Finance Bill' 2017 : A Crisp Analysis of Income Tax Provisions

38

A Crisp Analysis of Income Tax Provisions Finance Bill’2017 Blue Consulting Pvt. Ltd. Doing common things, Uncommonly well. GST I F&A Outsourcing I Internal Audit I Consulting

-

Upload

chandan-goyal -

Category

Economy & Finance

-

view

81 -

download

0

Transcript of Finance Bill' 2017 : A Crisp Analysis of Income Tax Provisions

A Crisp Analysis of Income Tax Provisions

Finance Bill’2017

Blue Consulting Pvt. Ltd.

Doing common things, Uncommonly well. GST I F&A Outsourcing I Internal Audit I Consulting

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

Index

2

1. TaxIncen+ves 3-5

2. Interna+onalTaxa+on 6-12

3. Discouragementtocashtransac+ons 13-15

4. SomeImportantChanges 16-28

5. Proceduralchanges 29-33

6. PersonalTaxa+on 34-35

7. Aboutus 36-38 28

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

1. Tax Incentives

3

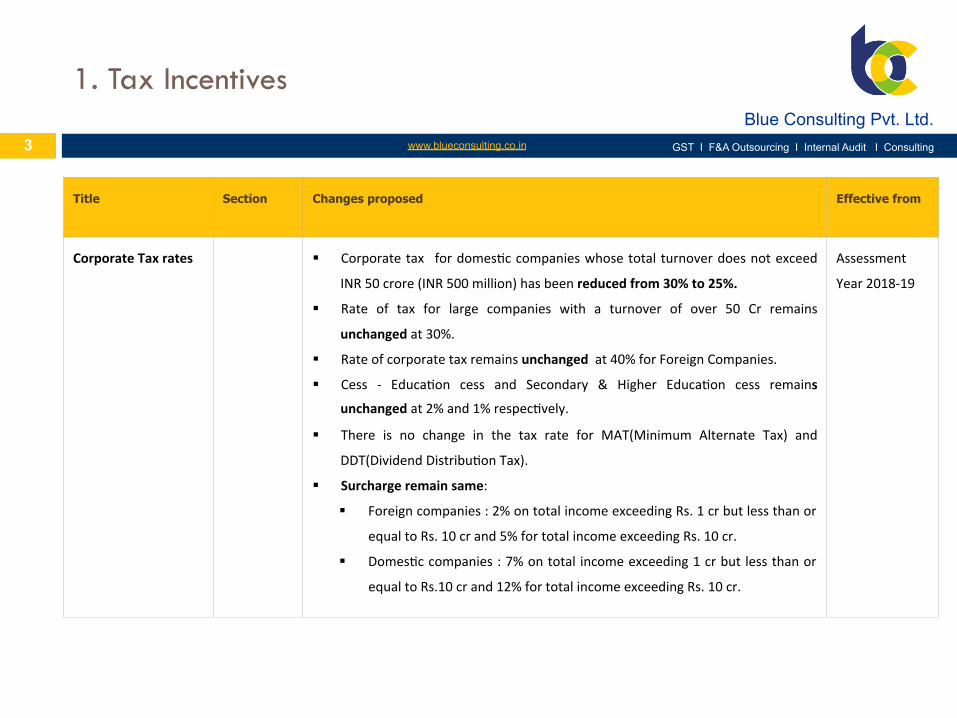

Title Section Changes proposed Effective from

CorporateTaxrates § Corporatetax fordomes+ccompanieswhosetotalturnoverdoesnotexceed

INR50crore(INR500million)hasbeenreducedfrom30%to25%.

§ Rate of tax for large companies with a turnover of over 50 Cr remains

unchangedat30%.

§ Rateofcorporatetaxremainsunchangedat40%forForeignCompanies.

§ Cess - Educa+on cess and Secondary & Higher Educa+on cess remains

unchangedat2%and1%respec+vely.

§ There is no change in the tax rate for MAT(Minimum Alternate Tax) and

DDT(DividendDistribu+onTax).

§ Surchargeremainsame:

§ Foreigncompanies:2%ontotalincomeexceedingRs.1crbutlessthanor

equaltoRs.10crand5%fortotalincomeexceedingRs.10cr.

§ Domes+ccompanies:7%ontotal incomeexceeding1crbutlessthanor

equaltoRs.10crand12%fortotalincomeexceedingRs.10cr.

Assessment

Year2018-19

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

...contd. [1. Tax Incentives]

4

Title Section Changes proposed Effective from

Incen=vesfor

promo=ng

Investmentin

ImmovableProperty

2(42A) § Aspercurrentprovisions,animmovablepropertyisconsideredasalong-term

assetifitisheldfortheperiodofmorethan36months.

§ Inordertopromotetheinvestmentinrealestatesector,theperiodofholding

hasbeenreducedto24monthsfrom36monthsforanimmovablepropertyto

qualifyasalong-termcapitalasset.

§ Accordingly, the benefits of concessional rate of tax and indexa+on can be

availedifanimmovablepropertyisheldforaminimumperiodof24months.

As ses sment

Year2018-19

Set-offandcarry

forwardoflossin

caseofchangein

shareholding

79 § Aspertheexis+ngprovisions,acloselyheldcompanyisnotallowedtocarry

forwardandset-offlossesofearlieryearsifitsshareholdingchangesbymore

than50%.

§ Inordertofacilitateeaseofdoingbusinessandtopromotethestart-upsin

India,lossesincurredbyaneligiblestart-upcanbecarriedforwardandset-off

againsttheincomeofthepreviousyear,ifalltheshareholdersofsuch

company(asexistedintheyearofloss)con+nuetoholdthesharesonthelast

dayofthepreviousyear.

A s ses sment

Year2018-19

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

...contd. [1. Tax Incentives]

