Accounting Principles: A Business Perspective 9e Student prices ...

Upload

lydia-olsenCategory

view

30download

0description

FINANCIAL ACCOUNTINGFINANCIAL ACCOUNTINGA USER PERSPECTIVEA USER PERSPECTIVE

Hoskin • Fizzell • Davidson

Second Canadian Edition

Liabilities Liabilities

Chapter Nine

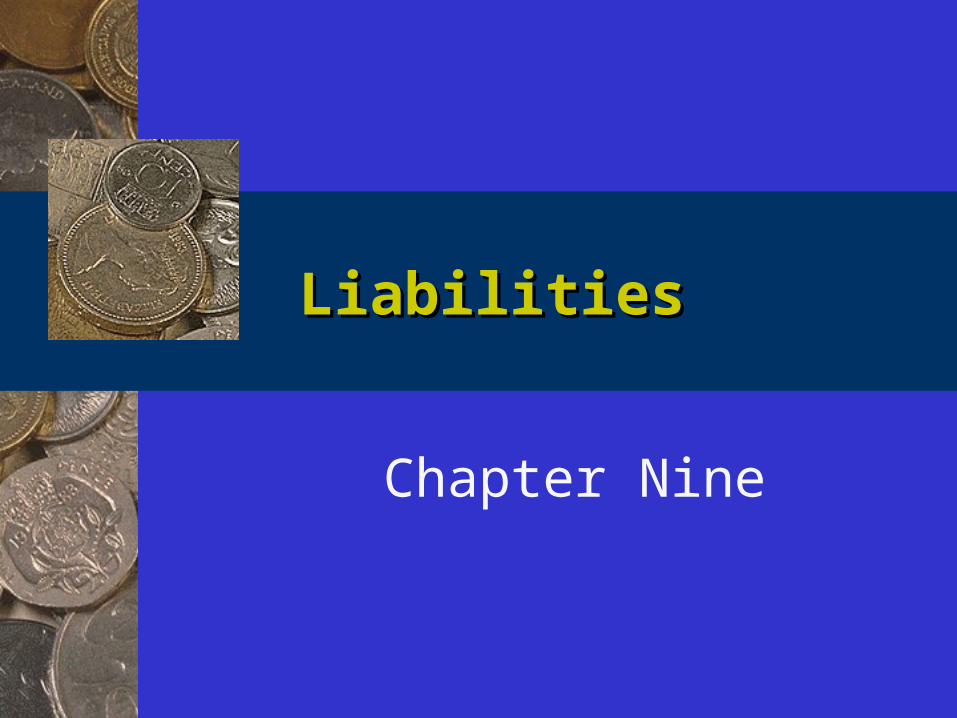

Recognition for Liabilities

• Classify as liabilities if– Transfer of assets or the delivery of

services or other benefits

– Company has little or no discretion

– Results from an event that has already occurred

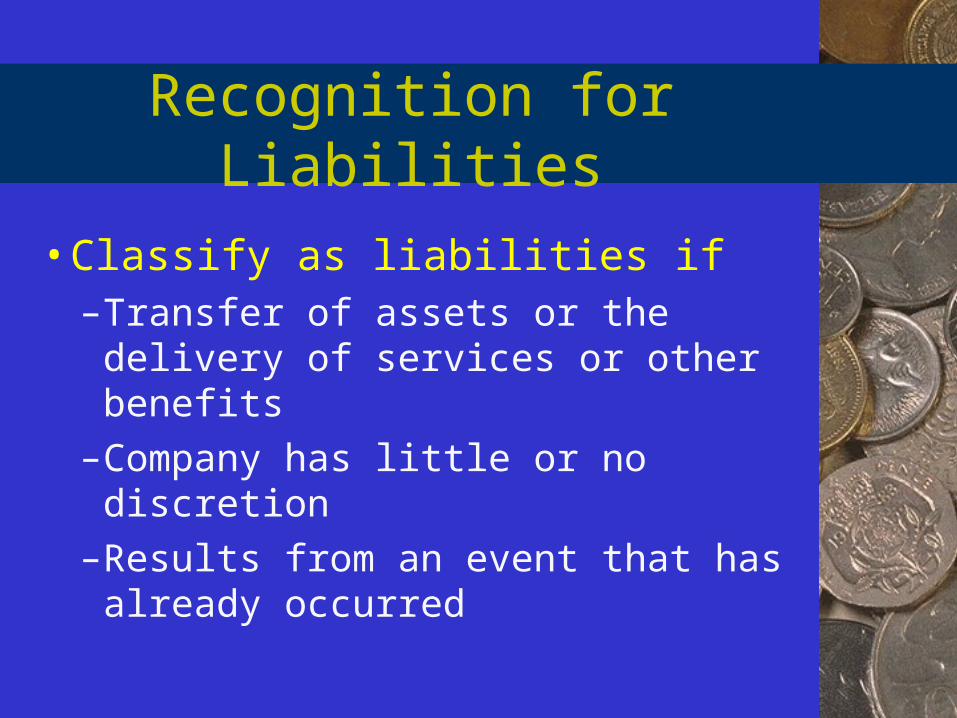

Contingent Liability

• If there is a possibility of the future transfer of assets, and

• If the future obligation is contingent on certain events occurring, then

• Company should disclose in a note to the financial statements

Valuation Methods

• Gross amount of the obligation– May not measure obligation

accurately

– Ignores the time value of money

Valuation Methods

• Net present value of the obligation– Recognizes the time value of money

– Future payments of principal and interest are discounted back to the current period using a discount rate

Valuation Methods

• Canadian practice– Record liabilities at the present

value of the future payments

– Exception: short-term liabilities

Working Capital Loans and Lines of Credit

• Short-term loan from a bank

• Secured by accounts receivable or inventory balances

• Results in negative cash balance

Accounts Payable

• Occur when goods or services are purchased on credit

• Called trade accounts payable• Payment deferred for 30-60 days• Generally do not carry interest

charges, unless payment is delayed

Wages and Other Payroll Payables

• Accrual of wages since the last pay period

• Fringe benefits– Health care, pensions, vacation pay

• Company acts as government agent in collecting taxes– Income taxes, CPP (QPP), EI, WCB

