File 17539

34

1 Introduction to Letters of Credit Jenni Lajzerowicz Senior Associate Energy Trade & Transport Group Norton Rose LLP 22 October 2008

-

Upload

prashant-gupta -

Category

Documents

-

view

218 -

download

0

Transcript of File 17539

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 1/34

1

Introduction to

Letters of CreditJenni LajzerowiczSenior Associate

Energy Trade & Transport GroupNorton Rose LLP22 October 2008

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 2/34

2

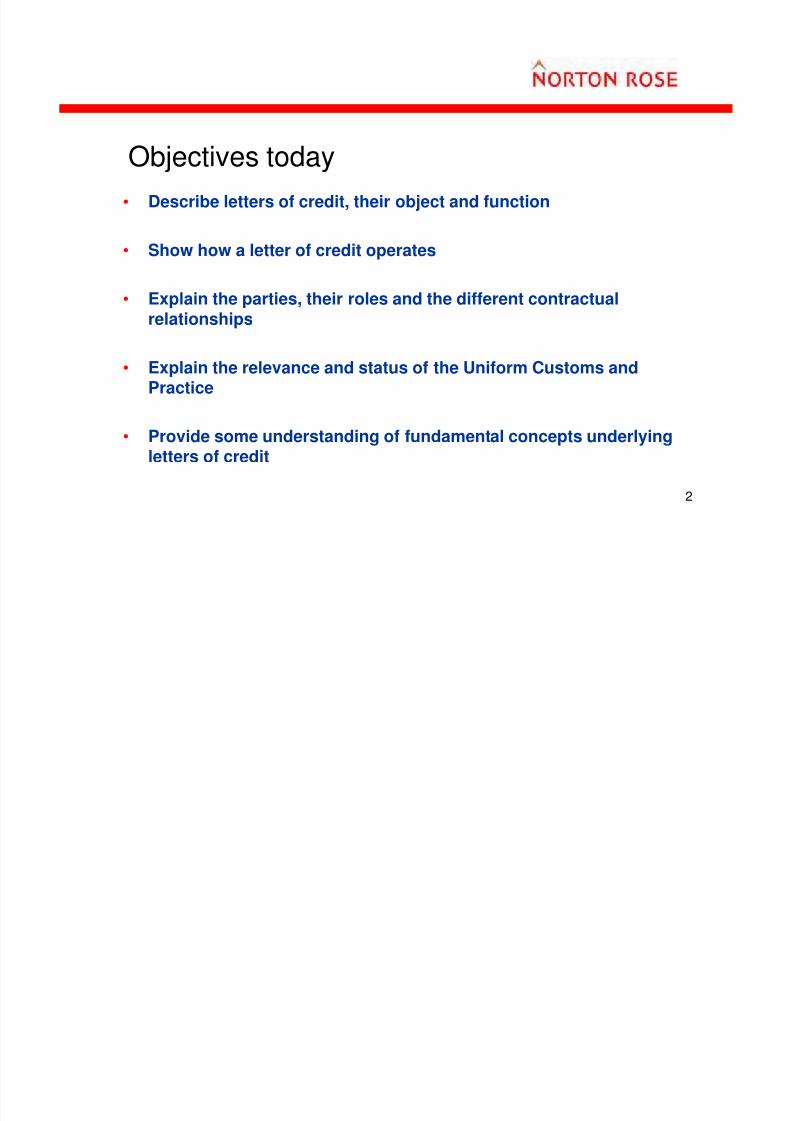

Objectives today

• Describe letters of credit, their object and function

• Show how a letter of credit operates

• Explain the parties, their roles and the different contractualrelationships

• Explain the relevance and status of the Uniform Customs and

Practice

• Provide some understanding of fundamental concepts underlyingletters of credit

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 3/34

3

What is a letter of credit? Why is it used?

• Seller in country A – Malaysia

• Seller sells palm oil to the buyer

shipped from Malaysia to

Rotterdam

• Risk to seller if it parts with

possession and title and ships

goods on basis of buyer’s promise

to pay alone

• Buyer in country B - USA

• Buyer buys palm oil for delivery at

Rotterdam

• Risk to buyer if it pays for goods before

shipment

• Plus immediate tying up of buyer’s

capital

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 4/34

4

“A letter of credit is a commercial instrument used as a means offinancing international business transactions”

“A letter of credit is a contract under which a bank agrees to pay theseller in connection with the export of specific goods against thepresentation of specified documents relating to those goods … Thecredit is issued at the request of the buyer (the applicant) in favourof the seller (the beneficiary)”

What is a letter of credit? Why is it used?

