256556875 annat-pai-the-cowherd-of-alawi-amar-chitra-katha-2007-pdf

Upload

michelle-phuaCategory

view

65download

3description

ePROCEEDINGS FOR 2011 INTERNATIONAL RESEARCH CONFERENCE AND COLLOQUIUM Contemporary Research Issues and Challenges in Emerging Economies

1

CORPORATE SOCIAL RESPONSIBILITY DISCLOSURE IN RESPONSE TO CSR AWARD WITH THE MODERATING

EFFECT OF FAMILY GROUP AFFILIATION IN YEMEN

Nahg Abdul Majid Alawi College of Business, Universiti Utara Malaysia,

E-mail: [email protected]

Azhar Abdul Rahman

College of Business, Universiti Utara Malaysia, E-mail: [email protected]

ABSTRACT

In the recent years the Yemeni Government is increasingly calling Yemeni companies to participate in the country‟s economic developments as their social responsibility. Driven by this measure, this study examines the level of corporate social responsibility disclosure (CSR) and its categories made in annual reports, websites, and newspapers of the 73 most active shareholding companies registered in Yemen. The study also examines whether these companies have expanded their corporate social responsibility disclosure in response to CSR Award announcement. Finally, the study seeks to examine factors that may influence the level of corporate social responsibility disclosure by considering the moderating effect of family group affiliation. A content analysis procedure is used to measure the level of corporate social responsibility disclosures over a period of three years which includes the pre and post announcement of CSR Award. The results indicate that while the disclosure level of corporate social responsibility is low, companies have increased the CSR disclosure in response to CSR Award announcement. The OLS regression analysis results indicate that the firm‟s characteristics (company size, industry type, profitability) affect the level of CSR disclosure in Yemen. Interestingly, the moderated multiple regression (MMR) analysis results also reveal that family group affiliation has significant moderating effect on the relationships between firm size, profitability, foreign ownership and CSR disclosure. This study aims to contribute to the CSR literature by providing empirical evidence of the moderating effect of family group affiliation and the CSR disclosure in one of less-developed country.

KEYWORDS: Corporate social responsibility disclosure, Yemen, Family group affiliation, CSR Award.

INTRODUCTION

The Yemeni government has called on the private sectors to participate in the welfare and development of the country in fulfilling their social responsibilities by financially contributing to social programs or by reducing harmful effects of the industrialization to the environment and society at large.

There is noticeable evidence to suggest that some Yemeni companies are developing and implementing social responsibility policies. For example, the Hayel Saeed Anam Group has established the Hayel Saeed Anam and Associates Welfare Corporation and Al-Saeed Foundation for Science and Culture as institutional entities to organize social responsibility action of the group (Hayel, 2008). But unfortunately most companies have singularly failed to embrace any but the traditional model of accounting and “most companies in Yemen are still not aware of the broad view of social responsibility, believing that CSR is no more than building mosques, donations for charities or seasonal work during Ramadan; and these activities do not require any disclosure” (Althawra, 2008).

ePROCEEDINGS FOR 2011 INTERNATIONAL RESEARCH CONFERENCE AND COLLOQUIUM Contemporary Research Issues and Challenges in Emerging Economies

2

In Yemen the disclosure of CSR within the traditional financial reports is no longer optional, but has become an important factor, to allow the government to ensure that this contribution is consistent with Yemen‟s sustainable economic and social development plans. However, Yemen has not passed any legislation or disclosure requirements in this regard, neither in the Companies Act 1997, Labour Act 1998 or Environment Act 1995. In addition, there is no Stock Exchange in Yemen, which would require the disclosure of social responsibility information, as in the case of many developed and developing countries‟ Stock Exchanges that require listed companies to provide information on their CSR activities. For example, in France all companies listed on the Paris Stock Exchange are required to include information about their social and environmental performance in their financial statements. In South Africa, the Johannesburg Stock Exchange requires all listed companies to comply with a CSR based code of conduct. This emphasise the importance of CSR disclosure regulations regarding CSR in these countries.

As there have been no prior studies that have attempted to evaluate the corporate social responsibility disclosure in Yemen, the apparent problem of CSR in Yemen is to what extent Yemeni companies disclose CSR activities to show their partnerships with the government in order to achieve the objectives of sustainable development. Consequently it creates the ability to measure and evaluate whether their participation can be regarded as an act of charity or institutional and it‟s within the framework of sustainable development. In addition evaluate the effect of CSR Award announcement on CSR disclosure. Also what are the factors that might influence this CSR disclosure?

However, this study is important in providing a systematic empirical examination of the patterns of CSR disclosure in Yemen and other least developed countries in general. As it is difficult to generalize the results of studies on developed countries to less developed countries as the stage of economic development is likely to be an important factor affecting CSR practices (Tsang, 1998).

In addition this study seek to provide evidence about the factors that could affect the level of CSR disclosure, which can benefit Yemeni government and companies alike in order to improve the quality and quantity of corporate social reporting (Adam et al., 1998).The objectives of this paper are: (i) to determine the level of corporate social responsibility disclosure practices by companies in Yemen in annual reports, websites and newspapers, (ii) to examine whether companies in Yemen have increased the level of corporate social responsibility disclosures in response to CSR Award, (iii) to determine whether certain firms‟ characteristics (such as size, industry type, profitability and foreign share ownership) are associated with the level of corporate social responsibility disclosure and (iv) to examine the moderating impact of family group affiliation on the association between companies‟ characteristics corporate social responsibility disclosure. This paper contributes to the body of CSR literature in terms of: firstly attempting to fill the gap in CSR literature by conducting the first comprehensive study on CSR in one of least developed countries with no stocks exchange market. Secondly, examine the moderating impact of family group affiliation on the association between company‟s characteristics and corporate social responsibility disclosure. Finally, attempt to fill the gap in CSR literature by examining the effect of CSR Award on the level of corporate social responsibility disclosures.

THEORETICAL FRAMEWORK AND LITERATURE REVIEW 2.1 Legitimacy Theory

The existence, survival and growth of any company require support from the community. In order to gain and sustain this support, companies must report specific information voluntarily, to show and convince the society that their activities, are legitimate and have contributed to the society.

Thus, legitimacy theory is built upon the concept of “social contract” and it considers that the organisation‟s continuous existence will be under threat if society becomes aware that the organisation has violated its social contract. If the society does not agree that the organisation is operating in an acceptable or permissible manner, then the society will end the organisation‟s “contract” to continue its

ePROCEEDINGS FOR 2011 INTERNATIONAL RESEARCH CONFERENCE AND COLLOQUIUM Contemporary Research Issues and Challenges in Emerging Economies

3

operation. Therefore legitimacy theory developed to explain the nature and basis of the relationship between a company and its society is considered to be an essential resource on which an organization is dependent for survival and this is achieved by showing that organizations‟ activities are harmonious with social values (Dowling and Pfeffer, 1975)

Dowling and Pfeffer (1975) stated that there are two elements of consistency in organizations‟ activities and social values: First is the element of action, which refers to the organizations‟ activities that are harmonious with social values. Secondly, is reporting organizational activities that are harmonious with social values, through the use of different strategies. According to Lindblom (1994) there are four different strategies of providing social information to the society to legitimize their behaviors. First, businesses attempt to educate the public about the real changes in corporate performance and activities to fill the legitimacy gap, which arise from their deteriorating performance. Second, businesses attempt to affect the perception of society to reduce the misperceptions on the companies‟ activities that can affect society. Third, businesses attempt to control the perception of society by diverting the attention of public from the serious issues such as pollution to other issue such as social or environmental charities. The last strategy is that businesses attempt to change the understanding of the public when the public have unclear ideas about the performance of the company. Thus, it can be expected that businesses will provide social information (for example community involvement, human resources, physical resources, environment contribution and product and service contribution) for the public to legitimize their activities with the aim of influencing the public and stakeholders‟ perceptions about the organization.

Adams (2002) noted that the reason behind the increase in the number of companies publishing environmental reports since the early 1990‟s, was due to their strategies to support their image with customers, state authorities and journalists without the influence of regulation or public pressure. Furthermore, Zain (1999) also confirmed these strategies that the social reports prepared by corporations are represent a form of advertising to promote or to enhance the company's image and to please the financial statements readers or users or to attract their attention to a particular issue while diverting their attention from the major issue. Belal and Owen (2007) also had similar opinion and argued that CSR development in Bangladesh was driven by a concern to enhance corporate image and to control the perceptions of the main powerful stakeholders in Bangladesh.

It is expected that legitimacy theory could explain the CSR disclosure practice in Yemen as least developed country due to the absence of stock exchange market and the lack powerful NGOs in Yemen, where companies will disclose social information in several medium such as annual reports, websites and newspapers, to improve their image and to ensure the continued inflow of capital, labour and customers necessary for their long-term survival (Neu et al., 1998, p. 265).

Since the mid-1970s, many previous studies investigated the social responsibility disclosures and in various countries and at different time periods .However, only A very few published studies examine the corporate social responsibility disclosure in the Arab world and in least developed countries (LDCs) in general. Abu Baker and Naser (2000) study, one of the earliest studies in Middle East .They examined the corporate social responsibility disclosure practiced in a sample of 143 companies in Jordan using content analysis approach. The result of the show that in terms of space given and subjects covered in annual reports CSD was given a little. However, there was a limited number, of Jordanian companies operating in the banking and manufacturing sectors which have disclosed their CSD responsibilities in a convincing manner. The human resources and community involvement were the most themes disclosed across the four industry group.

