Final Exam for ACCT 5330 - Balanced Scorecard

12

Final Exam for ACCT 5330 By Jeff Benedict 624-01-6649 Tuesday, May 12, 1998 Dr. Frank Selto

Transcript of Final Exam for ACCT 5330 - Balanced Scorecard

Final Exam for ACCT 5330

By

Jeff Benedict624-01-6649

Tuesday, May 12, 1998Dr. Frank Selto

Part One:

Memo

To: Christine Howard, CEOFrom: Jeff BenedictDate: May 12, 1998Re: Explanation of the Balanced Scorecard

The purpose of this memo is to clarify the concept of a balanced scorecard to which you have

recently been introduced. I understand you recently heard Robert Kaplan speak on the topic, he

has made this topic popular and since it is his idea you may need some additional verification

that this idea works in the “real world.”

First we must establish what is wrong with the current system which focuses on financial

measures. Management currently makes sacrifices in the current year so things like net income

will be better reported at the cost of future financial performance. The balanced scorecard looks

at ways to measure the financial performance in the long-term. Considering research and

development costs, if you look at the first year you have a large expense and the last year large

revenue, but you have to look at it over its entire life to evaluate the performance. The balanced

scorecard first looks at the company’s mission statement and strategy then translates into four

measures by which the long-term financial performance of the organization can be assessed. The

four measures are broadly defined as organization learning & growth, internal business

processes, customer value, and financial results. The organization learning and growth comes

which have been performance measures for years. The key to the balanced scorecard idea is that

within an organization causal relationships exist such as how a change in human capital causes

changes in other areas. A balanced scorecard can tell you whether spending more time to train

employees will translate into increased profits. Through assessments of an organization one can

create causal relationships which are tied to the mission. Then this, so called model should be

tested to validate whether these relationships exist. The power of a balanced scorecard should

not be underestimated. Suppose a possible causal relationship model looks as such: increased

training, causing less defects, causing lower cycle times and ultimately increased financial

performance. Now, a strategy like increasing training can be measured with some certainty on

how it will affect the overall performance of the organization.

To address your concerns as to whether causal models can really be created and what other

management gurus think. Although, Kaplan stated some examples of effective implementations

of the balanced scorecard, the causal models will be different for every organization and may or

may not be able to be created in this organization. Through discussions you can determine what

the causal model may look like, but that model must be tested to estimate its accuracy. Many

management gurus have bought in on the idea of the balanced scorecard. It has been documented

that the French have used a similar technique for fifty years, their titled translates to English as

the "dashboard." Many articles other than those published by Kaplan and Norton were written

concerning the balanced scorecard, two in particular I would recommend. An article by Chow,

Haddad and Williamson titled, "Applying the Balanced Scorecard to Small Companies," and

another by Curtis and Ellis titled, "Balanced Scorecards for New Product Development. Both

Part Two:

(This part is answered as the responses I would have to the specific questions independent

of each other)

In response to the VP of Marketing:

This concept may very well be a fad, but SWAT analysis, ABC, Target Costing and many

other widely accepted management tools started out as management fads. Not until these

techniques are embraced worldwide and proven to be useless can they be determined to

be truly a fad. The economy today sets us in a highly competitive environment; new

ideas, and chances need to be taken in order to stay afloat. Whether a balanced scorecard

is useless and just a fad is a concern but has yet to be determined as such. As I mentioned

to Ms. Howard, a concept similar to the balanced scorecard has been used for nearly fifty

years in France. This adds some creditability to manager's perception that this tool can

work and is not just a fad. To address your second concern on the time it takes to validate

whether causal relationships exist and whether they will be obsolete. The purpose of a

balanced scorecard is to tie the mission of an organization to the financial performance

and so only if the mission of an organization is changed should the causal relationships or

model change. Considering a model in which highly educated employees equals better

customer retention and better financial performance. The mission of the organization

would be something like delivery of a quality service, and in order to maintain that

Your concern is that these relationships are just someone’s best guess, and you are right.

That is how you first determine causal relationships, but then you test these relationships

either with logic like reality checks or multiple evaluations, or you test it with statistics. I

assume many decisions you make are built off a hunch or your best guess, but to prove

that they will work you either have to roll the dice and take a chance or test the theory. In

addition you mentioned communication of strategy over a management tool. This is a

good question for it seems logical to see that it is a good method to communicate strategy,

but it is not as easy to see its manageability. By communicating strategy all personnel

will work in unity toward a common organizational goal, this in essence is the stepping

stone toward success. You no longer need to manage like you are used to, now

employees will evaluate their contribution in context of how the organization is doing

overall. Basically, you manage the employees by evaluating how well they are doing in

context to their contribution to the overall financial success of the organization.

