Final Report 2003

52

A REPORT ON AWARENESS OF INSUARANCE BY : - ADITI KULSHRESHTHA BIFT,HYDERABAD (2008-2010) ORGANISATION : BAJAJ ALLIANZ LIFE INSURANCE COMPANY LIMITED ALWAR ACKNOWLEDGEMENTS

-

Upload

aditi-kulshreshtha -

Category

Documents

-

view

217 -

download

0

Transcript of Final Report 2003

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 1/52

A REPORT

ON

AWARENESS OF INSUARANCE

BY : -

ADITI KULSHRESHTHA

BIFT,HYDERABAD (2008-2010)

ORGANISATION :

BAJAJ ALLIANZLIFE INSURANCE COMPANY LIMITED

ALWAR

ACKNOWLEDGEMENTS

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 2/52

Sometimes words fall short to show gratitude ,the same happened with

me during this project. The immense help and support from Bajaj

Allianz Insurance Company overwhelmed me during this project.

My sincere gratitude to Mr. Gaurav Khatri,who provided me with this

opportunity to work with BAJAJ Allianz company.

I am highly indebted to Mr.Chandrakant Gupta (Branch Service

Manager,BajajAllianz,Alwar) who provided me with the necessary

information and his valuable suggestions and comments on bringing out

this project in the best possible way.

I also thank Ms. Mehnaz Siddiqui and the faculty members who have

sincerely supported me with the valuable insights in the project.

Last but not the least, my heartfelt love for my parents whose constant

support and blessings have helped me through out this project.

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 3/52

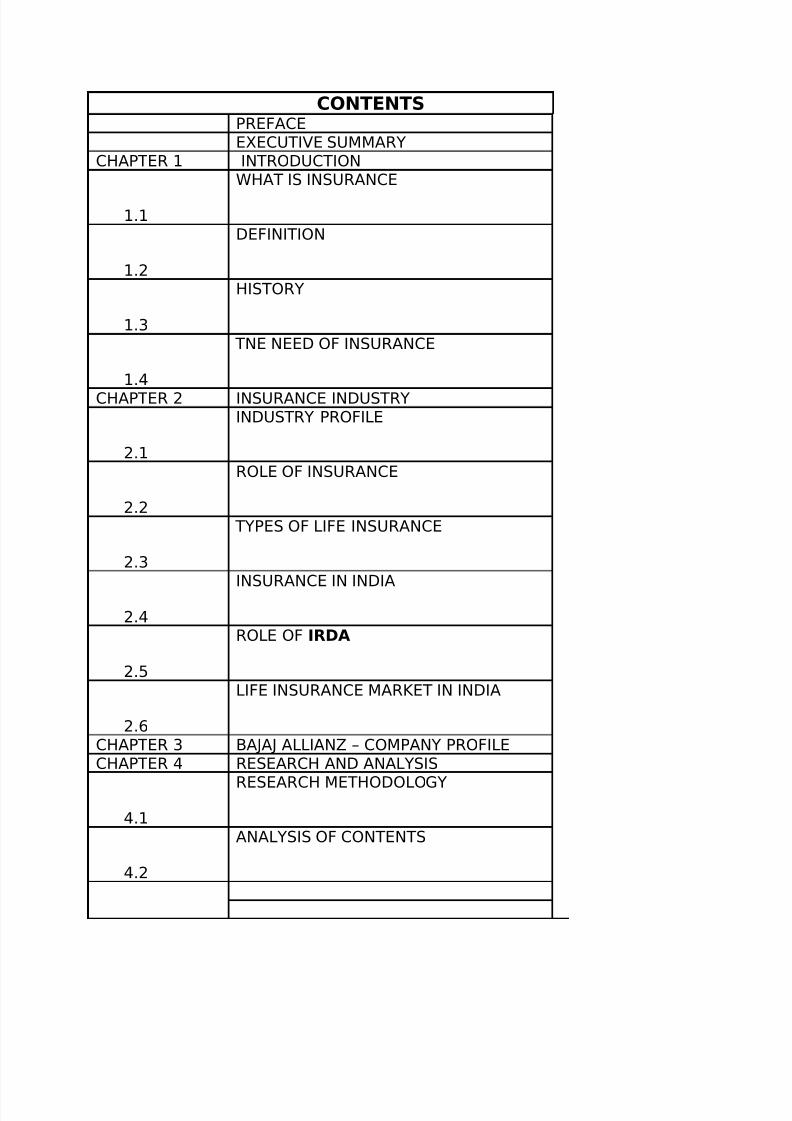

CONTENTSPREFACE

EXECUTIVE SUMMARY

CHAPTER 1 INTRODUCTION

1.1

WHAT IS INSURANCE

1.2

DEFINITION

1.3

HISTORY

1.4

TNE NEED OF INSURANCE

CHAPTER 2 INSURANCE INDUSTRY

2.1

INDUSTRY PROFILE

2.2

ROLE OF INSURANCE

2.3

TYPES OF LIFE INSURANCE

2.4

INSURANCE IN INDIA

2.5

ROLE OF IRDA

2.6

LIFE INSURANCE MARKET IN INDIA

CHAPTER 3 BAJAJ ALLIANZ – COMPANY PROFILE

CHAPTER 4 RESEARCH AND ANALYSIS

4.1

RESEARCH METHODOLOGY

4.2

ANALYSIS OF CONTENTS

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 4/52

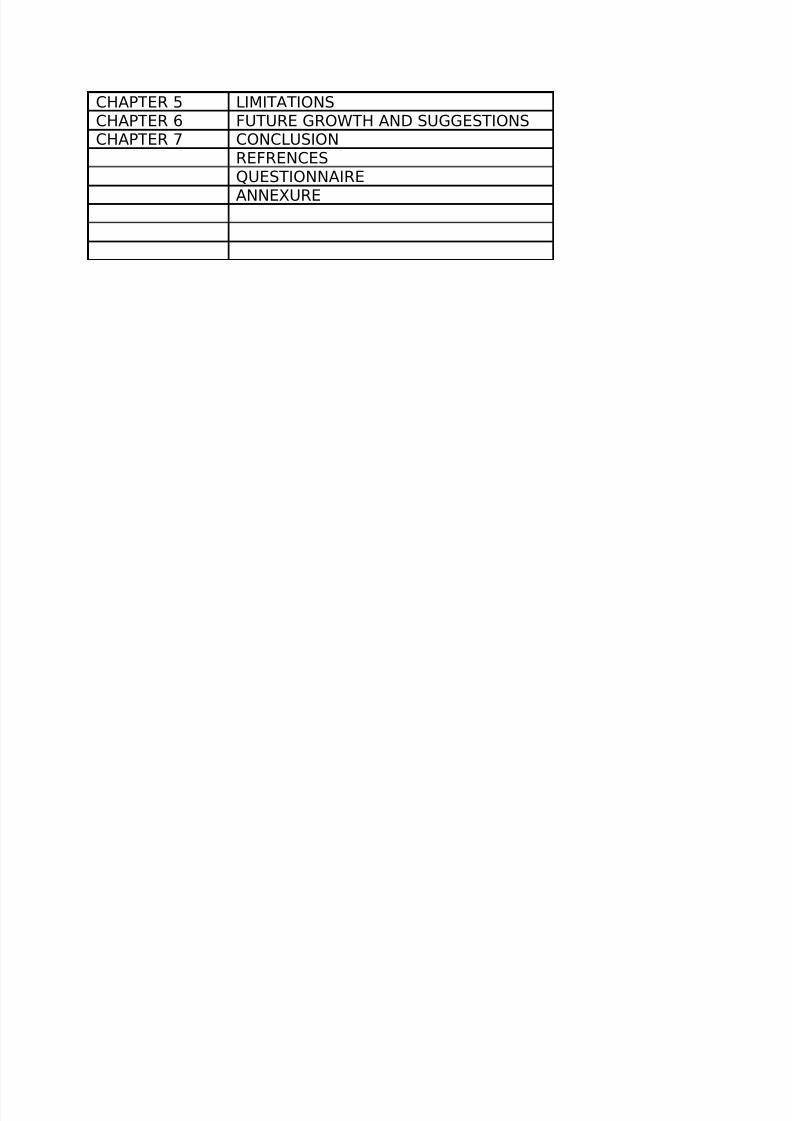

CHAPTER 5 LIMITATIONS

CHAPTER 6 FUTURE GROWTH AND SUGGESTIONS

CHAPTER 7 CONCLUSION

REFRENCES

QUESTIONNAIRE

ANNEXURE

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 5/52

PREFACE

The liberalization of Indian Insurance sector has been the subject of much heated debate for