Another recent study by Rizk et al (2008) examined CSR disclosure in 60 annual reports of manufacturing companies in Egypt and found that CSR disclosure was low and descriptive in natural .In addition they found that industry type affects the category of disclosure. In Bangladesh, Imam (2000) studied the annual reports of 40 listed companies at Dhaka Stock Exchange for 1996-1997. Of the companies surveyed, 100 percent made some form of human resource disclosure, 25 percent community, 22.5 percent environmental and 10 percent consumer. The study concluded that the disclosure level was very poor and inadequate.

ePROCEEDINGS FOR 2011 INTERNATIONAL RESEARCH CONFERENCE AND COLLOQUIUM Contemporary Research Issues and Challenges in Emerging Economies

4

Figure1. The relationship between company‟s characteristics and CSR disclosure with the moderating affect of family group affiliation.

Figure 1 lists company size, industry type, profitability and foreign ownership as the essential four company‟s characteristics. The study‟s conceptual framework is completed with family group affiliation as moderating variable and CSR disclosure as the dependent variable. CSR disclosure is measured by particular CSR information disclosed by the company in its annual report, website and newspaper. Company‟s characteristics (company size, industry type, profitability and foreign ownership) are expected elements that may lead Yemeni companies to disclose CSR. The following section discusses the hypotheses development.

HYPOTHESIS DEVELOPMENT

3.1 Company Size

There are a large number of empirical studies (e.g. Trotman and Bradley 1981; Chow and Wong-Boren 1987; Cowen et al. 1987; Cooke 1989, 1992; Hossain et al. 1994; Meek et al. 1995; Deegan and Gordon 1996; Hackston and Milne 1996; Stanwick and Stanwick 1998; Carven and Marston 1999; Gray et al.2001;Romlah et al. 2002; Haniffa and Cooke 2005; Zain and Janggu 2006; Ghazali 2007) that have showed that there is a positive relationship between firm size and the level of social disclosures.

A number of arguments have been introduced in the literature in an attempt to explain this relationship. For example, Watts and Zimmerman (1978) argues that larger firms are more visible in the public eyes and more politically sensitive. Firth (1979) suggests that large firms will disclose more information to improve the reputation of the firm, which are more visible in the “public eyes”, are likely to voluntarily. The larger companies are subject to more of stakeholder groups' attention therefore they are more likely to receive greater pressure to report about their social responsibility involvements (Cowen et al. 1987).

Company Size

Industry Type

Profitability

Foreign Ownership

CSR Disclosure

Family group affiliation

ePROCEEDINGS FOR 2011 INTERNATIONAL RESEARCH CONFERENCE AND COLLOQUIUM Contemporary Research Issues and Challenges in Emerging Economies

5

Patten (1991) argues that large companies will disclose more information of corporate social responsibility than small companies, as they are more visible they exposure to harsh public criticism from social groups. Moreover, Brammer and Pavelin (2004) argue that large firms disclose more CSR information as they are more able to manage the cost of disclosure. Based on the results of prior studies, it is expected that social responsibility disclosure is more likely to be positively related to the size of company.

H1: The level of social responsibility disclosure is positively associated with the size of the company 3.2 Industry Type Industry type is often referred as an important factor, when considering the social responsibility of companies. Ingram (1978) considers industry type as an important attribute for consideration because the nature of, and motivation for, disclosure varies according to the production-investment alternatives available to individuals. “These alternatives are likely to be more similar among firms in one industry than, between firms in different industries” (p. 277). Patten (1991) also argued that like company‟s size, the industry‟s nature has a strong influence on companies‟ social responsibility disclosure because the industry is exposed to harsh public criticism from social groups.

Carven and Marston (1999) argue that industry type could influence companies‟ political vulnerability forcing them to have same levels of disclosure. Moreover, they argue that if a company could not maintain industry disclosure level this will be viewed as a bad sign for the market, pointing out that the company is hiding bad news. Consistent with the legitimacy theory, it is believed that high profile manufacturing/ telecommunication companies with its high public profile due to the nature of its product and frequent public-policy controversy over the availability and pricing of its Products (Holder et al., 2009) and the great concern to improve corporate image (Branco and Rodrigues, 2008) will have higher levels of CSR disclosure comparison to their counterparts in other sectors. Several empirical evidences support this argument. Abu-Baker and Naser, (2000) found that manufacturing companies in Jordon disclose a high score of CSR information They explain that companies operating in this industry are large in size and profitable, and they can afford the cost process of collecting and classifying information and disclosure of corporate social responsibility. Brammer and Pavelin (2004) claimed that firms from food drink and tobacco and other manufacturing sectors in UK disclose more voluntary social information than other industries, because companies in those sectors have close relation to social and environmental externalities and their associated threats to corporate reputations. Moreover, Amran and Devi , (2008) pointed out that sector which dominated by big companies and exposed to environmental issues disclose better CSR information . Hackston and Milne (1996) similar to Patten (1991) and Roberts (1992) found that high-profile industry companies disclose significantly more social and environmental information than low-profile industry companies. They linked this result to the high political visibility of these companies; our hypothesis is directional for industry type. H2: The level of social responsibility disclosure positively associated with the high profile industries 3.3 Profitability

Profitability also exerts a significant impact on company social responsibility behaviour disclosure (see Waddock and Graves, 1997, McGuire, et al., 1988, Mangos and Lewis, 1995; Patten, 1991; Roberts, 1992). Haniffa and Cooke (2005) explain that Profitable companies have the freedom and flexibility to implement and disclose social responsibility activities to stakeholders, in order to legitimise their existence.

Moreover, Ulmann (1985) identifies two ways how a company‟s past and current profitability could determine organizational CSR. First, profitability determines the relative weight of a social demand and the attention it receives from top decision-makers. In periods of low profitability and in situations of high

ePROCEEDINGS FOR 2011 INTERNATIONAL RESEARCH CONFERENCE AND COLLOQUIUM Contemporary Research Issues and Challenges in Emerging Economies

6

debt, economic demands will have priority over social demands. Second, profitability influences the financial capability to undertake costly programs related to social demands.

In the literature, studies on relationship between profitability and CSR have produced mixed results. Bowman and Haire (1976) and Abbot and Monsen (1979), by using reputational scales (responses from the public to a social phenomenon), detected a positive correlation. They report significant differences for a five-year average return on equity (ROE) between disclosing and non-disclosing companies. Preston (1978) supported Bowman and Haire's study by reporting a higher ROE for high disclosers. Mills and Gardner (1984) concluded in their analysis of the relationship between social disclosure and financial performance that companies are more likely to disclose social responsibility activities when their financial statements indicate favourable financial performance. On the other hand, Cowen et al. (1987) and Hackston and Milne (1996), using multiple regression analysis, failed to find any positive relationship. Ulmann (1985) argued that the production for these mixed results is due to the weakness in the methodology used in most of the studies. Thus, this study expects that profitability will have an impact on CSR disclosure in Yemen. This expectation is built on the arguments which support that company‟s strong financial performance provides the freedom and resources for the company to involve in CSR activities such as employee concern, community relations or environment issues (Waddock and Graves, 1997).Hence, the next hypothesis is:

H3: The level of social responsibility disclosure is positively associated with the profitability of the company.

3.4 Foreign Share Ownership

Teoh and Thong (1984) argued that companies with large proportion of foreign ownership are more exposed to implement social responsibility programs, and thus companies whose ownership are dominated by foreign shareholders are expected to disclose more CSR information. Andrews et al .(1989) further argued that foreign ownership is expected to have greater effect on corporate social disclosure as foreign companies have greater visibility and are more likely to be subject to control by the host government. Foreign ownership will highlight their corporate social responsibility, through disclosing more CSR information, thereby legitimizing their existence to attract foreign investors as well as to please current investors (Amran and Devi , 2008). Evidences by Zain (1999) and Cormier et al. (2004) are consistent with these arguments, where they find that the country of ownership and foreign ownerships improves corporate social responsibility disclosure in Malaysian and Germany respectively Haniffa and Cooke (2002) also find a significant positive relationship between foreign ownership and the level of disclosure in Malaysia. Moreover, Mangena and Tauringana (2007) also found that foreign ownership is positively and significantly associated with disclosure in Zimbabwe. They argued that foreign ownership leads Zimbabwean companies to implement modern technology which enable them to gather and produce information with less cost than non- foreign ownership companies. Following the above arguments, it can hypothesised that:

H4: The level of social responsibility disclosure is positively associated with the foreign share ownership of the company.

3.5 CSR AWARD It is predictable that awards are devised to highlight companies with the best practice in the overall contents of their annual reports. Examples of such awards are the ACCA Environmental Reporting Awards, which was first introduced in United Kingdom (Hayatudin, 2002). According to the ACCA 2002, the ACCA UK Environmental Reporting Awards is influential in the development of environmental reporting in UK and the scheme has been mirrored by other countries.

