Final Project Report The impact of premiumisation on ... Premiumisation of drinks... · This report...

105

Final Project Report The impact of premiumisation on drinks packaging This report looks at the trend towards ‘premiumisation’ in the UK drinks market. It explores the meaning of ‘premium’, attempts to estimate the extent to which it is happening and looks at the implications for household waste and packaging. It also examines what activity there is in the sector, what barriers there are to greater resource efficiency and finally how to overcome these barriers and design premium, environmentally sustainable drinks packaging. Project code: RPO020 ISBN: 1-84405-426-8 Research date: 19 Sep 2008 to 22 Feb 2009 Date: September 2009

-

Upload

nguyenliem -

Category

Documents

-

view

213 -

download

0

Transcript of Final Project Report The impact of premiumisation on ... Premiumisation of drinks... · This report...

Final Project Report

The impact of premiumisation on drinks packaging

This report looks at the trend towards ‘premiumisation’ in the UK drinks market. It explores the meaning of ‘premium’, attempts to estimate the extent to which it is happening and looks at the implications for household waste and packaging. It also examines what activity there is in the sector, what barriers there are to greater resource efficiency and finally how to overcome these barriers and design premium, environmentally sustainable drinks packaging.

Project code: RPO020 ISBN: 1-84405-426-8 Research date: 19 Sep 2008 to 22 Feb 2009 Date: September 2009

WRAP helps individuals, businesses and local authorities to reduce waste and recycle more, making better use of resources and helping to tackle climate change.

Written by: Sprout Design Ltd. and Eco3 Ltd. www.sproutdesign.co.uk & www.eco3.co.uk

Front cover photography: SIP is a functional water aimed at women, which communicates its premium status through simple, elegant design rather than through excessive use of materials. Any trade marks, copyright material and or intellectual property that is reproduced in the images of packaging shown in this report are not the property of WRAP and WRAP acknowledges the proprietors' rights in such intellectual property. WRAP, Sprout Design and Eco 3 believe the content of this report to be correct at the date of writing. However, factors such as prices, levels of recycled content and regulatory requirements are subject to change and users of the report should check with their suppliers to confirm the current situation. In addition, care should be taken in using any of the cost information provided as it is based upon numerous project-specific assumptions (such as scale, location, tender context, etc.). The report does not claim to be exhaustive, nor does it claim to cover all relevant products and specifications available on the market. While steps have been taken to ensure accuracy, WRAP, Sprout Design and Eco3 cannot accept responsibility or be held liable to any person for any loss or damage arising out of or in connection with this information being inaccurate, incomplete or misleading. It is the responsibility of the potential user of a material or product to consult with the supplier or manufacturer and ascertain whether a particular product will satisfy their specific requirements. The listing or featuring of a particular product or company does not constitute an endorsement by WRAP and WRAP cannot guarantee the performance of individual products or materials. This material is copyrighted. It may be reproduced free of charge subject to the material being accurate and not used in a misleading context. The source of the material must be identified and the copyright status acknowledged. This material must not be used to endorse or used to suggest WRAP’s endorsement of a commercial product or service. For more detail, please refer to WRAP’s Terms & Conditions on its web site: www.wrap.org.uk

The impact of premiumisation on drinks packaging 3

Executive summary This report is presented as the final deliverable of this project, looking at the impact and implications of ‘premiumisation’ on drinks packaging. The project has been conducted, for WRAP (Waste & Resources Action Programme), by packaging and product design consultancy Sprout Design Ltd. in collaboration with environmental consultancy Eco3. Project objectives 1. To better understand the implications of premiumisation on efforts to promote resource efficient packaging in the UK’s drinks sector - focusing specifically on wine, spirits, beer (including ale and lager), cider, ready-to-drink, soft drinks and water. 2. To make recommendations to WRAP and the drinks sector to overcome barriers and encourage the optimisation of premium drinks packaging. The project was researched through interviews with 20 key sector representatives, through magazine and internet article searches, by carrying out environmental assessments of sample packs, from five retailer walkthroughs and from relevant marketing reports. References are given on page 77. The project and this report are split into distinct phases, with the findings summarised below: Market research Large brand owners generally dominate drinks production and packaging. Within the UK alcohol sector, these include: Diageo, Pernod Ricard, Constellation Europe, Bacardi-Martini, Coors Brewers, ABInbev, Heineken and Carlsberg UK. Within soft drinks; Britvic, Coca-Cola, Danone Waters, GlaxoSmithKline UK, Innocent, Nestlé and PepsiCo. UK are key players. Within packaging, Rexam, Crown and Ball dominate in metal, O-I, Quinn Glass, Ardagh Glass, Allied Glass and Beatson Clark in glass and Artenius, Linpac and Rexam in plastic. Whilst many of these are large multi-nationals, independent companies such as Innocent have shown the influence that they can have on the market and also on packaging. The UK Drinks sector (both on and off-tradeA ) is worth approximately £54.6bn with total volume sales of 19.4bn litres.35 & 5 Alcohol makes up 77% of this by value (£42bn) but only 39% by volume (7.5bn litres)5. By volume, carbonates are one third of the entire drinks market and after that, lager and fruit drinks & juices are second and third largest respectively. Definitions and themes The section ‘Definitions and Themes’ examines definitions of ‘premium’ and ‘premiumisation’. There is no clear consensus on a definition of either, but the term ‘premium’ clearly relates to actual or perceived product quality and also to price. ‘Premiumisation’ of a sub-category generally refers to an increased demand for and proportion of premium products, but it can also describe the trading up of consumers from lower to higher price points. There are many strategies for positioning drinks as ‘premium’ and these have been distilled into eight key themes: 'Designer', 'Quality', 'Luxury', 'Responsible', 'Health', 'Exotic', 'Functional' and 'Functional Packaging'. These themes have been mapped against sub-categories for relevance. The market is commonly split into five price tiers: Value / Budget, Core / Mainstream, Premium, Super Premium and Ultra Premium. The price points defining these tiers are particular to whichever organisation is using the system. On top of this, it has recently been seen that Tesco has launched a ‘super-budget’ line, undercutting their own economy range. At the other end of the spectrum, there is also ‘luxury’. ‘Luxury’ products exist outside the ranges commonly stocked by supermarkets and are unattainable by the masses.

A Definitions:

“On-trade” – refers to any licensed establishment that allows the sale and consumption of alcohol to occur on the premises. Drinks are usually served in a ready-to-drink fashion and cannot be taken off the premises for consumption later. It is acknowledged that some on-trade establishments also offer off-trade sales, with these sales considered separately from on-trade sales.5

“Off-trade” – refers to any licensed establishment that legally sells alcohol for off-premise consumption 5 for example, retailers and off-licences.