Title Section Changes proposed Effective from

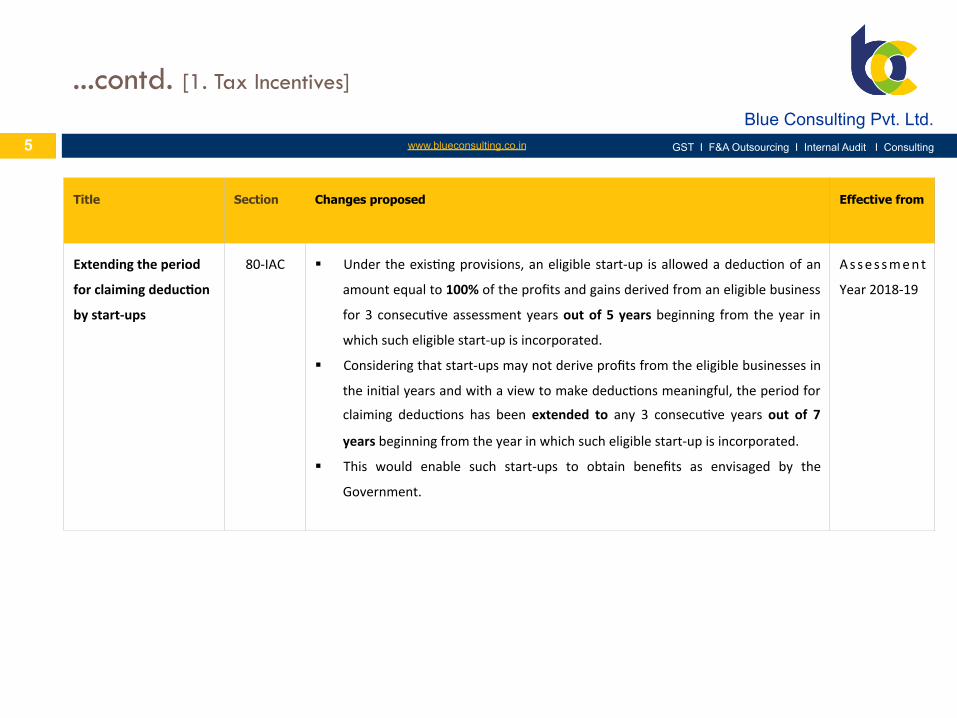

Extendingtheperiod

forclaimingdeduc=on

bystart-ups

80-IAC § Undertheexis+ngprovisions,aneligiblestart-up isallowedadeduc+onofan

amountequalto100%oftheprofitsandgainsderivedfromaneligiblebusiness

for3 consecu+veassessmentyearsoutof5yearsbeginning fromtheyear in

whichsucheligiblestart-upisincorporated.

§ Consideringthatstart-upsmaynotderiveprofitsfromtheeligiblebusinessesin

theini+alyearsandwithaviewtomakededuc+onsmeaningful,theperiodfor

claiming deduc+ons has been extended to any 3 consecu+ve years out of 7

yearsbeginningfromtheyearinwhichsucheligiblestart-upisincorporated.

§ This would enable such start-ups to obtain benefits as envisaged by the

Government.

As ses sment

Year2018-19

5

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

2. International Taxation

6

Title Section Changes proposed Effective from

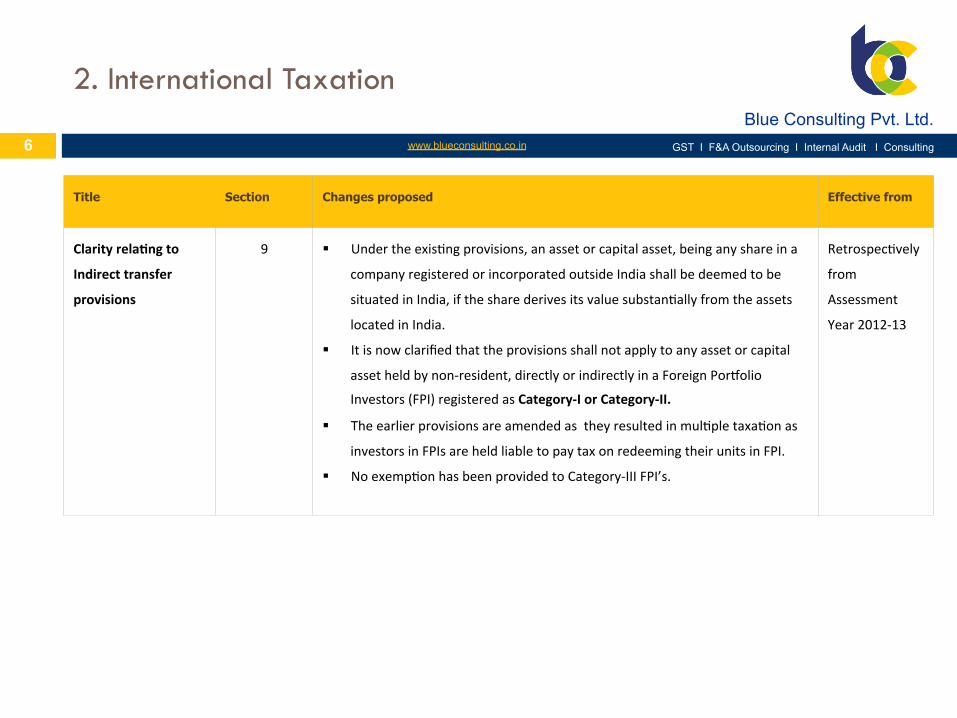

Clarityrela=ngto

Indirecttransfer

provisions

9 § Undertheexis+ngprovisions,anassetorcapitalasset,beinganyshareina

companyregisteredorincorporatedoutsideIndiashallbedeemedtobe

situatedinIndia,ifthesharederivesitsvaluesubstan+allyfromtheassets

locatedinIndia.

§ Itisnowclarifiedthattheprovisionsshallnotapplytoanyassetorcapital

assetheldbynon-resident,directlyorindirectlyinaForeignPor_olio

Investors(FPI)registeredasCategory-IorCategory-II.

§ Theearlierprovisionsareamendedastheyresultedinmul+pletaxa+onas

investorsinFPIsareheldliabletopaytaxonredeemingtheirunitsinFPI.

§ Noexemp+onhasbeenprovidedtoCategory-IIIFPI’s.

Retrospec+vely

from

Assessment

Year2012-13

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

…contd. [2. International Taxation]

7

Title Section Changes proposed Effective from

Provisionof

“Secondary

Adjustment”

introducedinTransfer

Pricing

92CE § InordertoalignthetransferpricingprovisionsinlinewithOECDtransferpricing

guidelinesandinterna+onalbestprac+ces,theassesseeshallberequiredto

carryout“SecondaryAdjustment”wheretheprimaryadjustmenttotransfer

price.

§ Inten+onistoremovetheimbalancebetweencashaccountandactualprofitof

theassesseonaccountof“PrimaryAdjustments”.

§ “Secondaryadjustment”willbemadeonlyinrespectoffollowing“Primary

Adjustments”:

§ voluntaryadjustmentinreturnofincome;or

§ acceptanceofadjustmentproposedbyAO;or

§ determina+oninanAPA;or

§ adop+onofsafeharbourrule;or

§ resolu+onunderMutualAgreementProcedure

§ TheSecondaryAdjustmentwouldbedeemedasadvancetoAEifsuchamountis

notreceivedwithinprescribed+melimitandinterestwouldbeapplicableina

mannertobeprescribed.

§ NoSecondaryAdjustmentifPrimaryAdjustmentdoesnotexceedINR1Cr.

Asses sment

Year2018-19

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

…contd. [2. International Taxation]

8

Title Section Changes proposed Effective from

Interestdeduc=on

restrictedto30%of

EBIDTA

94B § Undertheini+a+veoftheG-20countries,theOrganiza+onforEconomicCo-

opera+onandDevelopment(OECD)initsBaseErosionandProfitShihing(BEPS)

projecthadtakenuptheissueofbaseerosionandprofitshihingbywayofexcess

interestdeduc+onsbytheMNEsinAc+onPlan4.

