Figure 1.1 The Structure of Private Equity: Firms, Funds ...€¦ · Figure 2.1 T otal Capital...

27

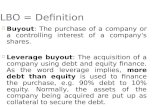

General Partners, Private Equity Firm Private Equity Fund 2 Private Equity Fund 1 Portfolio Company 1 Limited Partners •Pensionfunds •Endowments •Wealthy individuals Creditors •Banks •Bondholders Stakeholders •Managers •Workers •Suppliers •Communities Stakeholders •Managers •Workers •Suppliers •Communities Portfolio Company 2 Fees (2percentof capital annually) Owninvestment 1to2percent Equityinvestment (30to40percent ofprice) Equityinvestment (30to40percent ofprice) Loans (60to70 percent ofprice) Loans (60to70 percent ofprice) Capitalgains (assetsales, dividend recapitalizations, resale) Debtservice (interest, principal) 20percentprofits (carry)after 8percenthurdle Advisory/ management fees Advisory/ management fees 98percent ofcapital Returns Source: AdaptedfromWatt2008. Figure 1.1 The Structure of Private Equity: Firms, Funds, and Portfolio Companies

Transcript of Figure 1.1 The Structure of Private Equity: Firms, Funds ...€¦ · Figure 2.1 T otal Capital...

General Partners, Private Equity Firm

PrivateEquityFund 2

PrivateEquityFund 1

PortfolioCompany 1

LimitedPartners

•Pensionfunds•Endowments•Wealthy

individuals

Creditors•Banks•Bondholders

Stakeholders•Managers•Workers•Suppliers•Communities

Stakeholders•Managers•Workers•Suppliers•Communities

PortfolioCompany 2

Fees(2percentofcapitalannually)

Owninvestment1to2percent

Equityinvestment(30to40percentofprice)

Equityinvestment(30to40percentofprice)

Loans(60to70percentofprice)

Loans(60to70percentofprice)

Capitalgains(assetsales,

dividendrecapitalizations,

resale)

Debtservice(interest,principal)

20percentprofits(carry)after8percenthurdle

Advisory/managementfees

Advisory/managementfees

98percentofcapital

Returns

Source: AdaptedfromWatt2008.

Figure 1.1 The Structure of Private Equity: Firms, Funds, and Portfolio Companies

Table 1.1 Differences Between Private Equity–Owned and Public Corporations

Dimension Private EquityPublic

Corporations

Risk-taking High Low“Moral hazard” High LowerCapital structure 70 percent debt,

30 percent equity30 percent debt,

70 percent equityUse of junk bonds Considerable LowAsset sales for profits Higher LowerDividend recapitalizations Frequent RareFees Key part of earnings No advisory feesTaxes Capital gains rate Corporate rateLegal oversight Low HighTransparency Low HigherAccountability Low Higher

Source: Authors’ compilation.

Figure 2.1 Total Capital Invested in Leveraged Buyouts and Deal Count, by Year, 2000 to 2012

$91

$62

$69

$133

$197

$280

$460

$775

$281

$124

$306

$333

$309

740

547664

1,008

1,396

1,722

2,136

2,536

1,787

1,040

1,5311,673

1,529

0

500

1,000

1,500

2,000

2,500

3,000

$0

$100

$200

$300

$400

$500

$600

$700

$800

Capital Invested (Billions of Dollars)

Source: PitchBook.

To

tal

Cap

ital

In

ves

ted

(in

Bil

lio

ns

of

Do

llar

s)

Dea

l C

ou

nt

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Cumulatively, private equity firms invested a total of about $3.4 trillion

Figure 2.2 Cumulative Inventory of Private Equity Investments by Year, 2000 to 2012

Source: PitchBook.

417723

1,087

1,609

2,269

2,991

3,843

4,747

5,4275,702

6,114

6,4566,769

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

As of Year

2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2000

2001

Nu

mb

er o

f C

om

pan

ies

Figure 2.3 Total Capital Invested, by Sector, 2000 to 2012

Source: PitchBook.

Business Productsand Services

26%

Consumer Productsand Services

26%Energy9%

FinancialServices

9%

Health Care11%

InformationTechnology

13%

Materials andResources

6%

Figure 2.4 Total Capital Invested, by Region, 2000 to 2012

Source: PitchBook.