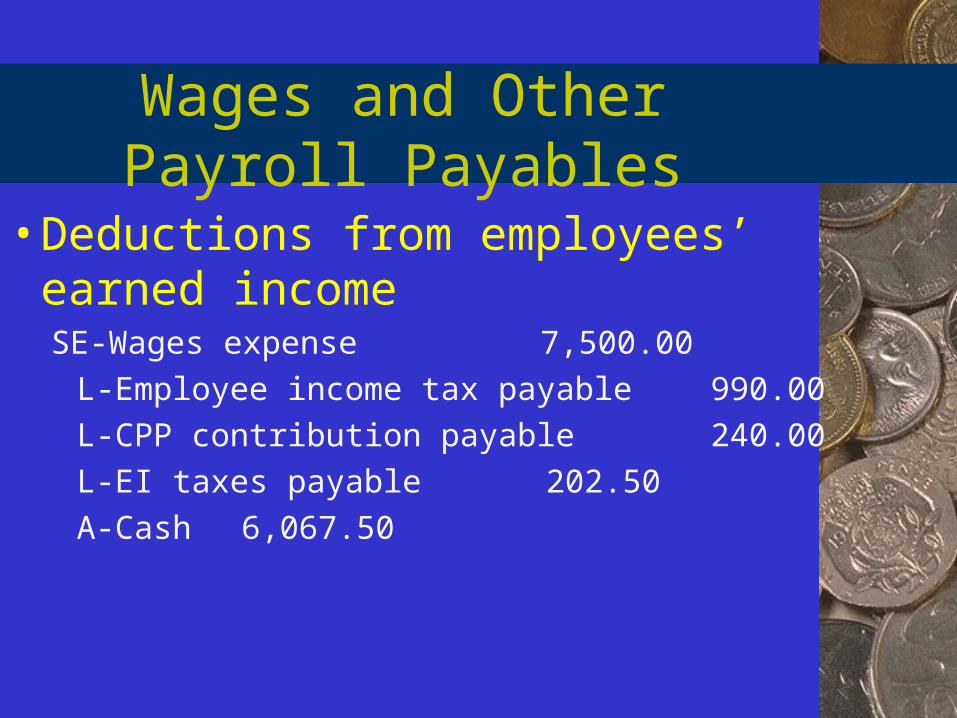

Wages and Other Payroll Payables

• Deductions from employees’ earned incomeSE-Wages expense 7,500.00

L-Employee income tax payable 990.00

L-CPP contribution payable 240.00

L-EI taxes payable 202.50

A-Cash 6,067.50

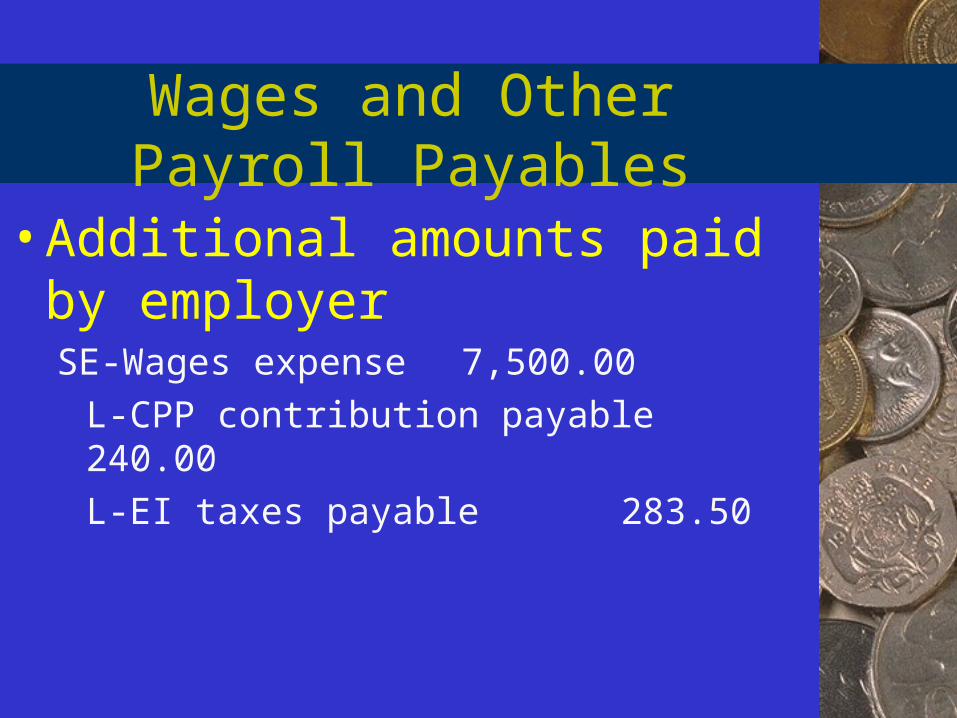

Wages and Other Payroll Payables

• Additional amounts paid by employerSE-Wages expense 7,500.00

L-CPP contribution payable 240.00

L-EI taxes payable 283.50

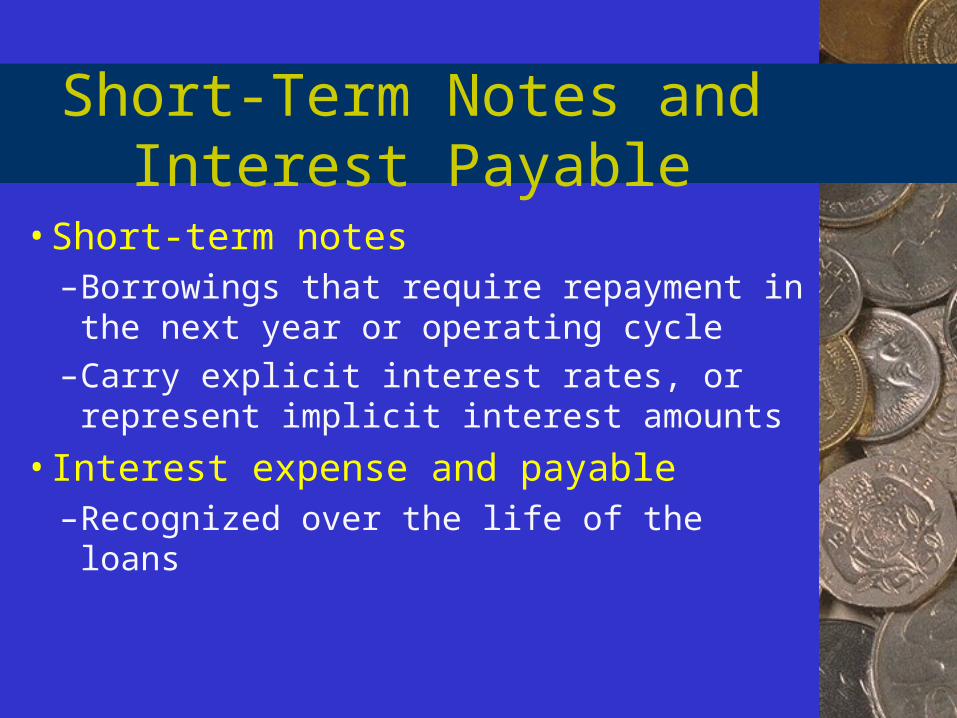

Short-Term Notes and Interest Payable

