Financial Analysis of the Grameen Bank - Wikispacesof...An Analysis of the Financial ... (MFIs) in...

22

An Analysis of the Financial Strategies of Grameen Bank Jess Lampe and Sagar Dedhia 7/23/2009

Transcript of Financial Analysis of the Grameen Bank - Wikispacesof...An Analysis of the Financial ... (MFIs) in...

An Analysis of the Financial

Strategies of Grameen Bank

Jess Lampe and Sagar Dedhia

7/23/2009

P a g e | 2

Contents

Introduction ..................................................................................................................................... 3

Increased Savings Deposits: A Changing Funding Profile ............................................................. 5

Increased Fixed-Deposits: Deployment of Capital ......................................................................... 7

Comparison with Other MFI Strategies .......................................................................................... 8

Rationale for Grameen’s Financing Strategy ................................................................................ 11

Rationale for Grameen’s Investment Strategy .............................................................................. 12

Impact of Grameen’s Strategy on Capital Adequacy ................................................................... 16

Recommendations to Improve Profitability and Capital Adequacy ............................................. 19

Conclusion .................................................................................................................................... 21

Bibliography ................................................................................................................................. 22

P a g e | 3

Introduction

Grameen Bank led by Prof. Muhammad Yunus has proven that poverty stricken borrowers can be

relied on to pay back loans even when they have no collateral. This was a revelation to banks,

governments, and development organizations around the world which, for the longest time, did not

believe it was possible to lend to the poor.

To reward poor borrowers for their integrity, Grameen Bank has offered generous interest rates

on loans and savings. Grameen offers loans at 10% flat rate interest (effective interest rate of 20%) and

roughly 8.5-10.4% on savings deposits. The spread is more favorable to borrowers than the spread offered

by most other Microfinance Institutions (MFIs) in Bangladesh. Other MFIs offer lending rates closer to

12.5% flat rate (25% effective interest) and savings rates from 4.0-6.0% (S.F. Ahmed and Co., 2009).

Essentially, other MFIs are charging borrowers more for lending money and are paying the borrowers less

for the use of their money.

While offering these generous terms to borrowers, Grameen has made two prominent changes

visible in Grameen’s financial statements between 2002 and 2008:

1. Grameen accepted an increased amount of savings deposits from members (28% CAGR1 over

2003-08) and started accepting deposits from non-members in 2003 to finance its bank operations

(55% CAGR over 2003-08)

2. Grameen has been increasing fixed deposit investments in commercial banks in Bangladesh to

take advantage of higher interest rates on high-value fixed deposits (40% CAGR over 2003-08).

It has done this instead of disbursing the capital as loans. In comparison, Grameen’s loan

portfolio grew at a high CAGR of 22% over 2003-08; but this was much slower than its growth

rate in fixed deposits.

Table 1: Grameen Balance Sheet Analysis 2003 and 2008

In Taka billion 2003 Percentage of

Total Assets

2008 Percentage of

Total Assets

CAGR

2003-08

Loan Portfolio 16.1 59% 44.4 54% 22.0%

Fixed Deposits in Banks 5.3 20% 28.5 34% 40.0%

Member Deposits 10.1 37% 35.1 42% 28.2%

Non-Member Deposits 3.3 12% 29.5 36% 55.0%

Total Assets 27.1 82.8 25.0%

Source: Grameen Bank Audited Financial Statements

1 CAGR – Compounded Annual Growth Rate

P a g e | 4

These financing and investment decisions impact the capital adequacy ratios of the bank. In

recent years, the bank’s capital ratio to risk-weighted assets has been declining in recent years. This

suggests that Grameen is increasing its portfolio of risky assets faster than it is increasing capital. To

avoid this, Grameen should strive to earn and maintain profits.

In this paper, we will elaborate on what the increase in savings deposits and fixed-deposit

investments means for Grameen Bank today and in the future. We will explain how Grameen is pursuing

this strategy while other MFIs in Bangladesh are not. We will then explore the possible reasons behind

increasing financing from deposits as well as increasing investment in fixed-deposits and analyze its

impact on capital adequacy ratios. It will be shown that there are a variety of good reasons for increasing

savings deposits. However, the increase in fixed-deposits suggests a more mature market for microfinance

that will pose challenges for maintaining profits in the future. Ultimately, we will argue that these changes

have impacted Grameen’s capital adequacy and may require Grameen new strategies to improve capital

adequacy.

P a g e | 5

Increased Savings Deposits: A Changing

Funding Profile

Since the implementation of the Grameen Generalised System, Grameen has increased the

amount of savings deposits from members and non-members. These increases were the result of two

decisions made by the bank beginning in the mid-nineties. The first decision was to eliminate foreign

donations. In his book Banker to the Poor, Prof. Muhammad Yunus clearly lays out his aversion to

accepting donor money from foreign organizations such as the World Bank because of the degree to

which these foreign actors attempt to shape the operations of Grameen (Yunus, Banker to the Poor, p.

