Final Year Project for MCom in manufacturing pencil

99

EXECUTIVE SUMMARY This project is based on the Customer Satisfaction survey of the TATA AIG insurance Company ltd. It is done to find out whether the customers are satisfied with the benefits they get with their respective policies or not, Further, in this Project Chapter 1 includes the introduction of the company where the Objectives of the study and profile of the TATA AIG are discussed. Chapter 2 includes the Research Methodology where I have discussed the Research Design and Various sources of the Data Collection. Chapter 3 includes the Data analysis and Findings where I have analyzed the data collected from the Questionnaire.

-

Upload

padmaja-menon -

Category

Documents

-

view

16 -

download

3

description

gives an idea of pg project in tn college ( arts college ) for mcom

Transcript of Final Year Project for MCom in manufacturing pencil

EXECUTIVE SUMMARY

This project is based on the Customer Satisfaction survey of the TATA AIG

insurance Company ltd. It is done to find out whether the customers are satisfied with

the benefits they get with their respective policies or not,

Further, in this Project

Chapter 1 includes the introduction of the company where the Objectives of the study

and profile of the TATA AIG are discussed.

Chapter 2 includes the Research Methodology where I have discussed the Research

Design and Various sources of the Data Collection.

Chapter 3 includes the Data analysis and Findings where I have analyzed the data

collected from the Questionnaire.

Chapter 4 represents the conclusion and the suggestions based on the customer

satisfaction survey.

CHAPTER - I

1. INTRODUCTION

CUSTOMER SATISFACTION

The project aims at analyzing customer satisfaction for TATA AIG

insurance products.

Customer satisfaction refers to how satisfied customers are with the products or

services they receive from a particular agency. The level of satisfaction is determined

not only by the quality and type of customer experience but also by customer’s

expectations.

A customer may be defined as, “Someone who has a direct relationship with, or

is directly affected by your agency and receives or relies on one or more of your

agency’s services or products.”

Customers in human services are commonly referred to as service users,

consumers or clients. They can be individuals or groups. An organization with a strong

customer service culture places the customer at the centre of service design, planning

and service delivery.

Customer centric organizations will:

· determine the customer’s expectations when they plan

· listen to the customer as they design

· focus on the delivery of customer service activities

· value customer feedback when they measure performance.

IMPORTANCE OF CUSTOMER SATISFACTION IN INSURANCE

SECTOR

There are a number of reasons why customer satisfaction is important in

Insurance Sector:

· Meeting the needs of the customer is the underlying rationale for the existence of

community service organizations. Customers have a right to quality services that

deliver outcomes.

· Organizations that strive beyond minimum standards and exceed the expectations of

their customers are likely to be leaders in their sector.

· Customers are recognized as key partners in shaping service development and

assessing quality of service delivery.

The process for measuring customer satisfaction and obtaining feedback on

organizational performances are valuable tools for quality and continuous service

improvement.

Although customer service is very important for winning new and retaining

existing customers, insurance companies struggle to achieve acceptable customer

satisfaction levels in their call centres. In particular, more sophisticated members are

demanding expanded advisory services for their retirement, pension, healthcare and

life insurance needs.

Insurance companies also have trouble meeting the needs of specific

constituents, namely agents, brokers and networks who are the most important

channels for bringing in new business. FileNet, an IBM company, conducted an

insurance industry survey on customer service, and results indicate that more than half

of insurance carriers identified current policy holders as the primary target audience

for their customer service efforts, whilst only 20% identified agents and brokers.

Larger agencies may require dedicated service teams and demand service level

agreements, whilst mid-size agencies may need local service and smaller agencies that

are expensive to service may need centralized call centres and self-service tools.

OVERVIEW OF THE INDUSTRY

The insurance industry provides protection against financial losses resulting

from a variety of perils. By purchasing insurance policies, individuals and businesses

can receive reimbursement for losses due to car accidents, theft of property, and fire and

storm damage; medical expenses; and loss of income due to disability or death.

The insurance industry consists mainly of insurance carriers (or insurers) and

insurance agencies and brokerages. In general, insurance carriers are large companies

that provide insurance and assume the risks covered by the policy. Insurance agencies

and brokerages sell insurance policies for the carriers. While some of these

establishments are directly affiliated with a particular insurer and sell only that carrier’s

policies, many are independent and are thus free to market the policies of a variety of

insurance carriers. In addition to supporting these two primary components, the

insurance industry includes establishments that provide other insurance-related services,

such as claims adjustment or third-party administration of insurance and pension funds.

Insurance carriers assume the risk associated with annuities and insurance

policies and assign premiums to be paid for the policies. In the policy, the carrier states

the length and conditions of the agreement, exactly which losses it will provide

compensation for, and how much will be awarded. The premium charged for the policy

is based primarily on the amount to be awarded in case of loss, as well as the likelihood

that the insurance carrier will actually have to pay. In order to be able to compensate

policyholders for their losses, insurance companies invest the money they receive in

premiums, building up a portfolio of financial asset and income-producing real estate

which can then be used to pay off any future claims that may be brought. There are two

basic types of insurance carriers: direct and reinsurance. Direct carriers are responsible

for the initial underwriting of insurance policies and annuities, while reinsurance

carriers assume all or part of the risk associated with the existing insurance policies

originally underwritten by other insurance carriers.

Direct insurance carriers offer a variety of insurance policies. Life insurance

provides financial protection to beneficiaries—usually spouses and dependent children

—upon the death of the insured. Disability insurance supplies a preset income to an

insured person who is unable to work due to injury or illness, and health insurance pays

the expenses resulting from accidents and illness. An annuity (a contract or a group of

contracts that furnishes a periodic income at regular intervals for a specified period)

provides a steady income during retirement for the remainder of one’s life. Property-

casualty insurance protects against loss or damage to property resulting from hazards

such as fire, theft, pilferage, malicious damage, war, riots and natural disasters.

Liability insurance shields policyholders from financial responsibility for injuries to

others or for damage to other people’s property. Most policies, such as automobile and

homeowner’s insurance, combine both property-casualty and liability coverage.

Some insurance policies cover groups of people, ranging from a few to

thousands of individuals. These policies usually are issued to employers for the benefit

of their employees or to unions, professional associations, or other membership

organizations for the benefit of their members. Among the most common policies of

this nature are group life and health plans. Insurance carriers also underwrite a variety

of specialized types of insurance, such as real-estate title insurance, employee surety

and fidelity bonding and medical malpractice insurance.

In addition to individual carrier-sponsored Internet sites, several “lead

generating” sites have emerged. These sites allow potential customers to input

information about their insurance policy needs. For a fee, the sites forward customer

information to a number of insurance companies, which review the information and, if

they decide to take on the policy, contact the customer with an offer. This practice gives

consumers the freedom to accept the best rate.

The insurance industry also includes a number of independent organizations that

provide a wide array of insurance-related services to carriers and their clients. One such

service is the processing of claims forms for medical practitioners. Other services

include loss prevention and risk management. Also, insurance companies sometimes

hire independent claims adjusters to investigate accidents and claims for property

damage and to assign a dollar estimate to the claim.

THE INSURANCE REGULATORY AND DEVELOPMENT AUTHORITY (IRDA)

Reforms in the Insurance sector were initiated with the passage of the IRDA Bill

in Parliament in December 1999.

The IRDA since its incorporation as a statutory body in April 2000 has

fastidiously stuck to its schedule of framing regulations and registering the private

sector insurance companies. The other decisions taken simultaneously to provide the

supporting systems to the insurance sector and in particular the life insurance

companies were the launch of the IRDA’s online service for issue and renewal of

licenses to agents.

