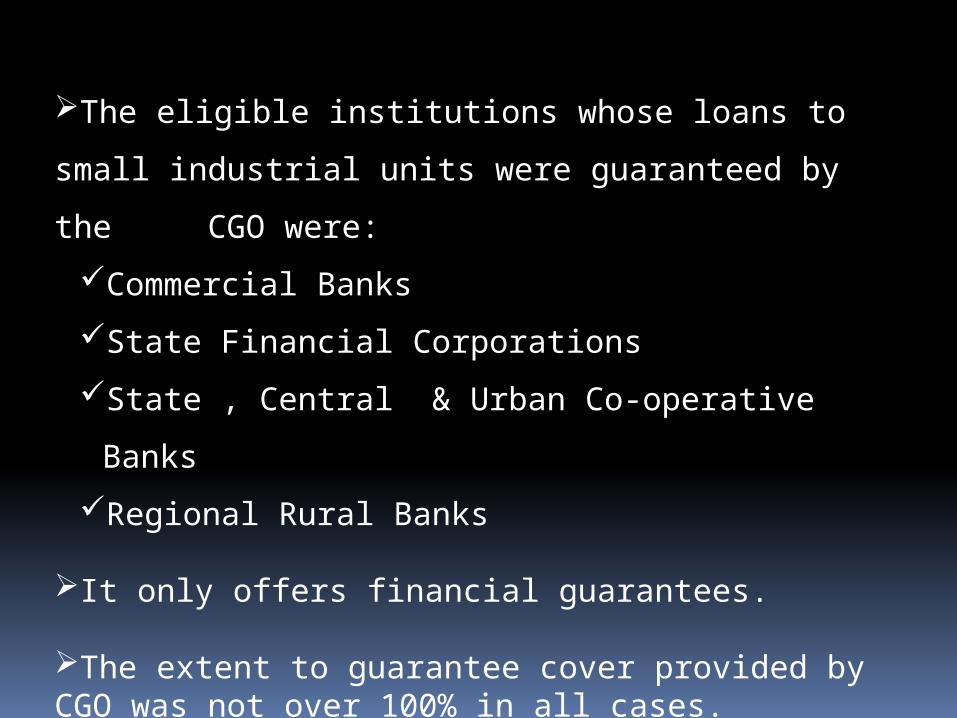

The eligible institutions whose loans to small industrial units

were guaranteed by the CGO were:

Commercial Banks

State Financial Corporations

State , Central & Urban Co-operative Banks

Regional Rural Banks

It only offers financial guarantees.

The extent to guarantee cover provided by CGO was not over 100% in all cases.

The CGO provides wide range of Credit facility.

The rate of guarantee commission charged by CGO is much lesser then commercial banks & insurance companies.

Deposit Insurance and Credit Guarantee Corporation (DICGC)

The DICGC came into existence in 1978 after the merger of Credit Guarantee Corporation(CGC) with the Deposit Insurance Corporation .

It guarantees loans to a wide spectrum of borrowers such as:Transport OperatorsRetail TradersProfessionalsSelf-employed PersonsBusiness enterprises

It cover diverse type of credit institutions. It includes commercial banks, central , state and primary level cooperative banks, RRBs ,SFCs and service cooperative societies.

The DICGC operates on the 5 credit guarantee schemes:

Small loans Guarantee scheme,1979

Small loans ( Financial Corporations) Guarantee

scheme,1971

Service Corporative socities Guarantee scheme,1971

Small loans (Co-operative banks) Guarantee scheme,1984

Small loans( Small scale industries) Guarantee

scheme,1981

Guarantee cover is usually 75% of the amount of default

The maturity of loan guaranteed varies between 5 months to 5

years

EXPORT CREDIT AND GUARANTEE CORPORATION( ECGC)

ECGC was set up in 1964 with the objective of offering financial protection to the exporter and improving the financial standing.