some years. The policy makers on the one hand wanted competition, development and growth of

this insurance sector which is extremely essential for channeling the investments into theinfrastructure sector. At the other end the policy makers had the fears that the insurance

premiums, which are substantial, would seep out of the country; and wanted to have a cautiousapproach of opening for foreign participation in the sector.

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 6/52

As one of the rare occurrences the entire debate was put on the back burner and the IRDA saw

the day of the light, thanks to the maturing politics emerging consensus among factions of

different political parties. Though some changes and some restrictive clauses as regards to theforeign participation were included the IRDA has opened the doors for the private entry into

insurance.

Whether the insurer is old or new, private or public, expanding the market will present multitudeof challenges and opportunities. But the key issues, possible trends, opportunities and challenges

the insurance sector will have still remains under the realms of the possibilities and speculation.

What is likely impact of opening up of india’s insurance sector?

The large scale of operations, public sector bureaucracies and cumbersome procedures hampersnationalized insurers. Therefore potential private entrants expect to score in the areas of customer

service speed and flexibility. They point out that their entry will mean better choice and productsfor the consumer. The critics counter that the benefit will be slim, because new players will

concentrate on affluent, urban customers as foreign banks did until recently. This seems to be a

logical strategy. Start up costs such as those of setting up a conventional distribution network are

large and high end niches offer better returns. However the middle market segment too has great potential. Since 8insurance is a volumes game. Therefore, private insurers would be best served

by a middle-market approach, targeting customer segments that are currently untapped.

Executive Summary

• Title : Awarenees of insurance

• Duration : 45 day

• Company: Bajaj allianz Life Insurance

• Research Objective

Objectives

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 7/52

Primary objective

The primary objective of this is to assist or to estimate market potential for life insurance

products in Alwar city and to find conclusion.

Secondary Objective

• To find out the market credibility of BAJAJ Allianz Brand as insurance company.

• Conduct a Questionnaire survey to gauge the mindset of a common man.

• To help designing the forth coming policies of the company to cater the needs of

customers.

• To make an analysis of the present market situation

• To know market potential for life insurance for Bajaj Allianz

• To study the history, present and future of life insurance market.

• To have an overview of the present status of company with respect to its competitors.

For this purpose, prior appointments were taken from the people we had to interview. The

purpose was not just to get the questionnaires filled but a marketing & sales person

accompanied us during the survey who use to tell various policies of BAJAJ Allianz to theinterested customers, its features and also the tailor made General insurance policies.

This survey thus acted as a dual purpose venture, analysis and survey along with marketingof the products.

Though many people seemed uninterested, but certainly some of them were quite cooperative

and listened carefully and many of them seemed interested while two of them opted for tailor made products too.

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 8/52

INTRODUCTION

What is insurance?

All assets have economic value. The asset would have been created through the efforts

of the owner, in the expectation that, either through the income generated there from

or some other output, some of his needs would be met. In the case of a motor car, it

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 9/52

provides comfort & convenience in transportation. There is no direct income. There is

a normally expected life time for the asset during which time it is expected to perform.

The owner, aware of this, can so manage his affairs that by the end of that life time, a

substitute is made available to ensure that the value or income is not lost.

However, if the asset gets lost earlier, being destroyed or made non-functional,

through an accident or other unfortunate event, the owner & those deriving benefits

there from suffer.Hence Insurance is a tool which helps to reduce effects of such

adverse events.

A human life is also an income-generating asset. This asset also can be lost through

unexpectedly early death or made non-functional through sickness & disabilities caused

by accidents. Accidents may or may not happen. Death will happen, but the timing is

uncertain. If it happens around the time of one's retirement, when it could be expected that

the income will cease, the person concerned could have made some other arrangements to

meet the continuing needs. But if it happens much earlier when the alternate arrangements

are not in place, insurance is necessary to help the dependents.

In case of a human being, he may have made arrangements for his needs after his

retirement. These would have been made on the basis of some expectations like he

may live for another 15 years, or that his children will look after him. If any of these

expectations do not come true, the original arrangement would become inadequate and

there could be difficulties.

Living too long can be as much a problem as dying too young. These are risks, which

need to be safeguarded against. Insurance takes care of it.

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 10/52

DEFINITION

• promise of reimbursement in the case of loss; paid to people or companies so concerned

about hazards that they have made prepayments to an insurance company

• policy: written contract or certificate of insurance; "you should have read the small print

on your policy"

•

indemnity: protection against future loss

Insurance is a system to alleviate financial losses by transferring risk of loss from one

entity to another

A contract in which one party agrees to pay for another party's financial loss resulting

from a specified event (for example, a collision, theft, or storm damage). Lease

agreements generally require that you maintain vehicle collision and comprehensive

insurance as well as liability insurance for bodily injury and property damage.

Plan in which individuals and organization who are concerned about potential risks will

pay premiums to an insurance company, who in return, will reimburse them if there is

loss. To generate a profit, the insurer will invest the premiums it receives. Examples of

the different types of insurance available are automobile, home, health and worker's

compensation. Whereas in most cases the insured is paid for their loss, with life insurance

a beneficiary is paid when the insured person passes away.

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 11/52

HISTORY

The origin and practice of insurance is as ancient as human civilization.

From Cave age till date, the story of evolution of mankind is in fact a saga of continuous

search for security. His problems have been the same, though the form has changed with

the social & economic circumstances.

When man used to live in the caves, he used to search for security against animals because

they could kill him while he was asleep. He was not at all sure if he could hunt every day

& get his food.

Because of the above insecurity he used to live in groups so that the other members of the

tribe could come to help him in time of crisis.

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 12/52

Later on, insurance was practiced in a different form. Small contributions of food grains

were collected from farmers, hoarded in the local temple premises to be released when

there was a famine or other calamity.

Today, insurance works on the same principle. But, with growing financial implications

the process started demanding money rather than community contribution.

The modern concept of insurance came to India with the arrival of Europeans. The first life

Insurance company was established in India in 1818 as Oriental life insurance company by

Europeans for the welfare of widows of Europeans.

It was strange that many of the Companies floated thereafter were looking after European

interest and even charged extra premium on Indian lives. Bombay mutual life Assurance society

Ltd. established in 1870 was the first to stop this discrimination . This was the year in which the

first Insurance act was passed by the British parliament. The insurance business flourished

thereafter.

By the year 1955 there were 245 insurance companies and provident societies, out of which 16

were non Indian companies.

