Final hindalc

22

Merger & Acquisition (Hindalco & Novelis)

-

Upload

anurag-pandey -

Category

Business

-

view

542 -

download

0

Transcript of Final hindalc

Merger & Acquisition(Hindalco &

Novelis)

INTRODUCTIONTo

Company

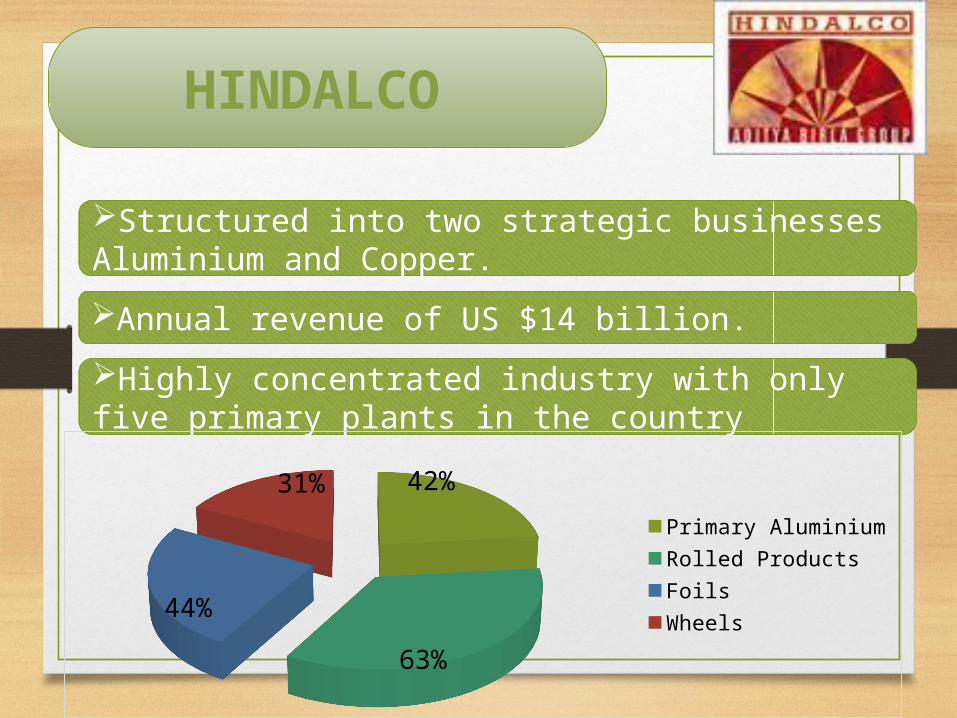

HINDALCO

Structured into two strategic businesses Aluminium and Copper.

Highly concentrated industry with only five primary plants in the country

Annual revenue of US $14 billion.

42%

63%

44%

31%

Primary AluminiumRolled ProductsFoilsWheels

SWOT ANALYSIS FOR HINDALCO

• Global brand image.

• Cost effective producer.

• Sound financial position.

• A high degree quality consciousness is the core competence of the

company, ISO 9001 and ISO 14001 have added more prestige to the

company.

• Company has a well-established distribution network, covering a

geographically wide and scattered market.

5

STRENGTH

• Present production capacity is not adequate to meet the rising high demand.

• Technology is not upgraded to mark as compare to global giants in aluminium industry.

6

WEAKNESS

•R & D collabratation with universities and another research organization.•More emphasis on downstream production of value added products.•Recycling should be adopted as routine production.•Raising more finance from marketing for more acquisition and merger.

OPPORTUNITY

• Innovative revolution in plastic and steel industry.• Reduce in Exide duty.• Fall in price of Al. In neighbour country.

7

THREATS

NOVELIS

Canada based company formed in early 2005 as a result of a ‘forced’ spin-off from its parent, the $ 23.6-billion aluminium giant and Canada-based Alcan Inc.