§ Inlinewithrecommenda+onsofAc+onPlan4,anewsec+onhasbeeninserted

whichrestrictstheclaimofinterestexpensestoassociatedenterprise(AE)tothe

extentofminimumoffollowing:

§ 30%ofitsearningsbeforeinterest,taxes,deprecia+onandamor+za+on

(EBITDA)OR

§ interestpaidorpayabletoassociatedenterprise

§ ThisprovisionisapplicabletoanIndiancompany,oraPermanentEstablishment

(PE)ofaforeigncompanyinIndia,beingtheborrower,whopaysinterestor

similarconsidera+oninrespectofanydebtissuedbyanon-residentAE.

§ Therestric+onisapplicableonlywhereinterestorsimilarconsidera+ontoitsAE

exceedsINR1crore(10million).

....contd.

As ses sment

Year2018-19

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

…contd. [2. International Taxation]

9

Title Section Changes proposed Effective from

....contd.(Interest

deduc+onrestrictedto

30%ofEBIDTA)

94B § Debtshallbedeemedtobetreatedas issuedbyanAEwhere itprovidesan

implicitorexplicitguaranteetoanon-AE lenderordepositsacorresponding

andmatchingamountoffundswiththenon-AElender.

§ Therestric+onwillnotapplytoanIndiancompanyorPEofaforeigncompany

whichisengagedinthebusinessofbankingorinsurance § Disallowedinterestexpenseshallbecarriedforwardupto8assessmentyears

immediately succeeding the assessment year for which the disallowance is

firstmade.

§ Deduc+oninsubsequentassessmentyearwillbesubjecttosamerestric+ons.

§ The term ̳debt‘ has been defined to mean any loan, financial instrument,

finance lease, financial deriva+ve, or any arrangement that gives rise to

interest, discounts or other finance charges that are deduc+ble in the

computa+on of income chargeable under the head “Profits and gains of

businessorprofession”.‖

A s ses sment

Year2018-19

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

…contd. [2. International Taxation]

10

Title Section Changes proposed Effective from

Computa=onof

MAT/AMTcreditin

caseofforeigntax

credit

115JAA

and

115JD

§ AnewRule128wasinsertedin2016toprovidethemechanismforgrantof

ForeignTaxCredit(FTC).

§ TheRuleprovidesthatthecreditofforeigntaxcanalsobeallowedagainst

MAT/AMT.

§ Aspersubrule7ofRule128,iftheamountofFTCavailableexceedstheMAT/

AMTliability,suchexcessamountofFTCamountshallbeignoredandwillnot

becarriedforward.

§ Now,byamendingtheSec+on115JAAand115JD,thescopeofunduebenefit

throughpossiblecarriedforwardhasbeencompletelyrestricted.

Assessment

Year2018-19

MinimumAlternate

Tax(MAT)provisions

amendedtobeinline

withIndAS

Amendment

toSec+on

115JB

§ Since,theGovernmenthasno+fiedIndASforcertaincompanies,thebook

profitofsuchcompaniesasperIndASfinancialstatementswillbedifferent

fromthebookprofitsaspertheexis+ngIndianGAAP.

§ Basedontherecommenda+onsofLohiaCommioee,amendmentshavebeen

madeinSec+on115Bforthecomputa+onofMATliabilityforIndAScompliant

companiesintheyearofadop+onandthereaher.

Assessment

Year2017-18

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

…contd. [2. International Taxation]

11

Title Section Changes proposed Effective from

Enablingclaimof

creditforforeigntax

paidincasesof

dispute

155 § Currently,theIncomeTaxAct,1961doesnotcontainanyprovisionforthe

amendmentofassessmentorderifthedisputeofforeigntaxpaidbythe

assesseegotseoledaherthein+ma+onorassessment.

§ However,Rule128(4)relatedtoForeignTaxCreditalreadycontainsthe

provisionwhichallowsthecreditofdisputedFTCsubjecttocertaincondi+ons.

§ Now,anenablingprovisionhasbeenmadeinIncomeTaxAct,1961by

amendingtheSec+on155andaddingasubsec+on14Awhichprovidesa

mechanismfortherec+fica+onoftheassessmentorder.

§ AsperSub-sec+on(14A),AOwillamendtheorderofassessmentorin+ma+on

iftheassesseefurnishesfollowingdocumentswithin6monthsfromtheendof

themonthinwhichthedisputeisseoled:

o Proofforpaymentofforeigntaxliability

o Proofofseolementofdispute

o Anundertakingthatcreditofsuchforeigntaxhasnotbeenclaimed.

Assessment

Year2018-19

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

…contd. [2. International Taxation]

12

Title Section Changes proposed Effective from

ConcessionalTDS

rateunderSec=on

194LC

194LC § Undertheexis+ngprovisions,ifborrowingsinforeigncurrencyismadeundera

loanagreemententeredintobetween01-07-2012and01-07-2017orbywayof

long-termbondsissuedbetween01-10-2014and01-07-2017,taxisdeductedat

therateof5%inrespectofinterestpayabletonon-residents.

§ The eligible period for the applicability of concessional rate of TDS has been

extended=ll1stJuly,2020from1stJuly,2017.

§ Thebenefitofconcessionalrateshallnowbeextendedtorupeedenominated

bondsissuedoutsideIndiabefore01.07.2020.Thisamendmentwilltakeeffect

retrospec+velyfrom01.04.2016.

Assessment

Year2018-19

Extensionofeligible

periodof

concessionaltaxrate

underSec=on194LD

194LD § Undertheexis+ngprovisions,alowerTDSrateof@5%isapplicableinthecase

of interest payable to FIIs and QFIs on their investments in Government

securi+es.

§ SuchbenefitoflowerTDSiscurrentlyavailableifsuchinterestispayableonor

aher1stJune,2013butbefore1stJuly,2017.

§ The eligible period for the applicability of concessional rate of TDS has been

extended=ll1stJuly,2020from1stJuly,2017.

Assessment

Year2018-19

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

3. Discouragement of cash transactions

Title Section Changes proposed Effective from

Measuresto

discouragecash

transac=ons

40A(3) § Under the exis+ng provisions, expenditure incurred in cash beyond the

monetarylimitofRs.20,000toapersoninasingledayisdisallowed.

§ In order to further dis-incen+vise cash transac+on, exis+ng threshold limit of

cashpayment to aperson in a singledayhasbeen reduced tohalf, fromRs.

20,000toRs.10,000.

Asses sment

Year2018-19

Limitspecifiedfor

Capitalexpenditurein

cash

43&

35AD

§ Currently, there is no provision in theAct to disallow the capital expenditure

incurredincash.

§ Therefore, to discourage cash payments for capital expenditure, any cash

paymentsaboveRs.10,000shallnotbeconsideredtodetermineactualcostof

assetunderSec+on43(1).

§ Further,no deduc=ons shall be available under Sec+on 35AD for any capital

expenditureincashinexcessofRs.10,000.

A s ses sment

Year2018-19

13

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

...contd. [3. Discouragement of cash transactions]

Title Section Changes proposed Effective from

Taxincen=vefor

digitalpayments

44AD § Aspertheexis+ngprovisionsunderthepresump+veincomeschemeincaseof

eligiblebusiness,asumequalto8%ofthetotalturnoverorgrossreceiptsshall

bedeemedtobetheprofitsandgainsofsuchbusinesses.