A comprehensive legislation "The Insurance act 1938" was passed with a view to consolidate

and amend the laws relating to the business of insurance. It came into force with effect from

July '01, 1939.The act was modified in 1950 .

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 13/52

The broader objectives of socialism prompted the government to nationalize the insurance

business, in the year 1956. The general insurance business was nationalized in 1972, through

GIC Act 1972. The Life Insurance corporation of India came into existence on 1st September

1956.

Why one needs Insurance?

Life is full of uncertainties. We all know that death is certain but the timing is uncertain. This

uncertainty of time has led to the invention of insurance

We all make efforts towards earning a living and then working hard for its betterment. Insurance

is necessary to ensure that the basic necessities of life, comfort and pleasure derived by all of us

from our living continues to be available for us.

People buy insurance because they realize the need of protection for their families after their

death or of a reserve for emergencies and of additional income for later years.

Hence we can say " Life insurance is indeed a necessity of life".

Life insurance protects against loss of income of an individual. Life insurance does not protect

the asset. It also does not prevent its loss.

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 14/52

The concept of insurance has been extended beyond the coverage of tangible assets. Exporters

run the risk of the importers in the other country defaulting as well as losses due to sudden

change in currency exchange rates, economic policies or political disturbances. These risks are

now insured.

Doctors run the risk of being charged with negligence and subsequent liability for damages. The

amounts in question can be fairly large, beyond the capacity of individuals to bear. These are

insured. Thus, insurance is extended to intangibles. In some countries,

the voice of a singer or the legs of a dancer may be insured.

INDUSTRY PROFILE

Origin Of Life Insurance

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 15/52

Almost 4,500 years ago, in the ancient land of Babylonia, traders used to bear risk of the caravan

trade by giving loans that had to be later repaid with interest when the goods arrived safely. In

2100 BC, the Code of Hammurabi granted legal status to the practice

That’s perhaps, was how insurance made its beginning.

Life insurance had its origins in ancient Rome, where citizens formed burial clubs that would

meet the funeral expenses of its members as well as help survivors by making some payments.

As European civilization progressed, its social institutions and welfare practices also got more

and more refined. With the discovery of new lands, sea routes and the consequent growth in

trade, medieval guilds took it upon themselves to protect their member traders from loss on

account of fire, shipwrecks and the like.

Since most of the trade took place by sea, there was also the fear of pirates. So these guilds even

offered ransom for members held captive by pirates. Burial expenses and support in times of

sickness and poverty were other services offered. Essentially, all these revolved around the

concept of insurance or risk coverage. That's how old these concepts are, really.

In 1347, in Genoa, European maritime nations entered into the earliest known insurance contract

and decided to accept marine insurance as a practice.

The first step...

Insurance as we know it today owes its existence to 17th century England. In fact, it began

taking shape in 1688 at a rather interesting place called Lloyd's Coffee House in London, where

merchants, ship-owners and underwriters met to discuss and transact business. By the end of the

18th century, Lloyd's had brewed enough business to become one of the first modern insurance

companies.

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 16/52

Enter companies...

The first stock companies to get into the business of insurance were chartered in England in

1720. The year 1735 saw the birth of the first insurance company in the American colonies in

Charleston, SC.

In 1759, the Presbyterian Synod of Philadelphia sponsored the first life insurance corporation in

America for the benefit of ministers and their dependents.

However, it was after 1840 that life insurance really took off in a big way. The trigger: reducing

opposition from religious groups

The growing years...

The 19th century saw huge developments in the field of insurance, with newer products being

devised to meet the growing needs of urbanization and industrialization.

In 1835, the infamous New York fire drew people's attention to the need to provide for sudden

and large losses. Two years later, Massachusetts became the first state to require companies by

law to maintain such reserves. The great Chicago fire of 1871 further emphasized how fires can

cause huge losses in densely populated modern cities. The practice of reinsurance, wherein the

risks are spread among several companies, was devised specifically for such situations.

There were more offshoots of the process of industrialization. In 1897, the British government

passed the Workmen's Compensation Act, which made it mandatory for a company to insure its

employees against industrial accidents.

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 17/52

With the advent of the automobile, public liability insurance, which first made its appearance in

the 1880s, gained importance and acceptance?

In the 19th century, many societies were founded to insure the life and health of their members,

while fraternal orders provided low-cost, members-only insurance.

Even today, such fraternal orders continue to provide insurance coverage to members as do most

labour organizations. Many employers sponsor group insurance policies for their employees,

providing not just life insurance, but sickness and accident benefits and old-age pensions.

Employees contribute a certain percentage of the premium for these policies.

In India...

Insurance in India can be traced back to the Vedas. For instance, yogakshema, the name of Life

Insurance Corporation of India's corporate headquarters, is derived from the Rig Veda. The term

suggests that a form of "community insurance" was prevalent around 1000 BC and practiced by

the Aryans.

Bombay Mutual Assurance Society, the first Indian life assurance society, was formed in 1870.

Other companies like Oriental, Bharat and Empire of India were also set up in the 1870-90s.

It was during the swadeshi movement in the early 20th century that insurance witnessed a big

boom in India with several more companies being set up.

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 18/52

As these companies grew, the government began to exercise control on them. The Insurance Act

was passed in 1912, followed by a detailed and amended Insurance Act of 1938 that looked into

investments, expenditure and management of these companies' funds.

By the mid-1950s, there were around 170 insurance companies and 80 provident fund societies

in the country's life insurance scene. However, in the absence of regulatory systems, scams and

irregularities were almost a way of life at most of these companies.

As a result, the government decided to nationalize the LIFE INSURANCE business in India.

THE LIFE INSURANCE CORPORATION OF INDIA was set up in 1956 to take over around

250 life companies.

For years thereafter, insurance remained a monopoly of the public sector. It was only after seven

years of deliberation and debate - after the RN Malhotra Committee report of 1994 became the

first serious document calling for the re-opening up of the insurance sector to private players --

that the sector was finally opened up to private players in 2001.The INSURANCE

REGULATORY & DEVELOPMENT AUTHORITY, an autonomous insurance regulator set up

in 2000, has extensive powers to oversee the insurance business and regulate in a manner that

will safeguard the interests of the insured

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 19/52

Role of Life Insurance

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 20/52

Risks and uncertainties are part of life’s great adventure – accident, illness, theft, natural

disaster – they’re all built in o the working of the Universe, waiting to happen.

Role 1: Life insurance as “Investment”

Insurance is an attractive option for investment. While most people recognize the risk hedging

and tax saving potential of insurance, many are not aware of its advantages as an investment

option as well. Insurance products yield more compared to regular investment options, and this is

besides the added incentives offered by insurers.

You cannot compare an insurance product with other investment schemes for the simple reason

that it offers financial protection from risks, something that is missing in non-insurance products.

In fact, the premium you pay for an insurance policy is an investment against risk. Thus, before

comparing with other schemes, you must accept that a part of the total amount invested in life

insurance goes towards providing for the risk cover, while the rest is used for savings.

In life insurance, unlike non-life products, you get maturity benefits on survival at the end of the

term. In other words, if you take a life insurance policy for 20 years and survive the term, the

amount invested as premium in the policy will come back to you with added returns. In the

unfortunate event of death within the tenure of the policy, the family of the deceased will receive

the sum assured.

“INSURANCE is a unique investment avenue that delivers sound returns in addition to

protection.”

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 21/52

Role 2: Life insurance as “Risk cover”

First and foremost, insurance is about risk cover and protection – financial protection, to be more

precise – to help outlast life’s unpredictable losses. Designed to safeguard against losses suffered

on account of any unforeseen event, insurance provides you with that unique sense of securitythat no other form of investment provides. By buying life

insurance, you buy peace of mind and are prepared to face any financial demand that would hit

the family in case of an untimely demise.