The approval of institutions for imparting training to agents has also ensured that

the insurance companies would have a trained workforce of insurance agents in place to

sell their products.

Since being set up as an independent statutory body the IRDA has put in a

framework of globally compatible regulations.

OBJECTIVES OF THE STUDY

PRIMARY OBJECTIVE

To study the preferences and satisfaction level of customers of TATA AIG

insurance products.

SECONDARY OBJECTIVES

To identify the insurance needs of the Indian population with respect to their

emotional, physical and financial conditions.

To study the awareness of customers regarding TATA AIG insurance.

To bring out the features of insurance preferred by customers.

To measure the customer satisfaction level of customers on various services

provided.

To identify the factors influencing customers during the selection of insurance

policies.

To know the most preferred insurance policy of TATA AIG insurance policies so

that other policies can also be provided in a better way.

COMPANY PROFILE

TATA AIG INSURANCE

Tata AIG General Insurance Company Limited (Tata AIG General) is a joint

venture company, formed by the Tata Group and American International Group, Inc.

(AIG). Tata AIG General combines the Tata Group's pre-eminent leadership position in

India and AIG's global presence as the world's leading international insurance and

financial services organization. The Tata Group holds 74 per cent stake in the insurance

venture with AIG holding the balance 26 percent. Tata AIG General Insurance

Company, which started its operations in India on January 22, 2001, provides insurance

solutions to individuals and corporates. It offers a complete range of general insurance

products including insurance for automobile, home, personal accident, travel, energy,

marine, property and casualty. The Company believes in offering innovative and

relevant insurance solutions in the retail and commercial space. Each product offering is

backed by expertise and an unparalleled claims service. The Company's products are

available through various channels of distribution like agents, brokers, banks (through

bank assurance tie ups) and direct channels like Tele Marketing, worksite etc.

ABOUT TATA GROUP

The Tata Group companies operate in seven business sectors:

Communications and Information Technology, Engineering, Materials, Services,

Energy, Consumer Products and Chemicals. The Group was founded by Jamsetji Tata

in mid 19th century, a period when India had just set out on the road to gaining

independence from British rule. Consequently, Jamsetji Tata and those who followed

him aligned business opportunities with the objective of nation building. This

approach remains enshrined in this Group's ethos to this day.

The Tata Group is one of India's largest and most respected business

conglomerates, Tata companies together employ some 3,50,000 people. The Group's 27

publicly listed enterprises have a combined market capitalization of some $ 60 billion

and a shareholder base of 3.2 million. The major Tata Companies are Tata Steel, Tata

Consultancy Services, Tata Motors, Tata Chemicals, Tata Communications, Tata

Power, Indian Hotels and Tata Tea. The Tata Group has operations in more than 85

countries across six continents and its companies export products and services to eighty

countries.

The Tata family of companies shares a set of five core values: integrity,

understanding, excellence, unity and responsibility. These values, which have been part

of the Group's beliefs and convictions from its earliest days, continue to guide and drive

the business decisions of Tata companies. The Group and its enterprises have been

steadfast and distinctive in their adherence to business ethics and their commitment to

corporate social responsibility. This is a legacy that has earned the Group the trust of

many millions of stakeholders in a measure few business houses anywhere in the world

can match.

ABOUT AMERICAN INTERNATIONAL GROUP INC. (AIG)

American International Group, Inc. (AIG) is a leading international insurance

organization with operations in more than 130 countries and jurisdictions. AIG

companies serve commercial, institutional, and individual customers through one of the

most extensive worldwide property-casualty networks of any insurer. In addition, AIG

companies are leading providers of life insurance and retirement services around the

world. AIG common stock is listed on the New York Stock Exchange, as well as the

stock exchanges in Ireland and Tokyo.

COMPANY BACKGROUND

AIG’s history dates back to 1919, when Cornelius Vander Starr established

an

insurance agency in Shanghai, China. Starr was the first Westerner in Shanghai to sell

insurance to the Chinese. In 1962, Starr gave management of the company's less than

successful U.S. holdings to Maurice R. \"Hank\" Greenberg, who shifted the company's

U.S. focus from personal insurance to higher levels.American International Group, Inc

is the leading U.S. based international insurance and financial services organization and

the largest underwriter of commercial and industrial insurance in the United States. Its

member companies write a wide range of commercial and personal insurance products

through a variety of distribution channels in over 130 countries and jurisdictions

throughout the world. AIG's Life Insurance operations comprise of the most extensive

worldwide network of any life insurer. AIG's global businesses also include financial

services and asset management, including aircraft leasing, financial products, trading

and market making, consumer finance and savings products.

MANAGEMENT PROFILE

The management team consists of many reputed people from the finance industry.

Gaurav D. Garg, Managing Director and CEO

Kaushal Mishra, Executive Vice President

Kurush Jal Daruwalla, Senior Vice President, Company Secretary , General Counsel

Miranjit Mukherjee, Chief Financial Officer

M. Ravichandran, National Head Commercial Lines

Ramesh Ramani, National Head Accident & Health

Bharat Govinda , National Head Personal Lines

Parvathi Singh, National Head Claims

Atri Chakraborty, National Head Operations

Suryanarayanan Subramanian, National Head Human Resources

Mohit Goel, Head Marketing

VISION AND VALUES

OUR VISION:-

To be India's most preferred General Insurance Company.

OUR VALUES:-

To create unmatched value for our customers, employees, business partners

and shareholders by delivering remarkable service that is consistent, fair and

transparent. Our values represent the core, shared beliefs that guide how we act and

work together to achieve our goals. We share a set of 6 core values: Customer First,

People, Passion, Performance, Integrity and Empathy.

CUSTOMER FIRST: Anticipate their priorities. Exceed their expectations.

INTEGRITY: We must conduct our business fairly, with honesty and transparency.

Everything we do must stand the test of public scrutiny.

PEOPLE: We must work cohesively with our colleagues across the Group and with

our customers and partners around the world, building strong relationships based on

tolerance, understanding and mutual cooperation. Strive to develop talent and reward

excellence.

PERFORMANCE: We must constantly strive to achieve the highest possible

standards in our day-to-day work and in the quality of the goods and services .

PASSION: We must be excited about what we do. We must have a strong

internalized drive to meet goals. Relentless determination to solve customer problems.

RESPECT: We must be caring, show respect, compassion and humanity for our

colleagues and customers around the world and always work for the benefit of the

communities we serve.

ORGANISATION STRUCTURE OF TATA AIG

TATA AIG insurance company follows a centralized form of organization. The

board of directors is in overall charge of the company and provides all policy decisions.

The board of directors is assisted by several officers like:

General manager

Assistant secretary

Head management services

Investment Committee or Manager

HR manager

It has offices at headquarters, regions, main and sub-branches whose number

depend upon size and geographic coverage of operations. The board of directors is

further by several heads of functions like ,

Actuary

Agency

Legal

Finance

Advertising

Medical

Accounting

Underwriting

DISTRIBUTION CHANNELS OF TATA AIG

Tata AIG has corporate agency channels, which handles its corporate agents and

have tie-ups with 38 corporate houses. Insurers want to lower distribution costs by

finding more efficient channels. The new private players are developing multiple

channel models; many insurers use or plan to use several banks as distributors. Because

most banks have strong regional bias, in this regards Tata AIG has agreement with

HSBC (corporate agency distribution) through that it is doing both life insurance and

general insurance business.. Because most banks have a strong regional bias, Insurers

can use several banks without creating large overlap. Many larger banks are sourcing

products from several insurers acting as manufacturers.