Midwest3% Mountain

7%

South19%

Southeast14%

West Coast13%

Great Lakes18%

Mid-Atlantic20%

NewEngland

6%

Table 2.1 Top Ten Largest Buyouts in History, as of 2012

Company

Deal Value (Billions of U.S.

Dollars) PE Investors Date Industry

TXU (Energy Futures Holding)

$43.80 KKR, Goldman Sachs Capital Partners, TPG

2007 Utilities/energy

Equity Office Properties Trust

38.90 Blackstone Real Estate Partners LP

2007 Real estate

HCA, Inc. 32.70 Bain Capital, Inc., KKR, Merrill Lynch Global Private Equity

2007 Health care

RJR Nabisco, Inc. 31.10 KKR 1988 Food/tobaccoAlltel Corporation 27.87 TPG, Goldman Sachs

Capital Partners LP2007 Telecom

First Data Corporation

27.73 KKR 2007 Finance/ technology

Harrah’s Entertainment, Inc.

27.40 Apollo Management LP, TPG

2008 Entertainment

Hilton Hotels, Inc. 25.80 Blackstone Group LP 2007 LodgingClear Channel

Communications, Inc.

24.86 Bain Capital, Inc., Thomas H. Lee Partners

2008 Media

Kinder Morgan, Inc. 21.56 Goldman Sachs Capital Partners LP, AIG Global Asset Management, Riverstone Holdings, and Carlyle Group, Inc.

2007 Energy

Source: Pensions&Investments, “Largest Leveraged Buyouts,” January 16, 2013. Available at: http://www.pionline.com/gallery/20130116/SLIDESHOW2/116009999/1 (accessed February 13, 2014).

Capital Invested

Source: PitchBook.

To

tal

Cap

ital

In

ves

ted

(in

Bil

lio

ns

of

Do

llar

s)

Dea

l C

ou

nt

$167

$172

$190

$245

$100

$55

$92

$35

$42

$20

$21

$41

$62

$68

$62

$114

$81

$73

$84

$97

$63

$67

$61

$118

634

666 639

597591

416

465

315 263

243 244

290

366

330338

497

397

411

405

460

386

352 346

445

0

100

200

300

400

500

600

700

$0

$50

$100

$150

$200

$250

$300

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

2007 2008 2009 2010 2011 2012

Deals Closed

Figure 4.1 Total Capital Invested in Leveraged Buyouts and Deal Count, Quarterly, 2007 Q1 to 2012 Q4

Source: Preqin, reprinted from Bain & Company, Inc., Global Private Equity Report 2013.Note: DPI is the ratio of distributed to paid-in capital.

Per

cen

tag

e

100

0

20

40

60

80

2000 2001 2002 2003 2004 2005 2006

Vintage Year

Percentage of Funds with DPI Less than One

2007 2008 2009 2010 2011 2012

13 12 31 42 48 71 96 92 97 90 98 100 100

Realized Capital Value Unrealized Capital Value Uncommitted Capital

Figure 4.2 Relative Mix of Realized, Unrealized, and Uncommitted Capital, 2000 to 2012

Table 4.1 U.S. Private Equity Firms with Assets Under Management Valued at More Than $20 Billion, 2013

Investor NameActive

Investments

Investments in the Last Five Years

Assets Under Management (Millions of

Dollars)

Blackstone Group (BX) 172 202 $248,000Carlyle Group (CG) 255 220 180,400Apollo Global Management (APO) 66 82 113,100Kohlberg Kravis Roberts (KKR) 120 173 90,200Goldman Sachs Capital Partners 119 122 76,217Oaktree Capital Management 80 100 74,900Bain Capital 69 110 70,000GTCR Golder Rauner 39 75 69,732CVC Capital Partners 41 51 68,034TPG Capital 100 129 60,551Apax Partners 62 96 46,619Warburg Pincus 144 116 39,370Resource Capital Funds 17 12 34,000Lone Star Funds 15 17 30,830Kelso & Co. 24 35 27,000Providence Equity Partners 54 66 27,000Silver Lake Partners 29 61 25,962Riverstone Holdings 67 66 23,445Cerberus Capital Management 57 42 23,000Lexington Partners 5 9 22,500New MainStream Capital 1 2 22,000First Reserve 51 41 20,897Hellman & Friedman 26 54 20,800Black Canyon Capital 6 8 20,000Centerbridge Partners 23 40 20,000Welsh, Carson, Anderson & Stowe 55 47 20,000

Source: PitchBook.

