Finance avenue - De Tijdstatic.tijd.be/finav/2013/nl/Montea.pdfVerzekering 10% Belfius Insurance 10%...

33

Finance avenue November 16th 2013

Transcript of Finance avenue - De Tijdstatic.tijd.be/finav/2013/nl/Montea.pdfVerzekering 10% Belfius Insurance 10%...

Finance avenue November 16th 2013

Topics

1. Montea

2. Portfolio

3. Highlights of 9 months – year 2013

4. Financial Results 9 months - year 2013

5. Financial structure

6. Conclusion & Outlook 2013

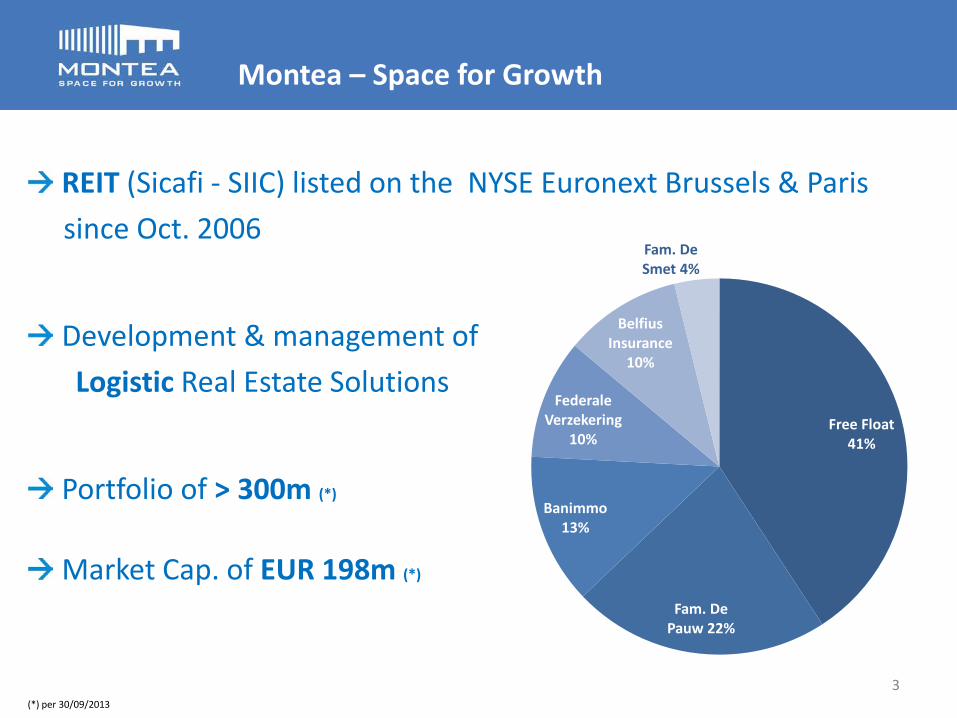

Montea – Space for Growth

REIT (Sicafi - SIIC) listed on the NYSE Euronext Brussels & Paris since Oct. 2006

Development & management of Logistic Real Estate Solutions

Portfolio of > 300m (*)

Market Cap. of EUR 198m (*)

Free Float 41%

Fam. De Pauw 22%

Banimmo 13%

Federale Verzekering

10%

Belfius Insurance

10%

Fam. De Smet 4%

(*) per 30/09/2013

3

Regulatory Framework of REIT

Belgian REIT status as a “Vastgoedbevak” / “Sicafi” •Listed on the stock exchange with mandatory free float of at least 30%

•Limited in its activities to property investments

•Tax transparency

Low Risk characteristics •Stringent supervision by the supervisory authority (FSMA)

•Portfolio diversification requirements and independent quarterly appraisals

•Restrictions with respect to the use of leverage, min. pay-out

Operating under the defensive umbrella of the respective REIT regime •Belgian REIT “Sicafi” or “Vastgoedbevak”

•French REIT “SIIC” or “Société d’Investissement Immobilier Cotée”

•Dutch REIT “FBI” or Fiscale Belegginsinstelling”