An important distribution challenge facing insurers is the need to meet the rural

and social sector legislative requirements stipulated in terms of market opening. For

Tata AIG, it takes rural insurance as an opportunity and not an obligation. For

achieving objective in rural area it has also tie with NGOs (Bridge stone for Karnataka

and Kerala).

In this project main focus is distribution channel of Life Insurance of Tata AIG

and little bit of distribution of General Insurance of Tata AIG also. So as the whole

topic of distribution can be known for the both company of Tata AIG (Life and General

insurance). Gradually channels are incorporating day by day for the growth of business.

In the span of two to three years Tata AIG achieve much more business growth

what it expected at the time of entrance in Indian market. It happened because it has

quality people, innovative management, be able to employ technology effectively

besides having right products with effective and modern distribution channel.

PERFORMANCE OF TATA AIG INSURANCE PRODUCTS

TATAAIG was awarded the Company of the Year Award 2011 for Health

Insurance segment during the Indian Insurance Awards. This award was to recognize th

e company that stood out amongst its peers in terms of its

Revenue growth, Profitability, Innovation and Customer service.

The award reinforces their perception as a strong health insurance company as

evidenced also by the HT MaRs Customer Satisfaction Survey (results published in

March, 2011) which ranked us as No.1 in customer service satisfaction and No.2 in clai

msettlement satisfaction.

It is a testament to their wide and strong product range of benefit based

secondary medical insurance products that have not only delivered a profitable

business line but also awards from the industry and a high degree of customer

satisfaction.

TATAAIG was recognized with the Best Product Innovation award

amongst General Insurance players in the Indian Insurance Awards. The

recognition was for Private Client Group Home secure Policy that was launched

in August 2009. It is a unique product catering exclusively to the High Net

Worth client’s need of insuring their high value possessions such s paintings,

valuables, work of art, jewelry, collectibles etc. It offers packaged cover for the

entire home contents including above items with first in the market covers such

as hole in on expenses, loss in value for fine art, pairs and sets, etc. Additional

services are offered along with the insurance cover e.g. vulnerability assessments,

transit supervision, conservation and storage assistance.

Tata AIG General Insurance Co. Ltd. was awarded the E-Commerce Award by

Asia Insurance Technology Awards (AITA) 2011 at a glittering ceremony held at The

Imperial Hotel in Seoul, South Korea on November 9, 2011.

The E-Commerce Award recognizes an insurer who demonstrates a market-

leading e-commerce offering which has deployed a distinct implementation that

demonstrated true innovation in the use of the distribution channel.Some other awards

won by TATA AIG insurance company in 2011 are,

Celent Model Insurer Awards 2011, NewYork

Indian Insurance Awards 2011: Company of the Year Award 2011 for Health

Insurance

Indian Insurance Awards 2011: Best Product Innovation Award 2011 for PCG

MIF-ILO (Microfinance Innovation Facility – International Labour Organization)

grant for implementation of project, “Usage of Mobile devices for enrolment and claim

settlement in cattle insurance.”

PRODUCT/SERVICES PROFILE

INSURANCE SOLUTIONS FOR INDIVIDUALS

1. MOTOR INSURANCE SOLUTIONS

PRIVATE CAR INSURANCEi. Comprehensive Value Added Car Insurance

ii. Extra protection through new and unique Add on covers

TWO WHEELER INSURANCEi. Cover Loss or Damage to your Vehicle

ii. No Claim Bonus on claim free experience

COMMERCIAL VEHICLE INSURANCE

i. Cover Loss or Damage to your Vehicle

ii. No Claim Bonus on claim free experience

2. HOME INSURANCE SOLUTIONS

INSTACHOICE

i. Instant Home insurance with the flexibility to decide your insurance cover basis your needs

ii. Insures appliances as well as jewellery.

HOME SECURE SUPREME i. A flexible home insurance product, which can be customized for individual

requirements.

ii. 15 comprehensive coverage options to choose from.

HOME COUPON

i. On the spot cover for your home. Easy documentation.

ii. Covers Fire and Special perils and Burglary.

INDIA FIRE- FIRE AND SPECIAL PERILS

i. Covers loss due to fire and some special perils.

ii. Affordable, offers additional coverage against earthquakes and terrorism.

3. HEALTH INSURANCE SOLUTIONS

WELLSURANCEi. Wellsurance is the first insurance product designed with unique features and

exclusive benefits that address the needs of today’s lifestyle.

ii. A comprehensive health insurance product, it provides for benefits like Critical

illness benefit, Surgical procedure benefit, Convalescence benefit, Children’s

education benefit and more.

ACCIDENT GUARD

i. Personal and family Accident Insurance Plan

ii. Offers Education allowance, repatriation of remains allowance..etc in case of

family option

INCOME GUARD

i. Personal Accident Insurance Plan designed to cover Accidental Death,

Dismemberment, Permanent Total Disability in one plan.

ii. Simple enrollment procedure with additional benefits like educational

allowance and home/ vehicle alteration benefit in case of an accident

SECURED INCOME PLAN

i. Provides the family with initial lump sum cash

ii. Monthly cash benefits for the next 5 years in case of accidental death.

SECURED FUTURE PLAN

i. Depending upon your monthly expenditure you can choose from Monthly

income benefits options.

ii. Monthly Income benefits ranging from Rs.10000 to Rs.35000, for a period of 5

years to 20 years.

MAHARAKSHA PERSONAL INJURY PLAN

i. Cash benefit for accidental injuries and hospitalization, loss of activity of daily

living.

ii. Provides protection up to 75 years of age.

INDIVIDUAL ACCIDENT AND SICKNESS HOSPITAL CASHi. Hospitalization expenses due to sickness up to Rs. 5000/day

ii. Accident hospital cash benefit available up to Rs.10000/day

iii. Accident Reimbursement benefit of upto Rs. 25000/-

4. TRAVEL INSURANCE SOLUTIONS

CRITICARE- CRITICAL ILLNESS COVER

i. Covers 11 Critical Illnesses

ii. Free Second Opinion

OVERSEAS TRAVEL INSURANCE

i. Global Protection policy valid 24 hours a day, 365 days a year

ii. Coverage of Medical Expenses, baggage delay / loss, loss of passport and more

DOMESTIC TRAVEL INSURANCE

i. A unique Travel Insurance product for travel anywhere within India for missed

departure, accommodation charges due to trip delay, lost ticket reimbursement

and more.

STUDENT TRAVEL INSURANCE

i. Designed for students travelling abroad to pursue their higher studies to cover

Study Interruption, Sponsor Protection, Compassionate Visit (2-way) apart from

Accident & Sickness Reimbursement and Personal Accident.

PROCEDURE FOR LODGING AND SETTLEMENT OF CLAIMS

The following steps are involved in general for lodging and settlement of claims:--

1. After the occurrence of a loss normally intimation to be given to the Policy issuing

office immediately.

2. This will be preceded by lodging a FIR to the nearest Police Station , in case the loss

has occurred due to any cause like Fire, Burglary, Theft, Damage to third party,

Accident etc., i.e. for any reason other than Act of God Peril e.g. Flood, Earthquake,

inundation etc.

3. Collect relevant claim form.

4. Fill up the claim form correctly after reading it thoroughly.

5. Submit claim form to the Policy issuing office either directly or by an authorized

Agent along with documents required /asked for, such as Police Reports, Doctors

Prescriptions, Reports of Pathological tests, Cash Memos from the Chemists Shop

for the medicine purchased, Admission and Discharge Certificates, Receipts from

Surgeon, Doctors etc. as the case may be.

6. The Policy issuing office may appoint Surveyor/ Loss Assessor or may refer the

case to panel Doctors, if necessary.

7. Claim is finally settled by the Policy issuing office and payment is made to the

Policy holder as a full and final settlement of claim.

8. Please note in some cases provisional payment is also made to the Policy holder

pending the final processing of the claim, depending on the merits of the case.

STAGES IN POLICY ISSUANCE

Once the underwriting process on the application for any of the insurance

policies is completed, TATAAIG insurance company will issue the new policy. The

customers are expected to submit all relevant documents to the insurer to support their

policy. At this point, the customer’s rating class and final premium rate are determined.

After issuing the policy, the details will be stored in one of the company’s mails.

It will be processed by the TATA AIG insurance staff and mailed to the

customer within one business day. Processing includes Quality Control of the policy for

errors and in putting policy information into database . The customers when they open

this mail, they are expected to check inside the package for a policy cover letter issued

by TATA AIG. This letter contains important information for putting the policy in

force.Also included will be a Business Reply return envelope for the customer’s

convenience.

Please note that any delivery requirements listed are time sensitive and must be

returned to TATA AIG promptly. If no delivery requirements are listed in the policy

cover letter, the policy will already be in force as of the policy date. Provided

everything is included and accurate, the insurance coverage will be effective as always.

SWOT ANALYSIS

STRENGTHS:

TATA AIG has the strong brand name of TATA and AIG .

It offers a good career path for advisors.

TATA AIG has a good reputation among customers.

It gives first year highest commission.

TATA AIG has a strong training support.

TATA AIG is the only insurance company in the world to be rated AAA by

SWP.

It is the only company that provides whole infrastructure to new advisors.

WEAKNESSES:

TATA AIG is conservative in the context of advertising.

OPPORTUNITIES:

TATA AIG provides protection against financial losses and helps in future planning.

They also provide additional rewards for advisors.

THREATS:

Because of the mushrooming of the private insurance companies , there is

increased competition.

CHAPTER II

RESEARCH METHODOLOGY

RESEARCH INSTRUMENT

The research instrument used in this project is the questionnaire method. A

questionnaire is a form prepared and distributed to secure responses to certain

questions. It is a device for securing answers to questions by using a form for

which information is desired. Purposes of questionnaire are two- fold.

To collect information from the respondents who are scattered in a vast area.

To achieve success in collecting reliable and dependent data.

RESEARCH DESIGN

The research design of this project is exploratory. Though each research study

has its own specific purpose, the research design of this project on TATA AIG is

exploratory in nature as the objective is the development of the hypothesis rather than

their testing.

METHODOLOGY

Every project work is based on certain methodology, which is a way to

systematically solve the problem or attain its objectives. It is a very important guideline

and lead to completion of any project work through observation, data collection and

data analysis.

According to Clifford Woody,” Research Methodology comprises of defining

and redefining problems, collecting, organizing and evaluating data, making deductions

and researching to conclusions.”

Accordingly, the methodology used in the project is as follows: -

Defining the objectives of the study

Framing of questionnaire keeping objectives in mind (considering the objectives)

Feedback from the employees

Analysis of feedback

Conclusion, findings and suggestions.

SAMPLING TECHNIQUE USED

This research has used convenience sampling technique.

CONVENIENCE SAMPLING TECHNIQUE

Convenience sampling is used in exploratory research where the researcher is

interested in getting an inexpensive approximation of the truth. As the name implies,

the sample is selected because they are convenient.

SELECTION OF SAMPLE SIZE

For the survey, a sample size of 50 has been taken into consideration.

SOURCES OF DATA COLLECTION

1) PRIMARY DATA:

QUESTIONNAIRE

Primary data was collected by preparing questionnaire for customers. The

questionnaire was filled through direct research.

2) SECONDARY DATA:

Secondary data will consist of different literatures like books, articles, internet,

the company manuals and websites of company.

STATISTICAL TOOLS

Questionnaire

Pie Charts

Bar Diagrams

Doughnut chart

Bubble chart

Line diagram

LIMITATIONS OF STUDY

Some of the problems faced while conducting the survey are as follows:-

Time and cost constraints were there.

Chances of some biasness and lack of cooperation could not be eliminated.

A Samples size of fifty has been use due to time limitations.

CHAPTER III

DATA ANALYSIS AND INTERPRETATION

FREQUENCY ANALYSIS

AGE OF RESPONDENTS

AGE MALE FEMALE PERCENTAGE

BELOW 20 2 2 8

20-30 12 19 62

30-40 9 4 26

ABOVE 40 - 2 4

TOTAL 23 27 100

INFERENCE:

We can see that more respondents of age group 20-30 prefer TATA AIG insurance a lot

as it is very much beneficial to them. TATA AIG insurance provides a lot of attractive

policies for youngsters. It is then followed by the other age groups.

AGE OF THE RESPONDENTS

EDUCATIONAL LEVEL OF THE RESPONDENTS

EDUCATION MALE FEMALE TOTAL

10th OR BELOW 3 2 10

10, +2 OR BELOW - 2 4

GRADUATE 12 22 68

POST GRADUATE 3 6 18

TOTAL 18 32 100

INFERENCE:

The above table shows the educational level of respondents. Many graduates

and post graduates utilize insurance for their security. This is because TATA AIG

insurance policies help in their education and savings also. It is then followed by school

students.

EDUCATIONAL LEVEL OF THE RESPONDENTS

OCCUPATION OF THE RESPONDENTS

OCCUPATION MALE FEMALE TOTALSALARIED 15 14 58

SELF EMPLOYED - 3 6

RETIRED 1 1 4

HOUSEWIFE - 4 8

STUDENT 5 6 22

NRI - 1 2

TOTAL 21 29 100

INFERENCE:

Salaried persons use TATA AIG insurance more as they offer a lot of scope for

savings and investments. It is then followed by students as it helps in their

education. Homemakers seem to prefer TATA AIG insurance more than self

employed, retired persons and NRI respondents.

OCCUPATION OF THE RESPONDENTS

MONTHLY INCOME (IF APPLICABLE)

MONTHLY INCOME

MALE FEMALE TOTAL

5,000-10,000 7 2 18

10,000-20,000 6 16 44

ABOVE 20,000 - - -

TOTAL 13 18 62

INFERENCE:

The above table shows the monthly income levels of the respondents who are

working. Most of the respondents are in the middle income group.Hence we can infer

that most of TATA AIG insurance customers are in the middle income group.

MONTHLY INCOME (IF APPLICABLE)

AWARENESS OF TATA AIG INSURANCE

AWARENESS OF TATA AIG

INSURANCE

MALE FEMALE TOTAL

NEWSPAPERS 14 17 62

RADIO - - -

TELEVISION 3 3 12

DIRECT SALES EXECUTIVE

3 10 26

TOTAL 20 30 100

INFERENCE:

TATA AIG insurance advertises a lot by means of newspapers and this is noticed

by most respondents as they are educated. Other than newspapers, TATA AIG

insurance is noticed more through the efforts of their direct sales executives.

TATA AIG insurance is also known through television. None of the respondents

seem to listen to radio.

AWARENESS OF TATA AIG INSURANCE

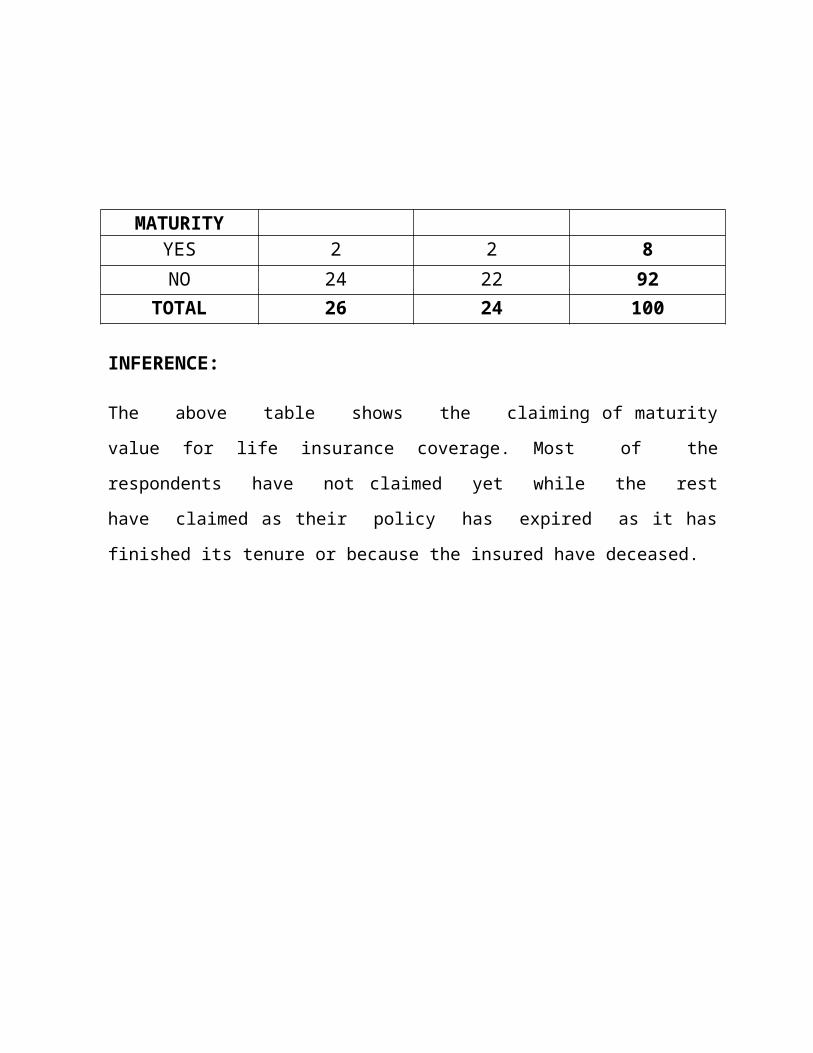

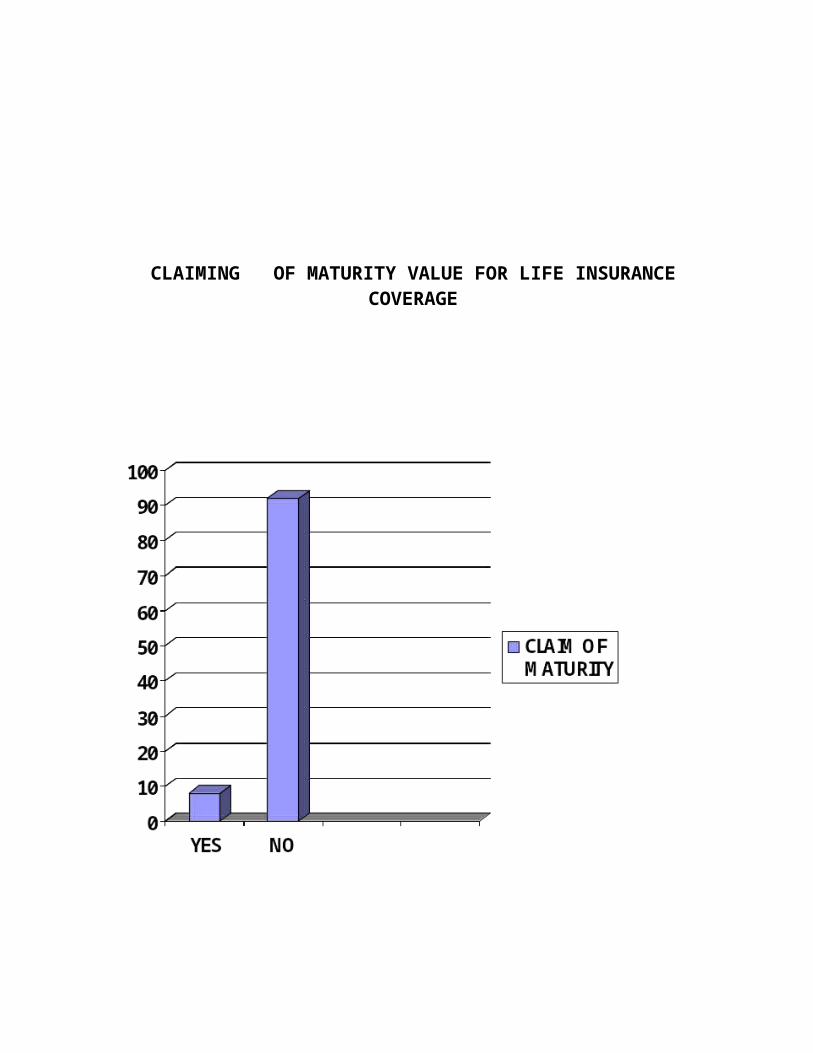

CLAIMING OF MATURITY VALUE FOR LIFE INSURANCE COVERAGE

CLAIMING OF MATURITY

MALE FEMALE TOTAL

YES 2 2 8

NO 24 22 92

TOTAL 26 24 100

INFERENCE:

The above table shows the claiming of maturity value for life insurance coverage.

Most of the respondents have not claimed yet while the rest have claimed as their

policy has expired as it has finished its tenure or because the insured have deceased.

CLAIMING OF MATURITY VALUE FOR LIFE INSURANCE COVERAGE

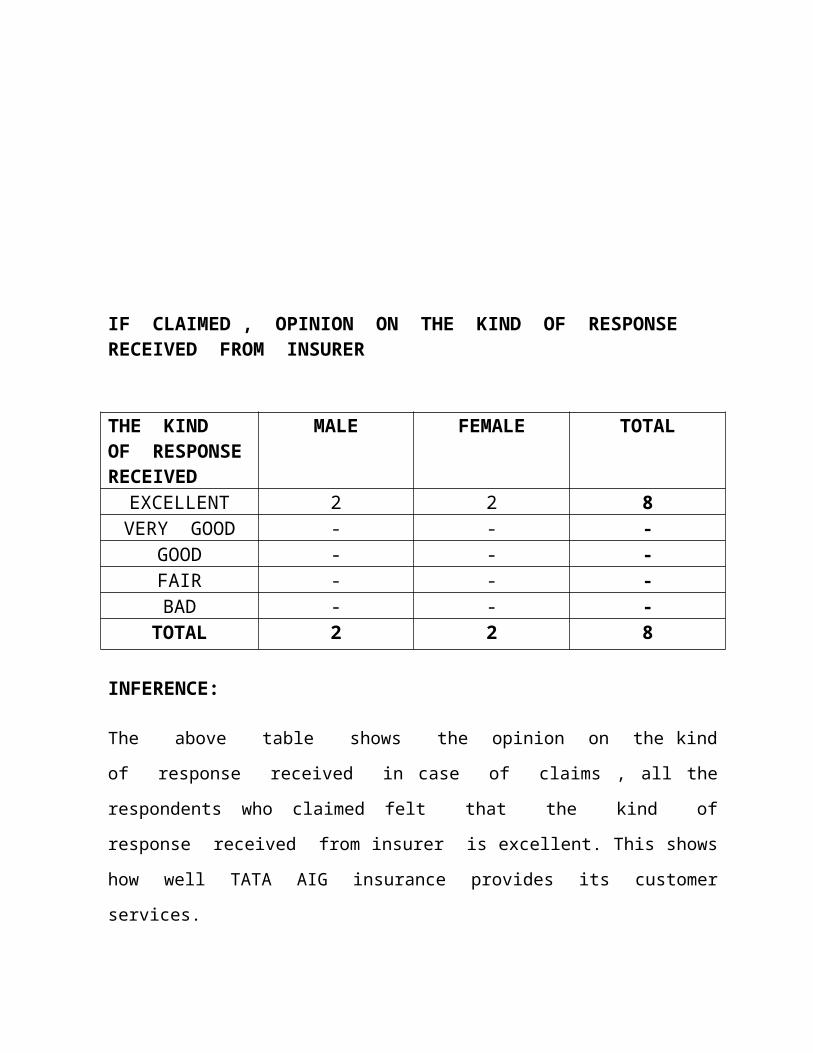

IF CLAIMED , OPINION ON THE KIND OF RESPONSE RECEIVED FROM INSURER

THE KIND OF RESPONSE RECEIVED

MALE FEMALE TOTAL

EXCELLENT 2 2 8VERY GOOD - - -

GOOD - - -FAIR - - -BAD - - -

TOTAL 2 2 8

INFERENCE:

The above table shows the opinion on the kind of response received in case of

claims , all the respondents who claimed felt that the kind of response received

from insurer is excellent. This shows how well TATA AIG insurance provides its

customer services.

IF CLAIMED , OPINION ON THE KIND OF RESPONSE RECEIVED FROM INSURER

HAS ANY POLICY BEEN DECLINED, POSTPONED , ACCEPTED AT EXTRA PREMIUM , ACCEPTED ON SPECIAL TERMS , ACCEPTED WITH REDUCED COVER OR WITHDRAWN BY YOURSELF

HAS ANY POLICY BEEN DECLINED,ETC

MALE FEMALE TOTAL

YES - - -

NO 26 24 100

TOTAL 26 24 100

INFERENCE:

All the respondents have said that no policy has been postponed, declined ,

accepted at extra premium , accepted on special terms, accepted with reduced cover

or withdrawn by yourself. This shows how much TATA AIG insurance `s services

have been effective.

HAS ANY POLICY BEEN DECLINED, POSTPONED , ACCEPTED AT EXTRA PREMIUM , ACCEPTED ON SPECIAL TERMS , ACCEPTED WITH REDUCED COVER OR WITHDRAWN BY YOURSELF

RESPONDENTS REASON FOR PREFERENCE OF TATA AIG INSURANCE

REASON FOR PREFERENCE

MALE FEMALE TOTAL

BRAND IMAGE 10 5 30

EXCELLENT PAST RECORD

20 1 42

MARKETING PEOPLE INSISTED

- - -

COMPANY ADS 8 2 20

FRIEND SUGGESTED

4 - 8

ANY OTHER REASON

- - -

TOTAL 42 8 100

INFERENCE:

Majority of the respondents have selected TATA AIG insurance due to its excellent

past record as it has always maintained it so over so many years, followed by its brand

image, mainly due to the brand `TATA’. The remaining respondents have selected

TATA AIG insurance due to the company ads and friend suggestions.

RESPONDENTS REASON FOR PREFERENCE OF TATA AIG INSURANCE

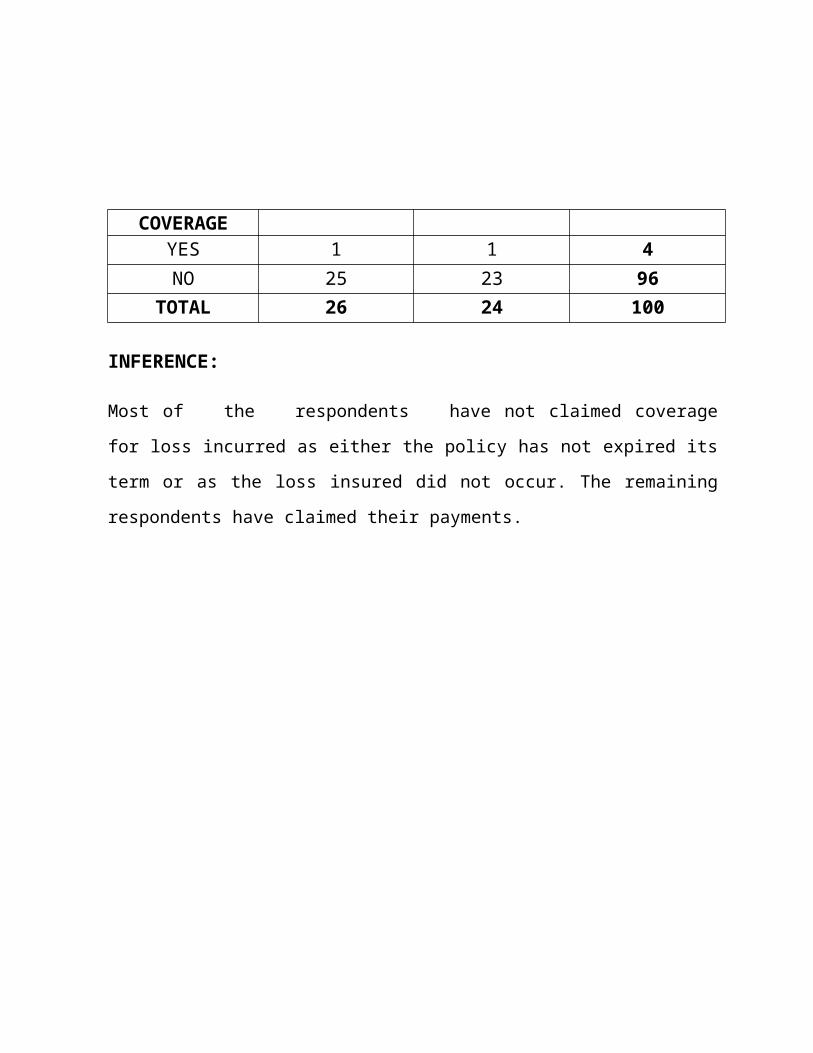

CLAIMING OF INSURANCE COVERAGE FOR LOSS INCURRED ( GENERAL INSURANCE )

CLAIMING OF INSURANCE COVERAGE

MALE FEMALE TOTAL

YES 1 1 4

NO 25 23 96

TOTAL 26 24 100

INFERENCE:

Most of the respondents have not claimed coverage for loss incurred as either the

policy has not expired its term or as the loss insured did not occur. The remaining

respondents have claimed their payments.

CLAIMING OF INSURANCE COVERAGE FOR LOSS INCURRED ( GENERAL INSURANCE )

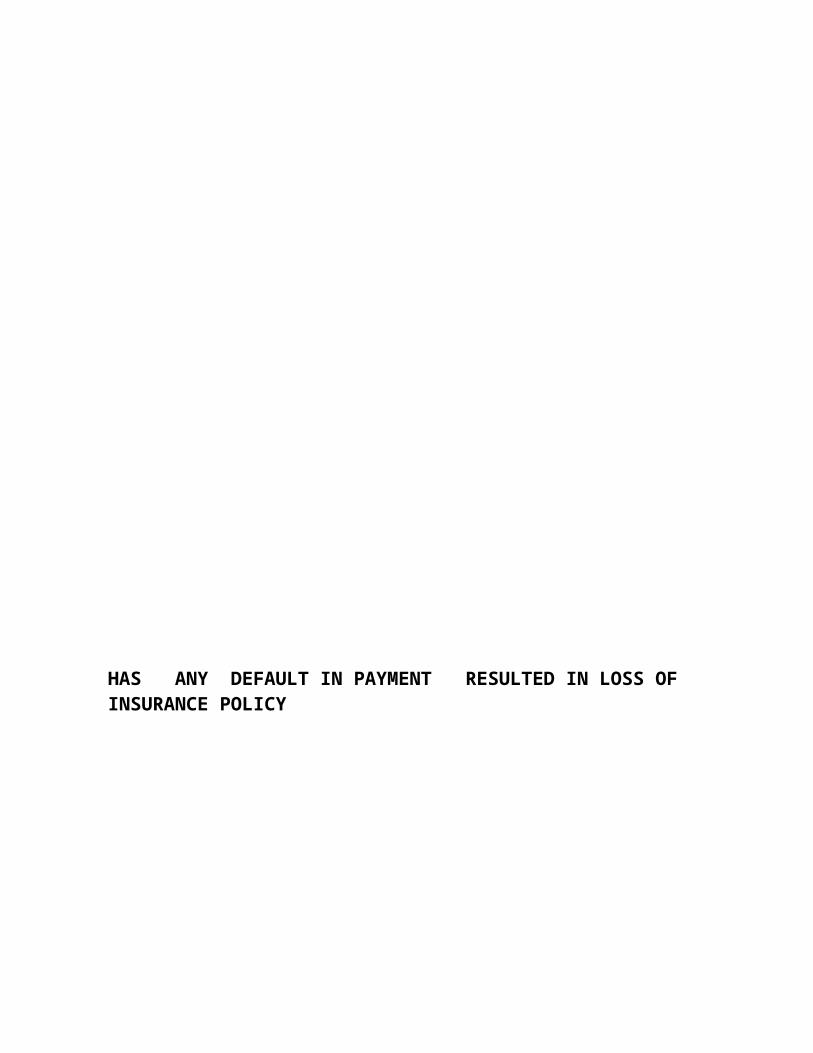

HAS ANY DEFAULT IN PAYMENT RESULTED IN LOSS OF INSURANCE POLICY

ANY DEFAULT RESULTED IN

LOSS OF INSURANCE

POLICY

MALE FEMALE TOTAL

YES - - -

NO 26 24 100

TOTAL 26 24 100

INFERENCE:

All the respondents have said that no default in payment has resulted in

loss of insurance policy. This shows that a certain level of default is allowed to

be paid later by the assured.

HAS ANY DEFAULT IN PAYMENT RESULTED IN LOSS OF INSURANCE POLICY

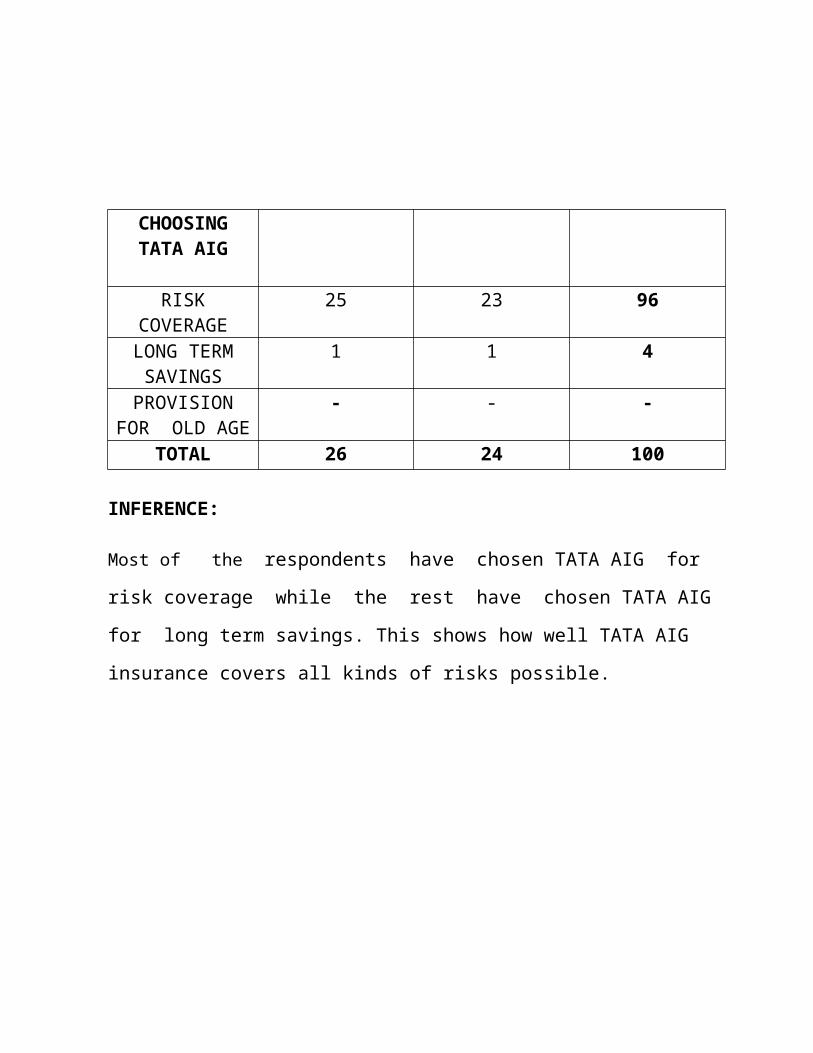

REASON FOR CHOOSING TATA AIG INSURANCE

REASON FOR CHOOSING TATA AIG

MALE FEMALE TOTAL

RISK COVERAGE

25 23 96

LONG TERM SAVINGS

1 1 4

PROVISION FOR OLD AGE

- - -

TOTAL 26 24 100

INFERENCE:

Most of the respondents have chosen TATA AIG for risk coverage while the

rest have chosen TATA AIG for long term savings. This shows how well

TATA AIG insurance covers all kinds of risks possible.

REASON FOR CHOOSING TATA AIG INSURANCE

IMPORTANCE OF MAKING RIGHT CHOICE OF A BRAND

IMPORTANCE OF MAKING

RIGHT CHOICE

MALE FEMALE TOTAL

VERY MUCH 25 25 100

SOMEWHAT - - -

NOT AT ALL - - -

TOTAL 25 25 100

INFERENCE:

All the respondents feel that making right choice of brand is very much

important. This shows that all the respondents would prefer only good brands like

TATA AIG.

IMPORTANCE OF MAKING RIGHT CHOICE OF A BRAND

DO YOU STICK TO SAME BRAND AND REMAIN LOYAL TO TATA AIG INSURANCE AND ITS PRODUCTS

DO YOU STICK TO

SAME BRAND

MALE FEMALE TOTAL

YES 23 25 96

NO 1 1 4

TOTAL 24 26 100

INFERENCE:

Almost all the respondents stick to same brand as they feel that quality of

services provided should be as good as TATA AIG insurance. It is only few

respondents who don’t seem to mind using any brand.

DO YOU STICK TO SAME BRAND AND REMAIN LOYAL TO TATA AIG INSURANCE AND ITS PRODUCTS

IS THERE ANY INSURANCE POLICY FOR WHICH YOU DO NOT PREFER TATA AIG INSURANCE

INSURANCE MALE FEMALE TOTAL

FOR WHICH YOU DO NOT PREFER TATA

AIGHOME INSURANCE

20 10 60

CAR INSURANCE

- - -

FIRE INSURANCE

- - -

HEALTH INSURANCE

- - -

LIFE INSURANCE

- - -

TOTAL 20 10 60

INFERENCE:

Of all the 50 respondents , some of the respondents have stated that they do

not prefer home insurance alone of all the TATA AIG insurance products.

Other products seem to be more suitable to them due to certain reasons.

IS THERE ANY INSURANCE POLICY FOR WHICH YOU DO NOT PREFER TATA AIG INSURANCE

REASON FOR NOT PREFERRING TATA AIG INSURANCE

REASON FOR NOT PREFERRING TATA

AIG

MALE FEMALE TOTAL

HIGH PREMIUM 20 10 60

INVESTMENTS/SAVINGS - - -

LACK OF SECURITY - - -

TOTAL 20 10 60

INFERENCE:

The same number of respondents have said that high premium is the

reason they do not prefer home insurance. Hence TATA AIG insurance

should try to reduce its premium atleast reasonably.

REASON FOR NOT PREFERRING TATA AIG INSURANCE

IS THE COVERAGE FOR EVEN PARTIAL LOSS IN CASE OF THEFTS, ACCIDENTS AND ALLIED PERILS USEFUL

IS THE COVERAGE FOR EVEN PARTIAL

LOSS USEFUL

MALE FEMALE TOTAL

YES 25 25 100

NO - - -

TOTAL 25 25 100

INFERENCE:

All the respondents feel that coverage for even partial loss in case of thefts,

accidents and allied perils is very much useful. Hence this special feature

provided by TATA AIG insurance is quite beneficial to its customers.

IS THE COVERAGE FOR EVEN PARTIAL LOSS IN CASE OF THEFTS, ACCIDENTS AND ALLIED PERILS USEFUL

IS THERE ANY SPECIFIC COMPLAINTS FOR YOU AGAINST TATA AIG INSURANCE

COMPLAINTS AGAINST

TATA AIG INSURANCE

MALE FEMALE TOTAL

YES - - -

NO 25 25 100

TOTAL 25 25 100

INFERENCE:

None of the respondents have any specific complaints against TATA AIG

insurance. This indicates the company’s excellent products and pleasing customer

service.

IS THERE ANY SPECIFIC COMPLAINTS FOR YOU AGAINST TATA AIG INSURANCE

RANKING OF TATA AIG INSURANCE COMPANY

RANKING OF TATA AIG

INSURANCE

MALE FEMALE TOTAL

EXCELLENT 17 20 74

VERY GOOD 8 5 26

GOOD - - -

FAIR - - -

BAD - - -

TOTAL 25 25 100

INFERENCE:

Most of the respondents feel that TATA AIG insurance is excellent , while

the rest feel it is very good. We can see that none of the respondents rank

TATA AIG insurance in a wrong manner.

RANKING OF TATA AIG INSURANCE COMPANY

FINDINGS

According to my survey the noteworthy points are:

Most of the people buy life insurance as just a tax benefit tool or as a life cover

while only a few of the respondent take it as a saving option. The reason for this is lack

of knowledge of insurance benefits among the people.

A Majority of the respondent buy insurance products because of the need reason

while rest of the respondents buy for the brand purpose.

A Majority of the people come to know about the policies from the Direct Selling

Agents.

A Majority of the people are satisfied by the incentives associated with their

policies.

Most of the respondents are satisfied by the services offered by their insurance

company while some says that they are not satisfied by the services.

Most of the respondents want more transparency from the side of the company.

CHAPTER IV

CONCLUSIONS AND SUGGESTIONS

CONCLUSIONS

After overhauling the all situation that boosted a number of Pvt. Companies

associated with multinational in the Insurance Sector to give befitting competition to

the established behemoth TATA AIG in private sector, we come at the conclusion that

TATA AIG has vast market and very firm grip on its traditional customers and

monopoly of life insurance products.

IRDA is also playing very comprehensive role by regulating norms mandating to

private players in this sector, that increases the confidence level of the customers to the

private players.

SUGGESTIONS

The study has provided with the useful data from the respondents. There has a

lot to be recommended. Following are the recommendations:

There is a need for better promotion for the insurance products and services. The

company should advertise its products more through television.

More returns should be provided on Insurance plans.

It should provide this facility by tie up with the other Insurance organizations as

well. They should have choice while selecting a suitable Insurance plans. This will

definitely add to the goodwill and profit for TATA AIG insurance company.

ANNEXURE

QUESTIONNAIRE ON CUSTOMER SATISFACTION

FOR TATA AIG INSURANCE PRODUCTS

Dear Sir/Madam

I am Aishwarya Menon, a student of Meenakshi College for Women, Department of Commerce, Chennai and presently doing a project on “Customer Satisfaction For TATA AIG Insurance Products”. I request you to kindly fill the questionnaire below and assure you that the data generated shall be kept confidential.

1. Educational Qualification

10th or below 10+2 or below Graduate

Post Graduate and above Others (please specify)

Name :

Gender M F

No of dependants :

Address :

2. Age Group

20-30 30-40 above 40

3. Your Occupation

Salaried Self Employed Retired Housewife

Student NRI (Please specify the country you belong)

4. If Salaried, employed with

Private Limited Partnership Proprietorship Public Limited

Public Sector Government Multinational

Mention the type of industry employed,

5. Monthly income (if applicable)

5,000-10,000 10,000-20,000 above 20,000

6. Which of the insurance policies have you taken from TATA AIG Insurance?

Home insurance Car insurance Fire insurance Health insurance

Life insurance Any others please specify, _____________

REASONS FOR SELECTION

7. How did you come to know TATA AIG insurance?

Newspapers Radio Television Direct Sales Executive

Friend Internet Bank Others (please specify)

8. What prompted you to buy insurance from TATA AIG? (Please rate them on scale of Importance from 1 to 5)

REASONS 1 2 3 4 5A) Brand image

B) Excellent past record

C) Marketing people insisted

D) Company ads

E) Friend suggested

F) Any other reason

CLAIMS

9. Have you ever claimed value for any insurance coverage for loss incurred (general insurance)?

Yes No

10. Have you ever claimed maturity value for life insurance coverage?

Yes No

11. If yes, please provide your opinion on the kind of response received from the insurer?

Excellent Very good Good Fair Bad

12. Has any policy ever been declined, postponed, accepted at extra premium, accepted on special terms, accepted with reduced cover or withdrawn by yourself?

Yes No

DEFAULT

13. Has any default in payment of premium resulted in loss of insurance policy?

Yes No

14.If yes, was the policy later accepted on special terms and conditions ?

Yes No

YOUR RATINGS

15. In selecting from many types and brands of the insurance products available in the market, you chose TATA AIG as, Risk coverage Long term savings Provision for old age

16. How important would it be to you to make a right choice of the brand?

Very much Somewhat Not at all

YOUR PREFERENCES

17. Do you tend to stick to the same brand and remain loyal to TATA AIG insurance company and its product?

Yes No

18. For which insurance policy you do not prefer TATA AIG?

Home insurance Car insurance Fire insurance Health insurance

Life insurance Any others please specify , _____________

19. Your reasons?

High premium investments/ savings Lack of security

SPECIAL FEATURE

20. Is the coverage for even partial loss in case of thefts, accidents and allied perils useful?

Yes No

COMPLAINTS

21. Is there any specific complaints for you against TATA AIG insurance?

Yes No

CONCLUSION

22. How much do you rank TATA AIG insurance company?

Excellent Very good Good Fair Bad

BIBLIOGRAPHY

www.tata-aig.com

en.wikipedia.org/wiki/Main Page

Brochures provided by the TATA AIG insurance company.

Kothari C .R. ‘Research and Methodology- Methods and Techniques’, New Age International (P) Ltd., 2004