Financial (and Commodity)...

139

1 Financial (and Commodity) Derivatives RNDr. Jiří Witzany, Ph.D. ([email protected], NB 178, Tuesday 10-12)

Transcript of Financial (and Commodity)...

1

Financial (and Commodity) Derivatives

RNDr. Jiří

Witzany, Ph.D.([email protected], NB 178, Tuesday 10-12)

2

Literature

Requirement ISBN Title Author Year of Publication

Required1 0-13-149908-4

Options, Futures, and Other Derivatives, 789 p.

Hull, John C. 2006, 6th edition

Optional 978-80-245-1274-7

International Financial Markets, Oeconomia VŠE, 180 p.

Witzany, J. 2007

Optional 80-245-1033-2

Deriváty, 297 s. Dvořák, Petr 2006

Optional 80-247-1099-4

Finanční a komoditní deriváty v praxi, 630 s.

Jílek, Josef 2005

Optional 0-471-96717-3

Financial derivatives in theory and practice, 393 p.

P.J.Hunt, J.E. Kenedy

2000

1) The course should cover Chapters 1-15 from John Hull

3

Content

•

Introduction –

principles of financial derivatives

•

Future and forward markets•

Determination of forward and futures prices

•

Interest rate and currency swaps•

Mechanics of options markets

4

Content - continued

•

Modeling of market rates and valuation of options

•

Options on stock indices, currencies, and futures (Greek letters, Delta-hedging etc., volatility smiles etc.)

•

(Credit risk and credit derivatives, exotic, weather, energy, and insurance derivatives if time allows)

5

Part 1 Introduction to Derivatives

Futures Markets

6

Introduction Principles of Derivatives

•

A derivative contract can be defined as a financial instrument whose value depends (is derived from) the values of other, more basic underlying variables (financial assets -

FX rates, interest rates,

stock prices, bond prices, commodities, weather,..)•

Derivatives are settled at a certain future time

•

Derivative markets –

trading with pure risk – physical settlement of underlying assets often

eliminated•

Derivative markets are

often

more liquid than the

spot markets (e.g. commodity futures) –

spot prices „derived“ from derivative prices

7

Interest Rate Derivatives Market Development

•

Derivative markets have become increasingly important during the last 25 years

8

Credit Derivatives Market Development

•

Some derivative markets grow exponentially

9

Exchange-Traded Markets versus OTC Markets

•

Standardized

derivative

contracts

defined by the

exchange

•

The

contracts

are always

between

the exchange

and

a participant

•

OTC derivatives

generally

between

any

two subjects

•

Derivative

Exchanges

exist

since

19th century

(Chicago Board

of

Trade

–

futures

like

contracts,…)

10

OTC versus Exchange Market Development

Source: John Hull, Options, Futures, and

Other

Derivatives, 6th edition

11

Global Capital Markets

12

Market Value

Versus Outstanding Amount

Source: BIS

13www.bis.org

14www.bis.org

Futures

15

Basic Derivative Types – Forward Contracts•

Forward contract –

an agreement to buy or

sell an asset at a certain future time for a certain price

Source: John Hull, Options, Futures, and

Other

Derivatives, 6th edition

Payoff=K-STPayoff=ST

-K

16

Forward contracts •

Arbitrage-less market … any possible arbitrage opportunity quickly disappears in an efficient market

•

FX forward transaction can be equivalently achieved as a combination of a reverse FX spot and two deposits

–

relatively straightforward

pricing•

Generally for FX direct quotations FC/DC:

360)(1

3601

360)(

1

3601

3601 drrdr

drr

dr

dr

spotFXforwardFX

FCDC

FC

FCDC

FC

DC

17

Domestic

Currency

Foreign

Currency

T+2 T+2+d

2. Buy

FC at

S

1. Borrow

at

rDC

3. Deposit at

rFC

4. Sell

FC at

F

FX Forward Arbitrage Argument

5. Repay

the

loan

18

FX Forward pricing

•

Example: Assume that the spot rate EUR/PLN equals to 3,76. Estimate the 6 M (months) forward exchange rate if the 6 M interest rates in EUR and PLN are 4,35% and 4,85%.

•

Solution:

769,31,02191,0244*76,3

3601810,04351

3601810,04851

*76,3

360dr1

360dr1

SFEUR

PLN

19

Other Basic Derivative Types

•

Futures contracts –

similar to forwards but traded on an exchange (Chicago Board of Trade,…), standardized, margins to cover daily P/L

•

Options –

right to buy/sell certain asset (stocks, currencies,…) by (at) a certain date for a certain price –

call/put options, strike/exercise price,

expiration/maturity, European/American options, traded OTC (FX,..) or on an exchange (Chicago Board Options Exchange,…), binary, barrier,…

20

Options • Example: profit/loss

on call/put options

Source: John Hull, Options, Futures, and

Other

Derivatives, 6th edition

21

Other Derivative types•

Swaps: two parties agree to a periodic exchange of certain cash flows –

interest rates, equity returns,

nominals

in different currencies etc., always OTC•

FRA –

Forward Rate Agreements –

payoff is

defined as the difference between agreed and future interest rates

-

OTC

•

Credit derivatives: the payoff on the creditwothiness

of one or more companies or

countries –

credit default swaps, CDO,…

-

OTC•

Other underlyings: weather derivatives (daily temperature), energy derivatives -

crude oil,

natural gas, electricity, …

22

Types of Traders

•

Hedgers –

fundamental need to reduce

(insure) risks

•

Speculators –

use derivatives as an easy way to take a position/speculate on the market –

for

example the „hedge funds“•

Arbitrageurs –

combine different products in

different markets to lock in a risk-less profit –

see e.g. the relationship between spot and forward prices –

only small arbitrage opportunities exist

23

Speculation example•

$2000 to speculate with: The Amazon.com stock $20, 2-month call option with strike $22,50 is sold for $1