Thompson and Zakaria (2004) argued that the most important factor that may encourage Malaysian firms to environmental disclosure is perhaps the Malaysia Environmental Reporting Awards (MERA), which was launched by the ACCA in the middle of 2002. Studies by Haniffa and Cooke (2005) and Hamid and Atan (2011) find that obtaining awards such as the Best Corporate Social Reporting Award and the Environmental Reporting Awards was the reason behind the increased of CSR disclosure in Malaysia.

ePROCEEDINGS FOR 2011 INTERNATIONAL RESEARCH CONFERENCE AND COLLOQUIUM Contemporary Research Issues and Challenges in Emerging Economies

7

The above discussion provides a basic to support the argument that CSR Award encourages disclosures concerning social responsibility positively .Therefore, we test the following:

H5 : The level of social responsibility disclosure is expected to significantly increase from 2007 to 2009 due to CSR Award announcement.

3.6 Moderating Variable 3.6.1 Family group affiliation

Dyer and Whetten (2006) believed that family involvement in a firm makes the responsible actors to be cautious and responsible with their decisions compared to a firm without family involvement. They believe that families see their images and reputations connected to the firms they own, therefore they are unwilling to damage those reputations by making irresponsible decisions. This conclusion and findings are based on their study, comparing the social performance of family and nonfamily firms in the S&P 500 over a 10-year period. They have found out that family firms are more likely to be socially responsible actors than are firms without family involvement.

Firms have incentives to be socially responsible, argues Godfrey (2005), since a positive reputation in the minds of key stakeholders may serve as a form of social insurance, protecting the firm‟s (and family‟s) assets in times of crisis. One way as Skinner points out, firms try to acquire a reputation of giving earnings warning before negative earnings report (Skinner,1994). This way it results in better disclosure-related benefits, such as increased following by analysts and money managers, as well as increased liquidity of the firms‟ stocks. Thus, it was found that reported earnings are of better quality for family f irms as compared to non-family firms (Ali et al., 2007).

Two studies were conducted on small European businesses, one in Dutch companies (Flbren and Wijers, 1996), and the other in Belgian companies (Donckels, 1998), found that the family business tends to have a different, more personal relationship with employees and clients when compared with the non-family business. The supporters of this research finding are Uhlaner et al. (2004) who found that the family character of the business has the most frequently impacts on the relationships between the company and its employees, clients, and suppliers. Based on their findings they believe that the family business owner might consider building good relationships with employees, clients, and suppliers as advantageous for their business.

In Yemen shareholding companies are mainly family group affiliated, thus, family values are easier to be induced to influence the way in which the businesses are run. Therefore, it is expected that the family group affiliation will have moderate impact on the association between company characteristics and corporate social responsibility disclosure. Therefore, based on the above discussion, the hypothesis is to be tested.

H6 : The family group affiliation moderates the relationship between association between company characteristics (size; industry type , profitability and foreign ownership ) and the level of social responsibility disclosure.

RESEARCH METHODOLOGY

4.1. Sample of the Study

The population of the study consists of all shareholding companies registered with the Ministry of Industry and Trade in Yemen. Since there is no stock exchange in Yemen, consequently, there are no listed companies. These companies have been chosen because the Companies Act (No 22) for the year 1997 on Commercial Companies in Article (92) requires shareholding companies to publish their financial annual reports to the public. Also these companies are required to summit copy of their annual reports to the Ministry of Industry and Trade. Therefore, a letter requesting the annual reports was addressed to

ePROCEEDINGS FOR 2011 INTERNATIONAL RESEARCH CONFERENCE AND COLLOQUIUM Contemporary Research Issues and Challenges in Emerging Economies

8

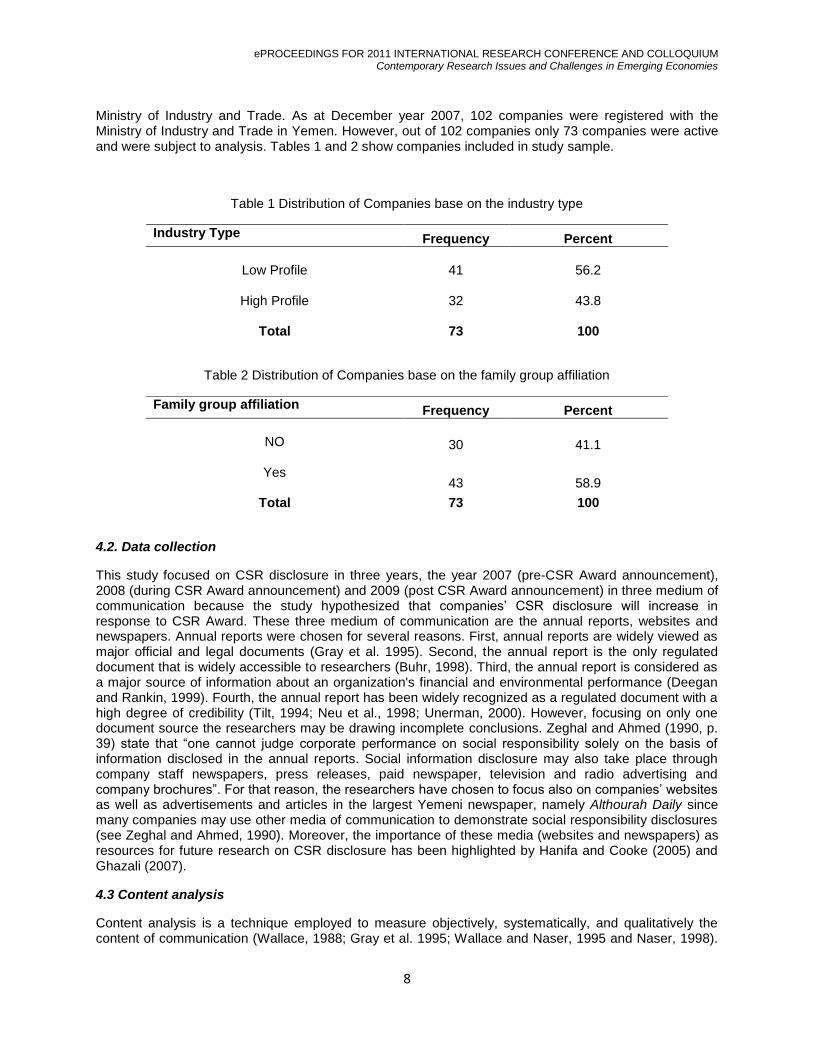

Ministry of Industry and Trade. As at December year 2007, 102 companies were registered with the Ministry of Industry and Trade in Yemen. However, out of 102 companies only 73 companies were active and were subject to analysis. Tables 1 and 2 show companies included in study sample.

Table 1 Distribution of Companies base on the industry type

Table 2 Distribution of Companies base on the family group affiliation

4.2. Data collection

This study focused on CSR disclosure in three years, the year 2007 (pre-CSR Award announcement), 2008 (during CSR Award announcement) and 2009 (post CSR Award announcement) in three medium of communication because the study hypothesized that companies‟ CSR disclosure will increase in response to CSR Award. These three medium of communication are the annual reports, websites and newspapers. Annual reports were chosen for several reasons. First, annual reports are widely viewed as major official and legal documents (Gray et al. 1995). Second, the annual report is the only regulated document that is widely accessible to researchers (Buhr, 1998). Third, the annual report is considered as a major source of information about an organization's financial and environmental performance (Deegan and Rankin, 1999). Fourth, the annual report has been widely recognized as a regulated document with a high degree of credibility (Tilt, 1994; Neu et al., 1998; Unerman, 2000). However, focusing on only one document source the researchers may be drawing incomplete conclusions. Zeghal and Ahmed (1990, p. 39) state that “one cannot judge corporate performance on social responsibility solely on the basis of information disclosed in the annual reports. Social information disclosure may also take place through company staff newspapers, press releases, paid newspaper, television and radio advertising and company brochures”. For that reason, the researchers have chosen to focus also on companies‟ websites as well as advertisements and articles in the largest Yemeni newspaper, namely Althourah Daily since many companies may use other media of communication to demonstrate social responsibility disclosures (see Zeghal and Ahmed, 1990). Moreover, the importance of these media (websites and newspapers) as resources for future research on CSR disclosure has been highlighted by Hanifa and Cooke (2005) and Ghazali (2007).

4.3 Content analysis

Content analysis is a technique employed to measure objectively, systematically, and qualitatively the content of communication (Wallace, 1988; Gray et al. 1995; Wallace and Naser, 1995 and Naser, 1998).

Industry Type Frequency Percent

Low Profile

41

56.2

High Profile

32 43.8

Total 73 100

Family group affiliation Frequency Percent

NO

30 41.1

Yes 43 58.9

Total 73 100

ePROCEEDINGS FOR 2011 INTERNATIONAL RESEARCH CONFERENCE AND COLLOQUIUM Contemporary Research Issues and Challenges in Emerging Economies

9

Another definition is given by Krippendorff who defines content analysis as a research technique for making replicable and valid inferences from data according to their context (Krippendorff,1980).Content analysis of counts of words has been used to determine the level CSR disclosure in Yemen in the four categories (community involvement, human resources, product/service and environment) in the three medium (annul reports , web sites and newspapers) . These categories were chosen as they are able to capture the areas that fall under CSR disclosure.

4.3 .1 Content analysis of annual reports

Each company‟s annual report was analysis and words count of each CSR theme related to any of the CSR categories was added to the scoring sheet. Each scoring sheet was code with the company‟s name and the year of annual report. This procedure replicated for the all annual reports. 4.3 .2 Content analysis of web sites

Each company‟s web site was accessed and examined entirely during 2007, 2008 and 2009 and each CSR theme related to any of the CSR categories disclosed and dated within the period of the study was printed and words count added to scoring sheet. Examined company‟s web site was by using McMurtrie (2001) approaches, were all links were followed, except for the following:

• Web pages that are not rooted in the company‟s name, excluding all external links that took the user outside the sphere of control of the target company.