‘Premium’ was not found to relate directly to particular customer profiles and retailers especially commented that their ‘good’, ‘better’ and ‘best’ own-label ranges are designed to allow consumers to trade up or down easily within their normal shop. Retailer own-label ranges are increasingly defining what ‘premium’ means on the supermarket shelves and brands are starting to position their launches in relation to them. Implications of the premium trend Premiumisation is evident in all categories including those outside of the drinks sector and seems to be surviving in the current economic climate. However, within the drinks sector, it is most clearly evident in spirits and liqueurs, fruit drinks and juices and in bottled water. It became clear, through interviews with the drinks sector, that ‘premium’, as a tier, is moving down the cost-curve with more every-day products becoming ‘premium’ during the recession. In order to better understand the level of premiumisation within each drinks sector, an attempt was made to estimate and identify the proportion within each drinks sub-category and then to calculate the packaging produced as a result of the ‘premium’ portion of the market. Due to there not being a universally recognised definition of what is or what is not ‘premium’, these figures are estimates only, but are still a useful way of examining the implications of premiumisation. Ales and stouts, functional drinks and alcoholic ready to drinks (RTD’s) have the highest proportion of premium products. Example products from premium and core areas of each sub-category were bought and their packaging weighed. The results showed that the packaging for premium drinks tended to be heavier than their core counterparts, even when packaged in the same material and format. Where premium products are sold in a different packaging material or format than the core equivalent, for example a bottle rather than a can, the difference in weight was more pronounced. However, care should be taken about solely measuring weight. There are many other factors which should be considered when determining not only the environmental impact of a pack but also its overall sustainability, which are discussed in Section 9 ‘Assessing the environmental impacts of premium drinks packaging’. Drivers behind premiumisation Interviewees representing retailers, producers, design agencies and industry bodies were asked about the drivers behind premiumisation. There were widely varying opinions about drivers. Design agencies and producers typically saw the producers driving premiumisation but retailers saw consumers driving it. One respondent thought that consumers, retailers and producers are all driving it, which may well best explain the actual situation. ‘Premium’ products do not only respond to increasing affluence and consumer expectations but also to consumers’ desire to ‘trade up’ at occasions for example, weekends. Identification of barriers Interviewees were also questioned about what barriers to the adoption of resource-efficient premium design the sector faces. These were grouped into technical, knowledge-based and economic barriers. Only one interview respondent saw a tension between premiumisation and resource efficiency within drinks packaging design. The majority did not see a tension, believing that clever design could achieve both things simultaneously, and that in the future, the “product would be the hero” and would not rely so heavily on packaging. In general, there was a high level of awareness of eco-design methods amongst interviewees, but some examples of a lack of knowledge about the comparative environmental performance of different materials and formats. Developing new structural packaging is generally limited to larger (drinks and packaging) producers, with retailers and smaller producers typically sourcing existing solutions, such as stock components. Resource efficiency innovations tended to be targeted at budget and core products rather than premium, due to the larger opportunities for waste reduction. One option for optimisation is lightweighting, but there is a limit as to how far lightweighting can go, as packs need to survive the supply chain intact, protect the product and maintain brand equity. In addition there was also some concern that consumers may think they are getting less from a pack that looks smaller, although not all lightweighted products are smaller or look smaller. Sector activity Within the drinks sector, interviewees agreed that premiumisation is a combination of delivering a premium product and a packaging solution that communicates that it is ‘premium’, both on shelf and at home. It is a commonly held view that glass conveys ‘premium’. Brands tended to think that heavier bottles do more to convey ‘premium’ and designers interviewed also felt that customers held this view. There may be an expectation for the use of glass in some sectors like whisky, which has a long tradition of bottling in glass. There is an increasing amount of lightweighting activity going on, primarily in glass but also in PET and aluminium. Supermarkets have recently started moving some own-brand spirits into PET. Some interviewees commented that this activity has

The impact of premiumisation on drinks packaging 4

been going on for decades but has only recently been linked to sustainability. There have also been moves to bottle, for example, wine in the UK rather than in the country of origin. This saves the distributor transport costs and allows products to be bottled in the UK in green glass bottles containing a high level of recycled content. Assessing the impact of premium drinks packaging A variety of premium drinks packaging samples were purchased, weighed and analysed using Eco3’s packaging assessment tool, to assess the potential environmental impacts associated with premium drinks packaging, and identify opportunities for change. The environmental elements investigated were; recycled content, recyclability, product/pack ratio, and volumetric efficiency. Packaging Benchmark Data analysis highlights that significant opportunities exist for packaging weight reduction through minimisation, with further reductions in environmental impact being achieved by increasing recycled content. Design guidelines and good practice This section of the report explores premium drinks packaging by pack format or type and gives guidance on how to design premium drinks packaging with less environmental impact. Topics cover; the waste hierarchy, recyclability, recycled content, changing pack format, lightweighting, reuse, gifting and graphic treatments. Case studies are put forward in each section with images of packaging solutions which demonstrate the various opportunities discussed. In conclusion, through informed design it is possible to overcome the majority of the barriers identified by this project and produce premium drinks packaging without compromising environmental performance, consumer acceptance, brand equity or functional performance. Conclusions Premiumisation is a clear current trend in the drinks sector and its impact on packaging waste is significant as premium drinks frequently use more packaging than their core equivalents. This trend could threaten the drive towards resource efficiency and packaging waste reduction being led by government, retailer and brand targets to reduce absolute packaging, such as the Courtauld Commitment. Although there is a high level of awareness of the need to address both premiumisation and resource efficiency at the same time, and there are examples of products which do, there is still a relatively small proportion of the sector as a whole which actual deliver both. However, good packaging technology can be used to help achieve both goals simultaneously: Technical barriers such as UV resistance and physical pack strength are being overcome through modern manufacturing, analysis and inspection techniques. Economic barriers such as the capital investment required to produce a lightweight mould can be overcome, for example, by waiting until a mould tool needs replacing and using this as an opportunity to replace it with a redesigned, lightweighted mould. Consumers have been shown to accept lightweighted bottles, and resource efficient packaging and lightweight packaging can resemble (if necessary) its predecessor. Good design, in terms of form, function and communication has the ability to ensure that packaging with reduced environmental impact can still communicate the ‘premium’ message and there are examples of where this has been achieved illustrated in Section 10, ‘Premium drinks design guidelines and case studies’.

The impact of premiumisation on drinks packaging 5

Contents 1.0 Introduction ........................................................................................................................... 10

1.1 Background.........................................................................................................................10 1.2 Objectives...........................................................................................................................10 1.3 Methodology .......................................................................................................................10

2.0 Market research ..................................................................................................................... 11 2.1 Overall UK drinks market .....................................................................................................11

2.1.1 Alcoholic drinks.......................................................................................................11 2.1.2 Soft drinks..............................................................................................................11 2.1.3 Comparison of drinks sub-sectors, by volume ...........................................................12 2.1.4 Estimating the size of the premium drinks market.....................................................13 2.1.5 Key players.............................................................................................................16 2.1.6 Key trends affecting the drinks sector ......................................................................16

2.2 Premium drinks sub-category overview.................................................................................17 2.2.1 Categorisation of the premium drinks sector .............................................................17 2.2.2 Premium still wine, sparkling wine and Champagne...................................................17 2.2.3 Premium lager, ales, stouts and cider.......................................................................17 2.2.4 Spirits and liqueurs .................................................................................................18 2.2.5 Premium alcoholic mixables and ready-to-drinks (RTD’s) ...........................................18 2.2.6 Premium carbonates ...............................................................................................18 2.2.7 Premium fruit juice, juice drinks, squashes, cordials and smoothies............................19 2.2.8 Premium bottled water............................................................................................19 2.2.9 Premium functional drinks (excluding water) ............................................................19

3.0 Definitions and themes .......................................................................................................... 20 3.1 Existing definitions of ‘premium’ ...........................................................................................20 3.2 Definitions of ‘premium’: Findings from interviews .................................................................21 3.3 Tiers of premium.................................................................................................................24 3.4 Premium themes .................................................................................................................25

3.4.1 ‘Designer premium’ .................................................................................................26 3.4.2 ‘Quality premium’....................................................................................................27 3.4.3 ‘Luxury’ ..................................................................................................................28 3.4.4 ‘Responsible premium’.............................................................................................29 3.4.5 ‘Health premium’ ....................................................................................................30 3.4.6 ‘Exotic premium’ .....................................................................................................31 3.4.7 ‘Functional premium’ ...............................................................................................32 3.4.8 ‘Premium functional packaging’................................................................................33

3.5 Premiumisation strategies by sub-category............................................................................34 4.0 Evidence of the premiumisation trend ................................................................................... 35