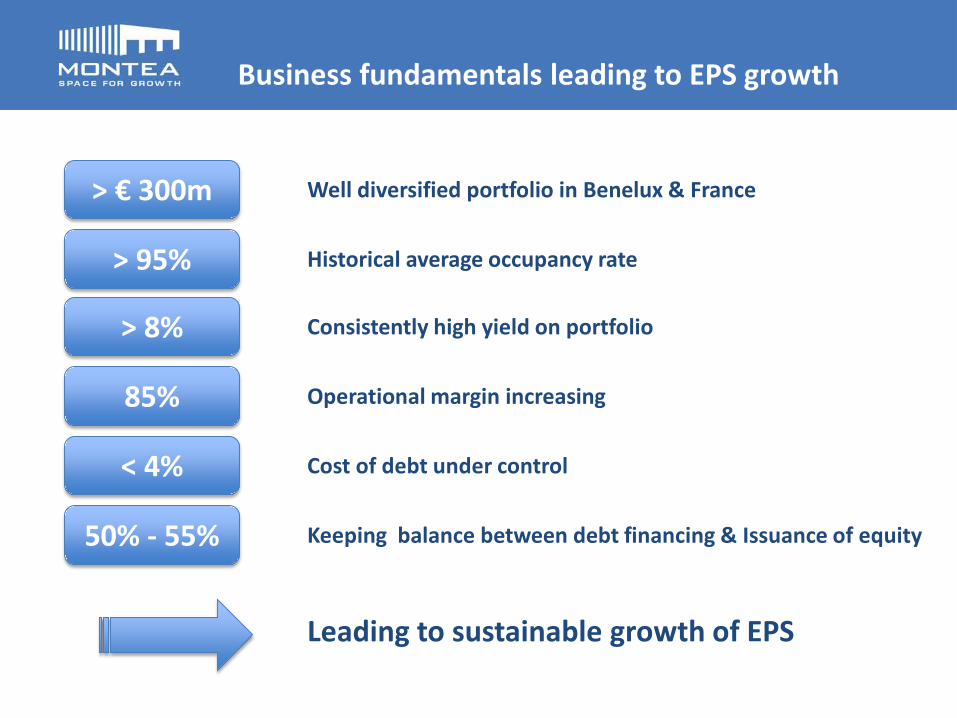

Business fundamentals leading to EPS growth

> € 300m

> 95%

> 8%

85%

< 4%

50% - 55%

Well diversified portfolio in Benelux & France

Historical average occupancy rate

Consistently high yield on portfolio

Operational margin increasing

Cost of debt under control

Keeping balance between debt financing & Issuance of equity

Leading to sustainable growth of EPS

3 Key Words

Warehousing • Land value has a higher share in the total

value than in other asset classes

• Life cycle of warehousing > other asset classes

• Renovation cost < than other RE asset classes

Pure player • Ambition to be best in class through

specialisation (Logistics, Real Estate & Finance)

• Ambition to be top of mind towards other market players (logistic players, brokers ...)

End investor No speculative development: therefore possible business partner for land owners and developers. Long term vision with focus on quality & sustainability (for example Blue Label)

400€/m²

45€/m²

200€/m²

Cost Logistic Development Prime Rent

Cost Land

Cost Development7,5%

2m² land for 1m² logistic development

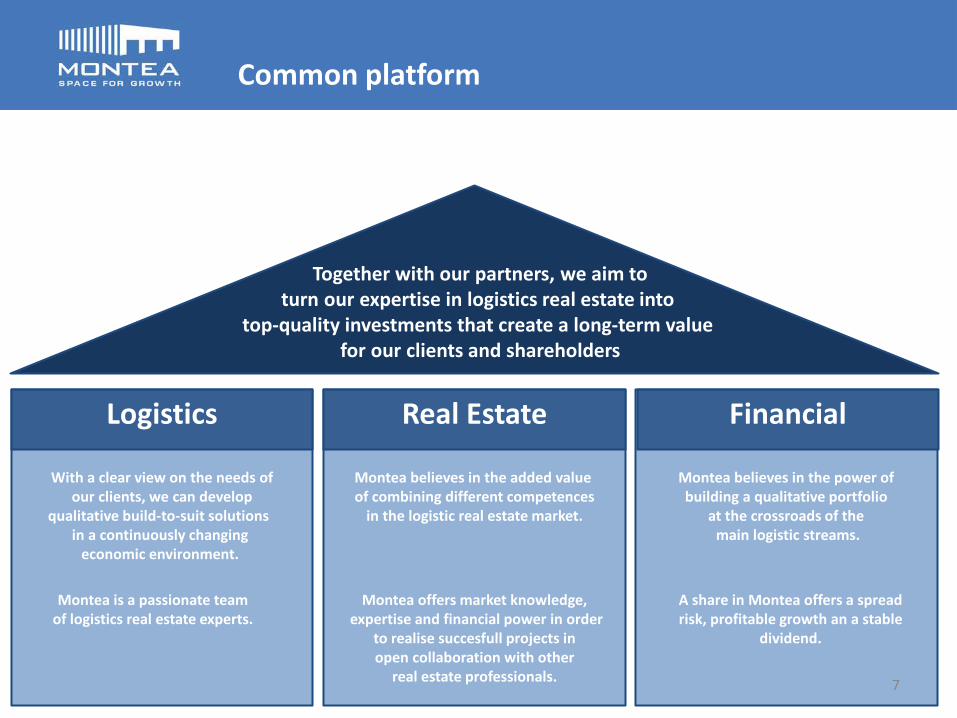

Common platform

Together with our partners, we aim to

turn our expertise in logistics real estate into top-quality investments that create a long-term value

for our clients and shareholders

ddd Logistics

With a clear view on the needs of our clients, we can develop

qualitative build-to-suit solutions in a continuously changing

economic environment.

Montea is a passionate team of logistics real estate experts.

Real Estate

Montea believes in the added value of combining different competences

in the logistic real estate market.

Montea offers market knowledge, expertise and financial power in order

to realise succesfull projects in open collaboration with other

real estate professionals.

