FEG AISNE Fall 2011 Fiduciary Responsibility of Committees Final Slides

24

November 7, 2011 Brian T. Gray Vice President – Institutional Client Development FIDUCIARY RESPONSIBILITY OF COMMITTEES

-

Upload

brian-gray -

Category

Documents

-

view

14 -

download

0

Transcript of FEG AISNE Fall 2011 Fiduciary Responsibility of Committees Final Slides

November 7, 2011 Brian T. Gray Vice President – Institutional Client Development

F I D U C I A R Y R E S P O N S I B I L I T Y O F C O M M I T T E E S

Confidential – Not for Redistribution 1 ©2011 Fund Evaluation Group, LLC

I. Summarize the Challenges Facing Governing Fiduciaries

II. Discuss Oversight Structures

III. Provide Thoughts on Best Practices

AGENDA

Confidential – Not for Redistribution 2 ©2011 Fund Evaluation Group, LLC

• Trustees / Investment Committee Members / Investment Advisors / Money Managers

• Varying Degrees / No Full Delegation

• Stewards – Bound by Loyalty and Good Faith

– Legal responsibility to act in best interest

• Responsible for Prudent Investment Decisions

– “Process is Prudence”

– Not defined by desirable outcomes

WHAT IS A FIDUCIARY?

Confidential – Not for Redistribution 3 ©2011 Fund Evaluation Group, LLC

• Manager Proliferation

• Market Complexity

• Manager Selection

• Committee Dynamics

• Process Deficiencies

• Summary of Ineffective Committees

CHALLENGES FACING FIDUCIARIES

Confidential – Not for Redistribution 4 ©2011 Fund Evaluation Group, LLC

Source: Investment Company Institute

Note: Data for funds that invest primarily in other mutual funds were excluded from the series.

The data contain a series break beginning in 1984. All funds were reclassified in 1984 and a separate category was created for hybrid funds.

PRODUCT PROLIFERATION – U.S. MUTUAL FUNDS

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Number of Funds of the U.S. Mutual Fund Industry 1970-2009

Confidential – Not for Redistribution 5 ©2011 Fund Evaluation Group, LLC

Source: PerTrac Financial Solutions. Numbers of new funds have not been adjusted to account for survivor bias.

