final copy.pdf

218

RISK MANAGEMENT IN MICROFINACE INSTITUITION A dissertation submitted in partial fulfilment of the requirements for the award of the degree of MASTER OF BUSINESS ADMINISTRATION By SIRIPURAPU DEEPTHI Register No 1120243 Under the guidance of DR ANIRBAN GHATAK Institute of Management Christ University, Bangalore March 2013

-

Upload

deepti-siripurapu -

Category

Documents

-

view

101 -

download

8

Transcript of final copy.pdf

RISK MANAGEMENT IN MICROFINACE INSTITUITION

A dissertation submitted in partial fulfilment of the

requirements for the award of the degree of

MASTER OF BUSINESS ADMINISTRATION

By

SIRIPURAPU DEEPTHI

Register No 1120243

Under the guidance of

DR ANIRBAN GHATAK

Institute of Management

Christ University, Bangalore

March 2013

ii

DECLARATION

I, Siripurapu Deepthi, do hereby declare that the dissertation entitled Risk Management In

Microfinance Institutions. has been undertaken by me for the award of the degree of Master

of Business Administration. I have completed this study under the guidance of Prof. Anand

Aivalli, Associate Professor, Institute of Management, Christ University, Bangalore.

I also declare that this dissertation has not been submitted for the award of any degree,

diploma, associateship or fellowship or any other title in this University or any other

university.

Place: Bangalore (Name & Signature of the

Candidate)

Date: Siripurapu Deepthi

Register No 1120243

iii

CERTIFICATE

This is to certify that the dissertation submitted by Miss Siripurapuu Deepthi on the title

Risk Management In Microfinance Institutions is a record of research work done by him

during the academic year 2012 – 13 under my guidance and supervision in partial fulfillment

of degree of Master of Business Administration. This dissertation has not been submitted for

the award of any degree, diploma, associateship or fellowship or any other title in this

University or any other university.

Place: Bangalore (Name & Signature of the guide)

Date: Dr Anirban Ghatak

iv

ACKNOWLEDGEMENTS

I am indebted to many people who helped me accomplish this dissertation successfully.

First, I thank the Vice Chancellor Dr Fr Thomas C Matthew of Christ University for giving me the

opportunity to do my research.

I thank Prof. Ghadially Zoher, Associate Dean, Fr Thomas T V, Director, Prof. C K T

Chandrasekhara, Head-Administration, Dr S Jeevananda, Coordinator, Kengeri Campus and Prof T S

Ramachandran, Head-Finance of Christ University Institute of Management for their kind support.

I thank Dr Anirban Ghatak, for his support and guidance during the course of my research. I

remember him with much gratitude for his patience and motivation, but for which I could not have

submitted this work.

I thank my parents for their blessings and constant support, without which this dissertation would not

have seen the light of day.

Siripurapu Deepthi

Register No: 1120243

v

ABSTRACT:

Inherently there is a high risk with the MFI segment. The small, medium and even larger

MFI find it difficult to manage risk or predict the outcome of credit transactions. In Indian

one can find various types of models with in micro financing, such as NGOs, NBFIs, Rural

Banking, Credit Union, these legal entities have different credit risk based on their business

focus, hence it becomes difficult for them, to be able to predict the credit risk that will be

involved. In this dissertation, I have tried to build a estimation model which can be used by

Micro financing institution in India. This model will project the credit risk based on

parameter such as operational self-sufficiency, operational efficiency, write offs, liquidity,

type of micro financing institution.

Apart from that, I have tried to analyze the level of credit risk management of NBFIs in

Bangalore and Hyderabad. And found that all NBFIs have almost the same kind of credit

management in place apart from some exceptional NFBIs, which have concentrated on

management quality along with the MIS in place, good reporting standards, good loan

portfolio management and etc.