Financial

Montea believes in the power of building a qualitative portfolio

at the crossroads of the main logistic streams.

A share in Montea offers a spread risk, profitable growth an a stable

dividend.

7

Management Team

Jo De Wolf Chief Executive Officer

• Active in professional real estate since 1997

• Experience in commercial functions and capital markets at Leasinvest, Extensa (both AvH) and The Brussels Airport Company

Peter Verlinde Chief Financial Officer

• Experience in various financial functions (including stock quoted cy’s)

Peter Demuynck Chief Commercial Officer Belgium

• Active in professional real estate since 1993

• Former Head of Industrial department at Cushman & Wakefield

• Well connected to all major players in Belgian industrial real estate

Jean De Beaufort Director France

• Active in professional real estate since more than 20 years

• Several functions @ CBRE and Jones Lang Lasalle

• Director logistics and light industrial @ Keops

• member of Afilog

Peter Snoeck Chief Operational Officer

• Active in logistic real estate since 30 years

• Co-Founder of Montea Comm. VA

Griet Capelle Chief Development Officer Belgium

• Extended international experience in logistics development management (IIG Group)

8

Topics

1. Montea

2. Portfolio

3. Highlights of 9 months – year 2013

4. Financial Results 9 months – year 2013

5. Financing structure

6. Conclusion & Outlook 2013

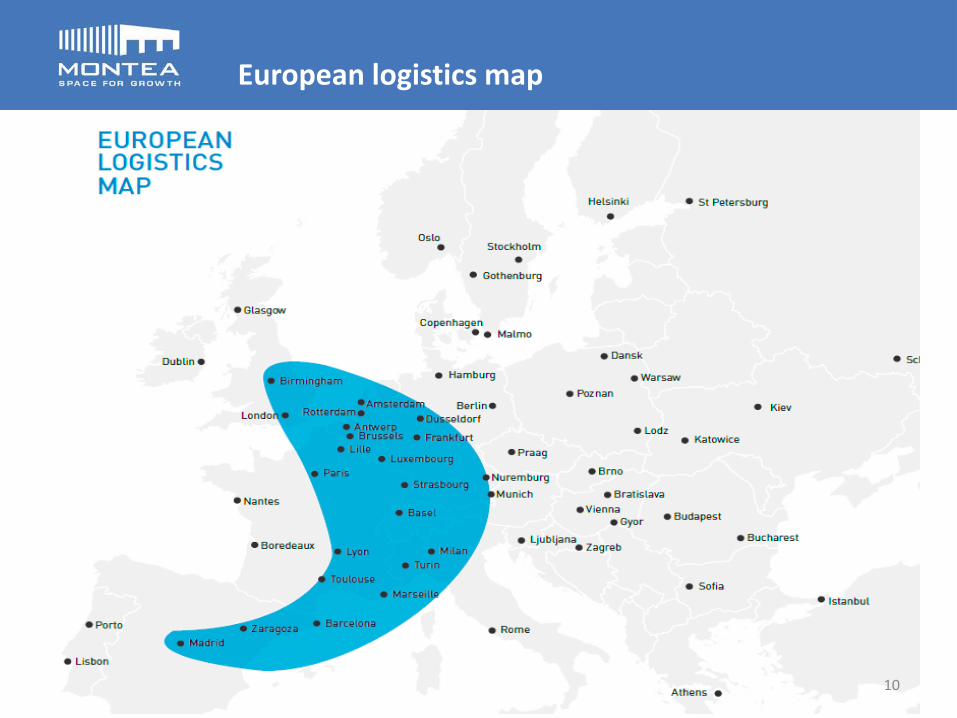

European logistics map

10

Portfolio in Belgium & France …

11

Nr of sites: 18 Fair Value (€m): 180,2 m²: 324.944 Contractual Rent (€m): 13,0 Occupancy rate (*) : 89,1% Yield (**): 7,95%

Nr of sites: 15 Fair Value (€m): 117,5 m²: 218.666 Contractual Rent k€): 10,7 Occupancy rate (*): 100,0% Yield (**): 9,15%

Nr of sites: 33 Fair Value (€m): 297,7 m²: 545.610 Contractual Rent €m): 23,8 Occupancy rate (*) : 93,8% Yield (**): 8,43%