Middle-Market Capital Invested

Source: PitchBook.

Mid

dle

-Mar

ket

Cap

ital

In

ves

ted

(Bil

lio

ns

of

Do

llar

s)

Dea

l F

low

Middle-Market Deal Flow

$84

$50

$58

$103

$147

$190

$273

$351

$173

$86

$244

$254

$230

521

327 408

648

945

1,149

1,438

1,792

1,129

628

1,051

1,190

1,092

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

$0

$50

$100

$150

$200

$250

$300

$350

$400

2000 2001 2002 2003 2004 2005 2006

Year

2007 2008 2009 2010 2011 2012

Figure 5.1 Middle-Market Leveraged Buyout Deal Flow, by Year, 2000 to 2012

Source: PitchBook.

Nu

mb

er o

f L

BO

s

0

500

1,000

1,500

2,000

2,500

3,000

2000 2001 2002 2003 2004 2005 2006

Year

2007 2008 2009 2010 2011 2012

$0 to $25 Million

$25 Million to $100 Million

$100 Million to $500 Million

$500 Million to $1 Billion

$1 Billion or More

Figure 5.2 Leveraged Buyouts by Market Segment, 2000 to 2012

Source: PitchBook.

Cap

ital

In

ves

ted

in

LB

Os

(Mil

lio

ns

of

Do

llar

s)

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

2000 2001 2002 2003 2004 2005 2006

Year

2007 2008 2009 2010 2011 2012

$0 to $25 Million

$25 Million to $100 Million

$100 Million to $500 Million

$500 Million to $1 Billion

$1 Billion or More

Figure 5.3 Capital Invested in Leveraged Buyouts by Market Segment, 2000 to 2012

Figure 5.4 Exits by Market Segment, Pre- and Post-Crisis, 2003 to 2012

Source: PitchBook.

0

100

200

300

400

500

600

700

2003 to2007

2008 to2012

2003 to2007

2008 to2012

2003 to2007

2008 to2012

2003 to2007

2008 to2012

Under$25 Million

$25 Million to$100 Million

$100 Million to$500 Million

$500 Millionor More

Initial Public OfferingCorporate AcquisitionSecondary Buyout

Nu

mb

er o

f E

xit

s

Figure 5.5 Debt and Equity Multiples by Market Segment, Pre- and Post-Crisis

Source: PitchBook.

Equity/EBITDADebt/EBITDAValuation/EBITDA

2.45x 2.40x3.28x 3.77x 3.62x 4.00x

2.95x 2.40x

5.42x 4.53x

8.33x6.00x

5.40x4.80x

8.70x 8.30x

11.95x

10.00x

x

2x

4x

6x

8x

10x

12x

14x

2003 to2007

2008 to2012

2003 to2007

2008 to2012

2003 to2007

2008 to2012

Under$100 Million

$100 Million to$500 Million

$500 Millionor More

Mu

ltip

les

Table 5.1 Total Number and Value of U.S. Leveraged Buyouts, by Market Segment, 2000 to 2012

Market SegmentTotal Number

of LBOsPercentage Deal Count

Total Capital Invested

Average Percentage

Capital Invested

$0 to $25 million 5,639 32% $56.67 2%$25 million to

$100 million5,701 32 287.70 11

$100 million to $500 million

5,307 28 1,105.72 36

$500 million to $1 billion

1,309 6 852.59 25

$1 billion or more 352 2 1,122.75 25Total 18,308 100 3,425.42 100

Source: PitchBook.

Table 6.1 Hypothetical Net Cash Flow Data from Funds X, Y1, Y2, and Z

Year Fund X Fund Y1 Fund Y2 Fund Z Fund XYZ

0 −100 −100 −100 −100 −4001 150 0 0 0 1502 0 0 0 0 03 50 0 0 0 504 0 0 0 0 05 0 100 100 50 2506 0 0 0 0 07 0 0 0 0 08 0 100 100 0 2009 0 0 0 0 010 0 0 0 0 011 0 0 0 0 012 0 0 0 10 10Internal rate of return 68% 11% 11% −8% 12%Multiple (distribution

to paid-in capital)2.00 2.00 2.00 0.60 1.28

Source: Phalippou 2008, 18.

