FEED THE FUTURE UGANDA COMMODITY …...DEHYDRATED PRECOOKED BEANS PROJECT FEASIBILITY STUDY &...

148

FEED THE FUTURE UGANDA COMMODITY PRODUCTION AND MARKETING ACTIVITY DEHYDRATED PRECOOKED BEANS PROJECT FEASIBILITY STUDY & PRODUCT TEST Final Report Submitted to Prepared by Research World International Ltd P.O. Box 34148, Kampala Tel+256 04 14 699901 , 0776 642 764 GRYPHON GROUP LTD P.O.BOX 12036 KAMPALA UGANDA PHONE +256-7811-49371 EMAIL: [email protected] WEBSITE:WWW.CHIKITABEANSPROJECT.COM

Transcript of FEED THE FUTURE UGANDA COMMODITY …...DEHYDRATED PRECOOKED BEANS PROJECT FEASIBILITY STUDY &...

FEED THE FUTURE UGANDA COMMODITY PRODUCTION AND MARKETING ACTIVITY

DEHYDRATED PRECOOKED BEANS PROJECT

FEASIBILITY STUDY & PRODUCT TEST

Final Report

Submitted to

Prepared by

Research World International Ltd

P.O. Box 34148, Kampala

Tel+256 04 14 699901 , 0776 642 764

GRYPHON GROUP LTD P.O.BOX 12036 KAMPALA UGANDA PHONE +256-7811-49371 EMAIL: [email protected] WEBSITE:WWW.CHIKITABEANSPROJECT.COM

Dehydrated Precooked Beans Feasibility Study& Product Test Draft Report Page ii of 94

Table of Contents

LIST OF TABLES ................................................................................................................................................................... V

LIST OF FIGURES ............................................................................................................................................................... VII

ACRONYMS......................................................................................................................................................................... IX

DEFINITION OF KEY TERMS .................................................................................................................................................. X

EXECUTIVE SUMMARY ........................................................................................................................................................ XI

CHAPTER 1 – INTRODUCTION .............................................................................................................................................. 1

1.1 INTRODUCTION ............................................................................................................................................................... 1

1.2 BACKGROUND ................................................................................................................................................................ 1

1.3 SURVEY OBJECTIVES ........................................................................................................................................................ 1

1.3.1 Overall objective .................................................................................................................................................... 1 1.3.2 Specific objectives

.................................................................................................................................................. 1

CHAPTER 2 – LITERATURE REVIEW ....................................................................................................................................... 3

2.1 OVERVIEW OF THE BEANS SUBSECTOR ................................................................................................................................ 3

2.2 VALUE CHAIN OF BEANS IN UGANDA .................................................................................................................................. 3

2.3 BEANS PRODUCTION IN UGANDA ...................................................................................................................................... 5

2.3.1 Bean varieties grown in Uganda ............................................................................................................................ 5

2.3.2 Bean growing areas ............................................................................................................................................... 6

2.4 BEANS CONSUMPTION IN UGANDA .................................................................................................................................... 6

2.4.1 Domestic market .................................................................................................................................................... 6

2.4.2 International market .............................................................................................................................................. 7

2.5 NUTRITIONAL STANDARDS ................................................................................................................................................ 8

2.6 LIMITATIONS TO BEAN CONSUMPTION ................................................................................................................................ 8

2.6 OPPORTUNITIES IN THE BEANS SUB-SECTOR ......................................................................................................................... 9

2.7 THE POTENTIAL FOR DEHYDRATED PRECOOKED BEANS ........................................................................................................... 9

CHAPTER 3 – RESEARCH METHODOLOGY .......................................................................................................................... 11

Dehydrated Precooked Beans Feasibility Study& Product Test Draft Report Page iii of 94

3.1 STUDY DESIGN ............................................................................................................................................................. 11 3.2 FEASIBILITY STUDY

........................................................................................................................................................ 11

3.2.1 Sampling .............................................................................................................................................................. 12 3.2.1.1 Schools .......................................................................................................................................................................... 12

3.2.1.2 Restaurants .......................................................................................................................................................................... 13 3.2.1.3 Relief Agencies ..................................................................................................................................................................... 13 3.2.1.4 Government Institutions ...................................................................................................................................................... 13

3.2.2 Secondary Data .................................................................................................................................................... 15

3.3 PRODUCT TEST ............................................................................................................................................................. 15

3.3.1 Sampling .............................................................................................................................................................. 16

3.3.2 Product that was tested ....................................................................................................................................... 18

3.3.3 Order of rotation .................................................................................................................................................. 18

3.3.4 Beans Preparation ................................................................................................................................................ 18

3.4 DATA COLLECTION PROCEDURES, METHODS AND INSTRUMENTS .......................................................................................... 18

3.4.1 Tool development ................................................................................................................................................ 18

3.4.2 Pre-testing of instruments ................................................................................................................................... 19

3.4.3 Tool administration .............................................................................................................................................. 20

3.4.4 Recruitment of team ............................................................................................................................................ 21

3.4.5 Training and Orientation ...................................................................................................................................... 21

3.4.6 Data Collection process explained further ........................................................................................................... 23

3.5 DATA PROCESSING, ANALYSIS, MANAGEMENT AND REPORTING ........................................................................................... 23

3.5.1 Data Processing ................................................................................................................................................... 23

3.5.2 Data analysis ........................................................................................................................................................ 23

3.6 QUALITY CONTROL ........................................................................................................................................................ 24

CHAPTER 4 – SURVEY FINDINGS......................................................................................................................................... 25

Dehydrated Precooked Beans Feasibility Study& Product Test Draft Report Page iv of 94

SECTION I: FEASIBILITY STUDY FINDINGS ....................................................................................................................... 25

4.1 SIZE & SCOPE OF INSTITUTIONAL MARKET OF BEANS IN UGANDA .......................................................................................... 25

4.1.1 Beans Purchase .................................................................................................................................................... 25

4.1.2 Pricing of beans .................................................................................................................................................... 28

4.1.3 Quality of beans ................................................................................................................................................... 31

4.1.4 Fuel consumption ................................................................................................................................................. 32

4.1.5 Storage practices ................................................................................................................................................. 35

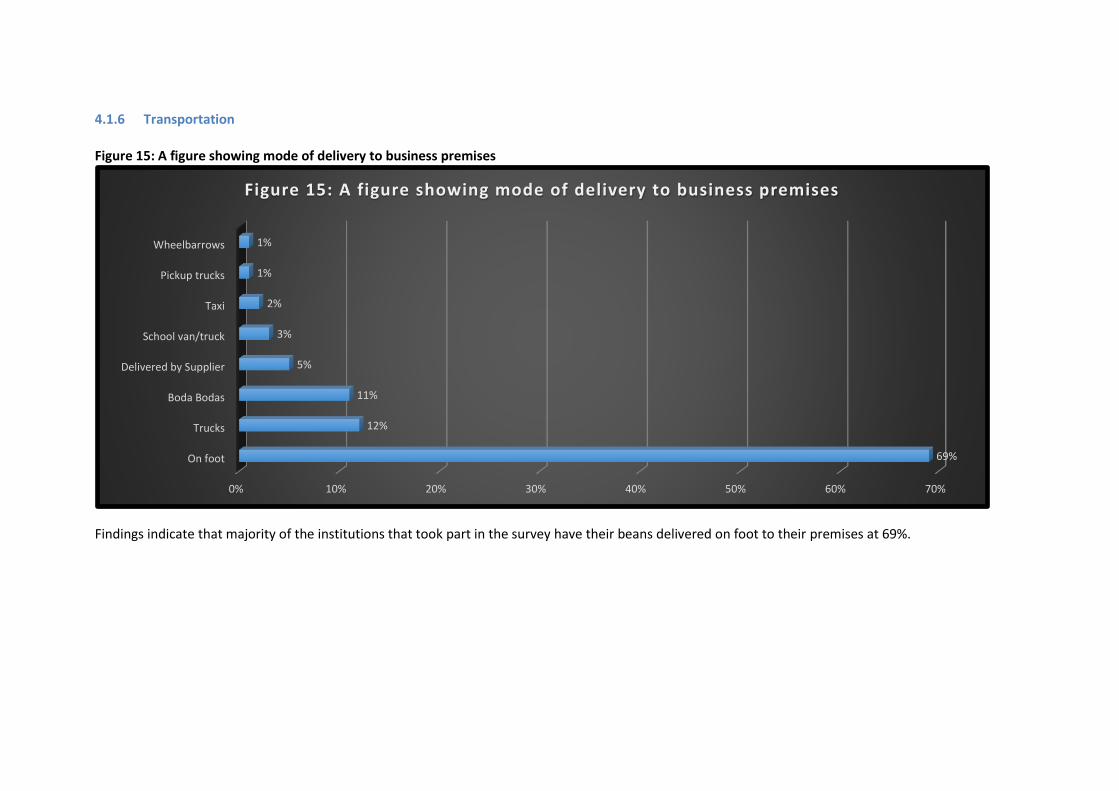

4.1.6 Transportation ..................................................................................................................................................... 35