4.1 Premiumisation trends outside of the drinks sector ................................................................35 4.2 Evidence of premiumisation within the drinks sector ..............................................................37 4.3 Premiumisation and new product development claims in the alcoholic drinks sector.................38 4.4 Conclusions.........................................................................................................................39

5.0 Drivers for premiumisation: Findings from interviews .......................................................... 40 6.0 The implications of premiumisation on packaging weight .................................................... 42 7.0 Barriers to the adoption of resource efficient packaging for premium drinks....................... 43

7.1 Interview responses ............................................................................................................43 7.2 Summary of factors cited as barriers to the adoption of resource-efficient premium packaging.44

7.2.1 Technical barriers ...................................................................................................44 7.2.2 Economic barriers ...................................................................................................44 7.2.3 Knowledge barriers .................................................................................................44

8.0 Premium packaging and the environment ............................................................................. 45 8.1 Packaging ...........................................................................................................................45 8.2 Environment .......................................................................................................................46

9.0 Assessing the environmental impacts of premium drinks packaging .................................... 47 9.1 Methodology .......................................................................................................................47 9.2 Lager, ales and cider ...........................................................................................................47 9.3 Bottled Water......................................................................................................................48

The impact of premiumisation on drinks packaging 6

9.4 Soft Drinks ..........................................................................................................................48 9.5 Wine...................................................................................................................................49 9.6 Spirits and Liqueurs .............................................................................................................49 9.7 Summary ............................................................................................................................50

10.0 Premium drinks design guidelines and case studies.............................................................. 51 10.1 Introduction ........................................................................................................................51 10.2 Disclaimer ...........................................................................................................................51 10.3 General packaging guidance.................................................................................................52

10.3.1 The waste hierarchy................................................................................................52 10.3.2 Overview of premium drinks packaging formats........................................................53

10.4 Glass packaging ..................................................................................................................54 Design guidelines....................................................................................................54 10.4.1 54 Lightweighting ........................................................................................................54 10.4.2 54 Strength of lightweighted glass bottles: ................................................................................54 Lightweighting and consumer perceptions:............................................................................54 UV and lightweighted glass bottles: ......................................................................................55 Lightweighting glass case studies: ........................................................................................55 Kingsland Wines & Spirits: Wine bottles ...............................................................................56 10.4.3 Use of recycled content ...........................................................................................56

10.5 Plastic packaging.................................................................................................................57 10.5.1 Examples of plastic packaging used in the premium drinks sector ..............................57 10.5.2 Design guidelines....................................................................................................57 Lightweighting and optimised packaging case studies: ..............................................58 10.5.3 58 SIP water............................................................................................................................58 Coca-Cola ...........................................................................................................................58 Highland Spring...................................................................................................................59 10.5.4 Use of recycled content case studies:.......................................................................59 Sainsbury’s ‘Taste the Difference’ orange juice ......................................................................59

10.6 Metal packaging ..................................................................................................................60 Examples of metals used in premium drinks sector ...................................................60 10.6.1 60 Volute ‘premium portable wine’ ............................................................................................60 10.6.2 Design guidelines....................................................................................................60 10.6.3 Lightweighting case study: ......................................................................................61 Coca-Cola Enterprises ..........................................................................................................61 10.6.4 Recycled content ....................................................................................................61 Recycled content case study: Volute ‘premium portable wine’ ................................................61

10.7 Flexibles and bag-in-box ......................................................................................................62 Examples of flexibles and bag-in-boxes used in the premium drinks sector .................62 10.7.1 62 10.7.2 Design guidelines....................................................................................................63 10.7.3 Recycled content case study....................................................................................63

10.8 Liquid carton packaging .......................................................................................................64 10.8.1 Examples of liquid carton packaging used in the premium drinks sector .....................64 10.8.2 Design guidelines....................................................................................................64

10.9 Gift packaging .....................................................................................................................65 10.9.1 Design guidelines....................................................................................................65

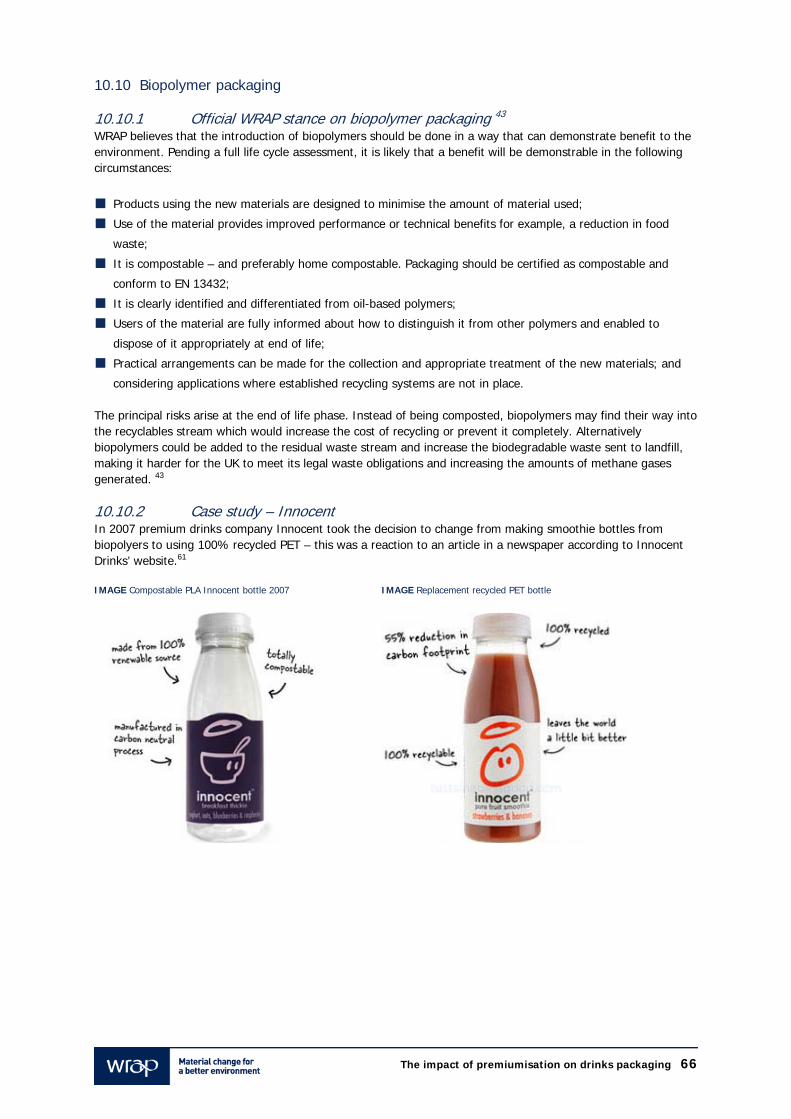

10.10 Biopolymer packaging..........................................................................................................66 10.10.1 Official WRAP stance on biopolymer packaging 43......................................................66 Case study – Innocent ............................................................................................66 10.10.2 66

10.11 Reusable packaging.............................................................................................................67 10.11.1 Guidelines – reusable packaging ..............................................................................67 10.11.2 Reusable packaging case studies .............................................................................67

11.0 Conclusion.............................................................................................................................. 68 References ......................................................................................................................................... 72 Appendix 1: Wine, sparkling wine and Champagne........................................................................... 74

The impact of premiumisation on drinks packaging 7

1.0 Market survey ........................................................................................................................ 74 1.1 Still wine .............................................................................................................................74

1.1.1 Store walkthrough findings ......................................................................................75 1.2 Champagne.........................................................................................................................75

1.2.1 Store walk-through results.......................................................................................75 1.3 Sparkling wine.....................................................................................................................76