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 5/34

5

What is a letter of credit? Why is it used?

• A banker’s assurance of payment

against specified documents

• Most frequent method of payment in

international trade

• Used for over [ ] years

• Adaptable – e.g. trade finance,

provision of services not just goods,

and as guarantee instruments in the

form of standby letters of credit

• Sales contract does not provide security for

either party. Object of credit is two-fold: to

(1) furnish security and (2) raise credit

• Risk to seller if it parts with possession of

and title to the goods and ships them on

basis of buyer’s promise to pay; and,

• Risk to buyer if it pays for goods before

shipment

• Raising credit without having to tie up capital

whilst goods are on board ship

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 6/34

6

To fully understand the operation of the letter of credit, we need to look at thefollowing:

(1) The parties involved and their respective roles

(2) The contracts involved

(3) The mechanisms of the transaction

(4) Fundamental concepts

(5) The UCP

How does a letter of credit operate?

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 7/34

7

Four parties and the contracts involved

Four parties• The buyer (the applicant)

• The issuing bank

• The advising bank (may also be the correspondent, nominated,

confirming bank)• The seller (the beneficiary)

Four bilateral contracts between

• The buyer and the issuing bank• The issuing bank and the advising/nominated/confirming bank

• The issuing bank and the seller

• The confirming bank and the seller

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 8/34

8

Role of the banks

Issuing bank• The issuing bank is buyer’s bank

• In buyer’s own country

• The seller will be wary of receiving a credit from a bank in a different

country

Advising bank

• The advising bank advises the credit

• Also known as the “correspondent” bank• Can be a nominated bank and/or a confirming bank

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 9/34

9

Role of the banks

Nominated bank• Normally the advising bank

• Nominated by issuing bank to be bank where the seller presentsdocuments

• and obtains payment

Confirming bank

• Nominated bank may be authorised to pay in accordance with the termsof the credit

• BUT it will only be liable to the seller if it adds its own undertaking to thecredit (= a confirmed letter of credit)

• Nominated bank becomes a confirming bank

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 10/34

10

How does a letter of credit operate?

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 11/34

11

How the letter of credit operates: the four stages

Stage 1 - Sales contract

• Starting point = the sales contract

• Provision for payment by letter of credit

• Precise terms of the letter of credit

• Mirror: sales contract requirements and the letter of credit opened

• No indication in the sales contract as to the type of credit required?

• Contract no.1: the sales contract between the buyer and the seller

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 12/34

12

How the letter of credit operates: the four stages

Stage 2 – Instruction to the issuing bank

• Buyer requests issuing bank to open credit in favour of the seller

• Involves completing bank’s standard application form

• Buyer will add his instructions: documents to be tendered; description ofgoods; type of credit to be opened

• Issuing bank acts on the buyer’s instructions alone

• Once the application is made, the bank notifies the buyer in writing of itsagreement to open the credit

• Contract no.2: application form = basis of contract between buyer and

issuing bank

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 13/34

13

How the letter of credit operates: the four stages

Stage 3 – Opening of the credit

• The issuing bank notifies the seller of the opening of the credit in his favour; or,

• It arranges for the advising bank to do so; usually, its correspondent bank in

the seller’s own country

• Advising the credit is usually done in electronic form; e.g. SWIFT

• Notification by the advising bank constitutes the letter of credit

• The issuing bank will become bound to the seller immediately as the sellerreceives the letter of credit

• Contract no.3: between the issuing bank and the advising bank

• Contract no.4: between the issuing bank and the seller

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 14/34

14

How the letter of credit operates: the four stages

Stage 3 – Opening of the credit – other parties

• Nominated bank: Unless the credit is only available with the issuing bank, it mustnominate the bank authorised to pay (or issue a deferred payment undertaking,accept drafts or negotiate the credit)

• Unless the nominated bank is also the confirming bank, neither the nomination by the

issuing bank nor the nominated bank’s receipt, examination or forwarding ofdocuments commits the nominated bank

• The advising bank does not incur any liability to the seller merely by advising theopening of the letter of credit

• Confirming bank: if a confirmed credit, the correspondent/advising bank must add its“confirmation” to the credit; i.e. undertake to seller to honour the credit on presentationof the documents