• Neither on-line copies of the annual report (Patten and Crampton, 2003) nor on-line copies of social and/or environmental reports, were included in the web page analysis;

• Links to external press release disclosures were also excluded (but press releases of the companies will be examined for CSR disclosure) Patten and Crampton, (2003).

• Neither on-line copies of the annual report (Patten and Crampton, 2003) nor on-line copies of social and/or environmental reports will be included in the newspaper analysis.

There are two reasons for the exclusions: first, for segregation, the idea is to collect the data separately on the two media analysed (Frost et al., 2005, p. 91). The second, because this exclusion is an appropriate means of setting the boundaries (Douglas et al., 2004, p.392)

4.3 .2 Content analysis of newspaper

Due to difficulties to obtain full soft copy issues, multiple visits to Althourah Corporation for Press, Printing and Publishing library in Yemen and all issues for the years 2007, 2008 and 2009 were entirely analysed. Wards of CSR theme related to any of the CSR categories disclosed by companies of the study‟s sample was counted and added to the company‟s scoring sheet.

4.4. Measurement

Both dependent variable and independent variables were measured as follows:

4.4.1 CSR Disclosure

The CSR disclosure level was measured by accumulating the content analysis results in the three medium of communication. 4.4.2 Independent variables

Size: There is no theoretical reason for a particular measure of size in disclosure studies (Choi, 1999). In the present study, total assets figures were used as a measurement of company size.

ePROCEEDINGS FOR 2011 INTERNATIONAL RESEARCH CONFERENCE AND COLLOQUIUM Contemporary Research Issues and Challenges in Emerging Economies

10

Industry type: was measured using dummy variable which took a value of one, if the company affiliated to high profile sectors (manufacturing/ telecommunication), and zero otherwise. The companies were reclassified into high profile sectors and low profile sectors, due to the small distribution of companies in different sectors, which could prevent performing a basis for statistical analysis and also to avoid the trap of dummy variable. Manufacture classification was chosen because high profile sector (manufacturing /telecommunication) sector was found previously be related with the high level of CSR disclosure (Patten 1991; Roberts , 1992; Hackston and Milne ,1996 ;Naser, 2000; Ratanajongkol,et.al 2006 ) and also because manufacturing sector contained companies dominated by Yemeni society as high profile companies .

Profitability: Similar to previous studies by Hakston and Milne (1996) and Haniffa and Cooke (2005), the measure of company profitability used in this study is return on equity (ROE).

Foreign Share Ownership: The measure of foreign share ownership is the percentage of shares held by foreign shareholders, similar to the measure used by many previous studies. For example Haniffa and Cooke (2005) and Amran and Devi, (2008).

4.4.3 Moderating variable: Family group affiliation

Consistent with previous studies, the family group affiliation measured using dummy variable which took a value of one, if the company affiliated to family group, and zero otherwise (Khanna and Rivkin, 2001; Singh and Gaur, 2009) 4.5 Data Analysis All data were analysed using the Statistical Package for Social Studies (SPSS) version 17.0 in order to answer the study‟s questions .Data analysis was as follows:

a) Paired T-Tests Paired t-tests were performed to examine whether corporate social responsibility disclosure increased from 2007 to 2009 in response to CSR Award announcement.

b) Ordinary Least Squares Regression Ordinary least squares regression was performed to investigate whether there is enough evidence to support the existence of a relationship between firms‟ characteristics (such as size, industry type, profitability and foreign share ownership) and the level of corporate social responsibility disclosure. The complete specification of the regression is: Model 1 CSRDL = ο+1SZE+2IND+3PRO+4FRGOWN +ε

c) Moderated Multiple Regression To examine the moderating impact of family group affiliation on the relationship company‟s characteristics and corporate social responsibility disclosure, moderated multiple regression analysis was conducted using two stage regressions (Li and Atuahene-Gima, 2001). In the first stage, the dependent variable is regressed with the independent variables and moderator variable to represent the variables in the ordinary least-squares (OLS) model: Model 2 (OLS model): Model 2 CSRDL = ß0 + ß1SZE + ß2IND + ß3PRO + ß4FOROW + ß5FAMGP + ε

In the second stage, to determine the presence of moderating effect an interaction term (independent × moderator variable) is added which was represented by Equation 2 below:

Model 3 (MMR model): Model 3 CSRDL = ß0 + ß1SZE + ß2IND + ß3PRO + ß4FOROW +

ß5 (SZE*FAMGP) + ß6 (IND*FAMGP) + ß7 (PRO*FAMGP) + ß8 (FOROW*FAMGP) + ε

ePROCEEDINGS FOR 2011 INTERNATIONAL RESEARCH CONFERENCE AND COLLOQUIUM Contemporary Research Issues and Challenges in Emerging Economies

11

Where,

CSRDL = corporate social responsibility disclosure level

= constant SZE = the natural log of total assets IND = 1 indicates industry type is high profile (Manufacturing / telecommunication)

, and 0 otherwise PRO = Return on Equity FRGOWN = percentage of shares held by foreign shareholders

FAMGP = 1 indicates company affiliated to family group , and 0 otherwise

DISCUSSION OF RESULTS 5.1 Descriptive Statistics of Social Responsibility Disclosure Level

Table3 shows that the mean of corporate social responsibility disclosure word count (CSRD) in annual reports, website and newspapers over the three years is about 1092 words. This score suggests a very low level of social responsibility disclosure.

The Table 3 also shows that the level of social responsibility disclosure in the three media over the three years varies widely. The minimum disclosure level obtained is 36 words for the year 2007, and the maximum is 6670 words for the year 2009. Also in each year of investigation a wide range of social responsibility disclosure level can be noticed. The minimum words of social responsibility disclosure increased slightly from 36 words in 2007 to 37 words for the following years. On the other hand, the maximum total social responsibility disclosure in words has increased dramatically from 2479 words to 3705 words and to 6670 in 2007, 2008 and 2009 respectively. Figure.2 presents the level of total social responsibility disclosure in the three years.

Table 3 Descriptive Statistics of Social Responsibility disclosure Level

Year N

Mean of word count

Median Std. D Skewness Kurtosis Min Max

2007 73 629 373 633.00 1.14 0.58 36 2479

2008 73 977 610 981.29 1.03 0.16 37 3705

2009 73 1670 869 1695.24 1.05 0.24 37 6670

Pooled 219 1092 654 1260.06 1.73 3.15 36 6670

ePROCEEDINGS FOR 2011 INTERNATIONAL RESEARCH CONFERENCE AND COLLOQUIUM Contemporary Research Issues and Challenges in Emerging Economies

12

Figure 2 Level of CSR disclosure

Table 4 presents the variation in the level of social responsibility disclosure categories over the period of study. It may be worth analyzing the level and trend of each category. To do this, the study starts by determining the difference in CSR disclosure across categories. Such analysis provides a clear understanding of the CSR disclosure policy that active companies prefer to apply during the period of study. In addition, it helps in understanding the effect of Yemeni culture on the CSR disclosure decision. It can be seen from table 2 that there is a gradual increase in the mean of words count of each of the three groups. However, the increasing score differs across the categories. For example, while the increasing score in the human resources information was 179 words, 345 words, and 615 words for the years 2007, 2008 and 2009 respectively, the increasing score of words count in community involvement information was 365 words, 490 words and 798 words for the same years.

However, the structure of total social responsibility disclosure is similar in each of the three years. For the year 2007, the community involvement category has the highest score, about 365 words, followed by human resources 179 words, product and service 68 words, and environmental information 16 words. The same structure was found in the year 2008 but only a little change in the year 2009.

In general, across the three years, community involvement has the highest mean, ranging from 365 words in 2007 to 798 words in 2009.On the other hand, environmental information has the lowest mean in all years starting from 16 words in 2007 to 49 words in 2009.