2.0 Definitions and themes (wine)............................................................................................... 77 3.0 Implications of the trend (wine)............................................................................................ 78 4.0 Market drivers ........................................................................................................................ 78 5.0 Wine sector response to demand for more ‘premium’ packaging.......................................... 79 Appendix 2: Lager, ale, stout and cider.............................................................................................. 80 1.0 Market survey ........................................................................................................................ 80

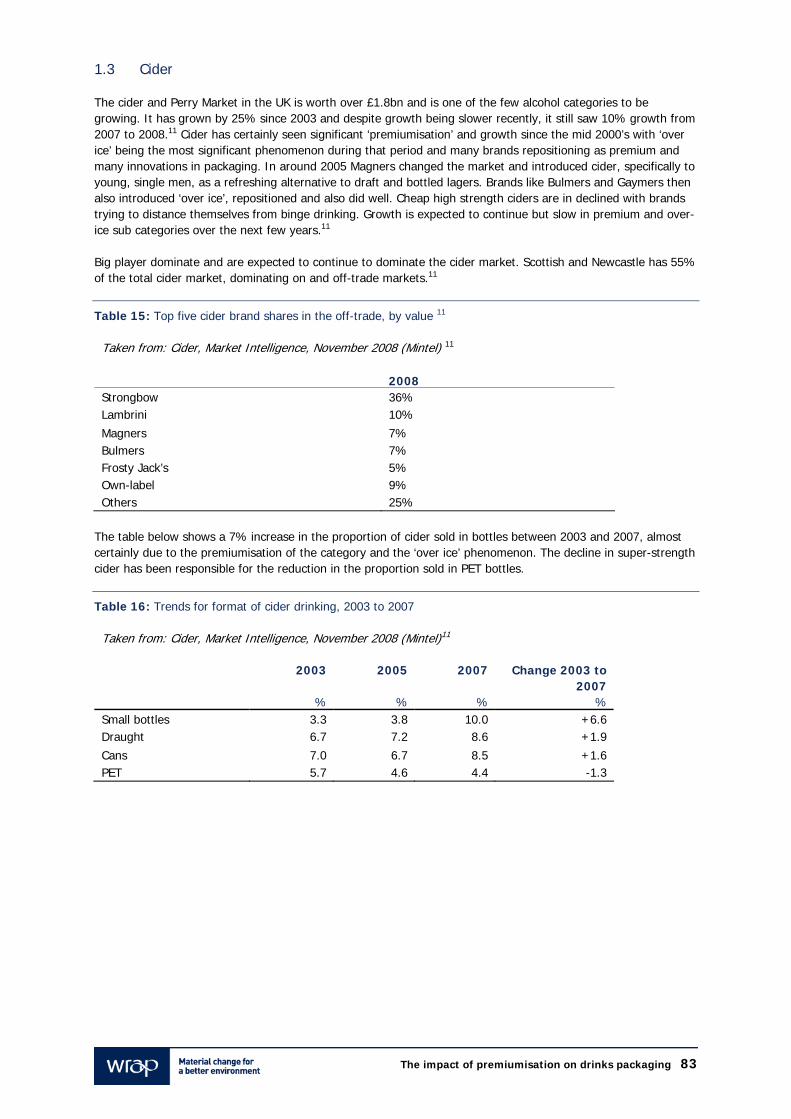

1.1 Lager..................................................................................................................................80 1.2 Ales and stouts....................................................................................................................81 1.3 Cider ..................................................................................................................................83 1.4 Non-alcoholic and low-alcohol drinks ....................................................................................84

2.0 Definitions and themes .......................................................................................................... 84 3.0 Implications of the trend ....................................................................................................... 84 4.0 Identification of barriers........................................................................................................ 85 5.0 Sector activity ........................................................................................................................ 85 Appendix 3: Spirits & liqueurs............................................................................................................ 86 1.0 Market survey ........................................................................................................................ 86

1.1 Vodka .................................................................................................................................87 1.2 Gin .....................................................................................................................................88 1.3 Whisky................................................................................................................................89 1.4 Rum ...................................................................................................................................89 1.5 Brandy................................................................................................................................89 1.6 Liqueurs..............................................................................................................................89

2.0 Definitions and themes .......................................................................................................... 90 3.0 Implications of the trend ....................................................................................................... 91 4.0 Identification of barriers........................................................................................................ 91 5.0 Sector activity ........................................................................................................................ 92 Appendix 4: Alcoholic mixables and RTD’s ........................................................................................ 93 1.0 Market survey ........................................................................................................................ 93

1.1 Alcoholic mixables ...............................................................................................................93 1.2 RTD alcoholic drinks ............................................................................................................93

2.0 Definitions and themes .......................................................................................................... 94 3.0 Implications of the trend ....................................................................................................... 94 4.0 Sector activity ........................................................................................................................ 94 Appendix 5: Bottled water ................................................................................................................. 95 1.0 Market survey ........................................................................................................................ 95 2.0 Implications of the trend ....................................................................................................... 96 3.0 Sector activity ........................................................................................................................ 97 Appendix 6: Carbonates ..................................................................................................................... 98 1.0 Market survey ........................................................................................................................ 98 2.0 Definitions and themes .......................................................................................................... 98 3.0 Implications of the trend ....................................................................................................... 98 Appendix 7: Functional drinks............................................................................................................ 99 1.0 Market survey ........................................................................................................................ 99

1.1 Sports and energy drinks .....................................................................................................99 1.2 RTD tea and coffee..............................................................................................................99

Appendix 8: Fruit juice, juice drinks, squashes, cordials and smoothies ......................................... 100 1.0 Market survey ...................................................................................................................... 100

1.1 Squashes and cordials ....................................................................................................... 100 1.2 Fruit juice and fruit drinks .................................................................................................. 101 1.3 Smoothies......................................................................................................................... 101

2.0 Definitions and themes ........................................................................................................ 102 3.0 Packaging............................................................................................................................. 102 4.0 Sector activity ...................................................................................................................... 102 Appendix 9: Premiumisation in specific non-drinks sectors ............................................................ 103

The impact of premiumisation on drinks packaging 8

The impact of premiumisation on drinks packaging 9

Figures Figure 1: Comparison of sub-sector sizes by volume, 2008, (estimated). ........................................................12 Figure 2: Proportions of each sub-category estimated to be ‘premium’ ...........................................................15 Figure 3: Drink sub-categories, their groupings and references to the appendices...........................................17 Figure 4: Price tiers.....................................................................................................................................24 Figure 5: U.S. spirits and wine price tiers......................................................................................................25 Figure 6: Relation between premiumisation strategy and sub-category...........................................................34 Figure 7: Claims accompanying new alcoholic drinks product launches 2005 to 2007 ......................................38 Figure 8: WRAP-approved waste hierarchy ...................................................................................................52 Figure 9: Pack types currently available to consumers, by drinks sub-category................................................53 Tables Table 1: UK sales of alcoholic drinks by volume.............................................................................................11 Table 2: Estimate of proportion of alcohol market which is ‘premium’, by sub-category, by volume ..................13 Table 2 (continued):....................................................................................................................................14 Table 3: list of interviewees for this project...................................................................................................21 Table 4: Barriers and opportunities for resource-efficient premium drinks packaging design.............................69 Table 6: Top ten UK off-trade wine brands, 2006 ..........................................................................................74 Table 7: Top ten uk off-trade wine brands, 2008...........................................................................................75 Table 8: Champagne, by brand ....................................................................................................................76 Table 9: Champagne, by style ......................................................................................................................76 Table 10: Sparkling wines............................................................................................................................77 Table 11: UK retail sales of lager, by type of packaging, by volume................................................................80 Table 12: Top lager brands..........................................................................................................................80 Table 13: Ales and stouts brand share (on-trade) .........................................................................................82 Table 14: Ales and stouts brand share (off-trade) .........................................................................................82 Table 15: Top five cider brand shares in the off-trade, by value 11 .................................................................83 Table 16: Trends for format of cider drinking, 2003 to 2007 ..........................................................................83 Table 17: Low alcohol and alcohol free drinks ...............................................................................................84 Table 18: Top ten spirits & liqueurs 2008 .....................................................................................................86 Table 19: New product launches in the UK spirits and liqueurs market by claim, Jan 2007 to April 2008 ...........86 Table 20: Top ten gin brands 2008 ..............................................................................................................88 Table 21: Volumes comparison of whisky sub-categories ...............................................................................89 Table 22: Liqueurs sub-sectors ....................................................................................................................90 Table 23: Alcoholic mixables ........................................................................................................................93 Table 24: RTD alcoholic drinks: top brands ...................................................................................................94 Table 25: Bottled water ...............................................................................................................................96 Table 26: Bottled water volumes, by packaging type, 2006............................................................................96 Table 27: Bottled water volumes, by water type, 2006 ..................................................................................96 Table 28: UK Carbonates brand share, by volume, 2005-2006 (%) ................................................................98 Table 29: Health sports and energy drinks (functional drinks) ........................................................................99 Table 30: RTD tea & coffee .........................................................................................................................99 Table 31: Squashes and cordials ................................................................................................................ 100 Table 32: Fruit juice and juice drinks.......................................................................................................... 101