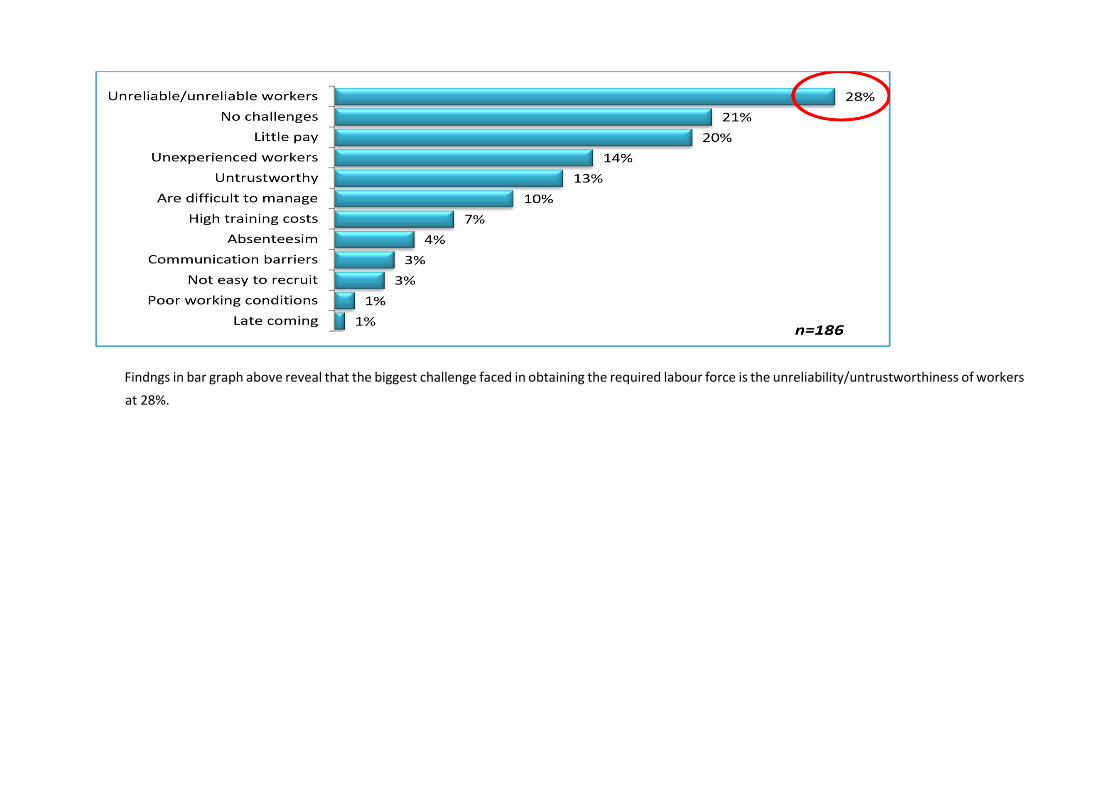

4.1.7 Labour .................................................................................................................................................................. 36

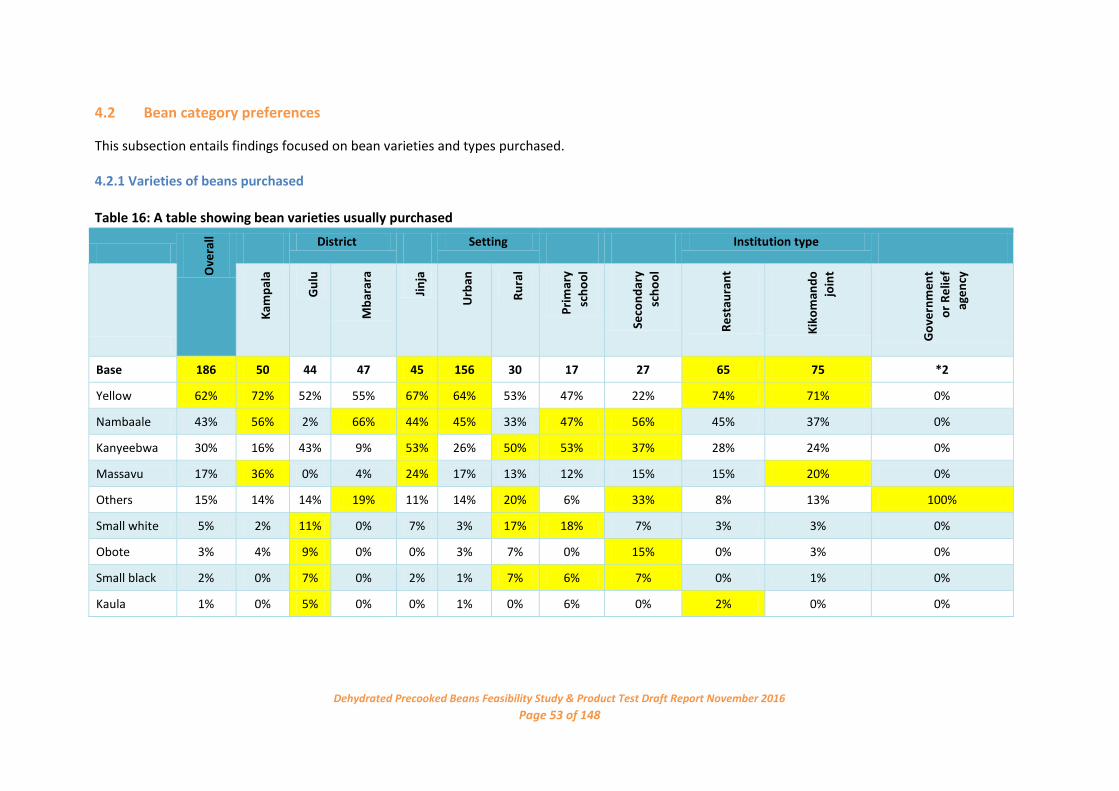

4.2 BEAN CATEGORY PREFERENCES ........................................................................................................................................ 37

4.2.1 Varieties of beans purchased ................................................................................................................................... 37

4.2.2 Type of beans purchased/consumed .................................................................................................................... 39

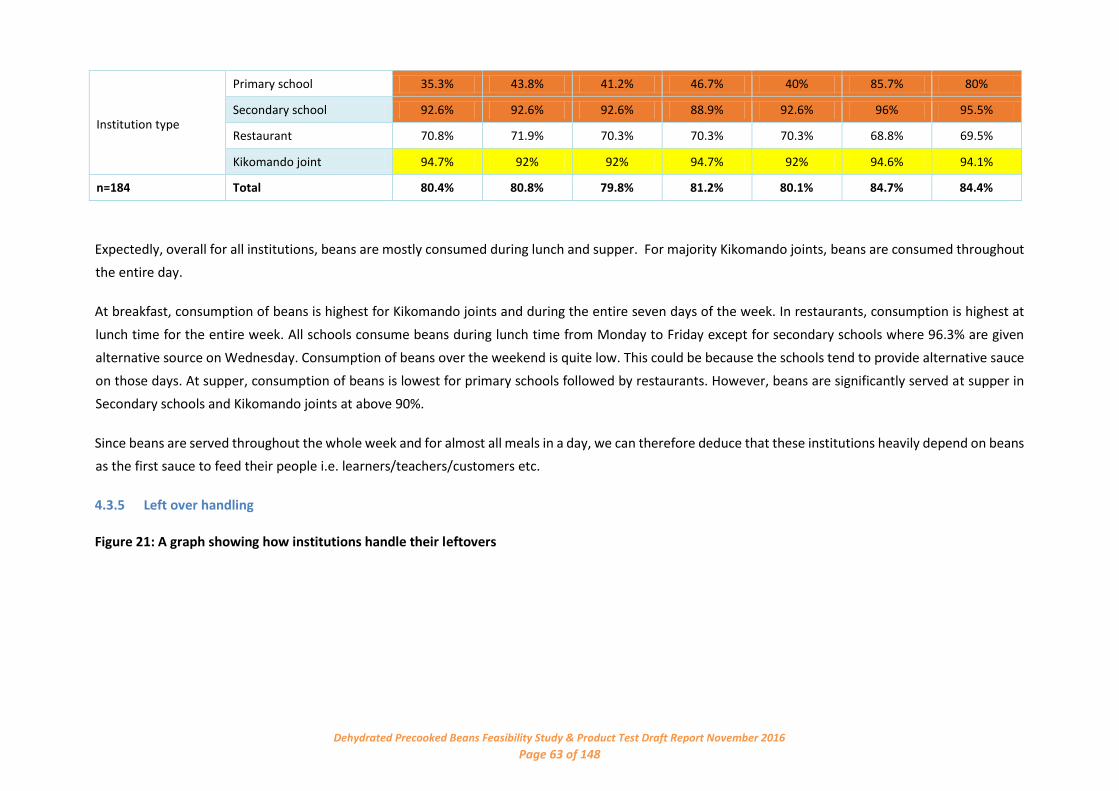

4.3 DATA ON CURRENT BEAN CONSUMPTION AND USAGE .......................................................................................................... 40

4.3.1 Quantities cooked per day ................................................................................................................................... 40

4.3.2 Factors that determine quantity of beans cooked ............................................................................................... 41

4.3.3 Preparation of beans ............................................................................................................................................ 43

4.3.4 Consumption of beans ......................................................................................................................................... 43

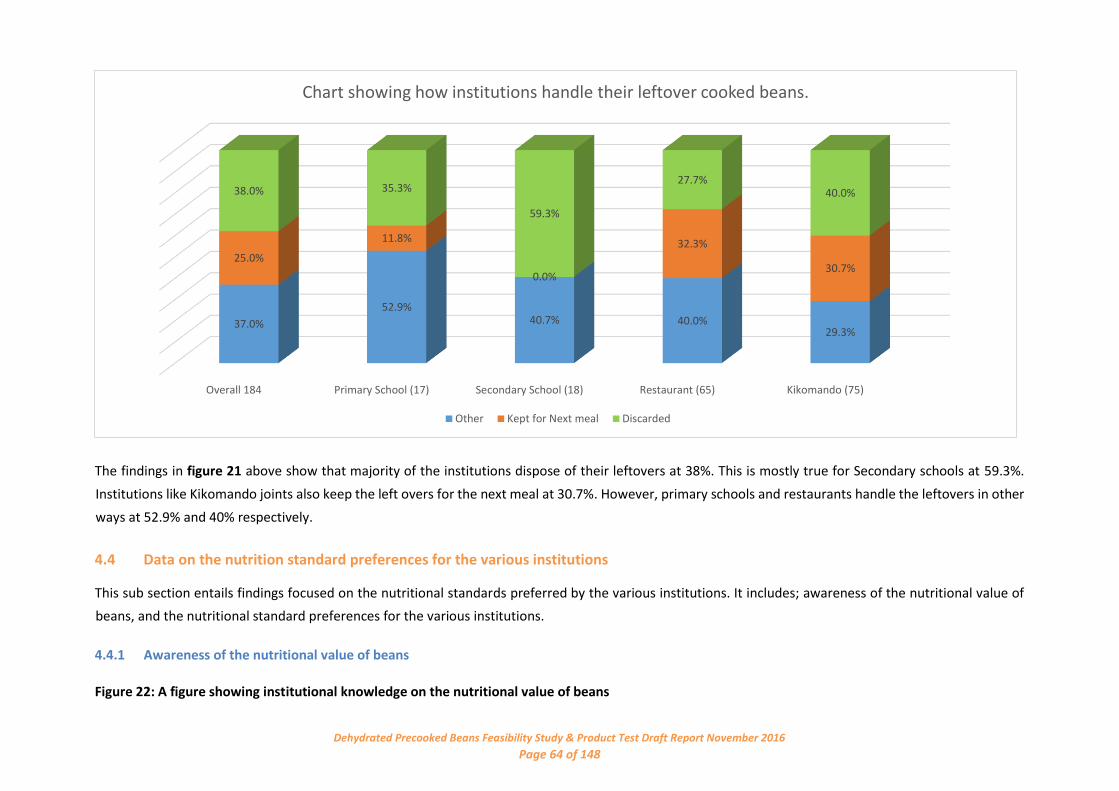

4.3.5 Left over handling ................................................................................................................................................ 44

4.4 DATA ON THE NUTRITION STANDARD PREFERENCES FOR THE VARIOUS INSTITUTIONS................................................................. 45

4.4.1 Awareness of the nutritional value of beans........................................................................................................ 45

4.4.2 Fortified foods ...................................................................................................................................................... 46

4.5 CONSTRAINTS FACED WITH THE CURRENT BEAN PRODUCT .................................................................................................... 47

4.5.1 Problems faced with the current beans ............................................................................................................... 47

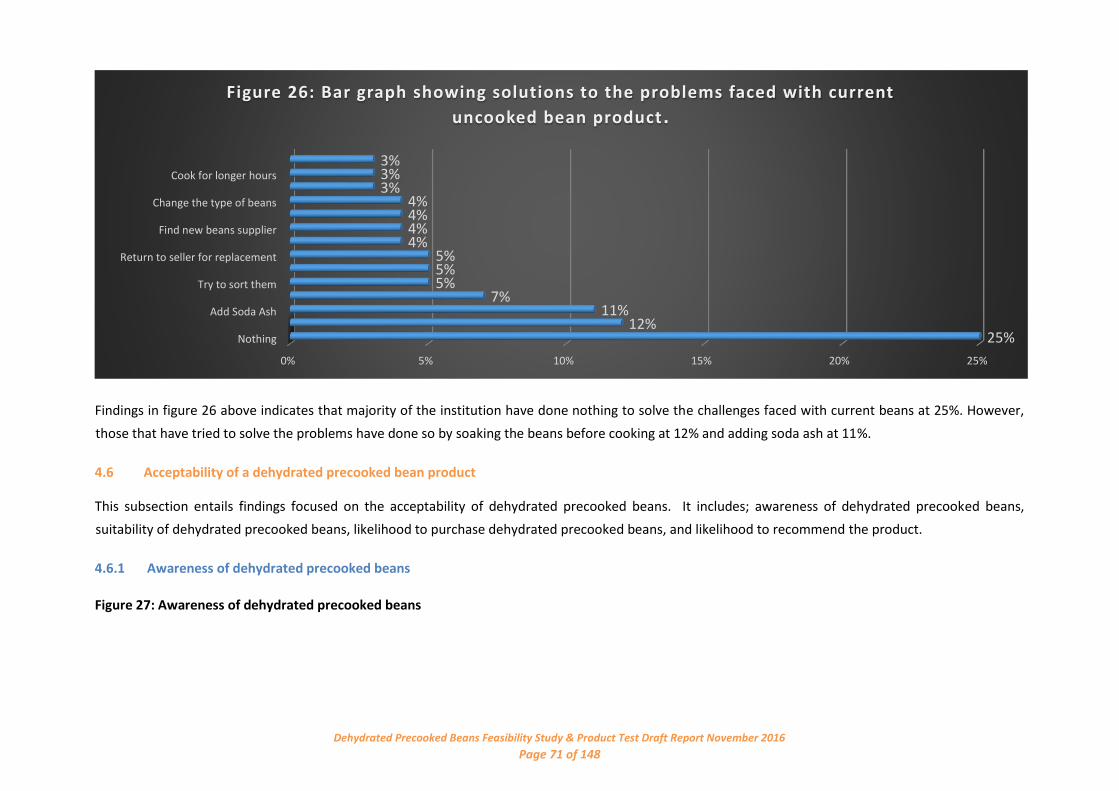

4.5.2 Solutions to the problems faced with the current beans ..................................................................................... 48

4.6 ACCEPTABILITY OF A DEHYDRATED PRECOOKED BEAN PRODUCT ............................................................................................. 49

4.6.1 Awareness of dehydrated precooked beans ....................................................................................................... 49

4.6.1 Suitability of dehydrated precooked beans ......................................................................................................... 49

4.6.2 Likelihood to buy dehydrated precooked beans .................................................................................................. 50

4.6.3 Likelihood to recommend dehydrated precooked beans ..................................................................................... 50

Dehydrated Precooked Beans Feasibility Study& Product Test Draft Report Page v of 94

SECTION II: NEW PRODUCT EVALUATION ................................................................................................................... 51

4.7 SPONTANEOUS THOUGHTS AND PERCEPTIONS ON THE PRODUCT ........................................................................................... 51

4.7.1 Initial thoughts and perceptions on dehydrated precooked beans ...................................................................... 51

4.7.2 Appearance of the beans before preparation ...................................................................................................... 51

4.7.3 Smell of the beans before preparation................................................................................................................. 53

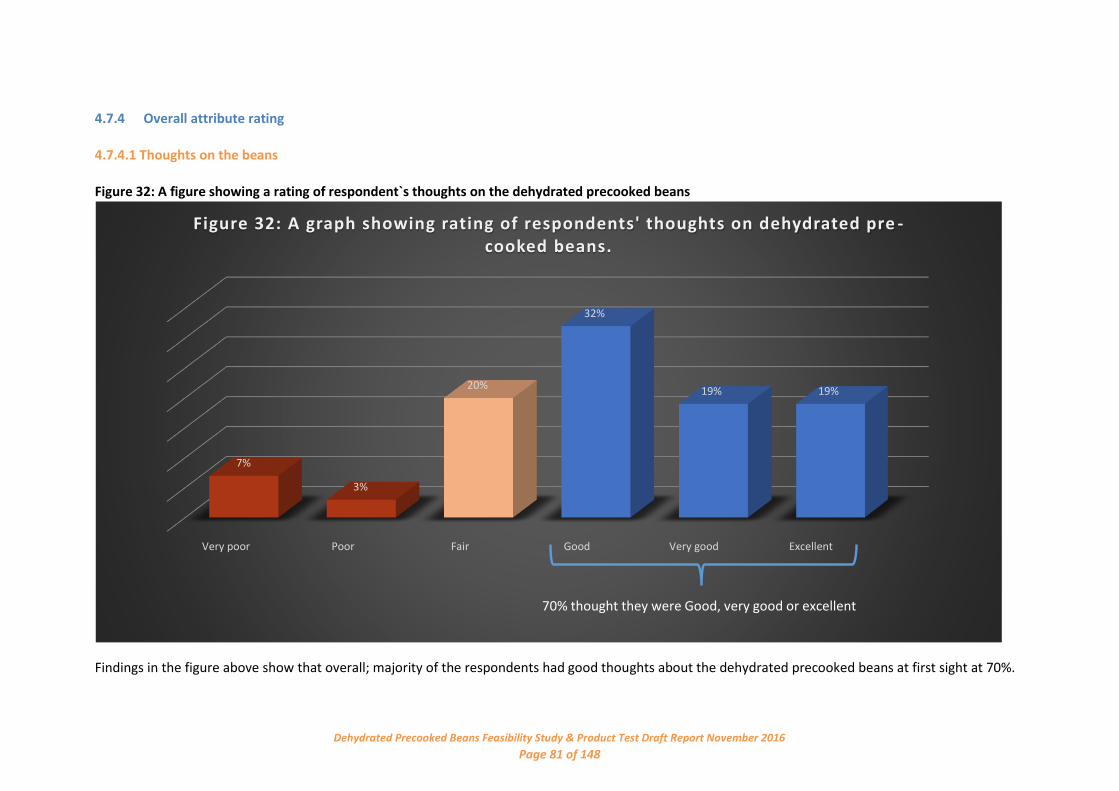

4.7.4 Overall attribute rating ........................................................................................................................................ 54 4.7.4.1 Thoughts on the beans ................................................................................................................................................. 54 4.7.4.2 Likeness on the beans ................................................................................................................................................... 55

4.7.5 Individual attribute rating .................................................................................................................................... 56 4.7.5.1 Appearance of the beans after preparation ................................................................................................................. 59 4.7.5.2 Reasons for rating of appearance of the beans after preparation ................................................................................ 60 4.7.5.3 Taste of the beans after preparation ............................................................................................................................ 61 4.7.5.4 Reasons for rating of tastiness of the beans after preparation .................................................................................... 62 4.7.5.5 Color of the beans after preparation .......................................................................................................................... 62 4.7.5.6 Reasons for rating of color of the beans after preparation ........................................................................................ 63 4.7.5.7 Aroma of the beans after preparation .......................................................................................................................... 64 4.7.5.8 Reasons for rating of aroma of the beans after preparation ........................................................................................ 64 4.7.5.9 Texture/mouth feel of the beans after preparation ..................................................................................................... 65 4.7.5.10 Reasons for rating of texture of the beans after preparation ....................................................................................... 65 4.7.5.11 Quality of the dehydrated precooked beans ................................................................................................................ 66 4.7.5.12 Comparison of dehydrated precooked beans with current beans ............................................................................... 66 4.8 LIKES, DISLIKES AND SUGGESTIONS FOR IMPROVEMENT ON THE DEHYDRATED PRECOOKED BEANS ............................................... 68

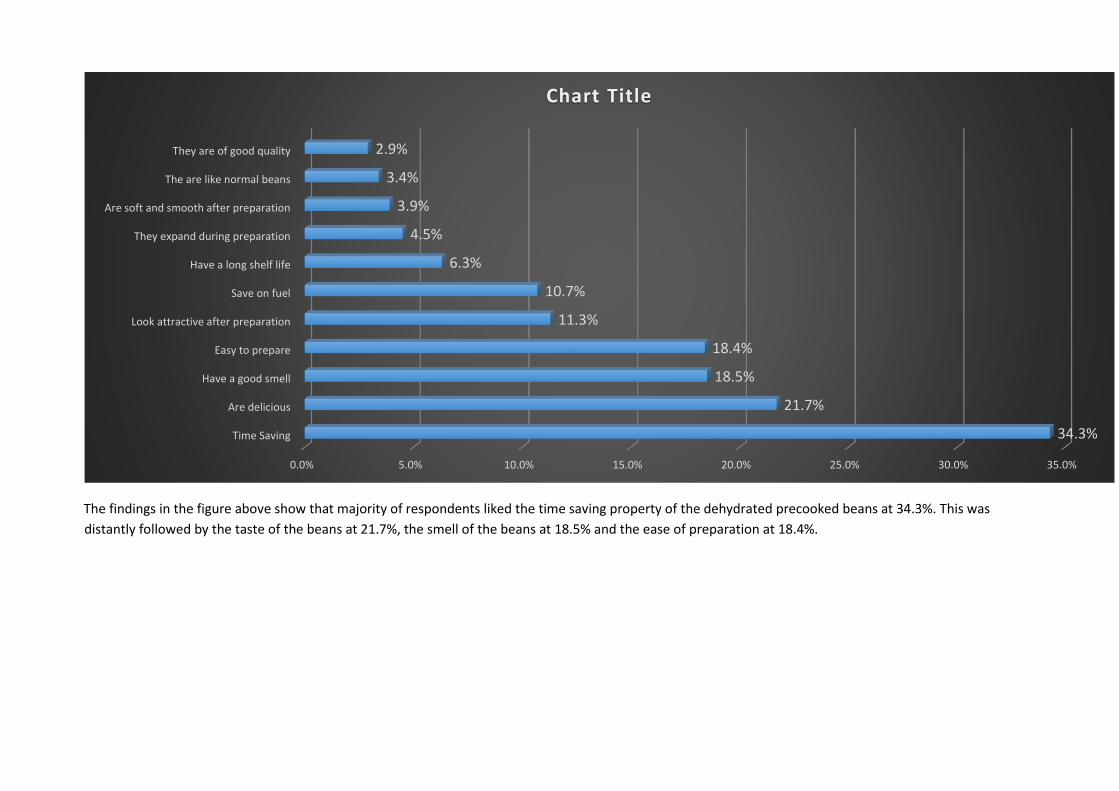

4.8.1 Likes for dehydrated precooked beans................................................................................................................. 68

4.8.2 Dislikes for dehydrated precooked beans ............................................................................................................ 68

3.9.3 Suggestions for improvement for dehydrated precooked beans ......................................................................... 69

4.9 LIKELIHOOD TO PURCHASE/CONSUME DEHYDRATED PRECOOKED BEANS ................................................................................ 70

Dehydrated Precooked Beans Feasibility Study& Product Test Draft Report Page vi of 94

4.9.1 The need for dehydrated precooked beans ......................................................................................................... 70

4.9.2 Purchase/consumption intent ............................................................................................................................. 71

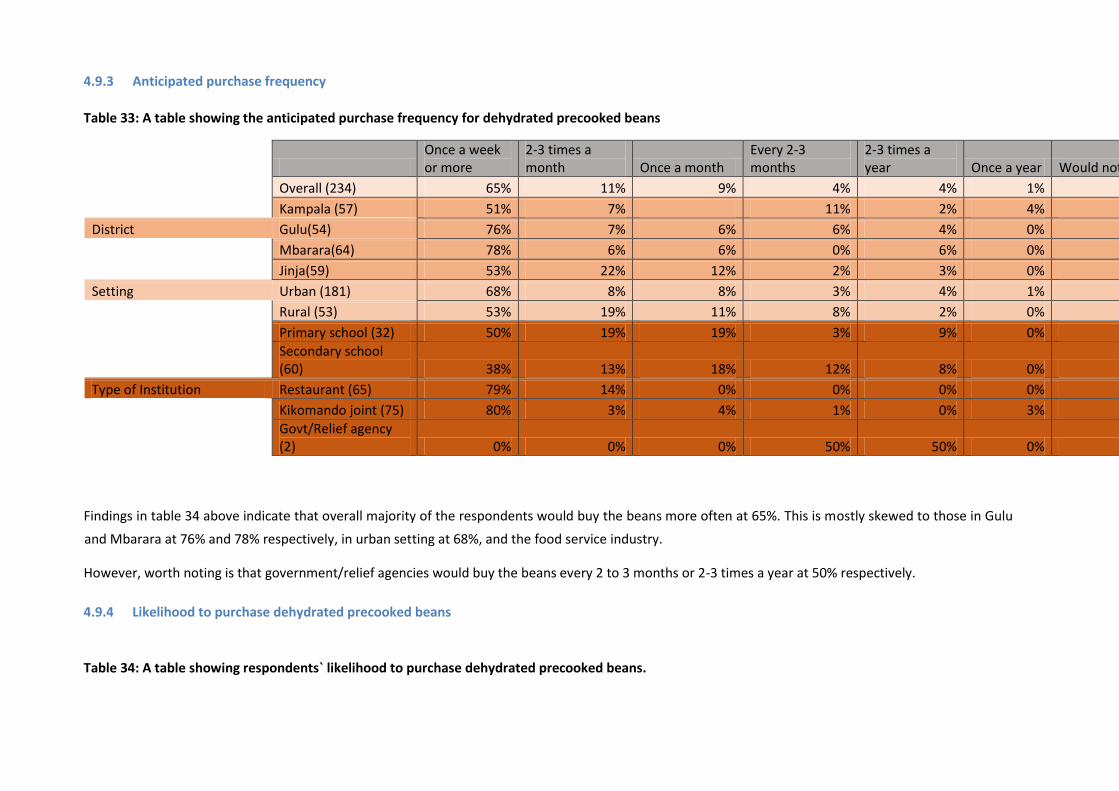

4.9.3 Anticipated purchase frequency .......................................................................................................................... 72

4.9.4 Likelihood to purchase dehydrated precooked beans .......................................................................................... 72

4.9. 5 Quantities of the dehydrated precooked beans likely to buy .......................................................................... 73

4.9.6 Price willing to pay for a kilo gram of the dehydrated precooked beans ............................................................. 73

4.10 LIKELIHOOD TO RECOMMEND DEHYDRATED PRECOOKED BEANS ............................................................................................ 74

4.10.1 Likelihood to recommend dehydrated precooked beans to other institutions ................................................ 74

CHAPTER 5: RECOMMENDATIONS AND CONCLUSIONS ..................................................................................................... 75

5.1 RECOMMENDATIONS ..................................................................................................................................................... 75

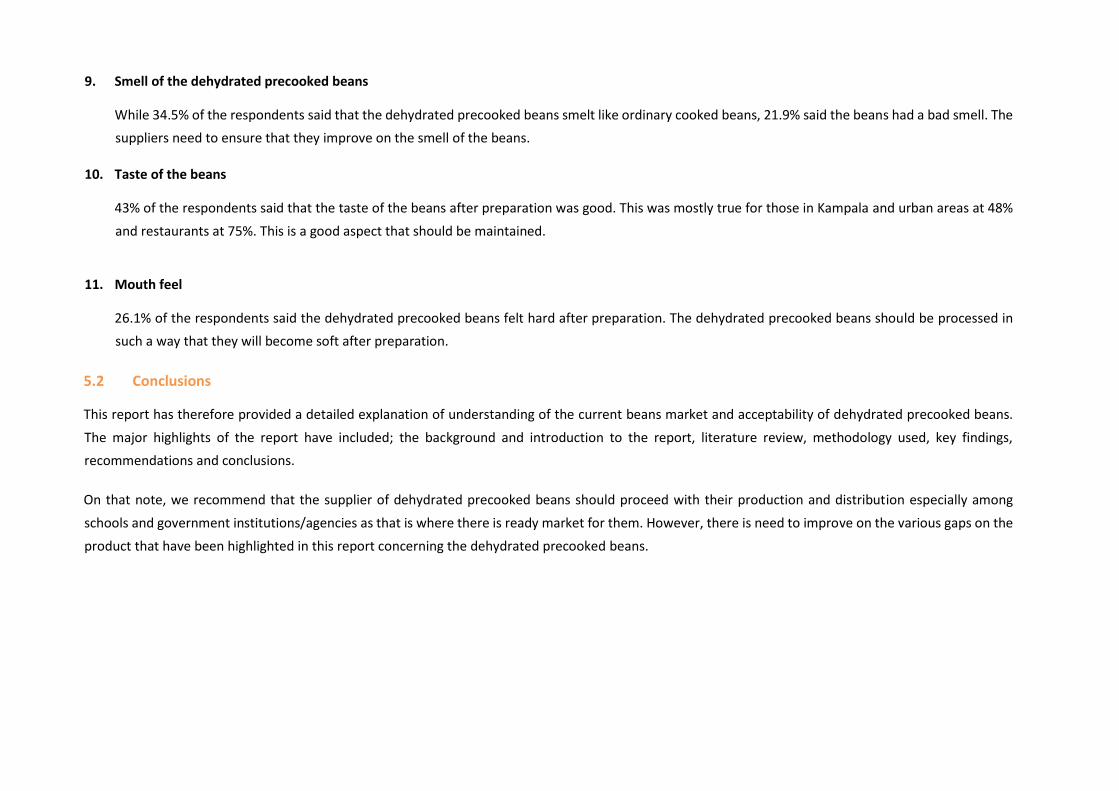

5.2 CONCLUSIONS .............................................................................................................................................................. 77

APPENDICES ...................................................................................................................................................................... 78

APPENDIX 1: LIST OF CURRENT BEAN TYPES IN UGANDA ................................................................................................................... 79 APPENDIX 2: LIST OF INSTITUTIONS THAT PARTICIPATED IN THE

STUDY ................................................................................................ 80

LIST OF TABLES

Table 1: Bean production per hectare 2004/2008 .....................................................................................................5 Table 2: Area of production of beans per region

2008/2009 .....................................................................................6 Table 3: Table showing the targeted sample vis-a-vis achieved sample per district

............................................. 14 Table 4: Table showing the targeted sample size for product test ......................................................................... 17 Table 5: Table

showing the achieved sample size for product test ...................................................................... 17 Table 6: Place of beans purchase

............................................................................................................................ 26 Table 7: Frequency of beans purchase

Dehydrated Precooked Beans Feasibility Study& Product Test Draft Report Page vii of 94

................................................................................................................... 26 Table 8: Quantities of beans purchased per time

................................................................................................... 27 Table 9: Packaging size

............................................................................................................................................ 27 Table 10: Pricing of 1kg of beans

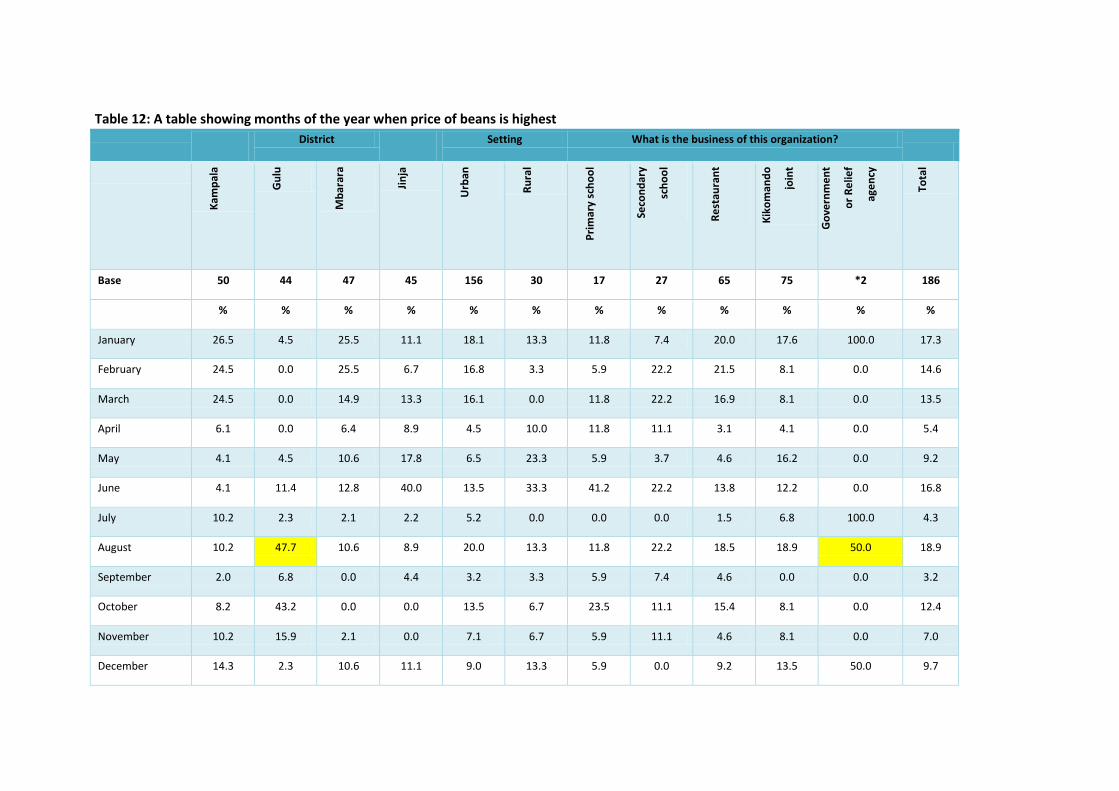

............................................................................................................................. 28 Table 11: A table showing months of the year when price of beans is lowest

....................................................... 30

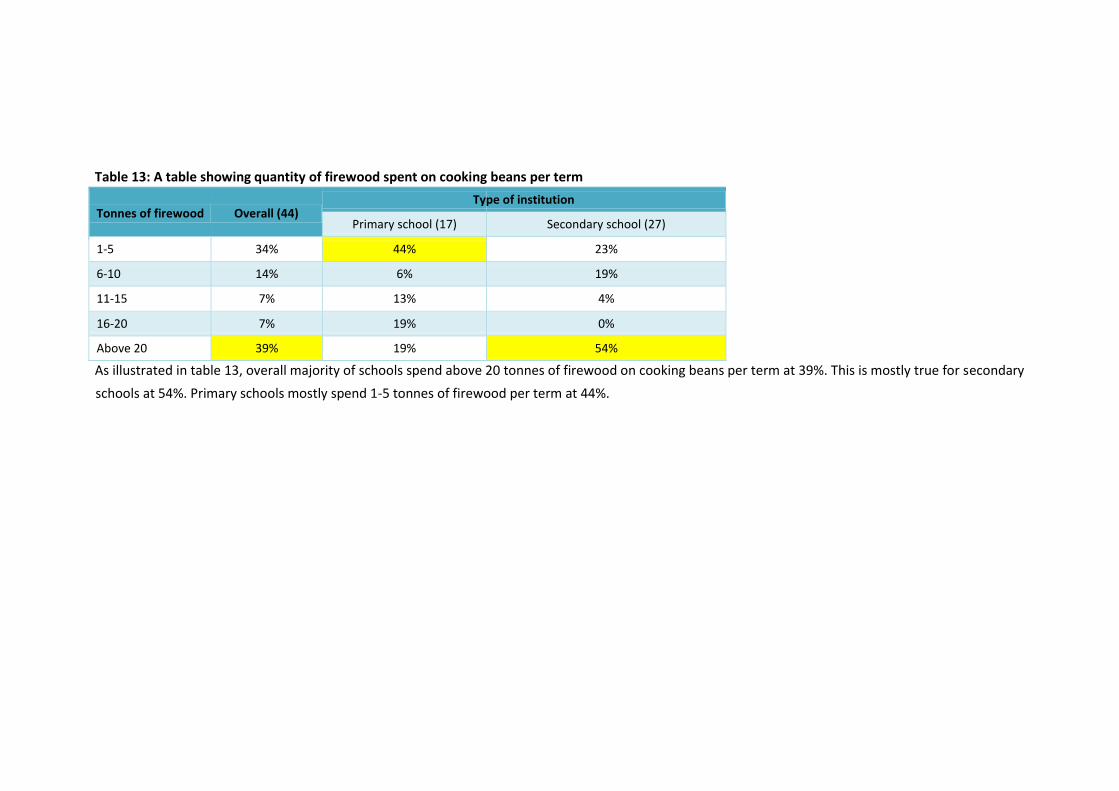

Table 12: A table showing months of the year when price of beans is highest ...................................................... 30 Table 13: A table showing quantity of firewood

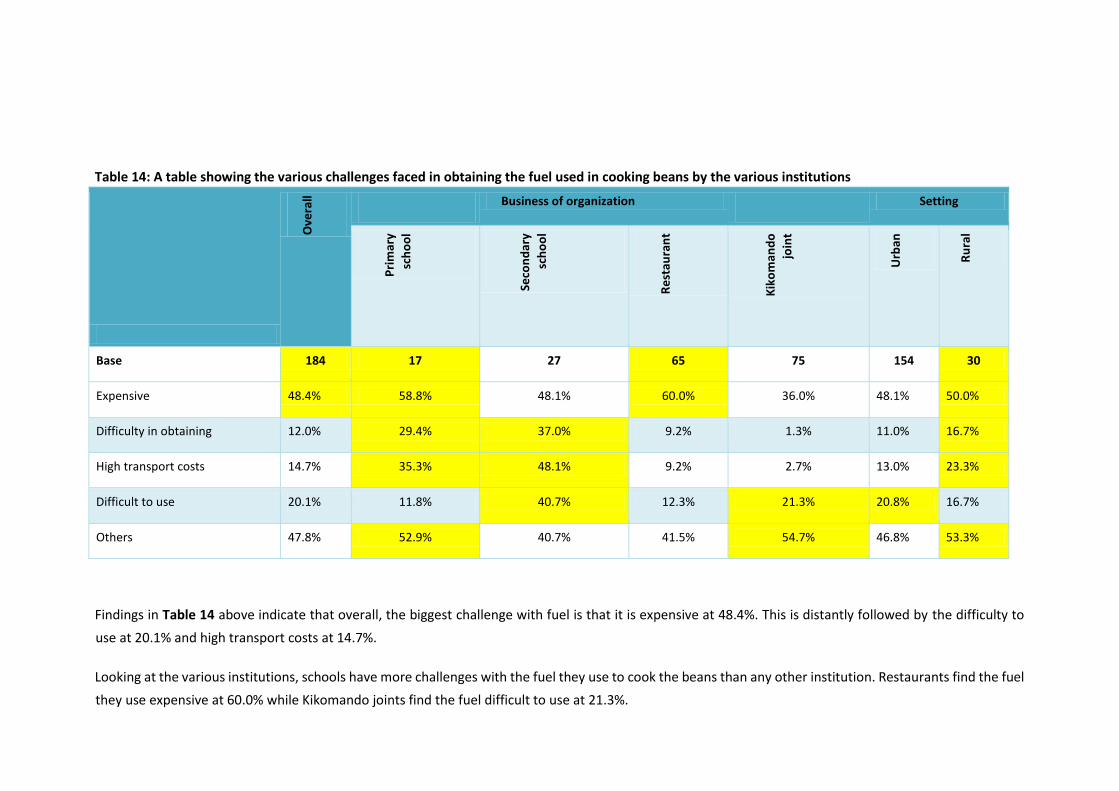

spent on cooking beans per term ............................................... 33 Table 14: A table showing the various challenges faced in obtaining the fuel used in cooking beans

by the various institutions ............................................................................................................................................................... 33

Table 15: A table showing the delivery of beans and who meets the cost of delivery ........................................... 36 Table 16: A table showing bean varieties usually

purchased .................................................................................. 37 Table 17: A table showing preferred bean varieties

............................................................................................... 38 Table 18: A table showing quantities of beans cooked per day by the various institutions

