Finance for Growth presentation SME Banking and Credit · Finance for Growth presentation SME...

14

Credit Review Office 1850 211 789 [email protected] Finance for Growth presentation SME Banking and Credit Paul Kerr Senior Reviewer Credit Review Office June 2018

Transcript of Finance for Growth presentation SME Banking and Credit · Finance for Growth presentation SME...

Credit Review Office

1850 211 789 [email protected]

Finance for Growth presentation

SME Banking and Credit

Paul Kerr Senior Reviewer

Credit Review Office

June 2018

Mission - ensure bank credit system operating effectively for small and

medium-sized enterprises, incl. sole traders and farmers.

• Simple and effective review process for businesses refused / reduced /

withdrawn credit by bank (AIB, BOI, Ulster, PTSB)

• Information and Helpline 1850 211789

• Reviews refusal/restructure/refinance of up to €3,000,000 (small fee)

• Small staff and a panel of experienced Credit Reviewers

• Reviewers engage directly (phone/email)

Recommends credit facilities be provided in > 50% of cases

Credit Review Office

1850 211 789 [email protected]

Irish SME Banking

1850 211 789 [email protected]

Banking Sector:

• Legacy Issues – Regulation, Capital Adequacy, Cost Cutting

• Concentration – 92% of market in 3 banks

• Focus on core home market – less international• Automation – online, call centre, centralisation• Separation of Relationship Mgr and Credit Decision Making• Change in staffing levels and experience• More risk averse

SME Banking – commodity or scarce resource?

Irish SME Banking - Transactional

1850 211 789 [email protected]

DAY TO DAY/TRANSACTIONAL BANKING

• Build a relationship with your bank – on paper/face to face

• Open an account as early as possible

• Track record with credit – small loan before you need big one

- Credit Bureau

• References/3rd party validation

• Bank views ‘Connection’ – personal and corporate

3 Parts to the Credit Process

1850 211 789 [email protected]

Step 1: Make the application

Step 2: Bank Credit Assessment/ Credit Approval

Step 3: Drawdown

ALWAYS TAKES MUCH LONGER THAN YOU THINK!

7

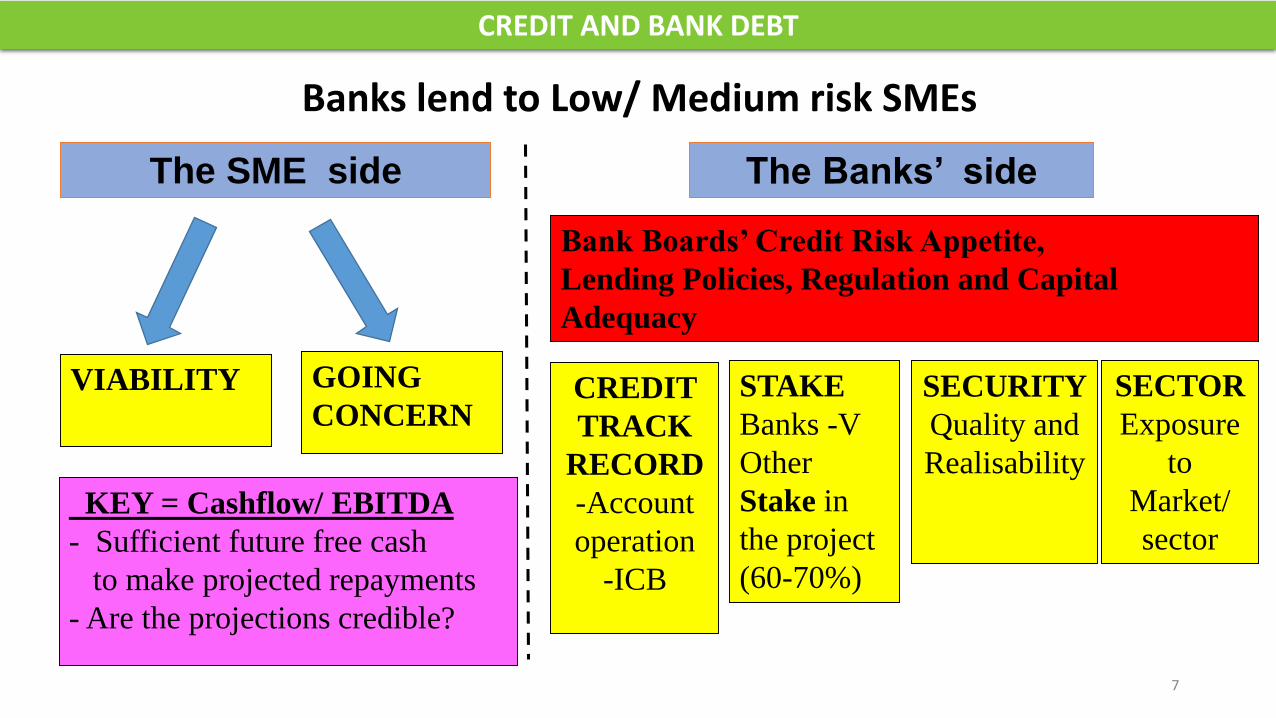

Banks lend to Low/ Medium risk SMEs

CREDIT AND BANK DEBT

KEY = Cashflow/ EBITDA

- Sufficient future free cash

to make projected repayments

- Are the projections credible?

Bank Boards’ Credit Risk Appetite,

Lending Policies, Regulation and Capital

Adequacy

STAKE

Banks -V

Other

Stake in

the project

(60-70%)

SECURITY

Quality and

Realisability

SECTOR

Exposure

to

Market/

sector

The SME side The Banks’ side

GOING

CONCERN

VIABILITY CREDIT

TRACK

RECORD

-Account

operation

-ICB

Common Problems with SME Credit Applications

1850 211 789 [email protected]

Requests for credit may be poorly presented by Borrowers

• no clear business plan

• lack sufficient detail

• inadequate and/or poor quality financial

information

Aging Financial Accounts - produced for filing/tax return purposes – info too old in times of rapid business change

Financial Advisers can assist Borrowers in presenting credit applications, but promoter must ‘own’ plan

Managing your bank interactions – keep the record clean

How to Make a Strong Application

1850 211 789 [email protected]

• This is a sales pitch – you are competing

• Preparation is Key – documentation required includes

• Business Plan – financial reports and cashflow projections: REALISTIC

• Statement of Affairs/Asset and Liability profile of owners/promoters

• Confirmation that tax affairs in order

• Details of Security on Offer

• Clear Aims/objectives: Convince bank proposal is viableEnsure your RM (agent) understands your businessConfirm all the information needed has been providedAdd a proposal document to the Application Form

• Support – bring someone with you – accountant/adviser

• Establish timelines and follow up proactively

1850 211 789 [email protected]

Credit Assessment

KEY: Demonstrate Viability / ability to repay

• Promoters Experience/Capability/Track Record (Business & Credit History)

• What market is the enterprise involved in-growing or declining? Competition?

• Past Performance - historic profit/cash flow

(past 2 years may not be indicative)

• Future Potential - projected profit/cash flow

how will business model change

• Performance against projections so far

• Sales pipeline

• Aged Debtors and Creditors

• Existing Debt incl Statement of Assets and Liabilities of promoters

Overall aim: reduce risk

• Viability/Going Concern : consider when applying

▪ improved clarity, up to date financials, address total connection, company structure, shift in business model, third party validation

▪ Shorten loan period/reduce risk to bank//match to use of funds

▪ Seek low cost or flexible funding – Strategic Banking Corporation (SBCI)

▪ Banking ratios – interest cover, Loan to Value, sensitivity analysis

• Stake – Directors loans, Equity investment, Microfinance Ireland, Angel investors, EIIS, ISIF

• Security – tangible assets, govt. guarantees (CGS)

• Sector – know your sector very clearly

1850 211 789 [email protected]

Finding Solutions

STAKE

Banks’ -V –

Others’

SECURITY

Quality and

Realisability

SECTOR

Exposure to

Market/locality

GOING

CONCERN

VIABILITY

Access to Credit - Government Supports

1850 211 789 [email protected]

Access to Bank Credit - main source of funding for majority of Irish SME’s

4 main Government initiatives to ensure credit is available for viable SME’s –addressing market failures

1. Credit Review Office

2. Credit Guarantee Scheme – lack of security/novel concept

3. SBCI/ISIF – cheaper funding/alternative providers

4. Microfinance Ireland – Microenterprises, up to €25k, less risk averse

Updates: SME ONLINE TOOL www.supportingsmes.ie

Access to Credit – Alternate providers

1850 211 789 [email protected]

Private Sector Alternatives: www.ifpireland.ie (trade body)

1850 211 789 [email protected]

Credit Review Office – Summary

• Businesses are starting/growing and need funding – credit and

equity/owners stake

• Credit is harder to get in recent years, and can cost more in Ireland

• Fail to prepare, prepare to fail

• Use all the tools in the Credit toolbox to de-risk/reduce risk for bank, and

cost for the borrower

• A negotiation process - informed borrowers do better