144). For most of its existence, the Grameen Bank financed its operations through borrower deposits,

loans from international organizations and banks, and from donations. Seeking greater independence from

the influence of foreign donors, Grameen stopped requesting donor money in 1995. The year 1998

marked the last year when Grameen received donor money (Yunus, Microcredit: Banking With the Poor

Without Collateral, 2006, p. 3). Since then, Grameen has relied almost entirely on borrower deposits and

local loans.

The second decision was to increase emphasis on non-member savings. In 2000, Grameen

incorporated a variety of new savings products targeted at members (i.e. borrowers) as well as non-

members (Wahab, 2003, p. 6). These products included the Grameen Pension Scheme as well as longer

term deposits such as the Double-in-7-years deposit scheme.

As Grameen abandoned foreign money and relied more on member and non-member savings, the

amount of deposits with the bank grew. The amount of total deposits increased from Tk 9.8 billion to Tk

68.3 billion2 between 2002 and 2008, representing an almost six-fold increase. However, over the same

time period, debt from other sources and equity remained relatively constant, as can be seen in Chart 1.

These changes resulted in Grameen funding itself more and more from depositor money only.

Chart 1: Grameen’s Historical Funding Profile

Source: Grameen Bank Audited Financial Statements

2 1 USD = 68 taka. All values pulled from the audited financial statements of the Grameen Bank from 2002 through 2008. Copies

are available online at www.grameen.com or in the annual reports.

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2002 2003 2004 2005 2006 2007 2008

In million

Taka

Borrowings from Banks Member Deposits

P a g e | 6

A traditional retail bank accepts savings deposits from consumers to finance its operations. The

bank pays depositors for the right to use money by promising an interest payment. The bank then takes

the money it has acquired in savings accounts and lends the money to others. Borrowers are charged

interest rates on their loans that are higher than the interest rates on savings deposits. The difference

between the two interest rates, commonly referred to as a spread, is used to cover the operating expenses

of the bank.

Most MFIs do not function like traditional banks in that they rely on grants or low interest loans

from development agencies to lower the cost of borrowing. Now, without donor money, Grameen Bank is

attempting to survive on this spread between interest income and interest expense. Grameen borrows

money from members and non-members and promises interest rates ranging from 8.5% to 10.4%.

Without donations, Grameen needs to ensure that its money lending generates several percentage points

more than 10.5% in order to cover the cost of lending as well as any additional operational costs.

P a g e | 7

Increased Fixed-Deposits: Deployment of

Capital

In addition to increasing savings deposits, Grameen Bank also increased its investment in fixed

deposit accounts at Bangladeshi Banks between 2002 and 2008. During the period, the amount of total

investments grew from Tk 4.0 billion to Tk 28.7 billion, representing a six-fold increase.

Chart 2: Allocation towards Loans & Advances and Investments in FDs

Source: Grameen Bank Audited Financial Statements

With a current loan balance of Tk 45.5 billion and investments totaling Tk 28.7 billion, Grameen

is essentially investing 63 cents in banks for every $1 it lends to the poor. In 2002 the rate was closer to

46 cents. This is a much higher ratio than comparable MFIs and even some western banks. The table

below compares the investment-to-lending ratio of the Grameen Bank in 2007 with the rates of other

banks. As can be seen below, Grameen invests more per dollar-lent than its primary competitor MFIs and

more than many US Banks.

Table 2: 2007 Savings Deposits/Money Lent at Major Microfinance and American Banks

Grameen ASA BRAC Bank of

America

Wells

Fargo

Capital

One

Washington

Mutual

US

Bancorp

Financial

Service

Group

65% 6% 0% 64% 32% 32% 18% 22% 10%

Source: Audited financial statements in annual reports from all organizations.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