vi

TABLE OF CONTENTS

Declaration ii

Certificate iii

Acknowledgement iv

Abstract v

Table of Contents vi

List of Tables vii

List of Charts viii

Abbreviations viii

CHAPTER I

INTRODUCTION

1.1 BACKGROUND OF THE STUDY 1

1.2 PHASES OF MICROFINANCE 4

1.3 PROBLEM STATEMENT 7

1.4 NEED FOR THE STUDY 7

1.5 PURPOSE OF THE STUDY 7

CHAPTER II

LITERATURE REVIEW

2.1 INTRODUCTION 8

2.2 MAJOR RISKS IN MICROFINANCE 9

2.3 HOW THE REVIEW HAVE BEEN CONDUCTED 10

2.4 STUDIES DONE IN THIS AREA 10

2.5 CONCLUSIONS 45

vii

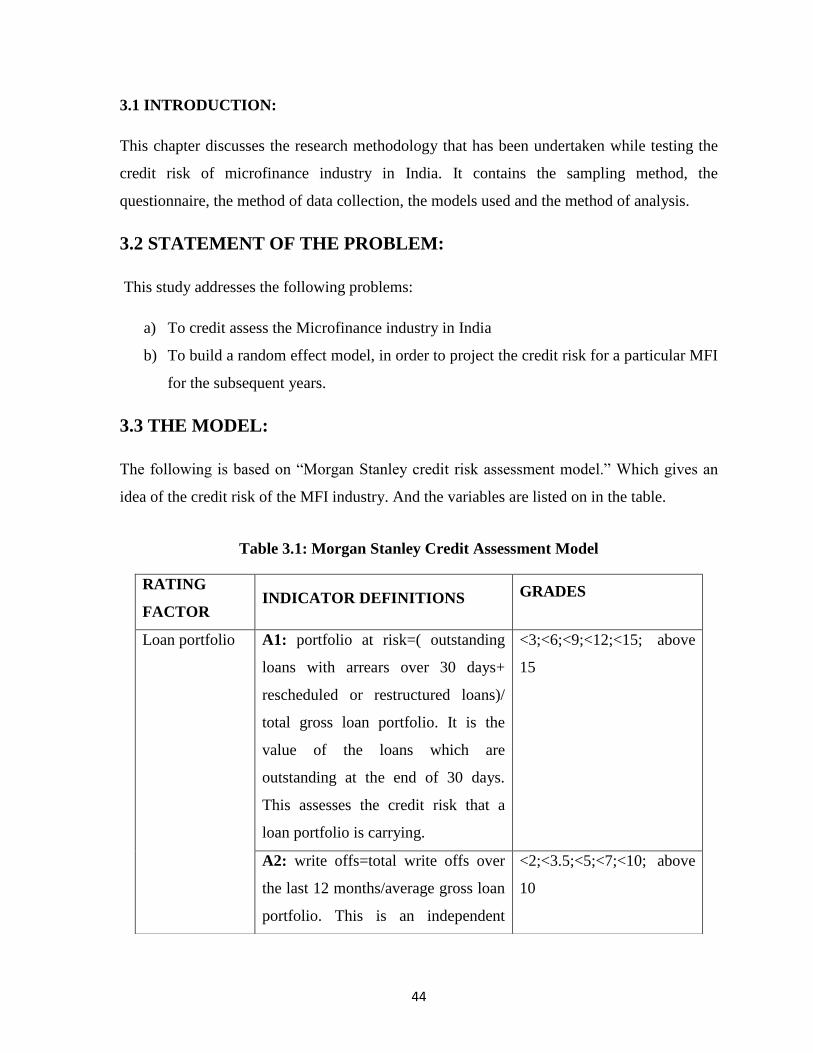

CHAPTER III

RESEARCH METHODOLOGY

3.1 INTRODUCTION 46

3.2 STATEMENT OF THE PROBLEM 46

3.3 THE MODEL 46

3.3.1 SAMPLING METHOD 50

3.3.2 DATA COLLECTION 50

3.4 THE REGRESSION MODEL 50

3.4.1 THE VARIABLES 50

3.4.2 HYPOTHESIS 50

3.4.3 REGRESSION MODEL 52

CHAPTER IV

INDUSTRY OVERVIEW

4.1 MICROFINANCE INDUSTRY 53

CHAPTER V

DATA ANALYSIS AND INTERPRETATION

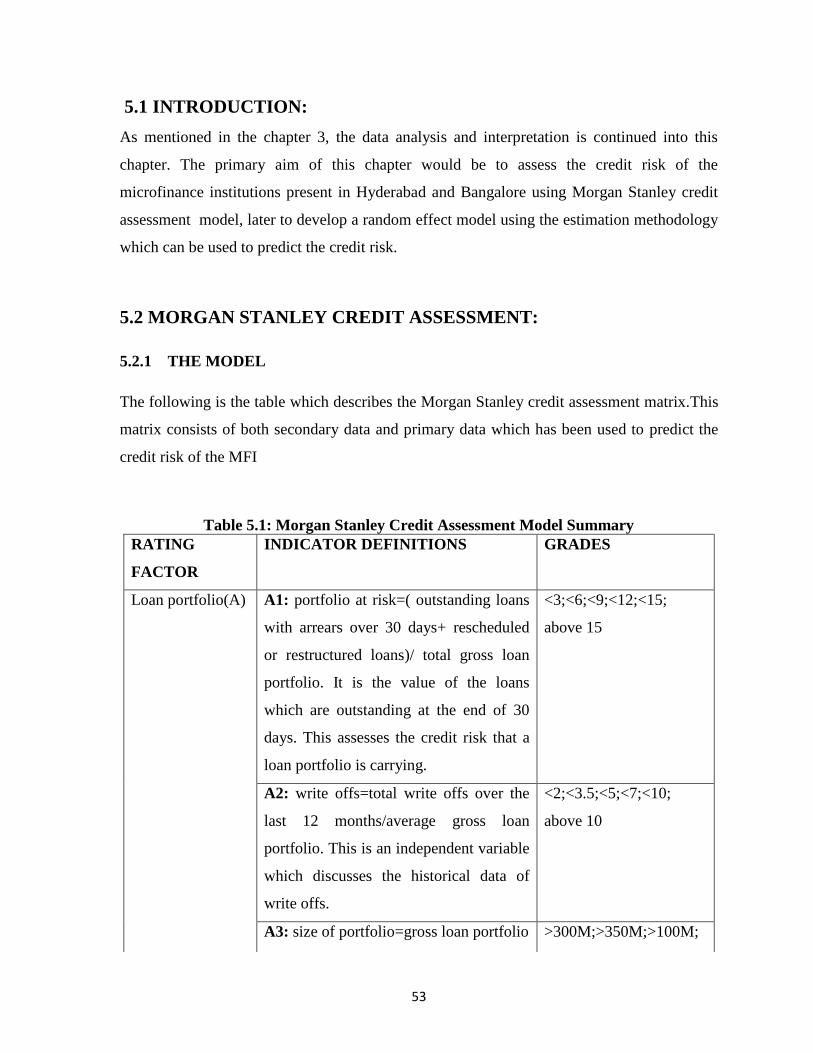

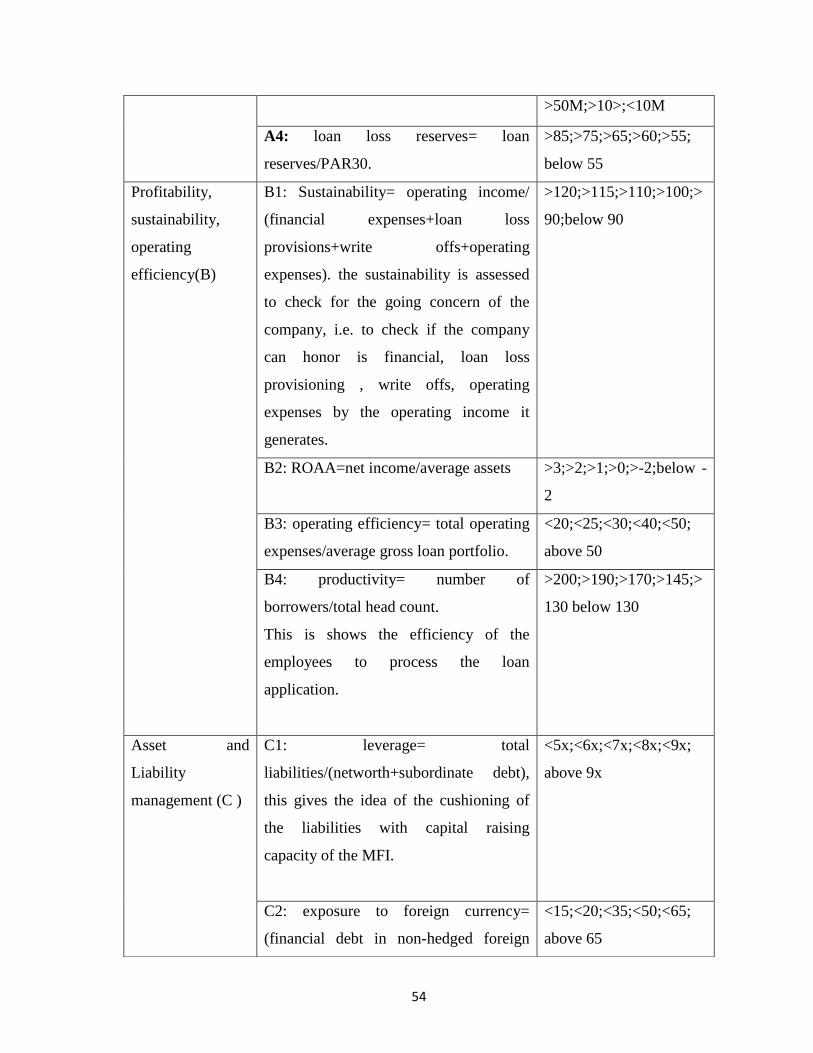

5.1 INTRODUCTION 55

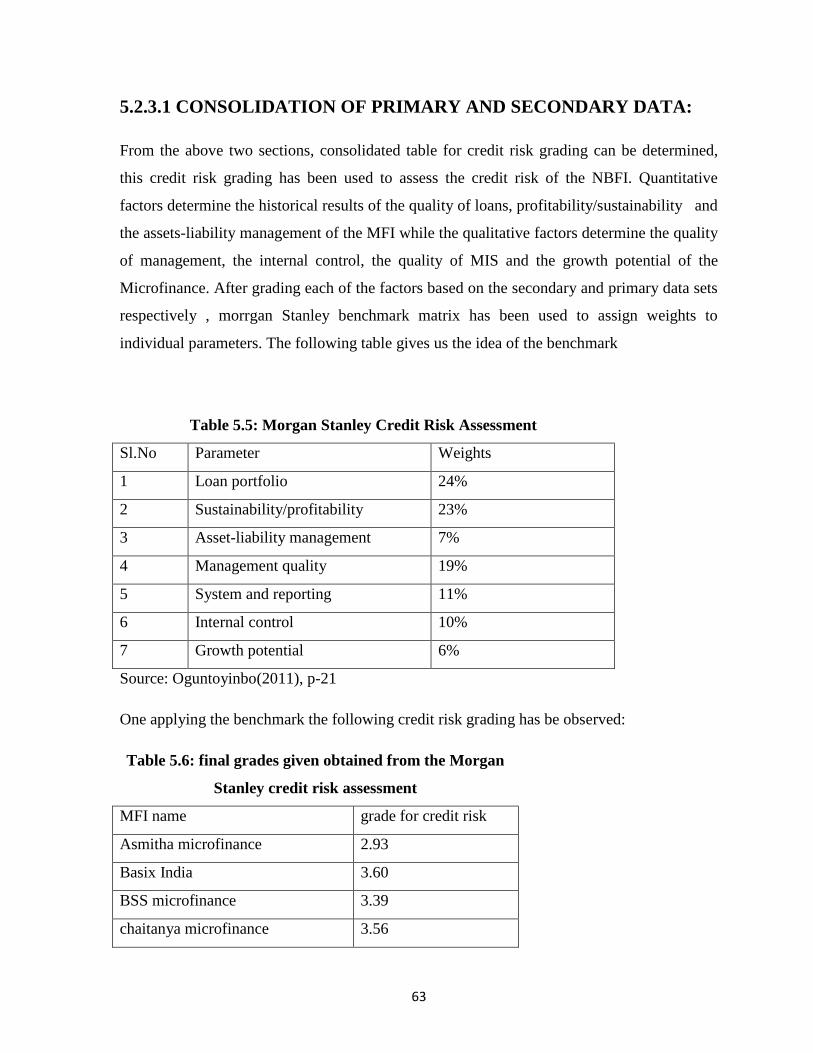

5.2 MORGAN STANLEY CREDIT RISK ASSESSMENT 55

5.2.1 THE MODEL 55

5.2.2 ANALYSIS OF PRIMARY DATA 59

5.2.2.1 RESPONDENTS PROFILE 59

5.2.2.2 DATA CONSOLIDATION AND ANALYSIS 59

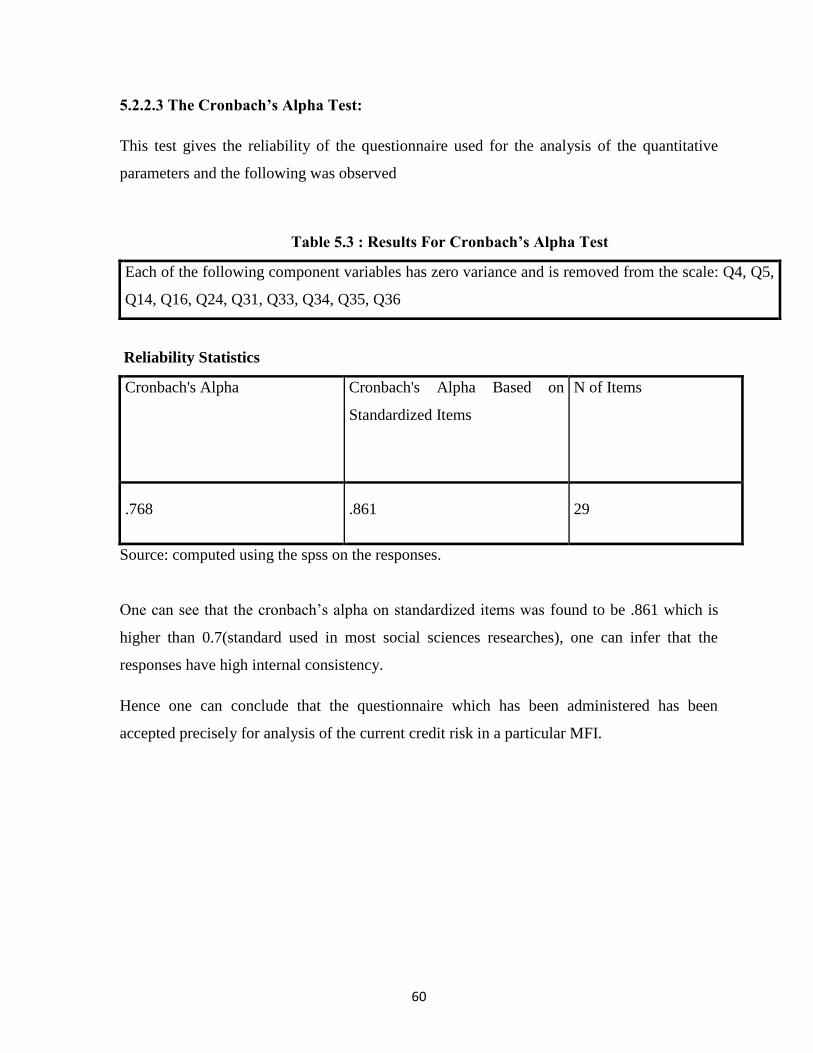

5.2.2.3 THE CRONBACH'S ALPHA TEST 62

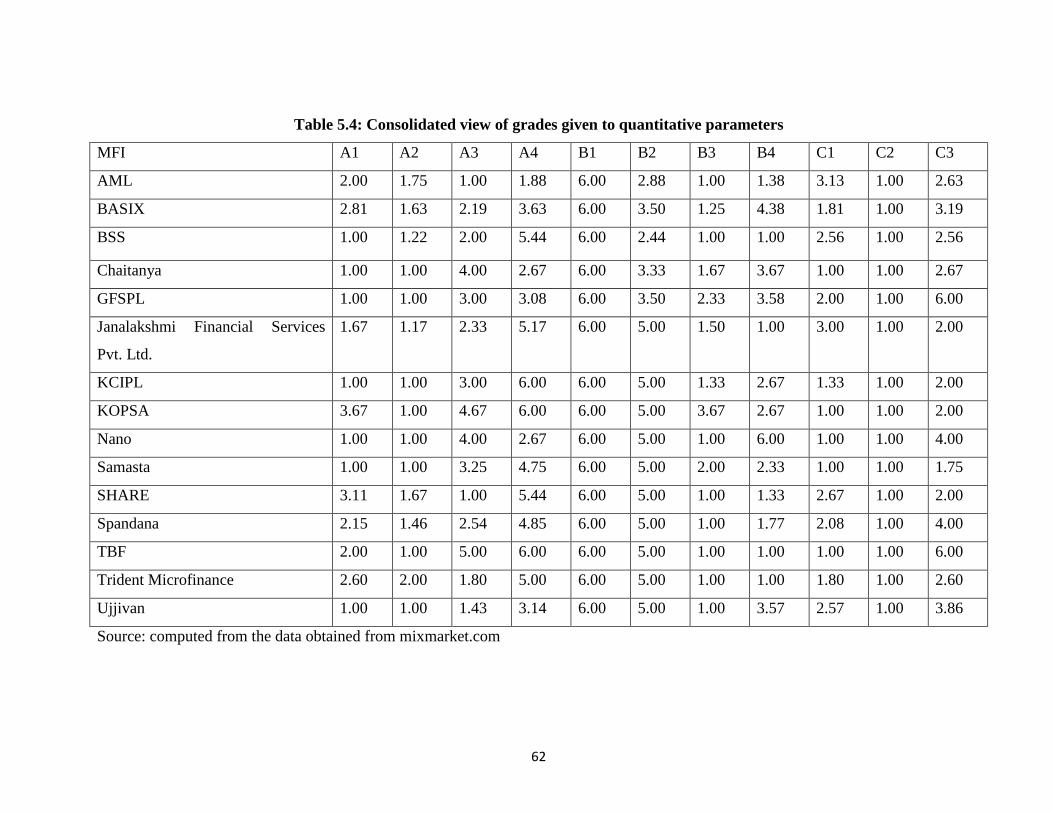

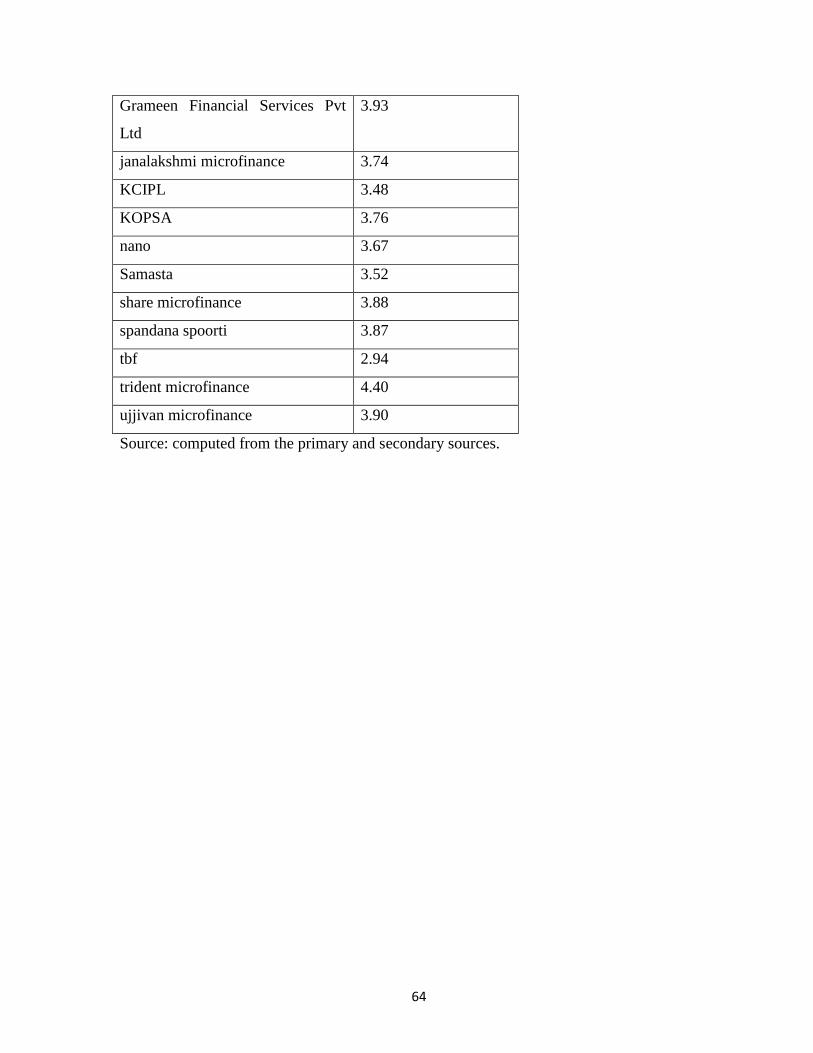

5.2.3 ANALYSIS OF SECONDARY DATA 63

viii

5.2.3.1 CONSOLIDATION OF PRIMARY AND

SECONDARY DATA 65

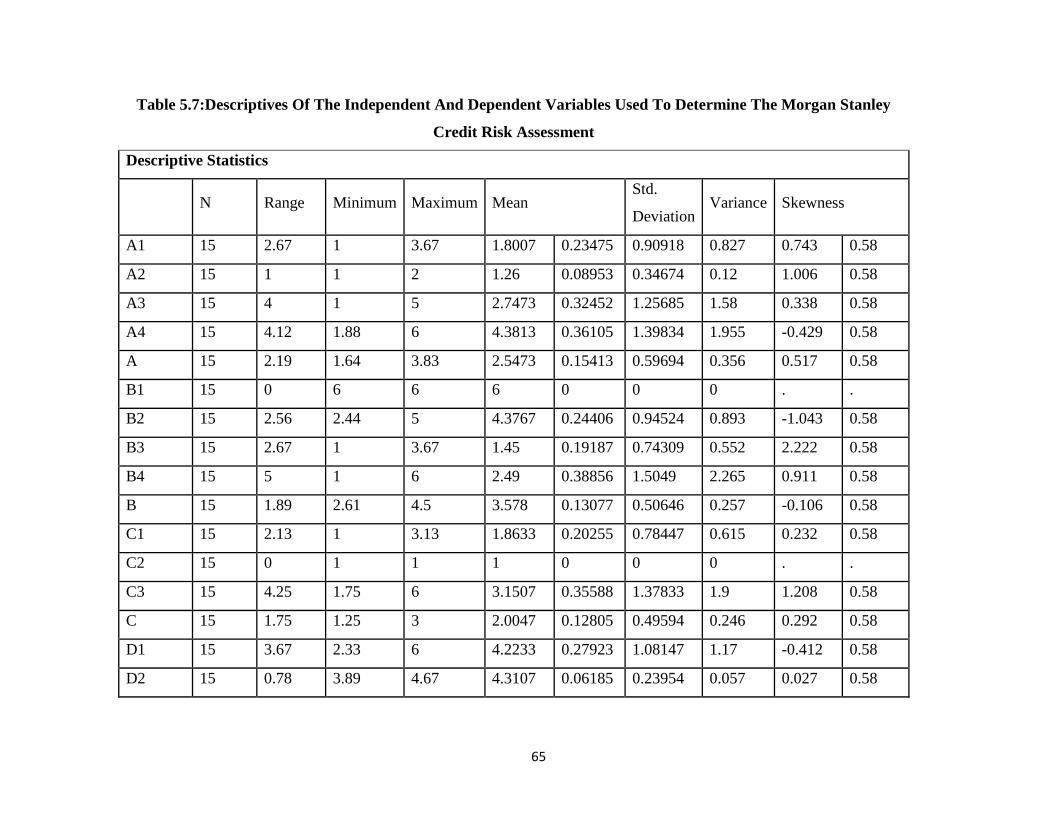

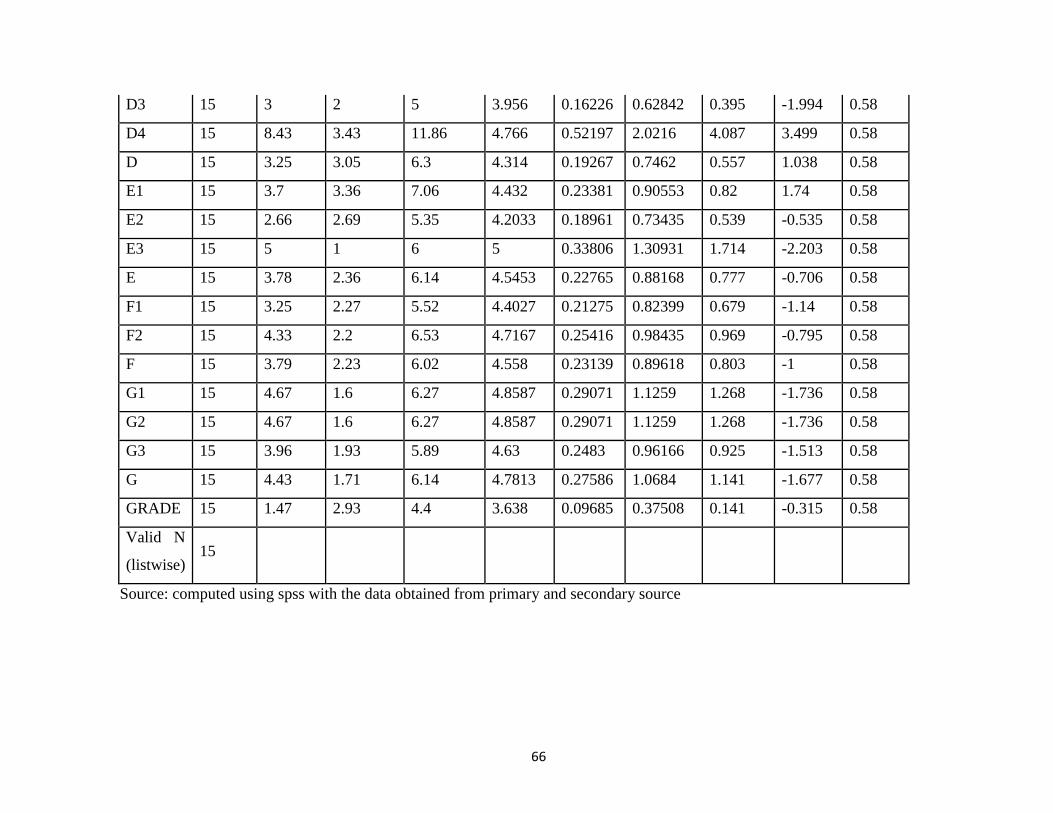

5.2.3.2 INTERPRETATION OF DESCRIPTIVE AND

CORRELATION TABLES 71

5.3 ESTIMATION METHODOLOGY 73

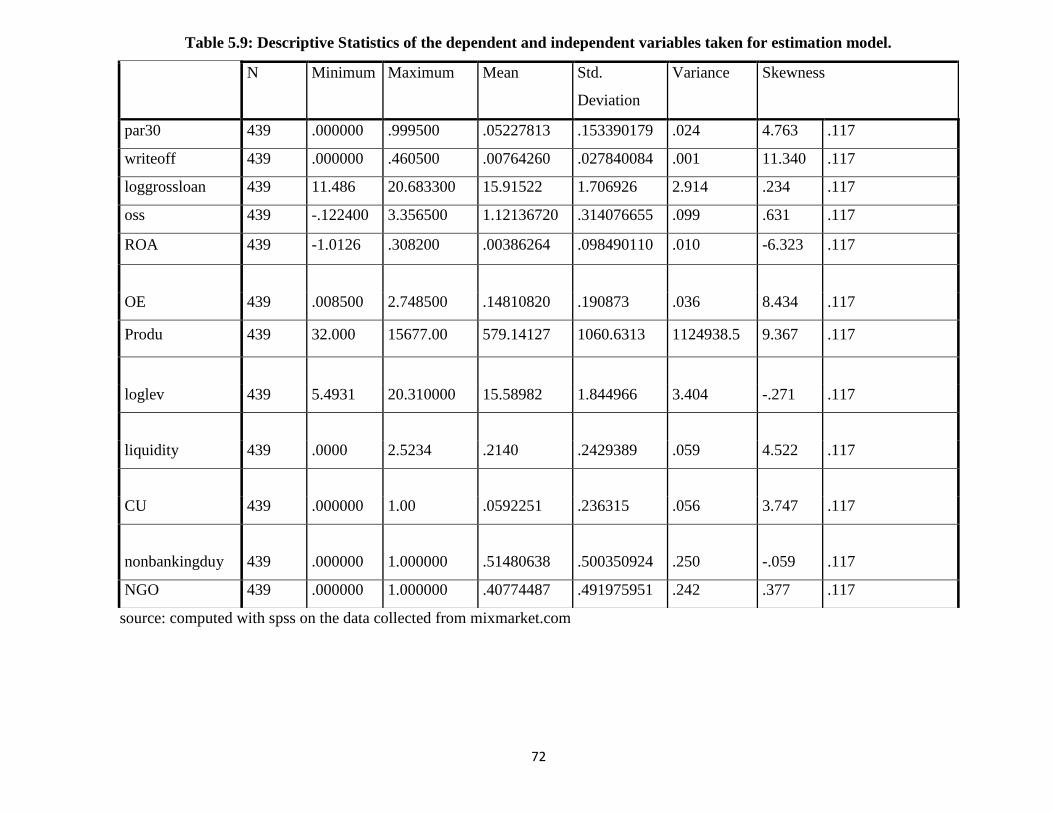

5.3.1 THE ESTIMATION METHODOLOGY 73

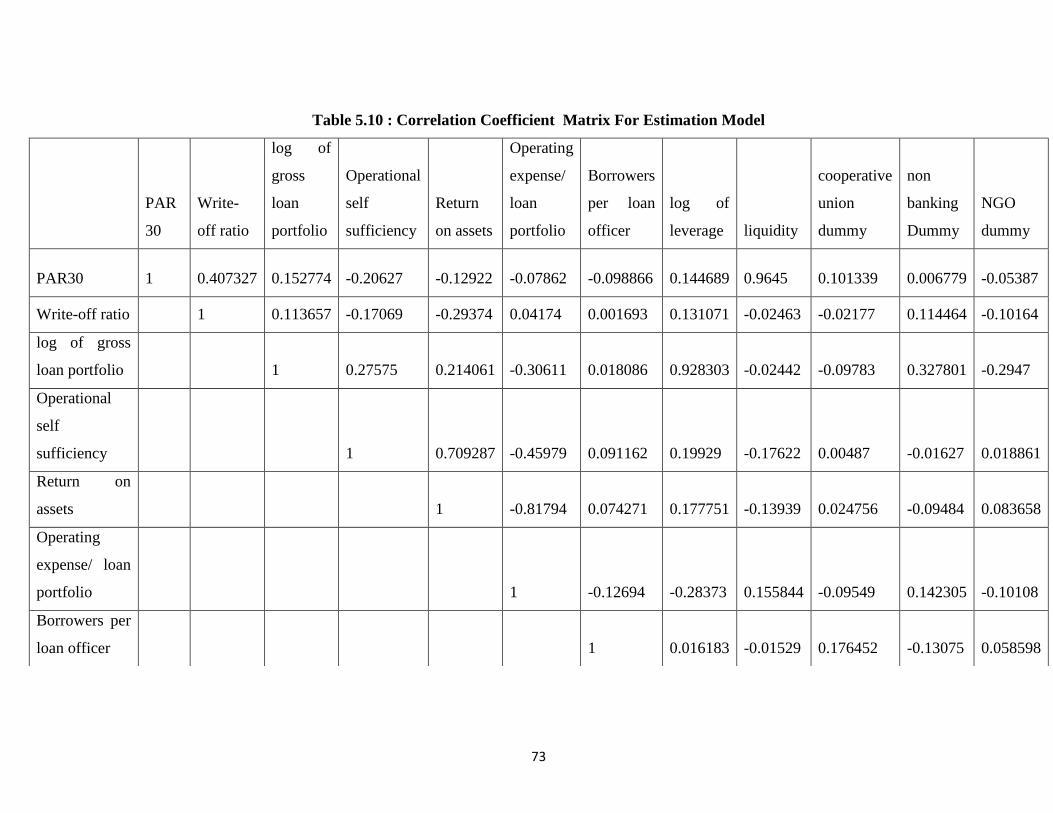

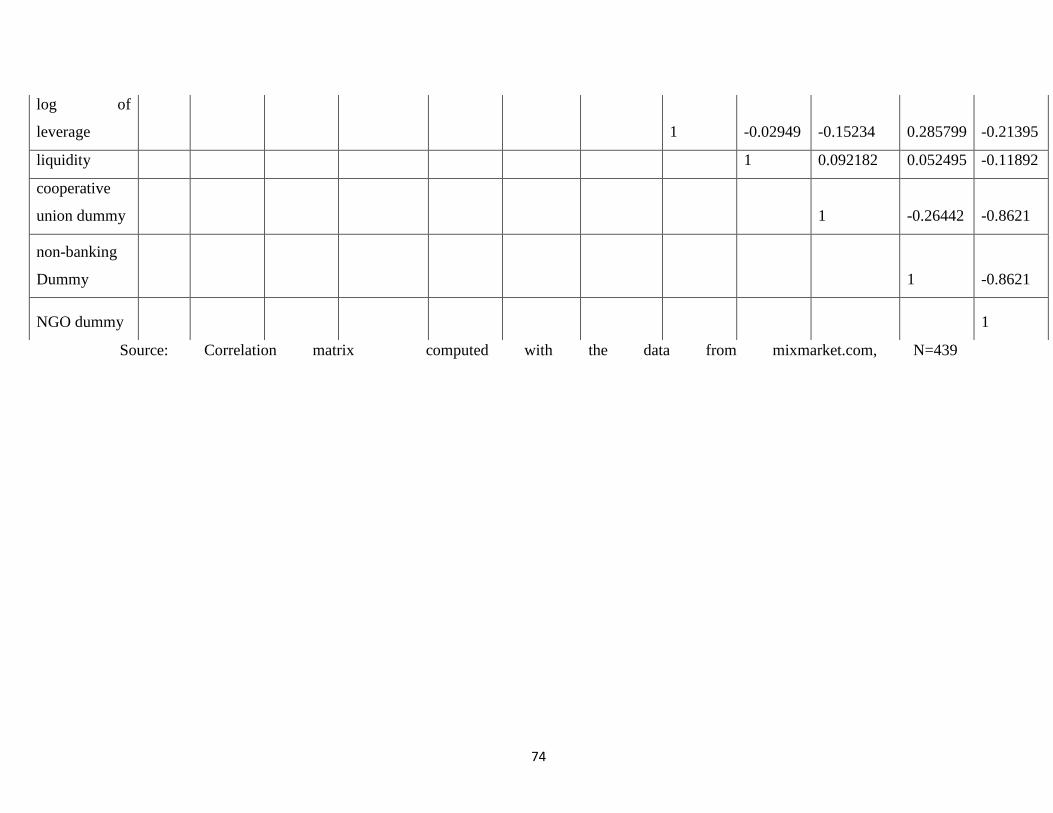

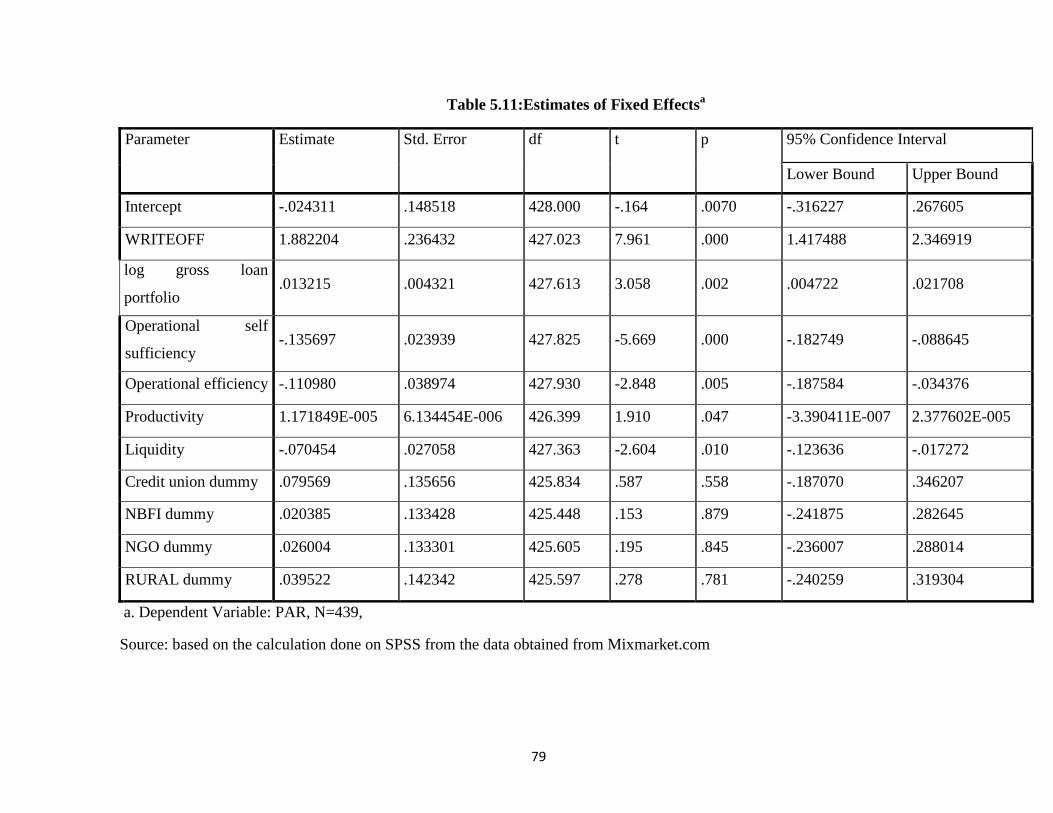

5.3.2 ANALYSIS OF THE CORRELATION MATRIX 77

5.3.3 THE RANDOM EFFECT MODEL 77

5.3.3.1 HYPOTHESIS 78

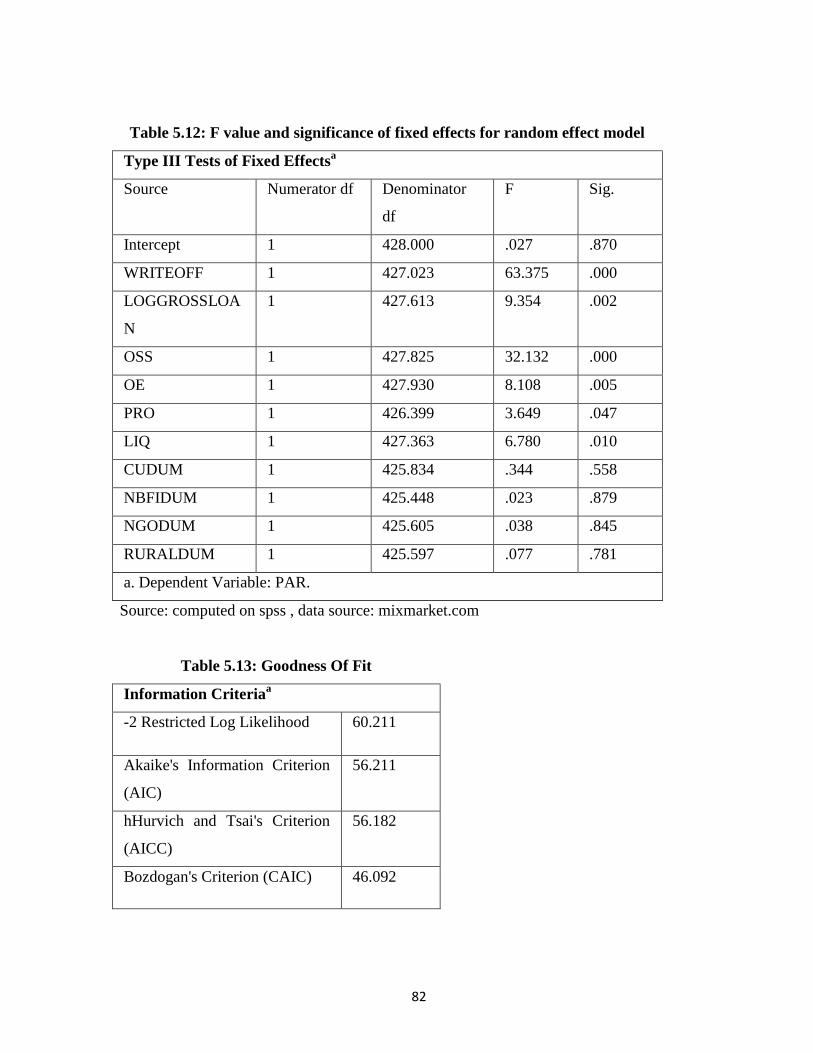

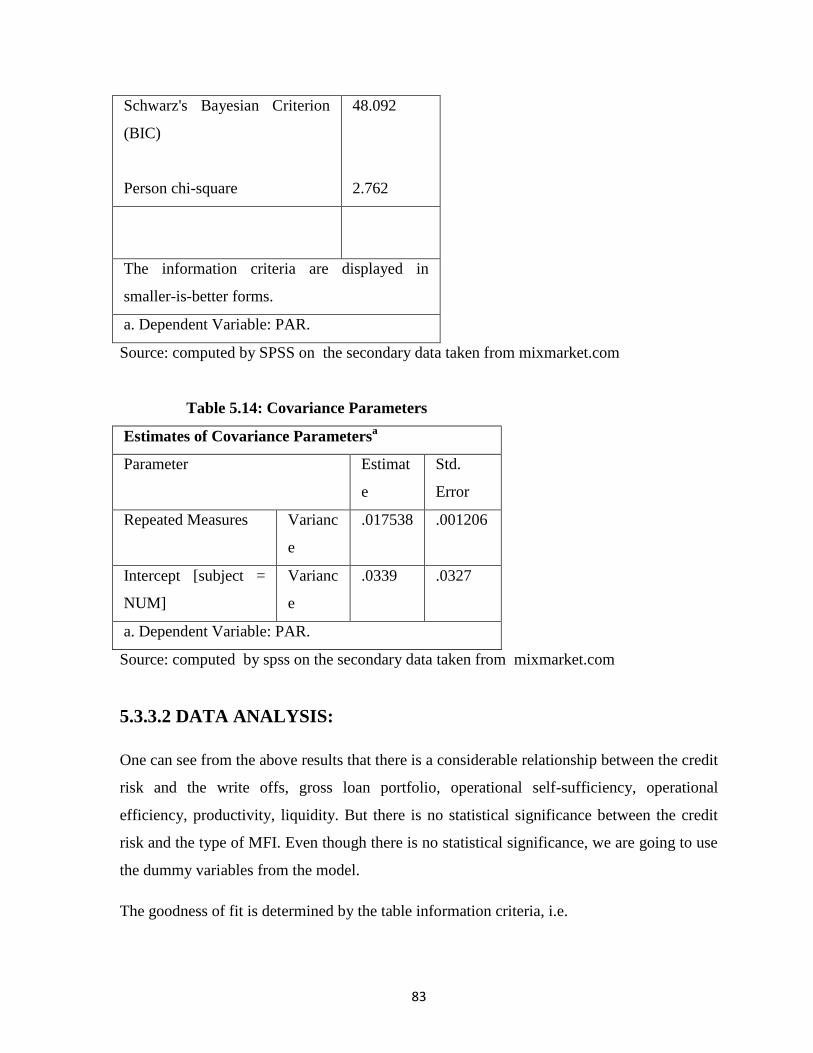

5.3.3.2 DATA ANALYSIS 83

5.3.3.3 THE RANDOM EFFECT MODEL

BUILT BY ESTIMATION METHODOLOGY 84

CHAPTER VI

FINDINGS, SUGGESTIONS AND CONCLUSION

6.1 INTRODUCTION 85

6.2 DISCUSSION OF THE FINDINGS 85

6.3 CONCLUSIONS 85

6.4 SUGGESTIONS 86

6.5 SCOPE FOR FURTHER RESEARCH 86

BIBLIOGRAPHY 87

ANNEXURES 90

ix

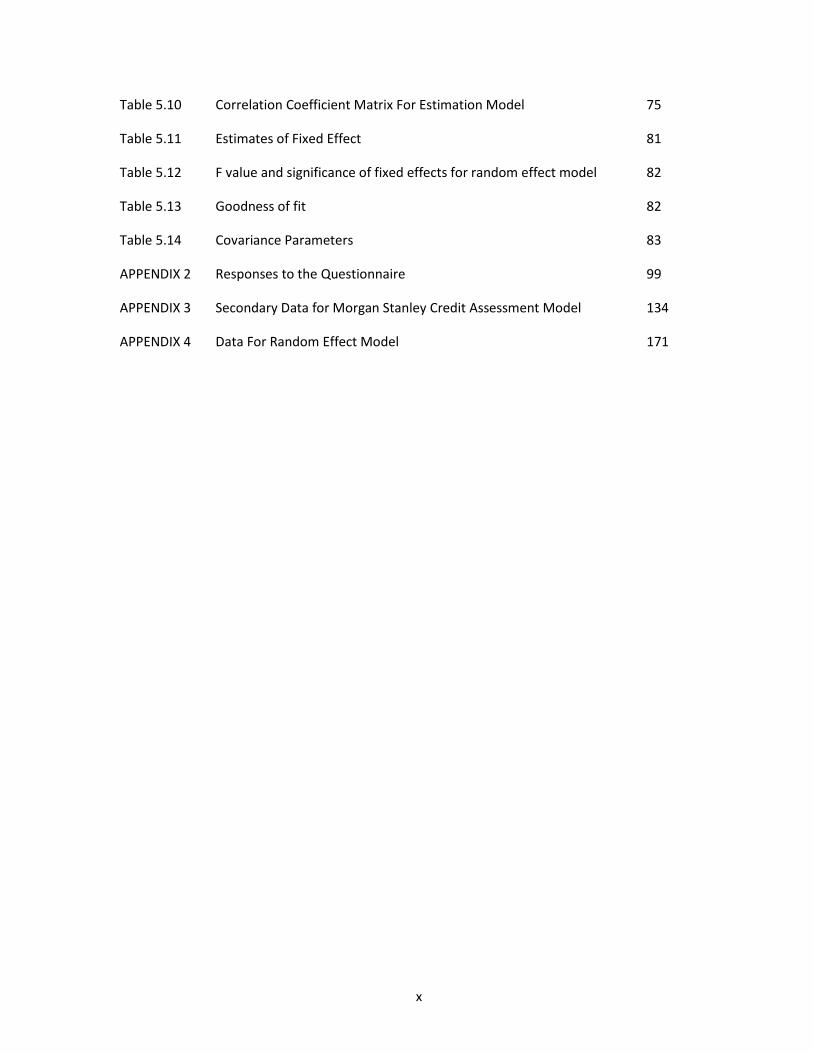

LIST OF TABLES

Table 1.1 Phases of microfinance 4

Table 1.2 Risk categories 5

Table 2.1 Major risks to microfinance institutions 9

Table 2.2 Classification of the microfinance industry 10

Table 2.3 Morgan Stanley credit assessment model 13

Table 2.4 Ratings of microfinance institutions 17

Table 2.5 Camel's indicators 24

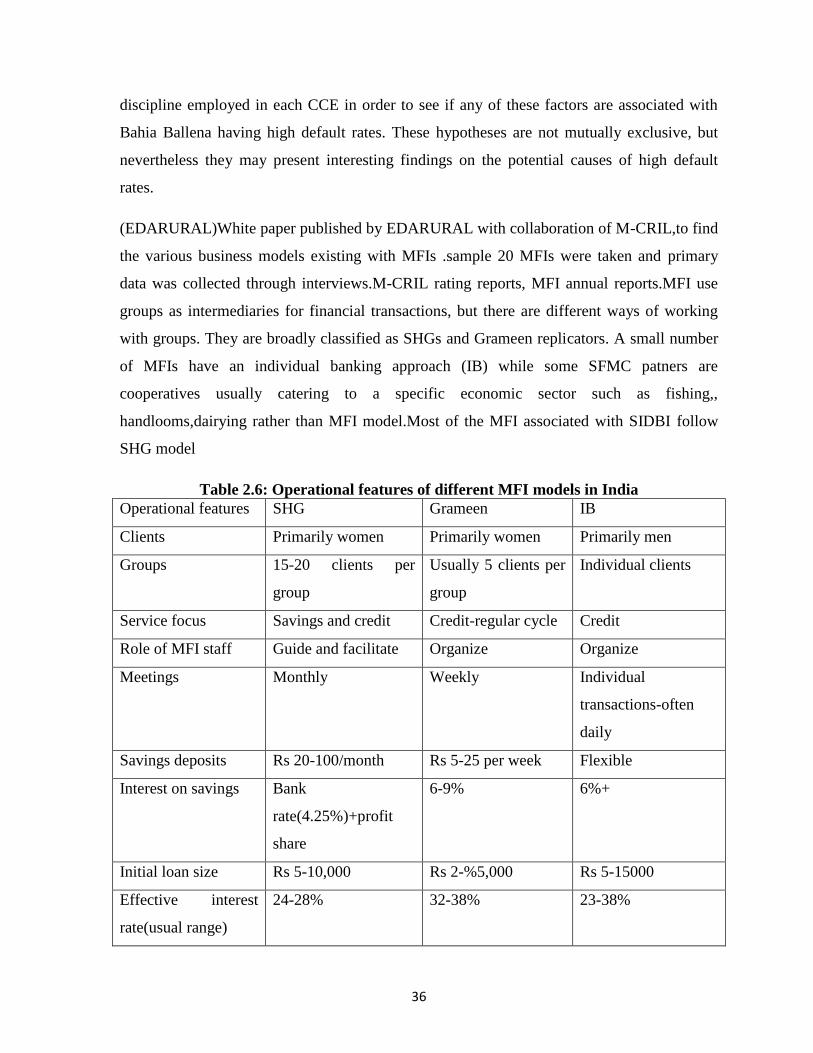

Table 2.6 Operational features of different MFI models in India 36

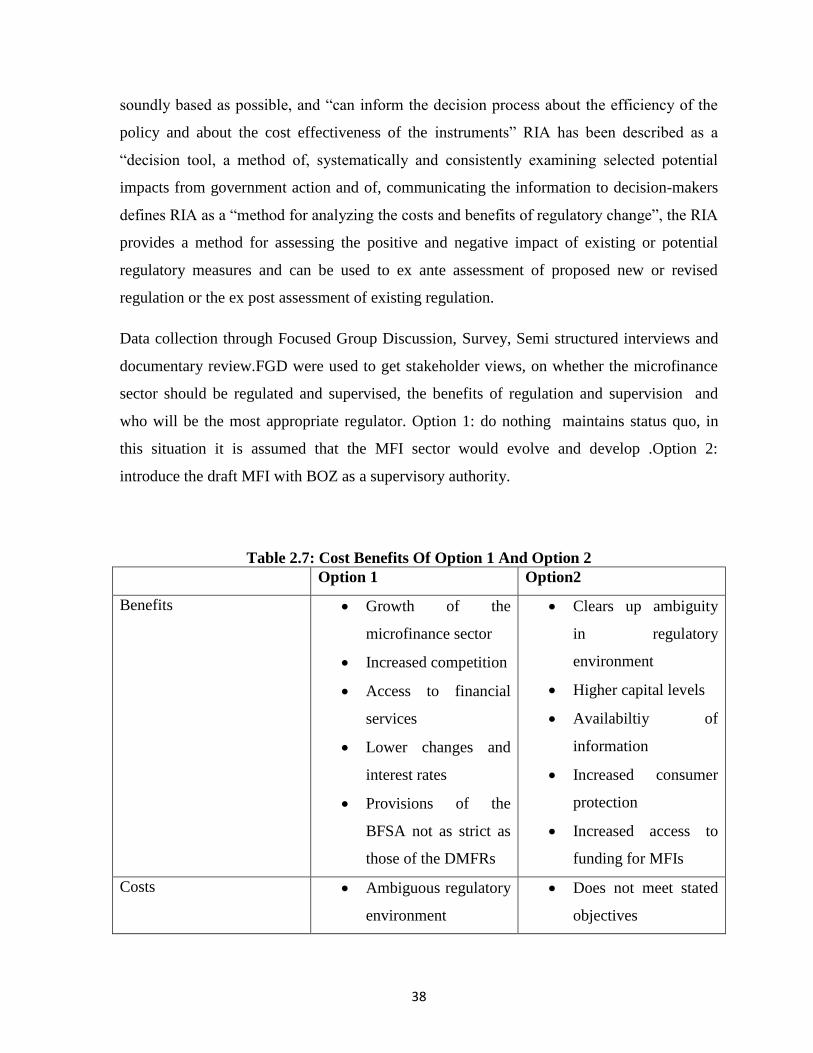

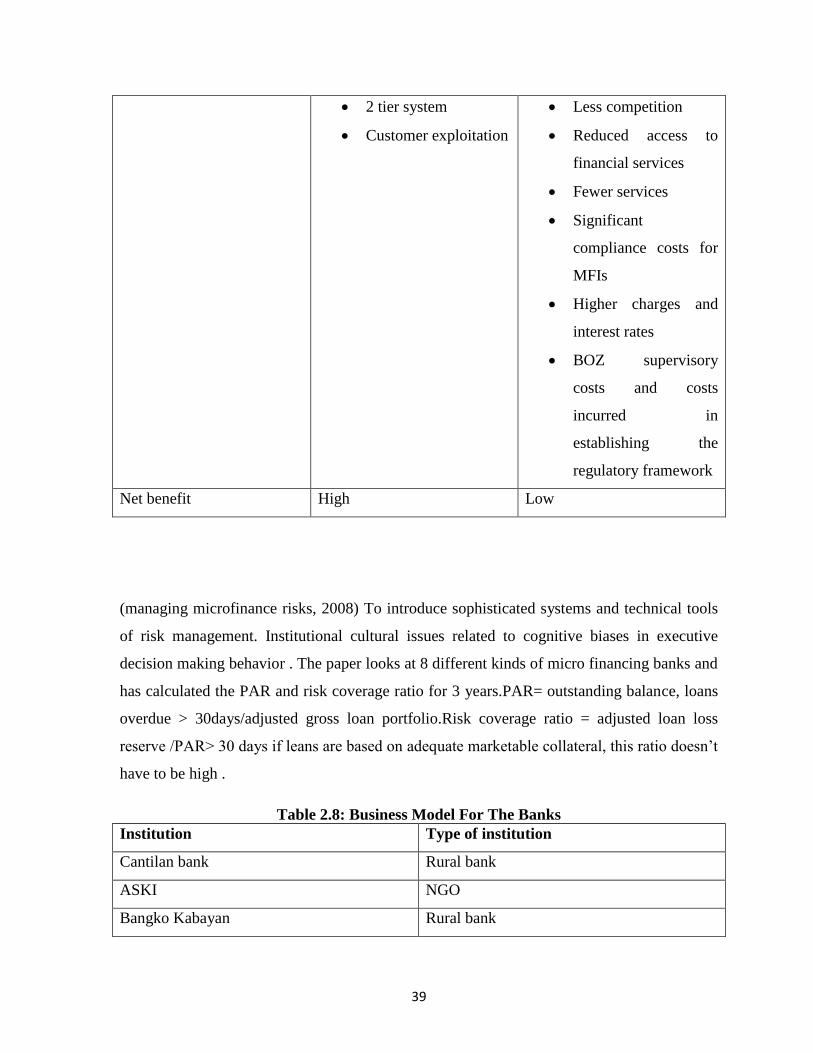

Table 2.7 Cost Benefits Of Option 1 and Option 2 38

