Mountain Goats in the Kicking Horse Canyon, Trans Canada Highway

Sample Analysis -‐ Prepared by Shirley Gee

TransCanada A Financial Analysis

January 2009

Sample Analysis -‐ Prepared by Shirley Gee 2

A look at financial profile of TransCanada as an investment opportunity.

A. Introduction

The goal of this review is to determine whether

TransCanada has a sufficiently strong financial

profile to recommend it as an investment

opportunity. TransCanada’s financial track record,

its prospect for future earnings, and its managerial

acumen were evaluated. The most current annual

report used was in 2007 and was the primary basis

for making this financial assessment. This review is

supported by financial statements going back

three years (i.e., 2004 to 2006) and was used to

assess TransCanada’s financial trends. To

compliment this review, general research was also

performed to determine whether there were

significant activities associated with TransCanada,

which would negatively impact on its financial

standing subsequent to its 2007 annual report.

Finally, comparable corporations were reviewed

to assess TransCanda’s performance in

relationship to others in the same industry. The

two corporations selected for this comparison

were TC Pipelines L.P., which owns and

participates in the management of United States-‐

based pipeline systems in the mid-‐western states,

and Enterprise Products Partners L.P., which

operates in Mid-‐America. Comparative results

between TransCanada and others in the industry

are reflected in Section D. Summary of Findings

using their respective 2007 annual reports.

It should be noted that all figures within the

Tables in this financial assessment are in Canadian

dollars and in $Million units.

A Company Embedded in Mutual Funds in many 401(k)’s

Sample Analysis -‐ Prepared by Shirley Gee 3

A Corporation with a Pipeline reaching from

Canada through United States to

Mexico

B. Overview

TransCanada is a corporation that operates a

pipeline system, which delivers natural gas

throughout North America via its vast pipeline

network and one of the largest providers of gas

storage. TransCanada’s organizational structure

reflects two primary segments; namely, Pipelines

and Energy. The Pipeline segment consists

primarily of Transamerica’s natural gas pipelines

in Canada, the U.S. and Mexico with one oil

pipeline (Keystone Pipeline Project). The Energy

segment includes the Corporation’s power

operations, natural gas storage business and

liquefied natural gas (LNG) projects in Canada and

the U.S. The corporation is expanding their

business into the oil pipeline business creating

another avenue for future growth. Their storage

capability and pipeline assets are the fundamental

basis for their business and the platform from

which they launch ancillary businesses (e.g.,

energy infrastructure projects, alternative energy

initiatives, etc.)

and growing …

Sample Analysis -‐ Prepared by Shirley Gee 4

Assessment of Financial Performance is Critical

C. Financial Performance and Management Assessment

1. General Financial Assessments – Income Statements between the period 2004 and 2007 were reviewed to

determine whether the business had a consistent, positive net income (owner’s equity) over multiple years.

An upward trajectory (i.e., an increase of net income over time) was considered a good indication of

financial health. Balance sheets over the same period were used to assess current and long-‐term assets and

to determine whether such assets were related to their primary business (i.e., pipeline systems or gas

storage). Liabilities were reviewed to assess the corporation’s debt load and to review its existing financial

obligations. Also of interest was the section on Shareholder’s Equity to assess other capital investments

and contributions in addition to net income.