2002 2003 2004 2005 2006 2007 2008

Loans and Advances Investments in FDs

Growth in Loans Growth in FDs

P a g e | 8

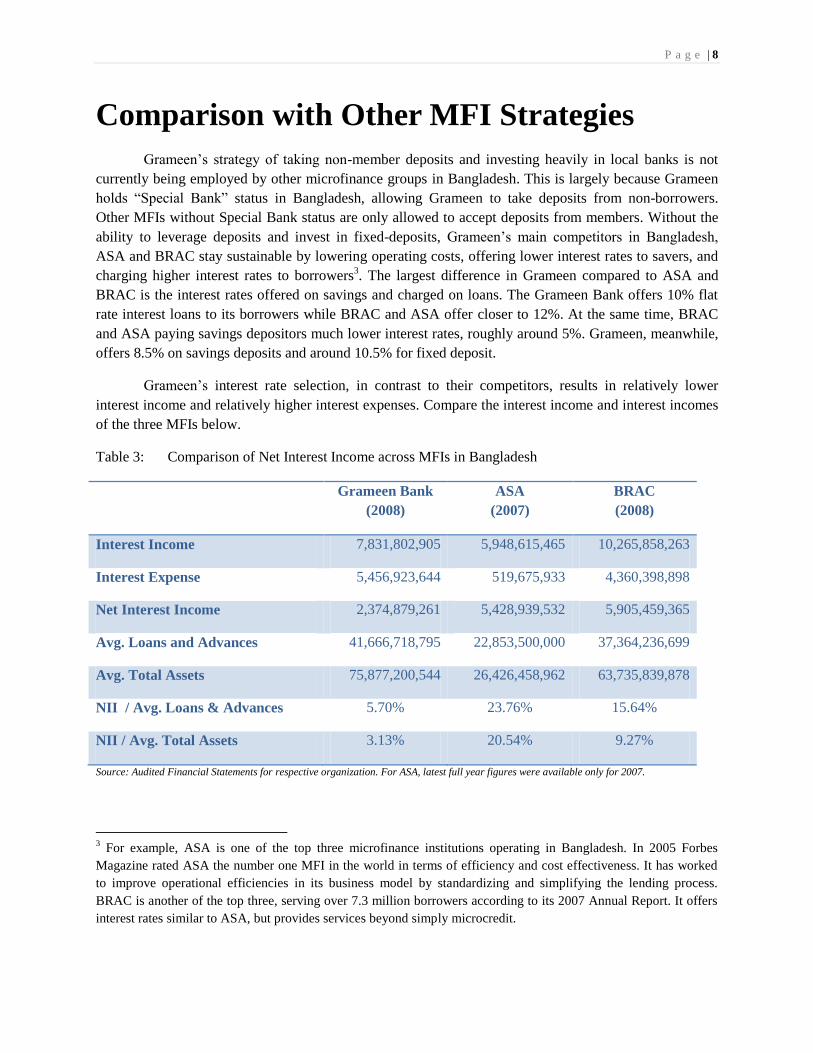

Comparison with Other MFI Strategies

Grameen’s strategy of taking non-member deposits and investing heavily in local banks is not

currently being employed by other microfinance groups in Bangladesh. This is largely because Grameen

holds “Special Bank” status in Bangladesh, allowing Grameen to take deposits from non-borrowers.

Other MFIs without Special Bank status are only allowed to accept deposits from members. Without the

ability to leverage deposits and invest in fixed-deposits, Grameen’s main competitors in Bangladesh,

ASA and BRAC stay sustainable by lowering operating costs, offering lower interest rates to savers, and

charging higher interest rates to borrowers3. The largest difference in Grameen compared to ASA and

BRAC is the interest rates offered on savings and charged on loans. The Grameen Bank offers 10% flat

rate interest loans to its borrowers while BRAC and ASA offer closer to 12%. At the same time, BRAC

and ASA paying savings depositors much lower interest rates, roughly around 5%. Grameen, meanwhile,

offers 8.5% on savings deposits and around 10.5% for fixed deposit.

Grameen’s interest rate selection, in contrast to their competitors, results in relatively lower

interest income and relatively higher interest expenses. Compare the interest income and interest incomes

of the three MFIs below.

Table 3: Comparison of Net Interest Income across MFIs in Bangladesh

Grameen Bank

(2008)

ASA

(2007)

BRAC

(2008)

Interest Income 7,831,802,905 5,948,615,465 10,265,858,263

Interest Expense 5,456,923,644 519,675,933 4,360,398,898

Net Interest Income 2,374,879,261 5,428,939,532 5,905,459,365

Avg. Loans and Advances 41,666,718,795 22,853,500,000 37,364,236,699

Avg. Total Assets 75,877,200,544 26,426,458,962 63,735,839,878

NII / Avg. Loans & Advances 5.70% 23.76% 15.64%

NII / Avg. Total Assets 3.13% 20.54% 9.27%

Source: Audited Financial Statements for respective organization. For ASA, latest full year figures were available only for 2007.

3 For example, ASA is one of the top three microfinance institutions operating in Bangladesh. In 2005 Forbes

Magazine rated ASA the number one MFI in the world in terms of efficiency and cost effectiveness. It has worked

to improve operational efficiencies in its business model by standardizing and simplifying the lending process.

BRAC is another of the top three, serving over 7.3 million borrowers according to its 2007 Annual Report. It offers

interest rates similar to ASA, but provides services beyond simply microcredit.