To provide such protection, insurance firms collect contributions from many people who face the

same risk. A loss claim is paid out of the total premium collected by the insurance companies,who act as trustees to the monies.

Insurance also provides a safeguard in the case of accidents or a drop in income after retirement.An accident or disability can be devastating, and an insurance policy can lend timely support to

the family in such times. It also comes as a great help when you retire, in case no untoward

incident happens during the term of the policy.

With the entry of private sector players in insurance, you have a wide range of products andservices to choose from. Further, many of these can be further customized to fit individual/group

specific needs. Considering the amount you have to pay now, it’s worth buying some extra sleep.

Role 3: Life insurance as “Tax planning”

Insurance serves as an excellent tax saving mechanism too. The Government of India has offered

tax incentives to life insurance products in order to facilitate the flow of funds into productiveassets. Under Section 88 of Income Tax Act 1961, an individual is entitled to a rebate of 20 per

cent on the annual premium payable on his/her life and life of his/her children or adult children.

The rebate is deductible from tax payable by the individual or a Hindu Undivided Family. Thisrebate is can be availed upto a maximum of Rs 12,000 on payment of yearly premium of Rs

60,000. By paying Rs 60,000 a year, you can buy anything upwards of Rs 10 lakh in sum

assured. (depending upon the age of the insured and term of the policy) This means that you get

a Rs 12,000 tax benefit. The rebate is deductible from the tax payable by an individual or aHindu Undivided Family.

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 22/52

Types of life insurance

Most of the products offered by Indian life insurers are developed and structured around these

"basic" policies and are usually an extension or a combination of these policies. So, what are

these policies and how do they differ from each other?

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 23/52

• A term insurance policy is a pure risk cover for a specified period of time. What this

means is that the sum assured is payable only if the policyholder dies within the policy

term. For instance, if a person buys Rs 2 lakh policy for 15-years, his family is entitled to

the money if he dies within that 15-year period.

• What if he survives the 15-year period? Well, then he is not entitled to any payment; the

insurance company keeps the entire premium paid during the 15-year period.

• So, there is no element of savings or investment in such a policy. It is a 100 per cent risk

cover. It simply means that a person pays a certain premium to protect his family against

his sudden death. He forfeits the amount if he outlives the period of the policy. This

explains why the Term Insurance Policy comes at the lowest cost.

WHOLE LIFE POLICY

• As the name suggests, a Whole Life Policy is an insurance cover against death,

irrespective of when it happens.

• Under this plan, the policyholder pays regular premiums until his death, following which

the money is handed over to his family.

This policy, however, fails to address the additional needs of the insured during his post-

retirement years. It doesn't take into account a person's increasing needs either. While the insured

buys the policy at a young age, his requirements increase over time. By the time he dies, the

value of the sum assured is too low to meet his family's needs. As a result of these drawbacks,

insurance firms now offer either a modified Whole Life Policy or combine in with another type

of policy.

TERM INSURANCE POLICY

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 24/52

ENDOWMENT POLICY

Combining risk cover with financial savings, an endowment policy is the most popular policies

in the world of life insurance.

• In an Endowment Policy, the sum assured is payable even if the insured survives the

policy term.

• If the insured dies during the tenure of the policy, the insurance firm has to pay the sum

assured just as any other pure risk cover.

• A pure endowment policy is also a form of financial saving, whereby if the person

covered remains alive beyond the tenure of the policy, he gets back the sum assured with

some other investment benefits.

In addition to the basic policy, insurers offer various benefits such as double endowment and

marriage/ education endowment plans. The cost of such a policy is slightly higher but worth its

value.

MONEY BACK POLICY

• These policies are structured to provide sums required as anticipated expenses (marriage,

education, etc) over a stipulated period of time. With inflation becoming a big issue,

companies have realized that sometimes the money value of the policy is eroded. That is

why with-profit policies are also being introduced to offset some of the losses incurred on

account of inflation.

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 25/52

• A portion of the sum assured is payable at regular intervals. On survival the remainder of

the sum assured is payable.

• In case of death, the full sum assured is payable to the insured.

The premium is payable for a particular period of time.

ANNUITIES AND PENSION

In an annuity, the insurer agrees to pay the insured a stipulated sum of money periodically. The

purpose of an annuity is to protect against risk as well as provide money in the form of pension

at regular intervals.

Over the years, insurers have added various features to basic insurance policies in order to

address specific needs of a cross section of people.

INSURANCE IN INDIA

The insurance sector in India has come a full circle from being an open competitive

market to nationalisation and back to a liberalised market again. Tracing the

developments in the Indian insurance sector reveals the 360 degree turn witnessed over a

period of almost two centuries.

A brief history of the Insurance sector

The business of life insurance in India in its existing form started in India in the year

1818 : With the establishment of the Oriental Life Insurance Company in Calcutta.

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 26/52

Some of the important milestones in the life insurance business in India are:

1912: The Indian Life Assurance Companies Act enacted as the first statute to regulate

the life insurance business.

1928: The Indian Insurance Companies Act enacted to enable the government to collect

statistical information about both life and non-life insurance businesses.

1938: Earlier legislation consolidated and amended to by the Insurance Act with the

objective of protecting the interests of the insuring public.

1956: 245 Indian and foreign insurers and provident societies taken over by the central

government and nationalised. LIC formed by an Act of Parliament, viz. LIC Act,

1956, with a capital contribution of Rs. 5 crore from the Government of India.

The General insurance business in India, on the other hand, can trace its roots to the

Triton Insurance Company Ltd., the first general insurance company established in the

year 1850 in Calcutta by the British.

Some of the important milestones in the general insurance business in India are:

1907: The Indian Mercantile Insurance Ltd. set up, the first company to transact all

classes of general insurance business.

1957: General Insurance Council, a wing of the Insurance Association of India, frames a

code of conduct for ensuring fair conduct and sound business practices.

1968: The Insurance Act amended to regulate investments and set minimum solvency

margins and the Tariff Advisory Committee set up.

1972: The General Insurance Business (Nationalisation) Act, 1972 nationalised the

general insurance business in India with effect from 1st January 1973.

107 insurers amalgamated and grouped into four companies viz. the National

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 27/52

Insurance Company Ltd., the New India Assurance Company Ltd., the

Oriental Insurance Company Ltd. and the United India Insurance Company

Ltd. GIC incorporated as a company.

Insurance sector reforms

In 1993, Malhotra Committee, headed by former Finance Secretary and RBI Governor R.

N. Malhotra, was formed to evaluate the Indian insurance industry and recommend its

future direction.

The Malhotra committee was set up with the objective of complementing the reforms

initiated in the financial sector.