Table 4 Level of Social Responsibility disclosure and its categories

Year Categories Mean of Word count Min Max

Std. Deviation

Human Resources 179 3 1007 227.42

2007 Community Involvement 365 0 1370 410.28

Product and Service 68 0 250 66.514

Environmental 16 0 530 73.84

ePROCEEDINGS FOR 2011 INTERNATIONAL RESEARCH CONFERENCE AND COLLOQUIUM Contemporary Research Issues and Challenges in Emerging Economies

13

Total 629 36 2479 633.00

Human Resources 345 3 2534 472.59

2008 Community Involvement 490 0 1600 517.418

Product and Service 119 0 607 119.96

Environmental 22 0 510 80.27

Total 977 37 3705 981.29

Human Resources 615 3 3230 720.56

2009 Community Involvement 798 0 2897 841.78

Product and Service 206 0 995 230.03

Environmental 49 0 700 145.61

Total 1670 37 6670 1695.24

Human Resources 379 3 3230 542.93

Total Community Involvement 551 0 2897 641.36

Product and Service 131 0 995 164.23

Environmental 29 0 700 105.56

Total 1092 36 6670 1260.06

Figure 3 social responsibility disclosures categories

ePROCEEDINGS FOR 2011 INTERNATIONAL RESEARCH CONFERENCE AND COLLOQUIUM Contemporary Research Issues and Challenges in Emerging Economies

14

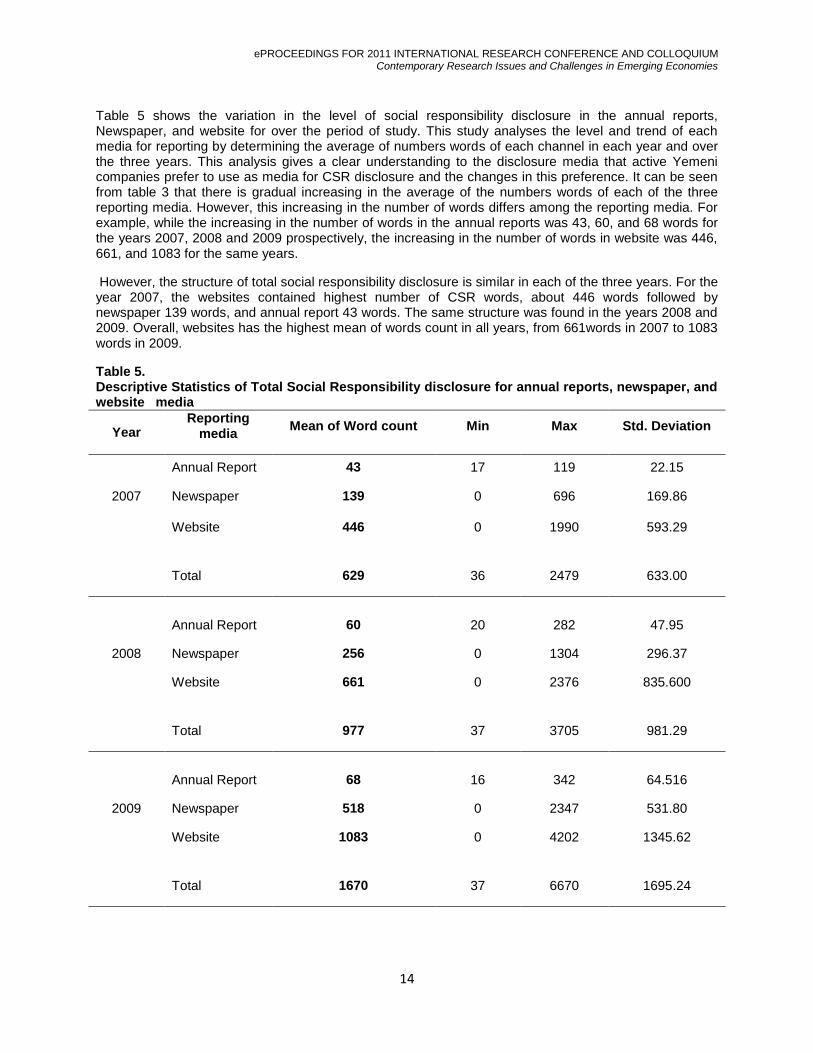

Table 5 shows the variation in the level of social responsibility disclosure in the annual reports, Newspaper, and website for over the period of study. This study analyses the level and trend of each media for reporting by determining the average of numbers words of each channel in each year and over the three years. This analysis gives a clear understanding to the disclosure media that active Yemeni companies prefer to use as media for CSR disclosure and the changes in this preference. It can be seen from table 3 that there is gradual increasing in the average of the numbers words of each of the three reporting media. However, this increasing in the number of words differs among the reporting media. For example, while the increasing in the number of words in the annual reports was 43, 60, and 68 words for the years 2007, 2008 and 2009 prospectively, the increasing in the number of words in website was 446, 661, and 1083 for the same years.

However, the structure of total social responsibility disclosure is similar in each of the three years. For the year 2007, the websites contained highest number of CSR words, about 446 words followed by newspaper 139 words, and annual report 43 words. The same structure was found in the years 2008 and 2009. Overall, websites has the highest mean of words count in all years, from 661words in 2007 to 1083 words in 2009.

Table 5. Descriptive Statistics of Total Social Responsibility disclosure for annual reports, newspaper, and website media

Year Reporting

media Mean of Word count Min Max Std. Deviation

Annual Report 43 17 119 22.15

2007 Newspaper 139 0 696 169.86

Website 446 0 1990 593.29

Total 629 36 2479 633.00

Annual Report 60 20 282 47.95

2008 Newspaper 256 0 1304 296.37

Website 661 0 2376 835.600

Total 977 37 3705 981.29

Annual Report 68 16 342 64.516

2009 Newspaper 518 0 2347 531.80

Website 1083 0 4202 1345.62

Total 1670 37 6670 1695.24

ePROCEEDINGS FOR 2011 INTERNATIONAL RESEARCH CONFERENCE AND COLLOQUIUM Contemporary Research Issues and Challenges in Emerging Economies

15

Annual Report 57 16 342 49.04

TOTAL Newspaper 304 0 2347 396.38

Website 730 0 4202 1007.61

Total 1092 36 6670 1260.06

5.2 Paired T-Tests To examine the response to CSR Award, the study used paired t- test to see the changes in corporate social responsibility disclosure levels from 2007 to 2009. The results of paired t- tests in Table 6 show that the mean word count of corporate social responsibility disclosure level from 2007 to 2009 ranged from 644 words to 1670 words with mean differences ranged from -333 to -692 , presenting significant increases in words count of corporate social responsibility disclosure level each year . From 2007 to 2008 and from 2008 to 2009 corporate social responsibility disclosure level in three medium raised significantly at the 1 % level.

Table 6

Result of Paired T- Test

N=73 Mean Mean Difference t Sig. (2-tailed)

Pair 1 CSRDL2007 644

CSRDL2008 977 -333 -6.220 .000

Pair 2 CSRDL2008 977

CSRDL2009 1670 -692 -7.798 .000

5.3 Multivariate Regression Analysis 5.3.1 Ordinary least-squares regression

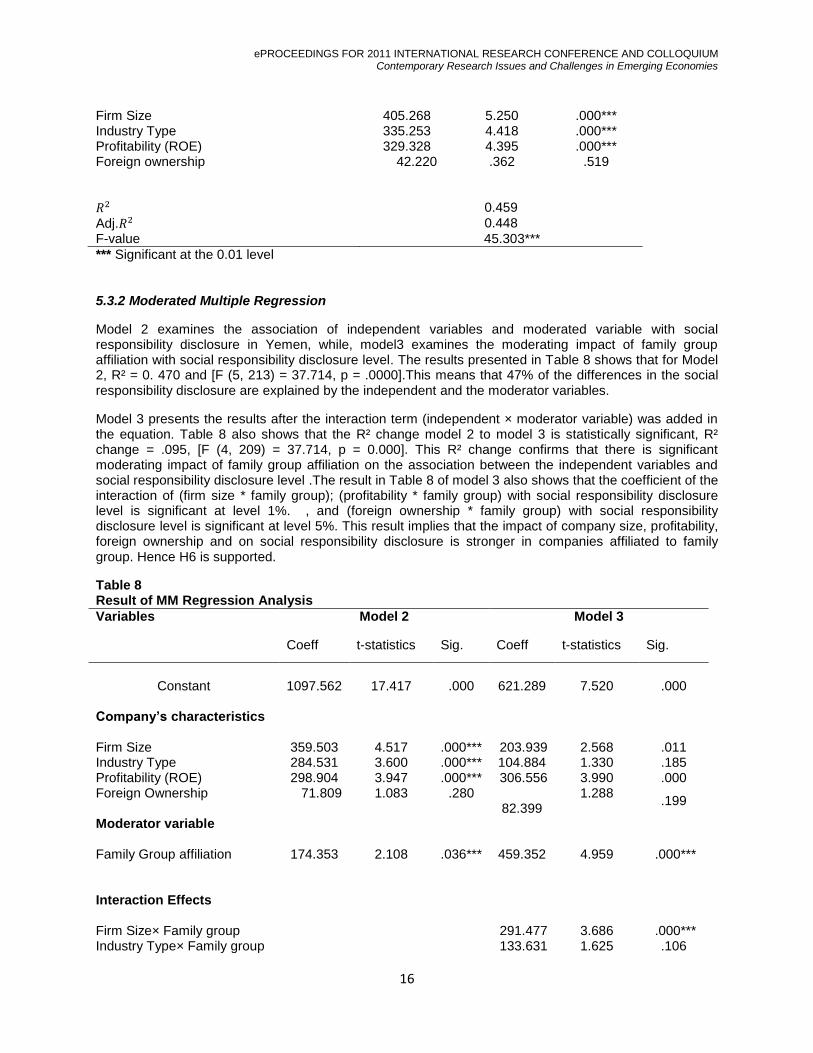

Table 7 below shows that for OLS Regression Analysis (Model 1), adjusted

was 0.459, which means that 45.9% CSR disclosure variance is explained by firms‟ characteristics (size, industry type, profitability and foreign share ownership).This value is in line with results found in previous studies (Hackston and Milne ,1996;Haniffa and Cooke ,2005; Branco and Rodrigues,2008 ).In addition the result in Table 6 shows that there is a highly positive significant (1% level) relationship between company size and corporate social responsibility disclosure level. The result also shows a significant relationship between industry type and corporate social responsibility disclosure level at 1% in the positive direction. Profitability was also found to be significantly related to corporate social responsibility disclosure level at 1% level in Yemen. However, foreign ownership did not show any significant relationship with corporate social responsibility disclosure level. Table 7 Result of OLS Regression Analysis

Variables

Model 1

Coeff t-statistics Sig.