1.0 Introduction 1.1 Background Premiumisation is the current retail trend (even within the current economic climate), and a key theme in today’s retailer market. Retailers and brands are increasingly seeking to take advantage of this trend. But what implications could this trend have on packaging, in particular on activities to reduce, optimise or make drinks packaging more resource efficient? 1.2 Objectives This project has been conducted for WRAP, by eco-packaging and product design consultancy Sprout Design Ltd. in collaboration with environmental consultancy Eco3. The objectives were: 1 To better understand the implications of premiumisation on efforts to promote resource efficient packaging in

the UK’s drinks sector - focusing specifically on wine, spirits, beer (including ale and lager), cider, ready-to-drinks (RTD’s), soft drinks and water.

2 To make recommendations to WRAP and the drinks sector to overcome barriers to the optimisation of premiumised drinks packaging.

1.3 Methodology A number of methods have been used to research this project: Marketing research: Various publications were reviewed, such as those produced by Mintel and Verdict and

used to identify market share and trend data. Unfortunately, some of the data identified was up to three years old but the most recent data available has been used and identified in all cases.

Store walkthroughs: Retailer walkthroughs were carried out in order to get a feel for the sorts of premium drinks packaging formats on the market, and the approaches taken by retailers and brands to ‘premiumise’ drinks. A number of case study packs were also identified and their environmental impacts assessed (see Section 9, ‘Assessing the environmental impacts of drinks packaging’).

Media searches: Searches were conducted in trade press for articles on premiumisation and sectoral market reviews.

Interviews: Interviews were conducted with 20 key representatives from UK retailers, brands, packaging and design companies. Interviewees ranged from for example, PR, packaging technology, store design, design to brand managers, and also covered a range of drinks sub-categories’.

Sample pack assessments: A range of sample products were purchased and analysed using eco3’s packaging assessment tool to assess and estimate the environmental impact, and potential for reduction, of within the premium drinks sector.

The impact of premiumisation on drinks packaging 10

2.0 Market research This section of the report looks at the size of the UK drinks market and identifies the key players and general trends, with particular reference to premium products. More detailed information is given for each sub-category in the Appendices. 2.1 Overall UK drinks market 2.1.1 Alcoholic drinks The UK alcoholic drinks market has a value of £42bn and volume sales of 7.5bn litres.5 This includes both the on-trade and the off-trade markets, with the off-trade being responsible for just over half of sales by volume. Table 1 shows the breakdown of volume sales during 2008 by sub-category and the change in sales from 2003 to 2008. The market as a whole has been declining since 2002 and is predicted to continue to decline over the next five years as consumers adopt healthier lifestyles.5 The alcohol retail sector underwent the biggest decline in sales of any retail sector in the UK in the 2000-2008 period, dropping 30% to £3,504m7. According to Mintel’s market intelligence report ‘Alcoholic Drink Packaging and Labelling’ (Feb 2008)8, the “‘Premiumisation’ trend is driving the packaging innovation in the alcoholic drinks market, led by the spirits category over the last few years, with demand high for products highlighting provenance as well as natural and authentic ingredients.”

Table 1: UK sales of alcoholic drinks by volume Source: Off Vs. On Trade Drinking, Mintel, Sept 2008 5

Total volume

2008 Share of alcoholic

drinks market 2008

Proportion which is off-

trade 2008

% Change 2003-08

Million litres % % by volume % by volume Beer 4,987 66% 42.3% -13.3% Cider 642 8.5% 49.4% 26.4% Wine 1,262 16.7% 83.4% 14.9% Spirits & Liqueurs 507 6.7% 71.6% -9.2% Alcoholic RTD’s* 159 2.1% 47.8% -42.8% Total 7,557 100% -7.8% * RTD’s – ready to drinks 2.1.2 Soft drinks Mintel’s report ‘On-Trade Soft Drinks’ (September 2007) estimates the UK soft drinks markets at £12.6bn35 by value and 11.90bn litres by volume, making it approximately 59% larger than the alcohol market by volume. Of this total, the UK off-trade soft drinks market is worth £3.4 billion, with value sales having increased by 9% in on 2006, while volume sales grew by l.5% (TNS Worldpanel 52 w/e 28 January 2007). The hard discounters, such as Lidl, Netto and Aldi, are the fastest-growing retailers of soft drinks, with sales up 21% on last year 9 and we can expect this trend to continue in the current economic downturn. Consumer demand for healthy drinks is reflected in the performance of soft drinks sectors which are perceived as healthier. For example, fruit juices are growing at 18% year-on-year, while carbonated drinks such as colas are growing less quickly, at 6% for the same period.9 In the last few years, growth across the market has largely come from consumers purchasing more frequently and spending more, especially in fruit juices, where premiumisation of the product range has resulted in a 17% rise on the average price paid per litre year on year.10 Premium soft drinks performed ahead of the market in 2007, growing by 10% to £83 million as consumers opted for healthier, natural soft drinks. Mintel forecasts that the value of the UK premium drinks market will increase by an estimated 20%, to reach £100 million at current prices, by 2011, before seeing a decline to £94 million by 2012.6 However, it is worth noting that Mintel define ‘premium soft drinks’ simply to be all those within the following categories:

The impact of premiumisation on drinks packaging 11

fruit and herb drinks (for example, Amé, Aqua Libra, Shloer and Appletiser); Pressés, from brands such as Bottlegreen, Belvoir and Duchy Originals; and premium flavoured sparkling waters – typically spring waters with a subtle flavour achieved by the addition to

the water of fruit juice, essences or flavourings plus usually some form of sweetener.

