Finance & Tax Seminar - SEIA | Solar Energy Industries ... Slides_2...Morgan Stanley Thomas...

61

Finance & Tax Seminar June 1 st -2 nd , 2017 New York, New York www.seia.org Thank You to Our Sponsors June 2, 2017 1

Transcript of Finance & Tax Seminar - SEIA | Solar Energy Industries ... Slides_2...Morgan Stanley Thomas...

Finance & Tax SeminarJune 1st-2nd, 2017

New York, New York

www.seia.org

Thank You to Our Sponsors

June 2, 2017 1

Welcome

Abby HopperPresident & CEO, SEIA

Master of Ceremonies

John MarcianoPartner, Akin Gump

Strauss Hauer & Feld LLP

Washington Update

William DavisTax Policy Counsel,

U.S. House of Representatives

Aruna KalyanamTax Counsel, House Committee on Ways and Means

Lee PetersonSenior Manager,

Renewable Energy, CohnReznick

ModeratorBrandon Audap

Director of Federal Affairs,

SEIA

Gregory JennerPartner, Stoel

Rives LLP

Finance & Tax SeminarJune 1st-2nd, 2017

New York, New York

www.seia.org

Thank You to Our Sponsors

June 2, 2017 5

Opening the Small C&I Sector: Platforms to Underwrite, Insure and

Pool Unrated Credits

Brian JonesFounder, Windmill

Capital Management

Graham SmithCEO and Founder,

Open Energy

Jonathan AbeCEO, SunWealth

Andrew GilliganSenior Director,

Investments, SolSystems

ModeratorMichael Mendelsohn

Senior Director of Project Finance and

Capital Markets, SEIA

Private Equity Investment

ModeratorAndrew Jack

Partner, Covington & Burling

David ZwillingerSenior Vice

President, D.E. Shaw & Co.

Laura SternCo-founder and

President, Nautilus Solar Energy

Ja KaoPresident, Onyx

Renewable Partners

Kathryn RasmussenVice President,

Capital Dynamics

Finance & Tax SeminarJune 1st-2nd, 2017

New York, New York

www.seia.org

Thank You to Our Sponsors

June 2, 2017 8

Mergers & Acquisitions

ModeratorMona Dajani

Principal Partner, Baker &

McKenzie LLP

Conor McKennaManaging Director,

CohnReznickCapital

Skip GrowManaging Director,

Morgan Stanley

Thomas PlagemannChief Commercial

Officer, Vivint Solar

John MarcianoPartner, Akin Gump

Strauss Hauer & Feld LLP

Financing & Tax Challenges with Solar+Storage Projects

ModeratorElliot Hinds

Partner, Crowell & Moring

Joel MeisterTax Manager,

Deloitte

Bill BushChief Financial

Officer, STEM, Inc.

Rhys MarshDirector, CIT

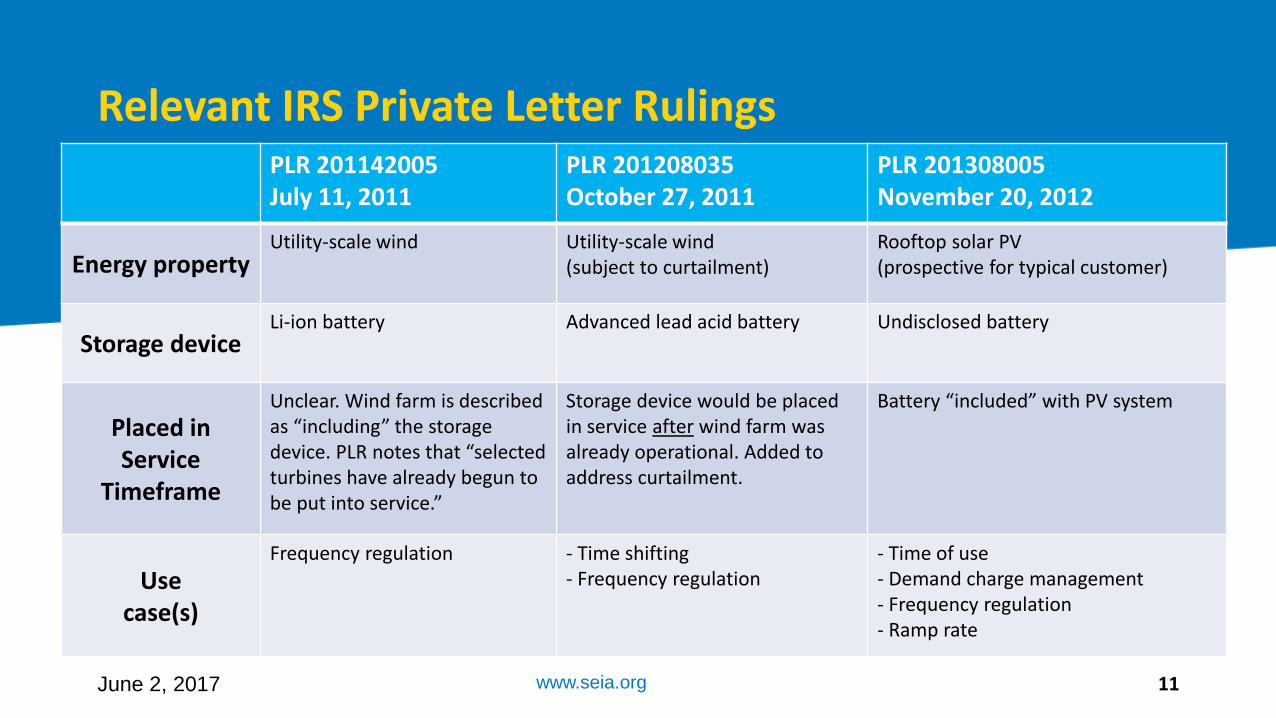

Relevant IRS Private Letter Rulings

www.seia.org 11

PLR 201142005July 11, 2011

PLR 201208035 October 27, 2011

PLR 201308005 November 20, 2012

Energy propertyUtility-scale wind Utility-scale wind

(subject to curtailment)Rooftop solar PV(prospective for typical customer)

Storage deviceLi-ion battery Advanced lead acid battery Undisclosed battery

Placed in Service

Timeframe

Unclear. Wind farm is described as “including” the storage device. PLR notes that “selected turbines have already begun to be put into service.”