Response to Human Resources Director:

You have to be happy if everyone buys into the program, one of its intentions is to have

all the managers working toward the mission of the organization and employing the same

strategies. I believe you are concerned about change and I agree that if you are going to

make the change to a new system it must be evaluated completely. As I have mentioned

before, the model must be tested and tested throughout all divisions, for all divisions need

Part Three:

The model is constructed as such:

Dimensions of Performance Measures of Performance

(The construction of this model is based solely on discussions with division managers andcontrollers)

The model begins with average grade level. Through discussions with various managersand controllers of the different divisions, an increase in the grade level would reduce theaverage number of defects per month, but would also increase the average hourly wagedue to higher skills needing to be paid more. It is felt that a higher hourly wage willbetter retain employees and therefore reduce the voluntary turnover rate. If moreemployees are retained, then both average defects per month and cycle time per order willbe reduced. The reduction of defects and cycle time will minimize the rework and overall

Avg. Grade Level Completed

Average Hourly Wage

VoluntaryTurnover Rate

Average Defects per Month

Cycle Time per Order

Percentage on-time Deliveries

Customer Satisfaction Score

Return on Assets

Organizational Learning andGrowth

Business and ProductionProcess Efficiency

Customer Value

Profitability

the model was been constructed this way. In the first line of Kaplan’s article “Why DoesBusiness Need a Balanced Scorecard?” he states, “If you can’t measure it, you can’tmanage it.”

The constructed on page 6 is developed based on logic derived from discussions withprominent individuals within the organization. To add some creditability to the model wewill test it with statistics.

Part Four:

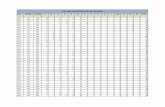

To test the model, each causal relationship was tested independently of each other.The relationship between average grade level and hourly wage was tested first. Thetesting was conducted by comparing the percentage change in grade level from division todivision with the percentage change in dollars paid from division to division. For a moreelaborate description of how the graphs were created, refer to page 10. The argument isthat an increase in grade level should cause an increase in hourly wage. Here is thegraphical representation.

Grade Level vs. Hourly Wage

-150%

-100%

-50%

0%

50%

100%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

are causally linked, but not in all. There is not a valid causal relationship.

à Next the average grade level completed was compared to average defects per month.Here is the graphical representation.

Grade Level Vs. Average Defects

0%

10%

20%

30%

40%

As you can see they are notcompletely causally linked. Not untildivision seven do we see the linesrunning parallel with each other.After division ten you that they are aradical inverse of each other. Basedon the graph we have to conclude thatwithin some divisions these measures

This one is a slam-dunk. Within alldivisions you see that when average gradelevel increases the average number ofdefects per month decreases and vice versa.A causal relationship exists between grade

à Argument is that an increase in hourly wage will reduce the voluntary turnover rate.Hourly Wage Vs. Voluntary Turnover

-60%

-40%

-20%0%

20%40%

60%

80%

100%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17

à When voluntary turnover rate decreases, the average cycle time per order willdecrease and the average defects will also decrease. Each relationship is graphedseparately.

Voluntary Turnover Vs. Avg. Defects

-60%

-40%

-20%

0%

20%

40%

60%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17

In many divisions the turnover rate is related to the average amount of defects, but youcan also see many divisions like 2 and 15 where the average defects has an inverserelationship with the turnover rate. It appears conclusive that in most cases the turnoverrate is related to the average amount of defects and is validated as a causal relationship.With the exception of a couple of divisions, 4, 13 & 14, the turnover rate is causallyrelated to the cycle time per order. The lines are to run parallel with each other and inmost cases they do.

à Average defects and cycle time in relation to the percentage of on-time deliveries.

As the average number of defects decrease,the percentage of on-time deliveries is toalso increase. This effect is split about

Defects Vs. % of On-Time Deliveries

30%

40%

Voluntary Turnover Vs. Cycle Time

-60%

-40%

-20%

0%

20%

40%

60%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17

You see that a causal relationship existsbetween hourly wage and voluntaryturnover rate. They are to be inverselyrelated. Compare division 7’s data,approximately 40% decrease in hourlywage causes an approximate10% increasein the turnover rate.

On the other hand, cycle time appears to bestrongly correlated with on-time deliveries.When the cycle time as a percentagedecreases, the percentage of on-timedeliveries increases nearly throughout alldivisions.

The argument has been made that customer value is related to the customer receiving thegoods on time. The graph below depicts the relationship of on-time deliveries andcustomer satisfaction score.

O n - T i m e D e l i v e r i e s V s . C u s t o m e r S a t i s f a c t i o n

- 3 0 %

- 2 0 %

- 1 0 %

0 %

1 0 %

2 0 %

3 0 %

1 2 3 4 5 6 7 8 9 1 0 1 1 1 2 1 3 1 4 1 5 1 6 1 7

For a causal relationship to exist the lines should run parallel and for the most part theydo. There is a definite relationship between on-time deliveries and the customersatisfaction score. Now let’s see if the customer satisfaction score translates in thefinancial measure of return on assets. It is argued that if the customers are happy thenthey will return and therefore create a higher return on assets.