Constant 1097.562

17.258 .000***

Company’s characteristics

ePROCEEDINGS FOR 2011 INTERNATIONAL RESEARCH CONFERENCE AND COLLOQUIUM Contemporary Research Issues and Challenges in Emerging Economies

16

Firm Size 405.268 5.250 .000*** Industry Type 335.253 4.418 .000*** Profitability (ROE) 329.328 4.395 .000*** Foreign ownership

42.220 .362 .519

0.459

Adj. 0.448

F-value 45.303***

*** Significant at the 0.01 level 5.3.2 Moderated Multiple Regression

Model 2 examines the association of independent variables and moderated variable with social responsibility disclosure in Yemen, while, model3 examines the moderating impact of family group affiliation with social responsibility disclosure level. The results presented in Table 8 shows that for Model 2, R² = 0. 470 and [F (5, 213) = 37.714, p = .0000].This means that 47% of the differences in the social responsibility disclosure are explained by the independent and the moderator variables.

Model 3 presents the results after the interaction term (independent × moderator variable) was added in the equation. Table 8 also shows that the R² change model 2 to model 3 is statistically significant, R² change = .095, [F (4, 209) = 37.714, p = 0.000]. This R² change confirms that there is significant moderating impact of family group affiliation on the association between the independent variables and social responsibility disclosure level .The result in Table 8 of model 3 also shows that the coefficient of the interaction of (firm size * family group); (profitability * family group) with social responsibility disclosure level is significant at level 1%. , and (foreign ownership * family group) with social responsibility disclosure level is significant at level 5%. This result implies that the impact of company size, profitability, foreign ownership and on social responsibility disclosure is stronger in companies affiliated to family group. Hence H6 is supported.

Table 8 Result of MM Regression Analysis

Variables

Model 2 Model 3

Coeff t-statistics Sig. Coeff t-statistics Sig.

Constant

1097.562 17.417 .000

621.289 7.520 .000

Company’s characteristics

Firm Size 359.503 4.517 .000*** 203.939 2.568 .011 Industry Type 284.531 3.600 .000*** 104.884 1.330 .185 Profitability (ROE) 298.904 3.947 .000*** 306.556 3.990 .000 Foreign Ownership

71.809 1.083 .280

82.399 1.288

.199

Moderator variable

Family Group affiliation

174.353 2.108 .036*** 459.352 4.959 .000***

Interaction Effects

Firm Size× Family group 291.477 3.686 .000*** Industry Type× Family group 133.631 1.625 .106

ePROCEEDINGS FOR 2011 INTERNATIONAL RESEARCH CONFERENCE AND COLLOQUIUM Contemporary Research Issues and Challenges in Emerging Economies

17

Profitability × Family group 291.945 4.033 .000*** Foreign Ownership × Family group

173.734 2.855 .005**

.470 .564

Adj. .457 .546

F-value 37.714*** 11.364***

*** Significant at the 0.01 level ** Significant at the 0.05 level

CONCLUSION This study focuses on the level of corporate social responsibility information disclosed in the three medium of communications (annual reports, websites, and newspapers) in Yemen. Overall, the descriptive results of this study show that the level of CSR disclosure in Yemen is very low with a total of 6670 words disclosed in the three medium of disclosure compared with the level of CSR disclosure in other countries in terms of CSR word counts .For example, Zeghal and Ahmed (1983) found that Canadian companies disclosed 14826 words of CSR activities in three medium of disclosure (annual reports, advertisements, and brochures). This result was expected in Yemen as it is a low developed county with secretive culture, weak accounting systems and no stock market in addition to the lack of powerful NGOs groups in contrast to those in the industrialized countries (Abu-Baker and Naser, 2000). This result is consistent with Choi et al. (2002) argument that the level of economic developments influences the development of the accounting system which in turn affects disclosure system. The result of this study also shows that the community involvements category followed by human resources category were the most commonly disclosed categories with a mean of 551 and 379 words respectively. This result is consistent with the study conducted by Hinson et al (2010) where they have found that the community involvement information is most frequently disclosed theme in Ghana. They have argued that in a poor country like Ghana that depends on donation for its development by focusing on community involvement will have an immediate gain to legitimatize their activities. Regarding the medium of disclosure, Yemeni companies provided more of CSR disclosures on web sites than the annual reports and newspapers. This result also coincides with previous studies (Williams and Ho Wen Pei,1999; Douglas et al 2004). Paired t-tests results show that Yemeni shareholding companies increased their social responsibility disclosure in response to CSR Award announcement, based on the mean number of words. Therefore the increase in CSR disclosure in Yemen between 2007 and 2009 could be linked to CSR Award announcement .This result is in line with Haniffa and Cooke (2005) finding that obtaining awards such as the Best Corporate Social Reporting Award and the Environmental Reporting Awards was the reason behind the increased of CSR disclosure in Malaysia. Hamid and Atan (2011) also noted that in Malaysia the introduction of these awards in 2002 was the reason behind the increased level of CSR disclosure. The adoption of CSR Award by Yemeni government was an attempt to attract Yemeni companies to engage in more CSR activities, by increasing their social responsibility disclosure in response to the CSR Award announcement, it shows that legitimacy theory can be used as the provenance to explain Yemeni companies are trying to prove that they are doing good and are responding to government‟s calls in order to gain favourable public expectations. However, the current social responsibility disclosure level suggests that companies in Yemen still have a long way to go before their CSR disclosure could be comparable with other countries. Ordinary least squares (OLS) analysis was preformed to examine the relationship between explanatory variables (company‟s size, industry type, and profitability) and level of CSR disclosure in Yemen. This study found a strong relationship between size and the CSR disclosure level in Yemen and there are strong supports for this finding from many previous studies. For example Authors such as Cowen et al. (1987), Patten (1991), Hackston and Milne (1996), Adams et al. (1998), Zain (1999) and Haniffa and Cooke (2005) ; Zain and Janggu (2006) and Branco and Rodrigues (2008 ) suggested that large companies are highly visible and they have to take consideration towards social responsibility activities

ePROCEEDINGS FOR 2011 INTERNATIONAL RESEARCH CONFERENCE AND COLLOQUIUM Contemporary Research Issues and Challenges in Emerging Economies

18

and disclosure in order to enhance their reputation. As for the company‟s size , the manufacturing industry type also found that it has significant relationship with CSR disclosure, and this result is consistent with prior studies‟ findings such as ; Abu-Baker and Naser, (2000); Ratanajongkol,et al. (2006) who found that manufacturing companies were related to the high level of CSR disclosure and Patten (1991); Roberts , (1992); Hackston and Milne (1996) ;Newson and Deegan (2002) and Amran and Devi (2008), who had found a positive relationship between high profile industry type and CSR disclosure. This finding on the impact of industry type provides support for the legitimacy theory argument, which proposed that high profile industry discloses high amount of CSR information due to their visibility. There is also significant relationship between the profitability and CSR disclosure level in Yemen which in

line with arguments of Haniffa and Cooke (2005) and Zain and Janggu (2006) that profitable companies

in Malaysia disclose high CSR information in their annual reports to publicise their image and legitimise

their activities. However, foreign ownership does not have a significant relationship with CSR disclosure

level in Yemen. This finding is in contrast with several studies that show strong support for a positive

relationship between the foreign ownership and CSR disclosure (Haniffa and Cooke, 2005). In the case of

Yemen the probable explanation for this result is that due to the weak investment and economical

environment in Yemen, there is an absence of real investments by multinational companies from

developed countries which have long history of sustainable developments meanwhile the top investors in

Yemen come from neighbouring countries such as Saudi, Kuwait and Libya which do not have a

remarkable sustainable developments. .

Concerning the impact of moderating effects of family group affiliation, on the relationships between firms‟

characteristics and the level of CSR disclosure in Yemen, interestingly, the results of moderated multiple

regression (MMR) analysis indicated that the family group affiliation has significant moderating effect on

the relationships between firm size, profitability foreign ownership and CSR disclosure. This result is

consistent with previous studies which provide strong support for the significant role of family businesses

towards CSR (Huang et a.l 2009; Dyer and Whetten, 2006; Uhlaner et.al, 2004).For instance, Huang et

a.l (2009) found that family business positively and significantly moderates the relationship between the

pressure of internal stakeholder and the adoption of green innovations in Taiwan. They have attributed

this moderating impact to the organizational culture and core values of family firms.

In similar view, Dyer and Whetten, (2006) found that family firms exhibit greater social responsibility

concern than non family firms. Uhlaner et.al (2004) studied the impact of family surname in firm name on

corporate social responsibility in family firms in Netherlands. They concluded that the existence of family

surname in firm name has increased the company‟s social responsibility. Gallo (2004) reported that family

firms are more socially responsible than non-family firms. He further argued that family firms have a more

long term orientation, which could lead to more sustainability management activities and ultimately higher

sustainability performance (Anderson & Reeb, 2003). It also has been found, that family ownership is

associated with the extent of voluntary. A possible explanation of the significant moderating impact of

family group affiliation is that, since Yemen is a poor country, the rich families have a strong commitment

to philanthropic activities. Thus the culture of giving is core value of these families and this supports the

contention that the core values of family business such as quality, hard work, ethical business practices

and corporate reputation are the expression of the family‟s values (Aronoff , 2004).