2.1.3 Comparison of drinks sub-sectors, by volume The figure below shows the relative sizes of drinks markets in the UK, by volume:

Figure 1: Comparison of sub-sector sizes by volume, 2008, (estimated). Total height of bottle represents UK market size by volume.5 & 35

The impact of premiumisation on drinks packaging 12

2.1.4 Estimating the size of the premium drinks market This section looks at how the size of the premium drinks market is estimated, in order to investigate the implications of the trend towards premiumisation on drinks packaging in a later section of this report. As the term ‘premium’ is poorly defined and means many different things to different groups (see Section 3, ‘Definitions and Themes’), it is impossible to get accurate figures for what proportion of each sub-sector is ‘premium’. However, it is possible to estimate these figures if certain assumptions are made. Table 2 shows estimated proportions of each sub-category which might be called ‘premium’, by volume, and details the assumptions, logic and sources used in making these estimations:

Table 2: Estimate of proportion of alcohol market which is ‘premium’, by sub-category, by volume

Sub-category UK market volume

Proportion estimated premium

Assumptions and logic

Million litres % Still wine 1262m litres5 3% From interview with Philip Malpass, Head of PR,

Constellation Europe Champagne 29.2m litres3

(2007) 10 to 15% http://www.novusvinum.com/features/prestigecuvees.html

Sparkling wine 29.2m litres3

(2008) 10% Of top ten brands, only ‘Friexnet’ seems to be ‘premium’ at

£11.99 and this has 6% of market. Also, assumed similar to Champagne in terms of proportion.

Whisky 88.2m litres24

(2008) 28% Total of all Deluxe, Imported and Malt as a proportion of

total volume.24 Vodka 61.6m litres

(Neilsen to yr end Aug ’08)

10% In 2007, Smirnoff, Glens & Vladivar, all non-premium, made up 66.7% by value. Own brands was 8% (non premium).

Gin 11.94m litres (Neilsen to yr end Aug ’08)

20% Gordon’s, non premium, approx 50% of market. Own brand was 19.8% by value (non premium). Approx half of other top ten brands are premium.

Rum 18.7m litres26 Unknown Liqueurs 30.95m

litres16 Unknown

Ales & stouts 1.43bn litres4 46% From draft, assume ‘nitrokeg’ and stout are premium and ‘mainstream’ are not. From packaged, assume ‘premium’ and ‘stout’ are premium and ‘mainstream’ is not.4

Lager 3950m litres14 (2007)

40% Class III = 1590m litres (refers to ‘premium lagers of 4.3-7.5% ABV’)14

Cider 726m litres 10% 2 biggest premium brands, Magners and Bulmers = 14% of the market by value (2007) - probably 10% by vol. 10% of cider sold in the same period was in glass bottles & and most premium cider is sold in glass bottles.

Alcoholic RTDs 151m litres22 88% 88% are PPSs (Premium Packaged Spirits) rather than alcoholic carbonates22

Alcoholic mixables

38m litres25 23% Pimms is only top ten brand which is premium = 18.2% of market by vol25. Own label (8%) not premium. Assume half of remainder are premium.

Low-alcohol & non-alcoholic

19.4m litres 17 50% Kaliber market leader – 40% in 2006. Most of others are German premium brands.

The impact of premiumisation on drinks packaging 13

Table 2 (continued): Estimates of proportion of soft drinks market which is ‘premium’, by sub-category, by volume

Sub-category UK market volume

(and source)

Proportion estimated premium

Assumptions and logic

Bottled water 1717m litres27 20% 17% of market sales by volume were in glass in 2006. Some premium would also be in PET.

Carbonates 6274m litres28 0.5% All top ten brands at almost the same price point. Whole Earth Organic one of few premium brands but with much smaller distribution.

Sports drinks 129m litres13 Energy drinks / Stimulants

313m litres13 70% Red Bull, Lucozade and Lucozade Sport made up 65.8% of the market by vol. in 2006 (DATAMONITOR) and these are all described as premium by Mintel. There are other brands which are also premium, so the proportion is likely to be higher.

Squashes, cordials & high- Juice

567m litres29 7.4% Assume all cordial and all High-Juice is premium.29

Fruit juice and fruit drinks

1970m litres29 51% Assume pure fruit juice is premium. Pure as %age of all fruit juice + fruit drinks29

Smoothies 92m litres31 Unknown “Organic smoothies are a relatively recent development, since manufacturers have been waiting for the market to be mature enough to support a premium tier.”31

RTD tea and coffee

19.07m litres28

Unknown

Figure 2 below provides a visual representation of these estimated proportions. The sub-categories with the highest proportions of premium products are therefore: 1 Alcoholic RTD’s; 2 Energy drinks / stimulants; 3 Fruit juice and fruit drinks; 4 Low alcohol and non-alcoholic; and 5 Ales and Stouts

The impact of premiumisation on drinks packaging 14

Figure 2: Proportions of each sub-category estimated to be ‘premium’

The impact of premiumisation on drinks packaging 15

2.1.5 Key players The UK drinks sector is dominated by large brand owners. Within the UK alcohol sector, these include Diageo, Pernod Ricard, Constellation Europe, Bacardi-Martini, Coors Brewers, ABInbev, Heineken and Carlsberg UK. Within soft drinks; Britvic, Coca-Cola Enterprises (CCE), Danone Waters, GlaxoSmithKline UK Ltd., Innocent, PepsiCo UK and Nestlé are key players. Within packaging; Rexam, Crown and Ball dominate in metal O-I, Quinn Glass, Ardagh Glass, Allied Glass and Beatson Clark in glass and Artenius, Linpac and Rexam in plastic. Whilst many of these are large multi-nationals, independent companies such as Innocent have shown the influence that they can have on the market and also on packaging. The Appendices to this report show the top ten brands in most drinks sub-categories and their respective market share. 2.1.6 Key trends affecting the drinks sector Research was undertaken into trends affecting the drinks industry in the UK in order to help assess the implications for resource efficient premium packaging in the future. These are summarised below: Increased drinking at home: While two thirds of alcohol sales by value are via the on-trade, this proportion

has fallen since 2005.5 The shift away from pubs, bars and restaurants towards more drinking at home is a major trend in the drinks sector and will encourage the consumption of premium drinks, which become more affordable to drink at home than in pubs and restaurants. This shift has been helped by the recession and smoking ban in the UK.5.

An ageing population: Older drinkers as a consumer segment are forecast to grow more rapidly than any other age demographic8. The expected impact of this is to favour the off-trade and exacerbate the swing towards more drinking at home.5.

Increasing number of ABC1 consumers: ABC is a socio-economic group that includes professional and skilled workers. According to Mintel’s ‘Off vs. On Trade Drinking’ report (September 2008), “In 2003, 53.7% of the population were ABC1, whereas in 2013 it will be 56.4%. This will benefit the off-trade sector as consumer research show that this group drink at home more frequently than the rest of the population. It is also good news for on-trade, which will be more reliant than before on premiumisation.” 5

Health consciousness: The last few years have seen an increased concern over health in the UK, helped by celebrity chefs and the Government’s 5-a-day, to encourage the consumption of fruit and vegetables. This has led to, for example, an 18% year-on-year growth in fruit juices compared to 6% in carbonates.10 The Government also, during 2008, launched a £6m ‘Know your limits’ campaign and a £4m campaign to emphasise the serious consequences of binge drinking to 18-24 year olds.8 This trend is illustrated by a reduction in sales of super strength ciders and lagers, which have dropped due to their associations with excessive drinking and alcoholic RTD’s.

Rise of the ethical consumer: Since around 2005 there has been greatly increased consumer awareness of and demand for environmentally friendly packaging and ethical, organic and fair trade premium products. Over the same period there has been a proliferation of NPD based around premium ethical and environmentally friendly drinks, so this trend seems to be encouraging the development of resource efficient premium drinks packaging. There currently seems to be no consensus about how this will be affected by the credit crunch and whether demand for low-cost products will erode this growing market.

Premiumisation: This has been a key theme across new product development (NPD) within drinks, and across all categories, particularly in spirits, seasonal launches and new drinks targeting females.5 Premium options are particularly important in the off-trade, with consumers happier to experiment with more expensive brands and products for home use before trying them in costlier on-trade settings. 30

Fluctuating energy and materials costs. Rising material and energy costs have squeezed margins at a time when prices are being driven down due to the credit crunch. Companies are set to benefit more from resource efficiency measures in light of high materials costs and this has been encouraging investment into lighter weight drinks packaging.