P a g e | 9

Even though Grameen is lending more to its borrowers than BRAC and ASA, its interest income

is much lower than that of BRAC and only slightly higher than that of ASA. To an extent, this can be

attributed to that fact that Grameen charges a lower interest rate to borrowers compared to BRAC and

ASA.

Simultaneously, Grameen’s interest expense is significantly higher than that of BRAC and ASA.

In recent years, Grameen has increasingly tapped member and non-member deposits by offering high

deposit rates.

The above table also shows Net Interest Income as a percentage of Average Loan and Advances

and Average Total Assets. ASA’s lower base of assets and a relatively higher value of net interest income

give it the highest ratios. However, Grameen Bank’s lower net interest income and a huge balance sheet

result in much lower ratios.

The below chart shows Grameen’s dependence on deposits compared to its competitors.

Chart 3: Comparison of the funding composition for Grameen, ASA, and BRAC 2007

Source: Audited Financial Statements of respective organization

In 2007 Grameen Bank had deposits and other funds in excess of Tk 51 bn. This amount alone

was greater than the total value of the liabilities and equity of ASA and BRAC, valued at Tk 28.8 bn and

Tk 42.3 bn respectively. Grameen’s efforts to fund operations more through member and non-member

deposits has resulted in the organization taking on significantly more deposits than other MFIs in

Bangladesh.

If this is an effort to function more like a traditional bank, Grameen has achieved its objective and

more with regards to raising funds through deposits; in fact, the bank has even taken on more deposits

relative to total assets than some of the western banks.

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Grameen 2007 ASA 2007 BRAC 2007

In millions TakaEquity Debt Deposits

P a g e | 10

Chart 4: Savings Deposits as a Percentage of Total Assets

Source: Audited Financial Statements of respective organization

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Grameen Bank

2007

ASA 2007 BRAC 2007 IDF 2007 Bank of

America 2007

Wells Fargo

2008

Washington

Mutual 2006

P a g e | 11

Rationale for Grameen’s Financing Strategy

Grameen’s financing does assist the organization in achieving many of its stated objectives

through deposits of borrowers and domestic non-borrowers. First, it allows the Grameen Bank to remain

independent of foreign donations and foreign lenders. In interviews with officials at the Grameen Bank

and other MFIs, there is a general consensus that foreign donations and money have downsides. MFIs that

are dependent on donor money must listen and react to the whims of donors and lenders. As such, they

may not be able to run the MFI in a way that bests suits the interest of the poor.

Borrowing locally also allows the MFI to avoid foreign currency exposure risk. MFIs that do

borrow from foreign sources suffer gains or losses related to currency fluctuations if the loan terms

require repayment in a foreign currency. For example, let us say that a Bangladeshi MFI borrows money

from a foreign source in US dollars at 0% interest and promises to repay the loan in a year. If the value of

the US dollar increases 5% relative to the Bangladeshi Taka during the course of the year, then the

effective rate that the MFI will pay will be 5%. By borrowing locally, the MFIs avoid this currency

exposure.

Most importantly, the Grameen Bank’s interest rate spread allows the poor borrowers to keep

more of their money. With lower interest rates on the loans, the borrowers are able to keep more of their

profits. With higher interest rates on savings, members earn a greater return on their investments. The

strategy allows more money to go to the poorest of society.

P a g e | 12

Rationale for Grameen’s Investment Strategy

Grameen’s decision to deploy capital towards investments in fixed deposits rather than issuing

new loans begs the question “Why?”4 If Grameen is a bank with the stated objective of providing more

loans to the poor, why not use this money to provide more loans? Why does Grameen place a substantial

amount in fixed deposits? The following theories could explain the decision:

1. Expansion is a Slow Process: If it takes time to find a market for new lending, Grameen could be

placing money in investments until new opportunities open up. If this is the case, one would expect

the amount of investments to decrease and new loans to increase as soon as new borrowers are

identified.

Can new borrowers be identified? It is possible. Grameen does not yet have permission from the

Bangladesh government to provide loans to the poor within the urban areas of Dhaka and other cities

in the country. With Dhaka alone having a population of 12 million people, the area could offer a

couple more million borrowers. Loans provided to these borrowers would easily cover the extra cash

in deposits.

2. Maintain Liquidity: While Grameen may want to provide more loans, loans are not as liquid an asset

as fixed deposit accounts. In the event that Grameen needs cash – for example, the extreme event of a

run on the bank – it would be difficult for Grameen to collect on outstanding loans. Fixed deposits,

however, can simply be closed down and the entire value of the deposit withdrawn (less an

insignificant penalty fee at worst).