The reforms were aimed at “creating a more efficient and competitive financial system

suitable for the requirements of the economy keeping in mind the structural changes

currently underway and recognising that insurance is an important part of the overall

financial system where it was necessary to address the need for similar reforms…”

In 1994, the committee submitted the report and some of the key recommendations

included:

1.) Structure

G overnment stake in the insurance Companies to be brought down to 50%

Government should take over the holdings of GIC and its subsidiaries so that these

subsidiaries can act as independent corporations

All the insurance companies should be given greater freedom to operate

2.) Competition

Private Companies with a minimum paid up capital of Rs.1bn should be allowed

to enter the industry

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 28/52

No Company should deal in both Life and General Insurance through a single

entity

Foreign companies may be allowed to enter the industry in collaboration with the

domestic companies

Postal Life Insurance should be allowed to operate in the rural market

Only one State Level Life Insurance Company should be allowed to operate in

each state

3.) Regulatory Body

The Insurance Act should be changed

An Insurance Regulatory body should be set up

Controller of Insurance (Currently a part from the Finance Ministry) should be

made independent

4.) Investments

Mandatory Investments of LIC Life Fund in government securities to be reduced

from 75% to 50%

GIC and its subsidiaries are not to hold more than 5% in any company (There

current holdings to be brought down to this level over a period of time)

5.) Customer Service

LIC should pay interest on delays in payments beyond 30 days

Insurance companies must be encouraged to set up unit linked pension plans

Computerization of operations and updating of technology to be carried out in the

insurance industry

The committee emphasized that in order to improve the customer services and increase

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 29/52

the coverage of the insurance industry should be opened up to competition. But at the

same time, the committee felt the need to exercise caution as any failure on the part of

new players could ruin the public confidence in the industry.

Hence, it was decided to allow competition in a limited way by stipulating the minimum

capital requirement of Rs.100 crores. The committee felt the need to provide greater

autonomy to insurance companies in order to improve their performance and enable them

to act as independent companies with economic motives. For this purpose, it had

proposed setting up an independent regulatory body.

The Insurance Regulatory and Development Authority

Reforms in the Insurance sector were initiated with the passage of the IRDA Bill in

Parliament in December 1999. The IRDA since its incorporation as a statutory body in

April 2000 has fastidiously stuck to its schedule of framing regulations and registering

the private sector insurance companies.

The other decisions taken simultaneously to provide the supporting systems to the

insurance sector and in particular the life insurance companies was the launch of the

IRDA’s online service for issue and renewal of licenses to agents.

The approval of institutions for imparting training to agents has also ensured that the

insurance companies would have a trained workforce of insurance agents in place to sell

their products, which are expected to be introduced by early next year.

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 30/52

Since being set up as an independent statutory body the IRDA has put in a framework of globally

compatible regulations. Total number of life insurers under the Authority has gone upto 21,while

total number of general insurers registered with IRDA has reached 20.

Insurance Sector

4.47 Reforms in the insurance sector commenced with the enactment of the Insurance Regulatory

and Development Authority Act 1999, which facilitated the entry of private insurance companies

into the Indian insurance market. The Insurance Regulatory and Development Authority

(IRDA) was set up on April 19, 2000 to protect the interest of the holders of insurance policies,

and to regulate, promote and ensure orderly growth of the insurance industry.

Life Insurance Market in India

source:www.freepress.in

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 31/52

Total Population 1.13 Billion (113 cr.)

Total Population of Middle

Class350 Million (35 Cr.)

Total Population Insured 80 Million (8 Cr.)

That is only 20% of the total insurable population is insured.

The Major Life Insurance Players in the industry…

Potential of Insurance Market

** Tremendous potential for selling insurance

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 32/52

COMPANY PROFILE

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 33/52

Bajaj Allianz Life Insurance Co. Ltd. is a joint venture between two leading

conglomerates- Allianz AG, one of the world's largest insurance companies,

and Bajaj Auto Limited, one of the biggest 2 and 3 wheeler manufacturers

in the world.

Bajaj Allianz Life Corporation limited was incorporated on 12th March

2001. the company received the Insurance Regulatory and

Development Authority (IRDA) certificate of Registration(R3) No. 116

on 3rd August 2001 to conduct Life Insurance Business in India.

Bajaj Allianz Shareholder Capital base stands at Rs.500 crore with

Bajaj Auto Limited and Allianz AG of Germany holding 74% and 26%

stake respectively. It is the 2nd largest private player in Insurance

industry in India with a market share of 13.2% amongst the private

companies as on 25th Feb,2009.

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 34/52

Bajaj Auto Limited

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 35/52

Bajaj Auto Ltd, the flagship company of the Rs. 8000 Crore Bajaj

Group is the largest manufacturer of two wheelers and three wheelers

in India and one of the largest in the world.

A household name in India, Bajaj Auto has a strong brand image &

brand loyalty synonymous with quality and customer focus. With over

15,000 employees, the company is a Rs. 4000 crore auto giant. AAA

rated by Crisil, Bajaj Auto has been in operation for over 55 years. It

has joined hands with Allianz to provide the Indian consumers with a

distinct option in terms of life insurance products.

As a promoter of Bajaj Allianz Life Corporation Ltd., Bajaj Auto has the

following to offer –

• Financial strength and stability to support the insurance

business.

• A strong Brand equity.

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 36/52

• A good market reputation as a world class organization.

• An extensive distribution network.

• Adequate experience of running a large organization.

• A 10 million strong base of customers using Bajaj products.

• Advanced Information Technology in extensive use.

• Experience in the financial services industry through Bajaj Auto

Finance Ltd.

Allianz AG

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 37/52

Founded in 1890 in Berlin, Allianz is now present in over 70 countries with

almost 174,000 employees. At the top of the international group is the

holding company, Allianz AG, with its head office in Munich.

Allianz AG is the business of General (Property and Casualty) Insurance; Life

and Health Insurance and Asset Management and has been in operation for

over 110 years. Allianz is one of the largest global composite insurers with

operation in over 70 countries. Further, the group provides Risk

Management and Loss Prevention Services. Allianz has insured most of the

world’s largest infrastructure projects (including Hong Kong Airport and

channel tunnel between UK and France), further Allianz insures the majority

of Fortune 500 companies, besides being a large industry insurer, Allianz has

a substantial portfolio in the commercial and personal lines sector, using a

wide variety of innovative distribution channels.

Allianz AG – A GLOBAL FINANCIAL POWERHOUSE

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 38/52

• Worldwide second by Gross Written Premiums(GWR) – Rs. 4,46,654

cr.

• 3rd largest Asset Under Management (AUM) & and largest amongst

insurance cos. AUM of Rs. 51, 96,959 cr.

• 12th largest corporation in the world.

• 49.8% of global business from life insurance.

• Established in 1890, 110 years of insurance expertise.

RESEARCH METHODOLOGY

Research is an art of scientific investigation

Research means “ a careful investigation or inquiry specially through search for new facts

in any branch of knowledge.”

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 39/52

In the project titled as “AWARENESS OF INSURANCE “ we need to find out the

general awareness amongst people as well as the brand image of Bajaj Allianz as a whole

so that we can estimate the current market position and credibility of the company for this

research need to be done. The market credibility required the collection of Primary as

well as Secondary data. The credibility literally means the market value and market

positioning of a particular brand or a company among its competitors. BAJAJ Allianz is

one of the private life insurance companies, which came into existence in 2001.Market

credibility, can be checked by seeing the awareness of people about a particular company

and its share in the market. comparing the products of term policies as well as the

endowment policies.

PRIMARY DATA : Questionnaire filled by people interviewed.

SECONDARY DATA : (i) Data collected from companies from various sites

available for various life insurance companies.