• Contract no.5: contract between correspondent/confirming bank and the seller

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 15/34

15

How the letter of credit operates: the four stages

Stage 4 – Operation of the credit by the beneficiary

• The seller/beneficiary has shipped the goods

• And has presented documents to operate the credit

• The bank will check that the documents comply and are presented in accordance

with the credit

• IF the documents are in order, the bank will pay the seller/beneficiary (or it willcomply with whatever undertaking the credit provides for)

• IF the documents are not in order, the bank must refuse them

• Before refusal becomes final, at seller’s request the bank may take instructionsfrom the issuing bank or the applicant itself (the buyer) to see whether the applicant

is prepared to accept non-conforming documents

• COMMON for buyers to waive discrepancies because they want the goods

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 16/34

16

How does a letter of credit operate?

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 17/34

17

At the request of the buyer, the issuing bank promises to pay the price of the

goods to the seller against the tender of relevant documents.

To fully understand the operation of the letter of credit, we need to look at thefollowing:

(1) The parties involved and their respective roles

(2) The contracts involved

(3) The mechanisms of the transaction

(4) Fundamental concepts

(5) The UCP

How does a letter of credit operate?

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 18/34

18

Fundamental concepts

• The autonomy of a letter of credit

• Bank’s concern with documents, not facts

• Non-conforming documents and the doctrine of strict compliance

• Each bank’s undertaking as principal

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 19/34

19

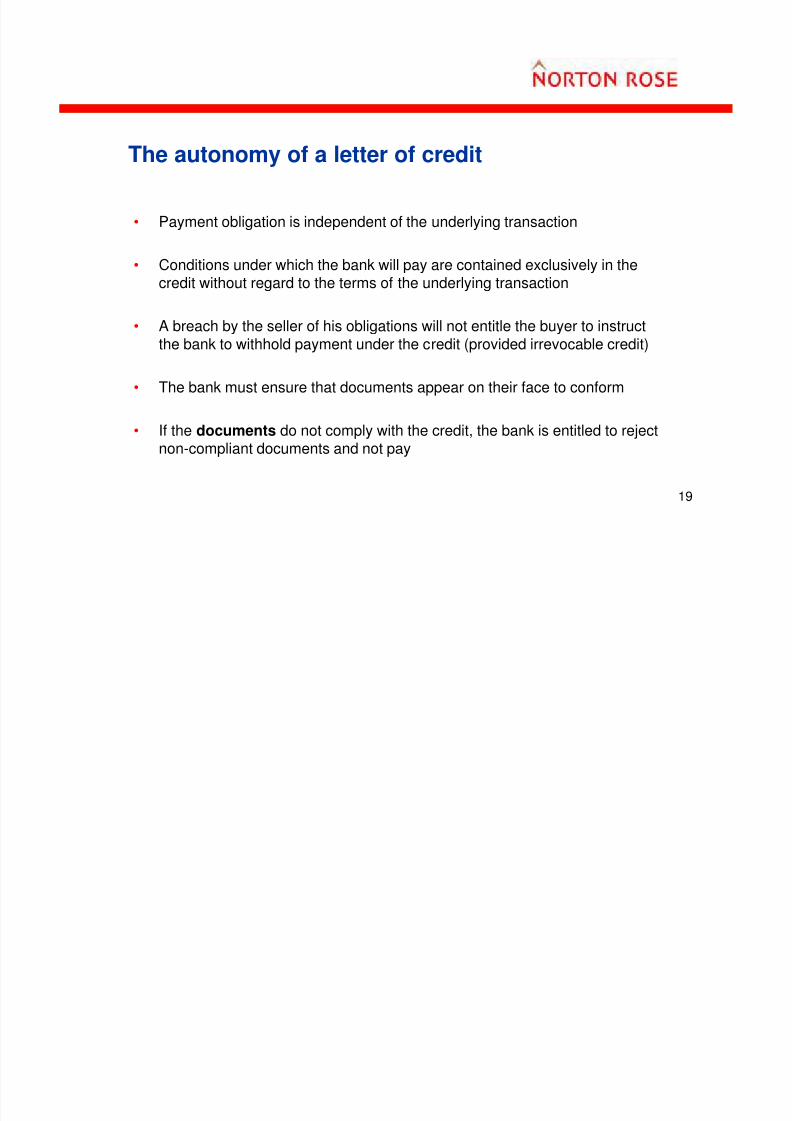

The autonomy of a letter of credit

• Payment obligation is independent of the underlying transaction

• Conditions under which the bank will pay are contained exclusively in thecredit without regard to the terms of the underlying transaction