There are important potential implications from the results of this study. First, this study shows that rules of CSR disclosure developments in developed and developing countries are also applicable in one of least developed country in particular Yemen. Some results, such as the response to CSR Award, company‟s characteristics variables impact and CSR disclosure categories preference are similar to international results. This implies that CSR disclosure in least developed countries is following the international CSR disclosure. Hence comparison is possible. Second, the result on CSR Award provides

ePROCEEDINGS FOR 2011 INTERNATIONAL RESEARCH CONFERENCE AND COLLOQUIUM Contemporary Research Issues and Challenges in Emerging Economies

19

data for Yemeni government to evaluate CSR Award on whether more action might be needed to encourage Yemeni companies to adopt more CSR disclosure in Yemen. Finally, this study provides evidences on the moderating role of family group affiliation on the relationship between company‟s characteristics and CSR disclosure and this result could be applicable to other Arabic countries where culture, family values and family ownership structure are similar. However, the study has two important limitations: First is the sample of the study, which consists of 73 active registered shareholding companies in Yemen. Hence, extending the sample by including other types of companies would provide extra evidences of CSR disclosure level. Additionally, larger sample size will help to provide more accurate information on the response to CSR Award. The second limitation is that the study examined only four characteristics of the firm (size, industry type, profitability and foreign ownership) that affect the level of CSR disclosure, where as there are several other firm‟s characteristics and managers‟ characteristics that may affect the level of CSR disclosure. Because of the absence of previous studies regarding CSR in Yemen, future studies can investigate the CSR disclosure relationship with other companies‟ characteristics (e.g., government ownership and location) or mangers‟ characteristics (e.g., age and education). Future studies could explore CSR perceptions in Yemen which would provide a better look on CSR in Yemen and in least developed countries in general.

REFERENCES

Abbott, W. F., & Monsen, R. J. (1979). On the measurement of corporate social responsibility: Self-reported disclosures as a method of measuring corporate social involvement. Academy of Management Journal, 501-515.

Abu-Baker, N., & Naser, K. (2000). Empirical evidence on corporate social disclosure (CSD) practices in

Jordan. International Journal of Commerce and Management, 10(3/4), 18-34. Adams, C. A. (2002). Internal organisational factors influencing corporate social and ethical reporting:

beyond current theorising. Accounting, Auditing & Accountability Journal, 15(2), 223-250. Adams, C. A., Hill, W. Y., & Roberts, C. B. (1998). CORPORATE SOCIAL REPORTING PRACTICES IN

WESTERN EUROPE: LEGITIMATING CORPORATE BEHAVIOUR?* 1,* 2. The British Accounting Review, 30(1), 1-21.

Ali, A., Chen, T. Y., & Radhakrishnan, S. (2007). Corporate disclosures by family firms. Journal of

Accounting and Economics, 44(1-2), 238-286. Amran, A., & Devi, S. S. (2008). The impact of government and foreign affiliate influence on corporate

social reporting: The case of Malaysia. Managerial Auditing Journal, 23(4), 386-404. Anderson, R. C., & Reeb, D. M. (2003). Founding-family ownership and firm performance: Evidence from

the S&P 500. Journal of finance, 1301-1328. Andrew, B., Gul, F., Guthrie, J., & Teoh, H. (1989). A note on corporate social disclosure practices in

developing countries: the case of Malaysia and Singapore. The British Accounting Review, 21(4), 371-376.

Aronoff, C. (2004). Self Perpetuation Family Organization Built on Values: Necessary Condition for Long

Term Family Business Survival. Family Business Review, 17(1), 55-59. Althawra Daily, Thursday. October 2008 NO(16059). Belal, A. R., & Owen, D. L. (2007). The views of corporate managers on the current state of, and future

prospects for, social reporting in Bangladesh: An engagement-based study. Accounting, Auditing

ePROCEEDINGS FOR 2011 INTERNATIONAL RESEARCH CONFERENCE AND COLLOQUIUM Contemporary Research Issues and Challenges in Emerging Economies

20

& Accountability Journal, 20(3), 472-494. Bowman, E. H., & Haire, M. (1976). Social impact disclosure and corporate annual reports. Accounting,

Organizations and Society, 1(1), 11-21. Brammer, S., & Pavelin, S. (2004). Voluntary social disclosures by large UK companies. Business Ethics:

A European Review, 13(2 3), 86-99. Branco, M. C., & Rodrigues, L. L. (2008). Factors influencing social responsibility disclosure by

Portuguese companies. Journal of Business Ethics, 83(4), 685-701. Buhr, N. (1998). Environmental performance, legislation and annual report disclosure: the case of acid

rain and Falconbridge. Accounting, Auditing & Accountability Journal, 11(2), 163-190. Choi, F. D. S. F., C. A.; Meek, G. K. (2002). International Accounting: Englewood Cliffs, NJ: Prentice Hall. Choi, J. S. (1999). An investigation of the initial voluntary environmental disclosures made in Korean

semi-annual financial reports. Pacific Accounting Review, 11(1), 73-102. Chow, C. W., & Wong-Boren, A. (1987). Voluntary financial disclosure by Mexican corporations.

Accounting Review, 533-541. Cooke, T. E. (1989). Disclosure in the corporate annual reports of Swedish companies. Accounting and

Business Research, 19(74), 113-124. Cooke, T. (1990). The impact of size, stock market listing and industry type on disclosure in the annual

reports of Japanese listed corporations. Cormier, D., Gordon, I. M., & Magnan, M. (2004). Corporate environmental disclosure: contrasting

management's perceptions with reality. Journal of Business Ethics, 49(2), 143-165. Cowen, S. S., Ferreri, L. B., & Parker, L. D. (1987). The impact of corporate characteristics on social

responsibility disclosure: a typology and frequency-based analysis. Accounting, Organizations and Society, 12(2), 111-122.

Craven, B., & Marston, C. (1999). Financial reporting on the Internet by leading UK companies. European

Accounting Review, 8(2), 321-333. Deegan, C., & Gordon, B. (1996). A study of the environmental disclosure practices of Australian

corporations. Accounting and Business Research, 26, 187-199. Deegan, C., & Rankin, M. (1999). The environmental reporting expectations gap: Australian evidence.

The British Accounting Review, 31(3), 313-346. Donckels, R. (1998), „Ondernemen in het familiebedrijf‟, in D.P. Scherjon and A.R.Thurik (eds),

Handboek Ondernemers en Adviseurs in het MKB, Deventer Kluwer Bedrijfsinformatie, pp. 86–9. Kluwer Bedrijfsinformatie, pp. 86–9. Douglas, A., Doris, J., & Johnson, B. (2004). Corporate social reporting in Irish financial institutions. The

TQM Magazine, 16(6), 387-395. Dowling, J., & Pfeffer, J. (1975). Organizational legitimacy: Social values and organizational behavior.

Pacific Sociological Review, 122-136. Dyer Jr, W. G., & Whetten, D. A. (2006). Family firms and social responsibility: Preliminary evidence from

the S&P 500. Entrepreneurship Theory and Practice, 30(6), 785-802.

ePROCEEDINGS FOR 2011 INTERNATIONAL RESEARCH CONFERENCE AND COLLOQUIUM Contemporary Research Issues and Challenges in Emerging Economies

21

Firth, M. (1979). The impact of size, stock market listing, and auditors on voluntary disclosure in corporate

annual reports. Accounting and Business Research, 9(36), 273-280. Flbren, R. H. a. W. R., W.J. . (1996). Handboek van het Familiebedrijf: Walgemoed Accountants and

Adviseurs. Frost, G., Jones, S., Loftus, J., & Laan, S. (2005). A survey of sustainability reporting practices of

Australian reporting entities. Australian Accounting Review, 15(35), 89-96. Gallo, M. (2004). The family business and its social responsibilities. Family Business Review, 17(2), 135-

149. Gamble, G. O., Hsu, K., Kite, D., & Radtke, R. R. (1995). Environmental disclosures in annual reports and

10Ks: An examination. Accounting Horizons, 9, 34-34. Ghazali, N. A. M. (2007). Ownership structure and corporate social responsibility disclosure: some

Malaysian evidence. Corporate Governance, 7(3), 251-266. Godfrey, P. C. (2005). The relationship between corporate philanthropy and shareholder wealth: A risk

management perspective. The Academy of Management Review, 777-798. Gray, R., Javad, M., Power, D. M., & Sinclair, C. D. (2001). Social and environmental disclosure and

corporate characteristics: a research note and extension. Journal of Business Finance & Accounting, 28(3 4), 327-356.

Gray, R., Kouhy, R., & Lavers, S. (1995). Constructing a research database of social and environmental

reporting by UK companies. Accounting, Auditing & Accountability Journal, 8(2), 78-101. Hackston, D., & Milne, M. J. (1996). Some determinants of social and environmental disclosures in New

Zealand companies. Accounting, Auditing & Accountability Journal, 9(1), 77-108. Hamid, F. Z. A., & Atan, R. (2011).Corporate Social Responsibility by the Malaysian Telecommunication

Firms. International Journal of Business and Social Science 2(5). Haniffa, R., & Cooke, T. (2005). The impact of culture and governance on corporate social reporting.