(ii) Data available with company’s database

ANALYSIS OF CONTENT

There were about 15 questions in the questionnaire on the basis of which findings were

done and analysis was made. The response to the questions in the questionnaire are

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 40/52

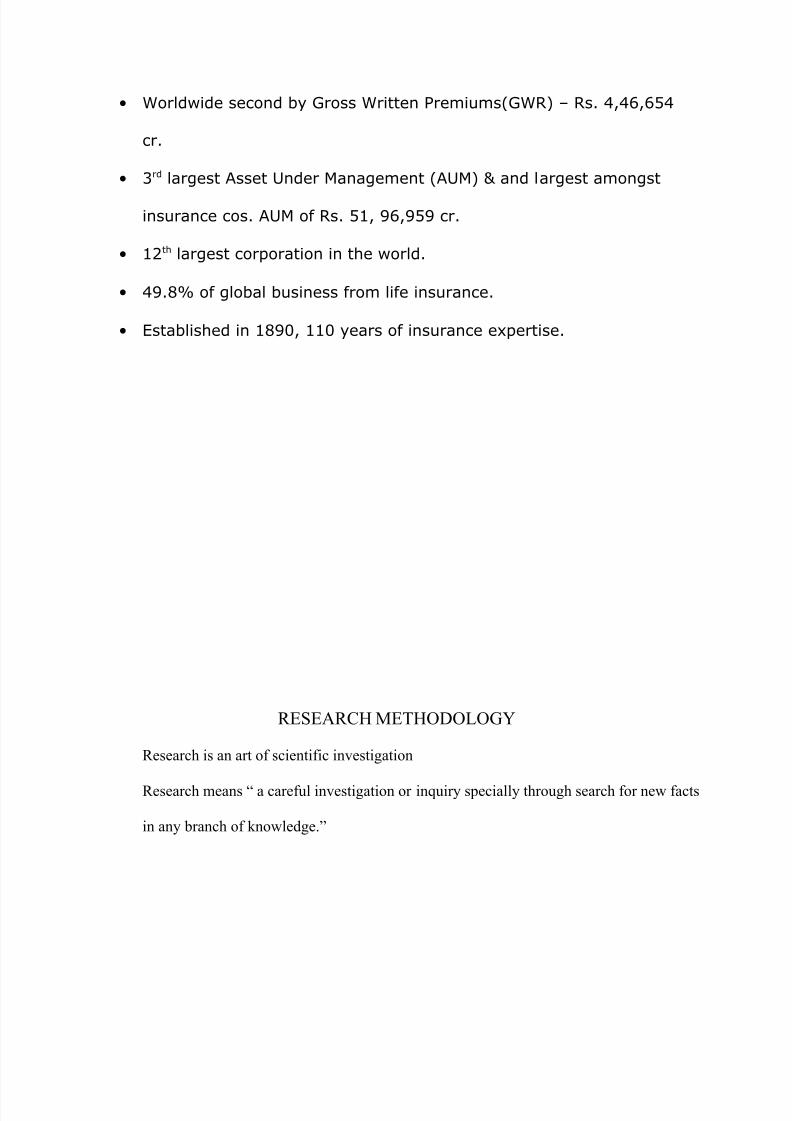

presented in the form of statistical tools such as pie charts and bar charts. There were 50

people being interviewed from different income groups and age groups.

1. Do you have a insurance policy? If yes then of which company or companies?

yes

no72%

28%

Bajaj Allianz

LIC

Max New York

ICICI Pru

TATA AIG

Birla SUN Life

Aviva

28%

32%

8%

17%

3%

6%

6%

Out of 50 insurable people interviewed, nearly 72% of people have taken insurance policy.

Out of this population being interviewed nearly 32% had LIC policy, 28% had Bajaj

Allianz policy, followed by ICICI pru. (17%), Max New York life (8%), TATA AIG (3%),

Birla Sun Life (6%), Aviva and HDFC having ^% shares each in the interviewed

population.

2. Do you see insurance policies as an investment alternative or a security option?

investment

alternative

securityoption

22%

78%

Out of 50 people interviewed, 78% people see insurance policies as a security option while

only 22% see it as an investment option.

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 41/52

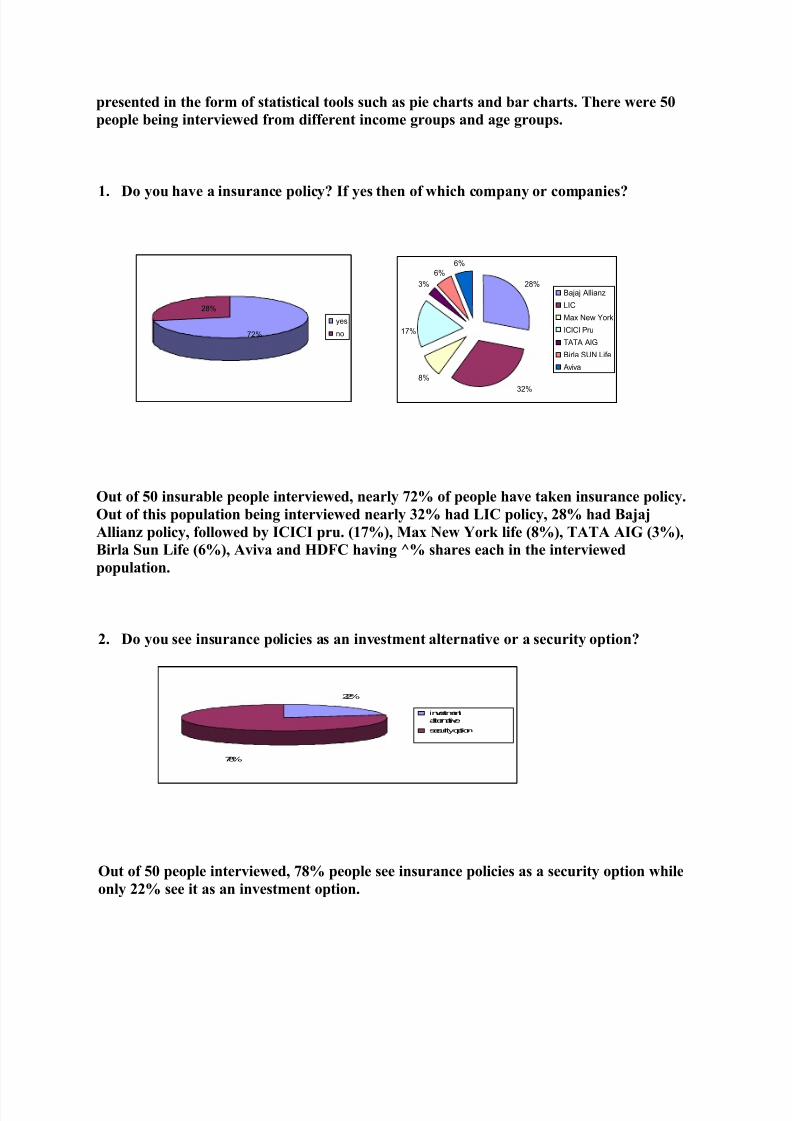

3. please rank the following as per your preference to investment in a financial year:

investment preferences in various alternatives are as follows:

0

2

4

6

8

10

12

14

16

18

shares mutual fund life

insurance

govt. bonds

Out of 50 people interviewed, 18 people invest in life insurance policies, 16 people invest in

shares, 12 people invest in mutual funds and 4 people invest in govt. bonds.