Source: John Hull, Options, Futures, and

Other

Derivatives, 6th edition

24

Derivatives Risk Management•

Derivatives can be used to take huge risk with minimal initial investment

•

Future derivatives settlement may allow to hide transactions for some time

•

Nick Leeson

–

Barrings

Bank –

Singapore office –

1 billion dollar loss

•

Jerome Kerviel

–

Societte

General –

Equity Index Derivatives –

5 bln

EUR loss

•

UBS, Merill

Lynch, Morgan Stanley, AIG… –

CDOs

– 100s bln

USD losses

•

Derivatives can be compared to electricity –

very useful but dangerous

Need for high quality risk management –

risk limits on exposures, products, counterparties etc.

25

Futures Markets

26

Futures Markets•

Financially

similar

to forwards

but

exchange

traded

•

Futures exchange/clearinghouse stands between the market participants

(compare to forwards)

•

Majority of future contracts do not lead to physical delivery

Futures Exchange

Counterparties

witha long

position

Counterparties

witha short

position

+N -N

27

Newspaper quotes

28

Specification of a Futures Contract

•

The asset: commodities must be exactly specified•

The contract size: depend on average user and delivery costs

•

Delivery arrangements: cash or physical, important for commodities (cattle, lumber, cotton…). The party with short position usually files a notice of intention to deliver –

selection of

location etc.•

Delivery time: usually end of month, or a longer delivery period

•

Price quotes conventions: e.g. $/barrel with two decimal places; price and position limits

29

Daily Settlement and Margins•

Settlement/counterparty risk: counterparty does not deliver

•

Margin mechanism –

daily financial settlement •

Initial Margin –

set so that daily losses are covered with

high probability (e.g.99,5%)•

Daily P/L (variation in futures price) is debited/credited on the margin account

•

Maintenance

margin (around 75% of the initial margin) must be always maintained

•

If the balance falls bellow the maintenance margin there is a margin call, the account must be topped to the initial margin level

•

The account balance is release when the position is closed out or settled

30

Daily Settlement and Margins•

Example: +2 (100 ounces) gold futures

contracts,

price

in $ per troy oz.

(Initial

Margin

$2000, Maintenance Margin $1500 per contract)

Source: John Hull, Options, Futures, and

Other

Derivatives, 6th edition

31

Forwards versus Futures

Source: John Hull, Options, Futures, and

Other

Derivatives, 6th edition

32

Hedging Using Futures

•

If future P/L depends linearly on the future price of an asset then futures contracts can be used for a perfect hedge

•

P/L = N x P, P future price of a unit of the asset, N positive or negative / the sensitivity

•

Take futures position equivalent to -N units of the asset (short for N positive, long otherwise)

•

Then

P/L = N x P -

N x P = 0 for the total position after the futures contract settlement

•

There are arguments for and against hedging

33

Hedging Using Futures

•

Example: A farmer plans to sell his cattle on a local market one year from now, let us say in August 2008. The market prices of live cattle are quite volatile so the farmer decides to use ten live cattle futures contracts to fix his selling price. The table on the next slide shows quoted live cattle futures (trade unit is 40 000 pounds and the price is in cents per pound). Propose an effective hedging strategy for the farmer.

35

Basis Risk•

Basis = spot price of the asset –

futures price of

the contract = S –

F = b … due

to: time, not exactly identical assets

• The

effective

hedging

price

= F1

+b2

= F1

+(S2

-F2

)

Source: John Hull, Options, Futures, and

Other

Derivatives, 6th edition

36

Cross Hedging

•

The hedged asset and the futures asset are not same, but the prices are correlated

•

For example hedging the price of jet fuel using heating oil futures, or hedging FX P/L from on equity investment using FX futures

•

Find the OLS regression coefficient: S= h* F + , i.e. h=

* S

/ F•

The hedge ratio h minimizes

the variance of P/L

caused by S

37

Cross Hedging Example

h = 0,78… using

elementary

statistics

formulas

Source: John Hull, Options, Futures, and

Other

Derivatives, 6th edition

38

Stock Index Futures• Cash settlement based

on actual

index value

39

S&P 500 Futures on CME

40

Hedging an Equity Portfolio Example

•

Value of S&P 500 index = 1000•

Value of the hedged portfolio = $5

mil.

•

Risk-free interest rate = 10% p.a.•

Index dividend yield = 4% p.a.

•

Beta of the hedged portfolio = 1,5•

Use 4-month S&P 500 futures (currently valued at 1020,20) to hedge the value of the portfolio.

•

Simulate the outcome using CAPM given different values of the index in 3 month (800, 900, 1100

etc.).

41

Hedging an Equity Portfolio Example

Source: John Hull, Options, Futures, and

Other

Derivatives, 5th edition

42

Hedging an Equity Portfolio•

Index futures can be used in case the portfolio manager assumes a temporary decline of the market,

•

or wants to speculate against the benchmark (index),

•

or wants to adjust the beta of the portfolio, •

or wants to take a temporary position without investing into the stocks etc.