PE-Owned Company PE Owners Unions

Company Economic Condition

Equity Invested Deal Value

Deal Year

Labor Relations

PE Outcomes, Returns

Company and Labor Outcomes

Spirit AeroSystems (Aerospace)

Onex Partners

IAM, SPEEA

Strong $464 $1,500 2005 Constructive 2007, 2001 IPOs yield $2.5 billion in returns; Onex still majority owner

2005–2012: Unions accept cuts in jobs wages and retiree benefits; com-pany IPO in 2006 yields large bonuses for work-ers; strong company per-formance; job growth; stable union relations

Five US Steel Legacy Companies (20 percent of industry)

Wilbur Ross & Co.

USWA Bankrupt $321 $1,285 2001–2003

Constructive Sold to Mittal Steel for $4.5 billion

Union drives work reorganization and accepts wage and job cuts with contract pro-tections; large cuts in managerial workforce; productivity gains immense; major cuts in retiree pensions of $4.5 billion, equal to pri-vate equity returns

(Appendix continues on p. 236.)

Table 7A.1 Case Summaries of Private Equity Labor Relations Strategies and Outcomes

PE-Owned Company PE Owners Unions

Company Economic Condition

Equity Invested Deal Value

Deal Year

Labor Relations

PE Outcomes, Returns

Company and Labor Outcomes

Dana Corporation (Auto supply)

Centerbridge UAW, USWA

Bankrupt $500 Undisclosed 2008 Constructive 2008; Company emerges from bankruptcy and remains profit-able thereafter

Union contract stipulates limits on debt liabilities to $1.5 billion, which saves company during recession; union agrees to reduced wages and benefits; retirees covered by new health and retire-ment fund

Delphi Corporation (Auto supply)

John Paulson & Co., Silver Point Capital

UAW Bankrupt Undisclosed Undisclosed 2009 Strongly anti-union

2011 IPO yields profit of 3,000 percent

25 of 29 plants shut down; 25,000 union jobs offshored; taxpayers pay $12.9 billion in subsidies

Hawker Beechcraft (Aerospace)

Goldman Sachs Capital, Onex Partners

IAM Strong Undisclosed $3,300 2007 Union marginaliza-tion

2012: Goldman Sachs writes down the com-pany’s value by 85 percent

3,500 workers (36 per-cent of total) lose jobs; union negotiates wage and benefit concessions; 2012 bankruptcy, with $2.6 billion debt; PBGC takes over pension plans

Table 7A.1 Continued

Archway & Mother’s Cookies (Food processing)

Catterton Partners

ICBWU Bankrupt Undisclosed Undisclosed 2005 Strongly anti-union

Management engages in fraud; company acquired by stra-tegic investor Lance, Inc. for $30 million

Substantial cost-cutting; product quality declines; 2008 bankruptcy; plants shutdown, 400 workers lose jobs; workers file lawsuit for violation of WARN Act; new owner re-opens as non-union plant with 60 workers.

Stella D’oro (Food processing)

Brynwood Partners

ICBWU Moderate Undisclosed $17.5 2006 Strongly anti-union

Company acquired by stra-tegic investor Lance, Inc. for $17.5 million

Brynwood found guilty of unfair labor practices in contract negotia-tions, shuts down plant in 2009; 134 workers lose jobs

Ormet Aluminum

Matlin Patterson

USWA Bankrupt Undisclosed $30.0 2004 Anti-union to constructive

2005 out of bankruptcy; 2013 back in bankruptcy; sold to Wayzata for $130 million

19-month union cam-paign leads to 2006 labor contract with decent wages and benefits for 1,500 workers; PGBC assumes $260 million in unfunded pension liabilities

US Foods (Food distribution)

Clayton, Dubilier, Rice; KKR; National City Equity Partners

Teamsters Strong Undisclosed $7,100 2007 Anti-union to constructive

2013: High debt of $4.6 billion viewed as high risk profile by S&P

Work intensification, job loss in union sites; expansion in non-union facilities

(Appendix continues on p. 238.)

PE-Owned Company PE Owners Unions

Company Economic Condition

Equity Invested Deal Value

Deal Year

Labor Relations

PE Outcomes, Returns

Company and Labor Outcomes

Energy Futures Holding (Utilities)

TPG, Carlyle IBEW Strong $8,300 $48,100 2007 Constructive 2007–2012: Profit losses; no returns for investors; Carlyle writes off investment; PE gets $171 mil-lion in annual fees

2007–2012: 25% job growth; Positive labor relations; but $44 bil-lion in debt 2013 leads analysts to predict bankruptcy

Hospital Corporation of America (Health care providers)

Bain, KKR, Merrill Lynch, Frist

SEIU, NNU

Strong $4,500 $21,000 2006 Constructive 2010–2011: PE recoups two times its investment— $9 billion through dividend recaps and IPO

2012: Employment relatively stable but on-going union complaints of understaffing; PE negotiates neutrality agreements that bring in over 20,000 new union members; debt remains at $26 billion over assets of $14 billion

Table 7A.1 Continued

Source: PitchBook.