Novelis is the world leader in aluminium rolling, producing an estimated 19 percent of the world's flat-rolled aluminium products.

The company is No. 1 rolled products producer in Europe, South America and Asia, and the No. 2 producer in North America.

With industry-leading assets and technology, the company produced the highest-quality aluminium sheet and foil products for customers in high -value markets including automotive, transportation, packaging, construction and printing

The company had 36 operating facilities in 11 countries as of December 31, 2005.

History

Objectives of Acquisition

• Higher profitability due to increased customer base i.e. increased scale and global footprint.

• To gain access to global aluminium market and expand production capacity to keep pace with growing demand for aluminium.

• This merger of Novelis into Hindalco will establish a global integrated aluminium producer with low-cost alumina

• Aluminium production facilities combined with high-end aluminium rolled product capabilities. Hindalco got the fusion technology of Novelis which increased the formability of aluminium.

• After merger Hindalco will emerge as the biggest rolled aluminium products maker fifth -largest integrated aluminium manufacturer in the world. Novelis had the capacity to 3 million tonnes while Hindalco had the capacity to produce 2,20,000 tonnes

Indian Deal makers

• Team MembersKumar Mangalam BirlaDebu Bhattacharya, Managing Director, HindalcoSumant Sinha, Group CFO

• Announced on Feb, 11, 2007• Completed in May 2007• Negotiation went for 18 months.

Hindalco

AV Metals(Canad

a)

Novelis(Canada)

100% Shares

AV Aluminium(Cana

da)

AV Minerals (Netherlands

)

6 Billion dollarsS

Aditya Birla Group

32 % stake

51 %

Financial Arrangements

• Showing the finances necessary for paying off the shareholders and the debtors

• ABN Amro Bank, Bank of America and UBS back-stopped the funding requirement at the recourse leg for USD 3.1 billion

• UBS and ABN Amro Bank provided back-stop facilities of USD 2.4 billion that was to be used to pay off the existing lenders

• Once the shareholders approved the bid and the courts in Canada as well as regulatory authorities in several countries approved the acquisition, the funds required to pay off the shareholders was drawn down on 11 May, 2007 into AB Minerals and AB Metals

Deal structure

Divided into 2 parts-

1. 100% of Novelis equity @44.93$ per share which add up to $3.6b

2. $2.4b debt on Novelis balance sheet

No Option of Leverage buyout unlike TATA Corus as debt: equity=7.23:1

• The deal was all cash transaction of USD 6 billion which included a debt of USD 2.4 billion

• Hindalco themselves contributed USD 450 million

• Group company Essel unlisted contributed USD 300 million

• USD 450 million through liquidation of investments

• Hindalco paid USD 44.93 in cash for each outstanding common share of Novelis at 15 % premium

• Hindalco replaced existing USD 2.4 billion loan by term loan of USD 1 bn and high yield bonds of USD 1.4 bn

Valuation Concerns

• Price paid by Hindalco being too high

Price per share never crossed USD 30

In its guidance, Novelis indicated a PBT of approx. USD 35-100 million for 2007

The long term contracts coming to an end by 2010

Not to compete with Alcan Inc.

Equity Stock:

Price Movements Volume Movements

48460.7; 29%1662.98; 1%

110807.76;

67%

4513.23; 3%

1018.31; 1% National Alu-

minium Company (Nalco)

Associated Profiles and Aluminium Limited

Hindalco Madras & Aluminium(Malco)PG Foils

2.18; 31%

1.1; 16%

2.42; 35%

0.25; 4%

1; 14%National Alu-minium Company (Nalco)

Indian Aluminium (Indal)

Hindalco Madras & Aluminium(Malco)Bharat Aluminium

(Balco)

Industry Overview before Acquisition of Novelis( in lac tonnes)

Industry Overview after Acquisition of Novelis (in Sales)

Thank YouPresented By:

Anurag Pandey

Omkar Salunke