3. Market Saturation: It is possible that Grameen is reluctant to invest more money lending to the market

because the target market of reliable borrowers is oversaturated with microfinance loans. The market

is currently served by numerous MFIs. The Bangladesh Microcredit Regulatory Authority Act of

2006 required MFIs to apply for official status with the government by February 26, 2007. 4,236

separate organizations applied for certification and 705 are currently being considered. The

Bangladesh Bank also estimates an overlap rate of 40% of the 30 million outstanding loans in 2006

(Bangladesh Bank).

Some simple math based on population estimates further hints at market saturation of the

Bangladesh microfinance market. In 2008, the combined number of borrowers of Grameen, ASA, and

BRAC was roughly 23.03 million5. This is roughly one-seventh of the total population of 156 million

(CIA the World Factbook, 2009), but it is important to remember that the total population of

Bangladesh is not eligible for microcredit loans. Grameen, BRAC, and ASA borrowers must fulfill

two criteria: be poor and be female. If you limit the population to women and the poor, the

4 It is also important to note how Grameen Bank decides whether to invest in fixed-deposits or to lend more money. No branch

office ever makes this decision directly; they simply issue loans to as many borrowers as they can. At the end of the day, any cash

in excess of a predetermined amount is transferred to the higher offices. The head office is ultimately the one that decides to

invest in fixed deposits. 5 Borrowers estimates from BRAC Annual Report 2008, Grameen Monthly Reports on the Grameen Website, and ASA New

Vision newsletter.

P a g e | 13

microfinance market size in 2009 would be roughly 35 million. Limiting the number even further to

discount women aged 14 and younger and 60 and older, the total market size becomes 17.2 million.

The reported number of 23.03 million borrowers shared between the three major MFIs indicates that

they serve about 1.4 times the current market size6.

4. Operating Costs Associated with Deploying More Loans Make Loans Cost Prohibitive: Even if the

market is not saturated, the costs of setting up new loans may be cost prohibitive. Reaching new

groups of borrowers may require opening new branches and paying new employees. MFI lending is

typically more expensive than traditional banking. Although labor costs are lower than in western

countries, branches can be located far from urban centers. Moreover, loan officers must physically

travel to visit lenders in order to collect. It could be that the cost of setting up new banks is not

worthwhile.

5. Spread on Loans Alone is Not High Enough to Cover Operating Costs: The low interest rate on the

loans and the high interest rate on savings may not create a large enough spread to cover the operating

expenses of the Grameen Bank. Discovering whether or not this is true is difficult from audited

financial statements alone because Grameen’s financing supports two different income generating

activities: lending and investing. One cannot simply subtract investment income from net profit to

determine if lending alone is profitable because some portion of Grameen’s interest expense is

attributed to earning investment income. In order to get a more accurate estimate of the sustainability

of lending, the following steps were taken:

a. Interest income is still included as this income is derived from lending activities.

b. A weighted interest expense was created that takes into account only interest expense

associated with lending. Since a portion of Grameen’s financing supports investments in

fixed deposits, the entire interest expense cannot be used. Income expense multiplied by the

ratio of loans outstanding to total assets7.

c. Total operating expenses and are still used since it is assumed expenses associated with

investment are inconsequential. Investments in fixed-deposits are done at the headquarters of

Grameen and not at the branch level.

d. Loan loss provisions are still included as this is all generated from lending activities.

The below chart shows Grameen Net Profit with the above adjustments

6 Estimates of ratio of women and age based on census data from the Bangladesh Bureau of Statistics 7 The ratio of loans outstanding/total assets is used as an approximation.

P a g e | 14

Chart 5: Net Profit of Grameen Less Income from Investments with Weighted Interest Expense

Source: Grameen Bank Audited Financial Statements

This chart suggests that Grameen is not generating enough money from lending alone to cover

operating and financing expenses and that the bank has come to rely more and more on fixed deposits to

cover expenses.

Relying on income from fixed deposits to cover costs may pose challenges for Grameen going

forward. That is because commercial banks in Bangladesh have recently reduced interest rates on fixed

deposits and may do so again in the future.

Chart 6 provides more information about the trend in short and long-term interest rates over the

past two years. As can be seen, the interest rates at all maturities are significantly lower for the June 2009

period as compared to August 2007. It should be noted that the interest rate curve is upward sloping i.e.

shorter term maturities have lower interest rates compared to longer term maturities.

Chart 6: Bangladesh Bank interest rates trend

Source: Bangladesh Bank Website

(2,000)

(1,500)

(1,000)

(500)

0

500

2001 2002 2003 2004 2005 2006 2007 2008

Millions TakaNet Profit

3.0%

4.5%

6.0%

7.5%

9.0%

10.5%

12.0%

13.5%

15.0%

16.5%

91-day 182-day 364-day 5-year 10-year 15-year 20-year

Jun-09 Dec-08 Jun-08 Dec-07 Aug-07

P a g e | 15

In April 2009, the Central Bank of Bangladesh pressured commercial banks to cap interest

payments at 13% with many banks settling on fixed deposits between 9 and 9.5% (Islam, 2009). Lower

interest rates on fixed-deposits means lower profits for Grameen’s investments. With fixed deposit rates

closer to the cost of borrowing associated with borrower savings deposits, Grameen will not be able to

cover many more additional expenses beyond the cost of borrowing.

The current maturity structure of Grameen suggests that Grameen is not taking full advantage of

the highest interest rates offered by longer term investments. Table 4 compares the maturity structure of

Grameen’s investments in 2003 with 2008. In 2003, more than 20% of its investments were in maturities

over 1 year, whereas currently only 1% of its investments have a maturity of over 1 year. This has now

been replaced by increased investments in the maturities of <3 months (now representing 25% of

portfolio). It may seem that most of the long-medium term investments from 2003 are now maturing (and

therefore the increased level of investments in the near term maturities). However, with just 1% of the

investment in the longer term maturities in 2008, this seems to be a conscious strategy from Grameen’s

perspective to invest more in the near term maturities. This trend does not seem to be favorable for

Grameen given that the interest rates in the shorter maturities are a lot lower than those in the more than 1

year maturity (see Chart 6).

Table 4: Maturity Structure of Investment Portfolio

2003 2008

< 1 month 4% 11%

>1 and <3 months 5% 14%

>3 and <1 year 71% 74%

>1 year and < 5 years 20% 1%

Total value Tk 5.3 billion Tk 28.7 billion

Five theories have been explored for why Grameen is investing in fixed-deposits. The first two

theories would be the best case scenarios for Grameen. Either the current investment decisions are a

temporary necessity before more loans are deployed or a permanent necessity to maintain liquidity. The

other three theories hint at a more challenging future for Grameen Bank. Only the directors of Grameen

can explain the reasons behind their decisions. If the latter three theories are the cause, Grameen will need

to investigate strategies for remaining profitable with higher costs, lower returns on investment, and a

saturated, mature market.

P a g e | 16

Impact of Grameen’s Strategy on Capital

Adequacy

Regardless of the rationale for the strategy, the increase in member and non-member savings

coupled with increased fixed-deposits has made Grameen less solvent than in past years. One of the most

important measures of the solvency and stability of traditional banks is the level of total capital balances

relative to assets. The Total Capital ratio is a comparison of capital with risk-weighted assets, and not

total assets8. Under risk-weighted assets, various assets such as cash, loans, investments, etc. are allotted

different weights based on their level of riskiness with riskier assets receive a higher weighting. This

method is followed under the Basel I and II capital standards. All regulatory institutions require banks

that are under their supervision to report these capital adequacy ratios and maintain them at certain

required levels.

Grameen’s performance in this ratio has declined in recent years. At this time Grameen is not

required to adhere to any strict capital requirements that would mandate a minimum capital ratio.

However, Grameen sets its required capital to risk weighted assets at a minimum of 10%9. Chart 7 shows

Grameen’s Total Capital ratio has declined steadily ever since the bank experienced tremendous growth

in fixed deposits and loans backed by a large increase in non-member deposits. While Grameen’s Total

Capital ratio has not passed the minimum desired capital ratio of 10%, it is likely if annual growth rates of

RWAs and Total Capital continue at their current rate.

Chart 7: Grameen Bank Total Capital Ratio

Source: Grameen Bank Audited Financial Statements

The below chart depicts the annual growth in the values of RWAs and Total Capital. Over 2003-

08, Grameen’s RWAs grew at 23% CAGR per annum, while Total Capital grew only at 12% CAGR.

8 Total Capital Ratio = { Tier 1 Capital (Core Capital) + Tier 2 Capital (Supplementary Capital)} / Risk Weighted Assets

19.30%

16.51%

13.41%14.38%

12.43% 12.02%

5%

10%

15%

20%

2003 2004 2005 2006 2007 2008

Total Capital Ratio

Minimum Desired Capital Ratio

10%

P a g e | 17

Chart 8: Annual Growth in Risk-Weighted Assets and Total Capital

Source: Grameen Bank Audited Financial Statements

If RWAs do continue to grow at a faster rate than total capital, the amount of RWAs will exceed a

threshold and the Total Capital Ratio will drop below 10%.

Keeping the Total Capital Ratio above 10% would require decreasing RWAs or increasing

Capital. Since Grameen is in the business of lending to the poor, decreasing RWAs is unlikely in the

future. This leaves Grameen with the option of increasing Capital. Understanding how to increase capital

requires understanding what constitutes Capital.