Storage device would be placed in service after wind farm was already operational. Added to address curtailment.

Battery “included” with PV system

Use case(s)

Frequency regulation - Time shifting- Frequency regulation

- Time of use- Demand charge management- Frequency regulation- Ramp rate

June 2, 2017

Relevant IRS Private Letter RulingsPLR 201142005July 11, 2011

PLR 201208035 October 27, 2011

PLR 201308005 November 20, 2012

Non-qualified input %

Redacted - reportedly ~3%no methodology discussed

Redacted - reportedly ~15%no methodology discussed

No mention of inputs from grid or other non-qualifying sources

IRS analysis Mentions dual use rules, but only concludes that it is not auxiliary equipment

Mentions dual use rules, but onlyconcludes that it is not auxiliary equipment

Notes inputs from solar and grid for off-peak/peak use, as well as supplying to grid during peak hours via NEM

IRS conclusion Full cost eligible for ITC in lieu of PTC election under IRC Section 48(a)(5)

Full cost eligible for ITC in lieu of PTC election under IRC Section 48(a)(5)

- Applies dual use rules- No additional credit for subsequent increase in %

June 2, 2017 www.seia.org 12

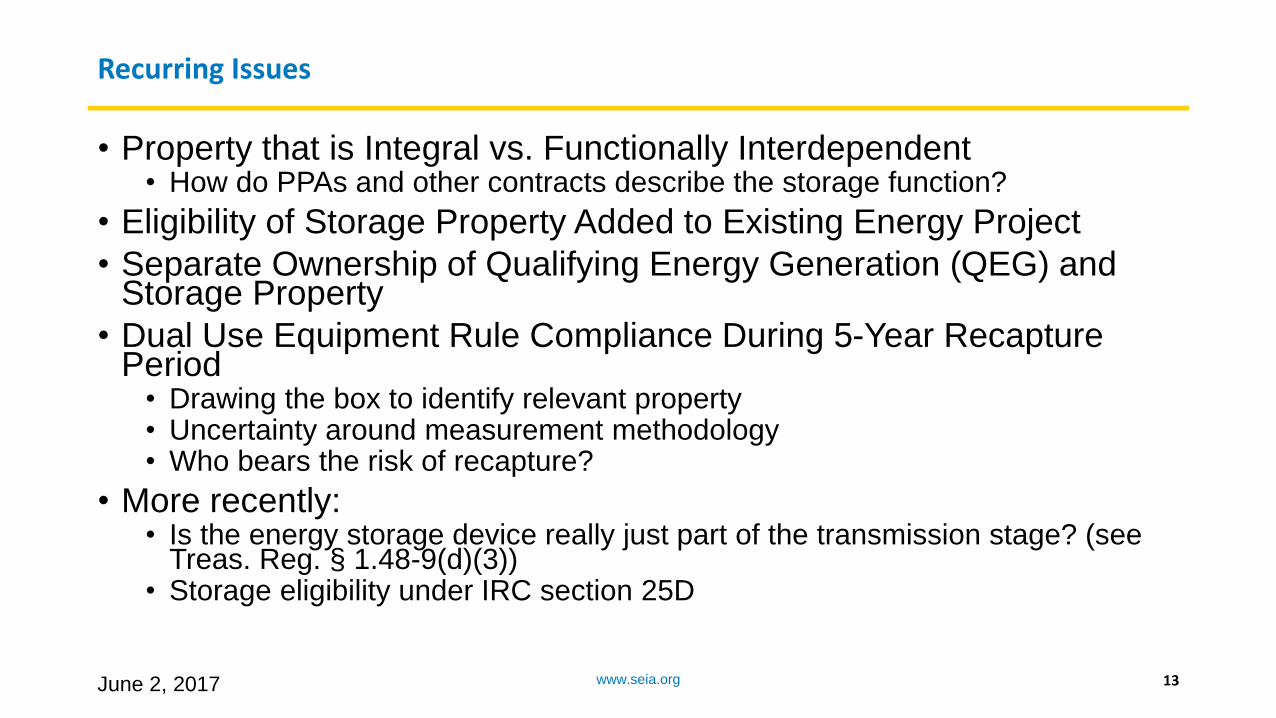

Recurring Issues

• Property that is Integral vs. Functionally Interdependent• How do PPAs and other contracts describe the storage function?

• Eligibility of Storage Property Added to Existing Energy Project

• Separate Ownership of Qualifying Energy Generation (QEG) and Storage Property

• Dual Use Equipment Rule Compliance During 5-Year Recapture Period

• Drawing the box to identify relevant property• Uncertainty around measurement methodology• Who bears the risk of recapture?