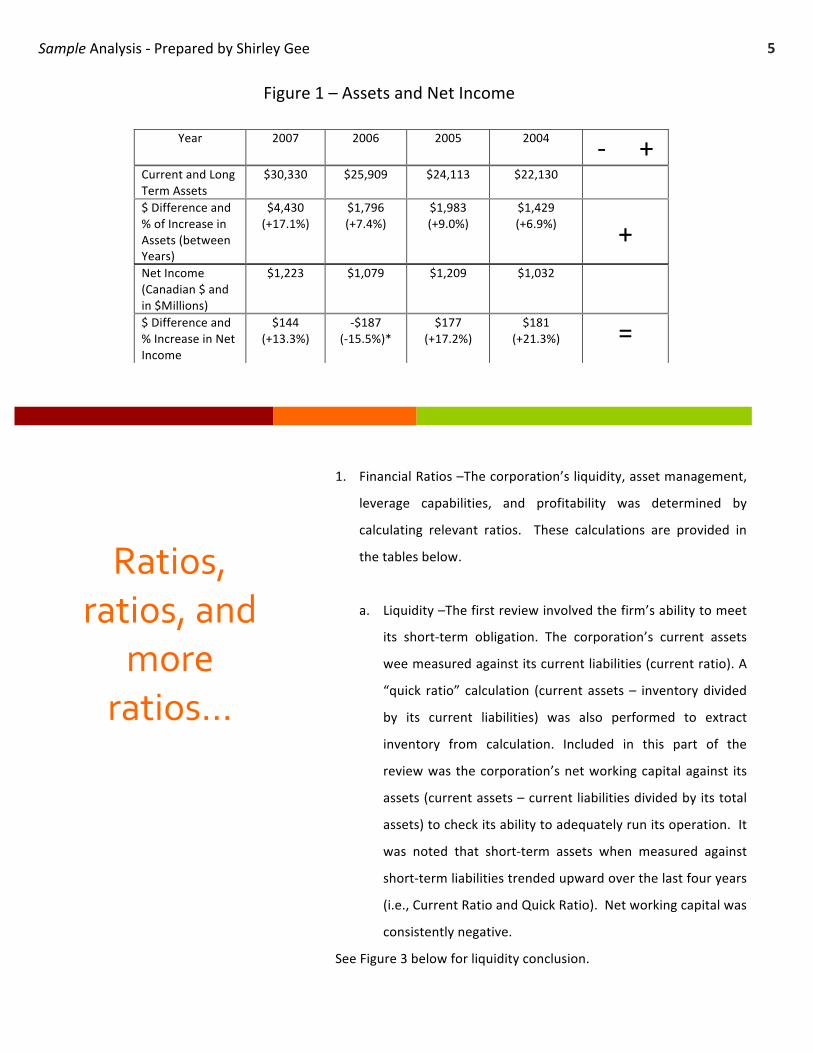

A quick review of total assets and net income revealed the following trends. Total assets had an upward

trend while net income had a downward trend between 2004 and 2007, with a significant drop in net

income in 2006. Under closer examination, it was determined that this drop in net income in 2006 was due

to a major acquisition in 2007 (of ANR Pipelines) by TransCanada. See Figure 1 – Assets and Net Income

Sample Analysis -‐ Prepared by Shirley Gee 5

Year 2007 2006 2005 2004 -‐ + Current and Long Term Assets

$30,330 $25,909 $24,113 $22,130

$ Difference and % of Increase in Assets (between Years)

$4,430 (+17.1%)

$1,796 (+7.4%)

$1,983 (+9.0%)

$1,429 (+6.9%)

+ Net Income (Canadian $ and in $Millions)

$1,223 $1,079 $1,209 $1,032

$ Difference and % Increase in Net Income

$144 (+13.3%)

-‐$187 (-‐15.5%)*

$177 (+17.2%)

$181 (+21.3%) =

Ratios, ratios, and

more ratios…

1. Financial Ratios –The corporation’s liquidity, asset management,

leverage capabilities, and profitability was determined by

calculating relevant ratios. These calculations are provided in

the tables below.

a. Liquidity –The first review involved the firm’s ability to meet

its short-‐term obligation. The corporation’s current assets

wee measured against its current liabilities (current ratio). A

“quick ratio” calculation (current assets – inventory divided

by its current liabilities) was also performed to extract

inventory from calculation. Included in this part of the

review was the corporation’s net working capital against its

assets (current assets – current liabilities divided by its total

assets) to check its ability to adequately run its operation. It

was noted that short-‐term assets when measured against

short-‐term liabilities trended upward over the last four years

(i.e., Current Ratio and Quick Ratio). Net working capital was

consistently negative.