As you see in most cases, the higher thecustomer satisfaction score, the higher returnon assets. Return on assets was computedfrom the table of data as throughput minusoperating expenses divided by assetsemployed. A causal relationship existsbetween customer satisfaction and return onassets.

C y c le Tim e V s . % o f On-T im e D e l iver ies

-40%

-20%

0%

2 0 %

4 0 %

1 17

Customer Satisfaction Vs. ROA

-30%

-20%

-10%

0%

10%

20%

30%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17

RELATIONSHIP

• GRADE LEVEL VS. AVERAGE HOURLY WAGE• GRADE LEVEL VS. AVERAGE DEFECTS• HOURLY WAGE VS. VOLUNTARY TURNOVER

RATE• VOLUTARY TURNOVER RATE VS. AVERAGE

DEFECTS• VOLUNTARY TURNOVER RATE VS. AVERAGE

CYCLE TIME• AVERAGE DEFECTS VS. ON. TIME DELIVERIES• CYCLE TIME VS. ON-TIME DELIVERIES• ON-TIME DELIVERIES VS. CUSTOMER

SATISFACTION• CUSTOMER SATISFACTION VS. RETURN ON

ASSETS

CAUSALLYRELATED

√ √

√

√

√ √

√

NOT CAUSALLYRELATED √

√

How the Graphs were Created:

By using the spreadsheet of data, I took the change from one division to the next andcompared that percentage to that of another measure. To demonstrate, consider the firstrelationship identified, Grade Level Vs. Hourly Wage.

D ivisions

Average grade level completed

Percent

Change

From One

D ivision to

the next

Average hourly wage

Percent

Change

From One

D ivision to

the next1 10.71 -15% 11.11$ 11%2 11.93 7% 9.49$ 0%3 11.95 0% 10.11$ -15%4 10.15 -2% 10.13$ 14%5 11.62 -3% 9.89$ -11%6 10.31 -21% 9.59$ 8%7 11.14 10% 7.59$ 7%8 11.97 -4% 8.35$ -12%9 10.47 8% 8.02$ 5%

10 11.02 0% 8.65$ -3%11 10.65 -26% 8.66$ 3%12 10.96 58% 6.42$ -8%13 10.14 -14% 10.13$ 6%14 10.73 -7% 8.71$ 0%15 10.75 -29% 8.09$ -4%16 10.36 85% 5.72$ 10%17 11.34 -3% 10.59$ -6%

The graph is created by taking the percentchange from one division to the next for gradelevel and comparing that with the percentchange from one division to the next foraverage hourly wage. The graph is as follows:

Grade Level vs. Hourly Wage

-150%

-100%

-50%

0%

50%

100%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

Division 16 provides a good example of howthe comparison takes place. You see thepercent change for grade level jump 85% and

The advantages are that you can use the data to compute statistical correlation betweenthe different measures in the model. It helps add confidence to your logical assumptionsabout causal relationships and how to measure your performance based on a balancedscorecard model. The biggest disadvantage is the validity of the numbers. Consider thecustomer satisfaction score that was computed by assumptions made from managers ofwhat customers really value. The measure was computed with measurable qualities likeaverage defects per month, but the customer could value things like brand name,appearance and other immeasurables. The balanced scorecard needs to be tested andstatistical testing appears to be the most conclusive, the only thing is that the measuresused to test the model should be tested before hand so that certain relationships are notexcluded for inaccurate numbers.

Additional Data:

As aforementioned, using population data may create a more balanced scorecard amongall the different divisions. To evaluate the performance of one division over anotheradjustments need to be made. If one division resides in a highly competitive market andthe other does not and adjustment should be made. The most useful data may not bemeasurable, such as the value of quality products and quality service. The controller ofDivision 11 hypothesized that the quality of the processes is derived from the employeeturnover rate. It is felt that this may be one component of many which equate to processquality and that not all are measurable. A measure much like customer satisfaction scorebut for internal processes would be useful, something like total quality management.

Part Five:

Throughout the management literature it is stated that most balanced scorecard modelsare not implemented until a couple of years of testing has taken place. This would be arecommendation. I would take the data computed in part four and see where thevariances are that make the relationship not causal, then talk to the particular divisionmanagers about their perceptions. You want to take the implementation slowly, for aswas mentioned by the director of human resources everyone will go along, so everyonewill either sink or swim. A pilot program on one division would not be effective, for thebalanced scorecard is to represent the organization as a whole, plus it is long-term innature.

The opportunity to better understand your business processes and how all divisions match

Resources Used:

"Why Does Business Need a Balanced Scorecard?" by Kaplan and Norton

"Why Does Business Need a Balanced Scorecard? (Part Two)" by Kaplan and Norton

"Applying the Balanced Scorecard to Small Companies," by Chow, Haddad, andWilliamson

"Balanced Scorecards for New Product Development," by Curtis and Ellis

Lectures given by Dr. Frank Selto