• More recently: • Is the energy storage device really just part of the transmission stage? (see

Treas. Reg. § 1.48-9(d)(3))• Storage eligibility under IRC section 25D

www.seia.org 13June 2, 2017

Finance & Tax SeminarJune 1st-2nd, 2017

New York, New York

www.seia.org

Thank You to Our Sponsors

June 2, 2017 14

Finance & Tax Considerations with Low & Middle Income Solar

ModeratorJames Duffy

Partner, Nixon Peabody

Harshul BanthiaDirector,

Sustainable Capital Advisors

Benjamin HealeyDirector, Clean Energy Finance,

Connecticut Green Bank

William BocraManaging Partner,

Baker Martin Capital, LLC

Lee PetersonSenior Manager,

Renewable Energy, CohnReznick

Ask the ExpertsSEIA Federal

Policy & Finance

Brandon Audap, Director of Federal

Affairs, SEIA

Michael Mendelsohn,

Senior Director of Project Finance

and Capital Markets, SEIA

Credit Risk

Jonathan SilverManaging Partner, Tax Equity Advisors

Low & Moderator

Income Solar

James DuffyPartner, Nixon

Peabody

Mergers & Acquisitions

John MarcianoPartner, Akin Gump

Strauss Hauer & Feld LLP

Tax Equity

Jessica RobbinsDirector of Structured

Finance, Sol Systems

Solar + Storage

Joel MeisterTax Manager,

Deloitte

Finance & Tax SeminarJune 1st-2nd, 2017

New York, New York

www.seia.org

Thank You to Our Sponsors

June 2, 2017 17

Welcome – June 2

Thomas PlagemannChief Commercial Officer, Vivint Solar

State of the Solar IndustryThomas Plagemann

Chief Commercial Officer | Vivint Solar

SEIA’sSolarGoesCorporate June2,2017www.seia.org

Growth of Residential Solar

www.seia.org 2SEIA’sFinanceandTaxSeminar

Source:GTMResearch/SEIA

Share of solar capacity additions by generation source

Key Question:

How should we interpret this recent slowdown in the residential solar space?

Installed Capacity Over Time is Nonlinear

www.seia.org 3SEIA’sFinanceandTaxSeminar

Source:EIA;U.S.EnergyInformationAdministration,ElectricPowerAnnualandPreliminaryMonthlyElectricGeneratorInventory

U.S. utility-scale electric capacity additions and retirements (2002 – 2016)U.S. utility-scale electric generating capacity by initial

operating year (as of December 2016

Industry Matures, Focus Shifts

www.seia.org 4SEIA’sFinanceandTaxSeminar

Source:VivintSolar

Vivint Solar installs and revenues (2015 – 2016)

More important metric for developer than year over year install growth is growth in installed base and increasing revenues.

Key Takeaway: 2015 2016 % Change

Installs (MWs) 230 222 -4%

Installed Base (MWs) 458 681 +48%

Revenues $64M $135M +111%

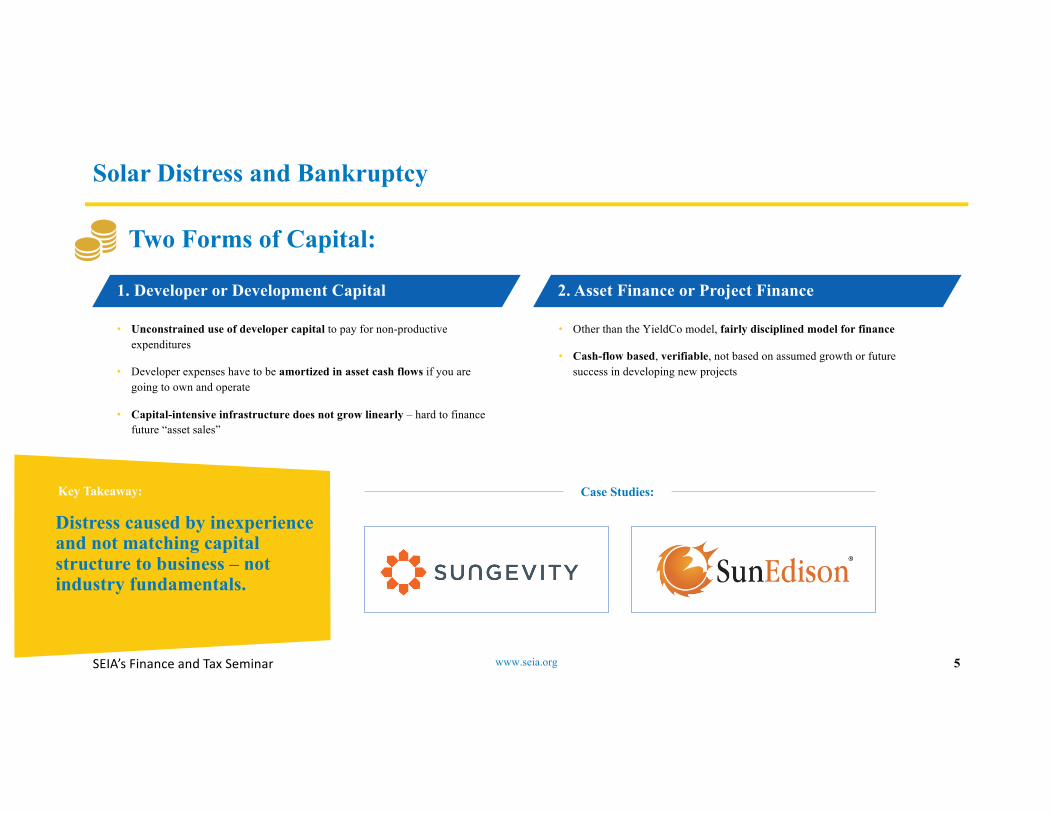

Solar Distress and Bankruptcy

www.seia.org 5SEIA’sFinanceandTaxSeminar

Two Forms of Capital:

1. Developer or Development Capital 2. Asset Finance or Project Finance

• Other than the YieldCo model, fairly disciplined model for finance

• Cash-flow based, verifiable, not based on assumed growth or future success in developing new projects

• Unconstrained use of developer capital to pay for non-productive expenditures

• Developer expenses have to be amortized in asset cash flows if you are going to own and operate

• Capital-intensive infrastructure does not grow linearly – hard to finance future “asset sales”

Case Studies:Key Takeaway:

Distress caused by inexperience and not matching capital structure to business – not industry fundamentals.

Availability of Capital

www.seia.org 6SEIA’sFinanceandTaxSeminar

Key Takeaway:

Sound capital structures and solid business plans will continue to drive capital investment.

Source:VivintSolar

Overview of VSLR Capital Raised Since March 2016

MAR 2016 Subordinated Hold Co. Debt $200M

JUL 2016 Tax Equity Fund $75M

AUG 2016 Bank Debt $300M

OCT 2016 2 Tax Equity Funds $100M

DEC 2016 Tax Equity Fund $100M

JAN 2017 Rated Long-term Bond $200M

MAR 2017 Renewed and Extended Warehouse Facility $375M

MAY 2017 Tax Equity Fund $100M

$1,450M

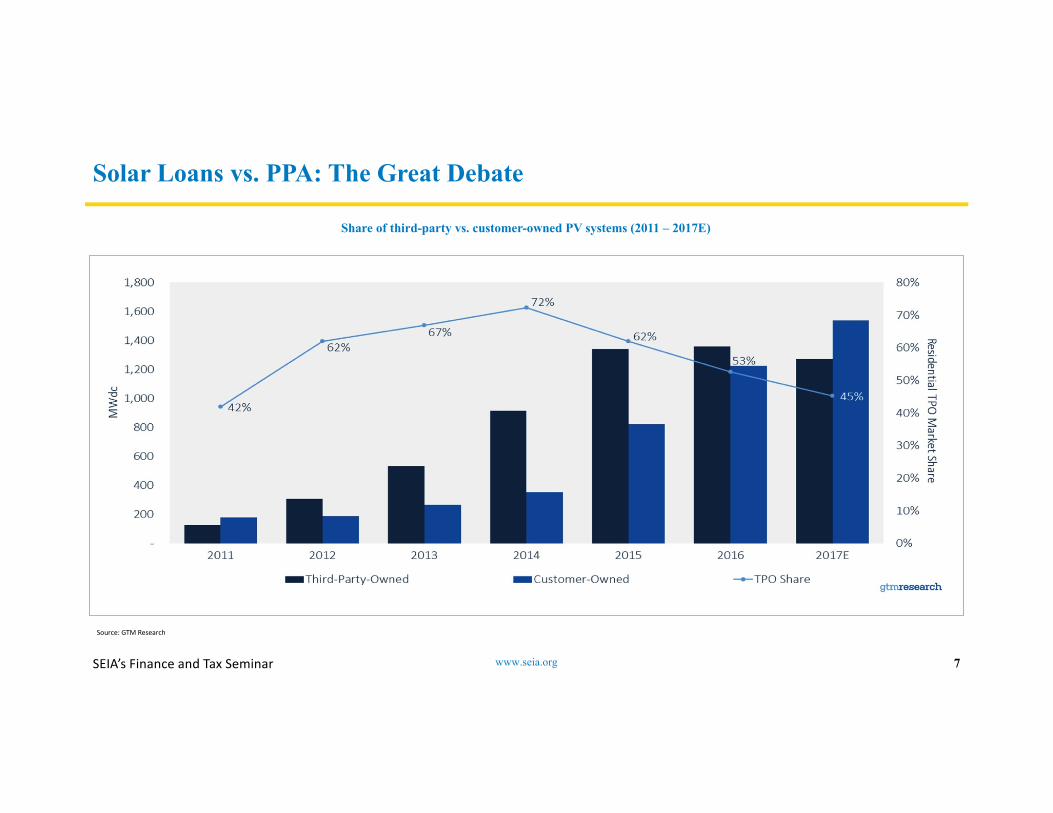

Solar Loans vs. PPA: The Great Debate

www.seia.org 7SEIA’sFinanceandTaxSeminar

Source:GTMResearch

Share of third-party vs. customer-owned PV systems (2011 – 2017E)

Loan Capital Availability Driving Adoption

www.seia.org 8SEIA’sFinanceandTaxSeminar

Key Question:

Are loans indicative of a shift in consumer preferences or something else?

• 20 year consumer financing is not the norm

• Early solar loan products were cumbersome and complicated

• Loan product evolved to meet market’s need for simplicity and frictionless origination

• Companies like Mosaic figured out how to access temporary capital and increasingly term capital for these loans

• Limited players offer Loans and PPAs side by side

• Insufficient history and experience to determine true preference

• Both are powerful financing tools and suitability will depend on various customer specific characteristics

www.seia.org 9SEIA’sFinanceandTaxSeminar

Paris AgreementClean Power Plan

Coal IndustryPower Grid Study Suniva 201 Filing

Why Coal is Declining

www.seia.org 10SEIA’sFinanceandTaxSeminar

49%26%18%

Competition from cheap natural gas

Lower than expected demand

Growth of renewable energy

Source:ColumbiaSIPA

Key Takeaway:

Coal is not coming back, and not just because of renewable energy.

Cost of Solar Continues to Decline

www.seia.org 11SEIA’sFinanceandTaxSeminar

$8.20 $7.60 $7.50

$6.61 $6.15

$5.22

$4.10 $3.78

$3.34 $3.03

$2.68 $2.39 $2.18 $2.01 $1.87

$7.50 $6.90

$6.40

$5.60

$4.90

$3.50

$2.86 $2.33

$2.07 $1.74

$1.49 $1.31 $1.22 $1.14 $1.08

$6.20

$5.25 $4.75

$3.58 $3.02

$2.09 $1.91 $1.81 $1.56

$1.28 $1.06 $0.99 $0.90 $0.86 $0.83 $-

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

$9.00

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017E 2018E 2019E 2020E 2021E

Residential C&I Utility Scale

Source:GTM,"U.S.PVSystemPricingH22016"Report

Share of third-party vs. customer-owned PV systems (2011 – 2017E)

www.seia.org 12

“Renewable energy continues to out-invest fossil by 2 to 1. I keep telling people, this is not alternative energy. This is just mainstream power-generating technology. No alternative energy, no alternative facts.”

Michael LiebreichChairman, BNEF

SEIA’sFinanceandTaxSeminar

Source:StateoftheIndustryKeynoteatBNEFGlobalSummit2017

www.seia.org 13SEIA’sFinanceandTaxSeminar

Nevada Aftermath

• Nevada essentially killed the solar industry, an industry that employed thousands of Nevada workers prior to December 2015.

• The state's 36,000 residential solar adopters vigorously protested the PUC decision to end NEM for existing customers and in response, the PUC did allow for grandfathering.

• Several casino companies, some of NV Energy’s largest customers, left for other energy providers.

• The fight to bring retail NEM back to Nevada is currently in play at the NV Legislature with Assembly Bill 405. Last November, NV voters voted overwhelming to deregulate by passing the Energy Choice Initiative. It will go before the voters again in 2018.

www.seia.org 14SEIA’sFinanceandTaxSeminar

Nevada taught us that consumers, when united, can force change.

Key Takeaway:

NEM 3.0

On May 10th SEIA adopted new NEM principles that anticipate an evolution to Net Metering.

www.seia.org 15SEIA’sFinanceandTaxSeminar

Basic Principles:

• Consumer right to reduce consumption

• Traditional NEM creates net benefits at low penetration levels

Criteria for Considering Alternatives to NEM

• Penetration levels

• Grandfathering • Process should be open and collaborative

• Simplicity, gradualism and predictability

Rate Design Guiding Principles

• Clear price signals that encourage complementary technologies

• Should encourage solar and other DERs• Time of use approaches are consistent with solar deployment

Guiding Principles for Alternative Compensation

• Fair value of solar

• Buy all Sell all rates at customer’s option• Should consider and promote adoption of complementary DER

technologies• Solar specific surcharges are discriminatory

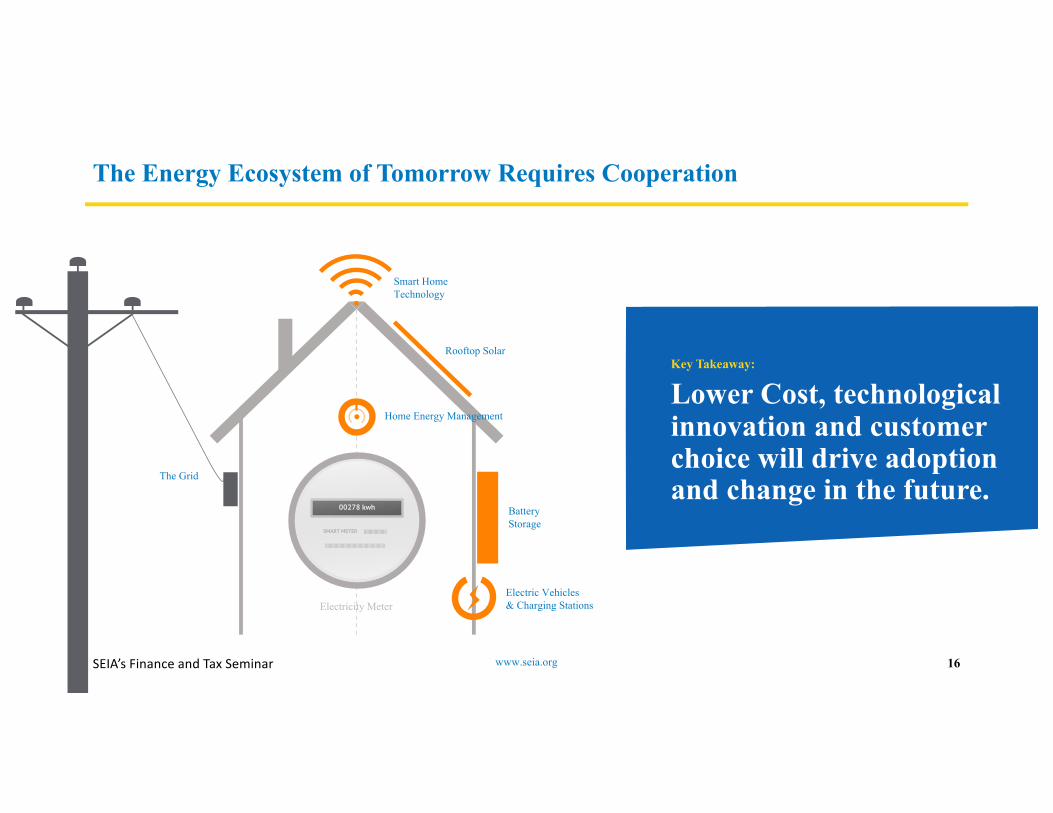

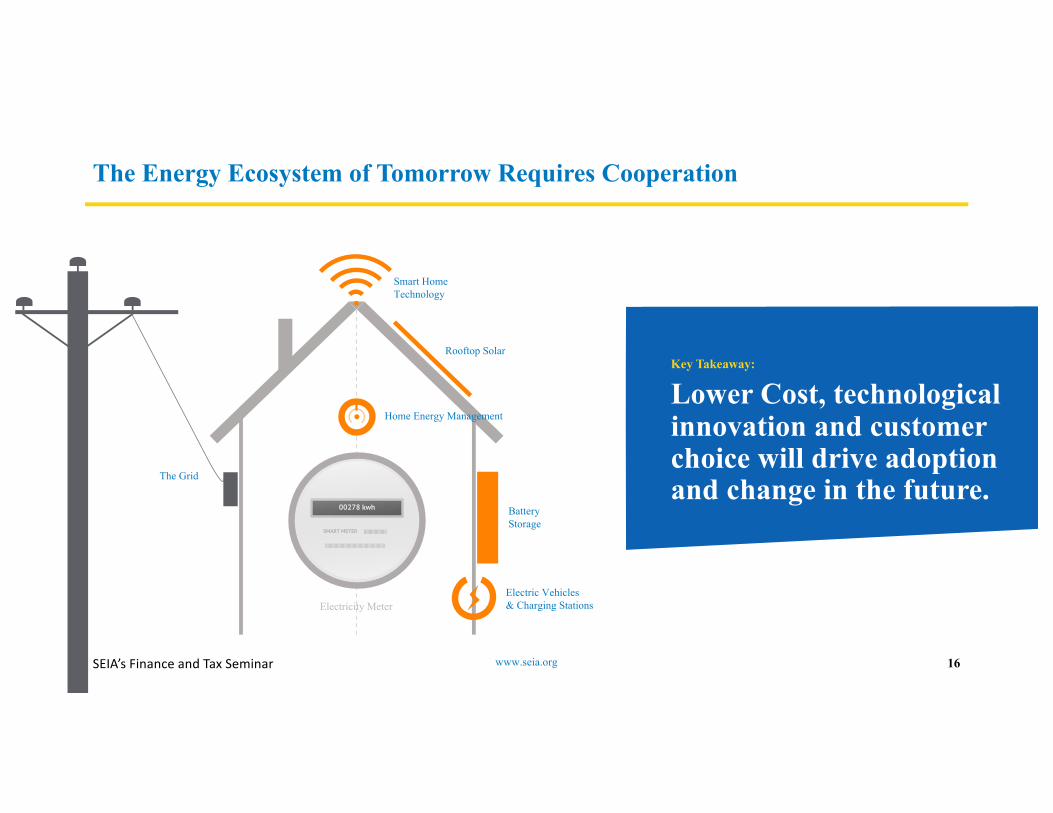

The Energy Ecosystem of Tomorrow Requires Cooperation

www.seia.org 16SEIA’sFinanceandTaxSeminar

Electric Vehicles& Charging Stations

Rooftop Solar

BatteryStorage

Solar

00278 kwh

|||||||||||||||||||SMART METER

||||||||||||||||||||||||||||||||||||||||||||||||||

Electricity Meter

Smart HomeTechnology

Home Energy ManagementLower Cost, technological innovation and customer choice will drive adoption and change in the future.

Key Takeaway:

The Grid

Current Finance & Tax Developments

ModeratorDavid Lowman

Partner, Hunton & Williams

Gary HecimovichPartner, Deloitte

Jaime ParkDirector, KPMG

Forrest MilderPartner, Nixon

Peabody

Panel Discussion Topics

1. White House Actions Impacting Renewable Energy

2. Government Guidance Projects• Proposed ITC Regulations

• Proposed Partnership Audit Regulations

• Beginning of Construction Guidance

• Service Contract Safe Harbor for Energy Sales Agreements / Rev. Proc. 2017-19

• CAIC Interconnection Gross-Ups / Notice 2016-36

3. 1603 Grant Litigation and Tax Controversy• Alta Wind Appeal

• Other Cases in Litigation or Settlement Talks

• IRS Audit Activity

• Refined Coal TAM

www.seia.org 20June 2, 2017

White House Actions Impacting Renewable Energy

Jaime Park

Director, KPMG

June 2, 2017 www.seia.org 21

White House Actions Impacting Renewable Energy

• Presidential Memorandum on Regulatory Freeze Pending Review (January 20, 2017)

• Freeze on “regulations”

• Executive Order on Reducing Regulation and Controlling Regulatory Costs (Signed January

30, 2017)

• “2 for 1” Executive Order

• Executive Order on Identifying and Reducing Tax Regulatory Burdens (Signed April 21, 2017)

• Review of “significant tax regulations”

• Executive Order on Promoting Energy Independence and Economic Growth (Signed March

28, 2017)

• Reduce regulatory burdens

• Executive Order on Implementing an America-First Offshore Energy Strategy (Signed April 28,

2017)

• Encourage energy exploration and production

www.seia.org 22June 2, 2017

White House Actions Impacting Renewable Energy

• Potential for “rolling back” or modifying Begun Construction Notices

• Deference afforded to prior notices / reliance and IRC section 7805(b) relief

• Key government players still undetermined

• Assistant Treasury Secretary Tax Policy - David Kautter

• Confirmation process will take time

• Chief Counsel at IRS Office of Chief Counsel

• TBD

www.seia.org 23June 2, 2017

Government Guidance Projects

Gary Hecimovich

Partner, Deloitte Tax LLP

Forrest Milder

Partner, Nixon Peabody

June 2, 2017 www.seia.org 24

Proposed ITC Regulations

• Notice 2015-70 (comments due February 2016)• Are storage devices and power conditioning equipment considered energy property?• What portion of the basis of dual use property should be taken into account in

computing the energy percentage?• What facilities/technologies should be defined?• What additional definitions are needed?

• 35 comment letters submitted

• SEIA comment letter• Re-affirm integral property rule• Re-affirm building component rule• Re-affirm a storage device is qualifying ITC system property• Revise the dual use equipment rule to provide flexibility and certainty to taxpayers• Apply integral property and primary use standard to dual function property• Clarify technical issues concerning energy property that includes a storage device

• Current status?

www.seia.org 25June 2, 2017

Proposed Partnership Audit Regulations

• On January 18, 2017, Treasury and IRS released proposed regulations (REG-136118-15) providing detail into the administration of the new centralized partnership audit regime enacted as part of the Bipartisan Budget Act (BBA) of 2015.

• The effective date for new rules under the BBA is for partnership taxable years beginning after December 31, 2017.

• The new rules are designed to shift the burden for actually assessing and collecting tax after a partnership-level adjustment from the IRS to the partnership and partners.

• Proposed regulations were immediately withdrawn as part of the Trump administration’s initial freeze on regulatory activity.

• The proposed regulations were never officially published in the Federal Register and thus became subject to the Trump administration’s January 20, 2017, regulatory ”freeze”.

• Proposed regulations provide important insights into the IRS’s views at the time issued regarding implementation of the BBA rules.

• Current status?

www.seia.org 26June 2, 2017

Beginning of Construction Guidance

• 6 IRS Notices defining the beginning of construction for the PTC (and ITC in lieu of PTC)

• Basic begun construction requirements• Physical work of a significant nature + continuous program of construction• 5% Safe harbor + continuous efforts toward completion

• Continuity Safe Harbor• Must be placed in service by the later of four years after calendar year during which BOC occurs or December 31, 2018

• Inventory rule

• Binding written contract rule

• SEIA comments:1. Provide a technology-neutral Continuity Safe Harbor that aligns with statutory placed-in-service deadline;

2. Confirm eligibility of property integral to qualifying activity and provide examples;3. Clarify relevant unit of property and adopt a single project election for units of property engaged in qualifying

activity;

4. Clarify application of inventory rule;

5. Provide specific examples of physical work of a significant nature;6. Adopt 5% safe harbor and incorporate a scale-back provision in recognition of cost over-runs;

7. Clarify requirements to preserve ITC eligibility when a project or solar energy property is transferred; and

8. Provide excusable disruptions specific to solar project development

www.seia.org 27June 2, 2017

Begun Construction for Solar Continuity Safe Harbor Recommendation

www.seia.org 28June 2, 2017

Continuity Safe Harbor Satisfied if Placed in Service before 1/1/2024

1/1/2019 1/1/2020 1/1/2021 1/1/2022

CY 2019 CY 2020 CY 2021

1/1/2023

CY 2023CY 2022

1/1/2024

Construction Begins

Before 1/1/2020

10% ITC30% ITC

Construction Beginsin 2020

10% ITC26% ITC

Construction Beginsin 2021

10% ITC22% ITC

10% ITC ValueRegardless of

Placed-in-Service Date

Construction Beginsin 2022

Service Contract Safe Harbor for Energy Sales AgreementsRev. Proc. 2017-19

• Federal regulations for government contracts have raised questions about whether certain energy contracts may be re-cast as leases or conditional sales.

• Example: Power Purchase Agreement to sell electricity on a military base.• Treatment as service contract is critical to preservation of ITC. Lease or sale

treatment would disqualify the project from the ITC.

• Rev. Proc. clarifies when government will not challenge the treatment of an energy savings performance contract (“ESPC”) sales agreement between an energy service company and the federal agency (“FA”) for provision of electricity from an “alternative energy facility”.

• Rev. Proc. States that the IRS will not issue rulings on this issue.

• Applies to any ESPC sales agreement entered into after February 5, 2017. Contracts executed prior to the effective date that meet the safe harbor criteria will not be challenged.

www.seia.org 29June 2, 2017

Service Contract Safe Harbor for Energy Sales AgreementsRev. Proc. 2017-19

• Under IRC section 7701, a contract related to an “alternative energy facility” will generally not be treated as a lease, unless the following occurs:

1. The service recipient (or a related entity) operates such facility,

2. The service recipient (or a related entity) bears any significant financial burden if there is nonperformance under the contract or arrangement (other than for reasons beyond the control of the service provider),

3. The service recipient (or a related entity) receives any significant financial benefit if the operating costs of such facility are less than the standards of performance or operation under the contract or arrangement, or

4. The service recipient (or a related entity) has an option to purchase, or may be required to purchase all or a part of such facility at a fixed and determinable price (other than for fair market value).

• Government will not challenge contracts if all of the following are true:1. Total term of the ESPC ESA cannot exceed 20 years in length and must be consistent with and appropriate for

the scope and scale of the renewable project,

2. ESPC ESA must satisfy other federal guidance, specifically the requirements of 42 U.S.C. section 828 and OMB Memorandum M-12-21,

3. Under no circumstances will the FA attempt to operate the renewable energy generation asset: in the event of a shut-down or mechanical issue, FA will immediately notify ESCO or its designated contractor,

4. ESCO bears all financial risk for non-performance, except to the extent such non-performance is attributable to a temporary shut-down of the facility for repairs, maintenance, or capital improvements,

5. Contract price for electricity will not be reduced if operating costs should diminish, and

6. FA may have the option to purchase, or may be required to purchase, the renewable energy generation asset at the end of the contract term, for its fair market value (FMV) at the time of the purchase.

www.seia.org 30June 2, 2017

CAIC Interconnect Gross-UpsNotice 2016-36

• Contributions made to a utility to encourage the provision of services to a utility customer – generally taxable.

• Interconnections – payments made by power plant owners to transmission grid owners – generally taxable unless specific requirements are met.

• IRS guidance• Notices 88-129, 90-60, 2001-82 and 2016-36• Many private letter rulings historically, but Notice 2016-36 states that the IRS will not

issue private letter rulings involving this safe harbor.

• Section 61(a) – gross income means all income from whatever source derived, unless excluded by law.

• Section 118(a) – exclusion from gross income for any contribution to the capital of a corporate taxpayer.

• Section 118(b) – exception from the term “contribution to the capital of the taxpayer” for any contribution in aid of construction from a customer or potential customer.

www.seia.org 31June 2, 2017

CAIC Interconnect Gross-UpsNotice 2016-36

www.seia.org 32June 2, 2017

• Requirements for exclusion• Transferor may be a electricity generation or cogeneration facility or an energy storage facility

• Asset may not be included in rate base of the transmission utility

• Title to power must transfer to purchaser before transmission

• No requirement for an interconnection agreement or power supply contract

• The transferor may not purchase electricity from the utility, unless the purchase satisfies the 5% test

• Amortization period of 20 years for the interconnection costs

Electrictransmission

utility Consumers orintermediaries,including affiliates(customer)

Stand-alonegenerator (supplier)

$ for construction or property

Electricity

CAIC Interconnection Gross-UpsNotice 2016-36

• This Notice applies to transfers of interties meeting all the requirements under this Notice made on or after June 20, 2016. However, taxpayers may choose to rely on this safe harbor for transfers with respect to qualifying transfers made prior to June 20, 2016.