60% 40%

(*) based upon m² (**) when 100% rented

… and entering a new market: The Netherlands

Press Release 09/10/2013

Montea continues to grow with first purchase in the Netherlands

Total area of 36,000m², 24,000m² warehousing / 700m² office space

Investment value of EUR 13.7 million

long-term lease agreement with initial yield of 8.0%

12

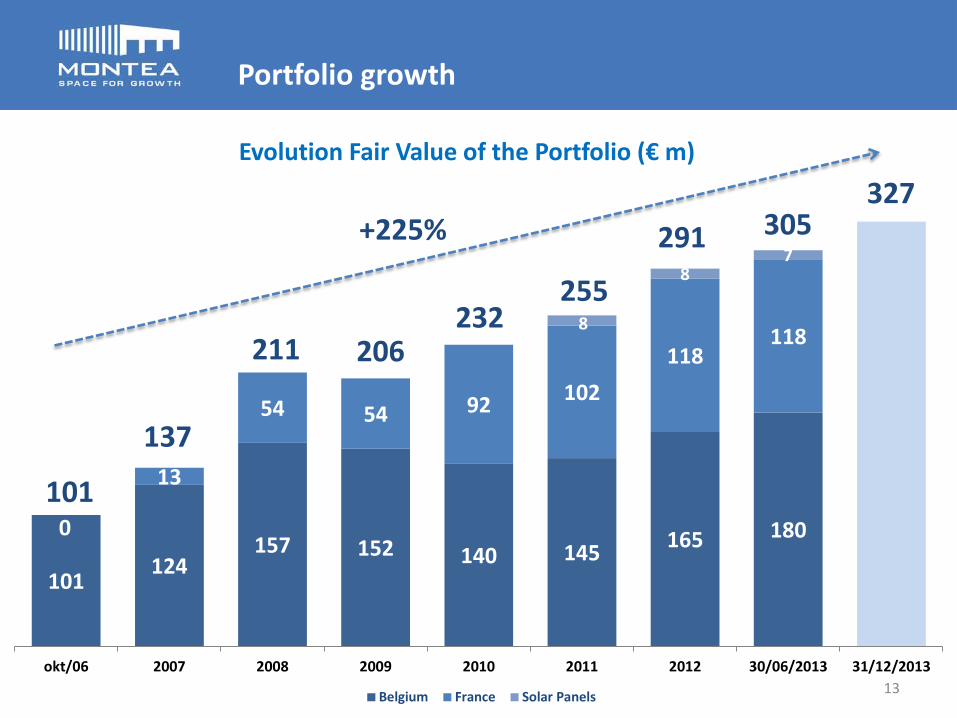

Portfolio growth

101 124

157 152 140 145 165 180 0

13

54 54 92 102 118

118 8

8 7

101

137

211 206 232

255

291 305 327

okt/06 2007 2008 2009 2010 2011 2012 30/06/2013 31/12/2013

Evolution Fair Value of the Portfolio (€ m)

Belgium France Solar Panels

+225%

13

… with declining average age of buildings to an average of 10 years

18,80%

28,67% 33,79%

18,74%

<1998 15j-10j 10j-5j <5j

Aging of Sites (%)

<1998 15j-10j 10j-5j <5j

> 50% of the sites less than 10 years

> 80% of the sites less than 15 years

14

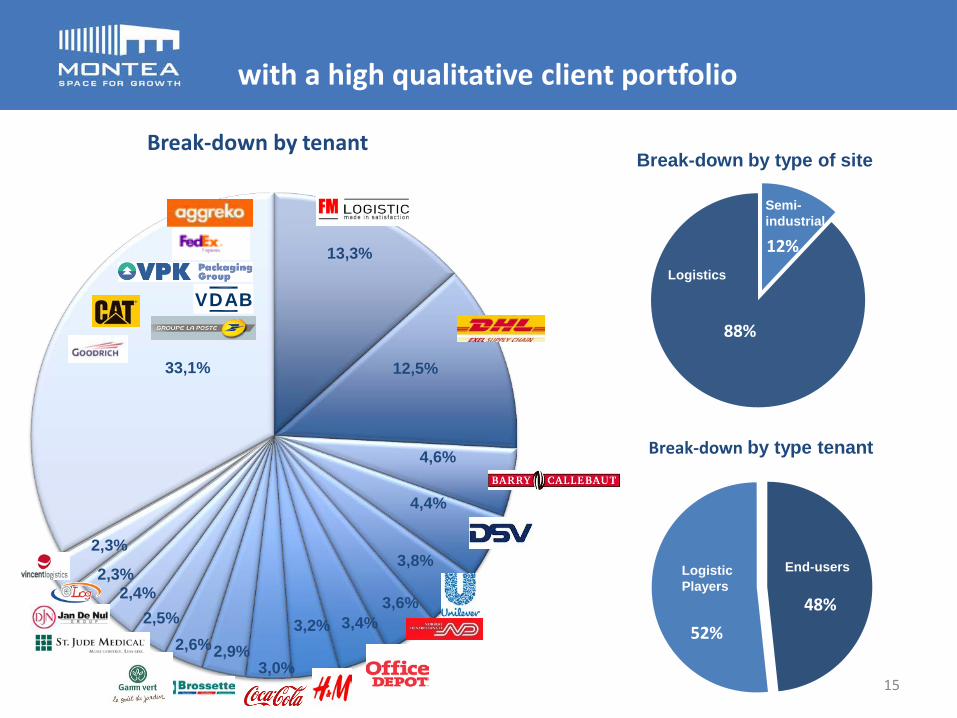

with a high qualitative client portfolio

VDAB

13,3%

4,6%

3,6%

3,8%

3,4%

3,0%

2,5%

2,3%

33,1%

12%

88%

48% 52%

Logistics

End-users Logistic Players

Break-down by type of site

Break-down by type tenant

Break-down by tenant

12,5%

2,3%

15

4,4%

3,2% 2,9% 2,6%

2,4%

Semi- industrial

with occupancy & maturity under control

96,6% 95,6% 92,9%

95,1% 96,5% 96,3% 96,6% 93,8%

94,2%

2007 2008 2009 2010 2011 2012 30/06/2013 30/09/2013 31/12/2013

Long term Target: > 95,0% (1)