§ In order to promote digital transac+ons and to encourage small unorganised

businesstoacceptdigitalpayments,thepresump+veincomeu/s44ADshallbe

deemedtobe6%ofthegrossreceipts.

§ However, this lower rate of 6% shall be applicable only in respect of total

turnoverorgrossreceiptsreceivedthroughpresceribedbankingchannel.

§ Theexis+ngrateof8%forthepresump+veincomeshallcon+nuetoapplyifthe

paymentisreceivedsbyanyothermode.

§ Payment received during the previous year or before the due date of return

filinginrespectofthatpreviousyearwillbeeligibleforthereducedrate.

1st April’2017

(Assessment

Year2018-19)

14

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

...contd. [3. Discouragement of cash transactions]

Title Section Changes proposed Effective from

Restric=ngcash

dona=ons

80G § Aspertheexis+ngprovisions,nodeduc+onisallowedforthecashdona+onsin

excessofRs.10,000.

§ To move towards a cash less economy and reduce the genera+on and

circula+onofcash,thethresholdlimitfortheavailmentofdeduc+onhasnow

beenreducedtoRs.2,000fromRs.10,000.

A s ses sment

Year2018-19

Transac=onsincash

aboveRs.3.lakhis

prohibited

269ST

&

271DA

§ InordertoachievethemissionoftheGovernmenttomovetowardsacashless

economyandtoreducethegenera+onandcircula+onofblackmoney,anew

Sec+on269SThasbeeninserted.

§ AsperSec+on269ST,receiptsofcashinexcessofRs.3lakhisprohibited,ifit

isreceivedfromapersoninasingleday:

‒ inrespectofasingletransac+onor

‒ Inrespectofoneeventoroccasion

§ Acorrespodingpenalprovisionhasbeenintroducedthroughinser+onofanew

Sec+on271DAfornon-complianceofthelimitofRs.3lacs.Itprovidesthelevy

ofapenaltyequivalenttotheamountofsuchreceipt.

§ However,thisrestric+onshallnotapplytoGovernment,anybankingCompany,

postofficesavingsbankoranyotherno+fiedperson.

1st April’2017

(Assessment

Year2018-19)

15

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

4. Other important changes

Title Section Changes proposed Effective from

Exemp=onoflong

termcapitalgainstax

10(38) § Under the exis+ng provisions, income arising from a transfer of long term

capitalasset,beingequityshareofacompanyoraunitofanequityoriented

fund, is exempt from tax if the sale transac+on is undertaken on or aher

01.10.2014andischargeabletoSecuri+esTransac+onTax(STT).

§ Such exemp+on provided under sec+on 10(38) is being misused by certain

persons for declaring their unaccounted income as exempt long-term capital

gainsbyenteringintoshamtransac+ons.

§ With the view to prevent this abuse, such exemp+on for income arising on

transferofequityshareacquiredonoraher01.10.2004shallbeavailableonlyif

theacquisi+onofsharesischargeabletoSTT.

§ However, thisexemp+onshall con+nue ingenuinecaseswhere theSTTcould

nothavebeenpaidlikeacquisi+onofsharesinIPO,FPO,bonusorrightissueby

alistedcompany,acquisi+onbynon-residentinaccordancewithFDIpolicyetc.

A s ses sment

Year2018-19

16

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

...contd. [4. Other important changes]

Title Section Changes proposed Effective from

Ra=onaliza=onof

provisionsofSec=on

10AA

10AA § Under the exis+ng provisions of Sec+on 10AA, deduc+on is allowed from the

total income of an assessee in respect of profits and gains from his unit

opera+nginSEZ.

§ In various cases, courts have taken a view that the deduc+on under Sec+on

10AA is allowed from the total income of the undertaking and not from the

totalincomeoftheassessee.

§ In order to remove this ambiguity, it is clarified that the deduc=on shall be

allowedfromthetotalincomeoftheassesseeandthededuc+onu/s10AAin

nocaseshallexceedthesaidtotalincome.

§ This clarifica+on will reduce the carry forward losses of non-exempted

undertakingsofanassesseetotheextentsamecanbesetoffagainsttheprofits

ofaneligibleundertakingu/s10AA.

As ses sment

Year2018-19

17

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

...contd. [4. Other important changes]

Title Section Changes proposed Effective from

Nono=onalincomefor

housepropertyheldas

stock-in-trade

23 § As per the exis+ng provisions, the assessee is liable to pay tax on deemed

annualvalueofhousepropertylyingvacant.

§ However, excep+on is given in those cases where property is either self-

occupiedorusedforthepurposeofbusinessorprofession.

§ Suchconceptofdeemedannual value is applicableeven forhouseproperty

heldasstock-in-trade.

§ Thisprovisionwascrea+ngprac+caldifficul+esfortherealestatedevelopers

astheyareforcedtopaytaxonno+onalincomeforunsoldflats.

§ In order to provide relief to the real estate developers, who are holding

residen+al property as stock-in-trade, the annual value of such house

propertyshallbedeemedtobeNILforaperiodofupto1yearfromtheend

ofthefinancialyearinwhichthecer=ficateofcomple=onofconstruc=onis

obtained.

Asses sment

Year2018-19

18

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

...contd. [4. Other important changes]

Title Section Changes proposed Effective from

Increaseinthreshold

limitofauditfor

assesseesop=ngfor

presump=vetaxa=on

44AB § TheFinanceAct,2016hasincreasedthethresholdlimitforpresump+vetaxa+on

schemefromRs.1croretoRs.2crores.

§ However,thethresholdlimitforthetaxauditu/s44ABwasnotincreasedtoRs.

2croresforthetaxpayersop+ngforthepresump+vescheme.

§ Inordertoreducethecomplianceburdenofthesmalltaxpayersandfacilitate

the ease of doing business, an eligible person op+ng for presump+ve income

scheme,shallnotberequiredtogethisaccountsauditedifthetotalturnoveror

thegrossreceiptsoftherelevantpreviousyeardoesnotexceedRs.2crores.

As ses sment

Year2017-18

Nocapitalgainson

conversionof

preferencesharesto

equity

47 § Conversionofbondordebentureofacompanyintoshareordebentureofthat

company are outside the scope of ‘transfer’ under the current provisions of

Sec+on47.

§ However, there is no clarity on similar tax neutrality for conversion of

preferenceshareofacompanyintoitsequityshare.

§ Amendments to Sec+on 47 have beenmade to clarify that the conversion of

preferencesharesintoequityshallnotberegardedastransfer.

A s ses sment

Year2018-19

19

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

...contd. [4. Other important changes]

Title Section Changes proposed Effective from

Shi_ingofbaseyear

ofCostInfla=onIndex

from1981to2001for

thecomputa=onof

CapitalGain

48&55 § Undertheexis+ngprovisions,forthecomputa+onofcapitalgainsinrespectof

anassetacquiredbefore01.04.1981,theassesseeisallowedanop+onof:

§ eithertakingthefairmarketvalueoftheassetason01.04.1981

§ ortheactualcostoftheassetascostofacquisi+on.