•

Index futures can be also used to hedge a single stock against the market volatility

43

Rolling the Hedge Forward•

Example of April 2004 –

June 2005 hedge using three

6 month futures rolled forward (short positions)

Source: John Hull, Options, Futures, and

Other

Derivatives, 6th edition

44

Rolling the FX Hedge Forward

•

Example: You run a CZK denominated money market fund for US investors. Show how to use 6 months forwards for a continuous FX hedging of the portfolio. The initial value of the portfolio is 1.7 bln

CZK, and the expected growth is 4%

annually. Give an example if the exchange rate development is

e.g.

17.00, 17.50, 18.00, 18.70,

18.50 CZK/USD in 6 months periods.

45

Part 2 Forward

and

Futures Pricing

Interest

rates

46

Interest Rates

•

Present

value

–

cashflow discounting

–

key concept

in derivatives

valuation

•

Risk free rate

x credit

margin•

Treasury rates

and

LIBOR rates

•

Different

interest

rate

conventions•

Different

compounding

frequency

•

Continuous

compounding

FV=AeRt

•

Bond pricing

and

zero

rates

-

bootstrapping

47

Bootstrapping

Source: John Hull, Options, Futures, and

Other

Derivatives, 6th edition

48

Bootstrapping Example

•

Calculate

EUR 6M, 1Y, 2Y, and

3Y zero coupon

discount

rates

in continuous

compounding

given

the

following

bid

rates:

49

Forward interest rates

•

Forward

rates

can

be

derived

from

the

zero

rates•

eR(T)T

= eR(t)t eR(t,T)(T-t)

… solve

for

R(t,T), the

forward

interest

rate

from

t to T•

FRA –

forward

rate

agreement

–

cash settlement

of

the

difference

between

agreed

rate

RK

and

the actually

observed

rate

RM

(Libor) –

usually

at

the beginning

of

the

interest

period

•

Valuation

of

FRA: V=L(RK

-RF

)(T2

-T1

)e-R2.T2, if RK

is

the

contracted

interest

earned, RF

is

the forward

rate

from

T1

to T2

at

the

time

of

valuation

50

Example

Source: John Hull, Options, Futures, and

Other

Derivatives, 6th edition

51

FRA Quotes

52

Forward and Futures Pricing

•

Forwards

and

Futures have

different

settlement, however

the

price

are very

close

•

Investment

x consumption

assets

… arbitrage argument can

be

used

only

for

investment

assets

•

Short

selling

–

possible

if

the

asset

can

be borrowed

–

in case of

stock

dividends

must

be

paid

to the

owner•

A forward

contract

can

be

replaced

by

shortselling/investing

into

the

asset

and depositing/borrowing

the

corresponding

amount

53

Arbitrage Example

Source: John Hull, Options, Futures, and

Other

Derivatives, 6th edition

54

Forward Pricing

•

If

the

current

price

of

an

investment

asset with

no income

is

S0

then

the

forward

price F0

=S0

erT

•

If

the

investment

asset

provides

income with

a present

value

I, then

F0

=(S0

–I)erT

•

If

the

investment

asset

provides

known yield

q with

continuous

compounding

then

F0

=S0

e(r-q)T, r-q is

also

called

the cost of carry

55

Domestic

Currency

Underlying

Asset

Spot Market Forward Market

Buy

the

asset

at

S

Financing

Cost

Storage

Cost

-

Income

Sell

the

asset

at

F

General

Forward

Arbitrage Argument

56

Arbitrage Example

Source: John Hull, Options, Futures, and

Other

Derivatives, 6th edition

57

Market Value of a Forward

•

Initially

the

value

of

a forward

contract

is

zero, later

it

may

be

positive or

negative

•

f=(F0

-K)e-rT, where

K is

the

contracted

price, F0 the

actual

forward

price, and

T time

to delivery

from

today.•

Notice

that

futures contracts

settle

F0

-K, not (F0

- K)e-rT

•

It

can

be

shown

however

that

forward

and

futures prices

are theoretically

same

if

the

margin

account

yields

the

market rate

58

Futures on Stock Indices

•

The

underlying

index is

assumed

to provide an

expected

yield

q (which

should

represent

the

average

annualized

dividend yield during

the

life

of

the

contract)

•

Then

F0

=S0

e(r-q)T

•

The

average

dividend yield

q is

usually lower than then r (F0

>S0

), but

may

be

also higher

in some

periods

(F0

<S0

)