See Figure 3 below for liquidity conclusion.

Figure 1 – Assets and Net Income

Sample Analysis -‐ Prepared by Shirley Gee 6

Meeting short-‐term obligations with liquidity.

Year Formula 2007 2006 2005 2004 -‐ +

Current Ratio

Current Assets/ Current Liability

$2305/ $3035 = 75.9%

$2092/ $2989 = 70.0%

$1566/ $3112 = 50.3%

$1109/ $2744 = 40.4%

+

Quick Ratio

Current Asset –

Inventory/ Current Liabilities

$2305-‐$297/ $3035 = 66.2%

$2092-‐$392/ $2989 = 56.9%

$1556-‐$281/ $3112 = 41.0%

$1109-‐$174/ $2744 = 34.1%

+

Net Working Capital to Assets

Current Asset – Current

Liabilities/ Total Assets

$2305-‐$3035/ $30330

= -‐2.4%

$2092-‐$2939/ $25909

= -‐3.5%

$1556-‐$3112/ $24113

= -‐12.9%

$1101-‐$2754/ $22422

= -‐7.4%

-‐

See Figure 2 –Liquidity

b. Asset Management –An attempt was made to review the corporation’s efficiency in creating sales

using its assets, but no information was available breaking out the revenue. Inventory turnover,

collection period, fixed asset turnover or total assets turnover, therefore, could not be determined

based on readily available, public sources.

c. Leverage – Next came the corporation’s degree of indebtedness and its ability to meet its long-‐

term obligations. It was determined that TransCanada’s liability was approximately 66% on

average to assets. Clearly TransCanada was maximizing its leverage capabilities and using its

assets to expand its business. The Debt to Equity ratio was 2:1 and leverage at 65+% of equity

(presumably for growth and expansion), while temporary, seemed high. There is some degree of

risk and exposure here.

See Figure 3 below for Asset Management and Leverage Conclusions.

Sample Analysis -‐ Prepared by Shirley Gee 7

d. Profitability – The corporation’s profit margin, return on assets and equity,

price/earnings ratio, and market-‐to-‐book ratio were all reviewed to

determine its current financial standing relative to profitability. In spite of a

trend downwards and given current economic conditions, the gross profit

margin seemed good at ~14%. Return on assets was positive each year and

return on equity was solid. Price/earnings was over 15 times each year,

which is good. See Figure 4 below for results.

Figure 4 – Profitability

Year Formula 2007 2006 2005 2004 -‐ + Gross Profit Margin

Net Income/ Revenue

$1223/ $8828 = 13.9%

$1079/ $7520 = 14.3%

$1209/ $6124 = 19.7%

$1032;/ $5497 = 18.8%

+ Return on Assets

Net Income/ Total Assets

$1223/ $30330 = 4.0%

$1079/ $25909 = 4.2%

$1209/ $24113 = 5.0%

$1032/ $22430 = 4.7%

+ Return on Equity

Net Income/ Owner’s Equity

$1223/ $9785 = 12.5%

$1079/ $7701 = 14.0%

$1209/ $7206 = 16.8%

$1032/ $6565 = 15.7%

= Price/ Earnings

Common Stock Price per Share /Earnings Per share

17.5

18.4

14.7

14.0

+

Year Formula 2007 2006 2005 2004 -‐ +

Debt Ratio

Total Liabilities/ Total Assets

$19546/ $30330 = 64.4%

$17453/ $25909 = 67.4%

$16124/ $24113 = 66.9%

$14430/ $22130 = 65.2%

-‐ Debt-‐to-‐Equity Ratio

Total Liabilities/ Owner’s Equity

$19546/ $9785 = 200% 2:1

$17453/ $7701 = 226% 2.3:1

$16124/ $7206 = 224% 2.2:1

$14430/ $6565 = 220% 2.2:1

-‐

See Figure 3 – Asset Management & Leverage

Lorem Ipsum

Leadership is key . . .