4. What is your criterion to select a particular insurance company and a scheme?

0

5

10

15

20

security time

span

market

share

return all of the

above

15

5

2

8

20

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 42/52

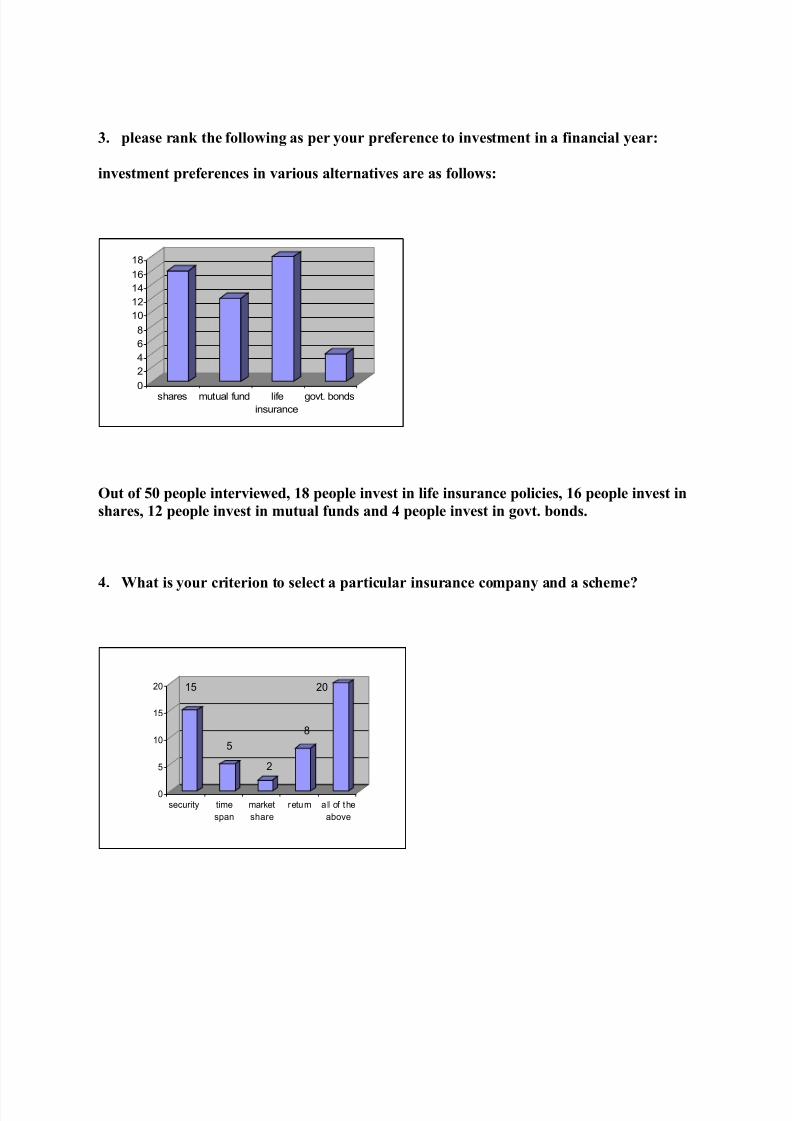

Out of 50 people interviewed, 15 people select an insurance company on the basis of

security, 5 people on time span basis, 12 people on the basis of market share, 8 people on

the basis of return and 20 people select an insurance on the basis of all the above

mentioned reasons.

5. Rank the life insurance companies on the basis of your order of preference:

BAJAJ Allianz

ICICI Pru

MAXNew York

HDFC

46%

24%

14%

16%

Out of 50 people interviewed, 46% had BAJAJ Allianz as their first preference for a pvt.

Life insurance Company followed by ICICI Prudential having 24% preference followed by

HDFC life insurance having16% market share and lastly Max New York Life Insurance.

6. Do you think that private life insurance companies are as safe as LIC for taking apolicy?

PERCEPTION ABOUT PRIVATE INSURANCE COMPANIES AGAINST LIC

yes

no

38%

62%

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 43/52

Out of 50 people interviewed, 62% of people do not find private life insurance companies to

be safe for buying a life insurance policy whereas 38% people find them safe for buying a

life insurance policy from a private life insurance company.

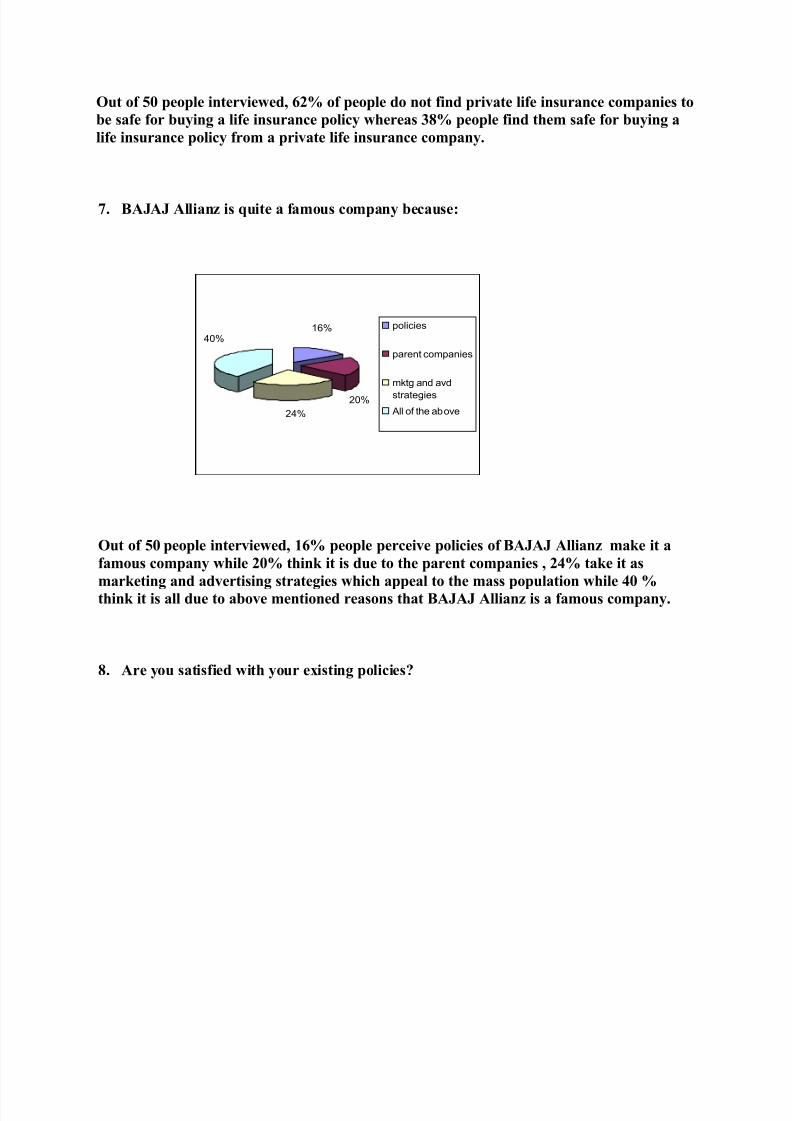

7. BAJAJ Allianz is quite a famous company because:

policies

parent companies

mktg and avd

strategies

All of the above

16%

20%

24%

40%

Out of 50 people interviewed, 16% people perceive policies of BAJAJ Allianz make it a

famous company while 20% think it is due to the parent companies , 24% take it as

marketing and advertising strategies which appeal to the mass population while 40 %

think it is all due to above mentioned reasons that BAJAJ Allianz is a famous company.