§ Now,thebaseyearhasbeenshi_edfrom1981to2001i.e.,2001-2002shallbe

takenasthebaseyearandtheGovernmentshallno+fytherevisedCost

Infla+onIndexstar+ngfromtheyear2001-2002.

§ Itwillremovethedifficul+esduetothenon-availabilityofrelevantinforma+on

forthecomputa+onofthefairmarketvalue(FMV)ofsuchassetason

01.04.1981.

§ Further,itmayresultinsignificantsavinginlongtermcapitalgainliabilityas

indexedcostofacquisi+onisgoingtoincrease.

As ses sment

Year2018-19

Expandingthescopeof

long-termbonds

54EC § Theexis+ngSec+on54ECallowsexemp+ons to theextentofRs. 50 lakhs in

respectoflong-termcapitalgaininvestedinbondsissuedbyNHAIorRECL.

§ To expand the scope of long-term bonds, the investment in any bond

redeemableaher3yearswhichhavebeenno+fiedbytheCentralGovernment

inthisbehalfshallalsobeeligibleforexemp+onunderSec+on54EC.

As ses sment

Year2018-19

20

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

...contd. [4. Other important changes]

Title Section Changes proposed Effective from

Gi_staxableinhands

ofeveryperson,not

onlyIndividualorHUF

56 § Sec+on 56(2)(vii) provides for the taxability of any sum of money or any

property received without considera+on or for inadequate considera+on in

excessofthespecifiedlimitofRs.50,000.

§ Theexis+ngprovisionsofSec+on56(2)(vii)areapplicabletoanIndividualand

HUFonly.

§ Thescopeofthisprovisioniswidenedbyintroducinganewclause56(2)(x)so

astocoveralltaxpayerswithinitsambit.

1st April’2017

(Assessment

Year2018-19)

Clarifica=onwith

regardto

interpreta=onof

‘terms’usedinDTAA

90&90A § In its final report, the Income-tax simplifica+on commioeehas suggested to

bring inmoreclarity intheAct inrespectof interpreta+onof 'terms'usedin

an agreement entered under sec+on 90 or 90A to reduce the avoidable

li+ga+onrelatedtotaxa+onofnon-residents.

§ Governmenthasacceptedtherecommenda+onandhasinsertedExplana+on

4inSec+on90&90Awhichclarifiesthatany‘term’usedinanagreement(i.e.

DTAA), entered into under Sec+on 90 and 90A of the Act, but not defined

under the said agreement, the said term is proposed to be assigned the

meaningasdefined intheActandanyexplana+ongivento itbytheCentral

Government.

Contd…

Asses sment

Year2018-19

21

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

...contd. [4. Other important changes]

Title Section Changes proposed Effective from

…Contd.(Clarifica+on

withregardto

interpreta+onof

‘terms’usedinDTAA)

90&90A § Inthisconnec+on,itshouldbeobservedthatasperAr+cle2ofDTAAentered

intobyGovernmentofIndiawithGovernmentofothercountries,itisagreed

that the competent authori+es of the Contrac+ng States shall no+fy each

other of any significant changes which have been made in their respec+ve

taxa+onlawsandofanyofficialpublishedmaterialconcerningtheapplica+on

oftheConven+on.

§ Further, Ar+cle 3 ofDTAA states that any termnot otherwise defined shall,

unlessthecontextotherwiserequires,havethemeaningwhich ithasunder

thelawsofthatContrac+ngStaterela+ngtothetaxeswhicharethesubjectof

thisConven+on.

§ The phrase 'unless the context otherwise requires' is absent under the

proposedamendmenttotheAct.

§ Though,theinten+onoftheGovernmentistosimplifytheprovisiontoavoid

possible li+ga+onsbut its actual applica+onmayhave theadverseeffecton

theDTAA’s.

A s ses sment

Year2018-19

22

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

...contd. [4. Other important changes]

Title Section Changes proposed Effective from

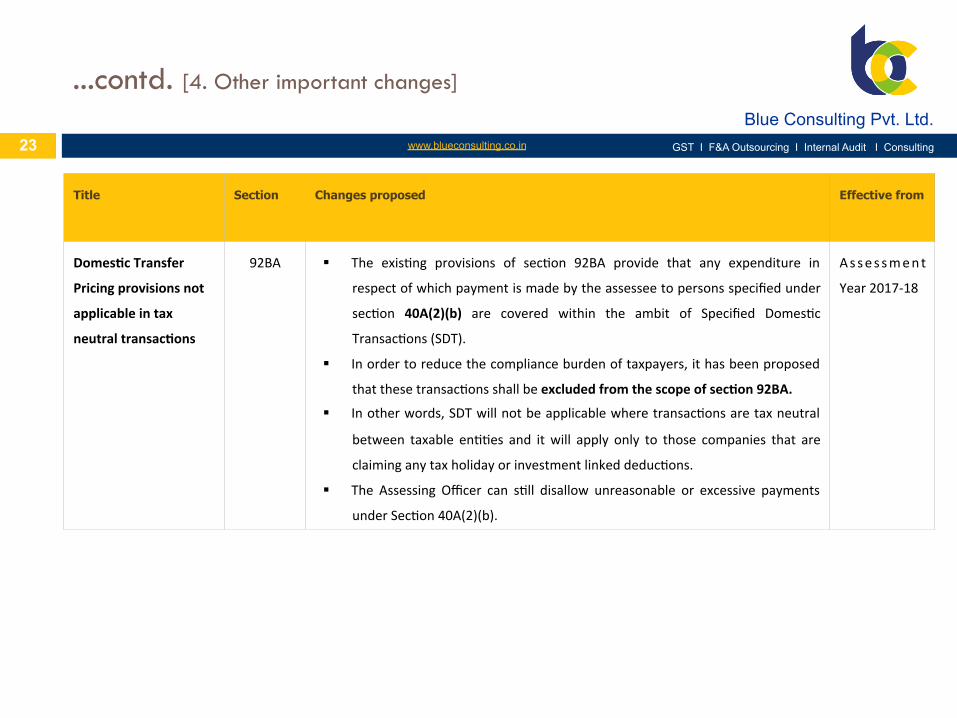

Domes=cTransfer

Pricingprovisionsnot

applicableintax

neutraltransac=ons

92BA § The exis+ng provisions of sec+on 92BA provide that any expenditure in

respectofwhichpaymentismadebytheassesseetopersonsspecifiedunder

sec+on 40A(2)(b) are covered within the ambit of Specified Domes+c

Transac+ons(SDT).

§ Inordertoreducethecomplianceburdenoftaxpayers,ithasbeenproposed

thatthesetransac+onsshallbeexcludedfromthescopeofsec=on92BA.

§ Inotherwords,SDTwillnotbeapplicablewheretransac+onsaretaxneutral

between taxable en++es and itwill apply only to those companies that are

claiminganytaxholidayorinvestmentlinkeddeduc+ons.

§ The Assessing Officer can s+ll disallow unreasonable or excessive payments

underSec+on40A(2)(b).