• Short-term notes– Borrowings that require repayment in the

next year or operating cycle

– Carry explicit interest rates, or represent implicit interest amounts

• Interest expense and payable– Recognized over the life of the loans

Short-Term Notes and Interest Payable

• Example: – Borrowing of $10,000 at 9%.– Six monthly payments of $1,710.70– Monthly instalments included reductions

of the principal, plus interest– Interest is calculated on the decreasing

amount of principal

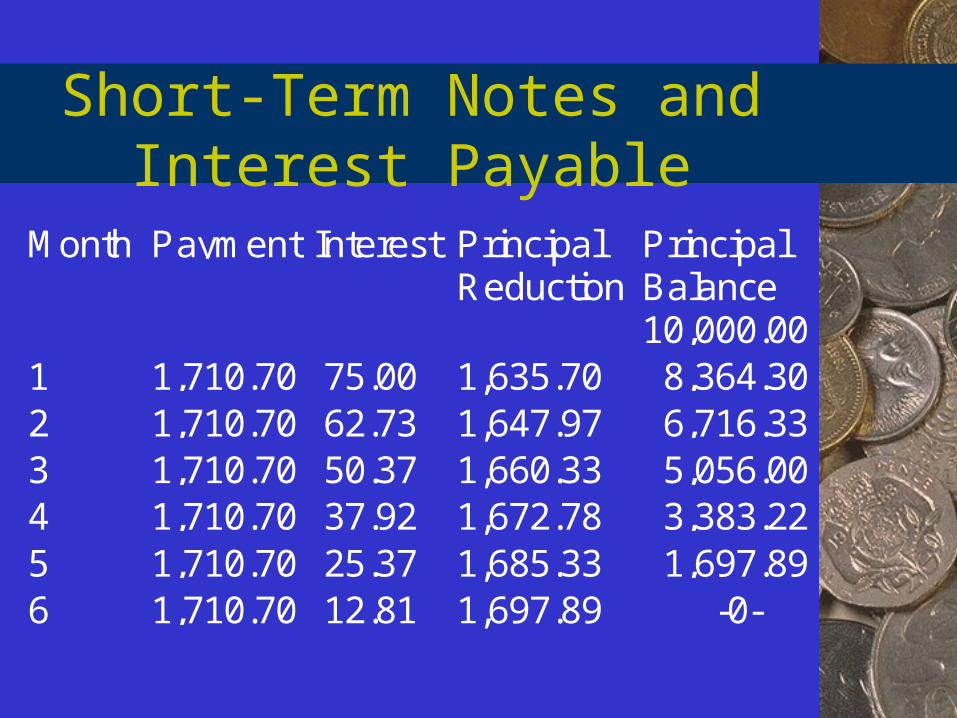

Short-Term Notes and Interest Payable

Month Payment Interest PrincipalReduction

PrincipalBalance10,000.00

1 1,710.70 75.00 1,635.70 8,364.302 1,710.70 62.73 1,647.97 6,716.333 1,710.70 50.37 1,660.33 5,056.004 1,710.70 37.92 1,672.78 3,383.225 1,710.70 25.37 1,685.33 1,697.896 1,710.70 12.81 1,697.89 -0-

Short-Term Notes and Interest Payable

• Entry at the end of the first monthSE-Interest expense 75.00

L-Short-term note payable 1,635.70

A-Cash 1,710.70

Income Taxes Payable

• Companies are subject to taxes– Federal corporate income taxes– Provincial corporate taxes