Journal of Accounting and Public Policy, 24(5), 391-430. Hayatudin, Hayati (2002) .Environmental Reporting could be made Compulsory, Nation, New Strait

Times, July 17. Hayel , S. A. (2008). Social responsibility in the thought of Hayel Saeed Anam Group: Motives – policies-

a vision for the future. Paper presented at the the first corporate social responsibility conference in Yemen.

Hinson, R., Boateng, R., & Madichie, N. (2010). Corporate social responsibility activity reportage on bank

websites in Ghana. International Journal of Bank Marketing, 28(7), 498-518. Holder-Webb, L., Cohen, J. R., Nath, L., & Wood, D. (2009). The supply of corporate social responsibility

disclosures among US firms. Journal of Business Ethics, 84(4), 497-527. Hossain, M., Tan, L. M., & Adams, M. (1994). Voluntary disclosure in an emerging capital market: some

empirical evidence from companies listed on the Kuala Lumpur stock exchange. International Journal of Accounting, 29(4), 334-351.

ePROCEEDINGS FOR 2011 INTERNATIONAL RESEARCH CONFERENCE AND COLLOQUIUM Contemporary Research Issues and Challenges in Emerging Economies

22

Huang, Y. C., Ding, H. B., & Kao, M. R. (2009). Salient stakeholder voices: Family business and green innovation adoption. Journal of Management and Organization, 15(3), 309-326.

Imam, S. (2000). Corporate social performance reporting in Bangladesh. Managerial Auditing Journal,

15(3), 133-142 Ingram, R. W. (1978). An investigation of the information content of (certain) social responsibility

disclosures. Journal of Accounting Research, 16(2), 270-285. Jamali, D., & Mirshak, R. (2007). Corporate social responsibility (CSR): theory and practice in a

developing country context. Journal of Business Ethics, 72(3), 243-262. Khanna, T., & Rivkin, J. W. (2001). Estimating the performance effects of business groups in emerging

markets. Strategic management journal, 22(1), 45-74. Krippedorff K. (1980). Content Analysis: An introduction to its Methodology, Sage, London, Li, H., & Atuahene-Gima, K. (2001). Product innovation strategy and the performance of new technology

ventures in China. Academy of Management Journal, 1123-1134. Lindblom, C. (1994). The implications of organizational legitimacy for corporate social performance and

disclosure. Paper presented at the the Critical Perspectives on Accounting Conference. Mangena, M., & Tauringana, V. (2007). Disclosure, corporate governance and foreign share ownership

on the Zimbabwe stock exchange. Journal of International Financial Management & Accounting, 18(2), 53-85.

Mangos, N. C., & Lewis, N. R. (1995). A socio-economic paradigm for analysing managers' accounting

choice behaviour. Accounting, Auditing & Accountability Journal, 8(1), 38-62. McGuire, J. B., Sundgren, A., & Schneeweis, T. (1988). Corporate social responsibility and firm financial

performance. Academy of Management Journal, 854-872. McMurtrie, T. (2001). Disclosure through the looking glass. Paper presented at the at the 3rd APIRA

Conference, Adelaide University. Meek, G. K., Roberts, C. B., & Gray, S. J. (1995). Factors influencing voluntary annual report disclosures

by US, UK and continental European multinational corporations. Journal of International Business Studies, 555-572.

Mills, D. L., & Gardner, M. J. (1984). Financial profiles and the disclosure of expenditures for socially

responsible purposes. Journal of Business Research, 12(4), 407-424. Naser, K. (1998). Comprehensiveness of disclosure of non-financial companies: Listed on the Amman

financial market. International Journal of Commerce and Management, 8(1), 88-119. Neu, D., Warsame, H., & Pedwell, K. (1998). Managing public impressions: environmental disclosures in

annual reports. Accounting, Organizations and Society, 23(3), 265-282. Newson, M., & Deegan, C. (2002). Global expectations and their association with corporate social

disclosure practices in Australia, Singapore, and South Korea. The International Journal of Accounting, 37(2), 183-213.

Patten, D. M. (1991). Exposure, legitimacy, and social disclosure. Journal of Accounting and Public

Policy, 10(4), 297-308.

ePROCEEDINGS FOR 2011 INTERNATIONAL RESEARCH CONFERENCE AND COLLOQUIUM Contemporary Research Issues and Challenges in Emerging Economies

23

Patten, D. M., & Crampton, W. (2003). Legitimacy and the Internet: An examination of corporate web

page environmental disclosures. Advances in Environmental Accounting and Management, 2(2), 31-57.

Preston, L. E. (1978). Analyzing corporate social performance: Methods and results. Journal of

Contemporary Business, 7(1), 135-149. Ratanajongkol, S., Davey, H., & Low, M. (2006). Corporate social reporting in Thailand: The news is all

good and increasing. Qualitative Research in Accounting & Management, 3(1), 67-83. Riahi-Belkaouhi, A. (2001). Level of multinationality, growth opportunities, and size as determinants of

analysts ratings of corporate disclosures. American Business Review, 19(2), 115-120. Rizk, R., Dixon, R., & Woodhead, A. (2008). Corporate social and environmental reporting: a survey of

disclosure practices in Egypt. Social Responsibility Journal, 4(3), 306-323. Roberts, C. (1992). Environmental disclosures in corporate annual reports in Western Europe. Owen

D.(ed). Romlah, J., Takiah, M., & Nordin, M. (2002). An Investigation of Environmental Disclosures: Evidence

from selected industries in Malaysia. International Journal of Business and Society, 3(2), 55–68. Singh, D. A., & Gaur, A. S. (2009). Business group affiliation, firm governance, and firm performance:

Evidence from China and India. Corporate Governance: An International Review, 17(4), 411-425. Skinner, D. J. (1994). Why firms voluntarily disclose bad news. Journal of Accounting Research, 32(1),

38-60. Stanwick, S. D., & Stanwick, P. A. (1998). Corporate social responsiveness: an empirical examination

using the environmental disclosure index. International Journal of Commerce and Management, 8(3/4), 26-40.

Tagesson, T., Blank, V., Broberg, P., & Collin, S. O. (2009). What explains the extent and content of

social and environmental disclosures on corporate websites: a study of social and environmental reporting in Swedish listed corporations. Corporate Social Responsibility and Environmental Management, 16(6), 352-364.

Teoh, H. Y., & Thong, G. (1984). Another look at corporate social responsibility and reporting: An

empirical study in a developing country* 1. Accounting, Organizations and Society, 9(2), 189-206. Thompson, P., & Zakaria, Z. (2004). Corporate social responsibility reporting in Malaysia. Journal of

Corporate Citizenship(13), 125-136. Tilt, C. A. (1994). The influence of external pressure groups on corporate social disclosure: some

empirical evidence. Accounting, Auditing & Accountability Journal, 7(4), 47-72. Trotman, K. T., & Bradley, G. W. (1981). Associations between social responsibility disclosure and

characteristics of companies. Accounting, Organizations and Society, 6(4), 355-362. . Tsang, E. W. K. (1998). A longitudinal study of corporate social reporting in Singapore: the case of the

banking, food and beverages and hotel industries. Accounting, Auditing & Accountability Journal, 11(5), 624-635.

Uhlaner, L. M., van Goor-Balk, H. J. M. A., & Masurel, E. (2004). Family business and corporate social

ePROCEEDINGS FOR 2011 INTERNATIONAL RESEARCH CONFERENCE AND COLLOQUIUM Contemporary Research Issues and Challenges in Emerging Economies

24

responsibility in a sample of Dutch firms. Journal of Small Business and Enterprise Development, 11(2), 186-194.

Ullmann, A. A. (1985). Data in search of a theory: A critical examination of the relationships among social

performance, social disclosure, and economic performance of US firms. Academy of Management Review, 540-557.

Unerman, J. (2000). Methodological issues-Reflections on quantification in corporate social reporting

content analysis. Accounting, Auditing & Accountability Journal, 13(5), 667-681. Waddock, S. A., & Graves, S. B. (1997). The corporate social performance–financial performance link.

Strategic management journal, 18(4), 303-319. Wallace, R. (1988). Corporate Financial Reporting in Nigeria. Accounting and Business Research ,Vol.

18, No. 72, pp. 352-362. Wallace, R. and Naser, K. (1995). Firm-Specific Determinants of the Comprehensiveness of Mandatory

Disclosures in the Corporate Annual Reports of Firms Listed on th Stock Exchange of Hong Kong. Journal of Accounting and Public Policy, Vol. 14, pp. 311-368.

Watts, R. L., & Zimmerman, J. L. (1978). Towards a positive theory of the determination of accounting

standards. Accounting Review, 112-134. Williams, S. M., & Ho Wern Pei, C. A. (1999). Corporate social disclosures by listed companies on their

web sites: an international comparison. The International Journal of Accounting, 34(3), 389-419. Zain, M. M. (1999). Corporate social reporting in Malaysia: the current state of the art and future

prospects. Unpublished PhD thesis, University of Sheffield, Sheffield. Zain, M. M., & Janggu, T. (2006). Corporate social disclosure (CSD) of construction companies in

Malaysia. Malaysian Accounting Review, 5(1), 85-114. Zeghal, D., & Ahmed, S. A. (1990). Comparison of social responsibility information disclosure media used

by Canadian firms. Accounting, Auditing & Accountability Journal, 3(1).