Table 2.8 Business Model For The Banks 39

Table 3.1 Morgan Stanley credit assessment model 46

Table 5.1 Morgan Stanley credit assessment model 55

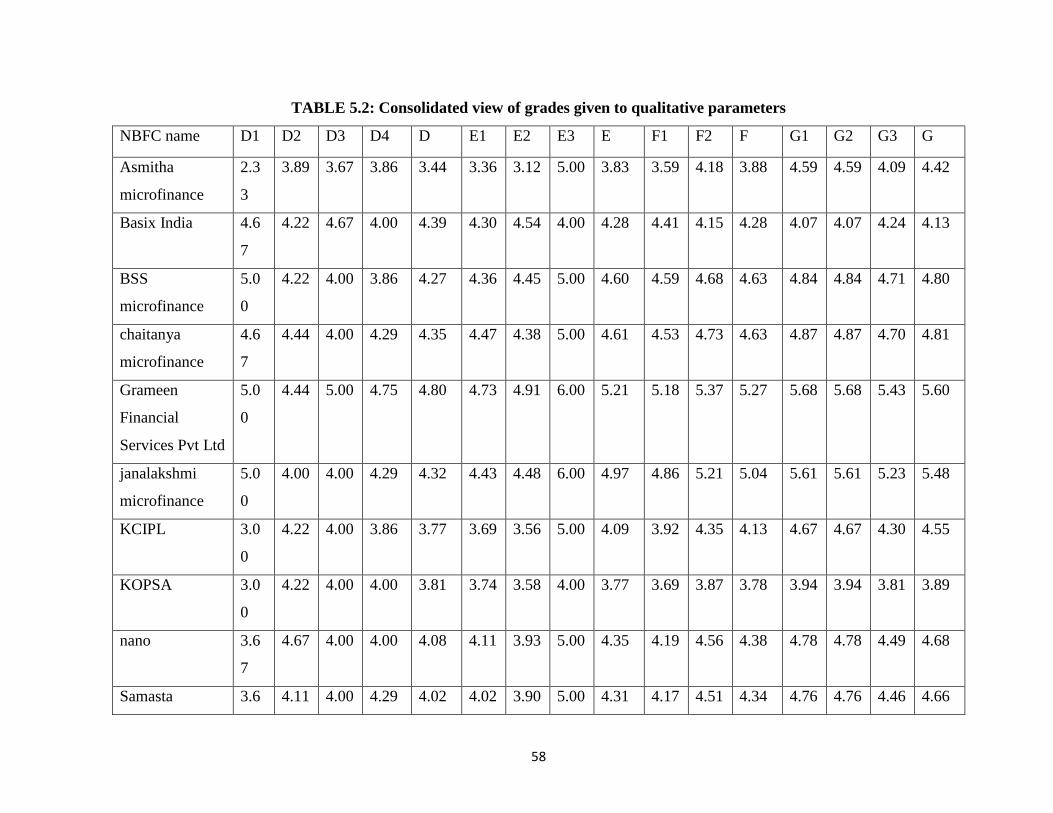

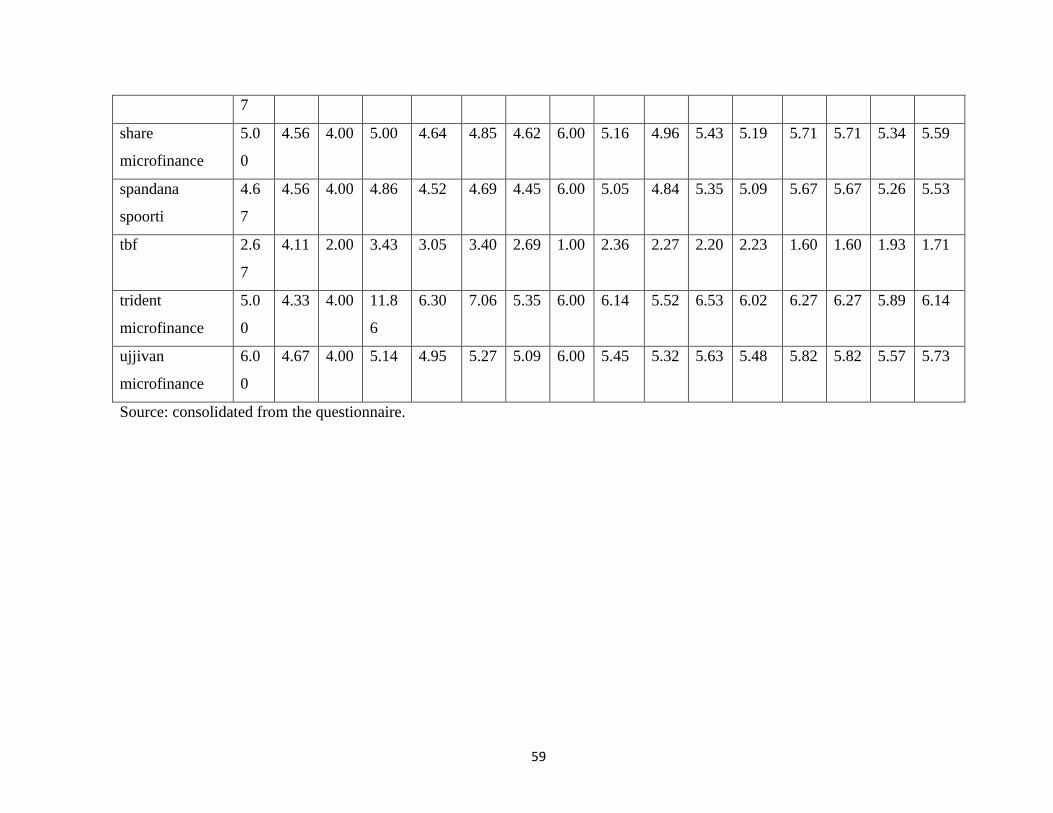

Table 5.2 consolidated view of grades given to qualitative parameters 60

Table 5.3 The Cronbach's Alpha Test 62

Table 5.4 consolidated view of grades given to quantitative parameters 64

Table 5.5 Morgan Stanley Credit Risk Assessment 65

Table 5.6 Final grades given obtained from the 65

Morgan Stanley credit risk Assessment

Table 5.7 Descriptive of the Independent And Dependent Variable 67

Used to Determine The Morgan Stanley Credit Risk Assessment

Table 5.8 Pearson Correlation between the parameter used in

Morgan Stanley credit risk assessment 69

Table 5.9 Descriptive of the Independent And

Dependent Variable Used to Determine Estimation Model 74

x

Table 5.10 Correlation Coefficient Matrix For Estimation Model 75

Table 5.11 Estimates of Fixed Effect 81

Table 5.12 F value and significance of fixed effects for random effect model 82

Table 5.13 Goodness of fit 82

Table 5.14 Covariance Parameters 83

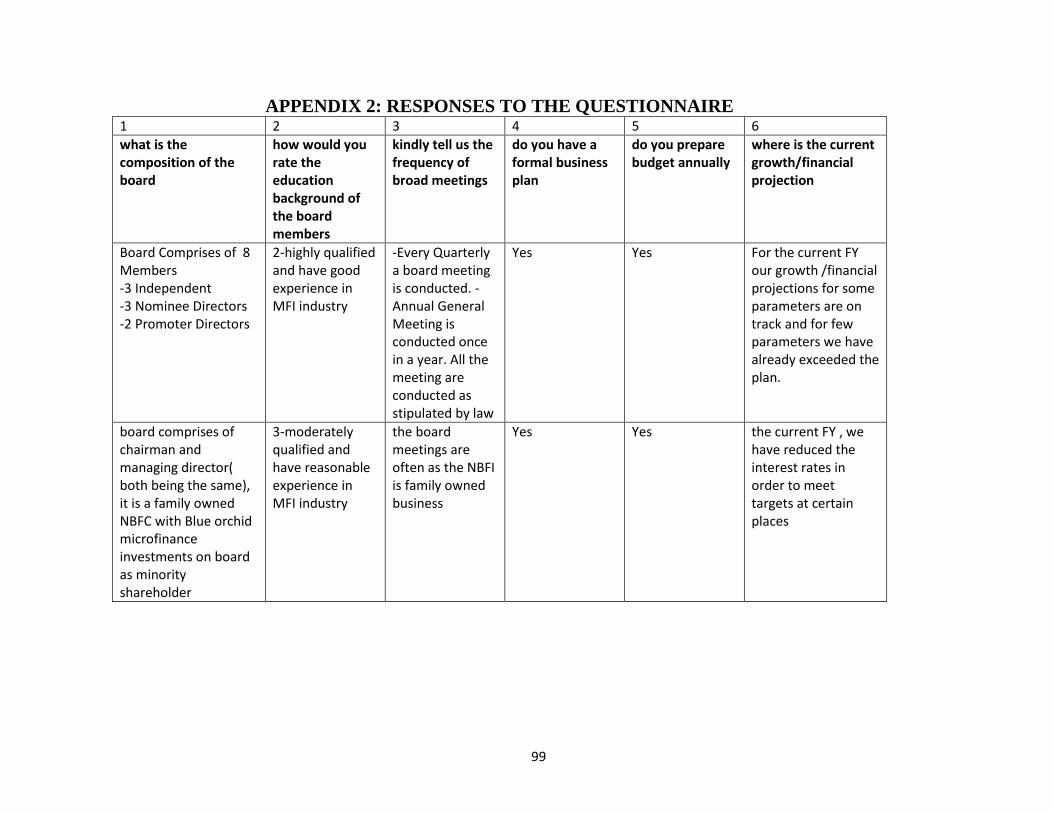

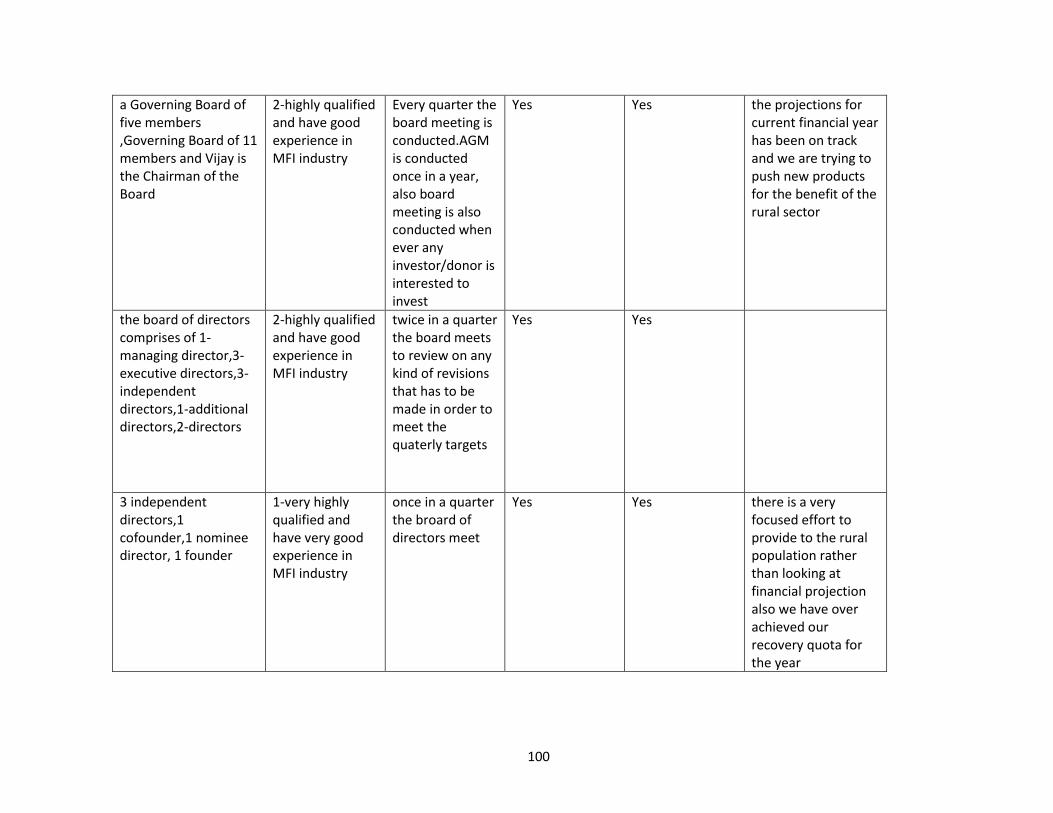

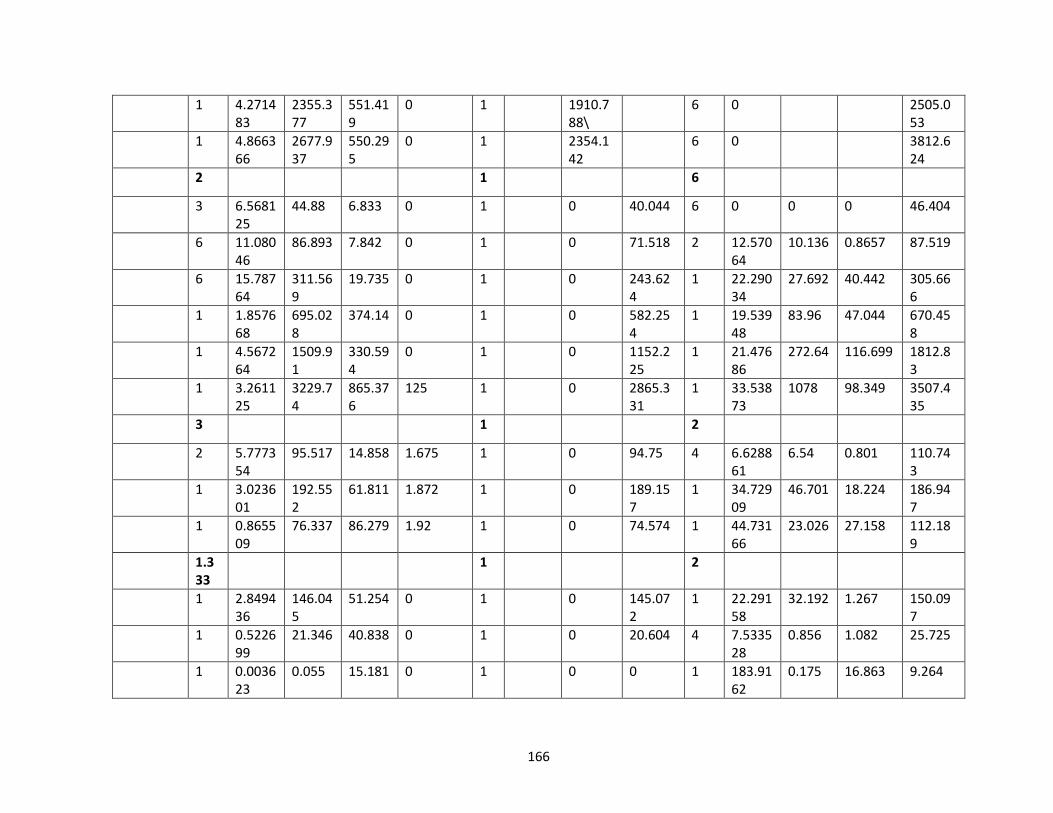

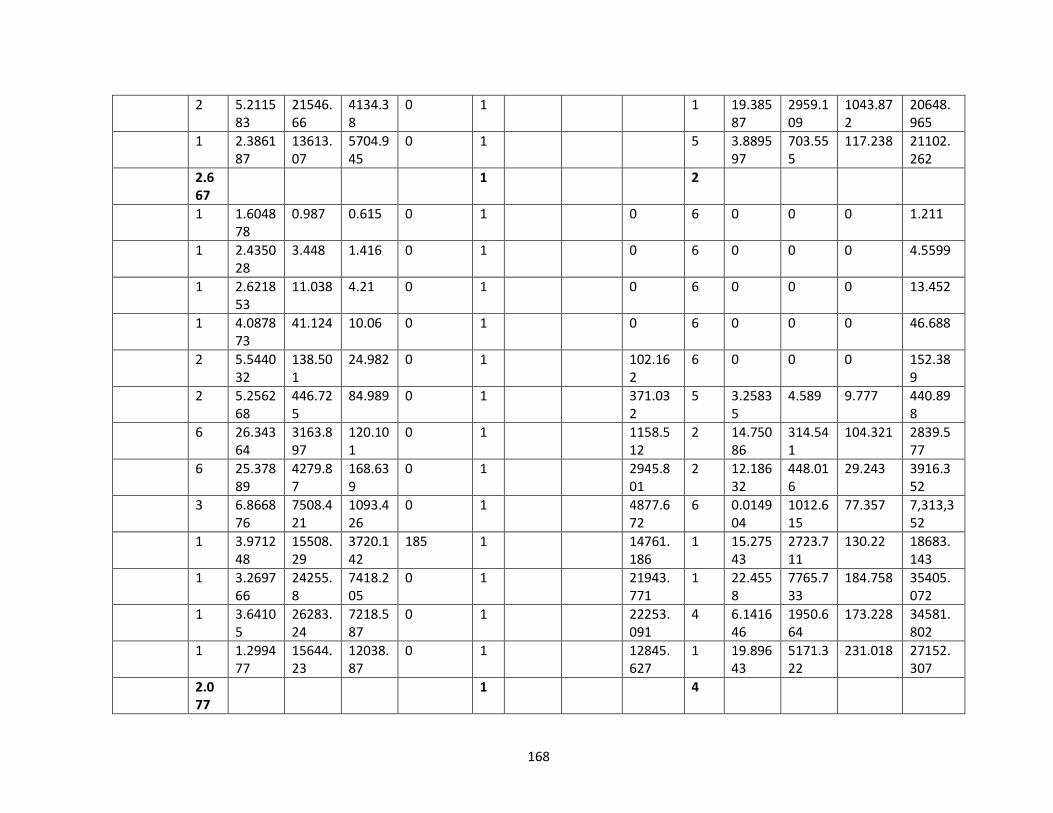

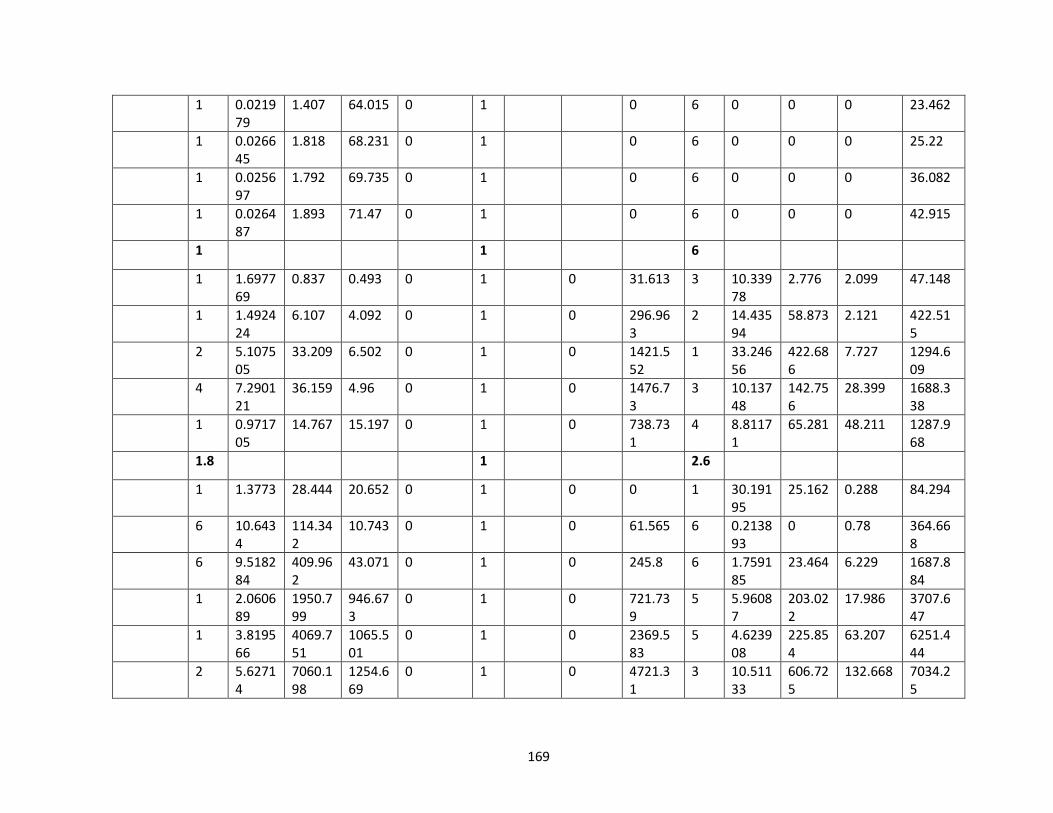

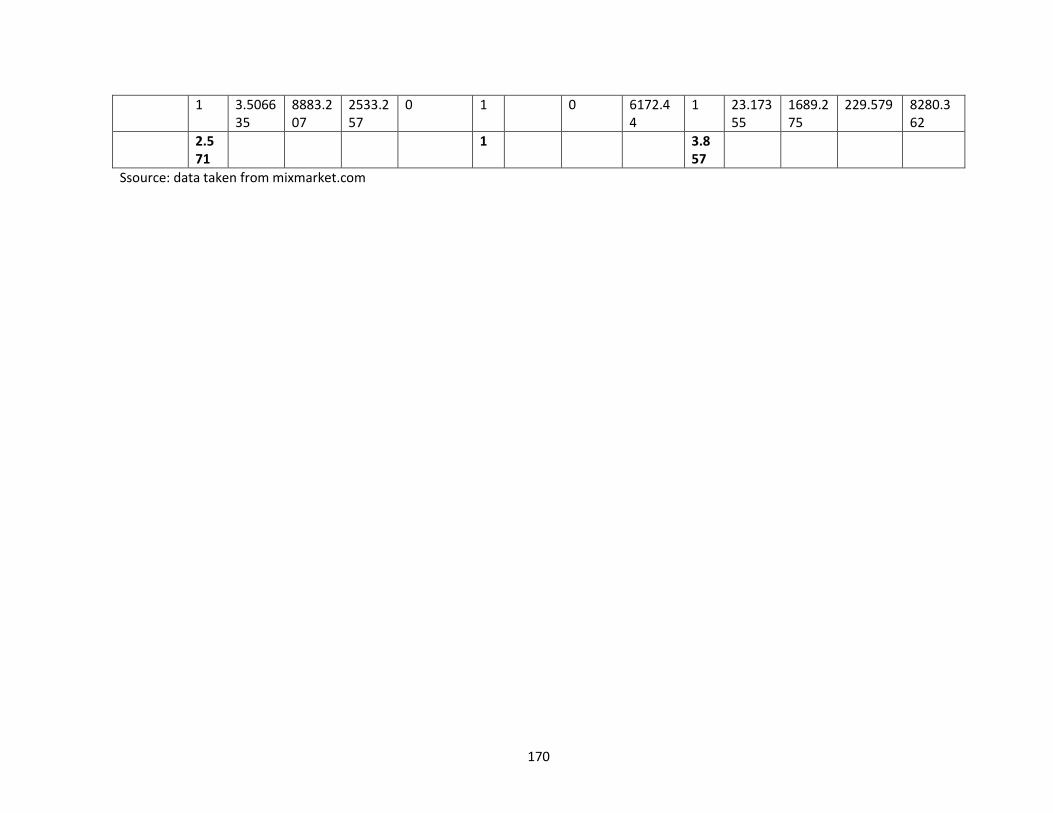

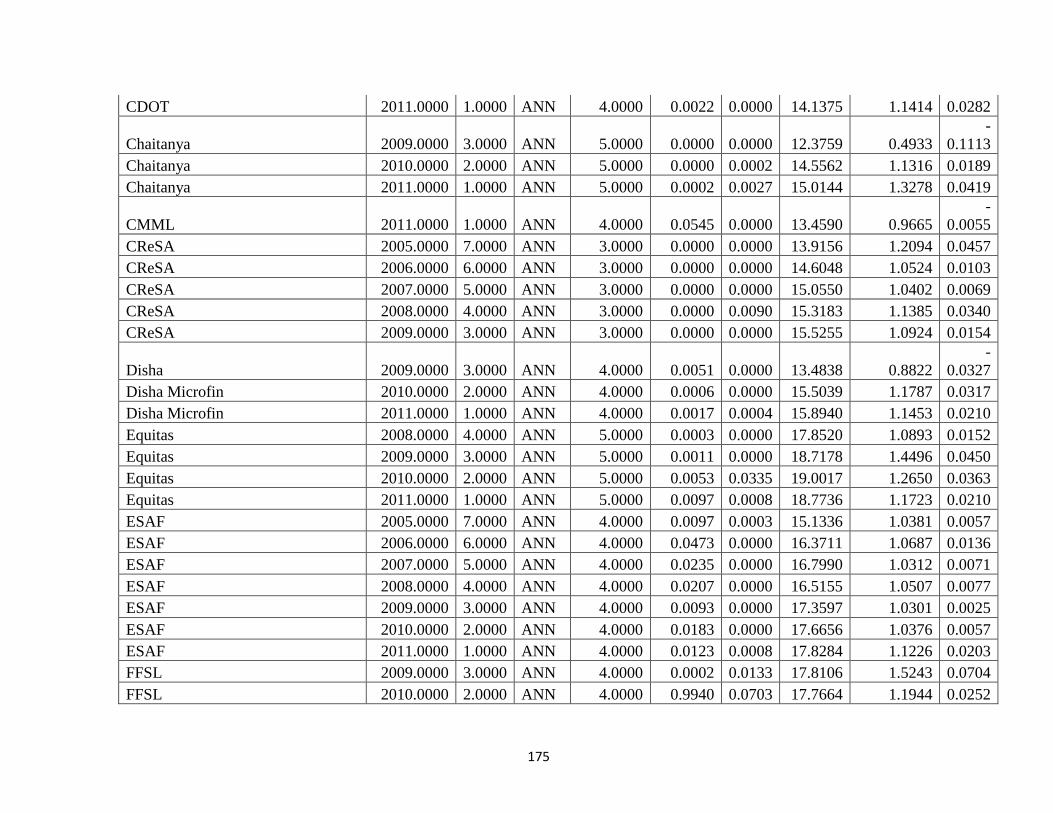

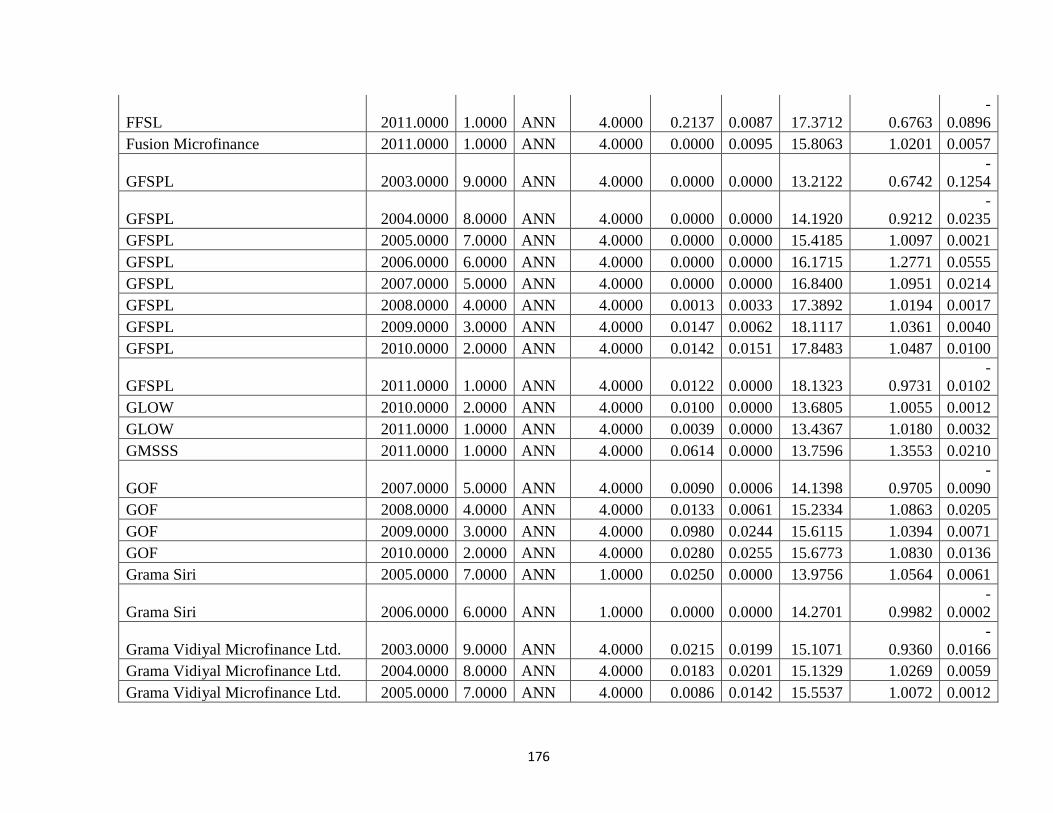

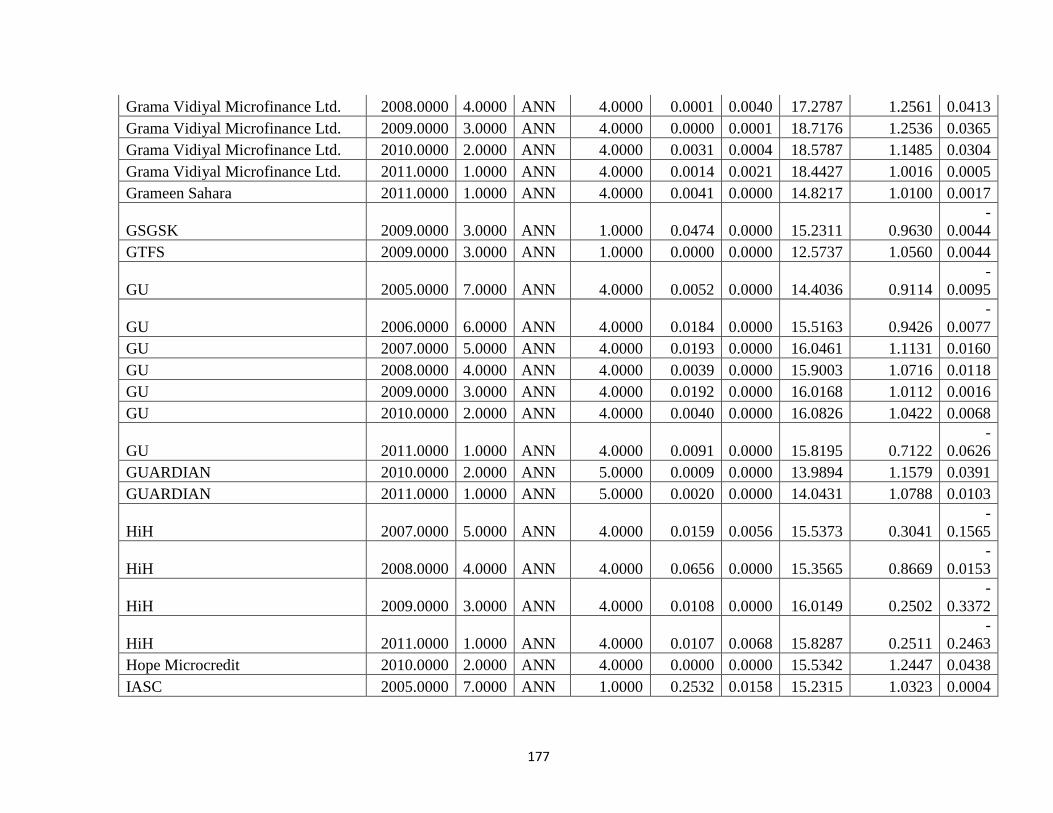

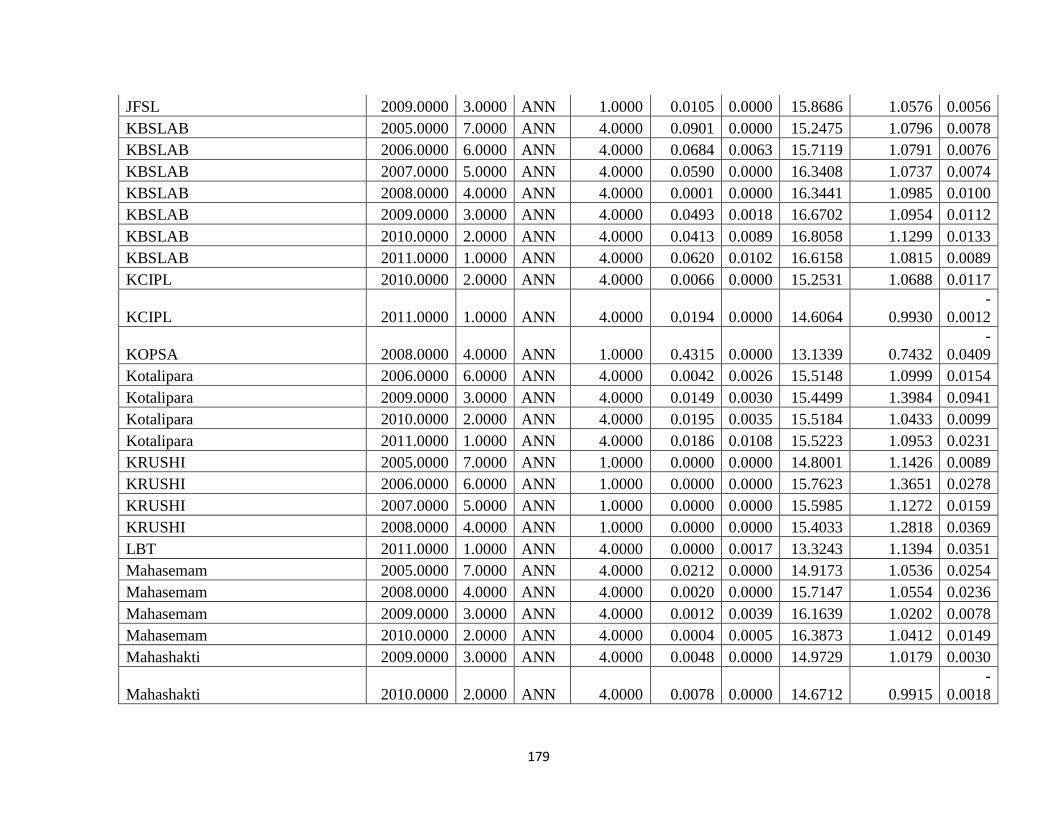

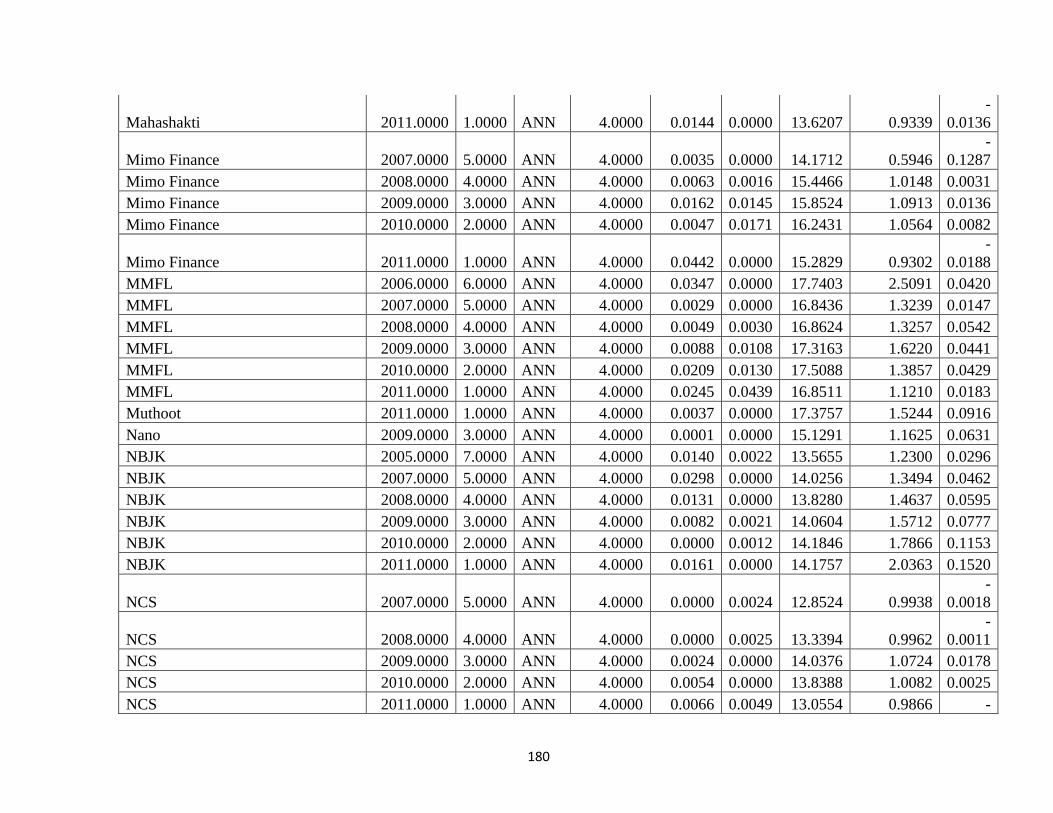

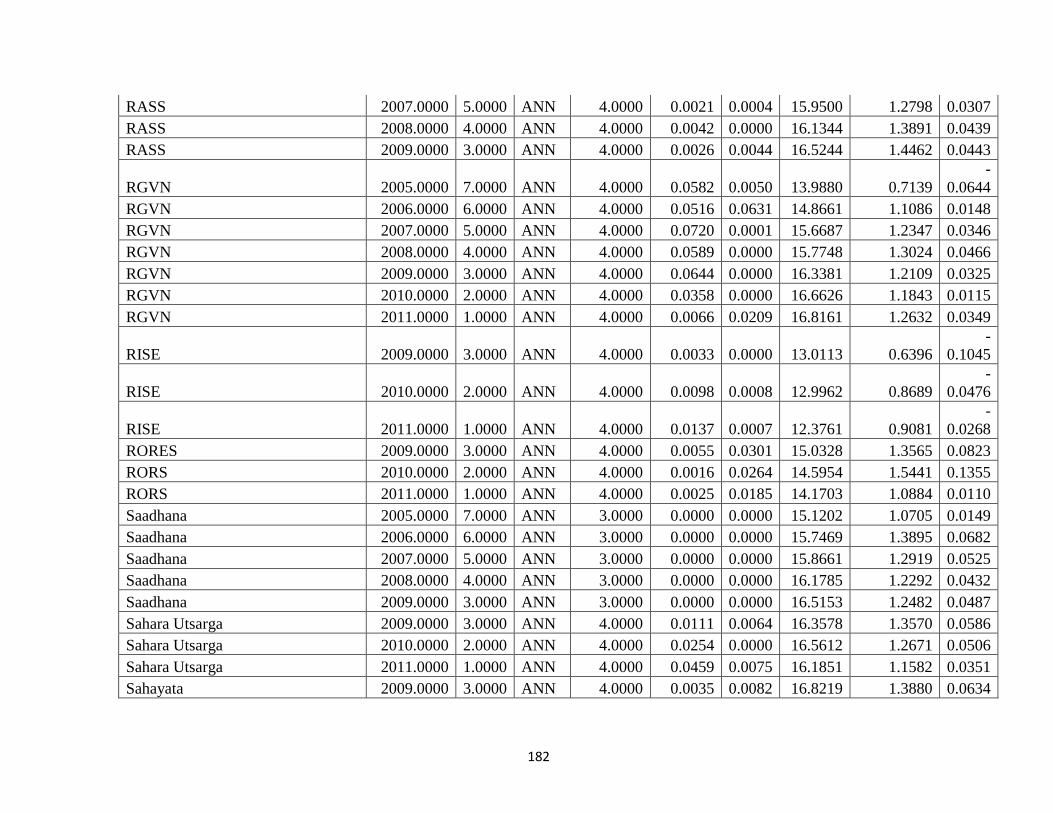

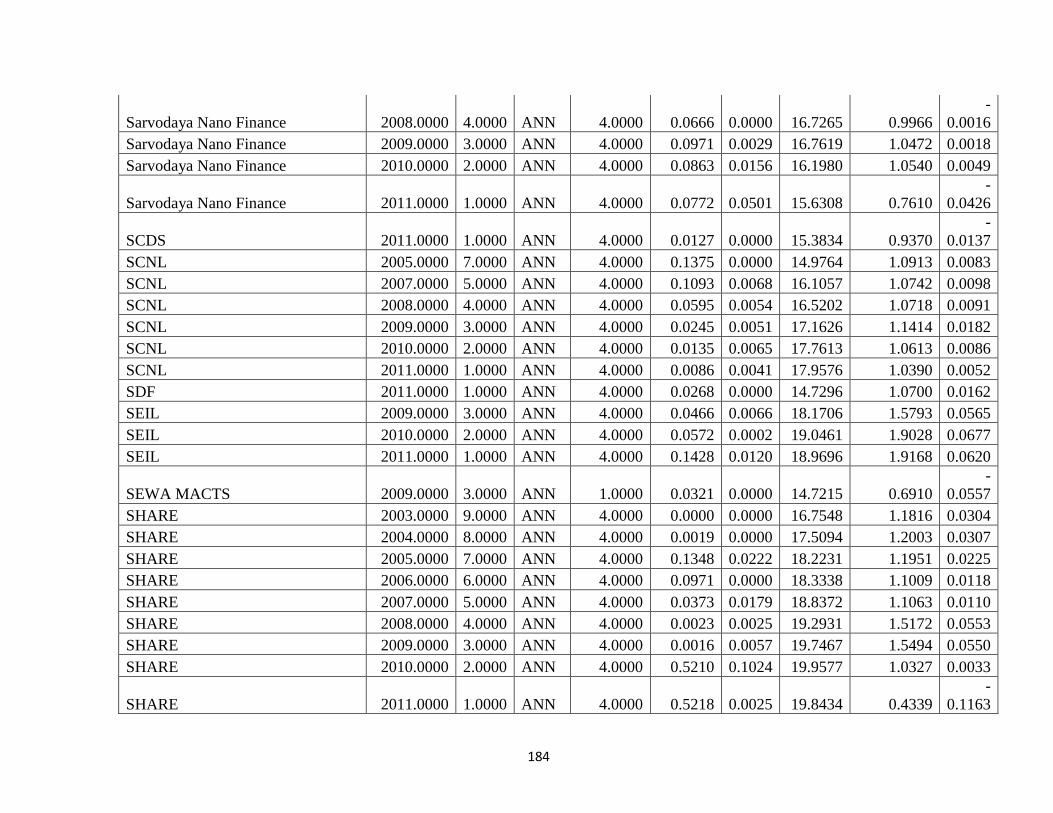

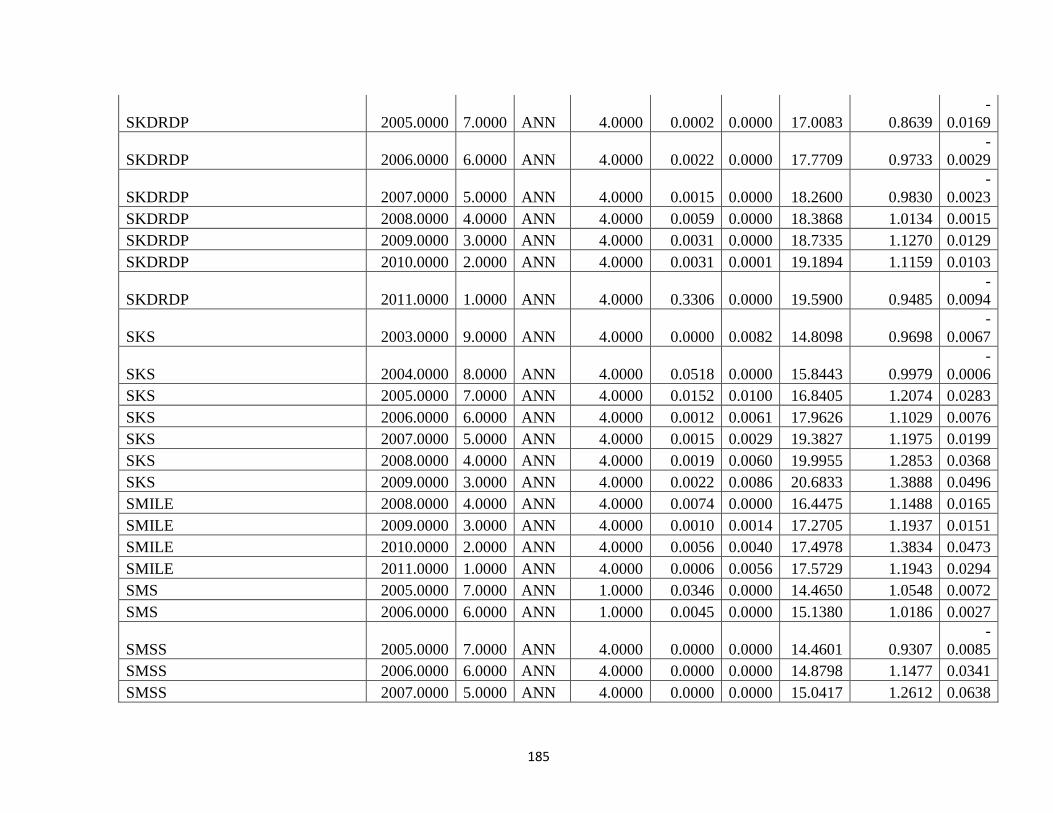

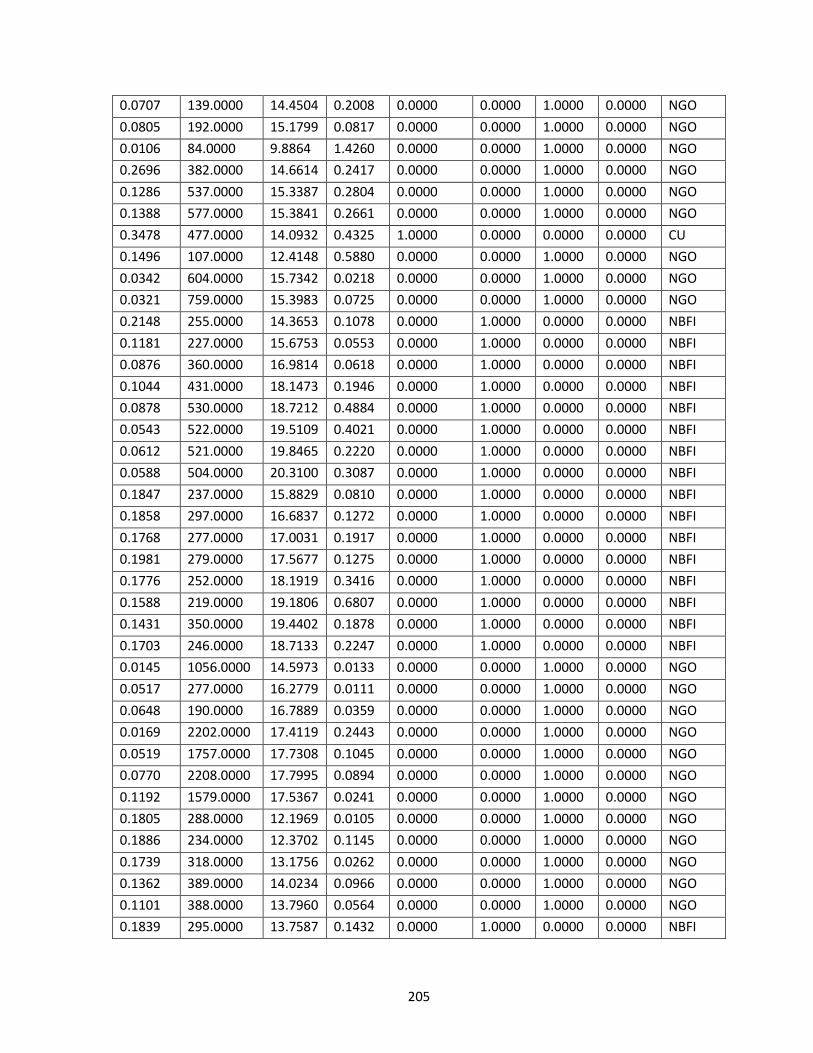

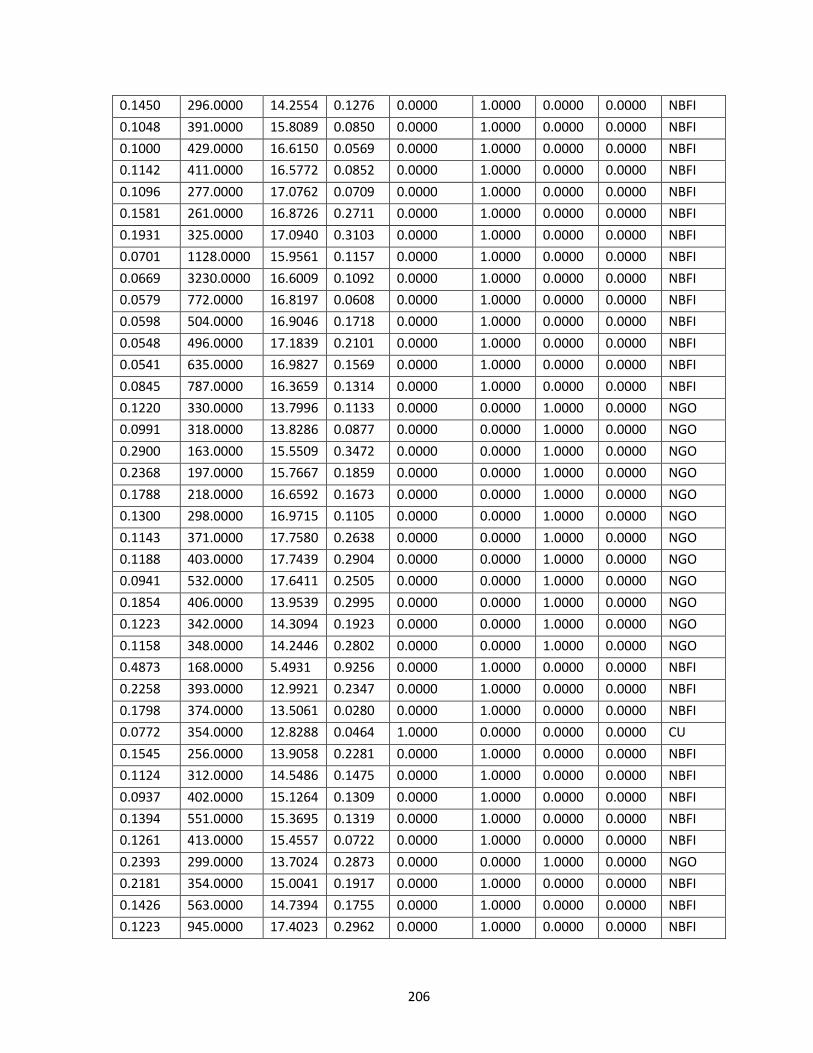

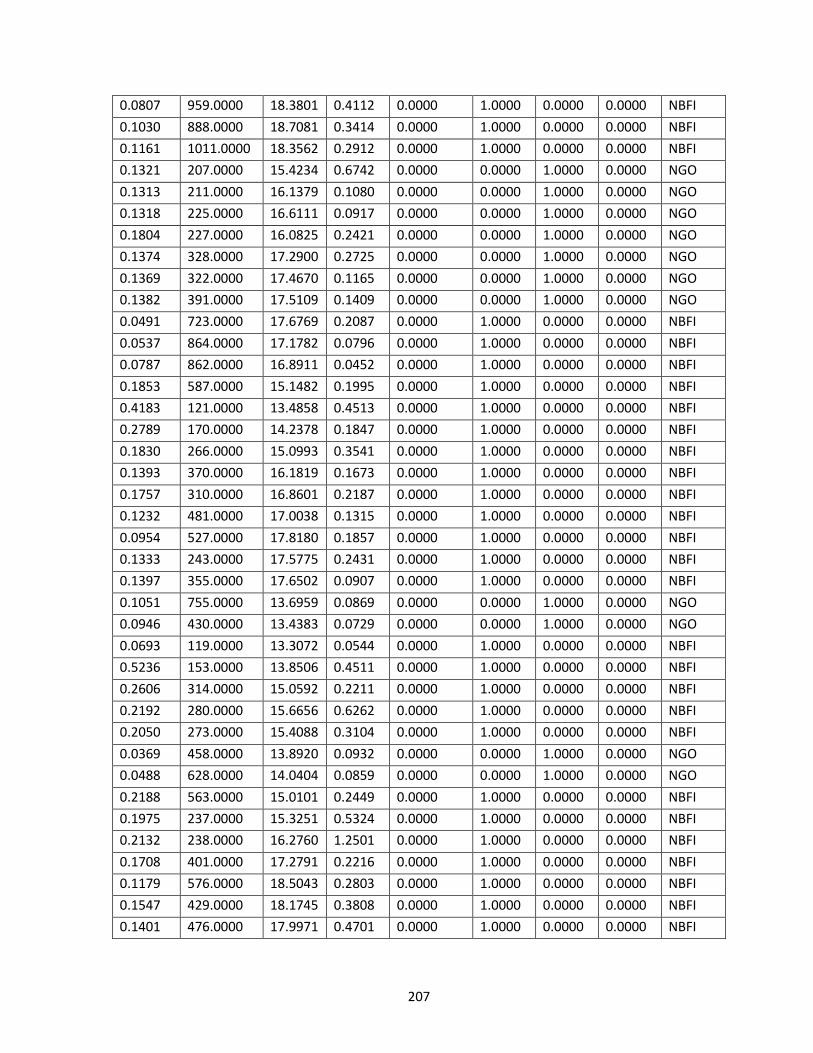

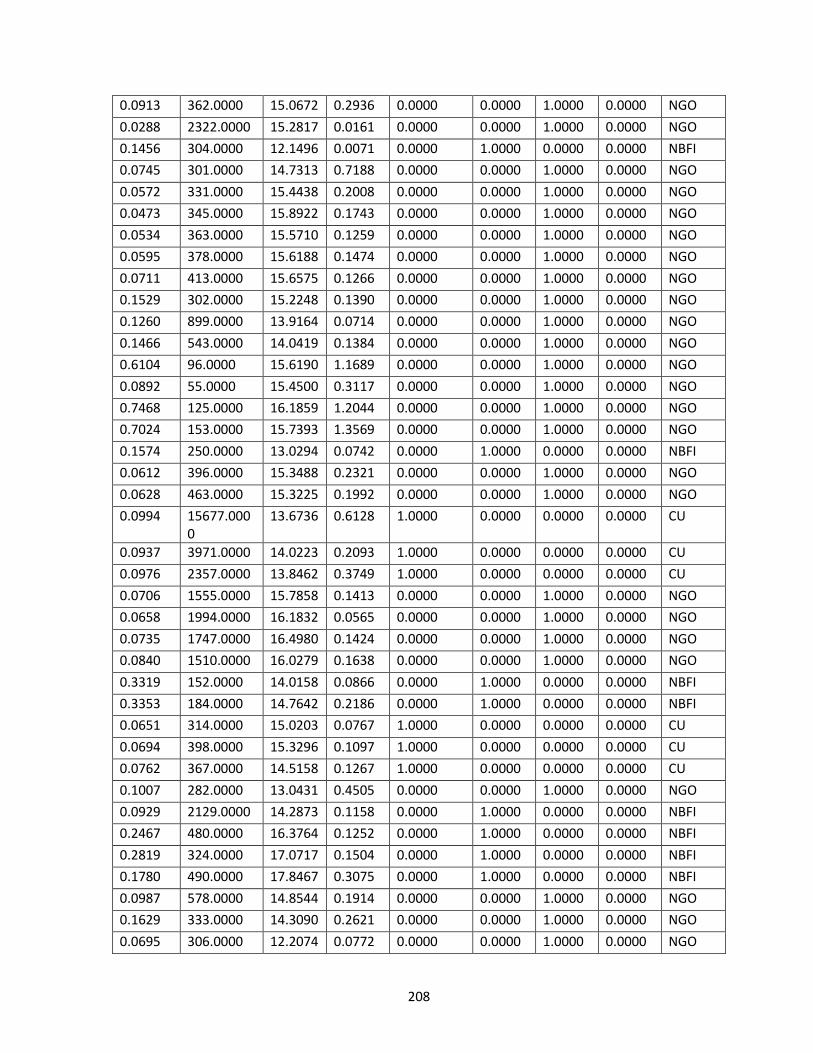

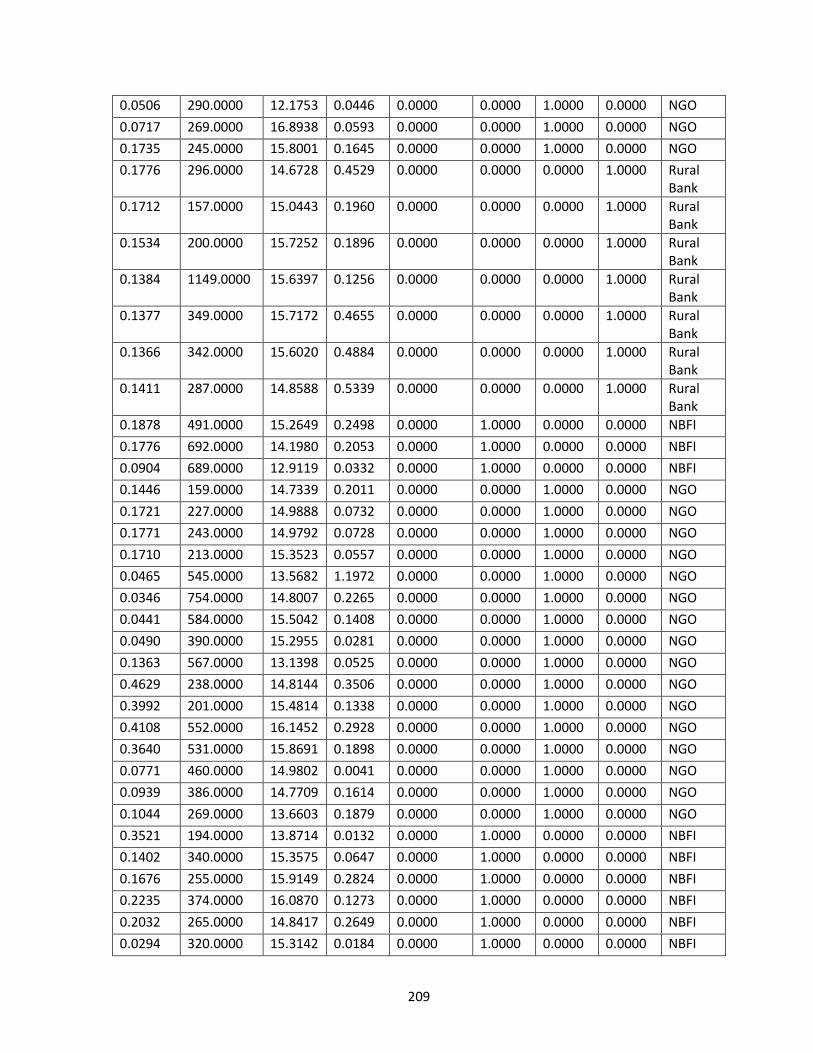

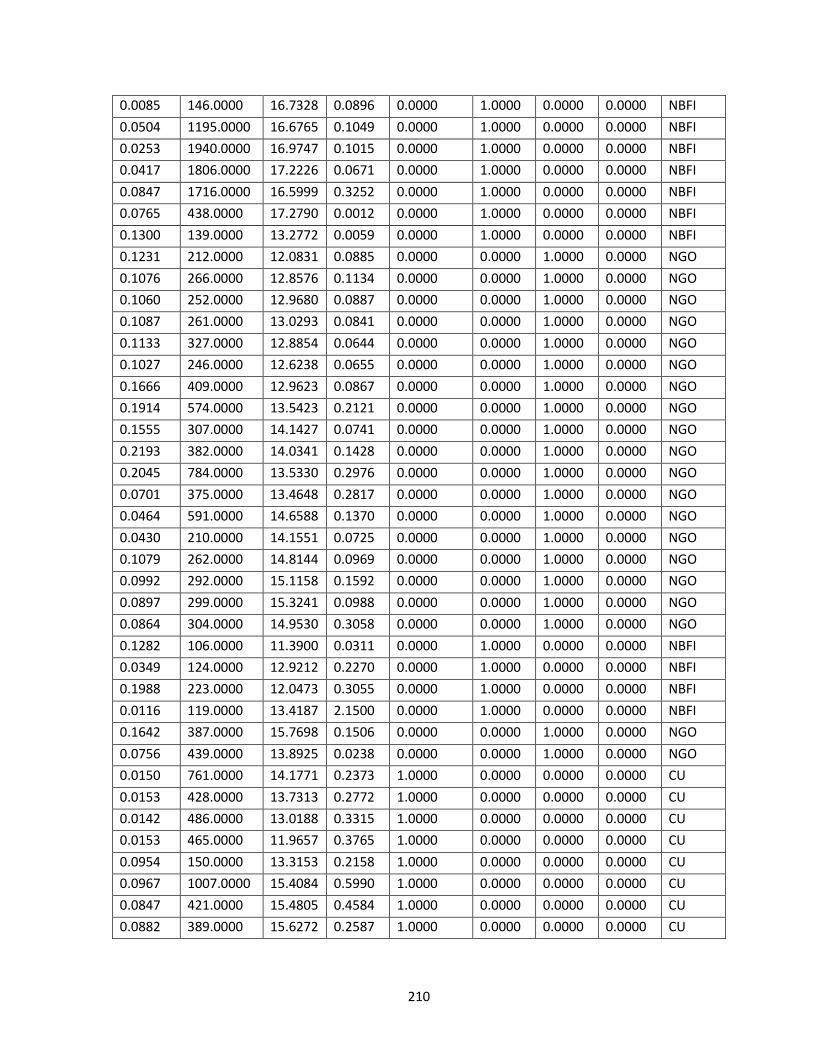

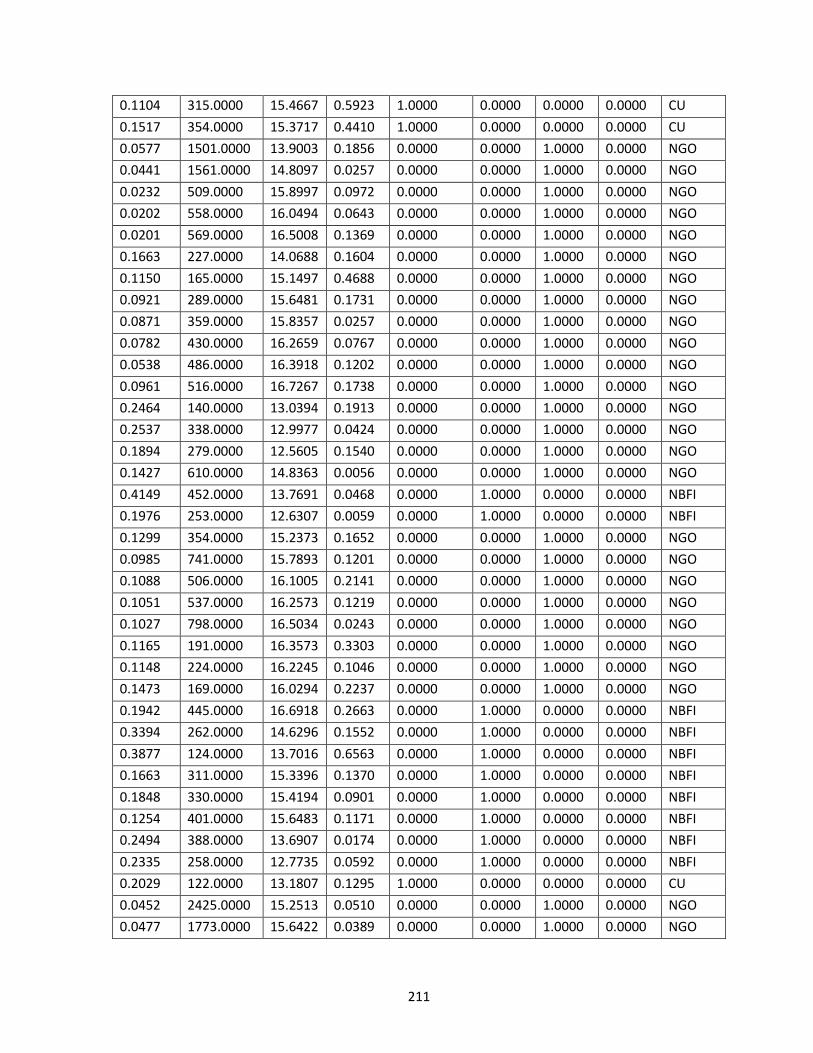

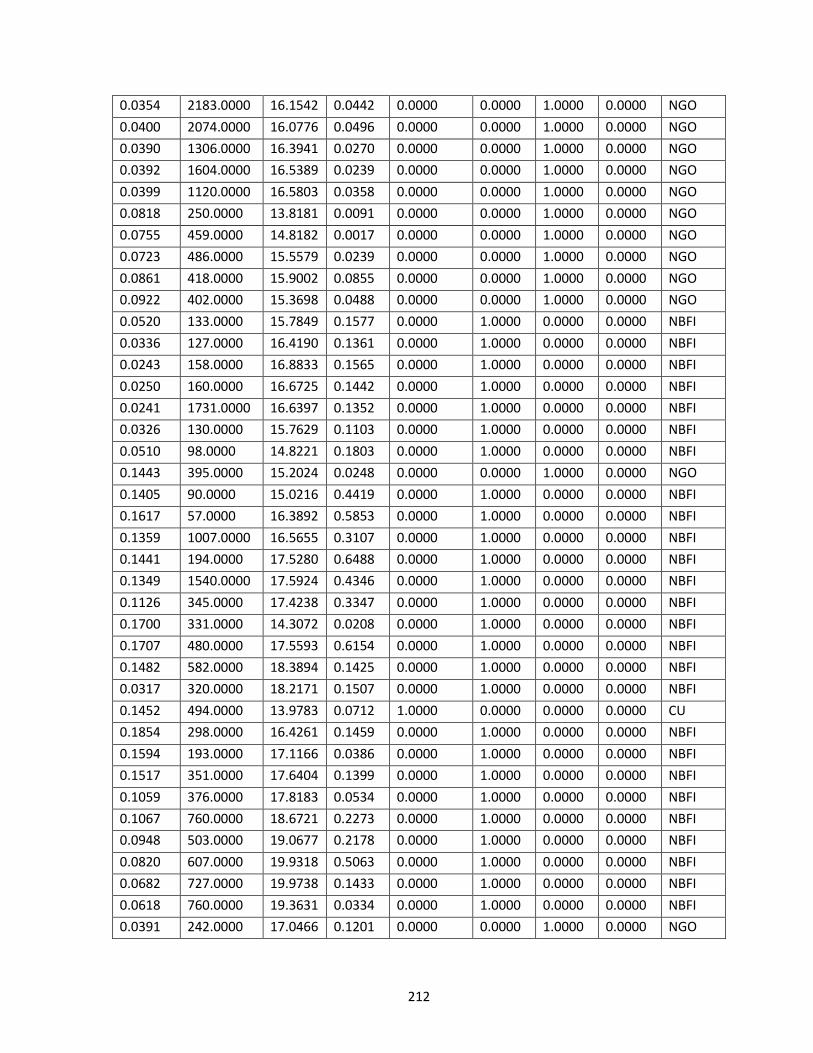

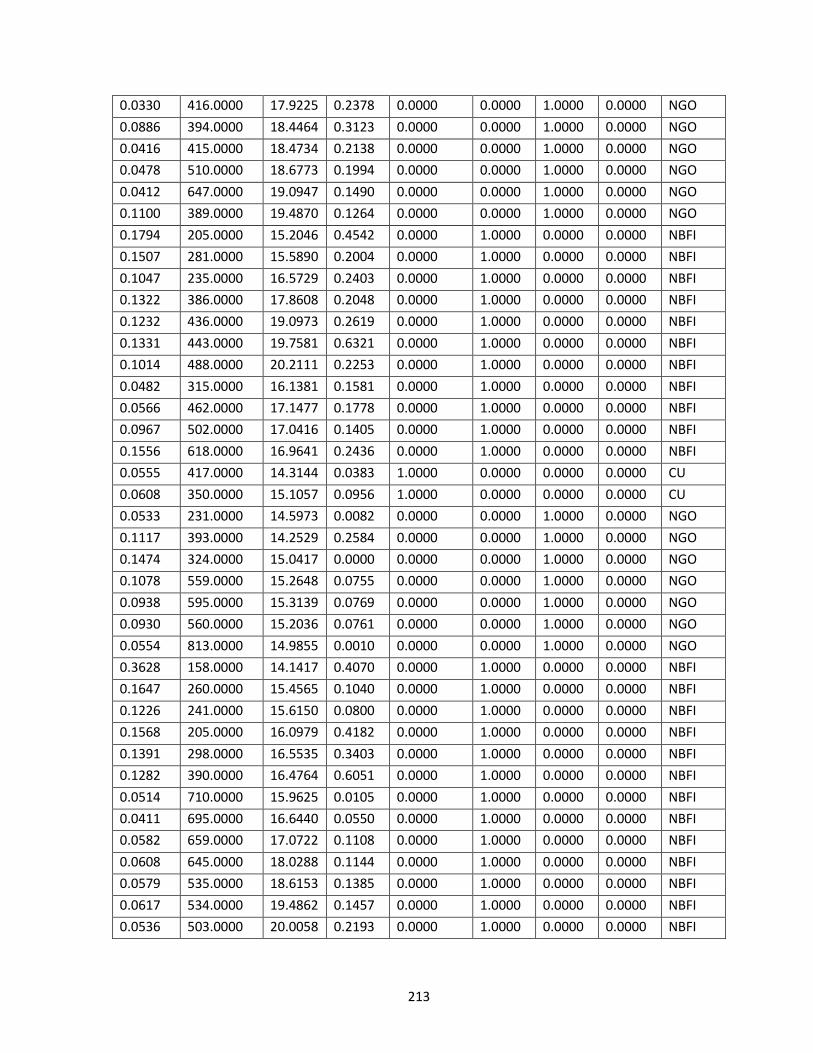

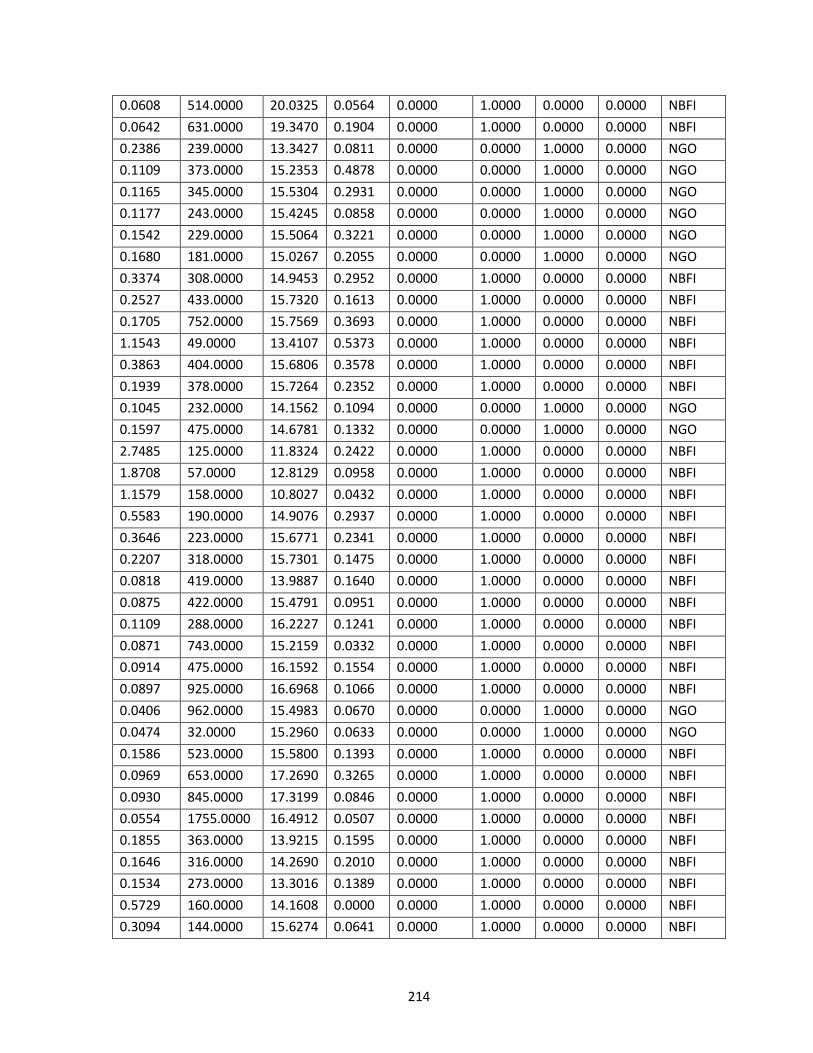

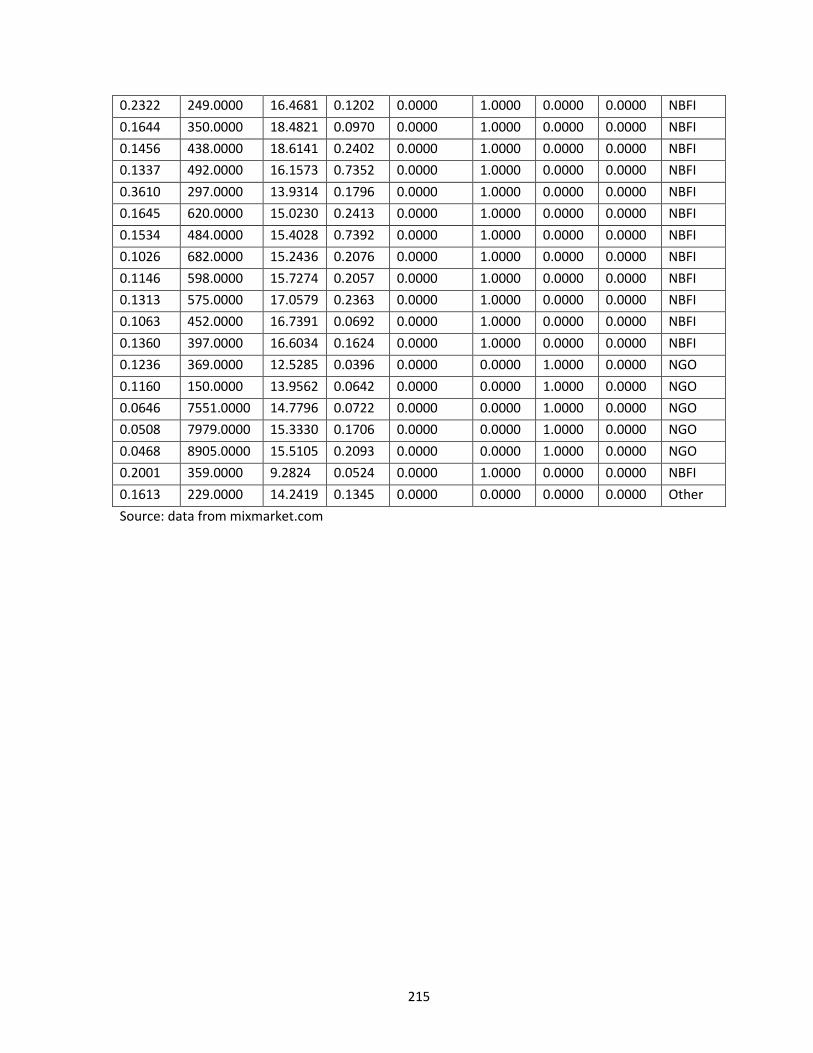

APPENDIX 2 Responses to the Questionnaire 99

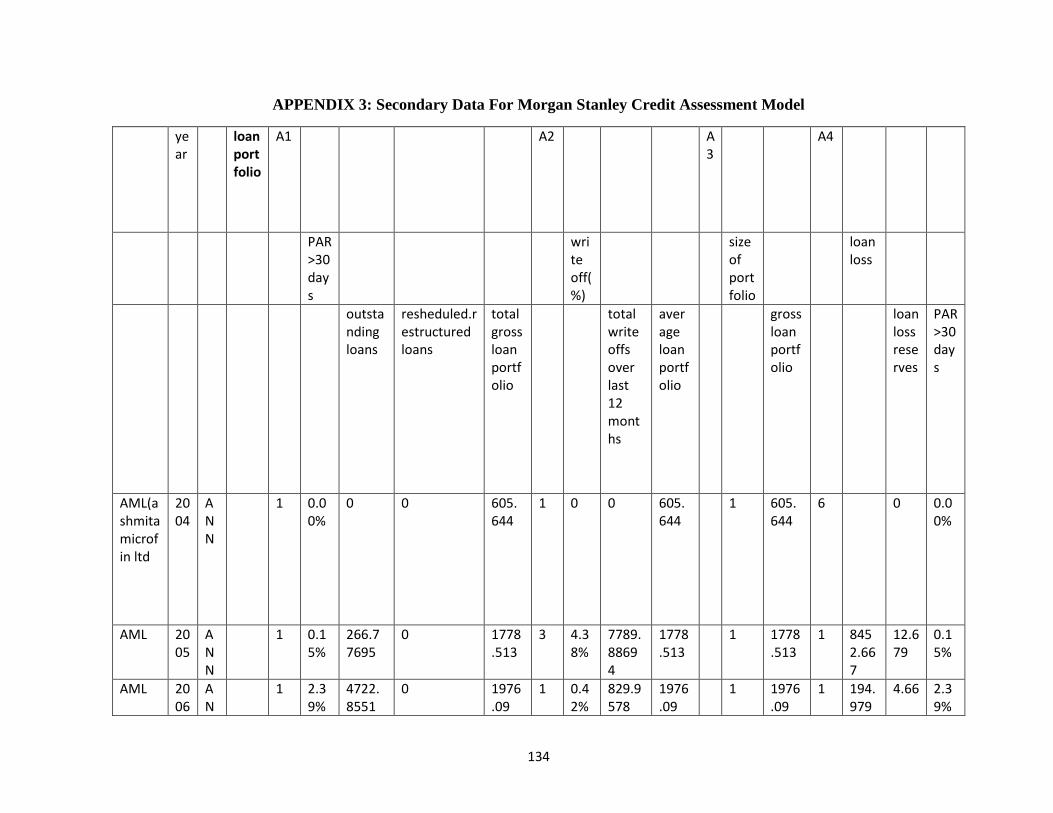

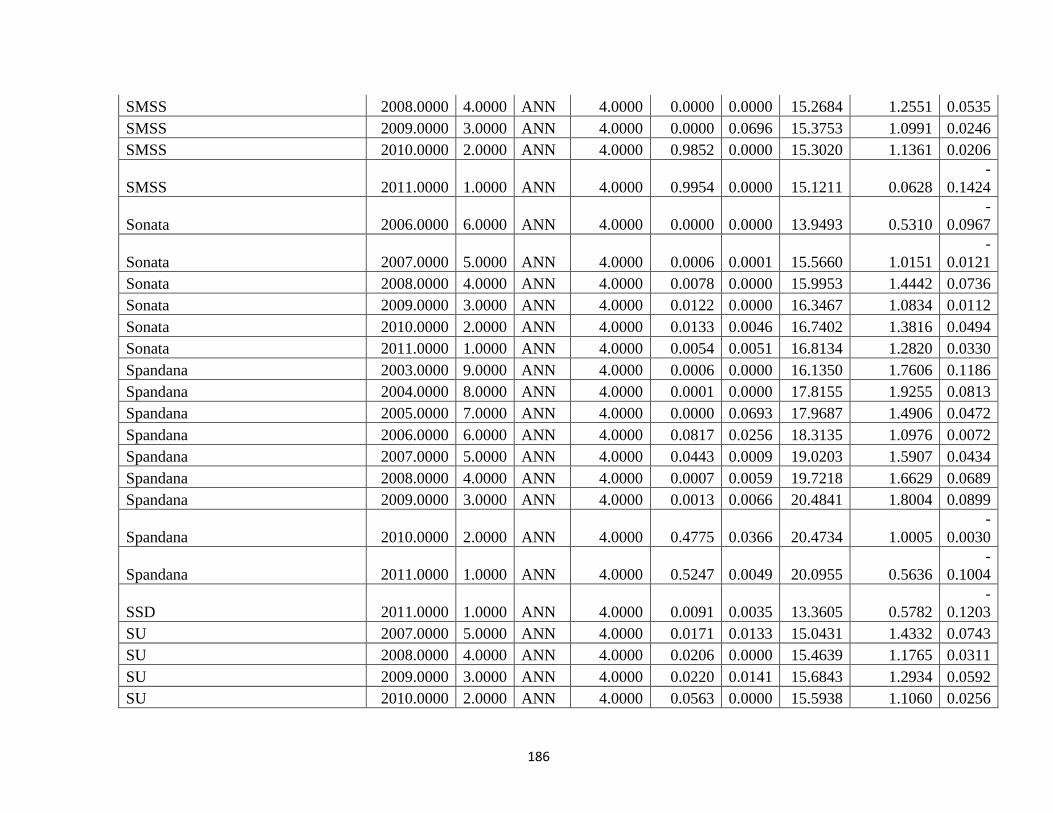

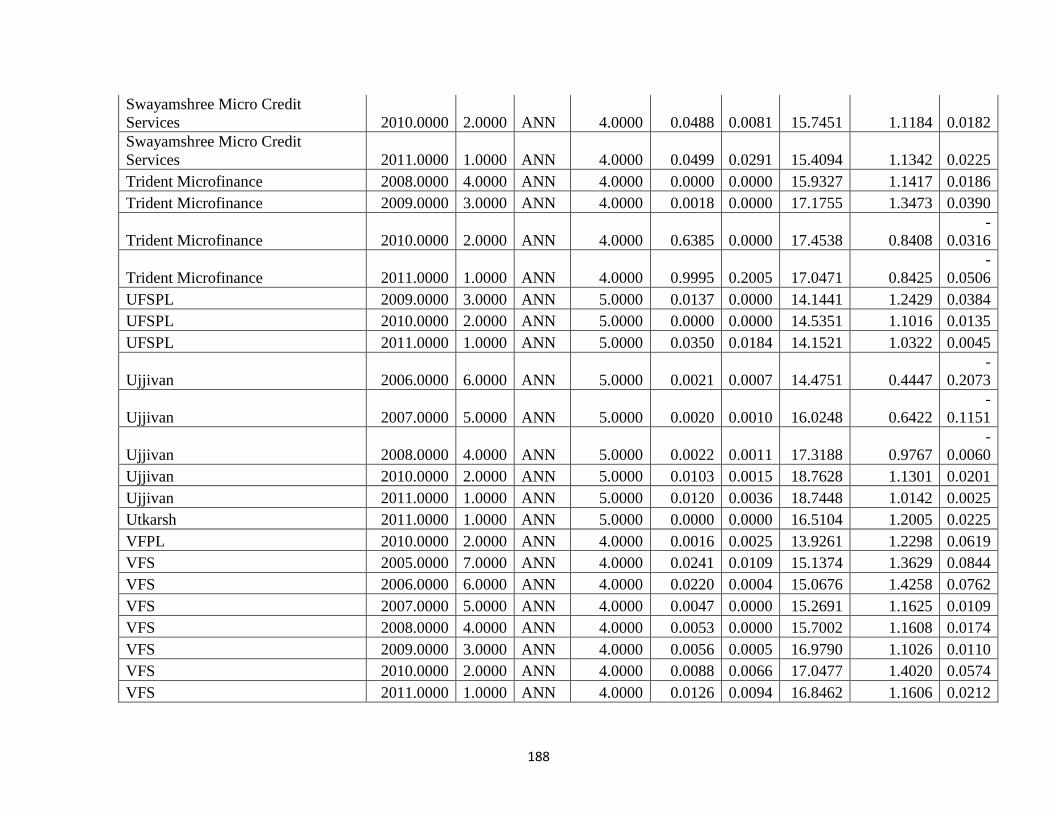

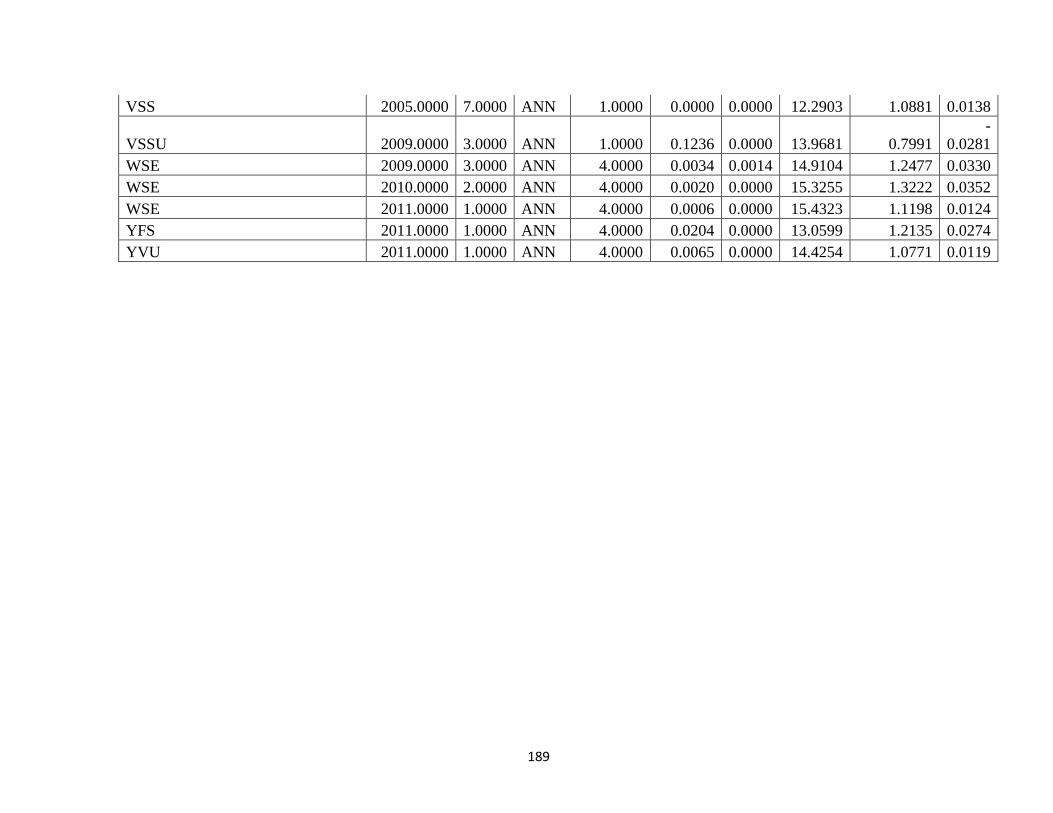

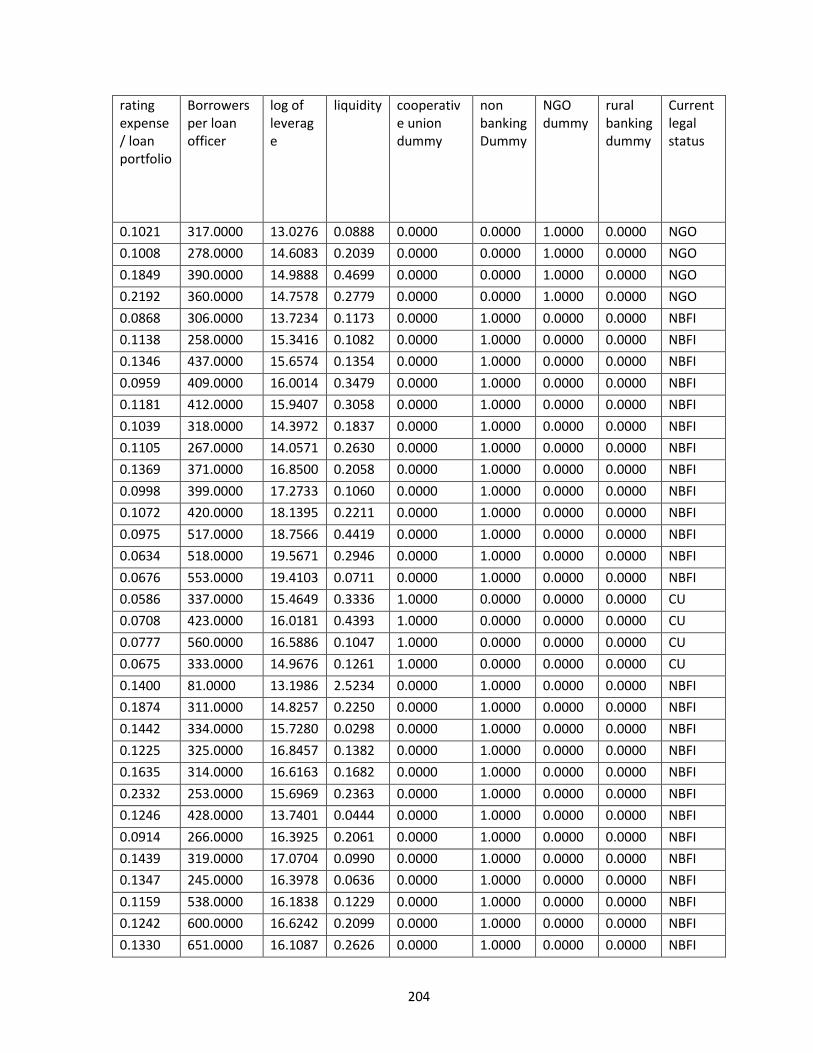

APPENDIX 3 Secondary Data for Morgan Stanley Credit Assessment Model 134

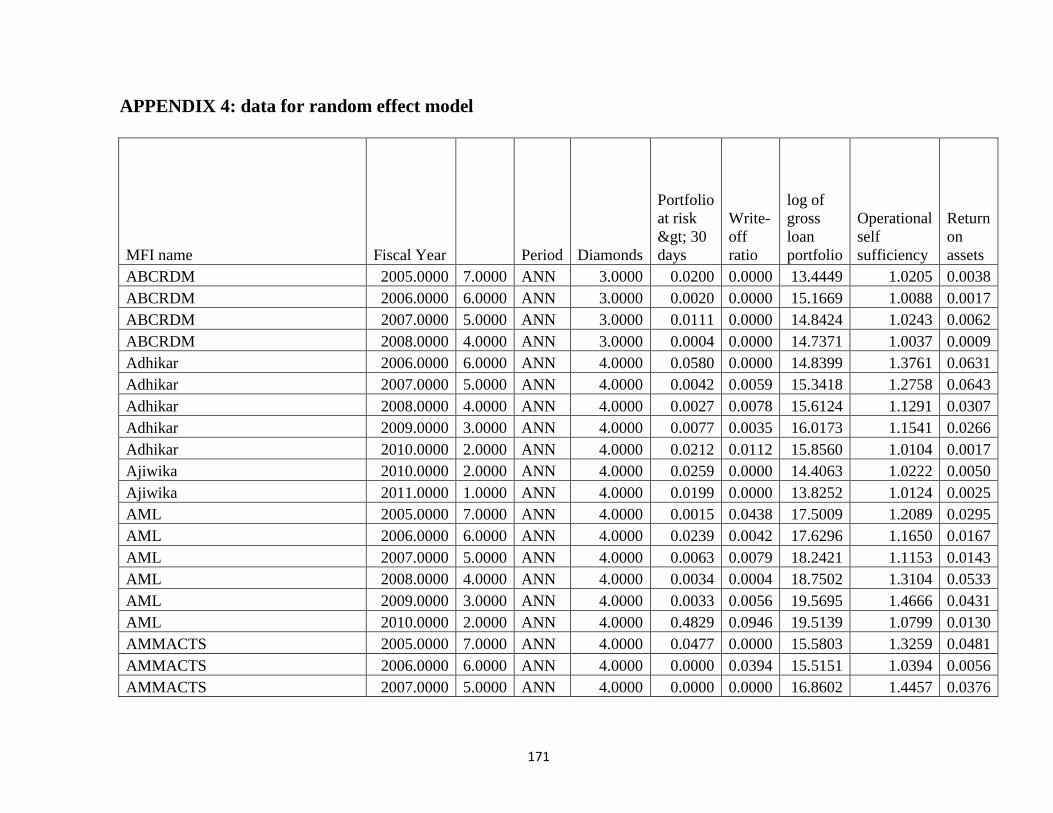

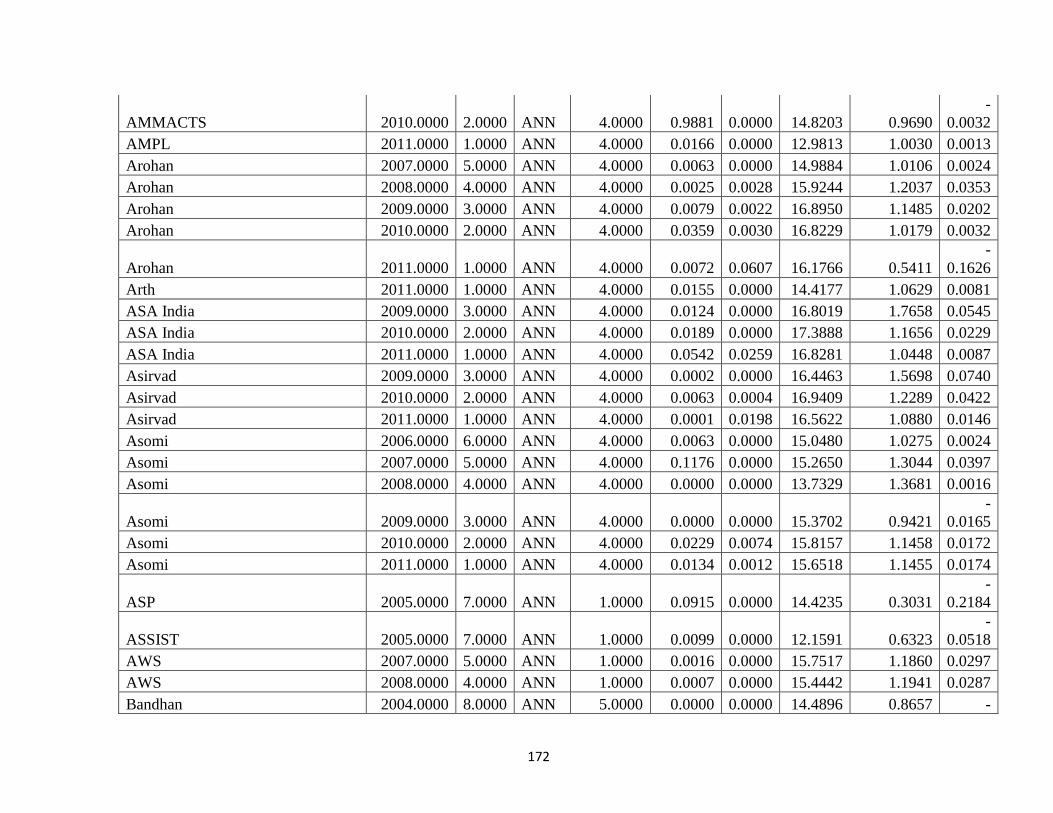

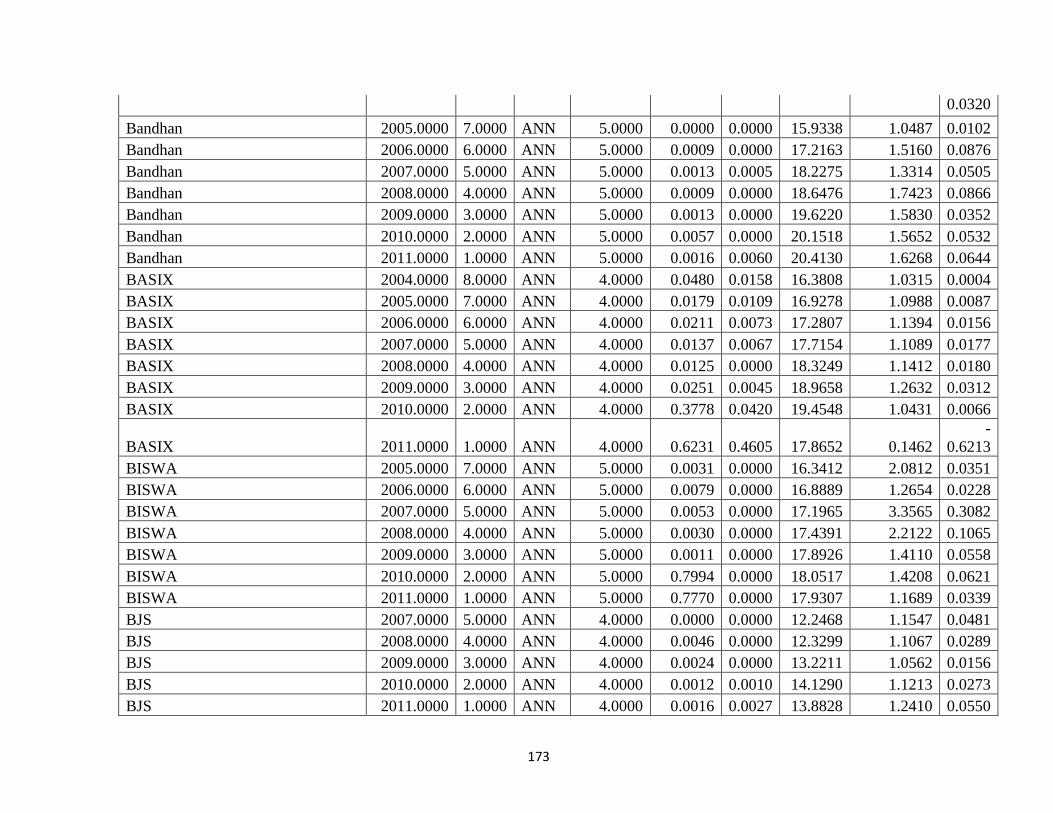

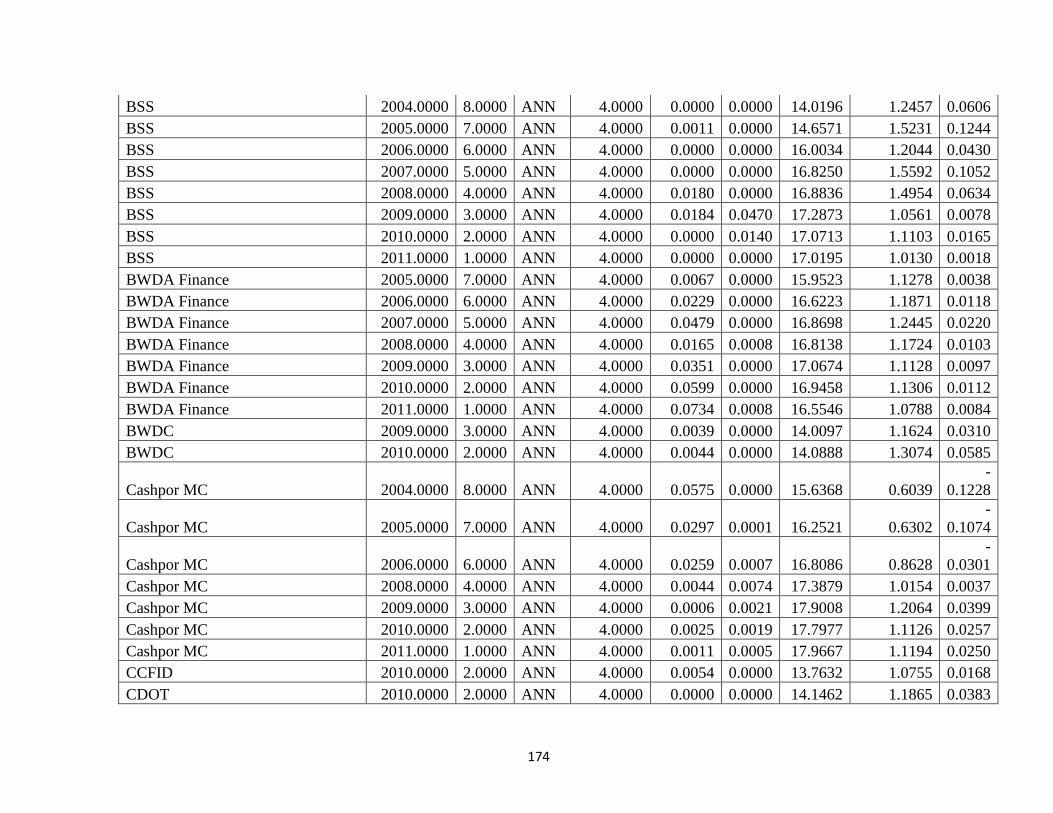

APPENDIX 4 Data For Random Effect Model 171

CHAPTER 1

INTRODUCTION

1.1 BACKGROUND OF THE STUDY :

According to “Fanie Jansen Van Vuuren in Risk management for microfinance institutions in

South Africa,” Risk is the probability that a decision will lead to a different outcome from the