59

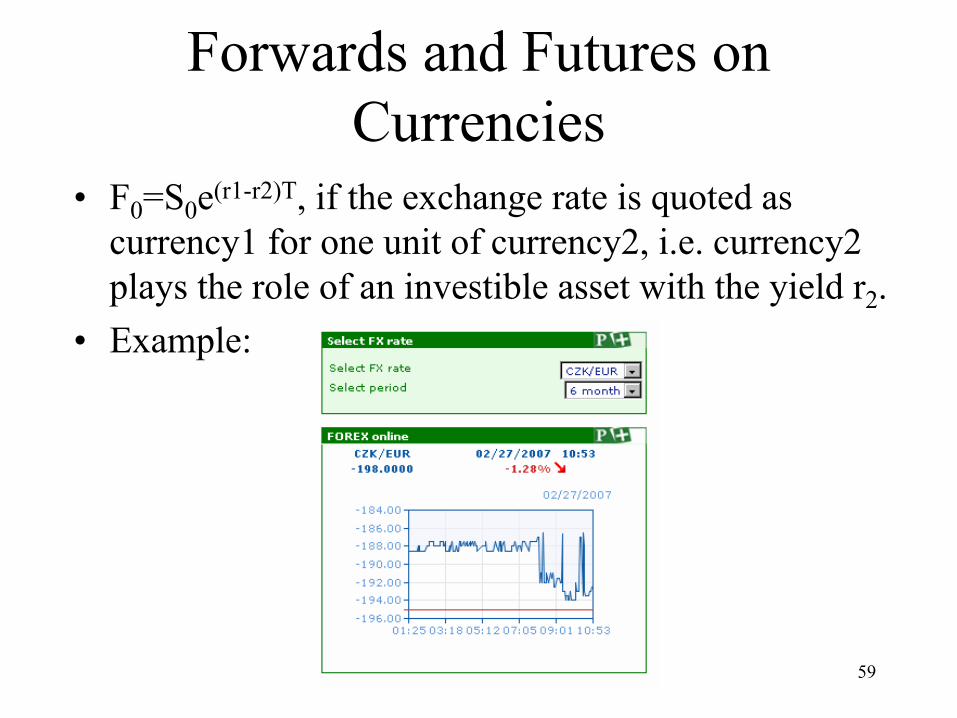

Forwards and Futures on Currencies

•

F0

=S0

e(r1-r2)T, if

the

exchange

rate

is

quoted

as currency1 for

one

unit of

currency2, i.e. currency2

plays

the

role of

an

investible

asset

with

the

yield

r2

.•

Example:

60

Futures on currencies

61

Futures on Commodities

•

Commodities

generally

have

storage

costs

and

do not provide

income, except

gold

and

silver.

•

Storage

costs

U (present

value) can

be

treated

as negative income, hence F0

=(S0

+U)erT

•

Some

assets

like

crude

oil

may

provide

so

called convenience

yield

y, then

F0

=(S0

+U)e(r-y)T= S0

e(r+u-y)T

•

Futures prices

of

oil

tend

to decrease, i.e. r+u<y, conevenience

yield

–

possible

shortages

62

Futures price versus expected spot price•

Long

futures position

is

equivalent

to investment

into

the

asset•

An

investor generally

require

extra return

for

systematic

risk•

If

k is

the

required

rate

of

return

on the

asset

then

it

follows

F0

=E(ST

)e(r-k)T, hence F0

<E(ST

) if

k>r•

This is the case in particular for futures on stocks or indexes

–

positive beta –

systematic

risk

•

If the asset has negative systematic

risk, then

F0

> E(ST

)

63

Normal

and

Inverted

Futures Prices

64

Contango and

Normal Backwardation

65

Interest

Rate

futures Eurodollar

futures

•

Eurodollars

are dollars

deposited

outside

of

the United

States

•

Three

month

Eurodollar

futures (CME) contracts 3-month

interest

rate. Delivery

March-June-

September-December

up

to 10 years

in the

future•

The

quote

= 100 –

r, where

r is

the

annualized

3-

month

rate

in the

Act/360 convention. One

basis point is

equivalent

to $25 settlement amount.

•

Example: Use futures contract

to lock

3-month interest

rate

earned

on $1 mil. one

year

later

66

Eurodollar futures

Wall

Street

Journal, Feb

5, 2004

67

Eurodollar

Fututres

Prices

on www.cme.com

68

Long Term Interest Rate Futures

•

Day count

conventions: Act/Act

(Treasuries), 30/360 (Corporate

bonds), Act/360 (Money

market)•

Bond prices: cash price

= clean

price

+ accrued

interest•

Treasury bond futures are quoted

in the

same

way

as the

bonds

(110-03 means

110 and

3/32

of the face value

$100 000)

•

Any Treasury

bond with

at

least

15 years

to maturity can

be

delivered

using so called

conversion factors (6% YTM convention)

69

70

71

72

Hedging Example

•

We

hold 100 T-Bonds

currently

priced

at 95% (Nominal=$100 000), with 20 years to

maturity and duration 15 years. We need to sell the bonds in 2 months.

•

Propose an appropriate number of 3 months futures contracts on 30Y T-Bonds to hedge the price provided the quoted futures price is 90%, the current conversion factor for the CTD is 1.3, and its duration is 10.

73

Are forward

and

futures prices equal?