(1) At the end of the period based upon m²

(2) Untill first break

4,8

30/09/2013Excl. Solar panels Impact Solar Panels

Long term Target: > 6y (2)

5,2

• Historical occupancy rate > 95%

• Logistics business knows by 3,6,9 contracts

• Increased from 3,5 years in 2010

• Mix between End users & Logistics players

16

Topics

1. Montea

2. Portfolio

3. Highlights of 9 months – year 2013

4. Financial Results 9 months – year 2013

5. Financial structure

6. Conclusion & Outlook 2013

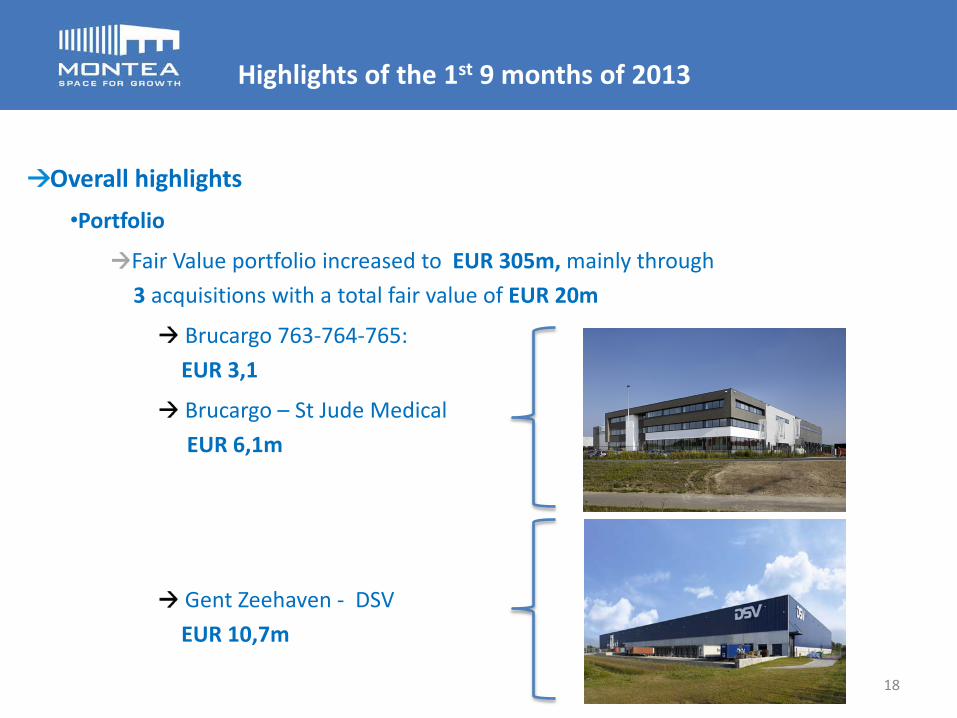

Highlights of the 1st 9 months of 2013

Overall highlights •Portfolio

Fair Value portfolio increased to EUR 305m, mainly through 3 acquisitions with a total fair value of EUR 20m

Brucargo 763-764-765: EUR 3,1

Brucargo – St Jude Medical EUR 6,1m

Gent Zeehaven - DSV EUR 10,7m

18

Highlights of the 1st 9 months of 2013

Overall highlights •Portfolio

Expected increase of FV with EUR 22m to EUR 327m at the end of this year with 2 additional acquisitions:

Puurs, Schoonmansveld 28: EUR 8,0m

Almere – Aware food Group: EUR 14,0m

19

Highlights of the 1st 9 months of 2013

Overall highlights •Portfolio

Divestment of Laken (EUR 2,9m)

Occupancy rate of 93,8% - lifetime contracts of 5,2y

•Financial

NCR of EUR 10,07m (EUR 1,53 per share) – growth of 20 % compared to last year

Operational margin of 83,7%

Successful placement of EUR 30m bonds @ 4,107% -> diversification of financing

50% of shareholders choose for the optional dividend EUR 4,1m equity increase

Forecasted NCR of EUR 13,4m (EUR 2,04 per share) growth of 19% compared to last year

•Other

Change in Board of Directors 3 new directors

20

Highlights of the 1st 9 months of 2013

Rental Activity - new rental contracts for > 22,000m²

•100% occupancy rate in Savigny-Le-Têmple due to Rental contract with LPF for a fixed period of 12y and 8m (8,850m²)

•9y contract with Geodis @ Brucargo (6,600m²)

•6y new rental contract with TNT Innight in Mechelen for 6y fix (6,600m²)