A s ses sment

Year2017-18

23

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

...contd. [4. Other important changes]

Title Section Changes proposed Effective from

Clarifica=onregarding

theapplicabilityof

Sec=on112

112 § Undertheexis+ngprovisions,concessionalrateof10%isprovidedforlong-

termcapitalgainsarising fromthetransferofunlistedsecuri+es incaseof

non-resident.

§ The ambiguity as to applicability of this provision to share of a private

companywasclarifiedbytheFinanceAct,2016,w.e.f.01-04-2017.

§ As the concessional rate in sec+on112(1)(c)wasprovidedw.e.f. 1stApril,

2013, therewas uncertainty about the applicability of the amendment to

theinterveningperiod.

§ With a view to resolve the above uncertainty, it is proposed that the

effec+vedateofamendmentmadetosec+on112(1)(c)(iii)videFinanceAct,

2016shallbew.r.e.f.01-04-2013insteadofw.e.f.01-04-2017.

A p p l i c a b l e

retrospec+vely

f r o m

A s s e s s m e n t

Year2013-14

24

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

...contd. [4. Other important changes]

Title Section Changes proposed Effective from

Incomefromtransfer

ofcarboncreditstobe

taxedat10%

115BBG § Presently, department has been trea+ng the income on transfer of carbon

creditsasbusinessincomesubjecttotaxattherateof30%.

§ However,divergentdecisionshavebeengivenbythecourtsontheissueasto

whether the income receivedor receivable on transfer of carbon credit is a

revenueorcapitalreceipt.

§ To stop any further li+ga+on, a new sec+on 115BBG has been inserted to

providethatanyincomefromtransferofcarboncreditshallbetaxableatthe

concessionalrateof10%(plusapplicablesurchargeandcess).

§ Noexpenditureorallowanceshallbeallowedfromsuchincome.

As ses sment

Year2018-19

Ra=onaliza=onof

taxa=onofincomeby

wayofdividend

115BBDA § Under the exis+ng provisions, dividend income in excess of Rs. 10 lakh is

chargeabletotaxatherateof10%incaseofanassesseebeinganindividual,

HUF,firmwhoareresidentinIndia.

§ The provisions of this Sec+on shall now be applicable to all the resident

assesseesexceptdomes+ccompanyandcertainfunds,trusts,ins+tu+ons,etc.

Contd…

Asses sment

Year2018-19

25

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

...contd. [4. Other important changes]

Title Section Changes proposed Effective from

…Contd

(Ra+onaliza+onof

taxa+onofincomeby

wayofdividend)

115BBDA § Therefore, AOP, BOI and other ar+ficial juridical persons including Private

Trusts are also liable to pay tax @10% if they receive dividend income

exceedingRs.10lakhs.

As ses sment

Year2018-19

MAT/AMTcarry

forward=melimit

increased

115JAA

(2A)

§ Undertheexis+ngprovisions,taxcreditinrespectofMinimumAlternateTax

(MAT)/AlternateMinimumTax(AMT)canbecarriedforwarduptothetenth

assessmentyears.

§ Withaviewtoproviderelieftotheassessee’spayingMAT/AMT,itisproposed

toprovideMAT/AMTcreditdeterminedcanbecarriedforwarduptofi_eenth

assessmentyears.

Asses sment

Year2018-19

26

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

...contd. [4. Other important changes]

Title Section Changes proposed Effective from

Exemp=onfromTDS

oninsurance

commission

194D § Asperthecurrentprovisions,anypaymentofinsurancecommissionaboveRs.

15,000shallbesubjecttoTDS@5%u/s194D.

§ Further,noop+on isallowed to theagent toavoid thededuc+onofTDSby

submizngtheForm15G/HunderSec+on197A.

§ Therefore,inordertoreducethecomplianceburdenincaseofIndividualsand

HUFs,sec+on197Ahasbeenamendedsoas toallowtheagent tofileForm

No.15G/15Htoreceivetheinsurancecommissionwithoutdeduc=onofTax

atSource(TDS).

June01,2017

LowerTDSfrom

paymenttocallcentre

194J § Undertheexis+ngprovisions,feeforprofessionalservicesorfeefortechnical

servicespaidtocallcentresaresubjecttoTDS@10%u/s194J.

§ Toreducethecomplianceburdenandtopromotetheeaseofdoingbusiness,

suchTDSratehasbeenreducedfrom10%to2%.

June01,2017

27

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

...contd. [4. Other important changes]

Title Section Changes proposed Effective from

FurnishingofPANin

TCS

206CC § AnewSec+on206CChasbeeninsertedintheIncomeAct,1961strengthening

themechanismofcollec+onoftaxatsource.

§ Anypersonpayinganysumoramount,onwhichtax iscollectableatsource

shallfurnishhisPANtothepersonresponsibleforthecollec+onoftax.

§ Incaseoffailure inthefurnishingofPAN,taxshallbecollectedattwicethe

ratemen=onedintherelevantSec=onor@5%,whicheverishigher.

§ The requirement to furnishPAN shall not apply to anon-residentwhodoes

nothaveapermanentestablishmentinIndia.

1st April’2017

(Assessment

Year2018-19)

Interestonrefunddue

todeductor

244A § Asperexis+ngprovisions,interestispayableontherefundamountduetoan

assesseeanaccountofexcesspaymentofadvancetax,TDS,TCSetc.

§ Currently,nointerestispaidtothedeductorifexcessTDShasbeenaccidently

deductedanddeposited.

§ Hence,[email protected]%permonth.

§ Thesimpleinterestshallbecalculatedfortheperiodbeginningfromthedate

onwhichclaimismadeandendingonthedateonwhichrefundisgranted.

§ Incaseofanappeal,theinterestshallbepayablebeginningfromthedateon

whichtaxispaidandendingonthedateonwhichrefundisgranted.

1st April’2017

(Assessment

Year2018-19)