one which is thought, due to the fact that the decisions are made under uncertainty with

imperfect information.

(Vijender, 2012)“Small-scale financial services primarily credit and savings, provided to

people who farm, fish or herd and adds that it refers to all types of financial services provided

to low-income households and enterprises.”

(Davis, 2006). ”Extension of small loans to entrepreneurs too poor to qualify for traditional

bank loans.”

The Reserve Bank of India defines, “microfinance is provision of thrift, credit and other

financial services and products of very small amount to the poor in rural, semi-urban and

urban areas for enabling them to raise their income levels and improve living standards.”

(khan) The practice of microfinance is not new and has probably been around for as long as

currency itself has. Informal credit and savings services probably formed around social

groups where the members got together to help one another as a community. Savings and

credit groups that have operated for centuries include the "susus" of Ghana, "chit funds" in

India, "tandas" in Mexico, "arisan" in Indonesia, "cheetu" in Sri Lanka, "tontines" in West

Africa, and "pasanaku" in Bolivia. One of the major concerns of microfinance is to increase

penetration so as to attain volumes and hence increase the number of people who can benefit.

Increasing penetration would raise the income levels of the people and hence improving the

living standards of people.

The interesting aspect of formal financial system is that, they can provide microcredit at low

interest rates and easy periodical installments, but this kind of facility is not available in

formal financial system. Microfinance operates mostly in an informal system since there

exist complex legal and operational procedures (such as collateral for microcredit, being able

to fulfill committee norms for working capital loans etc.). The problem gets complicated

2

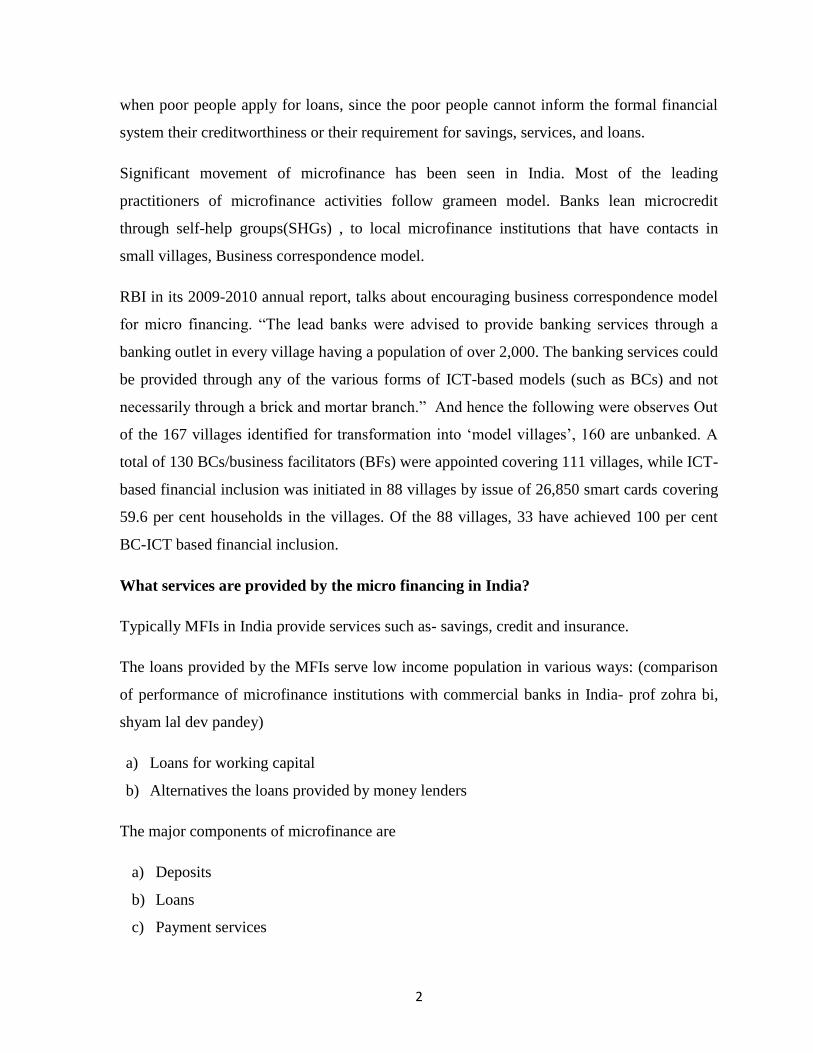

when poor people apply for loans, since the poor people cannot inform the formal financial

system their creditworthiness or their requirement for savings, services, and loans.

Significant movement of microfinance has been seen in India. Most of the leading

practitioners of microfinance activities follow grameen model. Banks lean microcredit

through self-help groups(SHGs) , to local microfinance institutions that have contacts in

small villages, Business correspondence model.

RBI in its 2009-2010 annual report, talks about encouraging business correspondence model

for micro financing. “The lead banks were advised to provide banking services through a

banking outlet in every village having a population of over 2,000. The banking services could

be provided through any of the various forms of ICT-based models (such as BCs) and not

necessarily through a brick and mortar branch.” And hence the following were observes Out