21

Highlights of the 1st 9 months of 2013

Investments •SPA with Group Cordeel for new logistic platform, rented to DSV Solutions in Gent

Total surface of +/- 74,000m²

23,400m² warehouse / 750m² offices

Investment value of EUR 10,9m

9 years fix contract with DSV Solutions

TAPA ‘A’ building

Additional development potential of 17,000m²

•SPA with Group Depaepe for new distribution center, rented St-Jude Medical Total surface of +/- 31,000m²

Still 10,000m² to develop

Total surface of 9,683m²

Investment value of EUR 5,6m

8,5 years fix contract with St-Jude Medical

22

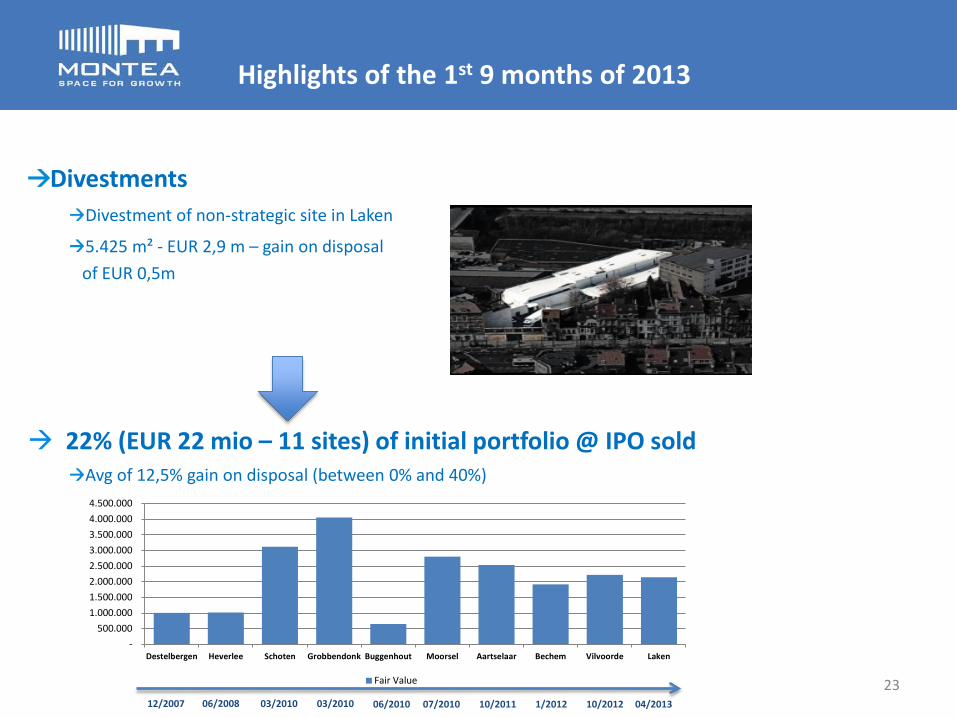

Highlights of the 1st 9 months of 2013

Divestments Divestment of non-strategic site in Laken

5.425 m² - EUR 2,9 m – gain on disposal of EUR 0,5m

22% (EUR 22 mio – 11 sites) of initial portfolio @ IPO sold

Avg of 12,5% gain on disposal (between 0% and 40%)

- 500.000

1.000.000 1.500.000 2.000.000 2.500.000 3.000.000 3.500.000 4.000.000 4.500.000

Destelbergen Heverlee Schoten Grobbendonk Buggenhout Moorsel Aartselaar Bechem Vilvoorde Laken