Different types of financial guarantees provided by ECGC are:Packing credit guaranteePost shipment export credit guaranteeExport finance guaranteeExport production finance guarantee

Non financial guarantees by ECGC are :Export performance guaranteeTransfer guaranteeInvestment insurance guarantee

LETTER

23 FEB, 2010:

RBI to shed 80% risk weight on govt-backed power loans

The Reserve Bank of India has decided to reduce the risk weight from 100% to 20%, when such loans are guaranteed by states.

Unlocking Rs 30,000 crore for the sector that is struggling to meet the capacity targets for the Eleventh Plan period.

20 AUG, 2010

Jet Airways seeks RBI nod to raise Rs 3,450 cr via ECB

Jet Airways is knocking on the doors of RBI to raise foreign currency loans to repay expensive rupee loans from local banks.Under current regulations, foreign currency loans, better known as external commercial borrowings (ECBs), cannot be used to refinance domestic loans.Jet has also proposed that the loans could be fully or partially guaranteed by the Indian banks and secured against credit card realisations outside India.

22 AUG, 2010

Fixed deposits to fetch higher returns

The deposits rates will go up as surging investments and monetary tightening have drawn out excess liquidity from the banking system. Over the past one year, fixed deposit interest rates had gone down from around nine percent to around five percent. As the economy started reviving, banks moved from being net lenders to net borrowers of funds from the Reserve Bank of India (RBI). This spells good news for individuals investing in term deposits.

Cont...

In case of banks' fixed deposits, the Deposit Insurance and Credit Guarantee Corporation of India guarantees repayment of Rs 1 lakh in case of default. There is no such guarantee offered on company deposits and the safety of your deposit depends on the financial position of the company.For non-banking financial services (NBFCs), the RBI has made it mandatory to have an 'A' rating to be eligible to accept public deposits.

Cont..

Investors should ideally go for 'AAA' or 'AA' rated schemes. Most companies accept fixed deposits for a period ranging from 1-5 years. Compared to mutual funds or bank fixed deposits, company fixed deposits are rather illiquid.In most cases, premature withdrawal is not allowed before completion of three months. If you wish to withdraw between the third and sixth months, you invariably get zero interest income. If you wish to withdraw between the sixth and the twelfth months, you get three percent less than the guaranteed returns.

26 MAR, 2010

Bharti takes SPV route for safe ride into Africa

Bharti Airtel, which taking over Zain Telecom’s African assets, has formed two special purpose vehicles (SPVs) in the Netherlands and Singapore to execute the $10.7-billion deal with a lower financial risk.Zain has also agreed to compensate Bharti for legal costs in case an ownership dispute erupts over the crucial Nigerian operations that contribute 36% to its Africa revenues. The guarantee from Zain, known as an indemnity, will be valid for some years.

Cont..

SPVs are companies formed to carry out a specific transaction. These SPVs, whose dealings will be guaranteed by Bharti, will own the African assets of Kuwait’s Zain.The SPV has to repay the debt from the cashflows of the African business. But Bharti will have to step in in case of a default.

11 Mar, 2010

Govt may let FIs guarantee infrastructure bondsThe government is weighing a proposal to allow financial institutions to guarantee bonds issued by infrastructure providers, a move which is expected to help channelise more funds for building roads, ports, airports and power projects.

State-owned insurance firms have been prominent in infrastructure investment and the government believes that measures such as offering a guarantee may provide comfort to private insurance companies and prompt them to put money in infrastructure bond offerings.The government-backed India Infrastructure Finance Company, or IIFCL, has appointed a consultant to vet this proposal.

5 Apr, 2010

Banks to seek RBI help to secure govt guarantee for education loans

CEOs of large commercial banks will seek the support of the Reserve Bank of India to secure a government guarantee for education loans.

Banks will request the central bank to take it up with the government to provide a guarantee, at least for loans below Rs 4 lakh,

NEWSPAPER POLISHES WHAT YOU READ IN BOOKS SO READ NEWSPAPER EVERYDAY.

THANK YOU