of the 167 villages identified for transformation into „model villages‟, 160 are unbanked. A

total of 130 BCs/business facilitators (BFs) were appointed covering 111 villages, while ICT-

based financial inclusion was initiated in 88 villages by issue of 26,850 smart cards covering

59.6 per cent households in the villages. Of the 88 villages, 33 have achieved 100 per cent

BC-ICT based financial inclusion.

What services are provided by the micro financing in India?

Typically MFIs in India provide services such as- savings, credit and insurance.

The loans provided by the MFIs serve low income population in various ways: (comparison

of performance of microfinance institutions with commercial banks in India- prof zohra bi,

shyam lal dev pandey)

a) Loans for working capital

b) Alternatives the loans provided by money lenders

The major components of microfinance are

a) Deposits

b) Loans

c) Payment services

3

d) Money transfer

e) Insurance to the poor

From the reports submitted by RBI, sub-committee of central broad of directors of RBI who

were studying on the issues and concerns of MFI sector pointed out the following points

a) Out of the total loans outstanding of 45600 crores, under the Micro Financing sector at

the end out March 2010 , MFI segment accounted for about Ra 18344crores i.e. 40

percent. Also the incremental growth of advances is high

b) Hence there is a setback between SHG-bank linkage segment

c) The committee pointed out that the apart from interest rate, other incidental charges such

as processing free, interest free security deposits have hiked the effective interest rate

d) For larger MFI effective rates of interest calculated on the mean outstanding portfolio

during 2009-2010 and has ranges between 31 percent to 51 percent with an average of 35

percent. For smaller MFI the average interest rate was about 29 percent. The main

e) Problem identified was multiple lending, over financing and ghost borrowers. The

presence of ring leaders who acted as intermediaries between the MFI and the potential

customers.

f) The committee also noticed coercive methods of recovery of MFI , lack of grace period.

g) The committee pointed out that for larger MFIs the overhead costs as a percentage of

outstanding was higher that of smaller MFIs, hence smaller the MFI the efficient is the

operation.

h) Only 25% of the credit was used for income generating activities

Suggestions from the committee:

a) A new regulation act for NBFC-MFI

b) The minimum capital requirement of the NBFC- MFI should be enhanced from Rs 2

crores to Rs.15crores.

4

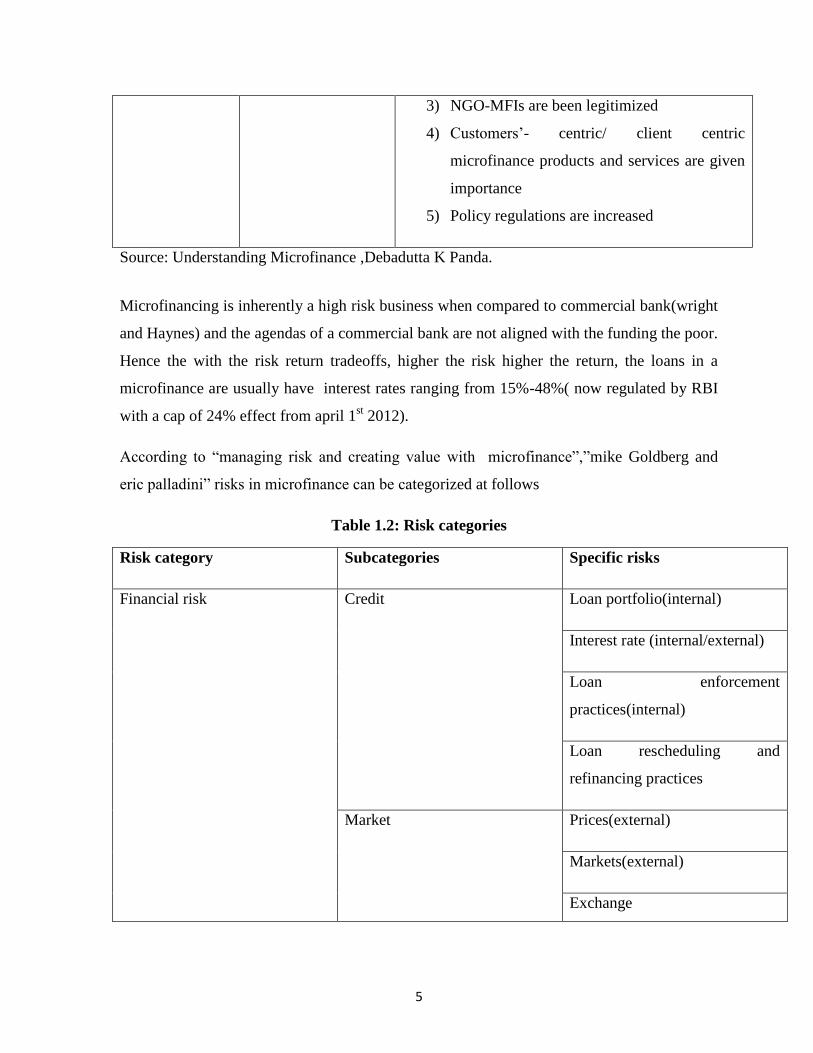

1.2 PHASES OF MICROFINANCE :

Table 1.1: Phases of microfinance

Phases Year Features

First Phase:

Social Banking

1960-1990 1) Nationalization of commercial banks.

Fourteen commercial banks were nationalized

in 1969 and 8 commercialized banks were

nationalized in 980

2) Lead bank scheme was initiated with district

credit plans

3) Expansion of the network of rural banking.