Fair Value

12/2007 03/2010 06/2008 06/2010 07/2010 10/2011 1/2012 10/2012 04/2013 03/2010

23

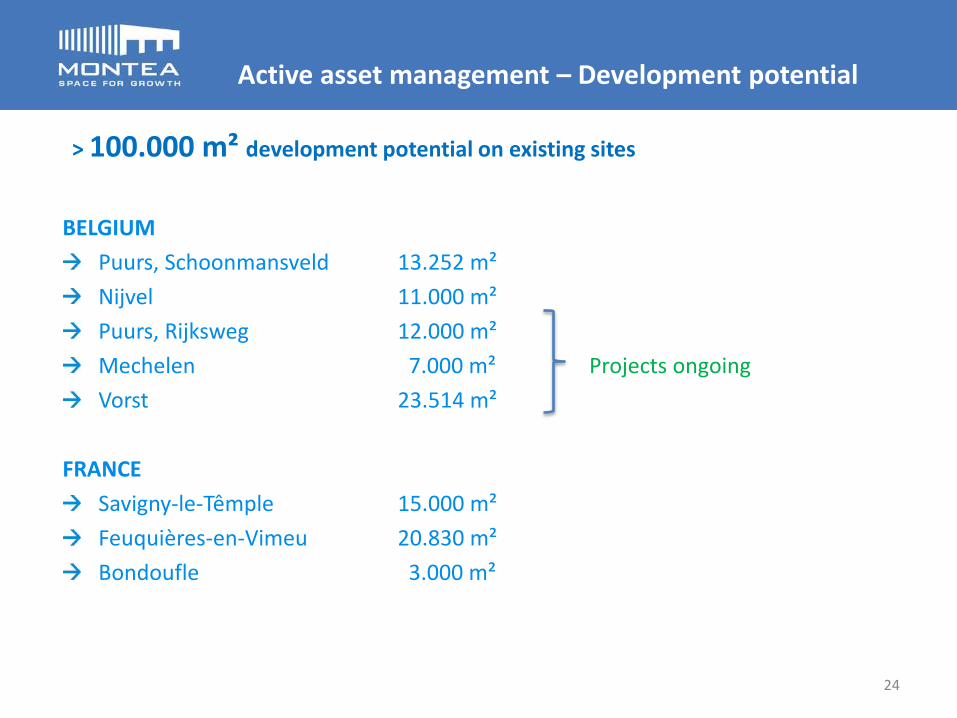

Active asset management – Development potential

BELGIUM

Puurs, Schoonmansveld 13.252 m² Nijvel 11.000 m² Puurs, Rijksweg 12.000 m² Mechelen 7.000 m² Projects ongoing Vorst 23.514 m²

FRANCE

Savigny-le-Têmple 15.000 m² Feuquières-en-Vimeu 20.830 m² Bondoufle 3.000 m²

> 100.000 m² development potential on existing sites

24

Topics

1. Montea

2. Portfolio

3. Highlights of 9 months – year 2013

4. Financial Results 9 months – year 2013

5. Financial structure

6. Conclusion & Outlook 2013

Consolidated Income Statement

+19% Net Rental Result

+17% Operational Margin

+11% Financial Result

+20% NCR +3% NCR / Share

ABBREVIATED CONSOLIDATED 30/09/2013 30/09/2012 PROFIT & LOSS ACCOUNT (EUR) Analytical 9 months 9 months

CURRENT RESULTNET RENTAL RESULT 17.351 14.577

PROPERTY RESULT 17.691 15.149

% compared to net rental result 102,0% 103,9%

TOTAL PROPERTY CHARGES -477 -782

PROPERTY OPERATING RESULT 17.213 14.367

Genera l corporate expenses -2.673 -1.963

Other operating income and expenses -24 2

OPERATING RESULT BEFORE THE PORTFOLIO RESULT 14.516 12.406

% compared to net rental result 83,7% 86,7%

FINANCIAL RESULT -4.417 -3.973

PRE-TAX RESULT (*) 10.100 8.433

Taxes -32 -37

NET CURRENT RESULT 10.068 8.396

per share 1,53 1,51

NON-CURRENT RESULTResult on disposa ls of investment properties 716 79

Resul t on disposa ls of other non-financia l assets 0 0

Changes in fa i r va lue of investment properties -3.571 -4.520

Other portfol io resul t 0 0

PORTFOLIO RESULT -2.855 -4.441

Changes in fa i r va lue of financia l assets and l iabi l i ties 4.723 -6.288 RESULT IN FAIR VALUE OF FINANCIAL ASSETS AND LIABILITIES 4.723 -6.288

NET RESULT 11.936 -2.333

per share 1,81 -0,41 26

Consolidated Balance Sheet

Solar Panels Valorisation done based upon NPV Model

Site of Vilvoorde, sold in July

Total debts of EUR 192,7m of which: • EUR 163,1m financial debts (see financial

structure) • EUR 14,6m neg. Variation of heding

instruments (IAS 39) • EUR 7,5m transitory accounts (mainly

relating to invoiced revenues for future periods)

• EUR 7,5m other debts

CONSOLIDATED 30/06/2013 31/12/2012 BALANCE SHEET (EUR) Conso Conso

NON-CURRENT ASSETS 306.234.847 290.212.151 Intangible assets 113.828 129.520 Investment properties 298.373.799 282.208.783 Other tangible assets 7.710.452 7.837.347 Trade receivables and other non-current assets 36.768 36.502 CURRENT ASSETS 15.019.468 20.492.584 Assets held for sale 0 2.225.000 Trade receivables 8.682.349 6.032.623 Tax receivables and other current assets 975.140 829.921 Cash and cash equivalents 1.920.960 9.063.354 Deferred charges and accrued income 3.441.019 2.341.685 TOTAL ASSETS 321.254.315 310.704.734 TOTAL SHAREHOLDERS' EQUITY 128.515.870 128.146.580 Shareholders' equity attributable to shareholders of the parent company 128.418.212 128.047.535 Minority interests 97.658 99.045 LIABILITIES 192.738.445 182.558.154 Non-current liabilities 176.818.602 140.058.081 Current liabilities 15.919.843 42.500.073 TOTAL SHAREHOLDERS EQUITY AND LIABILITIES 321.254.315 310.704.734