28

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

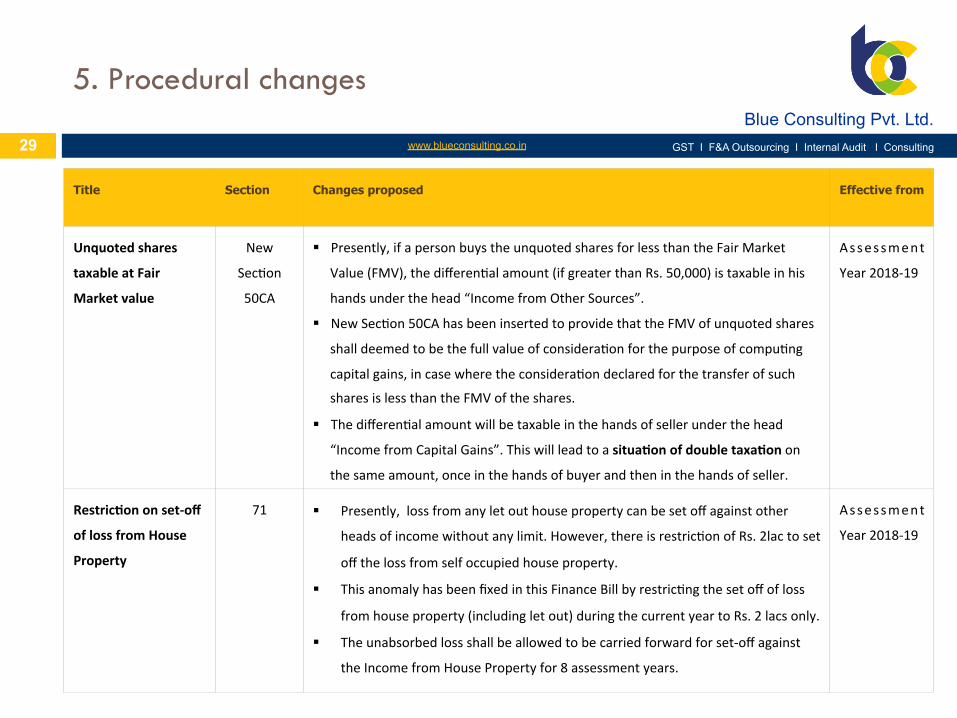

5. Procedural changes

29

Title Section Changes proposed Effective from

Unquotedshares

taxableatFair

Marketvalue

New

Sec+on

50CA

§ Presently,ifapersonbuystheunquotedsharesforlessthantheFairMarket

Value(FMV),thedifferen+alamount(ifgreaterthanRs.50,000)istaxableinhis

handsunderthehead“IncomefromOtherSources”.

§ NewSec+on50CAhasbeeninsertedtoprovidethattheFMVofunquotedshares

shalldeemedtobethefullvalueofconsidera+onforthepurposeofcompu+ng

capitalgains,incasewheretheconsidera+ondeclaredforthetransferofsuch

sharesislessthantheFMVoftheshares.

§ Thedifferen+alamountwillbetaxableinthehandsofsellerunderthehead

“IncomefromCapitalGains”.Thiswillleadtoasitua=onofdoubletaxa=onon

thesameamount,onceinthehandsofbuyerandtheninthehandsofseller.

Assessment

Year2018-19

Restric=ononset-off

oflossfromHouse

Property

71 § Presently,lossfromanyletouthousepropertycanbesetoffagainstother

headsofincomewithoutanylimit.However,thereisrestric+onofRs.2lactoset

offthelossfromselfoccupiedhouseproperty.

§ ThisanomalyhasbeenfixedinthisFinanceBillbyrestric+ngthesetoffofloss

fromhouseproperty(includingletout)duringthecurrentyeartoRs.2lacsonly.

§ Theunabsorbedlossshallbeallowedtobecarriedforwardforset-offagainst

theIncomefromHousePropertyfor8assessmentyears.

Assessment

Year2018-19

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

…contd. [5. Procedural changes]

30

Title Section Changes proposed Effective from

Shorteningof=me

forfilingrevised

return

139(5)

§ Undertheexis+ngprovisions,the+melimitforfilingtherevisedreturnwas2

yearsfromtheendofthepreviousyear.

§ The+melimitforfilinghasnowbeenreducedfrom2yearsto1yearfromthe

endofthepreviousyear.

Assessment

Year2018-19

Processingofreturn

withintheprescribed

=meandenable

withholdingofrefund

incertaincases

143(1D)

and

241A

§ Undertheexis+ngprovisions,processingofareturnisnotnecessarywherea

no+cehasbeenissuedtotheassesseein+ma+ngselec+onofcaseforscru+ny

assessment.

§ ThisprovisionallowstheAssessingOfficertowithholdtheprocessingofreturn,

whererefundisdue,+lltheverylastdateofthecomple+onofscru+ny

assessment.

§ Sec+on143(1D)hasbeensubs+tutedtorestricttheapplicabilityoftheabove

provisionsforanyreturnfiledfortheassessmentyearstar+ngfrom1st

April’2017.

Contd…

Assessment

Year2017-18

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

…contd. [5. Procedural changes]

31

Title Section Changes proposed Effective from

…contd.(Processing

ofreturnwithinthe

prescribed+meand

enablewithholdingof

refundincertain

cases)

143(1D)

and

241A

§ Itmeans,AOisnowliabletoprocessthereturnwithinoneyearfromtheendof

FinancialYearinwhichreturnhasbeenfiled.

§ However,toaddresstheconcernofrecoveryindoub_ulcases,anewSec+on

241AshallcomeintoforceauthorizingtheAOtowithholdthepaymentof

refundamount,ifsuchgrantofrefundmayadverselyaffecttherecoveryof

revenue.

Assessment

Year2017-18

Reduc=onofthe=me

limitforcomple=on

ofassessment

153 § Undertheexis+ngprovisions,the+melimitformakingassessmentunderSec+on

143or144,fortheassessmentyear2017-18orbefore,was21monthsfromthe

endoftheassessmentyearinwhichtheincomewasfirstassessable.

§ The+melimithasnowbeenreducedto–

§ ForAssessmentYear2018-19:18monthsfromtheendoftheassessment

Year.

§ ForAssessmentYear2019-20onwards:12monthsfromtheendofthe

assessmentyear

Assessment

Y e a r

2 0 1 8 - 1 9 /

Assessment

Year2019-20

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

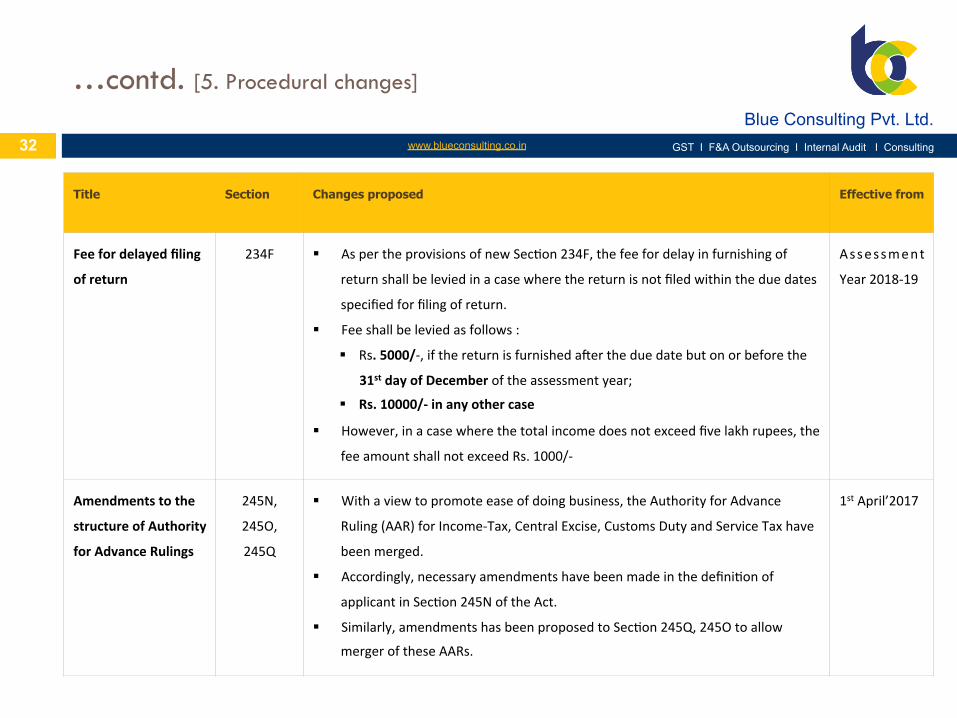

…contd. [5. Procedural changes]

32

Title Section Changes proposed Effective from

Feefordelayedfiling

ofreturn

234F § AspertheprovisionsofnewSec+on234F,thefeefordelayinfurnishingof

returnshallbeleviedinacasewherethereturnisnotfiledwithintheduedates

specifiedforfilingofreturn.