•

Yes, if

we

assume

that

the

interest

rates

are constant, or

at

least

sufficiently

independent

on underlying

asset

prices•

This

assumption

does

not hold for

interest

rate

futures and

forwards•

IR futures rates

are higher

that

IR forward

(FRA) rates

due

to the

discounting difference

and

the

convexity

adjustment

•

Forward

rate

= Futures rate

-

2T1

T2

/2

74Most of

the

volume –

Interest

Rate

Swaps

75

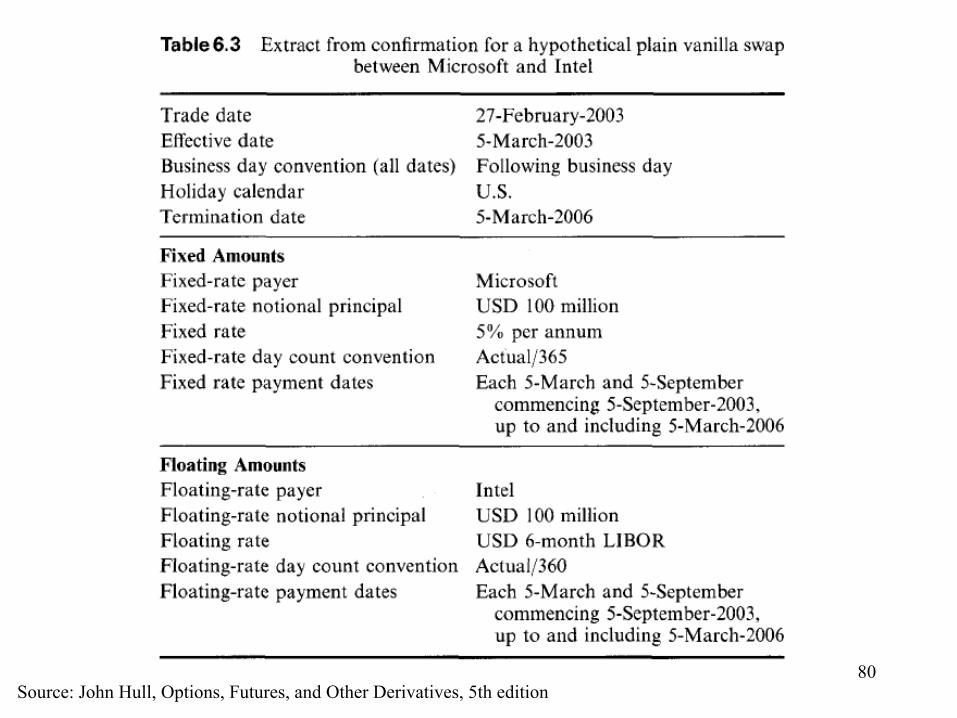

Swaps

•

Exchange of

cash flows

in the

future•

„plain

vanilla“ interest

rate

swaps

•

Currency

swaps

Source: John Hull, Options, Futures, and

Other

Derivatives, 5th edition

76

Interest Rate Swap Example

Source: John Hull, Options, Futures, and

Other

Derivatives, 5th edition

77

Interest Rate Swap Example•

Intel transforms

fixed

5,2% payments

to Libor +

0,2%•

Microsoft transforms

Libor + 0,1% payments

to

5,1% fixed

payments•

Assets

can

be

transformed

as well

78

Role of Financial Intermediary

•

Banks

play the

role of

intermediaries•

The

banks

moreover

exchange

„the

positions“

mutually, some

play the

role of

market-makers•

Banks

use so

called

ISDA master agreements

79

IRS Quotes

Source: www.kb.cz

80Source: John Hull, Options, Futures, and

Other

Derivatives, 5th edition

81

Interest Rate Swap Example – Valuation of IRS

Source: John Hull, Options, Futures, and

Other

Derivatives, 5th edition

• Can

be

regarded

as an

exchange

of

a fixed-coupon

bond (FCB) fora floating

rate

note, MV = Value

of

the

FRN –

Value

of

the

FCB

82

83

84

85

Currency Swaps (CCS)•

Exchange of

interest

payments

(usually

fix-fix) in two

currencies•

Exchange of

principals

at

the

beginnig

and

at

the

end

of

the

contract•

Valuation

similar

to IRS

•

Credit

risk of

CCS is

higher

than

that

of

IRS

86

Part 3 Options

Markets

87

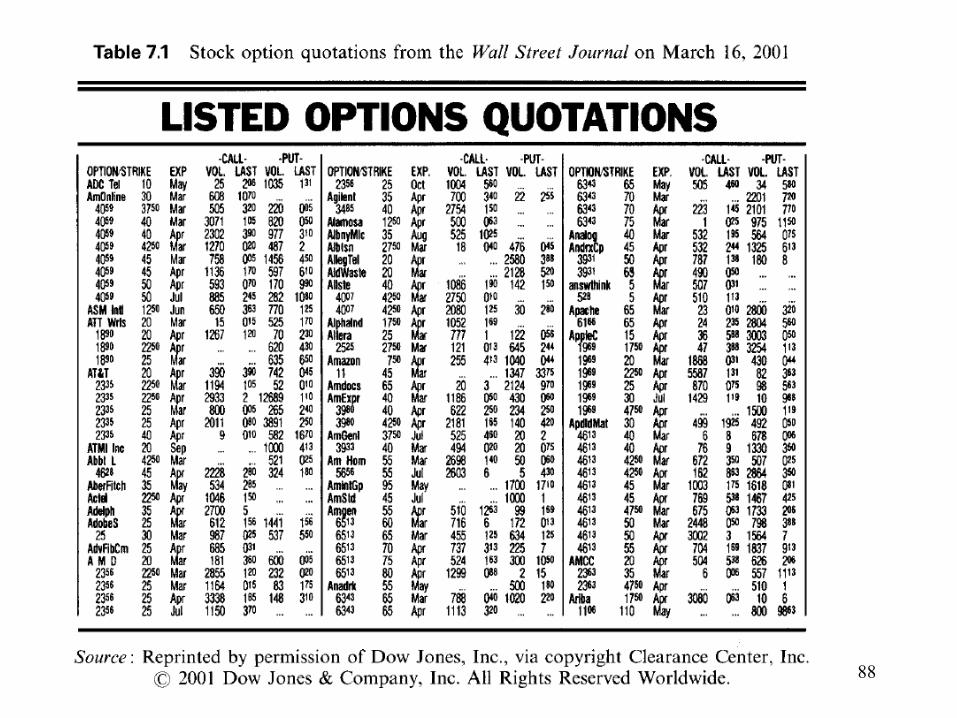

Underlying assets•

Call/Put, long/short

position, European/American,

in/at/out

of

the

money, intrinsic/time

value•

Stock

options

–

mostly

exchange

traded

–

CBOE,

PHLX, AMEX, PACIFEX, EUREX•

Options

on indices

–

exchange

traded

–

cash

settlement•

Currency

options

-

exchange

traded

and

OTC

•

Options

on futures contracts

–

exchange

traded

– options

to acquire

long

or

short

position

in a

futures contract•

Expiration

date

and

strike price

is

defined

–

options

are traded

at

a premium

88

89

90

EUR/USD options

volatility quotes

Source: Reuters, 27/11/07

91

Margins

•

Investors

writing

an

option

(short

position) must maintain

a margin

•

Naked

option

is

an

option

written

without

the offsetting

position

in the

underlying

stock

–

the

margin

than

must

be

at

least

10%, resp. 20% of

the underlying

price

•

Writing

covered

calls

–

the

underllying

is

already owned

•

An

Option

Clearing Corporation

usually guarantees

the

settlement

92

Factors affecting option prices

•

The

current

stock

price, S0

•

The

strike price, K•

The

time

to expiration, T

•

The

volatility of

the

stock

price, •

The

risk-free interest

rate, r

•

The

dividends

expected

during

the

life

of the

option

93

Factors affecting option prices

94

95

96

Factors affecting option prices

Source: John Hull, Options, Futures, and

Other

Derivatives, 5th edition

97

Assumptions and notation•

No transaction

cost, equal

taxes, borrowing

and

lending

at

the

risk-free rate, no arbitrage

opprotunities, no bid-ask spreads

•

Notation:

98

Upper and lower bounds for option prices•

A call option

can

never

be

worth

more than

the

stock

S0•

A European

put option

can

never

be

worth

more than

the

discounted

strike price

Ke-rT

•

A European

call option

on non-dividend stock

is

worth

at

least

S0 - Ke-rT

•

A European

put option

on non-dividend stock

is

worth

at

least

Ke-rT

- S0

99

Put-Call Parity

•

Portfolio A: one

European

call option

plus cash Ke-rT

•

Portfolio B: one

European

put option

plus one

stock

•

The

value

of

both

portfolios

at

T is max(K,ST

)•

Hence c+Ke-rT

= p+S0

, otherwise

there

is

an arbitrage

opportunity

100

Put-Call Parity Example

• Strategy: short

B, buy

A

Source: John Hull, Options, Futures, and

Other

Derivatives, 5th edition

101

Trading strategies involving options•

Different

strategies

combining

a long/short

position

in a stock

and

a long/short

position in a put/call option

•

More complex

strategies

involve

two different

options

•

Bull/Bear/Butterfly/Calendar/Diagonal spreads, straddles, strips, straps, strangles

102

Source: John Hull, Options, Futures, and

Other

Derivatives, 5th edition

103

Source: John Hull, Options, Futures, and

Other

Derivatives, 5th edition

104

Source: John Hull, Options, Futures, and

Other

Derivatives, 5th edition

105

Source: John Hull, Options, Futures, and

Other

Derivatives, 5th edition

106

Part 4 Pricing

of

options

107

Pricing of options – Binomial trees•

Example: European

call option

to buy

a

stock

in three

months

for

$21

Source: John Hull, Options, Futures, and

Other

Derivatives, 5th edition

108

One step binomial tree example

•

It

is

possible

to set up

a riskless

portfolio combining

a position

in the

stock

and

in the

option

•

The

portfolio is

riskless

if

the

profit/loss

is

the same

in all

(both) scenarios

•

Long: 0,25 shares•

Short: 1 option

•

The

value

of

the

portfolio is

$4,5 in three

months in both

cases

•

Hence the

present

value

of

the

option

is

calculated as $5 minus discounted

$4,5

109

General one-step tree

•

The

riskless

portfolio can

be

set up

in general

110

Risk-neutral Valuation

•

Note, that

the

result

does

not depend

on probabilities

of

the two

scenarios

•

However

if

we

set up

p, probability of

the

movement

up, so

that

E(ST

)=S0

eRT (the

stock

return

equls

to the

risk-free rate) then

it

turns

out

that

the

price

of

the

option

equals

to

the

discounted

expected

pay-off•

Risk neutral valuation principle: we can assume that the world is risk neutral when pricing an option. The result is valid also in the real world which is not risk-neutral!

111

Two-step binomial trees

Time

steps

are three

months, r=12%

112

Two-step binomial trees

The

option

price

equals

to the

expected

pay-off

in a riskneutral

world

113

European x American options

114

Delta

•

Riskless

portfolio: -1 call option, +

stock•

The

change

in the

option

price

is

offset by

* the

change

of

the

stock

price•

Delta equals

to 25% in the

one-step

binomial

tree

example•

Delta changes

in a two-step binomial

tree

115

Volatility•

Volatility

is

measured

as the

standard deviation

of

the

return

(with

expected

value

) normalized

by the

square root

of

the

time•

u and

d are usually

derived

from

those

parameters

•

N-step binomial

tree

can

be

then

used

for

a Monte-Carlo simulation

When

t is

small

116

Behaviour of Stock Prices

•

Stochastic

process

–

variable

whose

value

depends on time

and

changes

in an

uncertain

way

•

Discrete/continuous

time, discrete/continuous variable

•

Markov

process

–

only

the

present

value

of

a variable

is

relevant

for

the

future

•

Market rates

(stock

prices, exchange

rates, interest rates) are assumed

to follow

the

Markov

process

(x technical

analysis)

117

Wiener process

•

Continuous

time

process: any

time

period can

be divided

into

arbitrary

number

of

steps

•

Wiener

process

(Brownian

motion) –

Markov process

where

z(1)-z(0) has distribution

N(0,1) and

the

distributions

are „uniform“ for

smaller

time

steps•

The

square root

of

time

rule: z(T0

+t)-z(T0

) has the distribution

N(0,t)

•

Stochastic

difference

equation: dz=dt, where

is randomply

taken

with

the

distribution

N(0,1)