• Payment of taxes does not always coincide with the incurrence of the tax

• Results in taxes payable

Warranty Payable

• Goods or services sold may result in guarantees to the buyer

• May result in warranty service• Estimate the amount of warranty

expense to match to the revenue from the sale– Estimate % based on past history

Warranty Payable

• Record the estimated warranty obligation (in the period of the sale)SE-Warranty expense 460

L-Estimated warranty obligation 460

Warranty Payable

• Record the repair work (in the period when the work is done)L-Estimated warranty obligation 126

A-Cash 126

Unearned Revenues

• If customers are required to make downpayments prior to the receipt of goods or services

• Defer the recognition of revenue• Liabilities

– Unearned revenues, or – Deferred revenues

Current Portion of Long-Term Debt

• When long-term debt comes within a year of being due

• Must be reclassified as a current liability

Commitments

• Purchase commitment– An agreement to purchase items in

the future for a negotiated price

– Discuss in a note to the financial statements if material to future operations

Contingencies

• Contingent liabilities (losses)– When the incurrence of the liability

is contingent upon some future event– Examples

• Settlement of a lawsuit• Guarantee of another company’s loan

Contingencies

• In Canada, recognize a contingent loss if:– The use of assets or performance of

services are required

– The amount of the loss can be reasonably estimated

Deferred Taxes

• Differing calculations:– Income tax expense from the income

statement

– Income tax payable according to Revenue Canada

• Two methods: Liability method and Deferral method

Liability Method

• Focuses on the balance sheet

• Attempts to measure the liability to pay taxes in the future based on a set of assumptions about future revenues and expenses

Liability Method

• Calculate (pro forma) future income taxes payable based on temporary differences existing in the current period

• A liability in the current period will become a tax deduction as actual costs are incurred

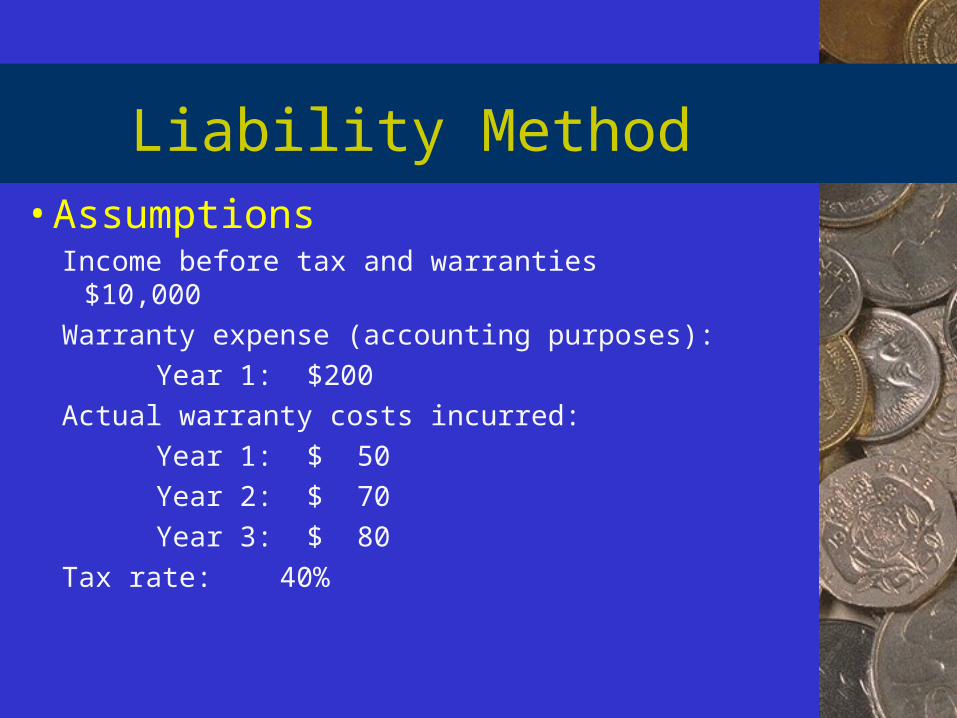

Liability Method• Assumptions

Income before tax and warranties $10,000

Warranty expense (accounting purposes):