§ Feeshallbeleviedasfollows:

§ Rs.5000/-,ifthereturnisfurnishedahertheduedatebutonorbeforethe

31stdayofDecemberoftheassessmentyear;

§ Rs.10000/-inanyothercase

§ However,inacasewherethetotalincomedoesnotexceedfivelakhrupees,the

feeamountshallnotexceedRs.1000/-

Assessment

Year2018-19

Amendmentstothe

structureofAuthority

forAdvanceRulings

245N,

245O,

245Q

§ Withaviewtopromoteeaseofdoingbusiness,theAuthorityforAdvance

Ruling(AAR)forIncome-Tax,CentralExcise,CustomsDutyandServiceTaxhave

beenmerged.

§ Accordingly,necessaryamendmentshavebeenmadeinthedefini+onof

applicantinSec+on245NoftheAct.

§ Similarly,amendmentshasbeenproposedtoSec+on245Q,245Otoallow

mergeroftheseAARs.

1stApril’2017

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

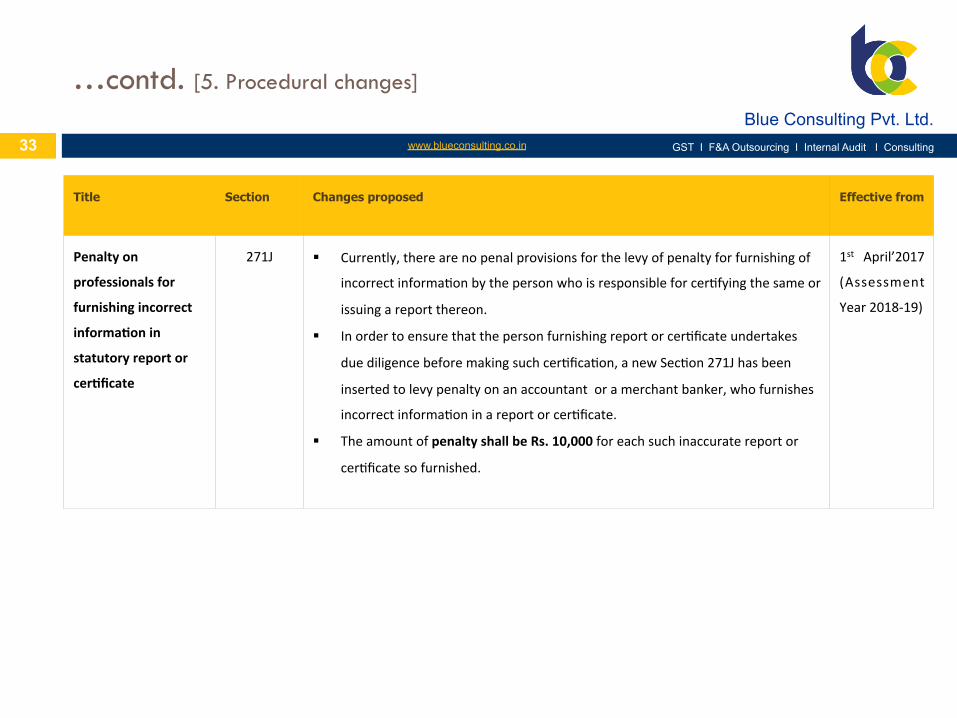

…contd. [5. Procedural changes]

33

Title Section Changes proposed Effective from

Penaltyon

professionalsfor

furnishingincorrect

informa=onin

statutoryreportor

cer=ficate

271J § Currently,therearenopenalprovisionsforthelevyofpenaltyforfurnishingof

incorrectinforma+onbythepersonwhoisresponsibleforcer+fyingthesameor

issuingareportthereon.

§ Inordertoensurethatthepersonfurnishingreportorcer+ficateundertakes

duediligencebeforemakingsuchcer+fica+on,anewSec+on271Jhasbeen

insertedtolevypenaltyonanaccountantoramerchantbanker,whofurnishes

incorrectinforma+oninareportorcer+ficate.

§ TheamountofpenaltyshallbeRs.10,000foreachsuchinaccuratereportor

cer+ficatesofurnished.

1st April’2017

(Assessment

Year2018-19)

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

6. Personal Taxation

34

Title Section Changes proposed Effective from

Individualand

otherstaxrates

§ Nochangeinthebasicexemp+onlimitofindividuals.

§ Rateof tax for assesseeswhose total incomeexceedsRs. 250,000butdoesnot

exceedRs.500,000hasbeenreducedto5%from10%.

§ FollowingarethenewratesofIncomeTaxforIndividuals(HUF,AOP,BOI)-

§ Surcharge–Surcharge@10%shallbeleviedonindividualshavingtaxableincome

betweenRs.50lakhsandRs.1crore.Thesurcharge onincomeexceedingRs.1

croreshallcon+nuetobelevied@15%.

§ Cess–Educa+on Cess and Secondary & Higher Educa+on Cess remains

unchanged.

Assessment

Year2018-19

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

...contd. [6. Personal Taxation]

35

Title Section Changes proposed Effective from

Deduc=onofTDSon

rentpaymentin

caseofcertain

IndividualsandHUF

194-IB § AsperthenewlyinsertedSec+on194-IB,everyIndividualandHUF(notliableto

Tax Audit) paying amonthly rent of Rs. 50,000 ormore shall nowbe liable to

deductTDS@5%.

§ TomakeiteasiertodeductanddeposittheTDS,theIndividualorHUFwouldbe

requiredtodeducttheTDSonlyonceinayear,onthelastmonthpayment.

§ Further,thepersondeduc+ngtheTDSwouldnotberequiredtoobtainTAN.

June01,2017

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

7. About us

36

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting

...contd. [7. About us]

37

Services GST

Consulting services

Consulting services

Finance & Accounts

outsourcing

Internal Audit

For more information about our GST Consulting Services, click here. ︎

www.blueconsulting.co.in

Blue Consulting Pvt. Ltd. GST I F&A Outsourcing I Internal Audit I Consulting 38

Disclaimer This publication is intended as a service to clients and to provide clients with the details of the important budget proposals on direct taxes. It has been prepared for general guidance on matters of interest only, and does not constitute professional advice. No person should act upon the information contained in this publication without obtaining specific professional advice. Due care has been taken while compiling the information ,however no representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication.