Final UK MiFID Response

109

UNCLASSIFIED UNCLASSIFIED 1 of 109 UK response to the Commission Services‟ consultation on the Review of the Markets in Financial Instruments Directive (MiFID) 1. INTRODUCTION MIFID has been decisive in strengthening the Single Market in wholesale financial services and the Commission and EU should be proud of its success. The abolition of the concentration rule has allowed for alternatives to conventional stock exchanges to emerge, fostering greater competition among trading venues. This is generally recognised as having driven down trading charges and stimulated innovation. These changes have also brought challenges. One consequence of competition has been the fragmentation of equities trading, which in turn has given rise to difficulties in data consolidation. Such issues need to be addressed if MiFID‟s clear single market and competitive benefits are not to be compromised. New technological developments and market practices have also emerged, partly to deal with the challenges of this fragmentation but also in response to the legislative framework itself. Given these developments, the UK agrees it is appropriate to assess whether and how the MiFID regime needs to be adapted to ensure resilient and sound financial markets. We also need to consider how elements of the MIFID review fit in to the international regulatory reform agenda, led by the G20, in response to the financial crisis. In this context, one aspect of MiFID will be critical in enabling the EU to deliver the G20 commitment to increase electronic platform trading of standardised derivatives where appropriate. 1 As we develop our own definition of suitable platforms in Europe, building on international agreements, we should remind ourselves of the objectives of the G20 – mitigation of systemic risk, enhanced transparency and added protection against market abuse. The UK considers that the MiFID review provides an opportunity to: contribute to the EU's delivery of the G20 commitment to enhance transparency, mitigate systemic risk and protect against market abuse; strengthen the quality and consolidation of post-trade information, as a key step in mitigating the risks from market fragmentation. The private sector should play the lead role in delivering this outcome, within clearly set parameters; further strengthen and develop the EU regulatory framework, taking account of the global dimension. The current MiFID arrangements for the treatment of third country providers have worked well. We do not support the imposition of a new regime for granting access from third countries to EU markets only on the basis of a strict equivalence assessment; ensure that MIFID continues to provide a robust basis for competition between different types of trading venue. We support delineating as a new type of trading venue those 1 Statement No. 13, Leaders’ Statement: The Pittsburgh Summit (September 24 – 25, 2009), http://www.g20.org/ Documents/pittsburgh_summit_leaders_statement_250909.pdf

Transcript of Final UK MiFID Response

UNCLASSIFIED

UNCLASSIFIED

1 of 109

UK response to the Commission Services‟ consultation on the Review of the Markets in Financial Instruments Directive (MiFID)

1. INTRODUCTION

MIFID has been decisive in strengthening the Single Market in wholesale financial services and the Commission and EU should be proud of its success. The abolition of the concentration rule has allowed for alternatives to conventional stock exchanges to emerge, fostering greater competition among trading venues. This is generally recognised as having driven down trading charges and stimulated innovation. These changes have also brought challenges. One consequence of competition has been the fragmentation of equities trading, which in turn has given rise to difficulties in data consolidation. Such issues need to be addressed if MiFID‟s clear single market and competitive benefits are not to be compromised. New technological developments and market practices have also emerged, partly to deal with the challenges of this fragmentation but also in response to the legislative framework itself. Given these developments, the UK agrees it is appropriate to assess whether and how the MiFID regime needs to be adapted to ensure resilient and sound financial markets. We also need to consider how elements of the MIFID review fit in to the international regulatory reform agenda, led by the G20, in response to the financial crisis. In this context, one aspect of MiFID will be critical in enabling the EU to deliver the G20 commitment to increase electronic platform trading of standardised derivatives where appropriate.1 As we develop our own definition of suitable platforms in Europe, building on international agreements, we should remind ourselves of the objectives of the G20 – mitigation of systemic risk, enhanced transparency and added protection against market abuse. The UK considers that the MiFID review provides an opportunity to:

contribute to the EU's delivery of the G20 commitment to enhance transparency, mitigate systemic risk and protect against market abuse;

strengthen the quality and consolidation of post-trade information, as a key step in mitigating the risks from market fragmentation. The private sector should play the lead role in delivering this outcome, within clearly set parameters;

further strengthen and develop the EU regulatory framework, taking account of the global dimension. The current MiFID arrangements for the treatment of third country providers have worked well. We do not support the imposition of a new regime for granting access from third countries to EU markets only on the basis of a strict equivalence assessment;

ensure that MIFID continues to provide a robust basis for competition between different types of trading venue. We support delineating as a new type of trading venue those

1 Statement No. 13, Leaders’ Statement: The Pittsburgh Summit (September 24 – 25, 2009),

http://www.g20.org/ Documents/pittsburgh_summit_leaders_statement_250909.pdf

UNCLASSIFIED

UNCLASSIFIED

2 of 109

types of OTC trading mechanism which have significant functional overlap with Multilateral Trading Facilities (MTFs). This includes those that would be suitable for on-venue trading of OTC derivatives. But it does not make sense to try to characterise broad swathes of OTC trading as taking place on an "organised trading facility" as some of the systems that would appear from the consultation document to fall into this category are not venue-like;

enhance market transparency in non-equity markets, through the introduction of post-trade transparency requirements. Such requirements will need to be carefully calibrated and based on detailed evidence and impact assessment so as not to damage liquidity in these markets, recognising that risk capital plays a significant role in supporting liquidity;

ensure that regulators have the information needed to be able to police markets effectively and ensure their integrity. A strong system of transaction reporting should be at the heart of such information, but the costs and benefits of collecting such reports need to be carefully assessed in each case. In some markets - such as commodity derivatives - position reporting is likely to be a more effective tool;

ensure that our markets are resilient and robust in the face of new technological developments. We need to take account of the benefits which these changes - such as automated trading - have brought, while ensuring that regulators have the appropriate tools to be able to address any risks;

ensure that commodity derivative markets provide robust and consistent price discovery mechanisms for the underlying commodities, and are sufficiently liquid to enable participants to hedge and manage their risks. However, there is no evidence that financial market regulatory tools can be used to systematically control commodity prices, and it would therefore be a mistake to develop policy proposals on this basis;

reform conduct rules to ensure that clients are better informed about the products and services they are offered and tackle the potential for remuneration set by product providers to bias investment advice.

SMEs In reviewing MiFID, we have a valuable opportunity to consider a targeted set of reforms that seek to improve SME access to European capital markets. This is about more than listing models (important as those are). We need to take a holistic approach to improving access to finance for SMEs and join up thinking across institutional boundaries and initiatives. Increasing the range of funding options that are available to SMEs is an important objective of the Commission and Council2. The Commission has made a good start with its proposals for a “SME market” regime that could be appropriately tailored to meet the needs of smaller companies. But there will be other funding options (such as early stage investment by business angels) that MiFID could facilitate more easily and we would therefore encourage the Commission to be ambitious and consider a package of reforms targeted towards SME financing. Investor protection Investor protection is a key theme of MiFID. We strongly support the Commission‟s work to increase the overall level of protection for investors. We have long been working to improve consumer outcomes, through initiatives such as the retail distribution review, and we are

2 Communication from the Commission, COM (2010) 608. Towards a Single Market Act

UNCLASSIFIED

UNCLASSIFIED

3 of 109

committed to pursuing this principle at the EU level. We hope that the UK‟s experience in this area will be of use. We must also be conscious of the economic and social need to provide consumers with the best opportunities for return on their investments, particularly during a time of economic recovery, and we must ensure there is an appropriate balance between protection, consumer responsibility and cost. We welcome the Commission‟s attention to selling practices, and in our response to the proposals for investment advice we provide detail from our own experience on how the proposals can be made more robust. For example on the definition of “independence” and in ensuring that all firms are clear in disclosing the basis upon which investment advice is provided, including where that advice is not “independent”. We also suggest that the Commission should stop product providers from setting remuneration for all firms providing investment advice, not just those whose advice is "independent". It will also be important to take existing frameworks into account and ensure that current levels of investor protection are retained, as explained in our response to section 8.1 on Article 4. However, we highlight our significant concerns for the proposals for the so-called “execution-only” and client classification regimes. We also remain concerned about the proposal to deliver selling practices for PRIPs through two distinct legislative instruments and processes, the MiFID and Insurance Mediation Directive reviews, rather than through an ambitious cross-sectoral approach. We hope that the Commission will take a more consolidated and ambitious approach to avoid unjustified divergence, and ensure a good outcome for consumers and a competitive market for firms as well as strengthening the single market. Review proposals There is much to welcome in the Commission‟s consultation paper. To ensure the review builds on the successes of MiFID, however, the UK considers it essential that any proposed reforms to markets regulation must be assessed against the following tests. Firstly, the proposals must promote the growth of the European economy. Secondly, we must look for ways that reform can strengthen the single market and encourage the global competitiveness of European markets. Thirdly, we must also ensure that the proposals continue to underpin sound and efficient markets. Finally, there must be a clear evidence base for intervention, with any legislative proposals supported by a full quantitative assessment of the costs and benefits. We would note that the Commission rejects or departs from CESR‟s detailed technical advice in a number of areas without explanation, including in the areas of pre and post-trade transparency, target setting for platform trading, transaction reporting, and client categorisation. CESR‟s advice was developed after extensive consultation with stakeholders and detailed consideration of the issues. We therefore consider that some justification of the Commission‟s approach in these instances is necessary so that its reasons for not following the CESR advice can be understood. The Commission has also proposed some changes where we consider the objective is unclear. Our detailed commentary on the issues raised in the consultation document is set out in the following sections. We highlight some of the main themes below. 3rd country provisions MiFID has had a positive impact on EU GDP - according to one study,3 it may have raised the long-run level of EU GDP by as much as 0.8%. It is therefore important to preserve the benefits

3 “Understanding the Impact of MiFID in the context of Global and National Regulatory Innovations”, a Report

prepared by London Economics for the City of London Corporation, October 2010

UNCLASSIFIED

UNCLASSIFIED

4 of 109

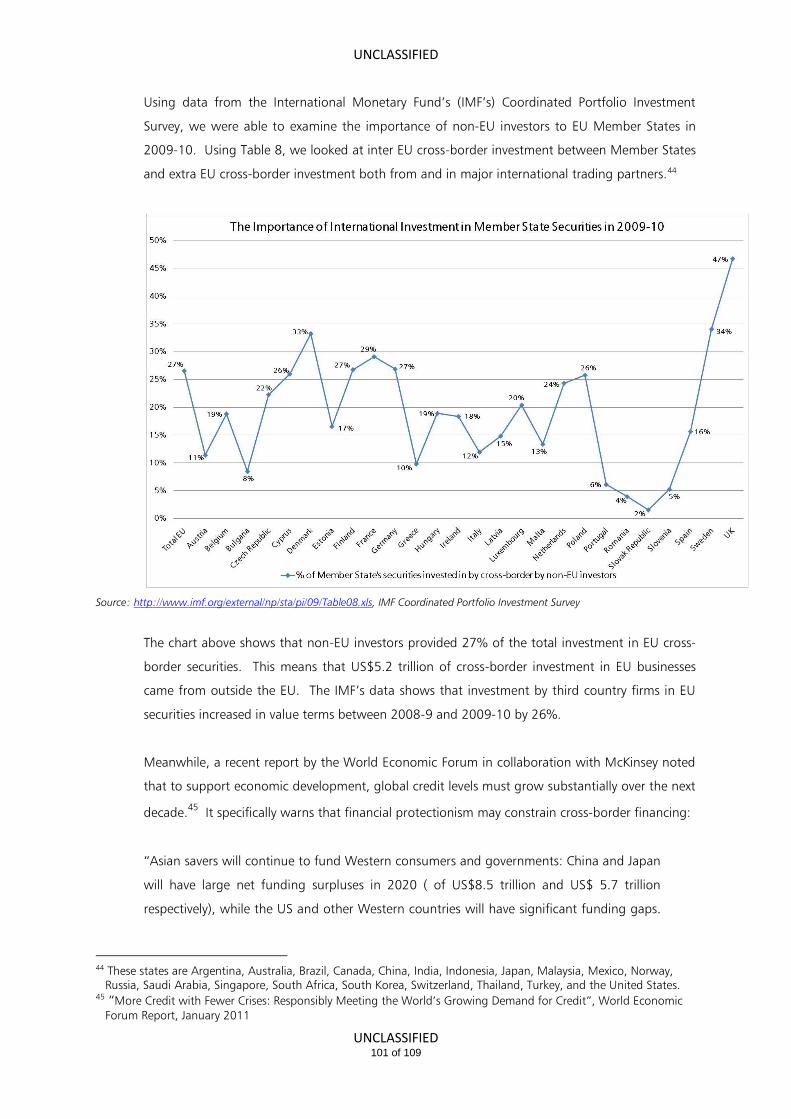

and advocate change only where this promotes further growth, taking care not to restrict the financing options available to European corporates or weaken competition. In this context, it is important to recognise that financial markets are global and that Europe is the world leader in global finance. If the European economy is to continue to grow, our companies and governments need more capital from beyond European borders – fortress Europe is not the answer. Global markets are highly sophisticated. Major changes are best contemplated on a step by step basis and in full understanding of different asset classes. Against that background we have strong reservations about the proposal to introduce a third country regime in MiFID based on the principle of exemptive relief for equivalent jurisdictions, which we consider has the potential to undermine both the principle of free movement of capital and the ability of EU firms to do international business To illustrate the significance of this issue, research by the IMF indicates that between 2008-09 and 2009-10 investment by third country firms in EU securities increased in value terms by 26%. A recent report by the World Economic Forum in collaboration with McKinsey noted that to support economic development, global credit levels must grow substantially over the next decade.4 It specifically warns that financial protectionism may constrain cross-border financing and that there is likely to be strong competition to attract finite global credit between the world‟s economies. Already we are seeing fierce competition not just from traditional financial centres in the US but increasingly from Asia. However, the growth of emerging market economies offer huge opportunities for Europe‟s financial services industry. Access of third country firms to invest in EU businesses should be seen as a key enabler for the EU‟s 2020 strategy for smart, sustainable and inclusive growth. Automated trading and related issues The Commission makes a number of proposals in relation to automated trading, with specific reference to the type of automated or algorithmic trading known as High Frequency Trading (HFT). The UK agrees with the Commission that „HFT is typically not a strategy in itself but the use of very sophisticated technology to implement traditional trading strategies‟ and that HFT is a „subcategory of automated trading‟. We also agree that existing evidence is inconclusive about its impact on markets. We need to understand better the impact of trends in computer automated trading. The UK Treasury is therefore sponsoring a new research project, led by the UK Government Office for Science, to explore how computer-generated trading may evolve in the future. We hope that the findings of this research will usefully inform debate on this area. In the meantime, we support the Commission‟s proposals for robust risk controls to be put in place by firms involved in automated trading or who provide sponsored access to automated traders. However in the absence of further research, we must be careful not to introduce measures based on the assumption that high frequency trading is, per se, harmful to markets. We do not think a case has been made to mandate the provision of liquidity by high frequency traders. Forcing high frequency traders to become market makers may deter them from entering the market altogether thereby removing the benefits of the liquidity they currently provide voluntarily. It may also create prudential risks to these firms, leaving them exposed to market movements when other participants are at liberty to withdraw. Similarly, the UK does not believe that the case has been made to require orders to rest on the book for a minimum period of time, or to limit the ratio of orders to transactions executed by

4 “More Credit with Fewer Crises: Responsibly Meeting the World‟s Growing Demand for Credit”, World Economic Forum Report, January 2011

UNCLASSIFIED

UNCLASSIFIED

5 of 109

any given participant. Any participant may wish to delete an order quickly for prudential reasons. Forcing participants to remain in the market could damage overall market efficiency and compromise firms‟ risk management. New category of Organised Trading Facility (OTF) The UK agrees that it is important to assess whether MiFID‟s existing regulatory categories remain appropriate given the new forms of trading functionality that have emerged. The UK recognises that Broker Crossing Systems (BCSs), for example, are growing in significance, and that in some instances they appear similar to other trading models. Following the principle of functional regulation it therefore may be reasonable to introduce requirements for BCSs that are consistent with, although differentiated from, those for MTFs. We also see justification in the provision of a new category of trading facility for trading services in standardised and sufficiently liquid OTC derivatives, which fall outside the boundaries of existing regulated market/MTF definitions. The minimum characteristics of such an Organised Trading Venue (or “OTV”) should be broadly defined so as to capture a spectrum of single/multi dealer trading models, as it would then be practicable to trade a greater range of standardised OTC instruments on such platforms, furthering G20 objectives and ensuring competition. However, following the principle that any intervention must be clear in its objective and supported by a robust evidence base, we do not see justification for an additional, broader-ranging OTF category aimed at other, unspecified, activities. Clarity on the purpose of this proposal will be necessary to ensure that intervention is justified and that the objectives of the regime are well defined. Regulators need to be able to define clearly what they are regulating and why; and market participants need to be clear about the rules that apply to them. Powers to ban services and activities With regard to intervention powers, as the Commission recognises, its proposal for a European level power to ban the provision of investment services and the carrying out of investment activities in certain financial instruments has potentially significant consequences for market participants and businesses. Banning products of any kind should be undertaken with great caution as otherwise innovation, effective risk management and economic growth could be detrimentally impacted. A greater justification is needed for the introduction of these powers without safeguards. We note that powers already exist under MiFID that effectively empower national regulators to ban a product, and for European cooperation on such action. Similarly, the new European Supervisory Authorities (ESAs) have been given the power to ban products temporarily (together with appropriate attached powers to obtain information critical to such decisions). We would therefore query how some of the proposals under this section relating to EU banning mechanisms would relate to these existing powers; and the consequent necessity for such powers. Commodities The UK welcomes the consultation‟s focus on measures to support delivery of the G20 commitment to improve the regulation, functioning, and transparency of financial and commodity markets to address excessive commodity price volatility. In determining which individual proposals to adopt to deliver this, it is important these are proportionate and evidence based. Of the proposals in the MiFID review the UK welcomes those to provide more position data in a standardised form to enable regulators to have stronger oversight and understanding of what is

UNCLASSIFIED

UNCLASSIFIED

6 of 109

happening across markets, enabling them to act if they have concerns of risks building up. The UK has particular concerns about the adoption of position limits, where there is a need for further evidence of their utility and where other proposals such as position management may meet the objectives of countering market manipulation without risking unintended consequences including harming market liquidity. Transparency The UK fully supports increased transparency where this will either help with regulatory oversight and / or improve the price formation process. An effective, well-calibrated regime is critical for ensuring fair, efficient and stable financial markets. There are clearly some areas of financial market regulation where we need to see change. However, poorly calibrated transparency regimes can have damaging and unintended consequences. Failure to understand these issues properly and at a granular level can lead to withdrawal of liquidity from markets and stifle the development of products which serve the needs of end-users. Before introducing new transparency regimes, we therefore need to be clear what the market failure is that we are trying to address. And it is essential that any transparency regime targeted at derivatives and corporate bonds takes account of the diverse range of asset classes, whose trading characteristics can differ significantly, and which will therefore require tailored requirements incorporating an appropriate system of waivers. Next steps The consultation paper implies changes that will have profound implications for many firms, ranging from retail financial advisers to the largest wholesale investment firms, across the EU and internationally. It is therefore vital that the Commission‟s ambition for reform is grounded in full appreciation of its possible impact. We are therefore surprised that the Commission considered such a short consultation period of eight weeks (over a holiday period) would be sufficient to canvass views from such a broad spectrum and collect enough evidence for a meaningful impact assessment. In the UK‟s view, the consultation period is inappropriately curtailed and not conducive to sound policy making or the production of carefully considered legislative proposals. We have addressed all the issues raised in the consultation as thoroughly as possible given the time constraints, but the extent of the proposals is such that we may wish to make further comments if, on further consideration, this becomes necessary. Looking ahead, it will be essential that the Commission continues to work closely with all interested parties to address the concerns of businesses across Member States, and ensure that any proposals are evidence-based and supported by a robust impact assessment. We hope this response will help in that process and look forward to close and constructive working with the Commission. 4/2/2011

UNCLASSIFIED

UNCLASSIFIED

7 of 109

2. DEVELOPMENTS IN MARKET STRUCTURES .................................................................... 8

2.1. DEFINING ADMISSION TO TRADING ......................................................................................................... 8 2.2. ORGANISED TRADING FACILITIES ........................................................................................................... 9 2.3. AUTOMATED TRADING AND RELATED ISSUES ....................................................................................... 20 2.4. SYSTEMATIC INTERNALISERS ............................................................................................................... 25 2.5. FURTHER ALIGNMENT AND REINFORCEMENT OF ORGANISATIONAL AND MARKET SURVEILLANCE

REQUIREMENTS FOR MTFS AND REGULATED MARKETS AS WELL AS ORGANISED TRADING FACILITIES 26 2.6. SME MARKETS ..................................................................................................................................... 27

3. PRE- AND POST-TRADE TRANSPARENCY ...................................................................... 31

3.1. EQUITY MARKETS ................................................................................................................................. 31 3.2. EQUITY-LIKE INSTRUMENTS ................................................................................................................. 34 3.3. TRADE TRANSPARENCY REGIME FOR SHARES TRADED ONLY ON MTFS OR ORGANISED TRADING

FACILITIES ............................................................................................................................................ 35 3.4. NON EQUITY MARKETS ......................................................................................................................... 36 3.5. OVER THE COUNTER TRADING .............................................................................................................. 40

4. DATA CONSOLIDATION ............................................................................. 41

4.1. IMPROVING THE QUALITY OF RAW DATA AND ENSURING IT IS PROVIDED IN A CONSISTENT FORMAT .... 42 4.2. REDUCING THE COST OF POST TRADE DATA FOR INVESTORS ................................................................. 44 4.3. A EUROPEAN CONSOLIDATED TAPE ..................................................................................................... 45

5. COMMODITIES ............................................................................. 49

5.1. SPECIFIC REQUIREMENTS FOR COMMODITY DERIVATIVES EXCHANGES ................................................ 50 5.2. MIFID EXEMPTIONS FOR COMMODITY FIRMS ....................................................................................... 53 5.3. DEFINITION OF OTHER DERIVATIVE FINANCIAL INSTRUMENT ............................................................... 55 5.4. EMISSION ALLOWANCES ....................................................................................................................... 57

6. TRANSACTION REPORTING ............................................................................. 58

6.1. SCOPE ................................................................................................................................................... 58 6.2. CONTENT OF REPORTING ...................................................................................................................... 62 6.3. REPORTING CHANNELS ......................................................................................................................... 64

7. INVESTOR PROTECTION AND PROVISION OF INVESTMENT SERVICES .................... 65

7.1. SCOPE OF THE DIRECTIVE ..................................................................................................................... 67 7.2. CONDUCT OF BUSINESS OBLIGATIONS .................................................................................................. 68 7.3. AUTHORISATION AND ORGANISATIONAL REQUIREMENTS ................................................................... 81

8. FURTHER CONVERGENCE OF THE REGULATORY FRAMEWORK AND OF THE

SUPERVISORY PRACTICES ............................................................................. 90

8.1. OPTIONS AND DISCRETIONS ................................................................................................................. 91 8.2. SUPERVISORY POWERS AND SANCTIONS ............................................................................................... 95 8.3. ACCESS OF THIRD COUNTRY FIRMS TO EU MARKETS .......................................................................... 100

9. REINFORCEMENT OF SUPERVISORY POWERS IN KEY AREAS ................................ 103

9.1. BAN ON SPECIFIC ACTIVITIES, PRODUCTS OR PRACTICES .................................................................... 103 9.2 STRONGER OVERSIGHT OF POSITIONS IN DERIVATIVES, INCLUDING COMMODITY DERIVATIVES ......... 105

UNCLASSIFIED

UNCLASSIFIED

8 of 109

2. DEVELOPMENTS IN MARKET STRUCTURES

As the consultation paper notes, there have been significant market developments (including the

types of trading facilities, the technological applications and the methods of execution that are

available) since the introduction of MiFID. The review presents an important opportunity to

assess whether legislative amendments are needed to take account of these developments.

The UK supports the Commission‟s stated objective at page 8 of the consultation paper that any

amendments to MiFID should aim to support market liquidity and efficiency, and improve

investor confidence. In preparing our response, the UK has considered the Commission‟s

proposals against these criteria.

The UK has also considered how the proposals might best deliver the reforms agreed by the G20

to enhance transparency, mitigate systemic risk and protect against market abuse in the

particular context of the trading of standardised OTC derivatives5. In this context, the UK is

mindful of the work already underway in other countries as well as international fora6 and would

encourage the Commission to ensure consistency as far as practicable in order to avoid

regulatory arbitrage and any competitive disadvantage to EU markets.

2.1. Defining admission to trading

(Q1)

(1) What is your opinion on the suggested definition of admission to trading? Please explain the

reasons for your views.

The UK is unclear as to the purposes the proposed definition is intended to serve. The UK

assumes that the proposal is not intended to modify, or affect the scope of, the requirements of

European directives (particularly the Market Abuse Directive and the Transparency Directive)

based upon an admission to trading, although if the Commission takes a different view this

5 Statement No. 13, Leaders‟ Statement: The Pittsburgh Summit (September 24 – 25, 2009), http://www.g20.org/ Documents/pittsburgh_summit_leaders_statement_250909.pdf

6 The FSB report of October 2010 mandated the IOSCO Task Force on OTC derivatives to prepare by 31 January 2011, a report analysing (i) the characteristics of the various exchanges and electronic platforms that could be used for derivatives trading; (ii) the characteristics of a market that make exchange or electronic platform trading practicable; (iii) the benefits and costs of increasing exchange or electronic platform trading, including identification of benefits that are incremental to those provided by increasing standardisation, moving to central clearing and reporting to trade repositories; and (iv) the regulatory actions that may be advisable to shift trading to exchanges or electronic trading platforms.

UNCLASSIFIED

UNCLASSIFIED

9 of 109

should be clarified and the precise implications spelled out. In general terms, the UK is unaware

of any circumstances where the absence of a definition has caused difficulties. If a legislative

definition is considered to be appropriate, its purposes and effect need to be clearly articulated

and such definition should specify that admission to trading occurs once the decision of a

platform operator becomes effective and the security is available to be traded (conditionally or

unconditionally) on the facilities of the platform.

During the recent review of the Prospectus Directive, the UK is aware that an issue arose in

relation to admission to trading. This was because the Prospectus Directive captures shares on

primary multilateral trading facilities (MTFs), such as AIM and PLUS in the UK, when public offers

of shares are undertaken. This was an issue during the negotiations of the amending Directive as

the proposals only benefited companies admitted to trading on a regulated market. This would

have meant that smaller companies who are often quoted on primary MTFs would have been

unable to benefit from a proportionate disclosure regime. However, the UK considers that the

Commission will be able to address this issue successfully through its proposal for a SME Market

and consequently this avoids the need for a definition of admission to trading.

2.2. Organised trading facilities

(Q2-5)

(2) What is your opinion on the introduction of, and suggested requirements for, a broad category

of organised trading facility to apply to all organised trading functionalities outside the current

range of trading venues by MiFID? Please explain the reasons for your views.

The UK understands from the Commission proposals that:

(a) the Organised Trading Facility (OTF) category will capture all organised trading that

occurs outside the current range of MiFID venues;

(b) the Commission‟s aim is to level the playing field between those venues (RMs, MTFs and

SIs) that are already subject to specific MiFID obligations as trading venues and those

regulated intermediaries that provide a type of organised trading service that is currently

categorised as OTC;

(c) broker crossing networks and organised trading venues (for certain standardised

derivative contracts) would be particular sub-regimes within the overall OTF category;

(d) the Commission does not intend the OTF category to capture any OTC trading that is

engaged in on an ad hoc and purely bilateral basis;

(e) The OTF would not replace the basic intermediary regulation to which firms are subject

but, where necessary, supplement it. We also note that the Commission proposes to

UNCLASSIFIED

UNCLASSIFIED

10 of 109

exclude systems or facilities used simply to execute an order on an external trading venue

or to route an order to an external trading venue.

The UK agrees that it is important to assess whether MiFID‟s existing regulatory categories remain

appropriate given the new forms of trading functionality that have emerged. We can see the case

for creating a new category of venue for broker crossing networks. We can also see the case for a

new category of trading facility which provides a mechanism to authorise and oversee facilities

offering trading services in standardised and sufficiently liquid OTC derivatives, which fall outside

the boundaries of existing regulated market/MTF definitions, as a basis for measures to help

deliver G20 commitments. (For convenience we refer to this proposed category as “OTV”, or

Organised Trading Venue, throughout this response).

However, we do not see that the Commission has provided any clear justification for going

further than this, and creating an overarching, very broad new category of “organised trading

facility”. The UK has significant concerns regarding the implications of such an approach, such

as the potential to require illiquid or bespoke OTC derivatives unsuited to organised trading to be

traded on an OTF, when this would not generate any benefits.

Instead, the minimum characteristics of an “OTV” should in our view be more broadly defined so

as to capture a spectrum of single/multi dealer trading models, as it would then be practicable to

trade a greater range of standardised OTC instruments on such platforms, furthering G20

objectives. We do not therefore support the proposal for an additional, broader-ranging “OTF”

category on top of that.

Any intervention must be clear in its objective and supported by a robust evidence base. The

consultation paper is not specific about exactly what activity the OTF category is intended to

capture, and why. Moreover, the requirements which the Commission indicates might attach to

the “OTF” category are already requirements which are reflected in the investment firm

regulatory regime. Applying an additional one-size-fits-all regulatory requirements on a category

of ill-defined facilities (which may serve different objectives and different needs of the market)

does not appear a sensible approach. Regulators need to be able to define clearly what they are

regulating and why; and market participants need to be clear about the rules that apply to them.

In this context, the UK notes the Commission‟s statement that MiFID is not intended to be

prescriptive about where trades much be executed and that the legislation is intended to provide

flexibility and choice for investors about where and how they wish to execute trades (page 9 of

consultation paper). The UK considers it essential that such flexibility is retained, both to facilitate

competition and investor choice.

UNCLASSIFIED

UNCLASSIFIED

11 of 109

(3) What is your opinion on the proposed definition of an organised trading facility? What should be

included and excluded?

As indicated in our response to Question 2, the UK supports the creation of some additional

categories, but has significant reservations about the creation of a generalised “OTF” category.

(4) What is your opinion about creating a separate investment service for operating an organised

trading facility? Do you consider that such an operator could passport the facility?

As a matter of principle, any separate investment service created under MIFID should be capable

of being passported.

(5) What is your opinion about converting all alternative organised trading facilities to MTFs after

reaching a specific threshold? How should this threshold be calculated, e.g. assessing the volume

of trading per facility/venue compared with the global volume of trading per asset class/financial

instrument? Should the activity outside regulated markets and MTFs be capped globally? Please

explain the reasons for your views.

As noted above, the UK has significant reservations about the creation of an “OTF” category. In

relation to broker crossing systems and organised trading venues, the UK does not consider it

would be necessary or appropriate that these types of system should be required to convert to

MTFs after reaching a specific threshold. This is on the basis that the obligations of any new

category should provide the regulatory oversight and transparency the UK believes the proposed

conversion to MTF status is intended to deliver (meaning in other words that the regulatory

benefit of any conversion to an MTF would fall away). Presumably the intention of the

Commission is that any new regulatory category (whether OTF or otherwise) would introduce a

clear set of robust regulatory requirements, that would be proportionate and capable of being

calibrated to the level of activity undertaken by the facility or system. The UK believes that it

would be inappropriate to require an operator of an organised trading facility to convert to an

MTF as this could necessitate an unjustifiable change to its business model simply as a

consequence of reaching a specific threshold.

(6) What is your opinion on the introduction of, and suggested requirements for, a new sub-regime

for crossing networks? Please explain the reasons for your views.

The UK recognises that Broker Crossing Systems (BCSs) are growing in significance, and that in

some instances they can look similar to MTFs. Following the principle of functional regulation it

UNCLASSIFIED

UNCLASSIFIED

12 of 109

therefore may be reasonable to introduce requirements for BCSs that are consistent with,

although differentiated from, those for MTFs.

The UK agrees with the definition of a BCS given in the CESR technical advice, namely „an internal

electronic matching system operated by an investment firm that executes client orders against

other client orders or, occasionally, house account orders on a discretionary basis‟. Furthermore,

the UK agrees that the additional requirements for the sub-regime as set out in points a) and b)

under section 2.2.2 of the consultation document are necessary to ensure that regulators are

able to undertake proper surveillance of the market and address concerns about the lack of

transparency in the market.

(7) What is your opinion on the suggested clarification that if a crossing system is executing its own

proprietary share orders against client orders in the system then it would prima facie be treated

as being a systematic internaliser and that if more than one firm is able to enter orders into a

system it would prima facie be treated as a MTF?

Under present legislation, it is not the case that a BCS executing its own proprietary share orders

against client orders is prima facie a systematic internaliser. MiFID (Article 4(1)(7) of Directive

2004/39/EC) states that for an investment firm to be classified as a systematic internaliser, it must

deal on its own account by executing client orders on an „organised, frequent and systematic

basis‟. Therefore an investment firm using its BCS for proprietary trading on an ad hoc basis

would not fall under this definition – and the suggestion in question 7 would represent a

substantive change, not simply a clarification.

Even if a firm were placing orders into a BCS, it is unclear why this should automatically result in

the firm being classified as systematic internalisation, because, for example, simply placing orders

into a BCS may not satisfy the SI frequency condition. What seems important to the UK in the

circumstances described above is that there is clarity that the SI obligations apply irrespective of

how the firm conducts its trading, if the SI conditions are met. Importantly, if venue identifiers

are to be applied across a wider range of venue-like systems (e.g. a specific MIC for a given

broker crossing system), a key issue will be to ensure there is an agreed protocol for the identifier

to be used for trade reporting in respect of, say, a situation where an SI trade is undertaken in a

broker crossing system.

Furthermore, the UK believes that the operator of a BCS must be able to apply discretion in order

to provide tailored outcomes for clients and ultimately achieve best execution. This is a valuable

service to brokers‟ clients and is distinct from other kinds of venue-like operations. By contrast, a

systematic internaliser must carry out its activities „in accordance with non-discretionary rules and

UNCLASSIFIED

UNCLASSIFIED

13 of 109

procedures‟ (Article 21 of MiFID Level 2 Regulation). This implies that these two business lines are

clearly distinct, involving the firm in question undertaking fundamentally different roles. As such,

the UK believes that there is no particular reason why a single firm cannot simultaneously be

both a systematic internaliser and the operator of a BCS.

In the same way, the UK does not consider that if more than one firm is able to enter orders into

a BCS it is prima facie an MTF. MiFID (Article 4(1)(15) of Directive 2004/39/EC) dictates that, to

be classified as an MTF, a firm must both operate a multilateral system and do so „in accordance

with non-discretionary rules‟. The UK recognises that the yielding of some element of discretion

to clients potentially takes broker crossing systems into a grey area that would benefit from more

clarity, but it also considers that any clarifications in this area need to result in consistency with

the functionalities of other regulatory categories.

The UK notes that this response assumes no change to the definition of a systematic internaliser

or an MTF. We recognise that the BCS category should not be used by firms to circumvent the

transparency requirements associated with being a systematic internaliser or MTF operator.

(8) What is your opinion of the introduction of a requirement that all clearing eligible and

sufficiently liquid derivatives should trade exclusively on regulated markets, MTFs, or organised

trading facilities satisfying the conditions above? Please explain the reasons for your views.

The UK is fully supportive of the G20 commitment to strengthen the functioning of derivatives

markets, including through greater levels of trading of standardised OTC derivatives on organised

trading platforms, where appropriate. The UK considers that such trading can complement and

reinforce post-trade measures by ensuring that platforms offering markets in standardised

derivatives are subject to authorisation and oversight in accordance with a set of clear regulatory

standards.

The UK considers that detailed measures around platform trading of OTC derivatives should be

applied where they would provide the specific benefits envisaged by the G20 (namely, the

mitigation of systemic risk, enhanced transparency and added protection against market abuse)

and in a manner not otherwise achieved by greater standardisation, central clearing and use of

trade repositories. In this context, the UK notes that a number of initiatives are already underway,

both at the EU7 and international level and while it is important to ensure consistency with this

work it is also essential to avoid duplication.

7 Such as the Proposal for a Regulation of the European Parliament and of the Council on OTC derivatives, central

counterparties and trade repositories (“EMIR”) 2010/0250 (COD), 15 September 2010.

UNCLASSIFIED

UNCLASSIFIED

14 of 109

In relation to the introduction of a requirement that all clearing eligible and sufficiently liquid

derivatives should trade exclusively on organised platforms, the UK considers this may be

unnecessarily restrictive. 100% mandation would prevent eligible derivatives from being

transacted to on an OTC basis even where there was a legitimate reason for doing so (for

example, where a transaction is composed of a number of inter-dependent legs). The UK notes

that in its technical advice8 to the Commission, CESR advocated the formulation of sufficiently

ambitious industry targets, to be developed in consultation with market participants. This

approach would increase the level of organised platform trading while recognising and

preserving the possibility of OTC execution for a specified proportion of business.

The UK notes that, with respect to other regulatory initiatives, regulatory action based on setting,

monitoring and revising performance targets has proved effective. For example, the OTC

Derivatives Supervisors Group (ODSG) has been working with market participants (referred to as

the G-14 dealers) for a number of years to increase central clearing of certain OTC derivative

products. The G-14 dealers committed in July 2008 to using a central counterparty for certain

credit derivatives transactions, and in September 2009, established targets for submitting and

clearing trades for certain interest rate and credit derivatives. In March 2010, the G-14 dealers

set dates to increase many of these targets. Regulatory action based on performance targets for

trading, with appropriate monitoring and enforcement capabilities, would build on this wider

approach and mitigate the risk of unintended market disruption arising from 100% mandation.

The UK notes that the G20 commitment refers to platform trading of derivatives “where

appropriate” and any proposal for 100% mandation would need to be supported by a robust

cost-benefit analysis. In the absence of any further data or evidence from the Commission to

support a move away from CESR‟s recommendation, the UK considers that an appropriate

target-setting process, combined with arrangements for such targets to be monitored, could

deliverthe G20 commitment while at the same time minimising any impact on the efficient

functioning of the derivatives markets.

In the context of a possible trading obligation, the UK would welcome clarification from the

Commission as to whether there will be an exemption for non-financial entities participating in

OTC derivatives markets for commercial purposes. The UK notes that other trading regimes in

the course of development, such as the US financial authorities‟ implementation of Dodd-Frank,

envisage an end-user exemption for non-financial entities that access derivatives markets to

mitigate a commercial risk. In addition, a similar exemption for entities which are not financial

institutions is expected to be made available within the Commission‟s proposed EMIR, in relation

to clearing obligations. The UK considers that, if a trading requirement is introduced,

8 CESR/10-1096

UNCLASSIFIED

UNCLASSIFIED

15 of 109

exemptions should be made available for commercial entities, other than those which meet pre-

determined criteria to be deemed to be of systemic importance.

The UK agrees with the Commission that liquidity is an essential criterion for determining

whether an OTC derivative is suitable for trading on an organised venue. In this regard, the

appropriate liquidity threshold will be linked with the minimum characteristics that a venue

would need to possess in order to qualify as an organised trading venue (the greater the

flexibility in permissible trading functionalities, the wider the range of standardised OTC

derivatives for which on-venue trading will be practicable). The UK notes that, in addition to an

assessment of liquidity, the Commission proposes an OTC derivative should first be subject to the

clearing obligation in order to be deemed eligible for platform trading. The UK does not

consider that acceptance for central clearing is, of itself, a necessary or sufficient condition for

platform trading. As an alternative to the clearing criterion, the UK considers that the

assessment of trading eligibility should (in addition to liquidity) focus upon the level of

standardisation (from the legal, process and product point of view) of an OTC derivative, given

that acceptance for central clearing does not assure a sufficient degree of standardisation to

support platform trading. This approach would be consistent with the conclusions of the 2010

FSB report on OTC Derivatives which noted that the relevant individual criteria for defining

whether an OTC derivatives was 'standardised' (i.e. standardisation and liquidity) could be met to

different degrees for central clearing vs. exchange trading.

(9) Are the above conditions for an organised trading facility appropriate? Please explain the reasons

for your views.

As a starting point, the UK would observe that previous public consultations on these issues9

have demonstrated there is a broad spectrum of trading functionalities already available for the

execution of derivatives transactions, which have been developed to meet a wide range of needs.

In this context, the UK believes that regulatory intervention to limit the range of market models

that can be made available to trade OTC derivatives should be approached with care. Continued

access to a wide range of functionalities (both voice and electronic) will help ensure future

market resilience during periods of stress, and as noted previously the wider the range of venues

the greater the number of derivatives that can be traded on them (thereby facilitating delivery of

the G20 commitment).

The UK suggests that the key elements of a regulatory regime that will ensure an effective and

proportionate delivery of the G20 commitment are as follows:

9 For example, CESR‟s consultation exercise with regard to the standardisation and exchange-trading of OTC

derivatives.

UNCLASSIFIED

UNCLASSIFIED

16 of 109

(a) regulatory action should be based on the use of targets developed in consultation with

industry, which ensure an increased level of trading of eligible derivatives on organised

trading platforms, appropriately defined, but do not exclude the possibility of transacting

by other means where justified;

(b) regulatory action should be targeted at a sub-set of standardised derivatives meeting

transparent and objective liquidity criteria which are consistent with international

principles;

(c) there should be a clear definition of an organised trading platform, which references a

minimum set of functional characteristics. Such characteristics should be those that, after

consideration of any costs and benefits, further the achievement of the G20 objectives

above and beyond greater standardisation, the use of trade repositories and central

clearing. On this basis, a definition should include those characteristics described at

paragraph 2.2.1 (currently proposed for organised trading facilities generally), combined

with appropriate transparency, but exclude the additional characteristic of multilateral

access proposed for the relevant sub-regime, if this would serve to exclude single dealer

platforms as an element of the market structure;

(d) it is not necessary to regulate systems or facilities offering execution services in bespoke or

illiquid derivatives as organised trading venues, as the characteristics associated with such

trading would not yield benefits for these instruments; and

(e) the transparency requirements attached to orders and transactions on organised trading

venues should be tailored to the particular product class and trading functionality in

question and incorporate an appropriate system of waivers.

The views of the UK in relation to specific elements of the proposed OTV regime are provided

below.

Multilateral Access:

The intended meaning of the term “multilateral access” used in the consultation document has

not been elaborated. The term could be interpreted to require the operator of a single dealer

platform to offer access to multiple liquidity takers according to transparent and non-

discriminatory rules. The UK considers this to be the preferable interpretation, given the

distinction between this term and the language currently used in MiFID to describe the

multilateral nature of other platform types, but notes that this could also be viewed as a

UNCLASSIFIED

UNCLASSIFIED

17 of 109

provision requiring the interaction of multiple third party buying and selling interests, in a way

that would preclude the provision of single dealer platforms, and so inhibit competition.

In the event the proposed requirements are intended to refer to a trading methodology which

requires multiple buyers to have the opportunity to interact with multiple sellers within the

system, the UK does not consider such a characteristic to be necessary in order to improve

transparency, protect against market abuse or mitigate systemic risk. In our view, facilities based

on the provision of liquidity by a single provider to multiple third party users (such as a single

dealer platform) could provide a component of an appropriate organised trading regime, co-

existing alongside multilateral platforms. The imposition of tailored requirements upon single

dealer markets as authorised entities, encompassing access rules, transparency, market

surveillance, management of conflicts of interest and operational resilience, would be sufficient

to ensure that derivatives markets adapt in the way envisaged by the G20 while providing

competition and choice to market participants.

In the example of a standardised OTC derivative which, while passing a liquidity threshold for

organised platform trading, does not exhibit the highest levels of liquidity necessary for order

book trading, a requirement for multilateral access would involve the agreement of multiple

liquidity providers to provide prices/quotes on a continuing basis. This may not be feasible for

instruments at the lower end of the liquidity spectrum, resulting in no admission to trading of

the instrument concerned and loss of the associated benefits. The argument has been made that

a requirement for multilateral trading will lead to pricing competition between liquidity providers,

thereby narrowing spreads. In the view of the UK, it should be the case that where multilateral

trading of a derivative product is practicable, liquidity will naturally gravitate to such competitive

models in order to exploit these pricing efficiencies without a regulatory mandate. The

continuing role for single dealer markets tends to suggest that, in some instances, execution

needs may be different (e.g., prioritising certainty or speed of execution, which may be better

achieved where a liquidity taker is able to deal bilaterally with the liquidity provider).

Transparency:

Comments on pre- and post-trade transparency requirements for non-equity instruments are set

out elsewhere in this response. The UK would observe here that while the transparency

requirements for shares within MiFID could be taken as a starting point, it is essential that any

transparency regime targeted at derivatives takes account of the diverse range of asset classes,

whose trading characteristics can differ significantly, and which will therefore require tailored

requirements incorporating an appropriate system of waivers. Market participants have noted

that information regarding completed trades in certain OTC derivatives would not be a reliable

guide to prevailing market conditions, as trade prices are seen to be particularly susceptible to

UNCLASSIFIED

UNCLASSIFIED

18 of 109

trade-sensitive factors such as trade size and the perceived position of the counterparty, in a way

that equities transactions are not.

In addition, the UK considers that any transparency regime should reflect the spectrum of trading

functionalities currently made available to trade OTC derivatives, and which in future could

operate within the parameters of an organised trading regime. Such functionalities include

voice, electronic and hybrid models, for which transparency may be most effectively delivered in

different ways including by means of request for quote facilities and the dissemination of

indicative prices. The UK notes that other trading regimes in the course of development, such as

those for swaps and securities-based swaps in the US, are likely to provide flexibility for organised

platforms to offer request for quote systems based on suitable transparency arrangements,

alongside other execution possibilities.

The UK considers that there should be an opportunity for extensive industry consultation in

relation to the calibration of pre- and post-trade transparency requirements, and that any

proposals in this area must be supported by a robust cost-benefit analysis.

Operators should be able to adopt trading processes which involve the use of discretion

(provided other regulatory requirements can be met). Such discretion is a critical component of

voice based models (often offered as an element of a hybrid model that includes electronic

execution), and ensures that the trading needs of clients can be met in the most efficient fashion.

In the view of the UK, the organisational and operational requirements for organised trading

facilities set out at paragraphs (a) to (h) of section 2.2.1 would be sufficient to ensure that the

G20 objectives were met in relation to the trading of OTC derivatives, when combined with a

carefully specified transparency regime. In addition, the UK would support clarification that

inter-dealer broker systems (bringing together third-party interests and orders by way of voice

and/or hybrid voice/electronic execution) could be examples of organised trading facilities in the

specific context of trading-eligible OTC derivatives. However, the UK does not believe that it is

necessary to regulate (as organised trading venues) systems or facilities offering execution

services in bespoke or illiquid derivatives, which do not meet the criteria to be deemed trading-

eligible. We note that non-standardised derivatives fall outside the scope of the G20

commitment with regard to the promotion of organised platform trading, and that the

characteristics of organised trading would not yield the benefits envisaged by the G20 for such

instruments.

(10) Which criteria could determine whether a derivative is sufficiently liquid to be required to be

traded on such systems? Please explain the reasons for your views.

UNCLASSIFIED

UNCLASSIFIED

19 of 109

The UK notes that work is currently underway under the auspices of IOSCO to consider the

characteristics of an OTC derivative that make on-platform trading practicable, including the

required level of liquidity. As this response was being finalised, IOSCO was due to finalise its

Trading Report imminently. The UK considers that criteria developed for the purposes of EU

legislation should be consistent with international principles and recognise that any liquidity

thresholds will be intrinsically linked to the level of flexibility afforded to trading platforms in

developing execution functionalities. Such criteria should be transparent and objective.

(11) Which market features could additionally be taken into account in order to achieve benefits in

terms of better transparency, competition, market oversight, and price formation? Please be

specific whether this could consider for instance, a high rate of concentration of dealers in a

specific financial instruments, a clear need from buy-side institutions for further transparency, or

on demonstrable obstacles to effective oversight in a derivative trading OTC, etc.

The UK considers that the key factors in the determination of eligibility for platform trading

should be the levels of standardisation and liquidity. Additional factors based on a judgement of

the condition of a particular market could also be valid, but would be secondary to the question

of whether on-platform trading would be practicable.

(12) Are there existing OTC derivatives that could be required to be traded on regulated markets,

MTFs or organised trading facilities? If yes, please justify. Are there some OTC derivatives for

which mandatory trading on a regulated market, MTF, or organised trading facility would be

seriously damaging to investors or market participants? Please explain the reasons for your views.

We support the technical advice of CESR in this regard and consider that the use of industry

targets could have some advantages over a mandatory trading requirement. Adopting a target-

based approach will incentivise platform trading as well as provide flexibility to undertake a

specified proportion of business in standardised derivatives on an OTC basis, where there is a

legitimate reason. Although out of scope of the G20 commitment in relation to the increased

use of trading platforms, and any resultant regulatory action, it is important to note for the sake

of completeness that market participants need to have the ability to trade customised products

on an OTC basis in order to meet legitimate hedging or risk mitigation needs. It is noted that

Dodd-Frank and its associated draft rule-makings do not envisage that “bespoke or illiquid”

swaps will fall within the scope of US trading requirements for “required transactions”10.

The mandatory trading of an OTC derivative on an organised platform could have a significant

detrimental impact where the range of trading functionalities within which such trading could

10

See , for example, draft CFTC rule-making “Core Principles and other Requirements for Swap Execution Facilities” http://www.cftc.gov/LawRegulation/FederalRegister/ProposedRules/2010-32358.html

UNCLASSIFIED

UNCLASSIFIED

20 of 109

take place could not support an instrument possessing the trading characteristics of that

derivative (e.g., the trading of a less liquid instrument on an order book), or where the associated

transparency requirements were too high (for example, in markets dependent on the support of

liquidity providers).

2.3. Automated trading and related issues

(Q13-20)

Summary comments on this subsection

Advances in technology continue to transform how our financial markets operate. The volume of

financial products traded through computer automated trading at high speed and with little

human involvement has increased dramatically in recent years. The UK fully recognises the need

to understand better the impact of these trends, in particular in light of the US “Flash Crash” on

May 6 2010, when US equity markets fell dramatically in the space of minutes, before sharply

rebounding. The UK Treasury is therefore sponsoring a new research project, led by the

Government Office for Science, to explore how computer-generated trading may evolve in the

future. This work will look at price formation, liquidity, financial stability and other issues, and

will complement work already undertaken by the FSA. The UK hopes that the findings of this

research will helpfully inform debate on these issues.

In the meantime there are steps that should be taken to ensure that high risk management

standards prevail across Europe, and the UK supports the Commission‟s proposals for robust risk

controls to be put in place by firms involved in automated trading or who provide sponsored

access to automated traders. Similarly the UK encourages the Commission to look at ways to

tailor the Market Abuse Directive to address any new market abuse risks that may be presented

by algorithmic trading.

However in the absence of further research the UK does not support measures based on the

assumption that high frequency trading is, per se, harmful to markets. The Commission‟s

proposals to subject high frequency traders to market-maker type obligations, and to introduce

restrictions on the submission of orders, appear to be made on the assumption that high

frequency trading is of itself a harmful activity. However, as high frequency traders are also

considered in some cases to be important providers of liquidity, the UK believes it is essential that

any such measures should only be considered after a thorough and scientific assessment of their

costs and benefits.

(13) Is the definition of automated and high frequency trading provided above appropriate?