RRBs were set up in 1976. NABARD was

formed in 1982. Cooperative banking was

structured and developed. SIDBI was

established

4) Extension disbursement of subsidized credits

Second Phase:

Financial

Systems

Approach

1990-2000 1) NGO-based FIs were developed to provide

Microfinance products and services on not for

profit basis

2) SHG-bank linkage programme was initiated

and rapidly replicated

3) Innovative credit lending mechanisms based

on “peer pressure” and “moral collateral”

were developed.

Third Phase:

Financial

Inclusion

2000 onwards 1) Microfinance is seen as a business

proposition and has been commercialized

2) Development of for profit MFIs like Non

banking finance companies(NBFCs) and non

banking financial institutions

5

3) NGO-MFIs are been legitimized

4) Customers‟- centric/ client centric

microfinance products and services are given

importance

5) Policy regulations are increased

Source: Understanding Microfinance ,Debadutta K Panda.

Microfinancing is inherently a high risk business when compared to commercial bank(wright

and Haynes) and the agendas of a commercial bank are not aligned with the funding the poor.

Hence the with the risk return tradeoffs, higher the risk higher the return, the loans in a

microfinance are usually have interest rates ranging from 15%-48%( now regulated by RBI

with a cap of 24% effect from april 1st 2012).

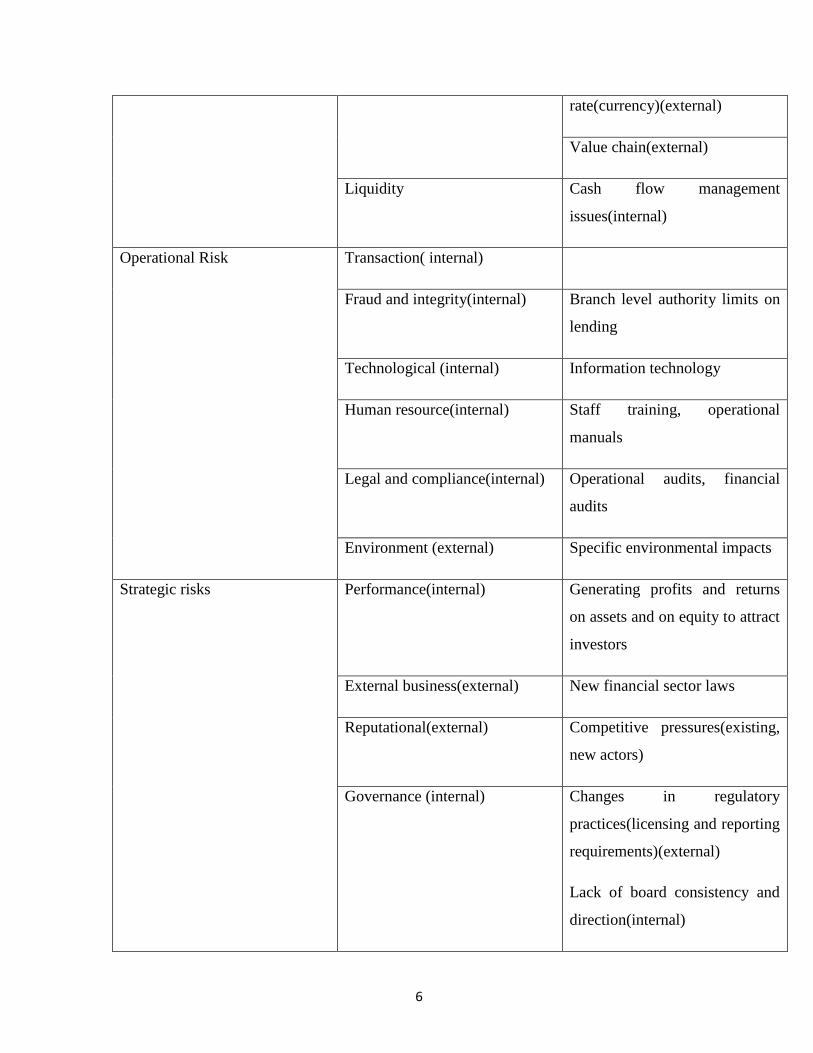

According to “managing risk and creating value with microfinance”,”mike Goldberg and

eric palladini” risks in microfinance can be categorized at follows

Table 1.2: Risk categories

Risk category Subcategories Specific risks

Financial risk Credit Loan portfolio(internal)

Interest rate (internal/external)

Loan enforcement

practices(internal)

Loan rescheduling and

refinancing practices

Market Prices(external)

Markets(external)

Exchange

6

rate(currency)(external)

Value chain(external)

Liquidity Cash flow management

issues(internal)

Operational Risk Transaction( internal)

Fraud and integrity(internal) Branch level authority limits on

lending

Technological (internal) Information technology

Human resource(internal) Staff training, operational

manuals

Legal and compliance(internal) Operational audits, financial

audits

Environment (external) Specific environmental impacts

Strategic risks Performance(internal) Generating profits and returns

on assets and on equity to attract

investors

External business(external) New financial sector laws

Reputational(external) Competitive pressures(existing,

new actors)

Governance (internal) Changes in regulatory

practices(licensing and reporting

requirements)(external)

Lack of board consistency and

direction(internal)

7

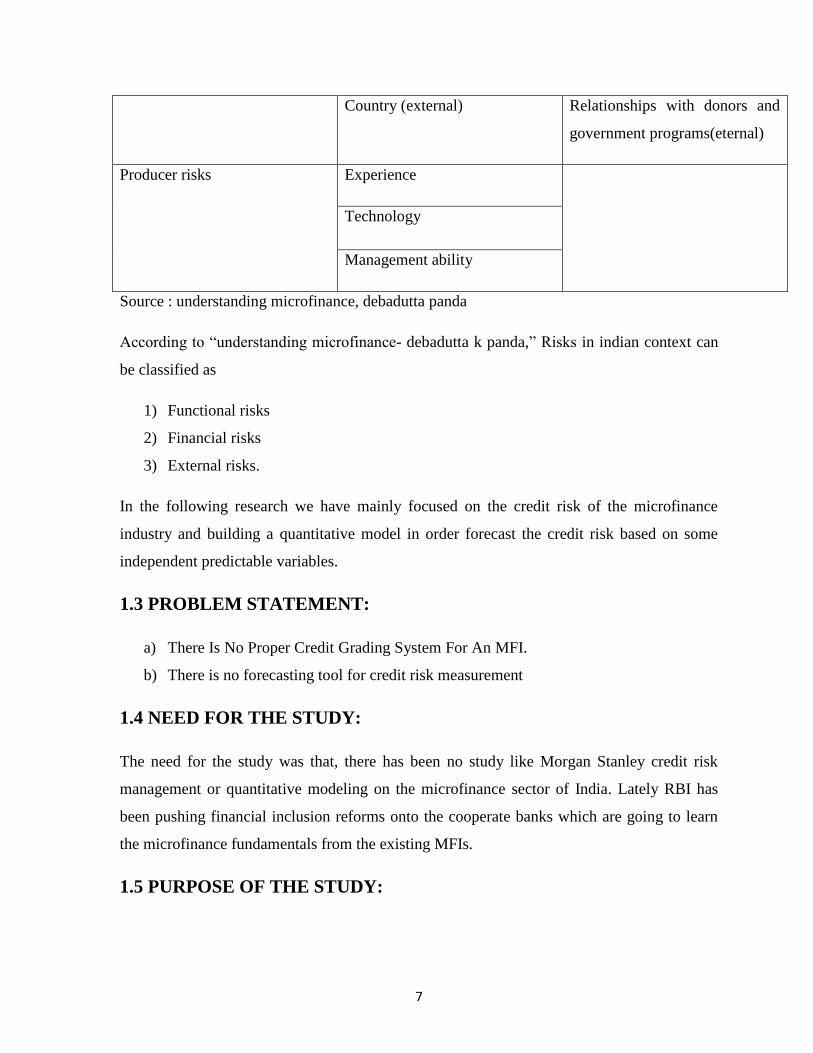

Country (external) Relationships with donors and

government programs(eternal)

Producer risks Experience

Technology

Management ability

Source : understanding microfinance, debadutta panda

According to “understanding microfinance- debadutta k panda,” Risks in indian context can

be classified as

1) Functional risks

2) Financial risks

3) External risks.

In the following research we have mainly focused on the credit risk of the microfinance

industry and building a quantitative model in order forecast the credit risk based on some

independent predictable variables.

1.3 PROBLEM STATEMENT:

a) There Is No Proper Credit Grading System For An MFI.

b) There is no forecasting tool for credit risk measurement

1.4 NEED FOR THE STUDY:

The need for the study was that, there has been no study like Morgan Stanley credit risk

management or quantitative modeling on the microfinance sector of India. Lately RBI has

been pushing financial inclusion reforms onto the cooperate banks which are going to learn

the microfinance fundamentals from the existing MFIs.

1.5 PURPOSE OF THE STUDY:

8

The purpose of the study is to assess the credit risk management structure of an MFI based

on parameters mentioned in chapter 3 also quantify and project the credit risk using a

quantitative model.

Inherently there is a high risk with the MFI segment. The small, medium and even larger

MFI find it difficult to manage risk or predict the outcome of credit transactions.

The probable reason could be due to the fact that the customer base is volatile or

intermediaries between the MFI and the customers who hide the customer details or lack of

risk management tools.

CHAPTER 2

LITERATURE REVIEW

2.1 INTRODUCTION

By the risk management framework for micro financing institutes published by microfinance

network,

The document focuses on helping senior managers and directors of MFIs design a

comprehensive and systematic approach for identifying, anticipating and responding to the

major risks faced by the MFIs. This document identifies that risk management is an essential

element of long term success and hence for financial institutions, to effectively management

risk they have to keep the following points in mind.

a) They have to have systematic approach to evaluate and measure risk so as to identify

the risk in the early stage and hence fix it.

b) A good risk management framework allows management to quantify the risk and fine

tune to the capital allocation and liquidity needs to match the on and off balance sheet

risks faced by the institutions and to evaluate the impact of potential shocks to

financial system or institution.

c) Having a good information on potential consequences for both positive and negative.

There has been a significant increase in the emphasis on risk management, hence the bank

managers and regulators are able to better anticipate risks, than just to react to them.

Therefore to foster stronger financial institutions the revised camels approach among US

regulators emphasizes the quality of internal systems to identify and address potential

problems quickly.

For MFIs proper internal risk management yields to practices designed to limit risk associate

with individual product lines and systematic, quantitative methods to identify, monitor and

control aggregate risks across financial institutions.

MFIs have been growing and serving large base of customers and also attract more

mainstream investment capital and funds, hence they have to strengthen their internal

capacity to identify and anticipate potential risks to avoid unexpected losses and surprises.

Creating a risk management framework and culture with in an MFI in the next step after

mastering the fundamental of individual risks, such as credit risk, treasury risk, and liquidity

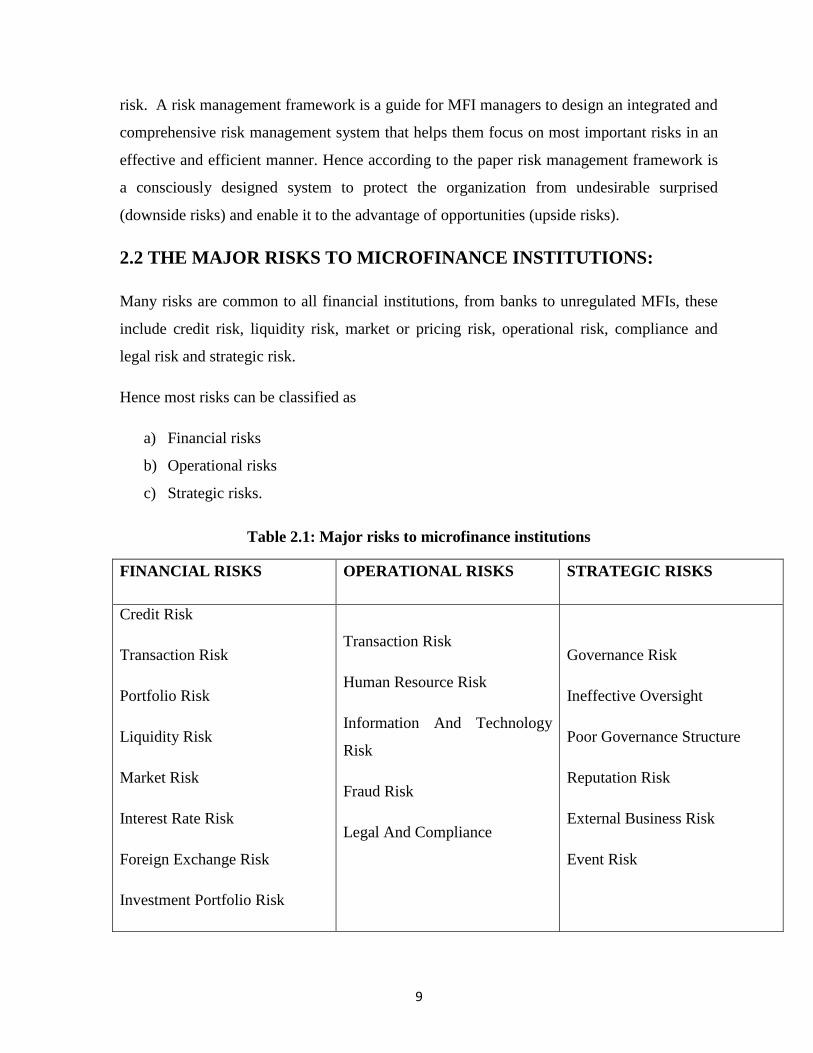

9

risk. A risk management framework is a guide for MFI managers to design an integrated and

comprehensive risk management system that helps them focus on most important risks in an

effective and efficient manner. Hence according to the paper risk management framework is

a consciously designed system to protect the organization from undesirable surprised

(downside risks) and enable it to the advantage of opportunities (upside risks).

2.2 THE MAJOR RISKS TO MICROFINANCE INSTITUTIONS:

Many risks are common to all financial institutions, from banks to unregulated MFIs, these

include credit risk, liquidity risk, market or pricing risk, operational risk, compliance and

legal risk and strategic risk.

Hence most risks can be classified as

a) Financial risks

b) Operational risks

c) Strategic risks.

Table 2.1: Major risks to microfinance institutions

FINANCIAL RISKS OPERATIONAL RISKS STRATEGIC RISKS

Credit Risk

Transaction Risk

Portfolio Risk

Liquidity Risk

Market Risk

Interest Rate Risk

Foreign Exchange Risk

Investment Portfolio Risk

Transaction Risk

Human Resource Risk

Information And Technology

Risk

Fraud Risk

Legal And Compliance

Governance Risk

Ineffective Oversight

Poor Governance Structure

Reputation Risk

External Business Risk

Event Risk

10

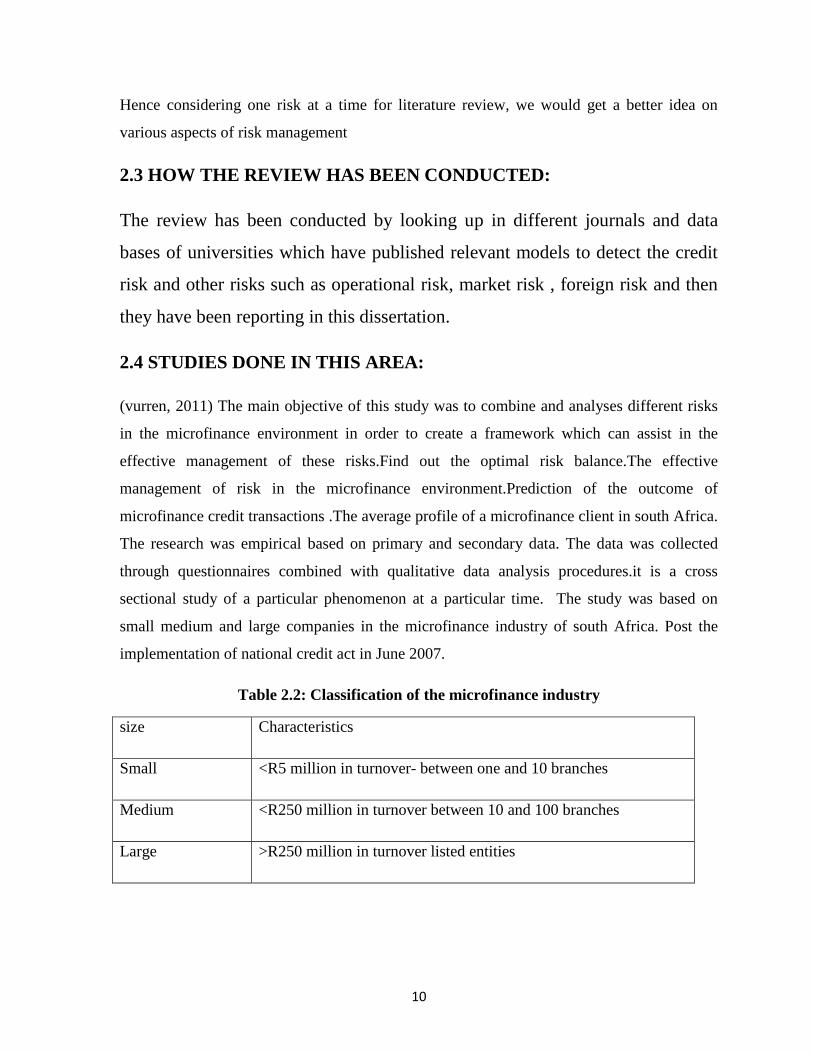

Hence considering one risk at a time for literature review, we would get a better idea on

various aspects of risk management

2.3 HOW THE REVIEW HAS BEEN CONDUCTED:

The review has been conducted by looking up in different journals and data

bases of universities which have published relevant models to detect the credit

risk and other risks such as operational risk, market risk , foreign risk and then

they have been reporting in this dissertation.

2.4 STUDIES DONE IN THIS AREA:

(vurren, 2011) The main objective of this study was to combine and analyses different risks

in the microfinance environment in order to create a framework which can assist in the

effective management of these risks.Find out the optimal risk balance.The effective

management of risk in the microfinance environment.Prediction of the outcome of

microfinance credit transactions .The average profile of a microfinance client in south Africa.

The research was empirical based on primary and secondary data. The data was collected

through questionnaires combined with qualitative data analysis procedures.it is a cross

sectional study of a particular phenomenon at a particular time. The study was based on

small medium and large companies in the microfinance industry of south Africa. Post the

implementation of national credit act in June 2007.

Table 2.2: Classification of the microfinance industry

size Characteristics

Small <R5 million in turnover- between one and 10 branches

Medium <R250 million in turnover between 10 and 100 branches

Large >R250 million in turnover listed entities

11

The target population has been divided into 4 categories The first category is unlisted entities

with less than 10 branches. The second category is unlisted entities with more than 10

branches The third entity is with banking license .The fourth category includes the

microfinance division of some of the traditional banks. According to the category the

questionnaires were designed. Data analysis was done through pie charts and bar charts and

then analysed. The following were the findings of the author. Five risk tools where to be

analyzed and the respondents gave “credit granting policy and customer affordability

calculations” the highest priority followed by “internal controls”, “debt controls”, “debt

collecting”, “staff training creating loyalty and integrity”, “credit scoring models.” The risks

that can be involved in non-bank microfinance institutions in south Africa where analyzed

and the respondents answered “internal and external fraud”, “bad debts”, customer migration

to competitors or the commercial banks” “regulation of the industry” and “lack of affordable

funding.” How well the risk tools used in banks can be applied to the micro financing

industry. Most effective way to lower the overall microfinance risk in south Africa. And the

respondents answered “conservative credit granting policy”, “improved internal controls”,

“better loan management system”, “better educated staff” , “better collecting on arrears

clients.” The biggest predictors of non-payment of new client in microfinance institution in

south Africa are “ disposable income” “number of loans” “ judgments” “employment

industry” credit enquiries” “gender”, “age”, “race”. The biggest contributor to minimize

credit risk in a microfinance institution in south Africa is accurate affordability calculation,

shorter term loans instead of longer ones , the use of a credit score model, small loan

amounts, the analysis of credit bureau information. The most efficient way to optimize client

service in a microfinance institution in south Africa, and the most efficient way to reduce risk

in microfinance institutions in south Africa are “real time loan management system”,”

decentralized credit decisions”, “cash disbursements to clients”, “ a call center function”,

centralized credit decision.” The items on which MFI would spend the most in a financial

year could be “ staff training, internal audit, independent review on the loan management

system”, “rewards for fraud tip offs” The biggest misperception in south Africa regarding

microfinance institutions. Are MFI were no affected negatively by the national credit act,

MFIs don‟t relieve poverty in SA, MFI in SA don‟t realy compete with the 4 major banks,

MFI in SA is an extremely high risk industry. The most efficient options to pro- actively

12

manage risk in a microfinance institution in SA are a credit scoring model, build customer

relationship with shorter products, extensive training for new staff, to only disburse 30 day

loans. The best predictors of on time payment of clients are correct affordability calculations

, a shorter term loan, work reference, a credit score model, a proper and signed credit

agreement. The findings from client information of 3000 microfinance clients in south

Africa: A good client means not in arrears for more than 2 installments And a bad client

means some on who is in arrears for more than 2 installments. The following table was

constructed for 2009 and 2010 year

In the paper the author identifies through literature review, identifies various ways to identify

the risks related to MFI, ie. The debt equity ratio( gearing risks), interest cover, liquidity risk,

market risk(beta) company specific risk, growth, management team, industry comparative

performance, theft and fraud and the non-performance of loans.

Then he identifies the relation between the business and credit risk. According to the author,

to lower the risk of loans not performing the emphasis should be on quality loans and a risk

portfolio not exceeding 5%. The quality of a loan is determined by the probability that the

credit decision is right. Hence usually the following are the ways for a proper credit decision.

Rationing credit ,Requiring collateral ,Screening applicants, Monitoring borrowers, Credit

scoring In this paper he takes up screening of applicants and monitoring borrowers. By

effectively managing the risk in the industry, south Africa has a good market where in

business models can be sustainable. By being able to service the poor through credit lending

it is creating opportunities to help build the economy. A combination of risk tools need to be

applied effectively in order to reduce material risks, predict good customer and also real time

loan management system with integrated credit scoring models, accurate affordability

calculation combined with well trained staff forms the basis of risk management . even

though there was a thorough examination of the MFI industry, the author did not look into

each risk and tools that need to be used to mitigate the risk.

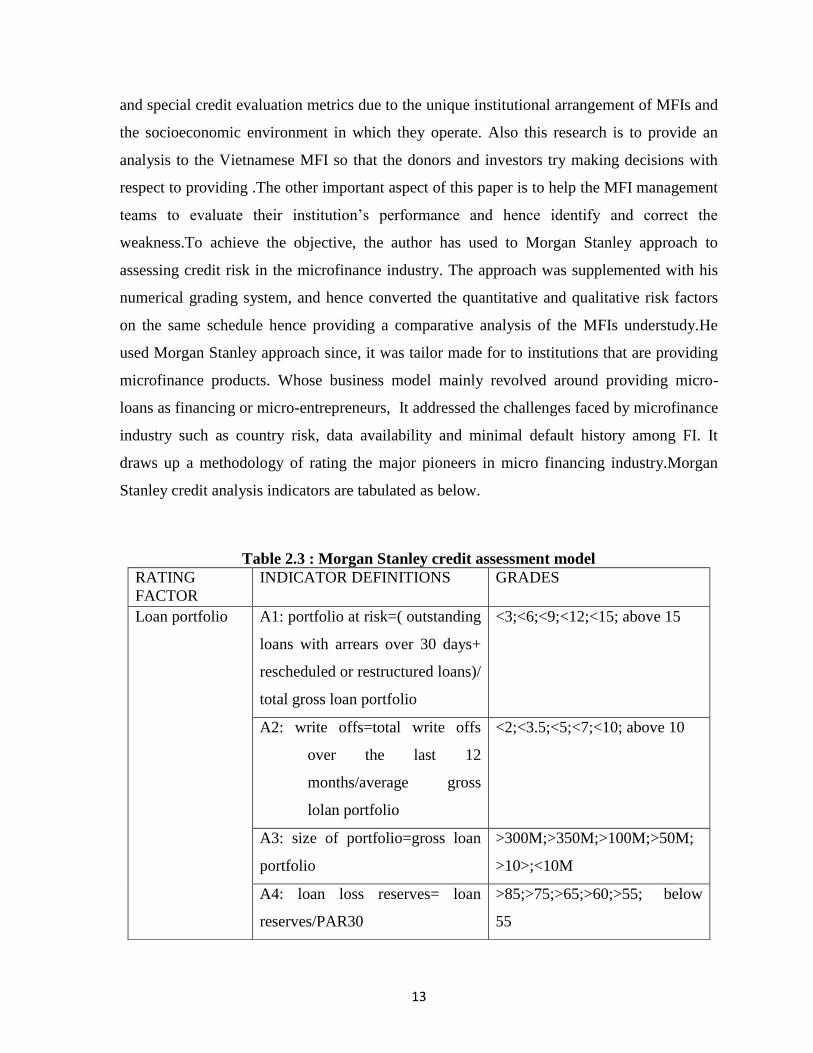

(Ayayi, 2012) Credit risk assessment in the microfinance industry: an application to a

selected group of Vietnamese microfinance institutions and an extension to east Asian pacific

microfinance institutions. The objective of this is to access credit risk in order to determine

internal global scale rating for Vietnamese MFI. Particular attention is paid to conventional

13

and special credit evaluation metrics due to the unique institutional arrangement of MFIs and

the socioeconomic environment in which they operate. Also this research is to provide an

analysis to the Vietnamese MFI so that the donors and investors try making decisions with

respect to providing .The other important aspect of this paper is to help the MFI management

teams to evaluate their institution‟s performance and hence identify and correct the

weakness.To achieve the objective, the author has used to Morgan Stanley approach to

assessing credit risk in the microfinance industry. The approach was supplemented with his

numerical grading system, and hence converted the quantitative and qualitative risk factors

on the same schedule hence providing a comparative analysis of the MFIs understudy.He

used Morgan Stanley approach since, it was tailor made for to institutions that are providing

microfinance products. Whose business model mainly revolved around providing micro-

loans as financing or micro-entrepreneurs, It addressed the challenges faced by microfinance

industry such as country risk, data availability and minimal default history among FI. It

draws up a methodology of rating the major pioneers in micro financing industry.Morgan

Stanley credit analysis indicators are tabulated as below.

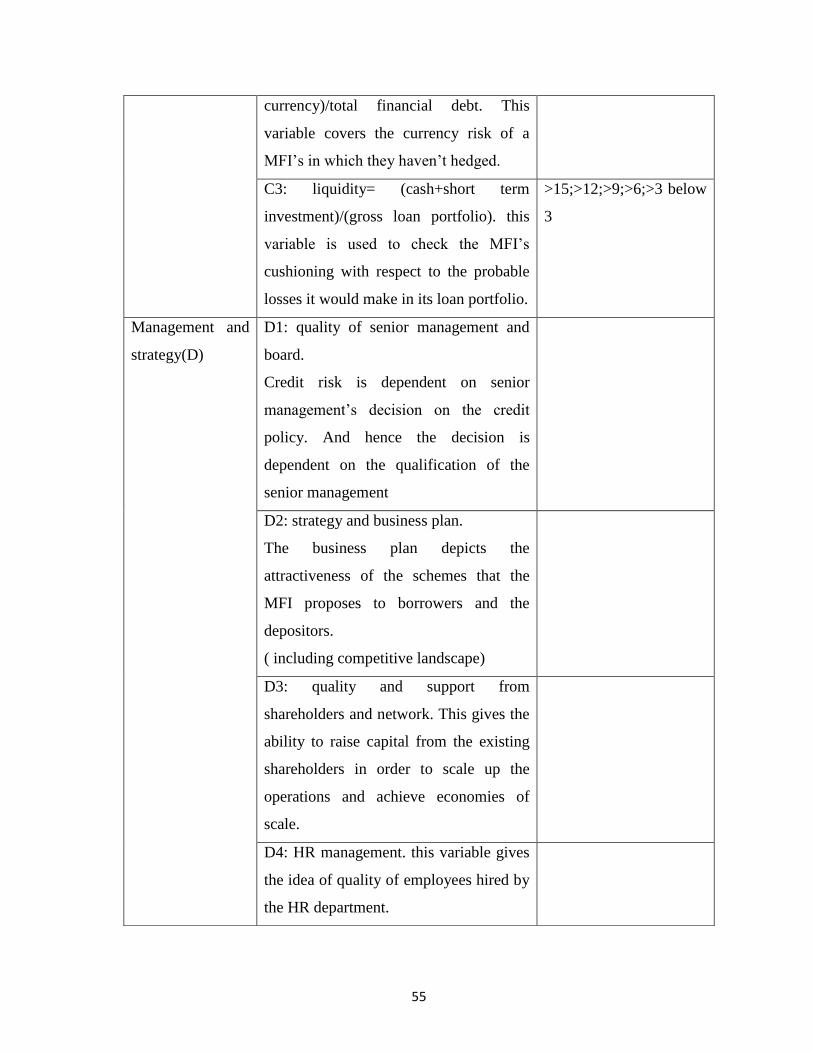

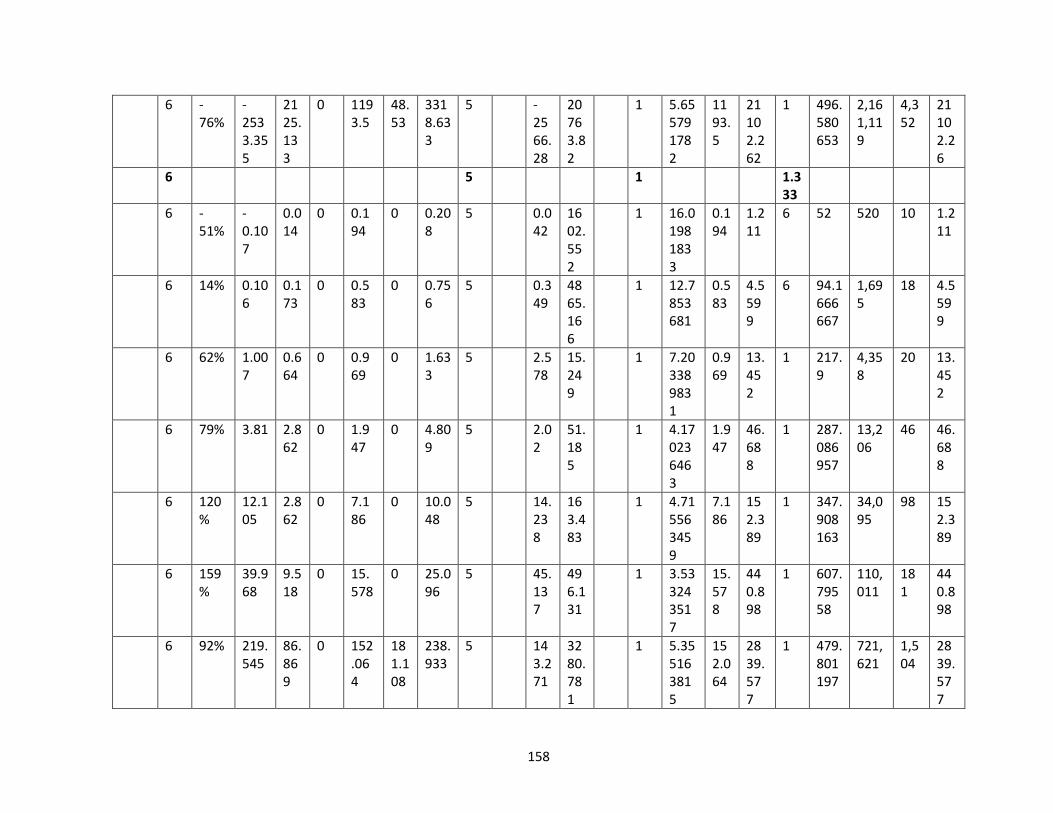

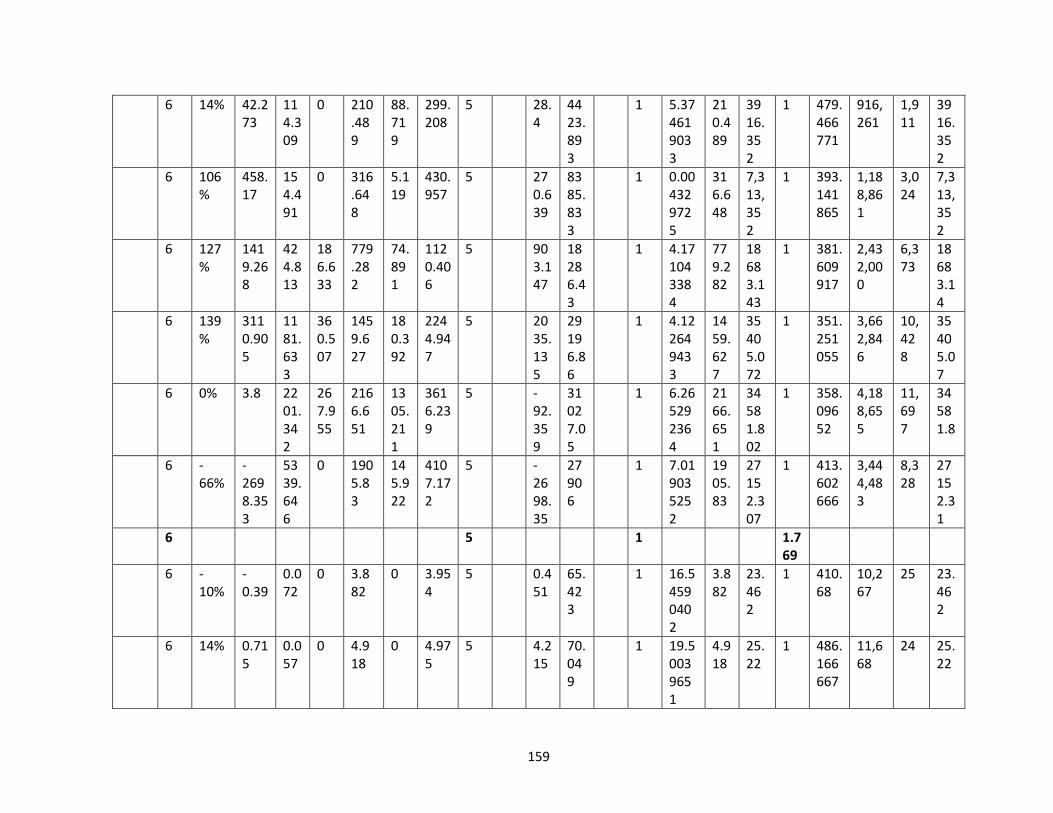

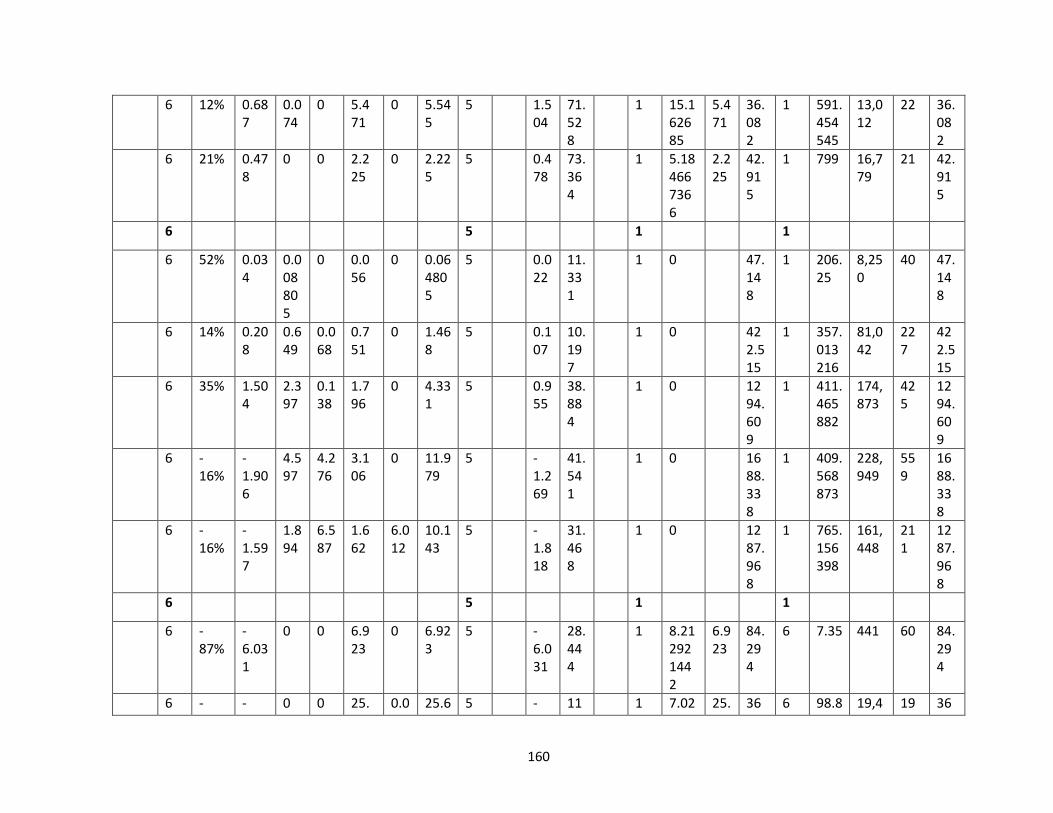

Table 2.3 : Morgan Stanley credit assessment model

RATING

FACTOR

INDICATOR DEFINITIONS GRADES

Loan portfolio A1: portfolio at risk=( outstanding

loans with arrears over 30 days+

rescheduled or restructured loans)/

total gross loan portfolio

<3;<6;<9;<12;<15; above 15

A2: write offs=total write offs

over the last 12

months/average gross

lolan portfolio

<2;<3.5;<5;<7;<10; above 10

A3: size of portfolio=gross loan

portfolio

>300M;>350M;>100M;>50M;