3. Assessment of Management

It appears the corporation is making reasonable

decisions regarding the business. The corporation

was sustaining its long-‐term value through its

existing assets by investing in energy infrastructure

projects, which are directly related to its core

business. All of these projects appear to be timed

to come on line around the same time (i.e., in 3

years) and barring any major, unforeseen event,

there should be a jump in revenue, return on assets

and return on equity by 2010 and beyond.

Management is also making decisions to diversify

into “other energy-‐related” projects (e.g., oil) and

“alternative” energy projects (e.g., wind), which

demonstrates a “forward leaning” posture

consistent with market direction (e.g., the Green

Movement). More importantly, the Corporation is

staying within its core business and competency.

Of particular interest was the sections in the

Management’s Discussion and analysis on how they

handled the business risks whether it was supply.

Competition, market prices, weather, plant

availability, execution and capital cost risks, and

power regulations. TransCanada’s management of

these risk seemed both thorough, orderly, and

reasonable. More importantly, it seemed

transparent and designed for comprehensibility, as

compared to the other corporations reviewed

(whether due to administrative inexperience, lack

of comparable resources, absence of available

data, or deliberate omission).

It was noted that the corporation manages 16

pipeline systems and controls 9 of them 100%; 5 of

them 50+%; and 3 of them less than 50%. This

provides for maximum control over the

management of the pipeline network and stability

within the corporation and industry within which it

operates.

It appears that management recognizes that

regulatory decision have a negative impact on

financial returns especially on existing and future

investments. This demonstrates an solid

awareness of the industry and its business

environment. This coupled with the size (large) of

TransCanada and its ability to take advantage of

“economy of scale” makes TransCanada less

Sample Analysis -‐ Prepared by Shirley Gee 9

vulnerable to external forces. As such, TransCanada

is probably more capable of managing regulatory

issues and it arises. In any case, adverse regulatory

decisions impact the industry as a whole; not just

TransCanada so the corporation should not lose its

competitive edge due to it.

Liquidity risk is always a problem, but

management seems to be managing its cash flow

needs pretty well with 5+ years of forecasting,

including provisions to cover both contractual

repayment obligations and long-‐term debt service.

TransCanada’s management capability and

competency seem solid and reasonable.

D. Summary of Findings

1. Financial Assessment

In reviewing the income statements and balance

sheets, I determined that the corporation had a

reasonably strong financial posture. Over a period

of four years, the corporation had a fairly steady

financial profile. It’s debt ratio was a bit high at over

65% of liabilities to assets, but this appears to be due

to the numerous expansion projects which should all

come on line by 2010. The numerous projects,

which either supports their primary business

(pipeline infrastructure expansion or maintenance)

or expands their gas storage business, all seem to

contribute to the profitability of the business which

is modest, but steady.

A review of their liquidity, leverage, and

profitability demonstrates a consistent picture of

reasonable financial health with maximum financial

flexibility. This financial state would enable the

corporation to take advantage of opportunities and

react to market shifts and challenges.

TransCanada’s success appears to be based on

maintaining a strong cash flow position in order to

take advantage of opportunities; its “forward

thinking” corporate culture with respect to energy

needs of customers in next 5-‐10 years; a deliberate

effort to construct infrastructure now to meet those

needs in the future; and a relatively conservative

approach to growth (i.e.., modest, steady growth).

Moreover, the corporation’s commitment to staying

within their core business and competency is wise

and its consistent ability to provide dividends to its

stockholders (even providing buying opportunities

at discounted rate) is a real plus. You always want

to keep the shareholders’ happy.

2. General Observations and Assessments

There were no major or significant findings found

during my general research which would raise

concerns about its dealings within the market.