UNCLASSIFIED

UNCLASSIFIED

21 of 109

We believe that a distinction should be drawn between automated and algorithmic trading. The

Commission defines automated trading as ”the use of computer programs to enter trading

orders where the computer algorithm decides on aspects of execution of the order such as the

timing, quantity and price of the order”. However we think this definition applies to a subset of

automated trading – since automated trading could also include, for example, trades entered

manually but executed electronically. We therefore suggest automated trading be defined as

trading involving the use of a computer, with algorithmic trading given the definition currently

assigned to automated trading in point a) and quoted above.

The UK agrees with the Commission that „HFT is typically not a strategy in itself but the use of

very sophisticated technology to implement traditional trading strategies‟ and that HFT is a

„subcategory of automated trading‟. However, the UK believes that further clarification is needed

on what differentiates a high frequency trader from any other automated trader. As such, the UK

would suggest a more detailed description of HFT as a form of trading with the following

characteristics:

(a) Highly automated and electronic;

(b) Latency sensitive;

(c) A small dispersed inventory, holding positions often for very short periods of time (this can

vary from milliseconds to potentially days or weeks, dependent on strategy);

(d) Low exposure or even „flat‟ overnight which minimises residual risk at end of day; and

(e) Strategies that seek to enter and leave the market with little or no impact.

HFT is not a new phenomenon but rather a natural progression of trading. The basic premise of

trading has not changed, but automation and technology has enabled proprietary traders to do

what they have always done albeit at greater speed and volumes with reduced margins per

trade.

(14) What is your opinion of the suggestion that all high frequency traders over a specified minimum

quantitative threshold would be required to be authorised?

The UK believes that HFT firms that are currently outside the scope of regulation under MiFID

should be regulated where failure to do so might reduce the ability of the markets to remain

efficient, orderly and fair. We do not believe that this occurs at any definable quantitative

threshold. Instead we would suggest that HFT firms could be required to be authorised as

investment firms if they are direct members of trading venues. As direct members, the activities

of high frequency traders directly affect the market and the risks they pose mirror those of

regulated investment firms. However for HFT firms accessing the market through an

UNCLASSIFIED

UNCLASSIFIED

22 of 109

intermediary, the risks associated with their trading (e.g. of erroneous activity) are taken on and

managed by the intermediary and the appropriate regulatory oversight can be delivered via the

regulation of the intermediary. To this end we are strongly supportive of ensuring that firms who

provide sponsored access have robust risk controls in place.

We note that this proposed approach would mesh well with the Commission‟s separate proposal

that trading venues be required to report the transactions of non-authorised members and

participants.

(15) What is your opinion of the suggestions to require specific risk controls to be put in place by

firms engaged in automated trading or by firms who allow their systems to be used by other

traders?

We agree with the Commission‟s view that robust risk controls need to be put in place by firms

involved in automated trading or who provide sponsored access to automated traders.

Automated trading firms need to ensure that they maintain their own strict risk controls both in

quantitative terms and in terms of monitoring trader/programmer competence and behaviour. In

that context, the majority of requirements the Commission propose for regulated firms are

sensible but need to be more specific.

However The UK does not agree with the proposal to require firms „to notify their competent

authority of the computer algorithm(s) they employ‟. The UK‟s reasons are threefold:

(a) Algorithms are continuously updated, which would make it difficult for regulators with

their current resources to keep on top of the latest changes.

(b) The parameters around an algorithm can be as important as the algorithm itself in an

assessment of the impact it might have on a market. For example, an algorithm may have

a parameter that limits its trading to a set percentage either side of the previous day‟s

closing price for a particular stock. A price deviation of a few percent may be reasonable,

but setting the parameter at, say, 20% gives sufficient latitude for the algorithm to cause a

significant shift in the market. Therefore analysis of the algorithm without knowledge of

the parameters is insufficient to form a reliable conclusion on its possible market impact.

Competent authorities being continuously updated with changes to the parameters,

however, would lead to an amplification of the challenge identified above as each

algorithm‟s parameters may be changed every day.

UNCLASSIFIED

UNCLASSIFIED

23 of 109

(c) Algorithms are developed by highly-trained technical specialists. It is therefore unlikely that

competent authorities would have the necessary expertise to conduct any meaningful in-

depth analysis of their functionality.

The UK therefore recommends that this point is not taken forward into legislation. What might

be of greater value would be to develop guidance on the types of algorithmic activity that might

be viewed as abusive. This could be addressed in the Commission‟s review of the Market Abuse

Directive.

(16) What is your opinion of the suggestion for risk controls (such as circuit breakers) to be put in

place by trading venues?

The UK agrees with the principle that risk controls should be in place at trading venues, and

indeed this is already a longstanding focus of the FSA‟s supervisory approach. However we would

point out that there are established alternatives to circuit breakers such as limit-up/limit-down

systems (which allow continuous trading within prescribed bands).

We also consider that trading venues need to have real-time trading checks and controls in place,

with the ability to halt a trading firm‟s message and order flow if needs be. Venues should also

conduct ongoing checks of their participants to ensure that they maintain and update their

controls as necessary, including those who co-locate at the platform data centre.

(17) What is your opinion about co-location facilities needing to be offered on a non-discriminatory

basis?

The UK agrees that space in a data centre for co-location should be provided on a non-

discriminatory basis. However, the UK believes that „equal and fair access‟ should refer to equality

of opportunity rather than equality of outcome. Venues do not have unlimited space available to

offer co-location facilities, and not every market participant has the resources or desire to invest

in the necessary infrastructure for co-location. Therefore the UK considers that: i) pricing should

be transparent and non-discriminatory; ii) co-location should be offered on reasonable

commercial terms; and iii) venue operators should be free to determine the space available for

co-location.

(18) Is it necessary that minimum tick sizes are prescribed?

We do not believe that it is necessary to prescribe minimum tick sizes. We consider that the

market has found and will continue to find the right levels of tick sizes, and that the possibility of

regulatory intervention provides sufficient incentive to ensure continued harmonisation. We are

UNCLASSIFIED

UNCLASSIFIED

24 of 109

unaware of any significant problems to date with the way venues set tick sizes; indeed the need

for a venue (and market participants) to update systems when tick sizes change or other venues

have different tick regimes tends to provide a natural check on frequent (and therefore

potentially disruptive) changes to tick sizes. Further we believe that, as venues are closer to

trading participants than regulators, they are better placed to understand their needs and set

appropriate ticks.

The potential difficulties and unintended consequences of mandating minimum tick sizes can be

seen in the US, where a minimum tick size of 1c is in place for all stocks over $1. There is a

strong belief amongst some market participants that trading of these stocks has been driven into

dark pools. Citigroup is commonly cited as a low-price equity (c.US$4-5) that is traded on dark

(ATS) venues that have a competitive advantage over registered exchanges due to the fact that

they are not bound by a minimum tick size regime. We are aware of a recent industry led

agreement on harmonised tick sizes and support this initiative.

(19) What is your opinion of the suggestion that high frequency traders might be required to provide

liquidity on an ongoing basis where they actively trade in a financial instrument under similar

conditions as apply to market makers? Under what conditions should this be required?

We do not think a case has been made to mandate the provision of liquidity by high frequency

traders. If trading platforms want to provide members the opportunity to become market makers

they can already do so. The UK considers that forcing high frequency traders to become market

makers may deter them from entering the market altogether, thereby removing the benefits of

the liquidity they currently provide voluntarily. It may also create prudential risks to these firms,

leaving them exposed to market movements when other participants are at liberty to withdraw.

Given these potentially harmful side effects, and an absence of evidence as to the potential

benefits, we cannot support this proposal.

(20) What is your opinion about requiring orders to rest on the order book for a minimum period of