The ‘credit crunch’: The effects of the ‘credit crunch’ at the time of writing this report, are increasingly evident as companies go out of business and jobs are lost. The recession is predicted to continue into 2009.

The impact of premiumisation on drinks packaging 16

The impact of premiumisation on drinks packaging 17

2.2 Premium drinks sub-category overview 2.2.1 Categorisation of the premium drinks sector The figure below shows how the drinks sector has been split up into sub-categories for the purposes of this project. More detailed information is given in the appendices for the various sub-category groups and the figure also indicates which appendix relates to which sub-category.

Figure 3: Drink sub-categories, their groupings and references to the appendices.

2.2.2 Premium still wine, sparkling wine and Champagne Interviews with sector representatives indicated that the still wine retail market seems to define ‘premium’ or ‘fine’ wines as bottles retailing for £7 or £8 and over, although one wholesaler defines ‘premium’ still wine as that which retails over £15. According to one respondent, these wines have seen a rise from 1% to 3% of the market in the last few years. Despite this ‘premiumisation’, ‘premium’ remains a small proportion of this still wine and the wine sector has seen a cycle of discounting at the same time. According to this same respondent, retailers and brands are keen to get the higher margins associated with trading up but UK consumers generally have limited knowledge and find it hard to see the value in more expensive wines. In terms of packaging and sustainability, the still wine market has seen significant lightweighting activity and experimentation with alternative packaging formats, such as aluminium cans and bottles, doy sachets, alternative formats for bag-in-box, liquid cartons and PET bottles. Champagne can be seen as a ‘premium’ sub-sector and within that, 10% to 15% of Champagnes are ‘deluxe’, or ‘vintage’ 44 and represents the best a maker can produce. Sparkling wineB has been growing faster than Champagne. The shift towards home entertaining is boosting volume sales of Champagne and sparkling wine in the off-trade and inspiring NPD in ultra-premium styles and secondary packaging for gift occasions.3 2.2.3 Premium lager, ales, stouts and cider At around 4bn litres a year, lager is the second biggest drinks sub-sector by volume in the UK. Historically, a ‘premium’ lager was defined as one having more than 5% alcohol, but this definition is no longer applicable and low alcohol premium products are now available. ‘Premium’ was seen by interviewees to represent a broad range of characteristics including heritage, sense of place, scale of production, provenance, personality and packaging. In terms of packaging, twice as much lager is sold in glass than aluminium cans and that proportion is B ‘Sparkling Wines’ including, white, rosé and red, are known by a variety of terms, dependant upon region of production.3

‘Champagne’ including rosé and vintage Champagne, is produced under strict regulation within the tightly defined Champagne appellation of France. Within the EU, the term méthode champenoise is similarly restricted solely to the Champagne area.3

increasing.14 The volume of lagers sold in glass increased by 17% from 2004 to 2006.14 According to Mintel’s Lager report (July 2007) 14, this is partly due to less draft lager being sold because more people are drinking at home. The report states “Product presentation has an impact of consumer perceptions of the quality of the lager contained within it. Lager presented in bottles is perceived by consumers as better quality than that presented in cans.” Ales and Stouts sell in smaller volumes, but have a very high and increasing proportion of ‘premium’ products. Smaller niche producers are enjoying a revived interest in this category, but beer as a whole is a declining market. Cider is a small category compared to lager but has seen 25% growth since 2005 due to Magners ‘over ice’ campaign and the resulting re-branding of Bulmers and Gaymers as a premium product11. This has resulted in a 6.6% increase in the proportion of cider sold in glass between 2003 and 2007, 11 showing a potential link between a higher proportion of premium products on the market and a higher proportion of glass packaging. There have been a number of high profile case studies on lightweighted bottles in this sub-category. Please refer to the Grolsch bottle case study in section 10.4.2 in ‘Premium drinks design guidelines and case studies’. There is also more information on the WRAP website: www.wrap.org.uk/retail/case_studies_research/case_study_2.html 2.2.4 Spirits and liqueurs This sector is relatively small in volume terms, compared to other drinks consumed in the UK, at 210m litres, however volume is growing by approximately 5% per year.15 Spirits and liqueurs have been leading the way in terms of premiumisation, with ‘premium’ being three times more common than other new product claims during 2008.25 Vodka brands are seeing the largest growth in consumption (13% by volume) and there is a huge expansion in the number of ‘premium’, ‘super-premium’ and flavoured vodkas being launched, commonly positioned as ‘designer premium’ (see Section 3, ‘Definitions and Themes’) and claiming purity and sophisticated manufacturing processes. The whisky sector is characterised by a large number of small distilleries, some of which are owned by large international brand owners, with around 90% of Scotch whisky being exported to international markets. The gin sector includes premium brands such as Bombay Sapphire, Tanqueray and newcomer Hendricks in the top ten UK sales for gin brands, all of which are experiencing growth.15 Spirits and Liqueurs do have a large proportion of products with additional packaging to encourage gift purchases and to increase shelf presence and a ‘premium’ feel. 2.2.5 Premium alcoholic mixables and ready-to-drinks (RTD’s) This market has grown in volume by 6.6% to 38m litres between 2003 and 2007 but it is still a small sub-category in relation to other alcoholic drinks, with growth recently stagnating.15 According to Mintel’s 2008 report on this sub-category, top brands such as Malibu and Martini have updated their bottle and labelling design to improve the premium feel, but in general, alcoholic mixables are seeing much less premiumisation than other categories.15 Alcoholic RTD’s (formerly referred to as Flavoured Alcoholic Beverages (FAB’s) or alco-pops)) are predicted to decline steeply in volume sales by 34% from 151m litres in 2007 to 2013.22 This is due to the increasing number of ABC1 consumers turning to more sophisticated alternatives, predominantly due to alcoholic RTDs’ association with binge drinking22. Premium RTD’s, such as Smirnoff Ice, have dropped in price, making this sector an example of how ‘premium’ products can make up the majority of sales, or how ‘premium’ has become ‘core’. According to one interview respondent representing a major supermarket, premiumisation has occurred within canned pre-mixed drinks as a result of the introduction of branded products such as Gordon’s Gin and Tonic. Prior to this, own-label products were the only ones available as pre-mixed. 2.2.6 Premium carbonates In the UK, over 6bn litres of carbonates are consumed every year, over 50% more than any other drinks sub-sector. 28 Coca-Cola hold almost one third of this market and have recently launched lightweighted versions of their 500ml PET bottle, ‘Contour’ glass bottle and aluminium can. Carbonates have a very small proportion of premium products, such as Whole Earth Organic and Fentimans. These products tend to be sold in the same packaging formats as the mainstream products, such as glass, PET