• A breach by the seller of his obligations will not entitle the buyer to instruct

the bank to withhold payment under the credit (provided irrevocable credit)

• The bank must ensure that documents appear on their face to conform

• If the documents do not comply with the credit, the bank is entitled to rejectnon-compliant documents and not pay

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 20/34

20

The autonomy of a letter of credit

Non-payment

• There are two main exceptions to the confirming or issuing bank’s obligationto pay notwithstanding that the documents appear to be in good order

• They are:

– Illegality; and,

– Fraud

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 21/34

21

Bank’s concern with documents, not facts

• Bank’s concern with documents, not facts

• Must check documents conform on their face (in the absence of strongevidence of fraud or illegality)

• Bank does not check the veracity of the statements contained in the

documents, nor to examine the goods

• This runs hand in hand with the principle of autonomy of the credit

• If the documents appear to be in order, the bank is entitled and obliged topay

• Non-compliant documents mean the bank can withhold payment even if thenon-compliance is purely technical and not material

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 22/34

22

Non-conforming documents and the doctrine of

strict compliance

• The doctrine of strict compliance applies to all contracts involved in theletter of credit operation

• A minor discrepancy or one which does not serve any useful purpose is stilla discrepancy

• UCP 600 provisions on examination of documents should assist slightly tolessen purely technical discrepancies

• ISBP which should be read with the UCP should also assist

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 23/34

23

Each bank’s undertaking as principal

• Issuing bank’s undertaking to the seller is given as principal and not as the

buyer’s agent

• He is a stranger to the letter of credit contract; i.e. not even an “undisclosedprincipal”.

• Therefore, primarily liable to seller to pay out under credit

• Consequences: the buyer is not entitled to give instructions to the issuingbank to refuse payment under the credit, nor to vary the terms of the credit

• The buyer cannot be sued under the letter of credit if the issuing bank failsto pay seller (although the buyer will incur liability for breach of the sales

contract)

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 24/34

24

The Uniform Customs and Practice (“UCP”)

• Rules for commercial credits

• Current edition: UCP 600 (issued in July 2007)

• Advantages

• International Standard Banking Practice (ISBP)