Year 1: $200

Actual warranty costs incurred:

Year 1: $ 50

Year 2: $ 70

Year 3: $ 80

Tax rate: 40%

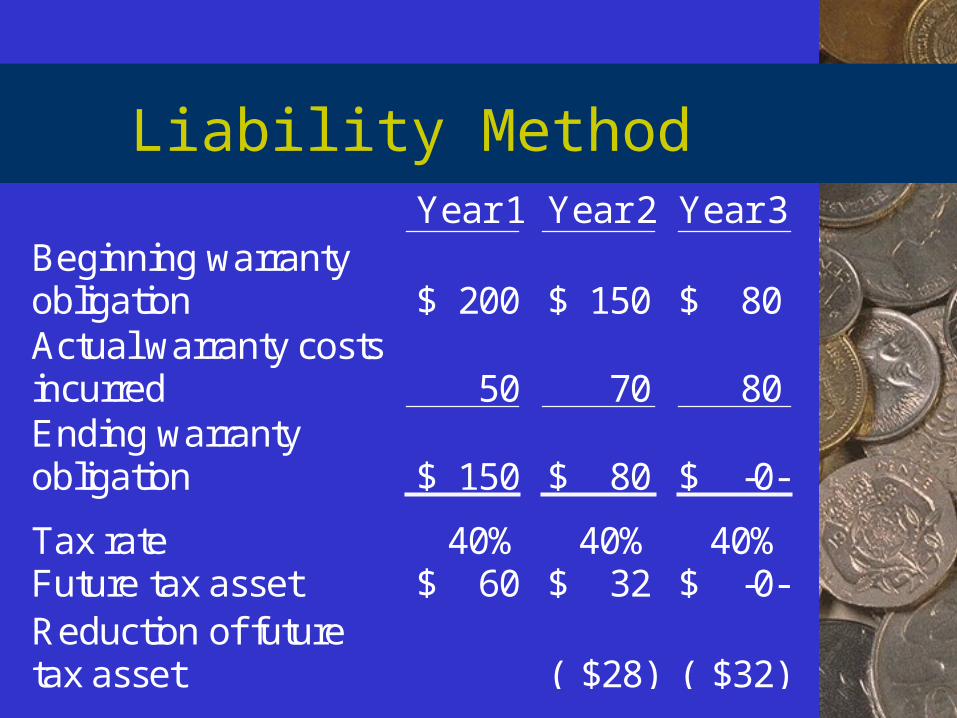

Liability MethodYear 1 Year 2 Year 3

Beginning warrantyobligation $ 200 $ 150 $ 80Actual warranty costsincurred 50 70 80Ending warrantyobligation $ 150 $ 80 $ -0-

Tax rate 40% 40% 40%Future tax asset $ 60 $ 32 $ -0-Reduction of futuretax asset ( $28) ( $32)

Liability MethodIncome tax payable: Year 1 Year 2 Year 3Income $10,000 $10,000 $10,000

Actual warrantycosts 50 70 80

9,950 9,930 9,920Taxes payable 3,980 3,972 3,968

$ 5,970 $ 5,958 $ 5,952

Taxes payable $ 3,980 $ 3,972 $ 3,968Future tax asset (60) 28 32Tax expense $ 3,920 $ 4,000 $ 4,000

Deferral Method

• Focuses on the income statement

• Tax expense is based on the recognized revenues and expenses on the income statement

• Uses the tax rates in effect in the current year

Deferral MethodTax expense: Year 1 Year 2 Year 3Income $10,000 $10,000 $10,000Warranty expense 200 -0- -0-

9,800 10,000 10,000Tax expense 3,920 4,000 4,000Net income $ 5,880 $ 6,000 $ 6,000

Taxes payable $ 3,980 $ 3,972 $ 3,968

Deferred taxes 60 (28) (32)

Differences

• Balance sheet focus

• Future tax rate

• Future reviews of tax assets and liabilities

• Income statement focus

• Current tax rate

• Deferred taxes drawn down; no periodic reviews

Liability Method Deferral Method

![Accounting] Vedika Software - Accounting User Guide (1998)](https://static.fdocuments.us/doc/165x107/546b5df0af795985298b4b6b/accounting-vedika-software-accounting-user-guide-1998.jpg)