•

Generalized

Wiener

process: dx=adt

+ bdt, i.e. x(T0

+t)-x(T0

) has the

distribution

N(at,bt)

118

119

120

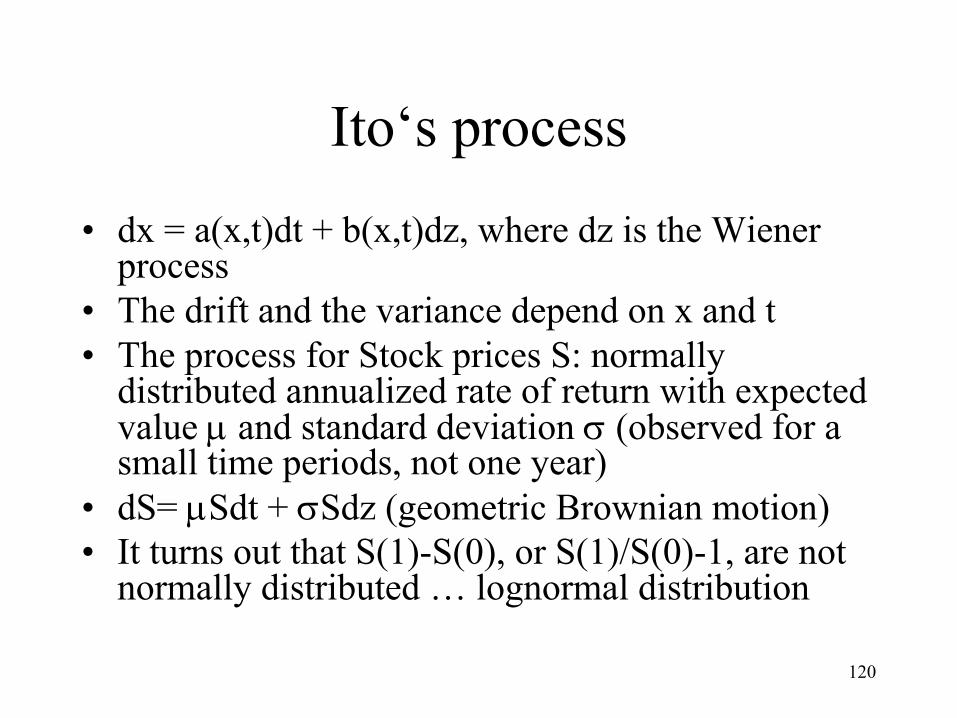

Ito‘s process

•

dx

= a(x,t)dt

+ b(x,t)dz, where

dz

is

the

Wiener process

•

The

drift and

the

variance depend

on x and

t•

The

process

for

Stock

prices

S: normally

distributed

annualized

rate

of

return

with

expected value

and

standard deviation

(observed

for

a

small

time

periods, not one

year)•

dS= Sdt

+ Sdz

(geometric

Brownian

motion)

•

It

turns

out

that

S(1)-S(0), or

S(1)/S(0)-1, are not normally

distributed

… lognormal

distribution

121

Lognormal distributionLognormal Distribution

00

f(x)

122

Monte Carlo simulation

123

Ito‘s Lemma

•

If

G=G(x,t) where

x follows

an

Ito‘s process

dx

= a(x,t)dt

+ b(x,t)dz, then

G

follows

the

Ito‘s process

•

Where

dz

is

the

same

as above

124

Application to forward contracts

•

Forward

price

of

a non-dividend paying stock

F=Ser(T-t)

•

Using

the

Ito‘s lemma it

follows

that

the process

for

F is:

125

Lognormal property

•

Let G=lnS, where

S follows

the

geomentric Brownian

motion, then

applying

the

Ito‘s

lemma we

get:

•

Consequently

lnS(T)-lnS(0) has a normal distribution

N((-2/2)T, T)

126

The Black-Scholes Model•

Lognormal

property

of

stock

prices

127

Lognormal property of Stock prices•

It

can

be

shown

that

•

Stock price can be modelled as

128

Estimating volatility from historical data

129

Black-Scholes differential equation•

Principle: set up

a risk-less

combination

of

an

option

and

the

underlying

stock

–

the price

of

the

option

f depends

on the

underlying

S and

t –

use the

derivative

– delta hedging

•

The

return

on this

portfolio in a short

time period must

be

equal

to the

risk free interest

rate

130

Black-Scholes differential equation

Source: John Hull, Options, Futures, and

Other

Derivatives, 5th edition

131

Black-Scholes differential equation

132

Black-Scholes differential equation

Discrete

version:

Ito‘s lemma:

133

Black-Scholes differential equation

Risk less

portfolio

I.e.

Use the

equations

above

134

Black-Scholes differential equationHence the

portfolio is

risk less, as expected, and

so

And we

get

the

Black-Scholes-Merton

differential

equation:

135

Risk-neutral valuation•

The

Black-Scholes-Merton

equation

does

not

depend

on the

expected

return

, i.e. on investors risk preferences!!!

•

We

can

assume

that

we

are in a risk-neutral

world.•

The

result

will

be

the

same

as in the

real

world

with

risk sensitive investors.•

Consequently

we

can

simply

discount

the

expected

pay-off

of

an

option

using

the

risk free rate.