Sample Analysis -‐ Prepared by Shirley Gee 10

There was no history of financial malfeasance or concerns regarding its corporate culture or managerial

philosophy.

The only critical accounting disclosure and information was in 2004 when the corporation did a re-‐

statement of its income statement and balance sheets to make the Canadian Institute of Chartered

Accountants better align its financial definitions to the International Financial Reporting Standards (IFRS) and

the U.S. GAAP (See 2007 Annual Report Note #2). The financial impact of this particular adjustment was an

increase in retained earnings by $4 million dollars for year ending 2007.

Of interest given a climate of high profile corporations going bankrupt due to questionable accounting

practices was the corporations position with respect to its retirement obligations. A quick review of their asset

retirement obligation as of December 31, 2007 was $88 billion. Settlement of the obligation ranges from 11 to

32 years. Using the 11 years, to be conservative, the corporation would need $8B to cover its retirement

obligations for any given year. With a net worth of $10B as of December 31, 2007, TransCanada could easily

cover its current retirement obligations.

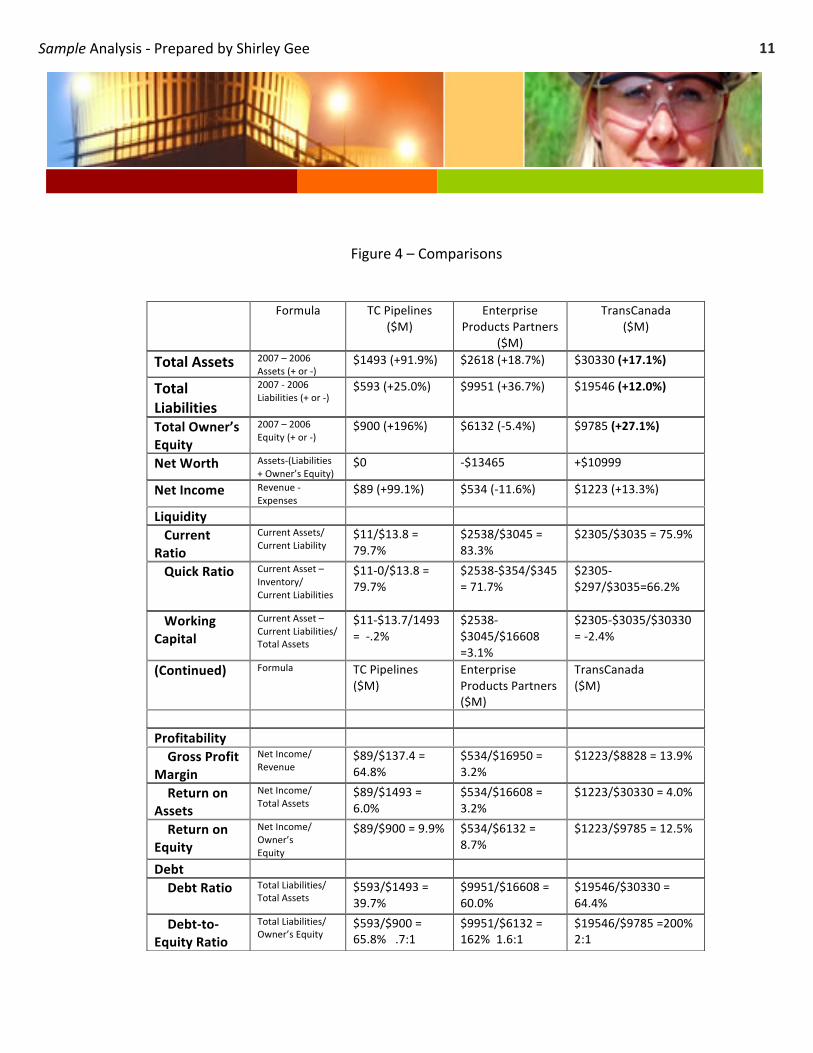

3. Industry Comparison

A review of TC Pipelines L.P. and Enterprise Products Partners L.P. gave a good industry comparison to

TransCanada. The following is the comparative chart. With respect to debt and profitability, TC Pipeline, while

smaller, might be a better buy than TransCanada based on their respective 2007’s performances. A more in-‐

depth analysis of TC Pipeline’s historical trend would be needed, however, before they could be

recommended. TransCanada does not seem particularly out of sync with the industry as a whole. The

following is a comparative table depicting the three corporations side by side.