$18.

2

$9.2

$11.

8

$6.9

$13.

9

$14.

2

$31.

2

$33.

2

$40.

3

$34.

4

$7.8

$15.

0

$16.

9

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Year of Fund Close

Pu

bli

c P

ensi

on

Co

mm

itm

ents

to

PE

(Bil

lio

ns

of

Do

llar

s)

Figure 8.1 U.S. Public Pension Commitments to Private Equity, 2000 to 2012

Source: PitchBook.

0

5

10

15

20

25

30

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Year of Fund Close

Per

cen

tag

e

Figure 8.2 Public Pension Funds as a Percentage of Private Equity Fund-Raising, 2000 to 2012

Source: PitchBook.

Nu

mb

er o

f F

un

ds

0

20

40

60

80

100

120

140

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Year of Fund Close

Made Commitment in Prior YearMade Commitment in Prior Three YearsMade Commitment in Prior Five YearsMade Commitment in Prior Ten Years

Figure 8.3 Public Pension Funds with Commitments to Private Equity, 2000 to 2012

Source: PitchBook.Note: 2012 figures as of September 30, 2012.

$(30)

$(25)

$(20)

$(15)

$(10)

$(5)

$0

$5

$10

$15

$20

$25

2000 2001 2002 2003 2004 2005 2006

Year

2007 2008 2009 2010 2011 2012*

ContributionsDistributionsCash Flow

Bil

lio

ns

of

Do

llar

s

Figure 8.4 Contributions from and Distributions to Limited Partners, 2000 to 2012

Table 8.1 Public Pension Funds with the Largest Commitments to Private Equity, 2013

Limited Partner

Private Equity Allocation

(Millions of Dollars)

Private Equity

(Percentage)

Assets Under Management (Millions of

Dollars)

California Public Employees’ Retirement System (CalPERS)

$42,000 16% $269,100

California State Teachers’ Retirement System (CalSTRS)

21,759 13 170,000

Washington State Investment Board

16,170 18 91,360

New York State Common Retirement Fund

14,926 9 160,400

Oregon Investment Council 14,900 18 81,000Oregon Public Employees’

Retirement System13,550 21 63,240

Teacher Retirement System of Texas

13,145 10 134,454

Ontario Municipal Employees’ Retirement System

10,257 12 84,769

Pennsylvania Public School Employees’ Retirement System

8,040 22 50,500

New York State Teachers’ Retirement System

7,400 8 95,100

Florida State Board of Administration

6,500 5 169,200

Florida Retirement System 6,476 5 168,100New York City Employees’

Retirement System5,925 6 46,389

Massachusetts Pension Reserves Investment Trust

5,917 12 54,400

Ohio Public Employees’ Retirement System

5,271 6 82,600

Virginia Retirement System 5,000 9 58,300Teachers’ Retirement System

of the State of Illinois4,600 12 40,200

State Teachers’ Retirement System of Ohio

4,386 7 68,000

New York City Retirement Systems

4,157 4 139,200

(Table continues on p. 246.)

Los Angeles County Employees’ Retirement Association

3,831 9 42,000

Indiana Public Retirement System

3,400 12 28,300

North Carolina Retirement Systems

2,960 4 81,100

Iowa Public Employees’ Retirement System

2,871 11 25,100

Maryland State Retirement Pension System

2,500 6 40,620

State of Connecticut Retirement and Trust Funds

2,265 9 26,600

Teachers’ Retirement System of the City of New York

2,100 6 32,775

Public School Retirement System of Missouri

1,943 6 34,600

Kentucky Retirement Systems

1,796 12 14,600

Arizona State Retirement System

1,754 6 28,400

Source: PitchBook, authors’ calculations.

Table 8.1 Continued

Limited Partner

Private Equity Allocation

(Millions of Dollars)

Private Equity

(Percentage)

Assets Under Management (Millions of

Dollars)