Financial Econometrics I Lecture 1...Financial econometrics typically models and analyzes return...

30

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns Financial Econometrics I Lecture 1 Fu Ouyang November 22, 2018

Transcript of Financial Econometrics I Lecture 1...Financial econometrics typically models and analyzes return...

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Financial Econometrics I

Lecture 1

Fu Ouyang

November 22, 2018

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Outline

Introduction to This Course

Asset Returns

Stylized Features of Financial Returns

Efficient Markets Hypothesis and Statistical Models for Returns

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Outline

Introduction to This Course

Asset Returns

Stylized Features of Financial Returns

Efficient Markets Hypothesis and Statistical Models for Returns

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

One Period Returns

The return for an asset (e.g., stock, bond, etc) is a percentage defined as thechange of the asset price as a fraction of its initial price. Returns exhibitmore attractive statistical properties than prices. Financial econometricstypically models and analyzes return data rather than price series.

There are various definitions for the asset returns: Let Pt denote the priceof an asset at time t.

• From time t− 1 to t, assuming no dividend paid, the one-period simplereturn is defined as

Rt = (Pt − Pt−1)/Pt−1

• The one-period gross return: Pt/Pt−1 = Rt + 1.

• The one-period log return: rt = log(Pt/Pt−1) = log(Rt + 1). Note thatwhen Rt is small, rt ≈ Rt, though theoretically rt ≤ Rt.

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Multiperiod ReturnsConsider multiperiod returns.

• the k-period simple return from time t− k to t can be similarly defined as

Rt (k) = (Pt − Pt−k)/Pt−k

• The k-period gross return: Pt/Pt−k = Rt(k) + 1.

• The k-period log return: rt(k) = log(Pt/Pt−k) = log(Rt(k) + 1).

• rt(k) is the sum of the k one-period log returns

rt (k) = log(Rt (k) + 1)

= log[(Rt + 1)(Rt−1 + 1) · · · (Rt−k+1 + 1)]

= log(Rt + 1) + log(Rt−1 + 1) + · · ·+ log(Rt−k+1 + 1)

= rt + rt−1 + · · ·+ rt−k+1

In this class, returns refer to log returns unless specified otherwise.

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Adjustment for Dividends

Let Dt denote the dividend payment between time t− 1 and t. Assumethat no dividends are re-invested in the asset.

Rt (k) =Pt +Dt + · · ·+Dt−k+1

Pt−k− 1

rt (k) =

k−1∑j=0

log

(Pt−j +Dt−j

Pt−j−1

)= rt + · · ·+ rt−k+1

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Continuously Compounded Returns and Bond Yields

rt is also called continuously compounded return: If a simple annual interestrate r for a bank deposit is fixed and earnings are equally paid m times peryear. Then the gross return at the end of one year is

(1 + r/m)m → er as m→∞

i.e., for continuously compounded interest, r = the annual log return.

Bonds are quoted in annualized yields. Consider a zero-coupon bond withthe face value 1, the current yield is rt and the remaining duration is D. Itscurrent price Bt satisfies Bt exp(Drt) = 1 and so the annualized log returnof holding the bond (ignoring that the remaining duration for Bt+1 isD − 1) is

log(Bt+1/Bt) = D(rt − rt+1)

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Excess Returns

In many applications, it is often convenient to use an excess return

rt − r∗t

where r∗t is a reference rate. Commonly used r∗t include

• Bank interest rates

• LIBOR

• Log return of riskless assets

• Market portfolio

The excess yield for a bond is called yield spread which is the differencebetween the yield of a bond and the yield of a reference bond.

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Outline

Introduction to This Course

Asset Returns

Stylized Features of Financial Returns

Efficient Markets Hypothesis and Statistical Models for Returns

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Behavior of Financial Return Data: Stationarity andVolatility Clustering

Stationarity• Asset prices are often not stationary over time (e.g., financial crisis,

economic growth/recession, technology improvement, etc).

• Most return sequences show certain level of stationarity (i.e., timeinvariant first two moments).

• The term stationarity will be formally defined in next lecture.

Volatility Clustering• The volatility of asset returns is time varying.

• Large price changes (i.e., absolute returns) often occur in clusters.

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Behavior of Financial Return Data: Stationarity andVolatility Clustering

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Behavior of Financial Return Data: Heavy tails

Heavy tails• The distribution of rt often exhibits “heavier-than-normal” tails.