Sample Analysis -‐ Prepared by Shirley Gee 11

Figure 4 – Comparisons

Formula TC Pipelines ($M)

Enterprise Products Partners

($M)

TransCanada ($M)

Total Assets 2007 – 2006 Assets (+ or -‐)

$1493 (+91.9%) $2618 (+18.7%) $30330 (+17.1%)

Total Liabilities

2007 -‐ 2006 Liabilities (+ or -‐)

$593 (+25.0%) $9951 (+36.7%) $19546 (+12.0%)

Total Owner’s Equity

2007 – 2006 Equity (+ or -‐)

$900 (+196%) $6132 (-‐5.4%) $9785 (+27.1%)

Net Worth Assets-‐(Liabilities + Owner’s Equity)

$0 -‐$13465 +$10999

Net Income Revenue -‐ Expenses

$89 (+99.1%) $534 (-‐11.6%) $1223 (+13.3%)

Liquidity

Current Ratio

Current Assets/ Current Liability

$11/$13.8 = 79.7%

$2538/$3045 = 83.3%

$2305/$3035 = 75.9%

Quick Ratio Current Asset – Inventory/ Current Liabilities

$11-‐0/$13.8 = 79.7%

$2538-‐$354/$345 = 71.7%

$2305-‐$297/$3035=66.2%

Working Capital

Current Asset – Current Liabilities/ Total Assets

$11-‐$13.7/1493 = -‐.2%

$2538-‐$3045/$16608 =3.1%

$2305-‐$3035/$30330 = -‐2.4%

(Continued) Formula TC Pipelines ($M)

Enterprise Products Partners ($M)

TransCanada ($M)

Profitability

Gross Profit Margin

Net Income/ Revenue

$89/$137.4 = 64.8%

$534/$16950 = 3.2%

$1223/$8828 = 13.9%

Return on Assets

Net Income/ Total Assets

$89/$1493 = 6.0%

$534/$16608 = 3.2%

$1223/$30330 = 4.0%

Return on Equity

Net Income/ Owner’s Equity

$89/$900 = 9.9% $534/$6132 = 8.7%

$1223/$9785 = 12.5%

Debt

Debt Ratio

Total Liabilities/ Total Assets

$593/$1493 = 39.7%

$9951/$16608 = 60.0%

$19546/$30330 = 64.4%

Debt-‐to-‐Equity Ratio

Total Liabilities/ Owner’s Equity

$593/$900 = 65.8% .7:1

$9951/$6132 = 162% 1.6:1

$19546/$9785 =200% 2:1

Sample Analysis -‐ Prepared by Shirley Gee 12

E. Recommendation

All in all and although the debt ratios were a bit high, I would still affirmatively recommend this corporation

due to its strong and steady financial posture and its consistent return on assets and equity over a sustained

period of time. Their regular dividend payouts over the last 5+ years shows a sustained ability to manage

operations for the benefit of stockholders. Their current projects indicate expansion opportunities (i.e., in oil,

wind, coal fire electric power, and additional pipeline acquisition and storage facilities), which should provide for

continual return on assets and equity well into the foreseeable future. The corporation’s move towards

alternative, renewable energy is in keeping with the direction of the market from all indications and

demonstrates an awareness of opportunities and the need to position itself to maximize leverage of its assets.

Finally, as compared to others in industry, it’s a very solid corporation with a positive net worth, manageable debt

ratio and good return on assets and equity. It’s a Buy!