>10>;<10M

A4: loan loss reserves= loan

reserves/PAR30

>85;>75;>65;>60;>55; below

55

14

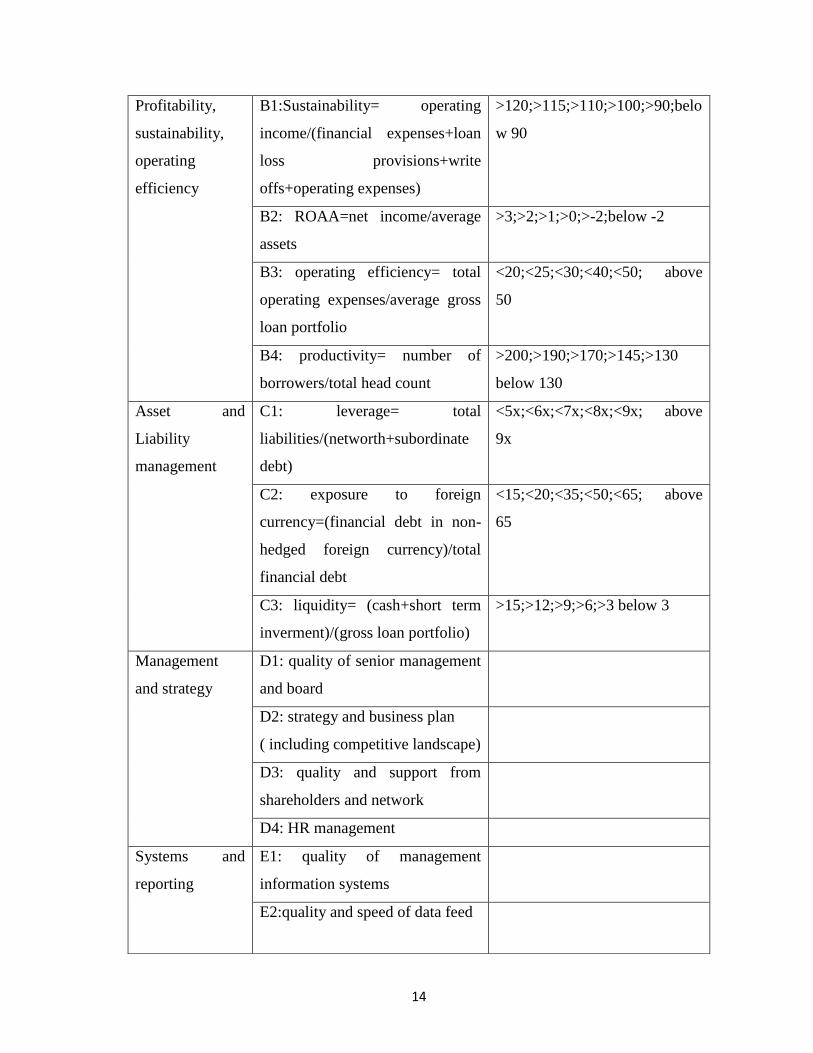

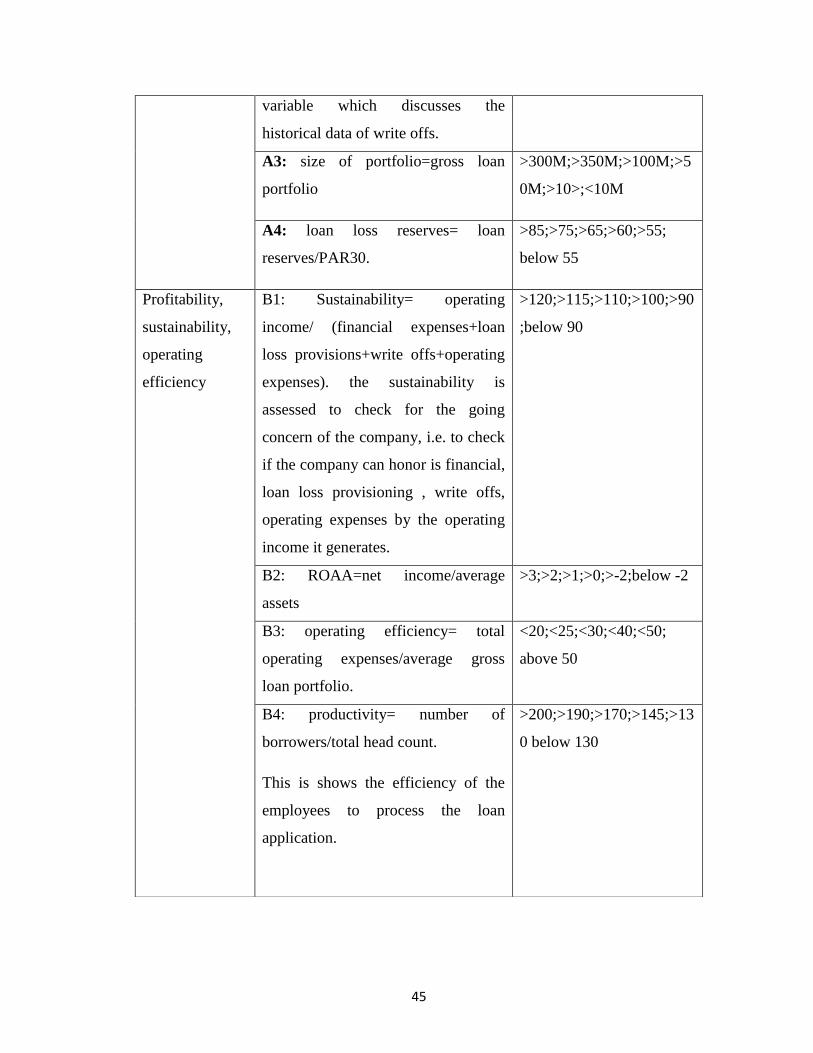

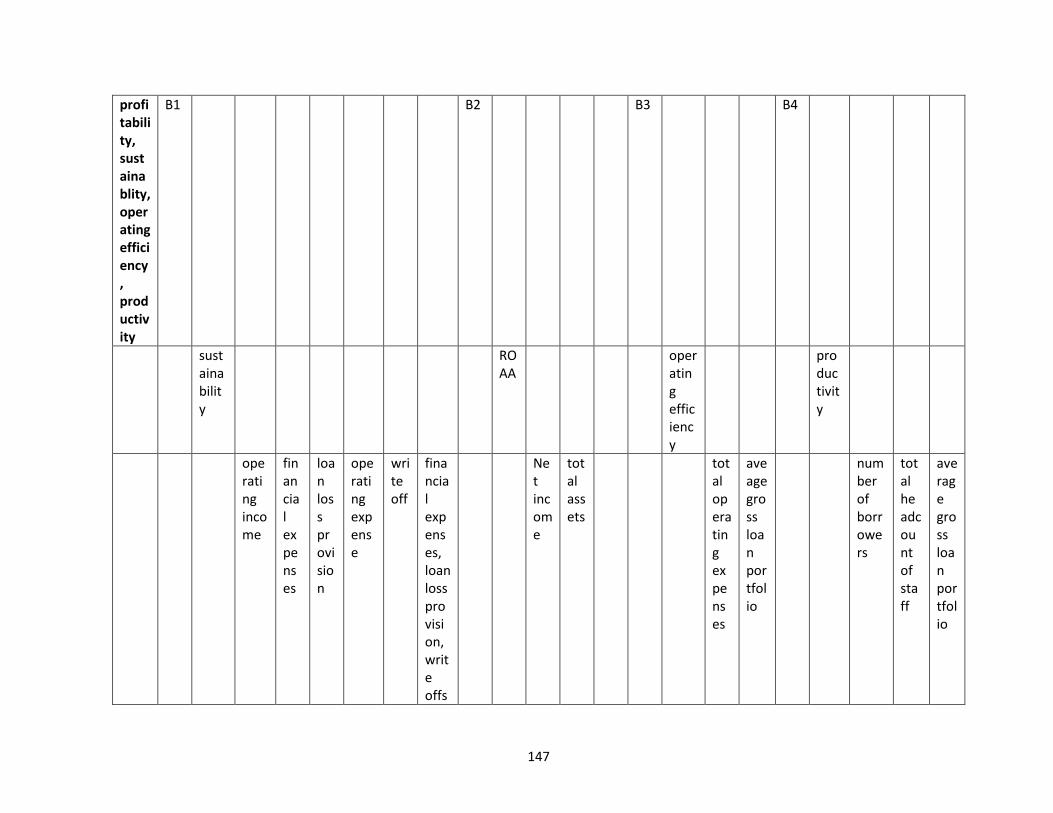

Profitability,

sustainability,

operating

efficiency

B1:Sustainability= operating

income/(financial expenses+loan

loss provisions+write

offs+operating expenses)

>120;>115;>110;>100;>90;belo

w 90

B2: ROAA=net income/average

assets

>3;>2;>1;>0;>-2;below -2

B3: operating efficiency= total

operating expenses/average gross

loan portfolio

<20;<25;<30;<40;<50; above

50

B4: productivity= number of

borrowers/total head count

>200;>190;>170;>145;>130

below 130

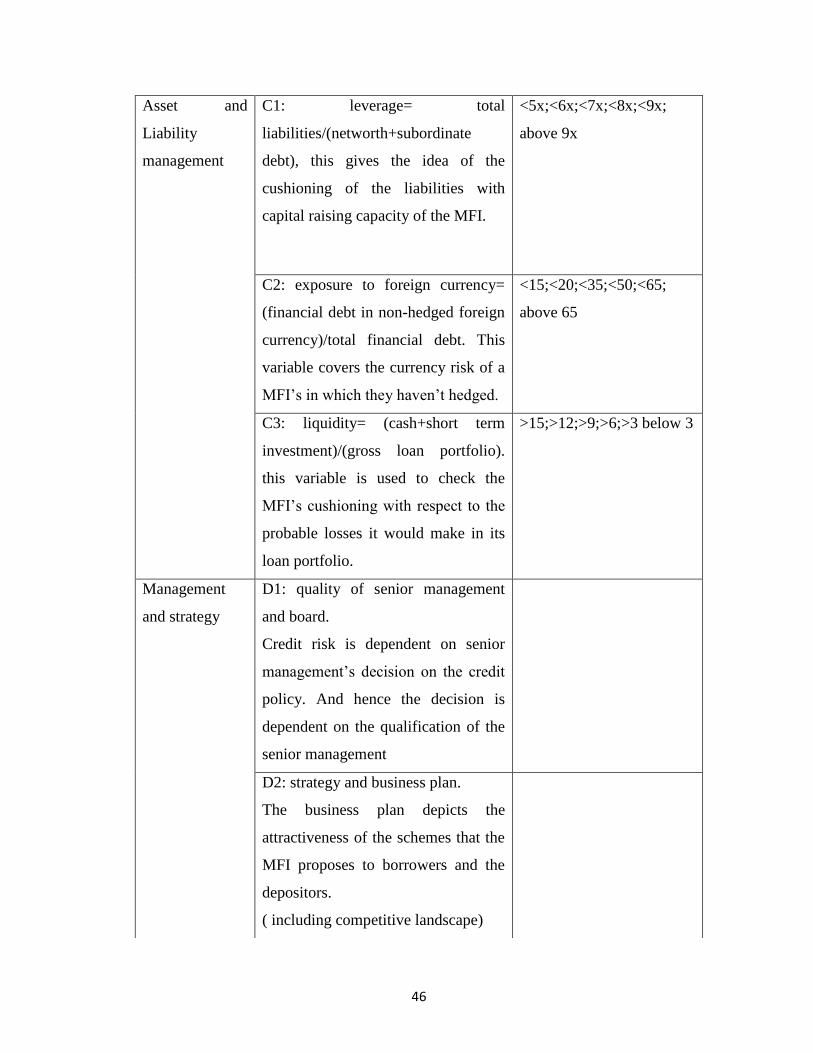

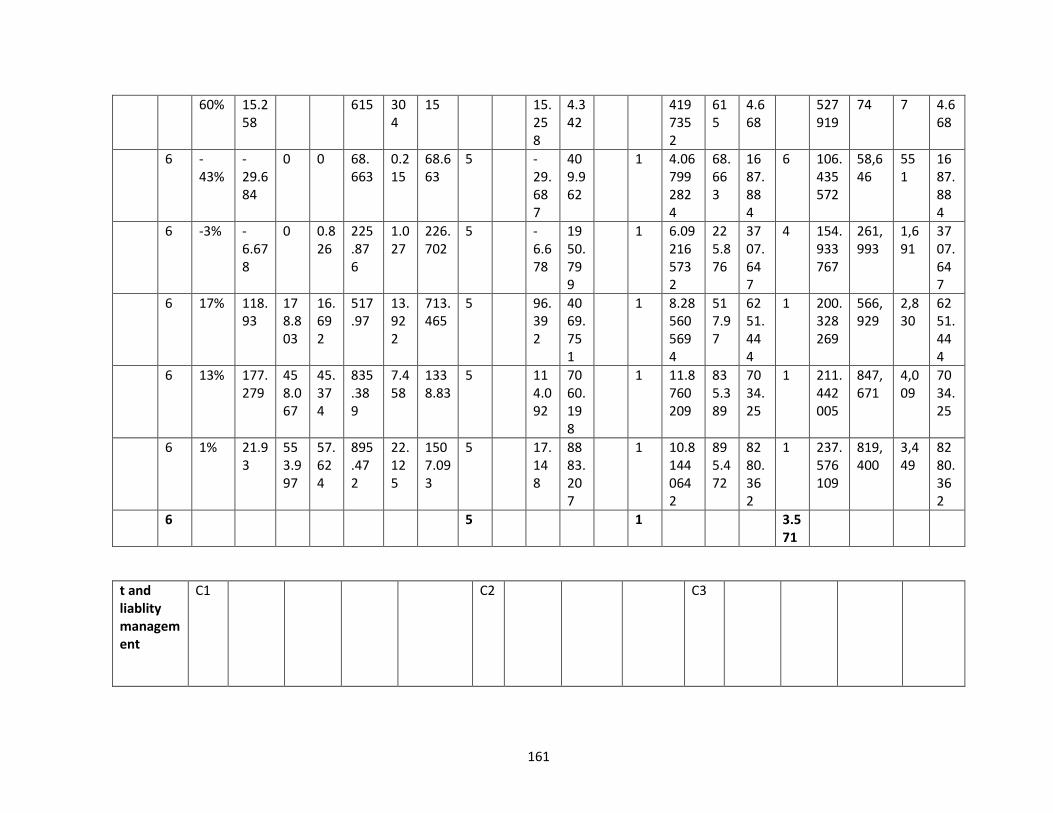

Asset and

Liability

management

C1: leverage= total

liabilities/(networth+subordinate

debt)

<5x;<6x;<7x;<8x;<9x; above

9x

C2: exposure to foreign

currency=(financial debt in non-

hedged foreign currency)/total

financial debt

<15;<20;<35;<50;<65; above

65

C3: liquidity= (cash+short term

inverment)/(gross loan portfolio)

>15;>12;>9;>6;>3 below 3

Management

and strategy

D1: quality of senior management

and board

D2: strategy and business plan

( including competitive landscape)

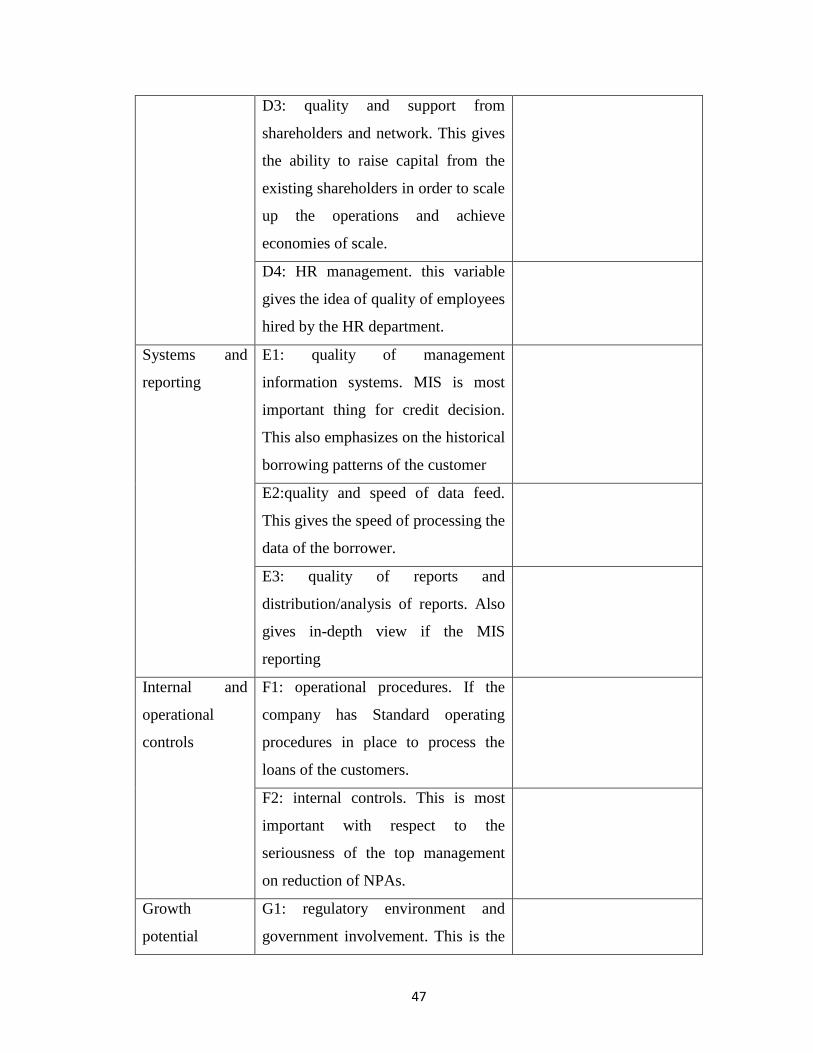

D3: quality and support from

shareholders and network

D4: HR management

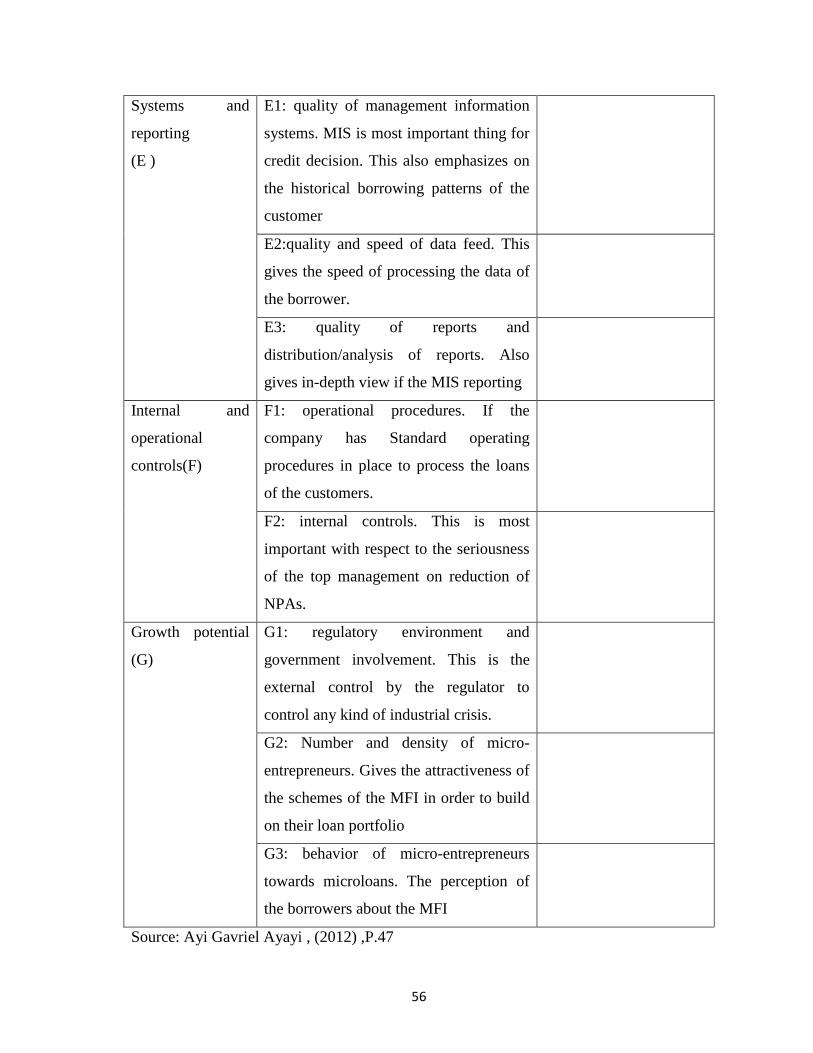

Systems and

reporting

E1: quality of management

information systems

E2:quality and speed of data feed

15

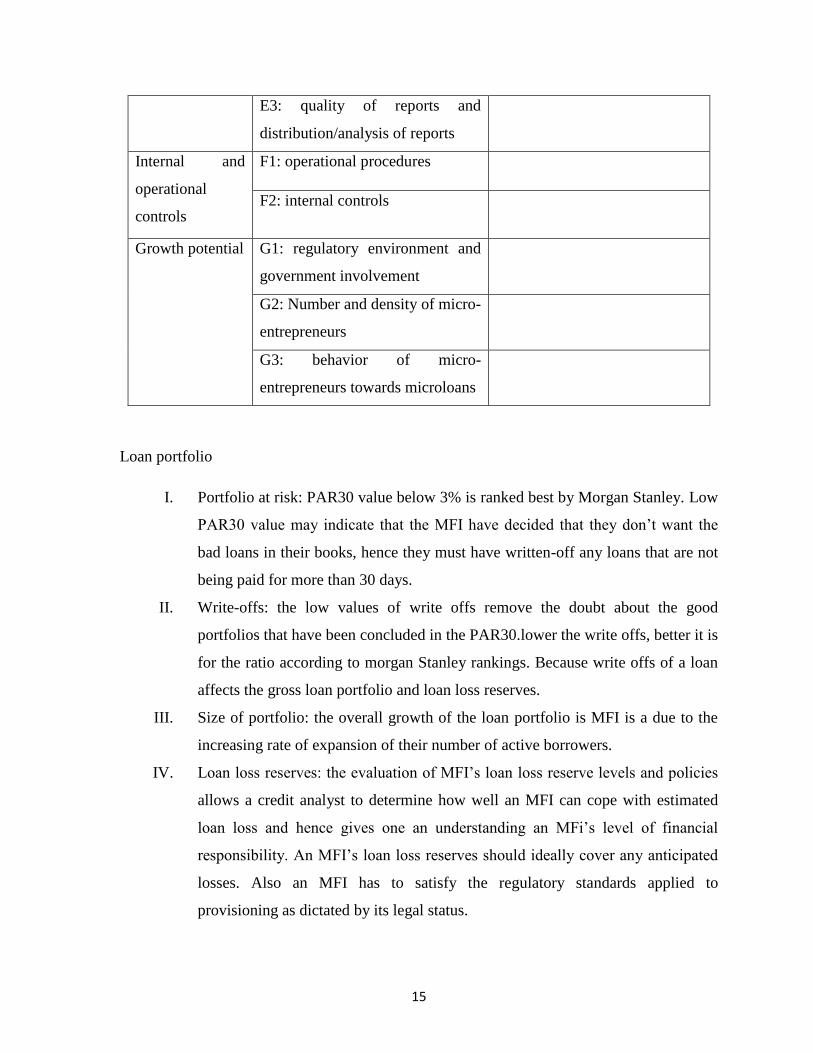

Loan portfolio

I. Portfolio at risk: PAR30 value below 3% is ranked best by Morgan Stanley. Low

PAR30 value may indicate that the MFI have decided that they don‟t want the

bad loans in their books, hence they must have written-off any loans that are not

being paid for more than 30 days.

II. Write-offs: the low values of write offs remove the doubt about the good

portfolios that have been concluded in the PAR30.lower the write offs, better it is

for the ratio according to morgan Stanley rankings. Because write offs of a loan

affects the gross loan portfolio and loan loss reserves.

III. Size of portfolio: the overall growth of the loan portfolio is MFI is a due to the

increasing rate of expansion of their number of active borrowers.

IV. Loan loss reserves: the evaluation of MFI‟s loan loss reserve levels and policies

allows a credit analyst to determine how well an MFI can cope with estimated

loan loss and hence gives one an understanding an MFi‟s level of financial

responsibility. An MFI‟s loan loss reserves should ideally cover any anticipated

losses. Also an MFI has to satisfy the regulatory standards applied to

provisioning as dictated by its legal status.

E3: quality of reports and

distribution/analysis of reports

Internal and

operational

controls

F1: operational procedures

F2: internal controls

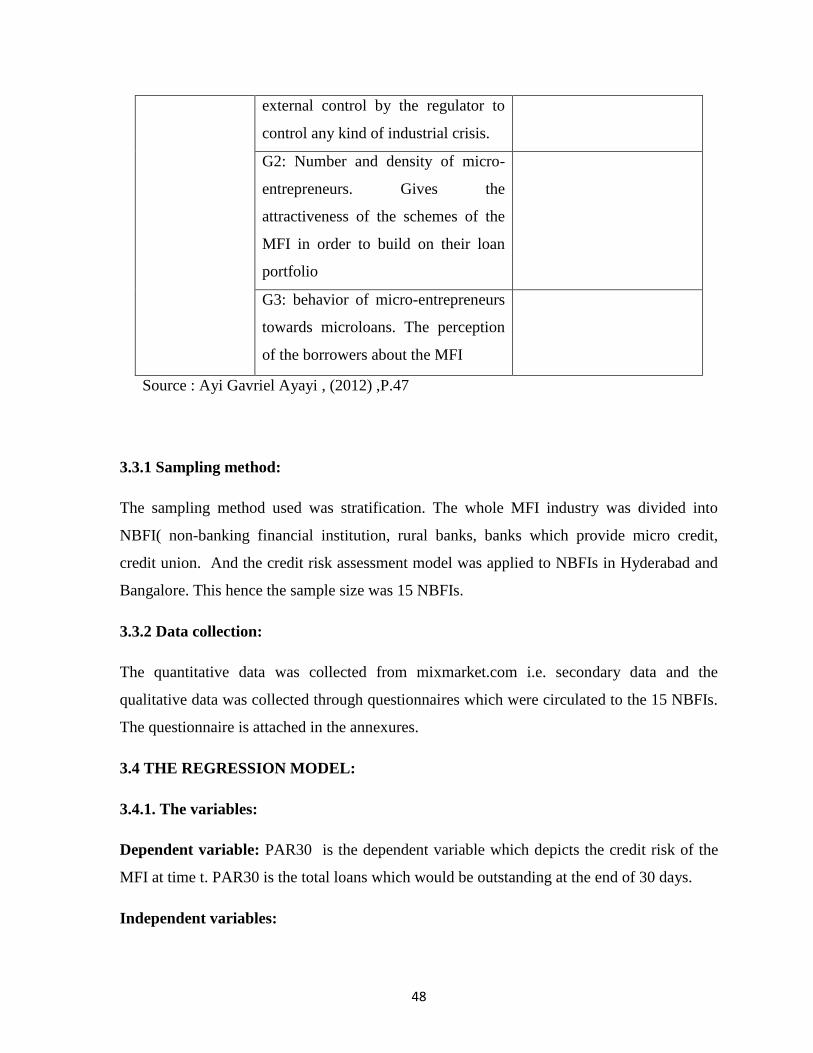

Growth potential G1: regulatory environment and

government involvement

G2: Number and density of micro-

entrepreneurs

G3: behavior of micro-

entrepreneurs towards microloans

16

i) Profitability, sustainability and operational efficiency: this parameter gives the

idea of the financial viability of the MFI. One has to set minimum expected

levels of profitability and cash flow sustainability, while taking into account

the MFI‟s ability to leverage its operational platform and flexibility In the

event of deteriorating margins.

I. Sustainability: this measures the free cash flows, there by reflecting the extent

of an MFI‟s financial cushion against margin or top line shocks.

II. ROAA: takes into account taxes and other sources of revenues, including

income earned on cash in the bank there by providing a more measure for

profitability.

III. Operational efficiency: this indicated the MFI‟s ability to operate efficiently and

leverage its infrastructure.

a) Econometric analysis: for the econometric analysis the MFI for east asia and pacific

were analyzed and correlation matrix for 118 different MFI with 14 variable was

made and conclusions were drawn. Econometric analysis showed that there was no

statistical difference in terms of risk management among different types of MFI.There

was no significant conclusion made even after the econometric testing, morgan

Stanley approach to credit assessment was used to understand the credit risk of the

MFI, the research gap is even though the econometric analysis was done, It was

compared with few MFI in limited to East Asia and Pacific rather than comparing

with the global players in MFI. It indirectly means the researcher narrowed down his

interests to one particular region.

(GUTHRIE, 2010)Determinants of Credit Ratings of Microfinance Institutions in the

Former Soviet Union.This study primarily seeks to explore two questions. First,

whether ratings respond to individual indicators as the existing literature on both the

traditional financial sector and the microfinance sector predict. This is important to

determine perception of credit risk of microfinance benchmarking it with other

financial institutions. It tries to determine the optimal model for predicting the credit

rating of a MFI given number of independent variable This tries to use the traditional

rating agencies and financial institutions to MFI and specialized rating agencies. Also

it expands little work that has been done on determining contributors to a strong

17

credit rating of MFI and fills a gap in the knowledge regarding the optimal model for

predicting an institution‟s credit rating.This research is based on the work from

Gutierrez and Serrano.The work from Gutierrez and Serrano finds 5 key components

to credit rating.Size was found to positively impact the credit rating and is consistent

with the research on contributors to ratings of Russian financial institutions.

Profitability and efficiency also were identified as positive contributors to credit

ratings.Increased risk and lower portfolio quality harmed a firm‟s rating. The work

for Gutierrez and Serrano showed that metrics or social performance have no bearings

on ratings of MFI.The rating agencies are primarily concerned with identifying

probability of default, not a firm‟s impact on poverty alleviation or economic

development. This analysis has replicated the model proposed by Gutierrez and

Serrano , to establish the validity of the results for MFI. But the paper also expands

to identify the specific model that best predicts the rating of an MFI.The paper

surveys the rating agencies of the MFIs and identifies the following

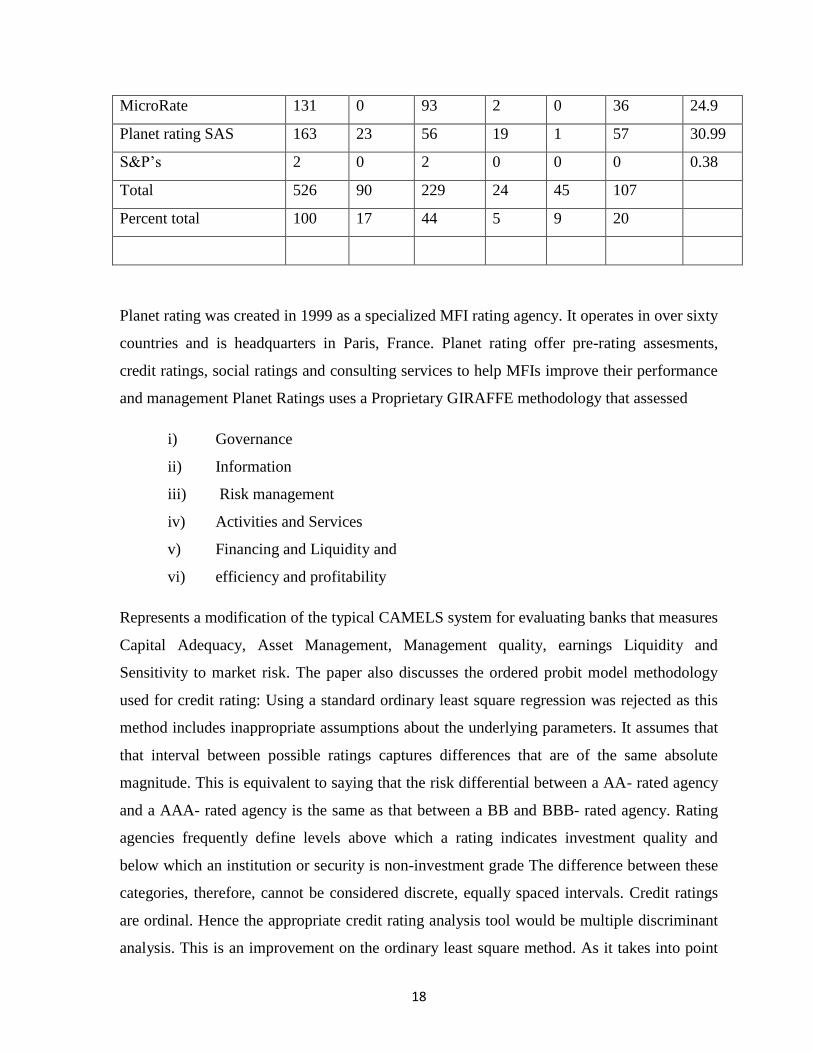

Table 2.4: Ratings of microfinance institutions

Ratings ECA LA MENA SA SSAf %

total

Apoyo and associados

internacionales S.A.C

1 0 1 0 0 0 0.19

Class and asociados

S.A.

3 0 3 0 0 0 0.57

CRISIL 24 0 1 0 21 0 4.56

Ecuability 2 0 2 0 0 0 .38

Equilibrium 8 0 8 0 0 0 1.52

Feller Rate 1 0 1 0 0 0 0.19

Fitch Ratings 10 0 10 0 0 0 1.9

JCR-VIS credit rating

company LTD

1 0 0 0 1 0 .19

M-CRIL 46 6 0 0 21 0 8.75

Microfinanza rating Sri 134 61 52 3 1 14 25.9

18

MicroRate 131 0 93 2 0 36 24.9

Planet rating SAS 163 23 56 19 1 57 30.99

S&P‟s 2 0 2 0 0 0 0.38

Total 526 90 229 24 45 107

Percent total 100 17 44 5 9 20

Planet rating was created in 1999 as a specialized MFI rating agency. It operates in over sixty

countries and is headquarters in Paris, France. Planet rating offer pre-rating assesments,

credit ratings, social ratings and consulting services to help MFIs improve their performance

and management Planet Ratings uses a Proprietary GIRAFFE methodology that assessed

i) Governance

ii) Information

iii) Risk management

iv) Activities and Services

v) Financing and Liquidity and

vi) efficiency and profitability

Represents a modification of the typical CAMELS system for evaluating banks that measures

Capital Adequacy, Asset Management, Management quality, earnings Liquidity and

Sensitivity to market risk. The paper also discusses the ordered probit model methodology

used for credit rating: Using a standard ordinary least square regression was rejected as this

method includes inappropriate assumptions about the underlying parameters. It assumes that

that interval between possible ratings captures differences that are of the same absolute

magnitude. This is equivalent to saying that the risk differential between a AA- rated agency

and a AAA- rated agency is the same as that between a BB and BBB- rated agency. Rating

agencies frequently define levels above which a rating indicates investment quality and

below which an institution or security is non-investment grade The difference between these

categories, therefore, cannot be considered discrete, equally spaced intervals. Credit ratings

are ordinal. Hence the appropriate credit rating analysis tool would be multiple discriminant

analysis. This is an improvement on the ordinary least square method. As it takes into point

19

the ordinal nature of the credit rating and treats each rating as a separate category and

requires more significant assumptions about the distribution of the independent variables.

The coefficients on the parameters will differ in interpretation from thos associated with the

standard ordinary least square method The positive sign indicates a positive impact on the

dependent variable. The magnitude of impact is not a direct linear relationship.

P(yt = 1) = F(c1 – xt*β),

P(yt = 2) = F(c2 – xt*β) - F(c1 – xt*β)

. . .

P(yt = k - 1) = F(ck-1 – xt‟*β) - F(ck-2 – xt*β)

P(yt = k) = 1 - F(c k-1 – xt*β)

The function F is cumulative distribution on function of a standard normal random variable.

Parameters are the vector of slop coefficients β and the threshold values c.This study has

contributed to the literature on microfinance in a number of ways. Donors and lenders can

also use the results to target specific areas .He attempted to apply the existing research to

some other area, which he was focusing on former soviet union ,using the research from

latin America.

(Muriu, 2011) what explains the low profitability of Microfinance Institutions In Africa? To

find out why MFIs of other regions have positive profits and those operating in sub-Sahara

Africa(SSA) economies continue to post negative profits. Also finds out the determinants of

MFI profitability Find the relation between credit risk, managerial efficiency, capitalization

with profitability. Corruption effect on the profitability. There are few observations in the

paper that the author has made. Even though there is a high loan repayment rates, only few of

the MFIs are profitable. The MFIs in Africa have on an average consistently posted negative

profits compared to other regions. Hence the two goals of the paper are:Identify on the basis

of empirical evidence and in a single static framework, significant determinants of MFI‟s

profitability.Investigate if the MFIs can maximize profits or whether they are pursuing

additional objective as well. The research was based on determinants of profitability in MFI

sector hence the author has built a model based on the same.MFI industry is characterized by

a different function to that of retail banks of any other profit seeking corporate entity. Hence

20

multivariate regression model was used to for the same. The linear regression model that was

predicted was based on the literature reviews. Hence the determinants are

Size: this variable was used to capture the economies of scale or diseconomies of scale in the

market.

Age: age is introduced in model to capture the learning effects. From the literature review of

the author, older firms have more amount of experience in the same industry hence enjoy

higher profits

Capital assets ratio (CAP): high CAP ratio signifies that the MFI is operating over cautiously

and ignoring profitable investment opportunities. On the contrary the cost of insurance

against bankruptcy can be high for MI with low CAP ratio. The gearing ratio defines the

source of business finance to boost financial performance.

Credit risk: this is another determinant in MFI industry. Poor quality of credit reducs the

profitability of the MFI. Hence the negative relationship between credit risk and the

profitability. This is calculated by taking sum of the level of loans past due 30 days or more

and still accruing interest hence portfolio at risk( PAR30) . write off ratio which is the value

of loans written off during the year as uncollectible as a percentage of average gross portfolio

over the year. Other measure for credit risk is risk coverage(RC) ratio which is measure as

the adjusted impaired loss allowance/PAR30. Loan loss reserve ratio this is measured by

ratio of loan loss reserves to gross loans.

Efficiency: is expenses management should ensure a more effective use of MFI‟s loanable

resources. Higher ratios of operating expenses to gross loan portfolio imply a less efficient

management. From the literature review we can say that microfinance is a costly business

since it has high transaction cost and information cost. This is measured by operating

expense/average gross loan portfolio and in robustness tests, cost per borrower can be used

The other two proxies , Macroeconomic environment, inflation and real GNI per capita

growth. Dependent variable is ROA or ROE. Efficiency in delivering microfinance is an

important determinant of profitability.A major drawback of the negative profitability in SA

could be due to the fact that the managerial practices have come down due to the increase in

21

technological innovations. Higher spending could be due to the same reasons. the main

research gap is the analysis was based on literature review rather than actually coming up

with original work.

(Venkataraman, 2006)To measure each kind of risk in the Basel II norm through a

comprehensive IT solution. Risk identification, Quantitative risk measurement, Risk

mitigation, Minimum capital allocation. The 3 pillars of Basel II are

a) Pillar I: minimum capital requirement

b) Pillar II: supervisory review process

c) Pillar III: market discipline requirements

Types of risk

a) Credit risk; default by the borrower to repay the borrowings

b) Market risk: volatility of the bank‟s portfolio due to change in market factors

c) Operational risk: risk arising out of banks inefficient internal processes, systems,

people or external events like natural disasters, robbery,etc

Minimum capital allocation for credit risk: Standardized approach: external credit rating

agencies , capital allocation and credit rating are inversely proportional. Internal rating,

Foundation IR approach, Advanced IR approach, In both the methods capital allocated is

based on the following 3 factors ,EAD exposure at default: amount of facility that is likely to

be drawn in default,LGD loss given at default: measure the proportion of lost exposure n

default Probability of default(PD) chances of default in terms of percentage (default- fails to

repay borrowings) Minimum capital allocation for market risk: VAR is used to measure

market risk. VAR measures the likely loss in value of a portfolio over a iven time period with

specified probability. Minimum capital allocation for operational risk: These three methods

are used to measure and allocate operational risk.Basic indicator approach: capital charge

should be 15% banks average annual positive gross income over previous years.

Standardized indicator approach: in this approach the bank activities are classified into 8

business line. Each business line is having an exposure indicator which is multiplied by the

factor( beta) will give the capital charge for operational risk. Advanced measurement

approach: loss distribution approach is of the advanced versions in this approach, in which

22

the impact of significant operation events on various business lines of banks and frequency of

occurrences of these events are captured in the form of normal distribution.

(I.B., 2007) performance of microfinance providers in karnataka. Objective of the study To

study the growth and pattern of microfinance in Karnataka.To evaluate the business

performance of the Microfinance providers.To study the impact of micro financial

institutions on member enterprises .To identify the constraints faced by the microfinance

providers. The data for the research was collected from the primary source with respect to

amount lent, portfolio lending by microfinance providers, cost and returns involved in each

activities, recovery performance under micro financial activities in selected districts was

collected with the help of a questionnaire. Analytical techniques used are.Triennium

averages: the 1st three years average and the last three years averages was calculated because

of plausibility of large number of continuous time series data . the annual average growth in

percentages calculated by dividing the changes during the period by number of years in the

study period.this is done to study the performance of microfinance activities undertaken by

non government microfinance providers Compounding growth rate analysis: the growth in

the number of SHGs credit link, banks loan and refinance of microfinance providers can be

assessed by taking for 14 year period.And the compound growth were computed by using

exponential function of the form.

Yt=ABtUt

where

Yt is SHG credit linked/bank loans/refinance/ number of family assistd/recovery/over dues

A is the time period

Ut= error term

B= 1+G where g is the growth rate

By taking logarithm

We see that log(Yt)=log A+t log B+log Ut

23

Which is of the form

Qt=a+bt+Ut

Hence g=antilog(b)-1*100

Paired t test: to find out the impact of NGOs on the SHGs the paired t test was done. Which

is statistical test for finding the differences in performance of SHGs before and after joining

the NGOs who are involved in microfinance. Impact index: the impact of the NGO on the

SHGs was also assessed using the scoring pattern Impact index=(average scored

obtained)/(average maximum scored to be obtained).The pattern of growth of SHGs in the

state 1992-1993 to 2005-2006 and that the importance of SHGs has increased in the lives of

the poor people and that the microfinance may also be possible because of refinance support

provided by the apex level institutions involved in microfinance. The total amount of loans as

expanded considerably through NABARD especially from selected villages.

(Saltzman, 1998)Capital Adequacy. The objective of the capital adequacy analysis is to

measure the financial solvency of an MFI by determining whether the risks it has incurred

are adequately offset with capital and reserves to absorb potential losses. There are three

indicators:First one is leverage, explains the relationship between the risk-weighted assets of

the MFI and its equity. Second one is ability to raise equity, a qualitative assessment of an

MFI‟s ability to respond to a need to replenish or increase equity at any given time. the third,

is adequacy of reserves, is a quantitative measure of the MFI‟s loan loss reserve and the

degree to which the institution can absorb potential loan losses.

Asset Quality. The analysis of asset quality is divided into three components

PORTFOLIO QUALITY: Portfolio quality includes two quantitative indicators: portfolio at

risk, which measures the portfolio past due over 30 days; and write-offs/write-off policy,

which measures the MFI‟s adjusted write-offs based on CAMEL criteria

PORTFOLIO CLASSIFICATION SYSTEM: entails reviewing the portfolio‟s aging

schedules and assessing the institution‟s policies associated with assessing portfolio risk.

24

FIXED ASSETS: fixed assets, one indicator is the productivity of long-term assets, which

evaluates the MFI‟s policies for investing in fixed assets.

MANAGEMENT: Five qualitative indicators make up this area of analysis:

Governance, human resources, processes, controls, and audit, information technology

system, strategic planning and budgeting. EARNINGS: Three quantitative and one

qualitative indicator to measure the profitability of MFIs: Adjusted Return On Equity:

measures the ability of the institution to maintain and increase its net worth through earnings

from operations. Operational Efficiency: measures the efficiency of the institution and

monitors its progress toward achieving a cost structure that is closer to the level achieved by

formal financial institutions. Adjusted Return On Assets: measures how well the MFI‟s

assets are utilized, or the institution‟s ability to generate earnings with a given asset base.

Interest Rate Policy: to assess the degree to which management analyzes and adjusts the

institution‟s interest rates on microenterprise loans (and deposits if applicable), based on the

cost of funds, profitability targets, and macroeconomic environment. Liquidity

Management:evaluates the MFI‟s ability to accommodate decreases in funding sources and

increases in assets and to pay expenses at a reasonable cost. Indicators in this area are

liability structure, availability of funds to meet credit demand, cash flow projections, and

productivity of other current assets. Under liability structure, CAMEL analysts review the

composition of the institution‟s liabilities, including their tenor, interest rate, payment terms,

and sensitivity to changes in the macroeconomic environment.

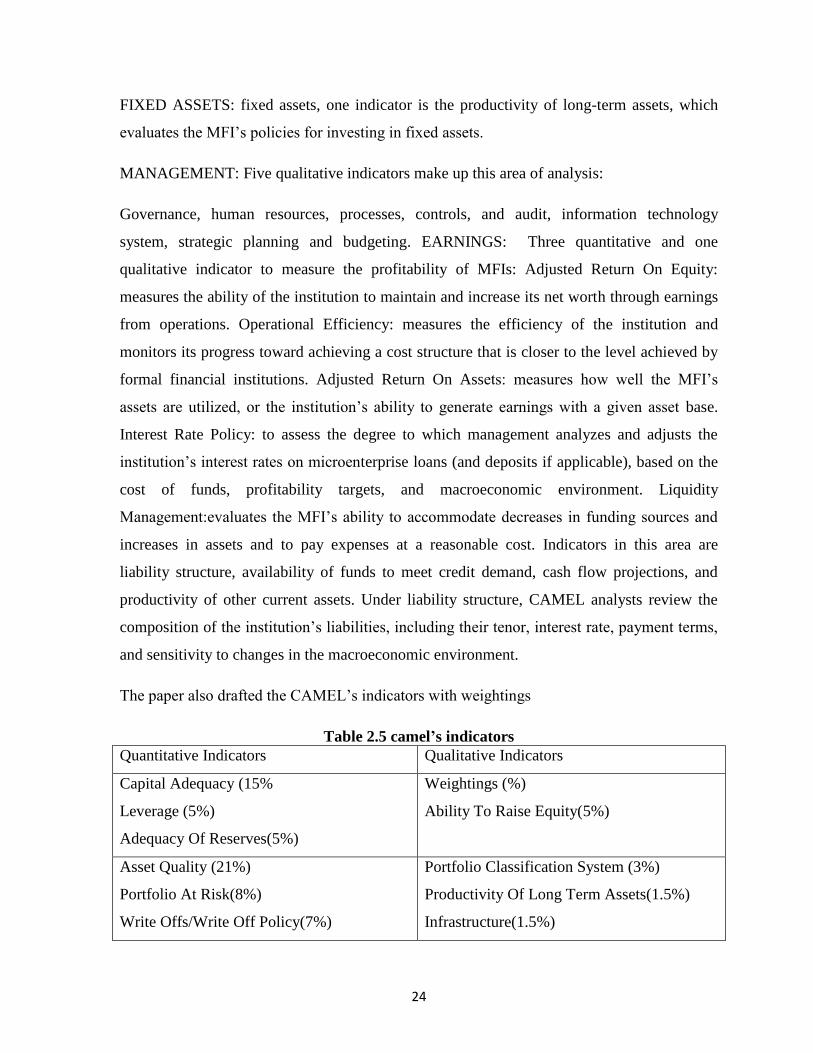

The paper also drafted the CAMEL‟s indicators with weightings

Table 2.5 camel’s indicators

Quantitative Indicators Qualitative Indicators

Capital Adequacy (15%

Leverage (5%)

Adequacy Of Reserves(5%)

Weightings (%)

Ability To Raise Equity(5%)

Asset Quality (21%)

Portfolio At Risk(8%)

Write Offs/Write Off Policy(7%)

Portfolio Classification System (3%)

Productivity Of Long Term Assets(1.5%)

Infrastructure(1.5%)

25

Management(23%) Governance/Management (6%)

Human Resources (4%)

Processes, Controls, And Audit (4%)

Information Technology System (5%)

Strategic Planning And Budgeting( 4%)

Earnings (24%)

Return On Equity (5%)

Operational Efficiency( 8%)

Return On Assets (7%)

Interest Rate Policy (4%)

Liquidity Management (17%)

Productivity Of Other Current Assets (2%)

Liability Structure( 8%)

Availability Of Funds To Meet Credit

Demand (4%)

Cash Flow Projections( 3%)

Total(100) 47% 53%

(Barman, 2009) Role Of Microfinance Interventions In Financial Inclusion: A Comparative

Study Of Microfinance Models.To study the relationship between the level of indebtedness

to moneylenders and the type of microfinance model through a case study in Varanasi, U.P.

Comparing two microfinance models prevalent in the research area.This survey was

conducted among 59 households of twelve villages covering four blocks of the selected

district. Primary data on different socio-economic aspects of the households and details of

micro-financial services availed by them were collected directly from the clients through the

structured questionnaire and personal interview. Qualitative information was collected

through Focus Group Discussions (FGDs) and semi-structured interviews of the bankers,

NGOs and MFIs operating in the area to understand the supply-and demand sides of the

problem of microcredit in the selected research area. The collected data are subjected with

the chi-square statistical test in order to determine if there is significant variation in the

tendency to borrow from the moneylenders among clients of SHG and MFI model of

microfinance. The test is applied when one has two categorical variables from a single

population. It is used to determine whether there is a significant association between the two

variables i.e. indebtedness to moneylender and being client of particular type of microfinance

26

model.The authors conclude that the level of indebtedness to moneylenders is higher in the

case of clients of Microfinance Institutions (MFI) model and without complete information

on the credit-worthiness of borrowers, MFIs may contribute to the over-indebtedness of their

clients as well as damage in their performance. there could be more number of variables

which could affect the indebtedness to money lenders.

(Khan, 2012)The main aim of this paper is to provide with a literature review on previous

work n transaction costs including operating costs, in microfinance.The second part of the

paper describes the research modalities followed by a section which provides the findings

based on empirical evidenvr.The depth into one case study of lean cost management .

Provides managerial recommendations. The data was collected from Microfinance

information exchange(MIX).the parameters considered were Average loan balance

outstanding per borrower in USD,Gross loan portfolio in USD,Number of depositors, Cost

per borrower in USD,Operating expenses as a percent of the gross loan portfolio, Nominal

yield on gross loan portfolio , And based on these data longitudinal analysis was conducted

from the data from MIX and analysis of top 10 MFIs, which accounted for about 92% of the

clients over the past 10 years. Time series data for outreach was presented and the top 3 mFIs

are in the league of their own and are about equal in size of growth rates. There are number

of factors that attribute to an MFI having lean operation and being cost effective. The

operating costs differ significantly for different institutions and can be attributed to achieving

economics of scale in operations .They saw that it is possible to adopt cost effective

operating structure while operating in same service space as other less efficient MFIs. they

used the existing literature to find out the costs that the MFis incur rather than using primary

data to find out about the different types of costs.

(Karlan, 2008) Credit Elasticities in Less-Developed Economies: Implications for

Microfinance.Test the assumption of price inelastic demand using randomized trials

conducted by a consumer lender in South Africa.identify demand curves for consumer credit

by randomizing both the interest rate offered to each of more than 50,000 past clients on a

direct mail solicitation, and the maturity of an example loan.The sample frame consisted of

all individuals from 86 predominantly urban branches who had borrowed from the Lender

27

within the past 24 months, were in good standing, and did not currently have a loan from the

Lender as of 30 days prior to the mailer. pilot-tested in three branches during July 2003

(wave 1), and then expanded the experiment to the remaining 83 branches in two additional

waves that started with mailers sent in September 2003 (wave 2) and October 2003 (wave

3).the randomized field experiment to estimate price and maturity elasticities of demand for

consumer credit. The sample includes former borrowers from a major, for-profit, South

African consumer micro lender to the working poor. In the Lender‟s case, the cost of

reducing interest rates (lost gross interest revenue on infra marginal loans) slightly exceeded

the benefits (increased gross revenue from marginal borrowing, increased net revenue from

higher repayment rates)

(Eversole, 2003)help, risk and deceit: micro entrepreneurs talk about microfinance. To find

the relation between the ostensibly commercial transactions which converted into complex

assumptions about the social development, external assistance and power? To illustrate the

divide between developed and developed in their shared quest to help business grow and

concludes that building strong lending institutions does not automatically translate into broad

based benefits for micro entrepreneurs of their businesses. While international agencies

priorities the development of sustainable microfinance organization to provide loans to the

micro and small businesses, the business people themselves may see their own interests as

quite different for those of the organizations meant to serve them. The reasons for this were

many such as loan products that were suited to only certain kinds of businesses, businesses

which were ill equipped to take out loans. Expectations that help equated to short term

assistance and flexible repayment schedules and assumptions that corruption was likely to be

rampant whenever development money arrived.

(Barone, 2011)Exploring Household Microfinance Decisions: An Econometric Assessment

For The Case Of Ghana. To analyze the relationship between household financial

instruments by determining the link between insurance coverage and household savings. The

data set used for the purposes of this paper uses data from 351 households captured at one

period in time. Because the data is not dynamic, a two-step approach is used to analyze the

relationship between insurance coverage and savings at the household level .

Variables:

28

a) Insurance purchase:

i) Health Insurance

ii) Life Insurance

iii) Old age Insurance

iv) Other Insurance

b) Savings:

i) Total HH savings

c) Shocks to house holds

i) Weather shock

ii) Crime shock

iii) Business shock

iv) Loss of job

v) Death of worker

vi) Illness of worker

vii) Family shock

viii) Severity of shock

d) Risk perception

i) Share of ill

ii) Share of injured

e) Additional risk measures:

i) Share of employed

ii) Share of dependents

iii) Avg HH age

iv) Life expectancy

v) Risk aversion measure

vi) Risk aversion measure

f) Income

g) Controls:

1) Female head

2) Age (in years)

3) Education (in years)

29

4) HH earnings (occupational)

5) HH additional earnings

6) Distance to health provider (in km)

7) Vaccinations

8) Private Hospital

9) Health center1

10) Chemist/Pharmacist

11) Government Hospital

12) Mission Hospital

The sample mean , std dev of each of the variables was taken and analyzed based on the data.

Regression model of the nature:

P( Y=1, Health insurance) = α+β1 savings+β2 life insurance + β3 old age insurance +µ

Was constructed and regression analysis was done There are a variety of reasons to support

this claim. Financial tools, when used in unison, provide households with options for

managing assets. Prior to a shock, households can allocate income between savings and

insurance products to help protect against potential risks. The findings of this paper suggest

expanding access to products increases use through simple exposure. Households use saving

mechanisms and insurance products, they appear to increase their use of both products.

(crabb, 2007) foreign exchange risk management practices of microfinance institutions. to

review the current practices in the management of forex risk for and by MFIs.The advantages

and disadvantages of these practices The standard framework of the Forex risk measurements

are ,MeasuringVAR to exchange rate fluctuations,Purchasing derivatives of adjusting

portfolios to offset this risk, Continuously monitor the risk position.Diversify both the source

of debt capital and the use of debt capital, Insuring the risk of devaluation in the network,

Using currency swaps. Three general conclusions can be drawn from this study of Forex

exchange risk and MFIs.First need additional funding to meet demands and debt capital is

most likely source for funding. Second Forex exchange rate risk is significant and though it is

only one factor in a decision to lend to a MFI , it is a strong deterrent. The risk devaluation

against most major currencies such as the US dollar and the Euro is high and it is in these

30

currencies that any new debt capital is likely to be denominated. The existing Forex practices

are prohibitively expensive, either to the client or the institution. the potential intermediaries

or counter parties to any potential currency swap agreements were not discussed in the paper.

(Abiola, 2011)impact analysis of microfinance in Nigeria. To apply the financing constraints

approach to study whether microfinance institutions improve access to credit for

microenterprise in Nigeria or not. This paper is based on generating financial constraint

theory model thing or an event.

Pri = (1+ exp(-λi))-1, where λ is linearly dependent on the variables hypothesized to affect

the probability: λi = α + βXi.

The probability thus varies from 0 to 1 (λ = ±∞), and the model is simplified by rearranging it

into a log of the odds,

ln(Pi /(1 - Pi)) = α + βXi.

Which, for examples consists of individual outcomes, and can be estimated with maximum

likelihood. Interpretation of the coefficients can also be done by reverting back to the

probabilities. Thus,

Pr(IFA = 1) = f(α + β1IF + β2IO + y/Z)

where IFA is the decision to invest in fixed assets, IF is the variable for internal funds capital;

IO is the investment opportunity variable, and Z is a vector of variables that capture various

characteristics of the enterprise and the states in which it operates. Firms without investment

opportunities would not invest even if they had capital. Thus, control for investment

opportunity (IO) and separated it from the effect of internal funds (IF). The paper uses the

financing constraints approach to study the impact of microfinance on access to credit for

microenterprises in nigeria.The model contained ten independent variables (average profit,

market & skill, hired employee, asset loan, enterprise age, internally generated revenue,

business location, entrepreneur gender and availability of investment opportunity).They show

that MFBs improved access to credit in locations where more MFBs offered financial

products because investment in local microenterprises was less sensitive to availability of

internal funds in unconstrained location, than investment in microenterprises in locations

31

where microfinance activities were limited or non-existent and where micro entrepreneurs

had to rely more on internal funds for investment. Popularity of microfinance forces MFBs to

be more transparent and thereby decreases the cost of assembling a database with MFBs

branch distribution, therefore making the financing constraints approach more attractive for

use in the future.

(Rahman, 2011)The Development Perspective of Finance and Microfinance Sector in China:

How Far Is Microfinance Regulations? The paper reviews the development process of bank

and microfinance sector in China and presents their regulatory status. Research methodology:

since this paper is a review of existing literature there is so quantitative research

methodology. Microfinance structure and their services Since the first microfinance seed was

planted in China, a vast number of different types of microfinance operators have appeared

within the Chinese market. Generally, there are three broad categories of microfinance

service providers. These include,Micro-credit by financial institutes This category mostly

includes state own formal microfinance service providers i.e. ABC, ADBC, RCCs, Rural,

Commercial Bank, Rural Cooperative Bank, Postal Savings, China Development Bank

(CDB), MCC, VTB, LC, andRMCCs. The microfinance market share is dominated by these

providers.,Micro-credit by NGOs & international organizationsThe service providers are-

NGOs, international organizations and social organizations. The internationalorganizations

have been providing financial services as project based with the collaboration of government

agencies.They also incorporate different services beside micro-credit i.e savings, training in

project sites. NGO lending services have covered countrywide and large volume of business.

Micro-credit by Government agencies This category provides micro-credit focusing on the

government poverty reduction program. For instance, Urban Credit Bank (UCB) was

established to support laid-off workers which ultimately expanded micro-credit services to

urban areas.Only NGO-MFIs and MCCs are non-financial institutions and consequently not

allowed to work with savings or receive funding from commercial banks –thus, preventing

them from enjoying economies of scale Even the lending companies are also not allowed to

work with savings. In addition, the three newly created rural financial institutions (VTBs,

LCs, and RMCCs) as well as MCCs are subjected to geographical restriction. The traditional

collateral system for micro-financing still exists particularly for micro-lending companies,

lending companies, postal saving banks, MCCs, and VTBs. Even RCCs and UCCs have

32

followed a special kind of collateral to credit disbursement. RCCs required collateral for

large loan amounts and UCCs required companies guarantee. On the other hand, the donor

funded projects (UNDP, UNFPA, UNICEF, Heifer Project, World Vision, Oxfam Hong

Kong and CIDA) are allowed to providing micro-credit services by collaboration with

government departments or agencies having certain conditions. that the banking and

microfinance services have expanded and improved gradually. Hence, the banking sector is

close to the maturity stage while the microfinance sector is still at learning stage. CBRC is

the sole institute to deal with policy regulations for banks and microfinance service providers

which may contradict to handle different goal oriented institutes (Banks and MFIs run their

business in different perspectives).Author recommended to the concerned authorities to have

a balanced policy regulation for the microfinance

(Jiwani, 2007) Sustainable Microfinance: The Impact Of Pay For Performance On Key

Performance Indicators. This study investigated the relationships between pay-for-

performance incentive programs and loan officer productivity in microfinance institutions

(MFIs).

Loan officers‟ performance is measured by five key performance indicators:

1) new borrowers,

2) portfolio value,

3) average loan size,

4) arrear rate,

5) default rate.

The independent variable is the loan officer‟s financial incentive (the percentage of salary

that is based on performance). Five dependent measures (performance outcomes) have been

examined:

a) number of new borrowers,

b) value of portfolio,

c) average loan size of the borrowers,

d) number of borrowers in arrears (loans overdue > 30 days),

e) number of borrowers in default (loan overdue >90 days).

33

The second research question uses survey questions from supervisors of loan officers, and

loan officers to assess the impact of the productivity level of MFIs with financial incentives

and MFIs without financial incentives: Is there a difference between the productivity level of

loan officers at MFIs with financial incentives and MFIs without financial incentives All five

hypotheses suggested that there would be an increase in productivity with higher incentives.

Results indicated that the number of new borrowers was related to the size of the incentive

program. The negative correlation between the number of new borrowers and the size of the

incentive program indicated that MFIs with larger incentive programs had loan officers with

a smaller number of new borrowers in each month, and overall. There were no relationships

between the size of the incentive program and any of the other performance measures.

(Kundu, 2012)Savings, Lending Rate and Skill Improvement in Microfinance Operating

Through Public-Private Cooperation.microfinance program through joint liability credit

contract is explained with the help of a two-stage game when the program is operated by a

non-motivated NGO with the help of a commercial bank and government. Initially, the

author assume that two homogeneous members belong to the same village form SHG on the

basis of joint liability only for two periods. The group is formed by the initiative of an NGO

whose basic activities are:

1) Motivating local housewives to form SHG;

2) Collecting savings (contribution) from them in installment and giving them technical

knowledge for skill improvement of the participants at the initial stage;

3) Bridging the gap between the group and the bank as well as the government;

4) Maintaining the group corpus;

5) Collecting subsidy and cash credit from the DRDA and bank respectively;

6) Disbursing credit simultaneously to both the members and recovering credit from the

members

7) Generating profit after performing all these activities at the end of the second period.

Government Subsidized Microfinance Program in the Total Absence of Social Sanction:

Suppose each member of the group is willing to contribute (save) x amount in each

installment and each member has to contribute 2t times in each year. The amount saved by

each group member in each installment is deposited in the office of the NGO and the NGO

34

deposits the amount in the linked commercial bank. assume that before getting first credit

from her group, each member has to save t times regularly. During this period, she is also

getting skill-training from the NGO without spending any amount. Total amount

accumulated in the group after contributing for „t‟ times by each member is:

2tx(1 + i) = 2X(1 + i), where 2tx = X.

The NGO withdraws 2X amount from bank and distributes that equally among the group

members as credit against a rate of interest rˆ. The income earned by each member after

utilizing the microcredit as the working capital can be expressed as:

Ym = ƟX, where mϵ {1, 2} ...(1)

Here Ɵ is the degree of technical knowledge gained by each group member after group

formation from the NGO and Ɵ > 1. It is also assumed that the husbands of both the

members are earning members and ready to contribute their entire income for their family.

The annual earning of the husband of each group member is W and 2x < W. At the end of the

first stage, we have four possible levels of consumption of both the member households. If

the group member is well-behaved and is ready to repay her own loan with interest at the end

of the year, then the consumption of the non-defaulter member household will be:

CmGR

= W+ƟX- 2X+ X(1+ rˆ)

where m ϵ{1, 2}

It reestablishes the fact that even in the presence of government subsidy in microcredit

program under joint liability through formation of SHG, social sanction or depriving the

members from enjoying further benefits from the government still plays an important role of

security at the time of repayment of loan.It is also proved that if the group members are not

equally powerful in the society, then in the second stage of the game, the powerful member

applying her social influence and taking advantage of joint liability may force the less

powerful member to repay her loan with interest and enjoy a free ride. So positive assortative

matching, both from the economic as well as social point of view, is necessary at the time of

35

group formation and that should be maintained in both the periods to keep repayment rate

100%.

(Arch, 2005)Microfinance and development: risk and return for a policy outcome perspective

This paper address microfinance- financial services products including credit loans and

insurance which encourage productive and entrepreneurial activity for the marginalized often

unbanked also known as the poverty market. This paper provides the overview of the

microfinance market space, its industry players and it addresses current issues in

development policy. This is a descriptive paper hence the author has considered various