PRODUCT PROLIFERATION – HEDGE FUND LAUNCHES

Confidential – Not for Redistribution 6 ©2011 Fund Evaluation Group, LLC

• Number of managers per fund/plan

– Diversification

– Alternative investments

– Global mandates

• Increased use of derivatives

– Substitution

– Hedging

MARKET COMPLEXITY

Confidential – Not for Redistribution 7 ©2011 Fund Evaluation Group, LLC

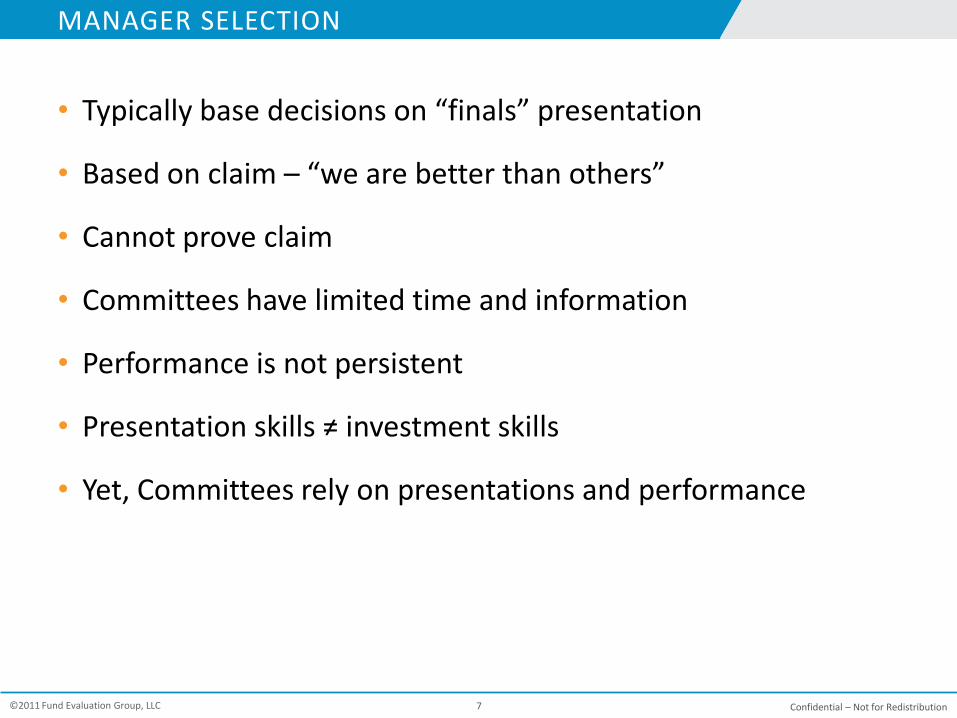

• Typically base decisions on “finals” presentation

• Based on claim – “we are better than others”

• Cannot prove claim

• Committees have limited time and information

• Performance is not persistent

• Presentation skills ≠ investment skills

• Yet, Committees rely on presentations and performance

MANAGER SELECTION

Confidential – Not for Redistribution 8 ©2011 Fund Evaluation Group, LLC

HIRING / FIRING MANAGERS IS DIFFICULT

Source: The Selection and Termination of Investment Managers by Plan Sponsors, Goizeuta Business School, Emory University, 2004 & Why Do Institutional Plan Sponsors Fire Their Investment Managers?, Heisler, Knittel, Neumann, Stewart, 2004

Pe

rce

nta

ge P

oin

ts

3 Year Excess Return Before and After Manager Termination

Confidential – Not for Redistribution 9 ©2011 Fund Evaluation Group, LLC

C R E AT E S I N V E S T M E N T S L I P PA G E

• Delays

• Inappropriate decisions

• No accountability

COMMITTEE DYNAMICS

VOLUNTEERS/ NOT FULL TIME

VARYING DEGREES OF INVESTMENT KNOWLEDGE

SEEK CONSENSUS QUARTERLY MEETINGS

DECISIONS BASED ON COMFORT /

REPUTATION

Confidential – Not for Redistribution 10 ©2011 Fund Evaluation Group, LLC

PROCESS DEFICIENCIES

Barriers to Excellence 1

1 Pension Fund Excellence, Keith P. Ambachtsheer and D. Don Ezra

98%

48%43%

35% 35%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Poor Process Inadequate Resources

Lack of focus on Mission

Conservatism Insufficient Skills

Confidential – Not for Redistribution 11 ©2011 Fund Evaluation Group, LLC

INEFFECTIVE COMMITTEES 1

1 Pension Fund Excellence, Keith P. Ambachtsheer and D. Don Ezra, and Investment Committees: Vanguard’s View of Best Practices, Catherine D. Gordon, June 2004

S t r u c t u r a l

Confer membership as a reward

Don’t take time to understand what they don’t know

Evaluate using wrong benchmarks

Rely too heavily on one person

Don’t consider

conflicts of interest

Act as portfolio managers, not

fiduciaries

Confuse opinions with facts

Support compensation system fails to align interests

Crave certainty

Confidential – Not for Redistribution 12 ©2011 Fund Evaluation Group, LLC

INEFFECTIVE COMMITTEES 1

1 Pension Fund Excellence, Keith P. Ambachtsheer and D. Don Ezra, and Investment Committees: Vanguard’s View of Best Practices, Catherine D. Gordon, June 2004

B e h a v i o r a l

Confuse opinions with facts

Fail to recognize investment

theory

React rather

than lead

Postpone decisions

Crave certainty

Take credit for

good things

Assign blame for bad things

Gravitate to those who promise it

Confidential – Not for Redistribution 13 ©2011 Fund Evaluation Group, LLC

I. Summarize the Challenges Facing Governing Fiduciaries

II. Discuss Oversight Structures

III. Provide Thoughts on Best Practices

AGENDA

Confidential – Not for Redistribution 14 ©2011 Fund Evaluation Group, LLC

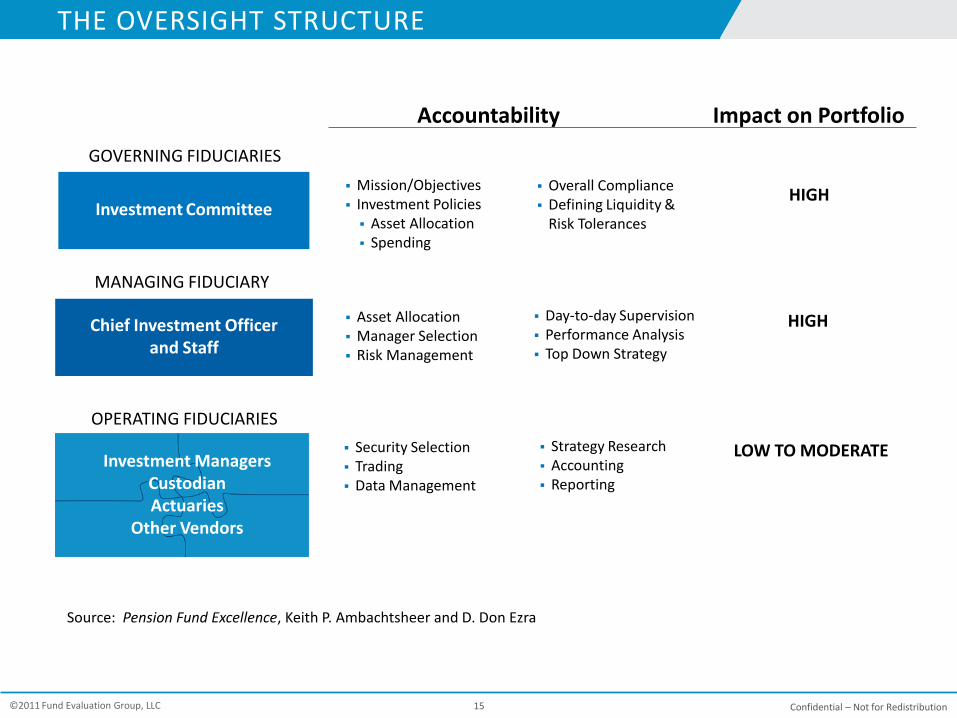

Three levels of fiduciary responsibility 1

• Governing

• Managing

• Operating

FIDUCIARY RESPONSIBILITY

1 Pension Fund Excellence, Keith P. Ambachtsheer and D. Don Ezra

Confidential – Not for Redistribution 15 ©2011 Fund Evaluation Group, LLC

THE OVERSIGHT STRUCTURE

Investment Committee

Chief Investment Officer and Staff

Investment Managers Custodian Actuaries

Other Vendors

GOVERNING FIDUCIARIES

MANAGING FIDUCIARY

OPERATING FIDUCIARIES

Source: Pension Fund Excellence, Keith P. Ambachtsheer and D. Don Ezra

Asset Allocation Manager Selection Risk Management

Day-to-day Supervision Performance Analysis Top Down Strategy

HIGH

Security Selection Trading Data Management

Strategy Research Accounting Reporting

LOW TO MODERATE

Mission/Objectives Investment Policies Asset Allocation Spending

Overall Compliance Defining Liquidity &

Risk Tolerances

Accountability Impact on Portfolio

HIGH

Confidential – Not for Redistribution 16 ©2011 Fund Evaluation Group, LLC

3-TIER CAPTIVE

Investment Committee

CIO and Staff

Investment Managers Custodian Actuaries

Other Vendors

THE OVERSIGHT STRUCTURES EMPLOYED

Adapted from: Pension Fund Excellence, Keith P. Ambachtsheer and D. Don Ezra

2-TIER COMMITTEE DRIVEN

Governing Fiduciaries Investment Committee,

Staff, and Consultant – Supporting

Fiduciary Managing Fiduciary

Operating Fiduciaries

Investment Managers Custodian Actuaries

Other Vendors

3-TIER OUTSOURCED

Investment Committee

Staff and Outsourced CIO

Investment Managers Custodian Actuaries

Other Vendors

Confidential – Not for Redistribution 17 ©2011 Fund Evaluation Group, LLC

I. Summarize the Challenges Facing Governing Fiduciaries

II. Discuss Oversight Structures

III. Provide Thoughts on Best Practices

AGENDA

Confidential – Not for Redistribution 18 ©2011 Fund Evaluation Group, LLC

COMMITTEE STRUCTURE AND PERFORMANCE

EFFECTIVE INEFFECTIVE

Cognitive Diversity Correlated Judgments

6-8 People 10+ People (Ringelmann Effect)

Focus on Process / Big Picture Lack Process Enables Distractions

Strong Leadership: • Reinforces Process / Objectives • Focus and Time Allocated Effectively • Extracts Unshared Information and Options • Decision Method (quorum/majority/consensus)

Weak Leadership: • Social Conformity / Groupthink • Distractions and Wanderers • Suppresses Discovery • Weak Decision Methods

Identify & Classify Problems Effectively Trouble Indentifying Problems

Document/Journal Decisions No Decision Journal

Seek Feedback Weak Feedback Loop

Buy Low, Sell High Buy High, Sell Low

Adapted from Sources: Michael J. Mauboussin – Mauboussin on Strategy: Investment Committees. Sept 1, 2009 and Think Twice – Harnessing the Power of Couterintuition.

Confidential – Not for Redistribution 19 ©2011 Fund Evaluation Group, LLC

• Investment policy statement

• Asset allocation approach

• Manager team

• Implementation shortfall (slippage)

• Define risk (unique to institution) vs. measuring risk of portfolio

• Define liquidity parameters

• Other sensitivities (debt covenants, funded status, etc.)

DECISION MAKING FRAMEWORK

Confidential – Not for Redistribution 20 ©2011 Fund Evaluation Group, LLC

SELF ASSESS

• Have your past decisions contributed or detracted from results?

• Do you have a plan for responding to extreme events?

• Do you chase performance?

• How long does it take to implement a decision you make?

DECISION MAKING FRAMEWORK

Confidential – Not for Redistribution 21 ©2011 Fund Evaluation Group, LLC

GOVERNANCE (Structural)

• Select appropriate oversight structure

• Define “decision rights” and delegate appropriately within structure

• Maintain strong investment process and focus – “Process is Prudence”

• Understand risk in context of institution

• Understand investment horizons required to achieve results

COMMITTEE (Behavioral)

• Leadership fosters open communication and alternative opinion sharing

• Focus on high impact items

• Avoid blame-seeking activities

• Identify and avoid conflicts of interest

• Seek ongoing education

BEST PRACTICES – EFFECTIVE GOVERNANCE

Confidential – Not for Redistribution 22 ©2011 Fund Evaluation Group, LLC

This presentation was prepared by Fund Evaluation Group, LLC (FEG) − an investment adviser registered under the Investment Advisers Act of 1940, as amended − providing non-discretionary and discretionary investment advice to its clients on an individual basis. Registration as an investment adviser does not imply a certain level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser.

The information herein was obtained from various sources. FEG does not guarantee the accuracy or completeness of such information provided by third parties. The information in this report is given as of the date indicated and believed to be reliable. FEG assumes no obligation to update this information, or to advise on further developments relating to it.

Past performance is not indicative of future results.

Neither the information nor any opinion expressed in this report constitutes an offer, or an invitation to make an offer, to buy or sell any securities. FEG, its affiliates, directors, officers, employees, employee benefit programs and client accounts may have a long position in any securities of issuers discussed in this report.

This report is prepared for informational purposes only. It does not address specific investment objectives, or the financial situation and the particular needs of any person who may receive this report.

DISCLOSURE

Confidential – Not for Redistribution 23 ©2011 Fund Evaluation Group, LLC

FIRM CONTACT INFORMATION

201 East Fifth Street

Suite 1600

Cincinnati, OH 45202

Phone: 513.977.4400

Fax: 513.977.4430

www.feg.com

Satellite Offices: Boston / Chicago / Detroit / Indianapolis