• A random variable X has “heavier tails” than Z if for sufficiently largeM ∈ R+, P (|X| > M) > P (|Z| > M).

• Example: t-distribution (with degree of freedom ν) whose PDF is

fv(x) ∝ (1 + x2/ν)−(ν+1)/2

with tails of the order |x|−(ν+1)(� |x|−(ν+1)). N(0, 1) has tails of orderexp(−x2/2). It is not hard to see that limx→∞ exp(x2/2)/|x|ν+1 =∞.

• Tail behavior is closely related to the existence of E(|rt|p). ForX ∼ N(0, σ2), E(|X|p) <∞ for all p ∈ R+, but if X ∼ tν , E(|X|p) <∞only for p ∈ (0, ν). rt is typically assumed to have at least E(r2t ) <∞.

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Behavior of Financial Return Data: Asymmetry andAggregational Gaussianity

Asymmetry• The distribution of rt is often negatively skewed (long left tails).

• Risk aversion: the market tends to react more strongly to negativeshocks than positive ones.

Aggregational Gaussianity• Recall rt(k) = rt + rt−1 + · · ·+ rt−k+1.

• As k increases (long time horizon), the distribution of rt(k) tends to anormal distribution (think the central limit theorem).

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Behavior of Financial Return Data: Heavy tails,Asymmetry and Aggregational Gaussianity

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Behavior of Financial Return Data: Heavy tails,Asymmetry and Aggregational Gaussiananity

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Testing Normality Assumption

QQ plots check normality assumption by informal graphical inspection. Toformally test this hypothesis, one can perform

• Kolmogorov-Smirnov test, or

• Jarque-Bera test (H0: x1, ..., xn are IID from a normal distribution),

JB =n

6[S2 + (K − 3)2/4]

d→ χ22

where S and K are sample skewness and kurtosis, respectively, i.e.,

S =

(n∑i=1

(xi − x̄)3/n

)/

(n∑i=1

(xi − x̄)2/n

)3/2

K =

(n∑i=1

(xi − x̄)4/n

)/

(n∑i=1

(xi − x̄)2/n

)2

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Behavior of Financial Return Data: Long RangeDependence

Long Range Dependence• The returns are almost serially uncorrelated, but not independent!

• Use the sample autocorrelation function (ACF) ρ̂k to measure the serialcorrelation of a return series {rt}Tt=1. Define ρ̂k = γ̂k/γ̂0 where

γ̂k =1

T

T−k∑t=1

(rt − r̄)(rt+k − r̄)

is the sample autocovariance at lag k and r̄ =∑Tt=1 rt/T .

• {r2t }Tt=1 and {|rt|}Tt=1 (long memory) exhibit significant (95% confidenceinterval for H0 : ρk = 0) ACF⇒ nonlinear dependencies over time.

• ρk’s become weaker and less persistent for longer sampling intervals.

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Behavior of Financial Return Data: Long RangeDependence

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Behavior of Financial Return Data: Leverage Effect

Leverage Effect• Assets returns are often negatively correlated with the changes of their

volatilities.

• Prices down⇒ firms more leveraged (riskier)⇒more volatile prices.

• Volatility up⇒ investors demand risk premiums⇒ prices down.

• Risk aversion: volatilities caused by price decline are typically largerthan the appreciations due to declined volatilities.

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Behavior of Financial Return Data: Leverage Effect

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Outline

Introduction to This Course

Asset Returns

Stylized Features of Financial Returns

Efficient Markets Hypothesis and Statistical Models for Returns

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Efficient Market Hypothesis (EMH)

Strong EMH: Security prices Pt of traded assets reflect instantly allavailable information up to time t, public or private. Individuals do nothave comparative advantages in the acquisition of information, and sothere is no arbitrage opportunities.

Semi-strong EMH: Security prices merely reflect efficiently all past publicinformation, leaving rooms for the value of private information.

Under the EMH, an asset return process may be expressed as

rt = µt + εt, E(εt) = 0, V ar(εt) = σ2t

• E(εt) = 0⇒ µt = E(rt), µt is the rational expectation of rt at time t− 1.

• εt is called an innovation representing the return due to unpredictable“news” that arrives between time t− 1 and t.