•

The

result

will

be

the

unique

solution

of

the differential

equation

136

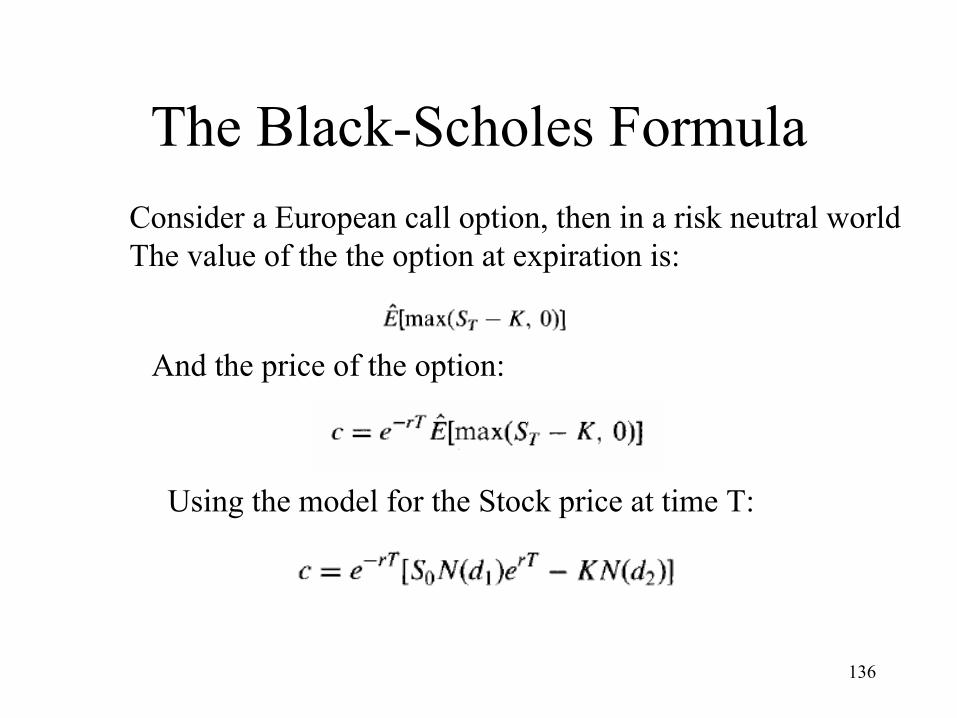

The Black-Scholes FormulaConsider

a European

call option, then

in a risk neutral

world

The

value

of

the

the

option

at

expiration

is:

And the

price

of

the

option:

Using

the

model for

the

Stock

price

at

time

T:

137

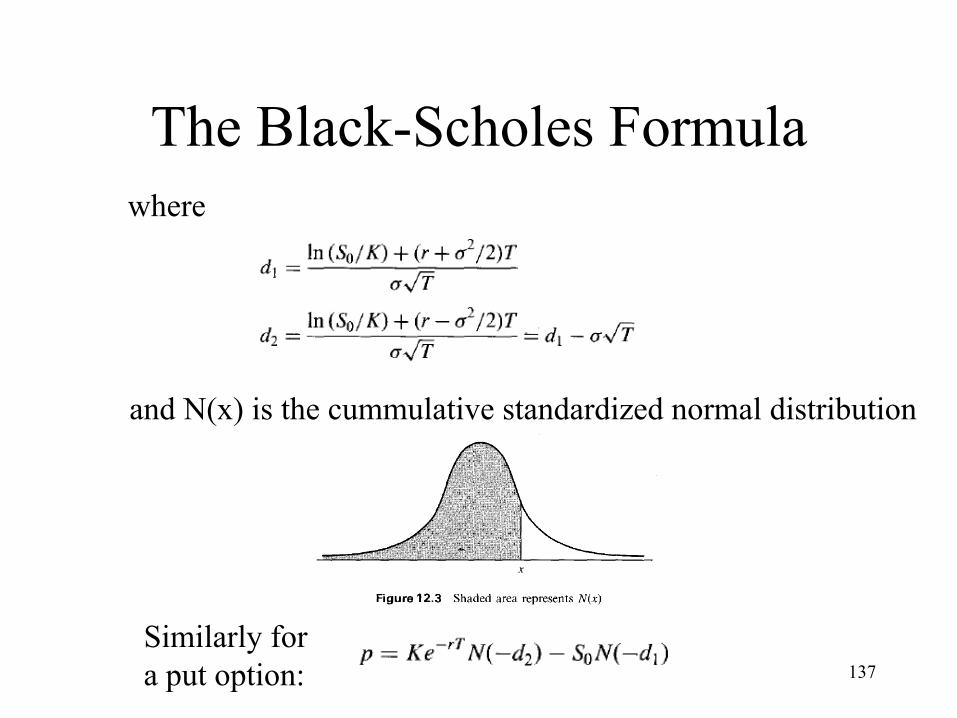

The Black-Scholes Formulawhere

and

N(x) is

the

cummulative

standardized

normal

distribution

Similarly

fora put option:

138

The Greeks

•

Partial

derivatives

of

an

option

(portfolio) market value

measure

sensitivity with

respect

to the

relevant

variables•

Delta, Gamma –

the

1st and

the

2nd derivatives

w.r.t. the

underlying

asset

price•

Vega –

the

derivative

w.r.t. the

volatility variable

•

Rho –

the

derivative

w.r.t the

interest

rate•

Theta –

the

derivative

w.r.t. to time, ususally

measured

as the

change

of

value

„per day“•

The

Greeks

are used

for

hedging… Delta-hedging,

Vega-hedging, Gamma-hedging e.t.c

139

International Financial Markets Lecture Notes – J.Witzany•

Includes

valuation

of

forwards

and

a

detailed

chapter

on derivatives

more or

less covering

1BP426 content

•

Oeconomia, vailable

in the

VŠE bookstore•

186 Kč, 180 pages, English