The impact of premiumisation on drinks packaging 18

The impact of premiumisation on drinks packaging 19

and cans and so further premiumisation of this sub-sector is unlikely to have a major impact on packaging resource efficiency. The carbonates sector has also seen a decline in sales due to increased health concerns and new legislation in schools to ban sugary drinks being sold from vending machines. This could well contribute to premiumisation of the carbonates sub-sector, as premium carbonates tend to be marketed as healthier alternatives. 2.2.7 Premium fruit juice, juice drinks, squashes, cordials and smoothies Cordials are defined by Mintel as having higher concentration levels than ‘squashes’ (see Appendix 8) and are a ‘premium’ alternative to core ‘squashes’. 29 ‘Premium’ cordials are seeing a rapid growth in sales, however these account for a small proportion of the category. 29 As squashes make up the majority of the sector and volume sales of squashes are declining, overall volumes of this sub-sector are falling. However, as premium cordials are normally packaged in glass there is likely to be an increase in the amount of glass within the sub-category as a result of further premiumisation.29 Fruit Juice and Juice Drinks make up the third largest category in this sector by volume, at 1.97bn litres for 2008.30 Premium brand Tropicana leads this market. The premium Smoothie market has grown from 12m litres in 2003 to 92m litres in 2008, led by InnocentC, but is still small in comparison with fruit juice and juice drinks. 31 Growth is now slowing as consumers swap from smoothies to premium juices in the economic downturn. 31 2.2.8 Premium bottled water Bottled water is the fourth largest drinks sub-sector by volume at approximately 1.7bn litres sold per year. 27 Use of glass is normally restricted to premium products and, according to Mintel’s report ‘Bottled Water, Market Intelligence, June 2007’, use of glass is on the decrease. 27 The water sector is likely to continue to push the resource efficiency agenda due to its coming under fire on environmental grounds with respect to high transportation impacts and as such, premium bottled water may come under pressure to reduce the amount of packaging material used. Increasing health concerns have seen consumers switching away from carbonates towards premium flavoured and functional waters, resulting in a nine-fold increase in sales of this sub-category from 2000 to 2006. 21 There has been a plethora of premium new product development activity in this sector, with premium products launched which claim to give improved health, alertness, energy, vitamins and even younger looking skin and it is this trend which is mainly responsible for the premiumisation of the water sub-category. According to Zenith International, whilst the poor summer weather was identified as key reason for an overall 4% decline in UK sales volumes, ethical brands are expected to become a major driver in the segment in the future.36

Another trend we are increasingly seeing is company-branded in-office glass water bottles encouraging employees to re-use bottles and discouraging the buying of bottled mineral water, for example EcoPure Waters. IMAGE Reusable water bottles are being introduced in offices

2.2.9 Premium functional drinks (excluding water) These include sports and energy drinks and RTD teas and coffees. GSK’s premium product Red Bull has dominated the market over the last few years and been partly responsible for its strong growth and premiumisation.

C Innocent is both an independent producer and a market leader in packaging innovations, such as its development of 100% recycled PET bottles. It is also an interesting case study in terms of environmentally friendly packaging materials as Innocent switched from using bioplastic bottles to recycled bottles in 2007. Furthermore, its use of graphics to position the product as premium in liquid cartons is also interesting.

3.0 Definitions and themes This section looks at the meaning of ‘premium’ and ‘premiumisation’ within the drinks sector, exploring whether there is a common definition, and identify the ways in which retailers, brands and designers have developed and marketed drinks products as ‘premium’. 3.1 Existing definitions of ‘premium’ The dictionary definition of 'premium' as an adjective relates to quality, value, price and cost: “ - adjective of exceptional quality or greater value than others of its kind; superior: a wine made of premium grapes. of higher price or cost.” 47

Mintel’s 2006 Report ‘Premium Foods, Market Intelligence’ defines ‘premium food’ as follows: “Premium foods are defined … as food products that take a premium position within mainstream food categories, whether processed food such as ready meals, soups etc or primary commodities foodstuffs such as red meat, rice, oil etc.” 33 It goes on to say: “Products with a luxury image, like caviar and truffles, for example, are excluded as one-offs belonging to no mainstream market, and special seasonal assortments, like Christmas hampers and gift packs, are also excluded.” 33 Taking these definitions and applying them to the drinks sector, it could be argued that sub-sectors such as Champagne are ‘luxury’ rather than ‘premium’. It could also be argued that all Champagne is premium but for the purposes of this report, it is most useful to look at the highest end of each sub-sector. In the case of Champagne, this would refer to ‘deluxe’ Champagnes, which make up 10% to 15% of the Champagne sector.44 The Institute of Grocery Distribution issued a report called Shopportunities’ in 2005 that defined ‘premium groceries’ as follows: “The use of the word premium to describe a product suggests to shoppers that the product will be of better quality than competitor products. However, for many shoppers the word premium can imply a higher price-point and can therefore be a barrier to purchase. Use of other words which indicate a superior product and imply added benefits but are not immediately associated with price are therefore preferable to the word premium. Ongoing improvement and innovation are important for a product to maintain its premium status as shoppers see premium as being a comparative term. Therefore, unless a product stays ahead of its competitors it will no longer be considered premium. The main reason for buying a premium product is the expectation of a high quality product. The description and product delivery therefore need to meet with shoppers aspirations.” 35 From these definitions, it can be concluded that ‘premium’ refers both to price and to product quality. It could be argued that it relates also to packaging format (is Coca-Cola sold in a glass bottle more premium than the same Coca-Cola sold in a 2 litre PET bottle?). Furthermore, it is clear that the same product can lose its premium status – either due to competition, as a result of stagnation and lack of innovation, or due to retailers cutting prices. The following sections of this report look at these issues in more detail.

The impact of premiumisation on drinks packaging 20

3.2 Definitions of ‘premium’: Findings from interviews Twenty key representatives from the drinks, retail and design sectors were interviewed for this project about what the terms ‘premium’ and ‘premiumisation’ meant to them within their organisation. For confidentiality reasons, and for the purposes of this report, the interviewees are identified as follows:

Table 3: list of interviewees for this project Organisation Interviewee Retailer A (Supermarket) - Packaging Technical Manager Retailer B (Supermarket) - Head of Packaging and Print Retailer C (High Street) - Marketing and Store Design +

CSR Project Manager + Senior Packaging Technologist Beer Brand D Small brewery Beer Brand E (Large international brand) - Senior Brand Manager Wine Brand F (Large wine brand) - Senior Marketing Director Alcoholic Drinks Brand G (Large international brand) - Head of Public Relations Alcoholic Drinks Brand H (Large international brand) - Innovation Manager + Packaging Technology

and Innovation Bottled Water Brand I (Large water brand) - Packaging Development Manager Functional Water Brand J (Small water producer) - Co-Founder and Director of Sales and Operations Premium Fruit Drink Brand K (Independent producer) Sustainability Manager Design Agency L Client Director Design Agency M Structural Design + Planner Glass Sector Association N Director General Spirits Sector Association O Environment Manager The range of definitions relating to a premium drinks offering varied considerably between respondents. This reflects the key issue of trying to define premiumisation - that it lacks a single definition. Premiumisation was taken to mean (amongst other things): more expensive; better quality; more expensive and better quality; having more expensive, ‘lush’ packaging; having more considered packaging using different fonts, colours, textures, materials etc. that attract a

different customer – generally a higher spending or more ‘sophisticated’ customer; having packaging that projects quality cues. These cues are often seen as shorthand for a range of larger

quality associations, maybe related to other products and categories even; additional layers of packaging; the heritage of the product; the provenance of the product; the target market; sold in selective outlets; out of reach of the average shopper; very sector specific; or ‘trading up’ by customers to higher price point products

The philosophy of premium, however, was seen more uniformly with all respondents viewing the trend for premiumisation as a way of more effectively segregating the market in order to provide a ‘better’ offering to those customers with larger incomes or greater product interest. Some went as far as to acknowledge that premium means not affordable or attainable to the majority. There was also a suggestion that premium can happen both intentionally and unintentionally, although the latter is undesirable as customers looking for value may well be put off by a premium appearance. In many cases premiumisation manifests itself as the ‘up selling’ and re-alignment of existing brands. The issue of defining a ‘better’ offering is complex. Beer is an extremely interesting example. Traditionally stronger beers (over 5% ABV) were considered premium, however this is not necessarily the case anymore. Premium is now represented by a much more complex mix of attributes including the heritage of the beer, its provenance and ingredients, its packaging (glass providing significantly enhanced premium cues over PET or aluminium), its country of origin, and its price. There are examples of brands that have reduced alcohol strength