• Automatic accounting method changes

www.seia.org 33June 2, 2017

1603 Grant Litigation and Tax Controversy

David Lowman

Partner, Hunton & Williams

www.seia.org 34June 2, 2017

1603 Grant Litigation and Tax Controversy

Alta Wind v. U.S. (October 24, 2016)

• §1603 Grant requested for 30% of purchase price of eligible property

• Treasury reduced Grant award to 30% of Alta’s cost to build

• Court awarded $206 million in damages to taxpayer

• IRS expert witness testimony dismissed

• Court rejected government’s arguments holding:• § 1060 does not apply

• No goodwill or going concern value could attach

• PPAs not separate intangible assets with value independent of tangible property

• Wind projects had “turn-key value”

• No “peculiar circumstances” indicating inflated purchase prices

• Appealed to Federal Circuit: Government brief filed April 27th

• Decision expected this Fall

www.seia.org 35June 2, 2017

1603 Grant Litigation and Tax Controversy

Sequoia Pacific Solar I, LLC v. U.S. (October 24, 2016)

• Residential solar with valuation issues

• Currently in mediation

LCM Energy Solutions v. U.S., 170 Fed. Cl. 770 (2016)

• LCM sued for basis reductions equal to approximately $400,000 in residential DG solar systems (roughly 50% haircut)

• Court determined Treasury was correct to disregard taxpayer’s claimed basis and use “the better, more reasonable approach” to use installation costs plus a 20% profit, which is what Treasury did in issuing the original 1603 Grants

• Court rejected Government counterclaims

www.seia.org 36June 2, 2017

1603 Grant Litigation and Tax Controversy

GUSC Energy, Inc. v. U.S., Fed. Cl. (Nov. 8, 2016)

• Treasury awarded 6.6% of claimed award for co-generation biomass plant where only 6.6% of total steam available for end-use was converted to electricity

• Government expert proposed an “efficiency method” allocation by focusing on energy used for electricity generation, and comparing that generation efficiency to the efficiency of a hypothetical electricity-only biomass plant (i.e., facility generates 15.25% of the electricity it would generate if it only generated electricity).

• Plaintiff expert argued 100% of costs should be treated as qualifying because all equipment was necessary for the generation of electricity.

• As a co-generation facility the Court found the steam generated to serve predominately significant role in heating, rather than electricity generation

• Court choose to follow “energy efficient method” allocation presented at trial by Government’s expert witness and rejected policy arguments made by Plaintiff

• Court rejected Government counter claims to recapture grant for prolong periods where the plant ceased operations

www.seia.org 37June 2, 2017

1603 Grant Litigation and Tax Controversy

• Increased IRS audit activity

• IDRs requesting justification for eligible basis higher than similar projects awarded grant under the 1603 Program

• Eligible basis and valuation risk typically born by Project Sponsor

• Tax equity imposing limits on cost approach vs. accepting valuations based on income approach

• Refined Coal TAM• What does refined coal have to do with the solar ITC? • IRS disallowed tax credits as an impermissable “sale of tax credits”• IRS cites lack of variability- upside and downside –where payments

tied directly to credits

www.seia.org 38June 2, 2017

Finance & Tax SeminarJune 1st-2nd, 2017

New York, New York

www.seia.org

Thank You to Our Sponsors

June 2, 2017 39

Debt Panel

ModeratorDavid Burton

Partner, Mayer Brown

Susan NickeyManaging Director, Hannon Armstrong

Scott ZajacCEO, Rockwood

Group

Jordan BlanchardGeneral Manager –Renewable Energy Lending, Live Oak

Bank

Jean-Pierre BoudriasManaging Director,

Goldman Sachs

Finance & Tax SeminarJune 1st-2nd, 2017

New York, New York

www.seia.org

Thank You to Our Sponsors

June 2, 2017 41

Credit And Tax Risk Mitigation

David DeBerryCEO, Concord Specialty Risk,

Inc.

ModeratorGary Blitz

Senior Managing Director, Aon

Transaction Solutions

Jason CavaliereVice President, Project Finance,

Sunrun

Ira PalgonPartner, Energy and

Infrastructure, Wilson Sonsini

Goodrich & Rosati

Chris RoetheliBusiness

Development Officer, US Bancorp

Community Development Corporation

Victoria Dal SantoExecutive Director,

Energy Investments, J.P. Morgan

Tax Equity Update

ModeratorKeith Martin

Partner, Chadbourne &

Parke LLP

Anand DandapaniExecutive

Director, JP Morgan

Jessica RobbinsDirector of Structured

Finance, Sol Systems

Matthew PtakDirector,

BlackRock

Judy KwokVice President

and Tax Counsel, GE Energy Financial Services

Lan Adair SasaAssistant Director

of Project Management,

Renewable Energy Investments, U.S.

Bancorp Community

Development Corporation

Finance & Tax SeminarJune 1st-2nd, 2017

New York, New York

www.seia.org

Thank You to Our Sponsors

June 2, 2017 44

The Energy Ecosystem of Tomorrow Requires Cooperation

www.seia.org 16SEIA’sFinanceandTaxSeminar

Electric Vehicles& Charging Stations

Rooftop Solar

BatteryStorage

Solar

00278 kwh

|||||||||||||||||||SMART METER

||||||||||||||||||||||||||||||||||||||||||||||||||

Electricity Meter

Smart HomeTechnology

Home Energy ManagementLower Cost, technological innovation and customer choice will drive adoption and change in the future.

Key Takeaway:

The Grid