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Efficient Market Hypothesis

Combining the EMH and the stationarity feature discussed in last lecture,it makes sense to assume

µt = µ

For {εt}, there are three different types of assumptions:

1. White Noise (WN) Innovations{εt} are white noise, denoted as εt ∼WN(0, σ2). Under WN assumption,for all t 6= s,

Cov(εt, εs) = 0

2. Martingale Difference (MD) InnovationsFor any t,

E(εt|rt−1, rt−2, ...) = E(εt|εt−1, εt−2, ...) = 0

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Efficient Market Hypothesis

3. IID Innovations{εt} are independent and identically distributed (IID), denoted asεt ∼ IID(0, σ2).

IID⇒MD: E(εt|εt−1, εt−2, ...) = E(εt) = 0

MD⇒WN: For any t > s, by the law of iterated expectations (LIE),

Cov(εt, εs) = E(εtεs)

= E[E(εtεs|εt−1, εt−2, ...)]= E[εsE(εt|εt−1, εt−2, ...)]= 0

To sum up, IID⇒MD⇒WN.

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Revisiting S&P 500

Figure 1: Time Series of Pt and rt

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Revisiting S&P 500

Figure 2: ACF of rt and r2t

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

IID Innovations and Random Walk

Recall rt = log(Pt/Pt−1). Under IID assumption, {logPt} form a randomwalk, i.e.,

logPt = µ+ logPt−1 + εt

• {Pt} form a geometric random walk.

• If εtiid∼ N(0, σ2), {Pt} form a log normal geometric random walk.

• As ∆t→ 0, logPt Brownian motion (Pt geometric Brownianmotion).

IID assumption is too strong to be true for modeling {rt} as it impliesCov[f(rt), f(rs)] = 0 for any function f (see Figure 2).

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

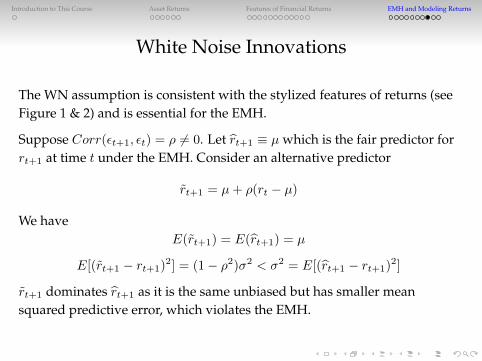

White Noise Innovations

The WN assumption is consistent with the stylized features of returns (seeFigure 1 & 2) and is essential for the EMH.

Suppose Corr(εt+1, εt) = ρ 6= 0. Let r̂t+1 ≡ µ which is the fair predictor forrt+1 at time t under the EMH. Consider an alternative predictor

r̃t+1 = µ+ ρ(rt − µ)

We haveE(r̃t+1) = E(r̂t+1) = µ

E[(r̃t+1 − rt+1)2] = (1− ρ2)σ2 < σ2 = E[(r̂t+1 − rt+1)2]

r̃t+1 dominates r̂t+1 as it is the same unbiased but has smaller meansquared predictive error, which violates the EMH.

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Testing White Noise Hypothesis

In many applications, white nose assumption is appropriate, i.e., {rt} areuncorrelated (linearly independent) but may depend on each other in somenonlinear manners. To formally test H0: {rt} is a white noise, one can usethe Ljung-Box test

Qm = T (T + 2)

m∑k=1

1

T − kρ̂2k

d→ χ2m

or the related Box-Pierce test

Q∗m = T

m∑k=1

ρ̂2kd→ χ2

m

where m is a prescribed integer. In practice, we often perform the test withdifferent values of m. We reject H0 at the significance level α if Qm > χ2

α,m

(Q∗m > χ2α,m) or 1− Fχ2

2(Qm) < α (1− Fχ2

2(Q∗m) < α).

Introduction to This Course Asset Returns Features of Financial Returns EMH and Modeling Returns

Martingale Difference Innovations

The MD assumption is consistent with the EMH. It is not hard to show that

E(rt+1|rt, rt−1, ...) = arg infg∈G

E[(rt+1 − g(rt, rt−1, ...))2]

and under the MD assumption

E(rt+1|rt, rt−1, ...) = µ+ E(εt+1|rt, rt−1, ...) = µ

i.e., given rt, rt−1, ..., the best point predictor for rt+1 is µ.

The MD assumption is the most appropriate mathematical form of theEMH as it is assures that asset returns cannot be predicted by any rules, butallows certain nonlinear dependence.