27

Topics

1. Montea

2. Portfolio

3. Highlights of 9 months – year 20132013

4. Financial Results Jun 9 months - 2013

5. Financial structure

6. Conclusion & Outlook 2013

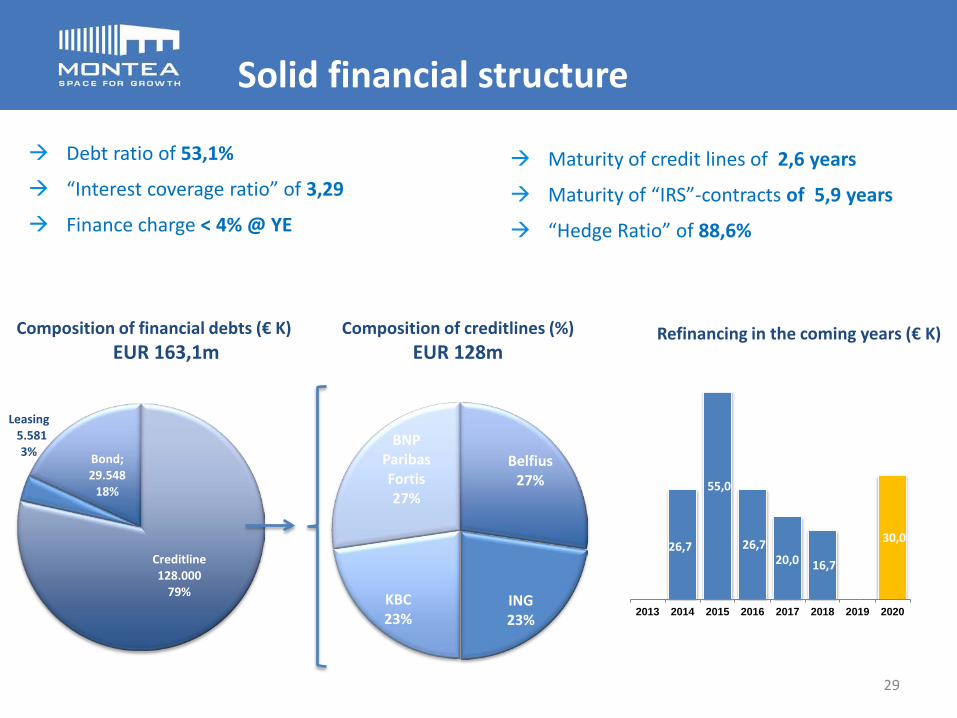

Solid financial structure

Debt ratio of 53,1%

“Interest coverage ratio” of 3,29

Finance charge < 4% @ YE

Creditline128.000

79%

Leasing 5.581

3% Bond; 29.548

18%

Composition of financial debts (€ K) EUR 163,1m

Maturity of credit lines of 2,6 years

Maturity of “IRS”-contracts of 5,9 years

“Hedge Ratio” of 88,6%

26,7

55,0

26,7 20,0 16,7

-

30,0

2013 2014 2015 2016 2017 2018 2019 2020

Refinancing in the coming years (€ K)

Belfius 27%

ING 23%

KBC 23%

BNP Paribas Fortis 27%

Composition of creditlines (%) EUR 128m

29

Topics

1. Montea

2. Portfolio

3. Highlights of 9 months – year 20132013

4. Financial Results 9 months – year 2013

5. Financial structure

6. Conclusion & Outlook 2013

Q3-2013 2012 Q3-2012 2011 2010

Portfolio Value (€m) 305,4 291,5 268,5 254,9 233,0

Occupancy (based upon m²) (%) 93,8 96,3 96,2 96,5 95,1%

Avg. Duration (excl. IAS 39) (y) 5,2 5,6 5,4 5,4 3,5

Yield (%) 8,43 8,25 8,30 8,50% 8,28%

P&L Net Rental Result (€m) 17,4 19,9 14,6 19,3 17,0

Operational Margin (%) 83,7 84,1 86,7 81,5 77,3

Financial Cost (%) 3,72 3,84 4,35 4,59

Net Current Result (€m) 10,07 11,25 8,40 10,24 7,94

Net Current result / share (€) 1,53 2,00 1,49 1,82 1,79

B/S NAV / share (excl. IAS 39) (€) 21,71 22,17 21,58 22,75 23,14

Stock rate (€) 30,08 28,40 27,01 24,52 23,49

Debt Ratio (%) 53,1 51,3 55,3 49,9 47,6

Solid KPI’s

+10%

+14%

+29%

+2%

+15%

+3%

+10%

+10%

+14%

+19%

+20%

+3%

YoY YoY Q3

Evolution of NCR and dividend (€/share)

2,22 2,36

2,08

1,79 1,82

2,00 2,04 1,99 2,09 2,09

1,84 1,84 1,93

2007 2008 2009 2010 2011 2012 2013

Evolution of Net Current Result & Dividend

5,9%

6,8%

8,5%

7,7%

7,5%

6,8%

(1) 1,84 is the add-up of EUR 0,97 per share for the first half of 2010 (before the capital increaese) and EUR 0,87 per share for the 2nd half of 2010 (after the capital increase)

(1)

32

Site Mechelen

“We guarantee a top-quality property portfolio that offers a solid

investment with a diversified risk, profitable growth and a stable

dividend”