Chart 9 provides the composition of Grameen’s Total Capital while Table 4 gives the breakdown

of capital and other reserves in 2008.

Chart 9: Composition of Total Capital

Source: Grameen Bank Audited Financial Statements

22%

33%

26%

15%

21%

5%8%

35%

-1%

17%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

2004 2005 2006 2007 2008

Growth in RWAs Growth in Total Capital

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2003 2004 2005 2006 2007 2008

6% 7% 6% 5% 5% 4%

94% 90% 85%82% 79% 74%

0% 4% 8% 12% 15% 20%General Provisions

Retained Surplus

Capital and Other Reserves

Paid up Capital

P a g e | 18

Table 4: Breakdown of Capital and Other Reserves as at December 2008

In million Taka 2008 Addition in 2008 Percentage of Total

Capital Reserve 4,280,410 0 71.7%

General Reserve 1,044,000 716,000 17.5%

Proposed Dividend 107,400 43,800 1.8%

Dividend Equalization Fund 421,854 -244,146 7.1%

Other Reserves 115,773 0 1.9%

TOTAL 5,969,437,278 515,654

Source: Grameen Bank Audited Financial Statements 2008

As seen in the above chart and table, the two major contributors to Capital and Other Reserves are

Capital Reserve and General Reserve. Capital and Other Reserves contribute >70% to total capital from

2003 until 2008. During this time the General Provisions have increased in size over the years.

The Capital Reserve constitutes more than 70% of the total of Capital and Other Reserves

account, and according to the 2008 Notes to Financial Statements, a majority portion of the Capital

Reserve represents revolving funds and grants that are no longer refundable. So, this seems to represent

funds that would permanently remain with Grameen. Most importantly, this means these funds are not

likely to grow.

General Reserve is the other account which Grameen can increase in value in order to solidify its

capital base. The contributions to General Reserve are from apportionments made from Net Profits earned

in any particular year. Growing Capital, therefore, requires that Grameen earn and retain profits year over

year.

P a g e | 19

Recommendations to Improve Profitability

and Capital Adequacy

If Grameen attempts to increase capital in order to maintain and strengthen its capital base it

would have to increasingly contribute to the General Reserve (via its income statement). This requires

greater profitability on the part of the bank.

There are several strategies that would enable Grameen to strengthen its capital ratios, either by

improving profitability or through other means:

1. Decrease dividend payments

Since 2006 Grameen has offered generous dividend payments to shareholders. In the first year

Grameen offered a 100% dividend payment. In subsequent years it lowered to 20% and 30%. While

popular among shareholders, repeated large dividend payments increase Grameen’s cost of capital.

Compare below a hypothetical situation in which Grameen issues sells Tk 100 worth of shares

and issues Tk 100 worth of debt. The interest on the debt will be 17%. In years 1, 2, and 3, Grameen will

offer dividend payments identical to those paid in 2006, 2007, and 2008 (100%, 20%, and 30%). Netting

the values of the cash flows in both cases yields -50. Essentially, the affect of the equity was the

equivalent of a loan with 17% annual interest.

Year 0 Year 1 Year 2 Year 3 Net Value

Loans 100 -17 -17 -117 -50

Equity 100 -100 -20 -30 -50

Grameen must also be wary of paying out additional dividend payments year over year in the

event that it issues new shares. Excessive payments will further drive up the cost of capital.

2. Widen the spread on loans and deposits

This solution would likely be the most controversial for Grameen Bank. For many years Grameen

has prided itself on the more favorable interest rates that it offers to borrowers. However, if the core

business of Grameen is unsustainable, the organization will always encounter problems with profitability.

If Grameen borrows and loans at a loss, it will always require additional sources of income. It will need to

generate enough money to cover the loss associated with lending in addition to any expenses incurred

while pursuing side businesses.

Increasing the spread would require Grameen to either increase the interest rates on loans or

lower the interest on savings deposits. Lowering interest paid on savings may be the least controversial

way of achieving this objective. Grameen could limit the number of high interest savings deposits that it

offers.

P a g e | 20

It is worth noting that an adjustment of interest rates does not indicate a failure of microfinance.

The value of the interest rates does not affect the core tenant of microfinance – that poor people can be

relied on to repay loans.

3. Equity Investments

Interest rates on fixed deposits may have declined, but Grameen may be able to find comparable

returns by taking equity investments in other companies. Grameen Phone famously provided a wonderful

return to Grameen and other Grameen organizations that had shares in the joint venture. While every

equity investment cannot be expected to perform as well, equity investments would offer the potential of

greater returns, in addition to the social benefit of improving industry within Bangladesh.

4. Microenterprise Loans

Since adopting the Grameen Generalised System earlier this decade, Grameen has increased its

focus on providing microenterprise loans. These loans have a much higher average loan value (between

Tk 15,000 – 50,000) compared to the traditional microfinance loan (Tk 5,000).

Grameen’s microenterprise loan portfolio has grown at a CAGR of 113% between June 2002 and

June 2009. Over this period, Grameen has disbursed loans worth Tk 47.5 billion and collected worth Tk

37.5 billion.

The below chart shows the Number of Loans Disbursed and the Average Value of Loans

Disbursed over six month intervals between Dec’02 and Jun’09. As can be seen, the number of loans

disbursed during each such interval has increased from about 110,000 to 250,000 over this period, with a

simultaneous increase in the average value of loans disbursed from about Tk 22,000 to Tk 30,000.

Chart 7: Analysis of Grameen’s Microenterprise Loans

Source: Monthly Reports on Grameen Bank Website

Grameen should continue to focus on these microenterprise loans in order to boost it interest

income and thereby its profitability. However, increase in this loan portfolio will cause a concurrent

increase in Grameen’s RWAs and thereby may affect its capital ratios negatively. Further analysis in this

regard is recommended.

15,000

18,000

21,000

24,000

27,000

30,000

-

50,000

100,000

150,000

200,000

250,000

300,000

Dec

-02

Jun

-03

Dec

-03

Jun

-04

Dec

-04

Jun

-05

Dec

-05

Jun

-06

Dec

-06

Jun

-07

Dec

-07

Jun

-08

Dec

-08

Jun

-09

Number of Loans Disbursed (LHS)

P a g e | 21

5. Paid-up Capital

Issuing new shares to the poor would also help Grameen generate additional capital. The

Ordinance under which Grameen Bank was established restricted Grameen’s authorized capital to Tk 500

million. However, it was only recently, in 2008, that Grameen was able to convince the government that it

required an increase of its authorized capital limit to Tk 3,500 million. This had become imperative

because Grameen had grown its member base from about 2.3 million in 1999 to 7.7 million in 2008.

Grameen provides an option to all its members to purchase shares of Grameen Bank – at a

nominal price of Tk 100 per share. The members also have an option to purchase more than one share if

they so desire. With an authorized capital limit of Tk 500 million, Grameen would have been able to

satisfy the demand for shares of a maximum of 5 million members, a figure that it crossed in 2005. With a

membership of more than 7 million now, Grameen convinced the government to allow an increase in its

authorized capital limit.

Thus, Grameen Bank can now increase its paid-up capital by issuing shares to its new members

or existing members who have not had a chance to participate in the share program. This would also

enable Grameen to shore up its capital based and thereby improve its capital ratios.

Conclusion

Grameen’s capital adequacy ratio indicates that Grameen does not face immediate or impending

solvency trouble, but it does urge caution. Given the maturing market, Grameen’s current strategy will

decrease the capital ratio below the 10% minimum in the coming years. Avoiding this would require

redefining its financing and investing strategies given changing circumstances. It means identifying a

strategy that will allow the bank to maintain sufficient levels of solvency. Several strategies to improve

solvency have been recommended, but the list of solutions is by no means exhaustive. Grameen should

consider the above recommendations while brainstorming other innovative approaches to addressing the

profitability of the bank. Improving profitability will ultimately benefit the poor – Grameen’s

shareholders and customers.

P a g e | 22

Bibliography

ASA. (2008). New Vision October-December 2008. Dhaka.

Bangladesh Bank. (n.d.). Retrieved July 21, 2009, from http://www.bangladesh-bank.org/

Bangladesh Bureau of Statistics. (2007, July 11). Bangladesh Data Sheet. Retrieved July 21, 2009, from

Bangladesh Bureau of Statistics: http://www.bbs.gov.bd/

CIA the World Factbook. (2009, June 26). Retrieved July 21, 2009, from

https://www.cia.gov/library/publications/the-world-factbook/geos/BG.html

Islam, S. (2009, June 21). All Headline News. Retrieved July 21, 2009, from

http://www.allheadlinenews.com/articles/7015558704

Monthly Report Archive. (2009, July 9). Retrieved July 21, 2009, from Grameen Bank:

http://www.grameen-info.org/

Morduch, B. A. (2005). The Economics of Microfinance. Cambridge: The MIT Press.

S.F. Ahmed and Co. (2009, March 17). Independent Auditor Report BRAC 2008. Dhaka, Bangladesh.

Wahab, A. H. (2003). Introduction to Grameen II. Dhaka: Grameen Bank.

Yunus, M. Banker to the Poor.

Yunus, M. (2006). Microcredit: Banking With the Poor Without Collateral. Dhaka: Grameen Bank.