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 25/34

25

UCP 600

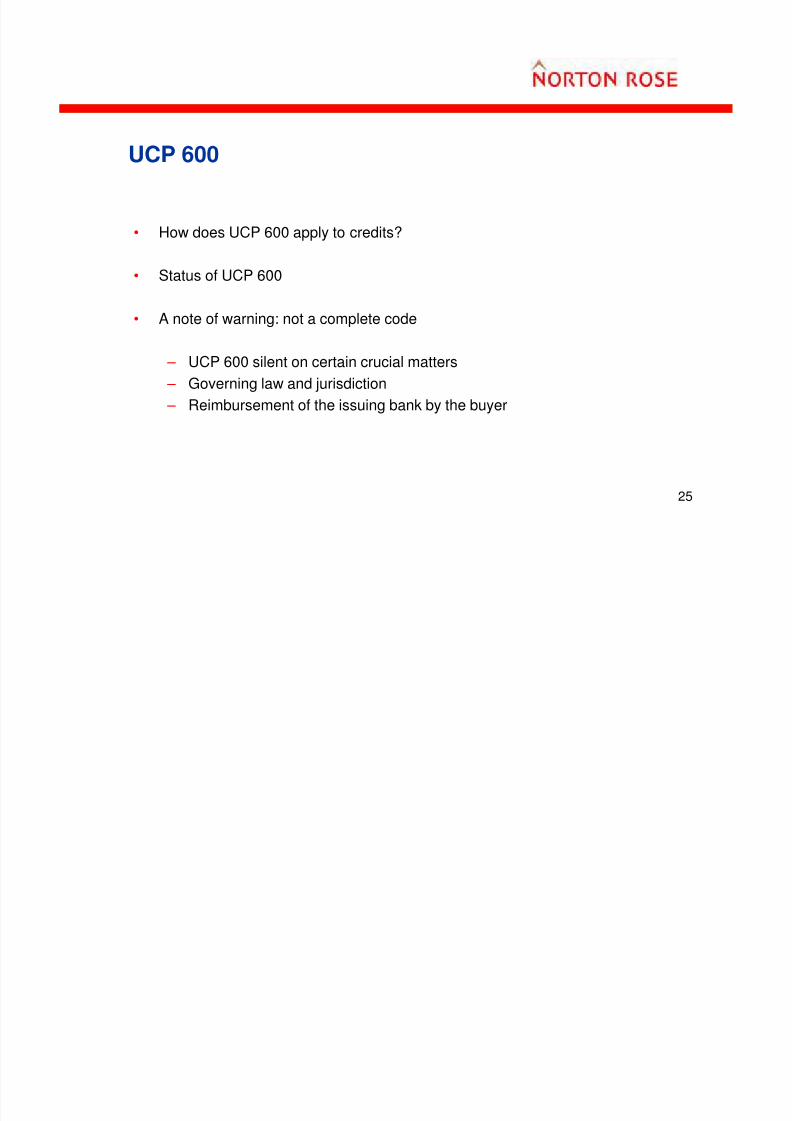

• How does UCP 600 apply to credits?

• Status of UCP 600

• A note of warning: not a complete code

– UCP 600 silent on certain crucial matters

– Governing law and jurisdiction

– Reimbursement of the issuing bank by the buyer

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 26/34

26

GOVERNING LAW

“A wholly undesirable multiplicity of potentially conflicting laws”

• A number of bilateral contracts not a single transaction

• Each potentially subject to a different governing law

• UCP 600 has no provisions to determine governing law therefore this must

be agreed between the parties and specified in the credit

• Conflict of laws: “closest connection” test under English law

– NOT location of central administration of banks, nor place where

contract made – Rather place where documents to be tendered are presented and

checked; and,

– where payment to the seller is to be made against those documents

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 27/34

27

UCP 600 VERSUS UCP 500

• Structural “cosmetic” changes and more fundamental changes

• Objective: to ensure clarity and consistency in approach

• Standard for examination of documents: Art 14, UCP 600 – data in

documents must “not conflict” with other data (versus “consistent”)

• mirror image no longer required

• Non-documentary conditions are disregarded

• Affects technical discrepancies as opposed to real ones

• Easier for a document to be compliant than under UCP 500

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 28/34

28

UCP 600

Bills of lading

• A bank will only accept a “clean” transport document (Art 27, UCP 600) whetheror not the credit requires this

• Bears no clause or notation expressly declaring a defective condition of the goods

or their packing. The word “clean” need not appear

• A claused bill of lading is not a “clean” bill. Defective bill? But bank cannot checkunderlying sales contract (principle of autonomy)

• De minimis? Allowance allowed? See credit terms

• What if bill states goods fine on loading BUT damaged on board?

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 29/34

29

Types of letters of credit

• Confirmed credits, sight credits, deferred payment credits and acceptance

credits

• Straight (or specially advised) credits and negotiation credits

• Revocable and irrevocable credits

• Revolving credits

• Red clause and green clause credits

• Transferable credits and back-to-back credits

• Demand guarantees and standby credits

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 30/34

30

Conclusion

• Complex area

• Understanding of why a letter of credit is used

• Better understanding of how a letter of credit operates in practice with

reference to the individual parties, their respective roles and the multiplecontracts in operation

• Brief view of fundamental concepts relevant to letters of credit and the role

and status of UCP 600

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 31/34

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 32/34

32

Our international practiceAsia

BangkokBeijingHong KongJakarta*

ShanghaiSingaporeTokyo

Middle East

Bahrain

DubaiRiyadh*

Russia

Moscow

Europe

AmsterdamAthensBrusselsFrankfurt

LondonMilanMunichParisPiraeusPrague

RomeWarsaw

*Associate offices

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 33/34

33

Presentation disclaimers

1 No individual who is a member, partner, shareholder, employee or consultant of, in or to any constituent part of Norton Rose

Group (whether or not such individual is described as a “partner”) accepts or assumes responsibility, or has any liability, to anyperson in respect of this presentation.

2 Any reference to a partner means a member of Norton Rose LLP or a consultant or employee of Norton Rose LLP or one of its

affiliates with equivalent standing and qualifications.

3 This presentation contains information confidential to Norton Rose Group. Copyright in the materials is owned by Norton Rose

Group and the materials should not be copied or disclosed to any other person without the express authorisation of Norton Rose.

4 This presentation is not intended to give legal advice and, accordingly, it should not be relied upon. It should not be regarded as a

comprehensive statement of the law and practice in this area. Readers must take specific legal advice on any particular matter

which concerns them. If you require any advice or information, please speak to your usual contact at Norton Rose Group.

8/8/2019 File 17539

http://slidepdf.com/reader/full/file-17539 34/34

34