8. Are you satisfied with your existing policies?

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 44/52

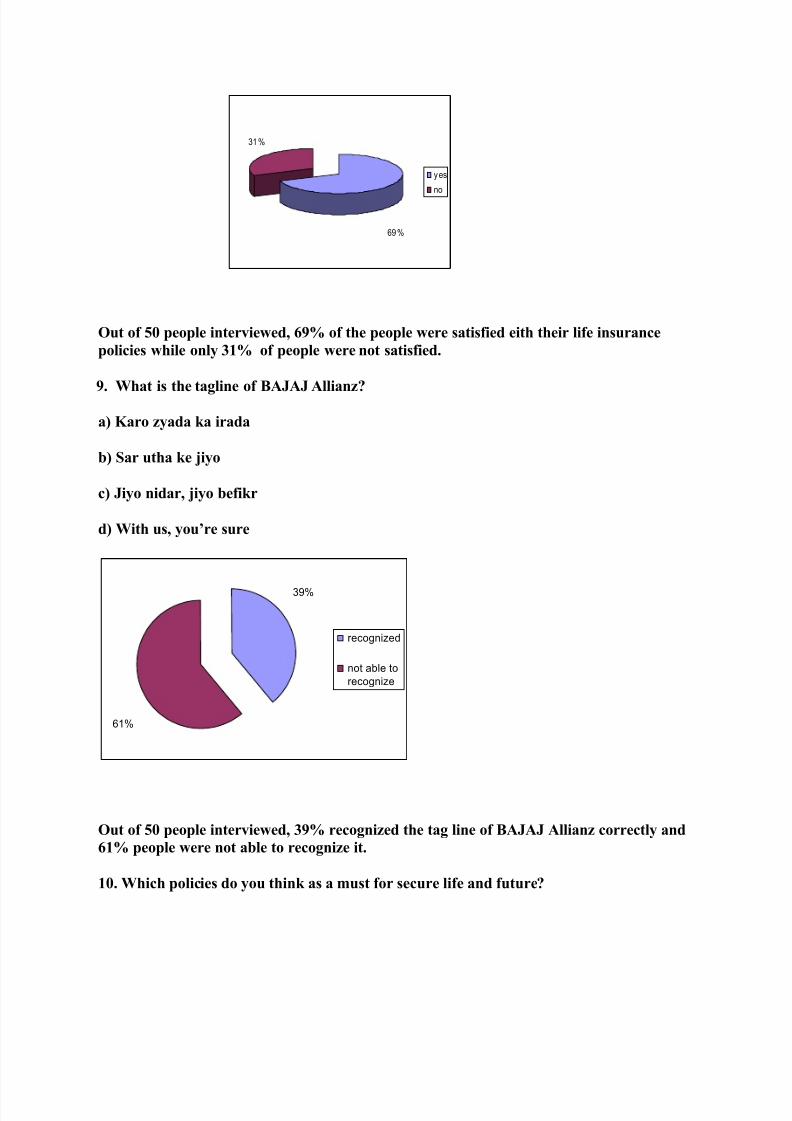

yes

no

69%

31%

Out of 50 people interviewed, 69% of the people were satisfied eith their life insurance

policies while only 31% of people were not satisfied.

9. What is the tagline of BAJAJ Allianz?

a) Karo zyada ka irada

b) Sar utha ke jiyo

c) Jiyo nidar, jiyo befikr

d) With us, you’re sure

recognized

not able to

recognize

39%

61%

Out of 50 people interviewed, 39% recognized the tag line of BAJAJ Allianz correctly and

61% people were not able to recognize it.

10. Which policies do you think as a must for secure life and future?

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 45/52

a) Life insurance

b) Health insurance

c) Home insurance

d) Children plans

e) Others

percentage of people

0

10

20

30

40

50

6070

l i f e i n

s u r a n c

e

h e a l t h

i n s u

r a n c

e

h o m e i n

s u r a n c

e

c h i l d

r e n p l a n

s

o t h e

r s

percentage of

people

LIMITATIONS

• Not filling up of certain questions in the questionnaire which led to the cancellation of particular questionnaire.

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 46/52

• Taking a sample of 50 people does not reflect the mindset of all kinds of people from

different backgrounds, different age groups and income groups.

• Again research study of two months is a time constraint and covering whole of alwar

population by taking a sample size of 50 is not feasible.

FUTURE GROWTH AND SUGGESTIONS

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 47/52

BAJAJ Allianz, in the present scenario is growing at an aggressive pace. The company does a lot

of survey & analysis in the market to discover customer’s needs & expectations & tries to

improvise on its existing market linked plans along with insurance policies. In addition to this,

the company from time to time keeps on introducing various new policies & tailor made plans

exclusively to cater people’s financial needs. This has enabled BAJAJ Allianz to become market

leader in the sector of insurance and investment companies since 2001 when it came into

existence.

Since many other companies are joining the field of insurance & investments but to remain one

of the leading companies, BAJAJ Allianz has to adopt new strategies earlier than others. This

could include widening the distribution networks to all parts of the country & catering to every

income group. Furthermore, it can improvise on its advertisements & promotion campaigns by

becoming more appealing and making them touch the hearts of millions & billions of middle

class families who are the hot prospects.

Lastly the students in the professional courses, apprentices, trainees may be good targets to

approach in times ahead.

FINDINGS AND CONCLUSIONS

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 48/52

The research project titled “AWARENESS OF INSURANCE AND MARKET

CREDIBILITY OF BAJAJ Allianz AMONG OTHER LIFE INSURANCE COMPANIES”

enabled to understand the competition among the various life insurance and general insurance

companies which have entered the Indian market of life insurance after 2000 when private life

insurance companies were allowed to enter the Life insurance sector in India. BAJAJ Allianz is

one of the companies in pvt. Sector which is doing exceptionally good in this sector due to their

policies which people find very attractive according to their needs. When people were

interviewed about the first preference among the private life insurance companies nearly 46%

replied for BAJAJ Allianz, this clearly indicates that BAJAJ Allianz is quite a household name.

The reasons for this are many like it is a company with very strong Brand names.

But if there are people accepting BAJAJ Allianz, there are people who are still hesitant to take up

private insurance company’s policy. This is due to the fact that LIC is a govt. organization. It can

be seen from the study that people have started recognizing BAJAJ Allianz as a life insurance

company and it will grow at a much faster pace in the future.

REFERENCES

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 49/52

To obtain more information regarding the present study and to substantiate it with theoretical

proof, following references were made:

List of Books and other supplementary material referred:

Textbook on Marketing Management, ICMR publication, Hyderabad.

Textbook on Marketing Management by PHILIP KOTLER:11th edition.

Websites visited:

www.Bajaj Allianz.com

www.lifeinsurance.com

www.Bajaj Allianzlifeinsurance.com

www.irdaindia.org

www.lic.gov.in

www.hdfc.com

www.icici.com

QUESTIONNAIRE

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 50/52

NAME - _____________________

AGE - _____________________

OCCUPATION - _____________________

1. Do you have a insurance policy? If yes then of which company or companies?

• YES - _____________________________________

• NO

2. Do you see insurance policies as an investment alternative or a security option?

• Investment alternative

• Security option

3. please rank the following as per your preference to investment in a financial year:

• Shares

• Mutual funds

• Life insurance

• Govt. bonds

4. What is your criterion to select a particular insurance company and a scheme?

• Security

• Time span

• Market share

•

Return

• All of the above

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 51/52

5. Do you think that private life insurance companies are as safe as LIC for taking a

policy?

• YES

• NO

6. Rank the life insurance companies on the basis of your order of preference:

• BAJAJ Allianz

• ICICIPru

• Max New York Life

• HDFC

7. BAJAJ Allianz is quite a famous company because:

• Policies

• Parent companies

• Marketing and Advertising strategies

• All of the above

8. Are you satisfied with your existing policies?

• YES

• NO

9. What is the tagline of BAJAJ Allianz?

• Karo zyada ka irada

• Sar utha ke jiyo

• Jiyo nidar, jiyo befikr

8/9/2019 Final Report 2003

http://slidepdf.com/reader/full/final-report-2003 52/52

• With us, you’re sure

10.Which policies do you think as a must for secure life and future?

• Life insurance

• Health insurance

• Children plans

• Home insurance

• Other insurance