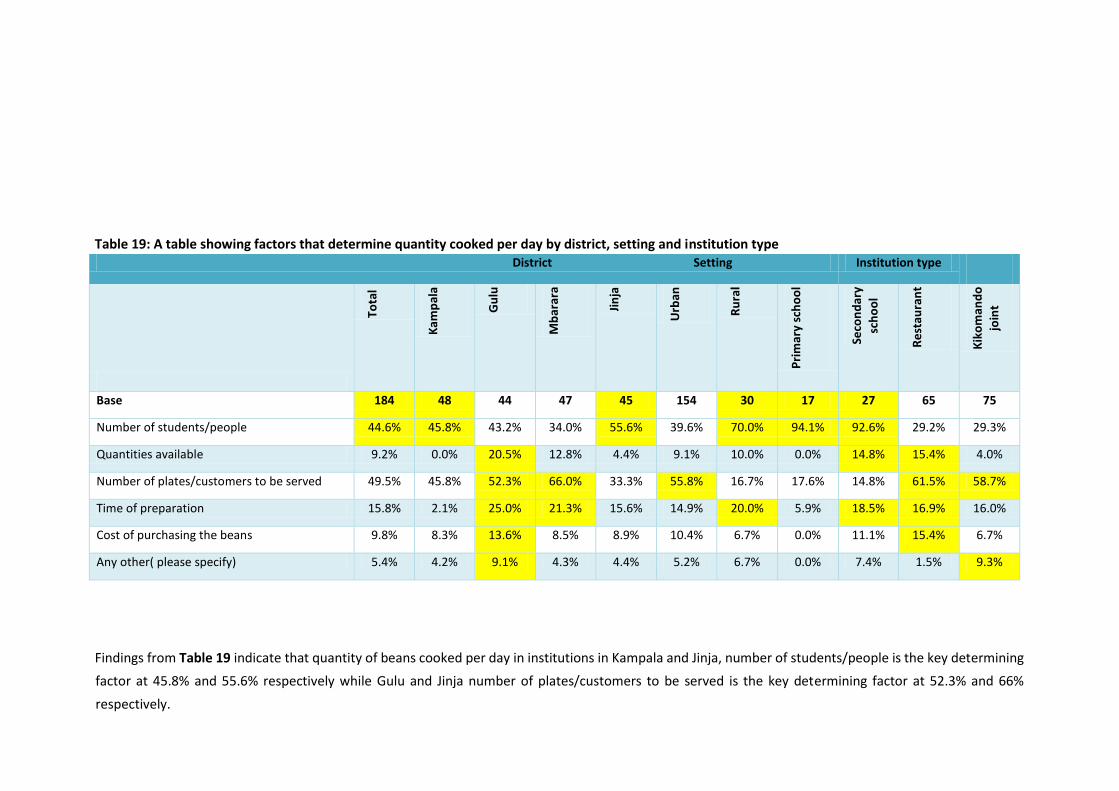

................................... 40 Table 19: A table showing factors that determine quantity cooked per day by district, setting and institution type

................................................................................................................................................................................. 42

Table 20: A table showing days and meals when beans are consumed ................................................................. 43

Table 21: A table showing problems institutions face with their current beans .................................................... 47 Table 22: A table showing the suitability of

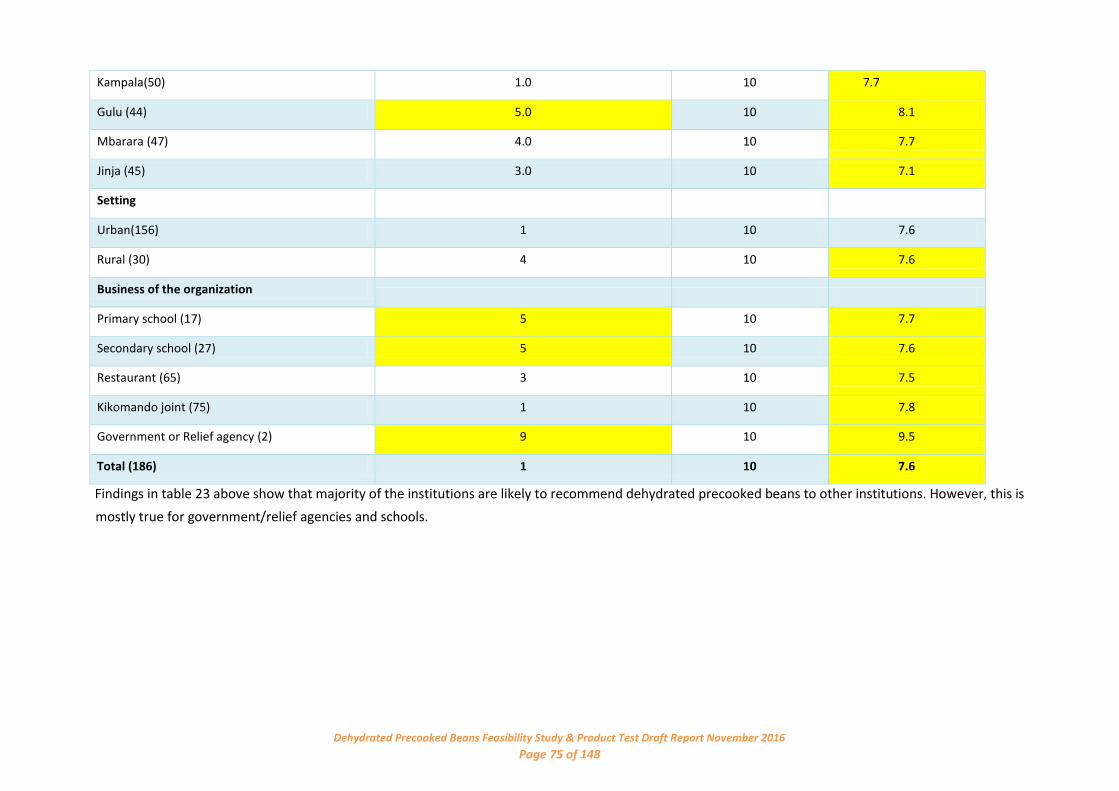

dehydrated precooked beans ............................................................ 49 Table 23: A table showing institutions` likelihood to recommend dehydrated precooked

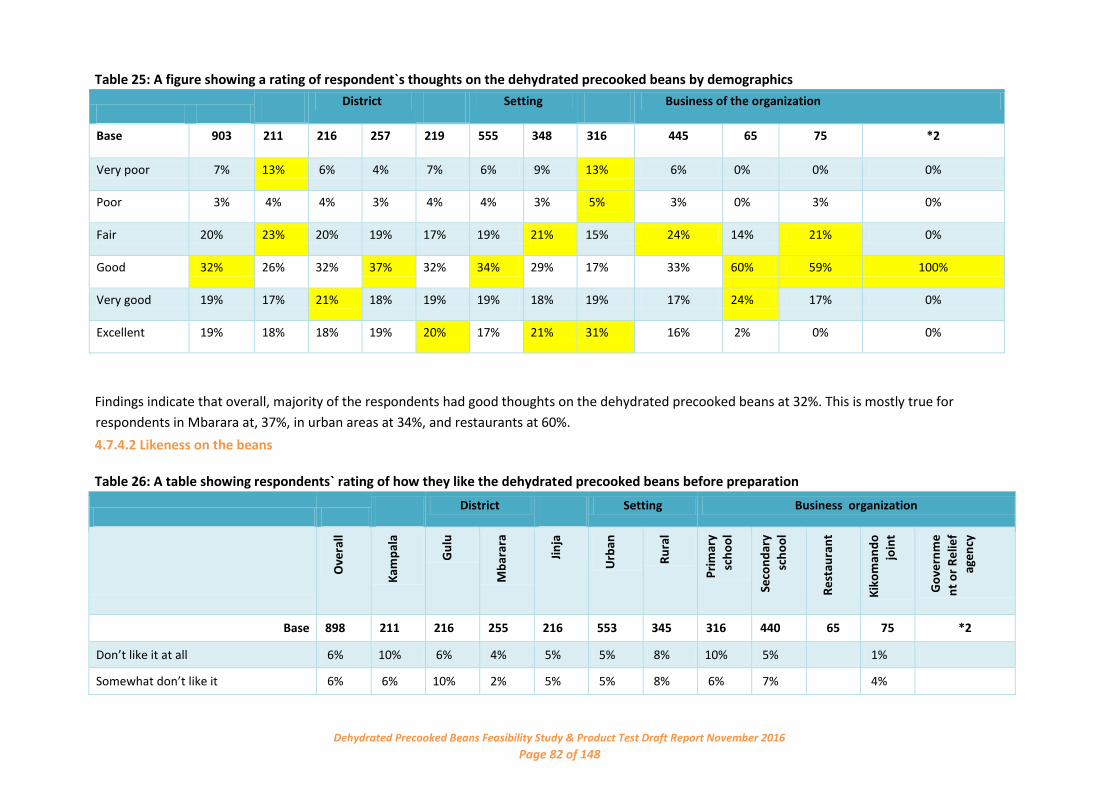

beans ......................... 50 Table 24 showing respondents` feedback on the appearance of the dehydrated precooked beans .................... 53 Table 25: A figure

showing a rating of respondent`s thoughts on the dehydrated precooked beans by

demographics .......................................................................................................................................................... 54

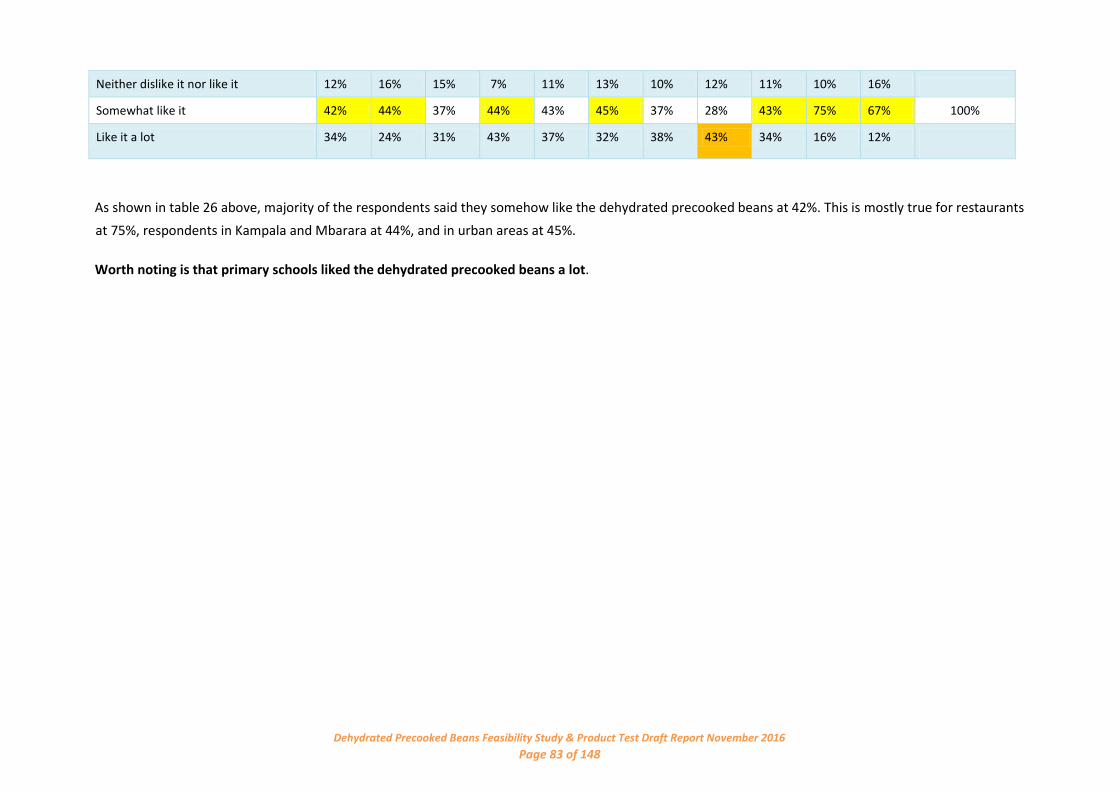

Table 26: A table showing respondents` rating of how they like the dehydrated precooked beans before

preparation .............................................................................................................................................................. 55

Dehydrated Precooked Beans Feasibility Study& Product Test Draft Report Page viii of 94

Table 27 showing the summary of respondents` feedback during the product test .............................................. 56 Table 28: A table showing respondents` rating of

the appearance of the like the dehydrated precooked beans

before after preparation ......................................................................................................................................... 60

Table 29: A figure showing respondents` feedback on the taste of the beans after preparation across

demographics .......................................................................................................................................................... 61

Table 30: A table showing respondents` feedback on the color taste of the beans after preparation across

demographics .......................................................................................................................................................... 63

Table 31: A table showing respondents rating of the aroma of the beans after preparation ................................ 64 Table 32: A table showing respondents rating on

the quality of the dehydrated precooked beans ..................... 66

Table 33: A table showing the anticipated purchase frequency for dehydrated precooked beans ....................... 72 Table 34: A table showing respondents` likelihood

to purchase dehydrated precooked beans. ........................... 72 Table 35: A table showing quantities of dehydrated precooked beans respondents are likely to buy

.................. 73 Table 36: A table showing respondents` likelihood to recommend dehydrated precooked beans to others ....... 74

Dehydrated Precooked Beans Feasibility Study& Product Test Draft Report Page ix of 94

LIST OF FIGURES

Figure 1: Picture showing the pre-testing process of preparing the dehydrated precooked beans ...................... 19 Figure 2: Picture showing the tool being administered

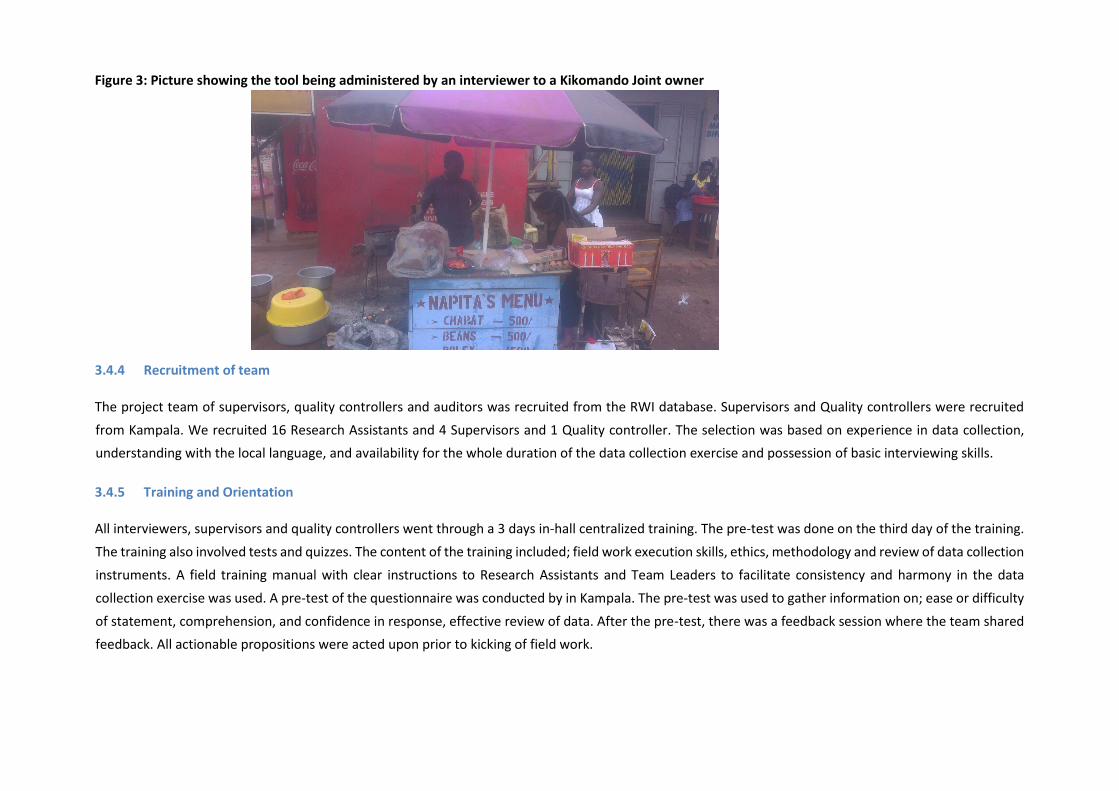

by an interviewer to the learners .................................... 20 Figure 3: Picture showing the tool being administered by an interviewer to a Kikomando Joint owner

............... 21

Figure 4: Picture showing training of the field teams ............................................................................................. 22

Figure 5: Picture showing training of the field teams ............................................................................................. 22 Figure 6: A figure showing proportion of institutions

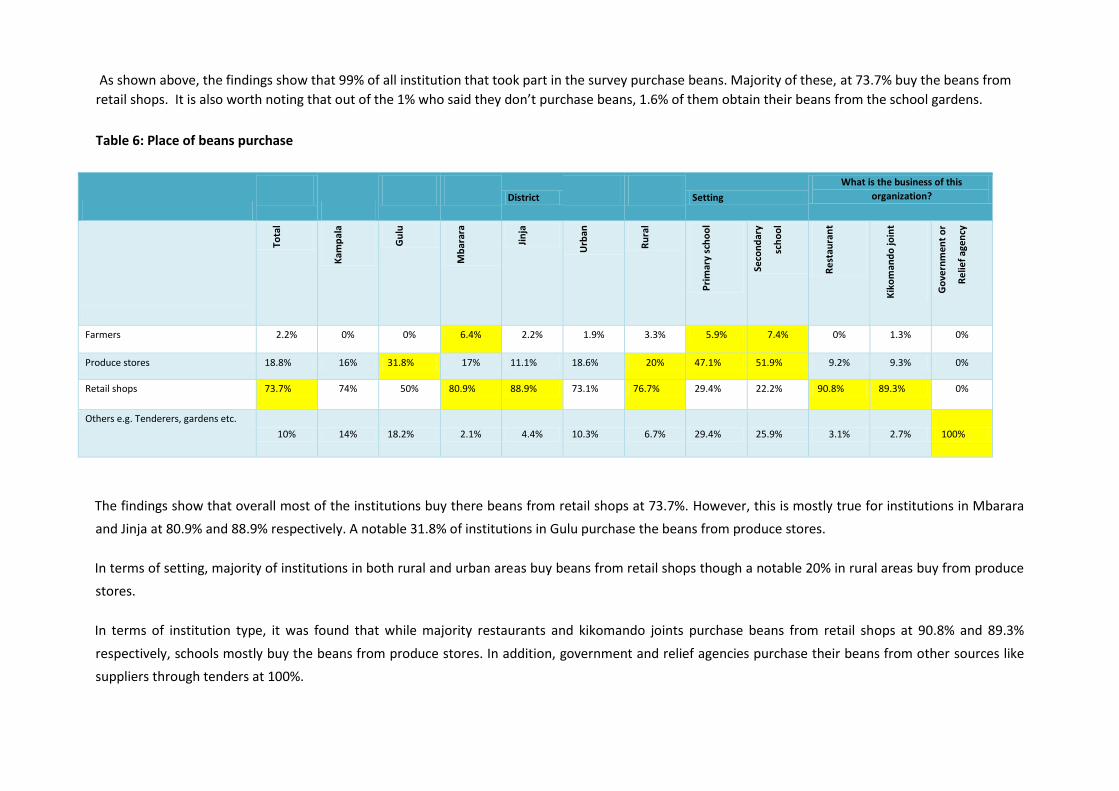

that purchase beans and place of purchase ....................... 25

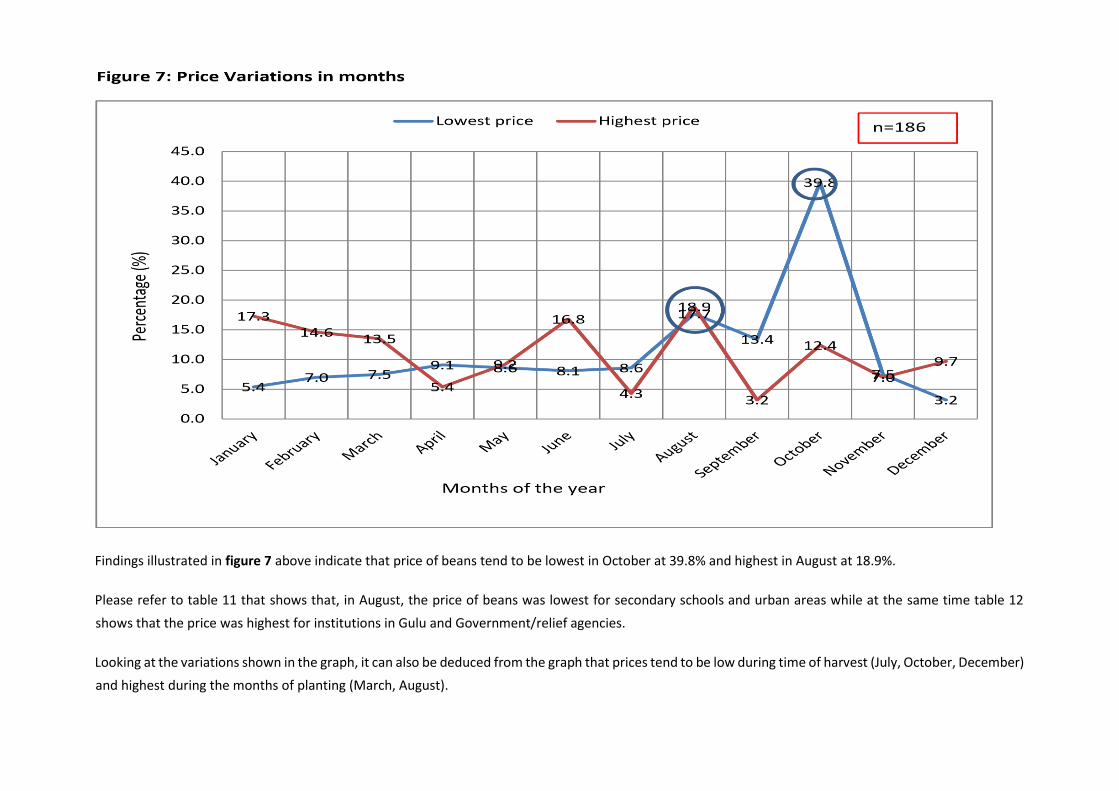

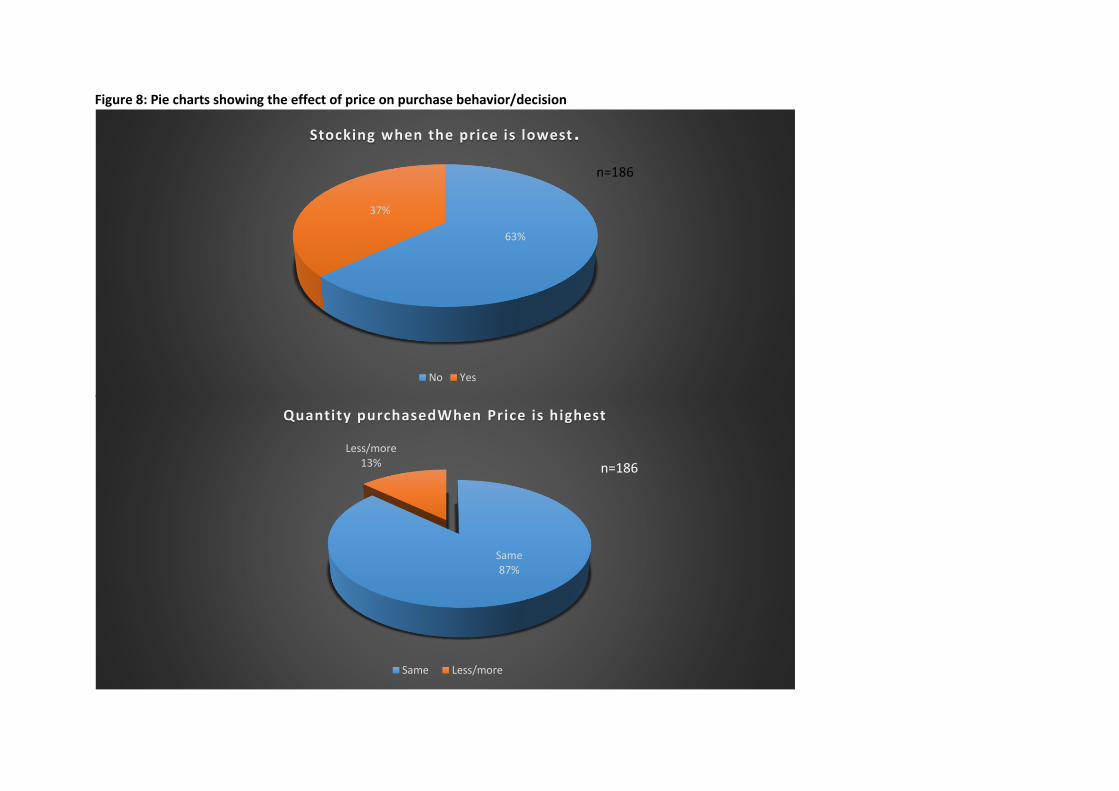

Figure 7: Price Variations in months ....................................................................................................................... 29 Figure 8: Pie charts showing the effect of price on

purchase behavior/decision ................................................... 31 Figure 9: A graph showing respondents thoughts on quality of beans purchased

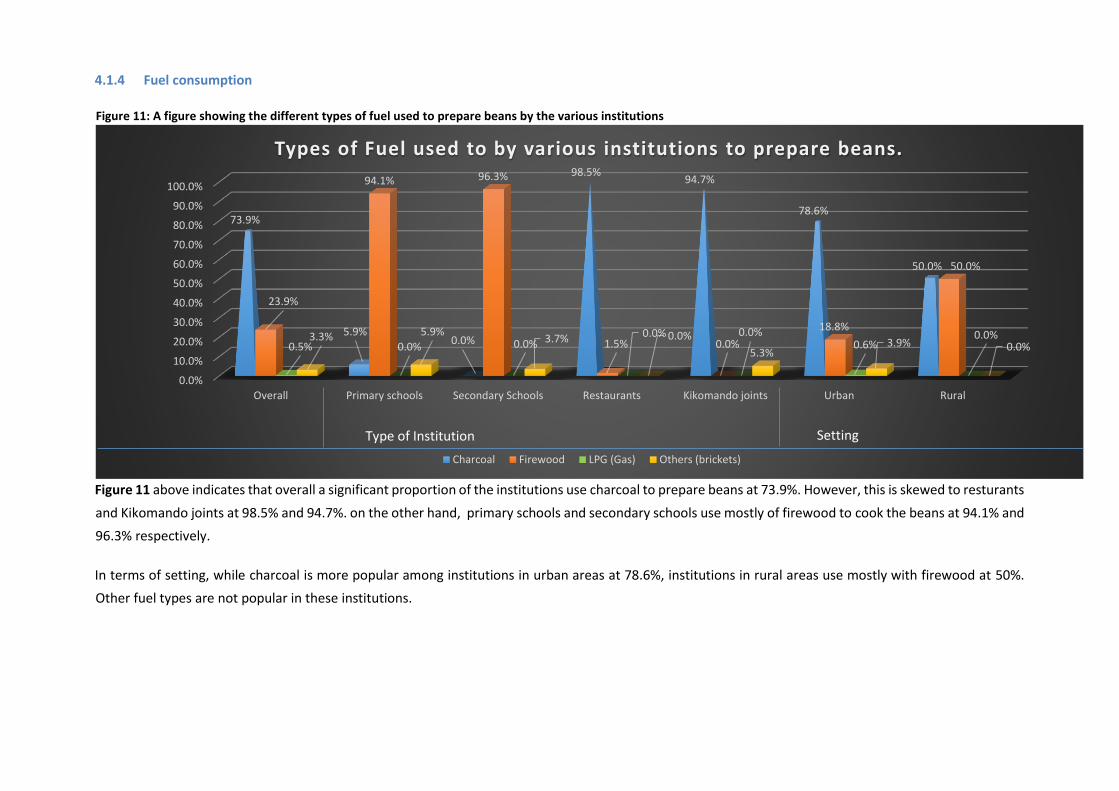

................................................. 31 Figure 10: A graph showing feedback on the quality of beans the various institutions purchase ......................... 32 Figure 11: A

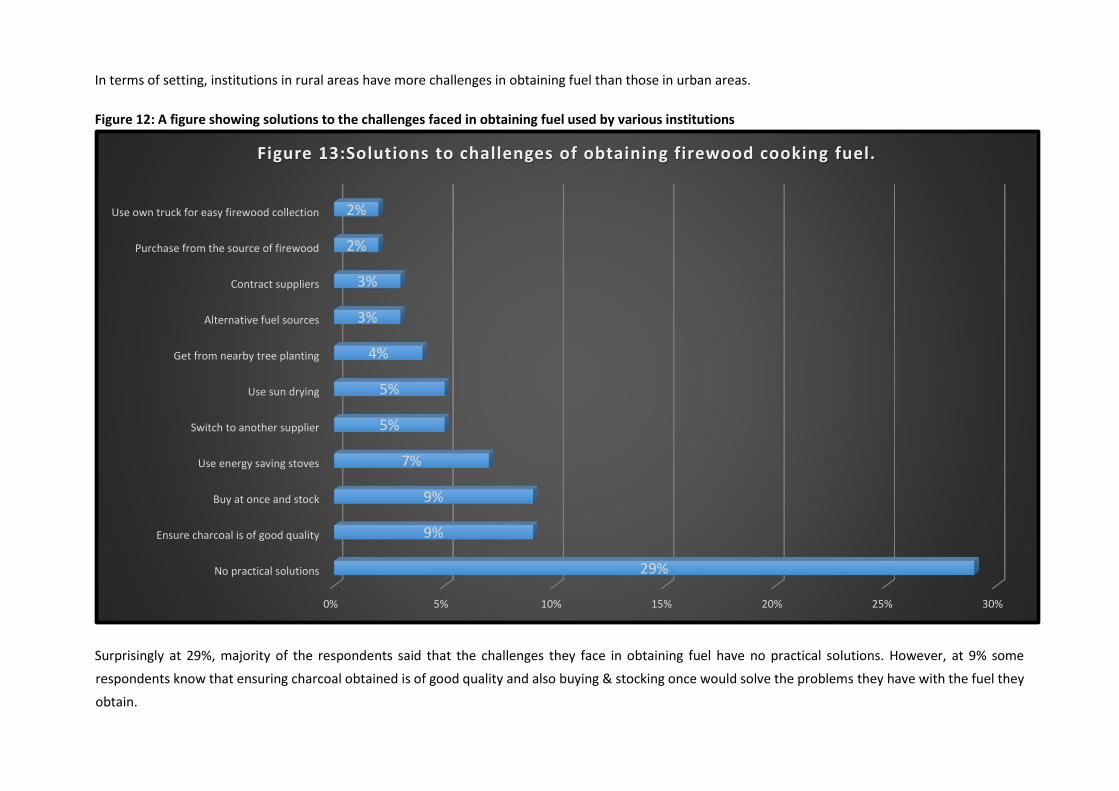

figure showing the different types of fuel used to prepare beans by the various institutions .......... 32 Figure 12: A figure showing solutions to the challenges faced in

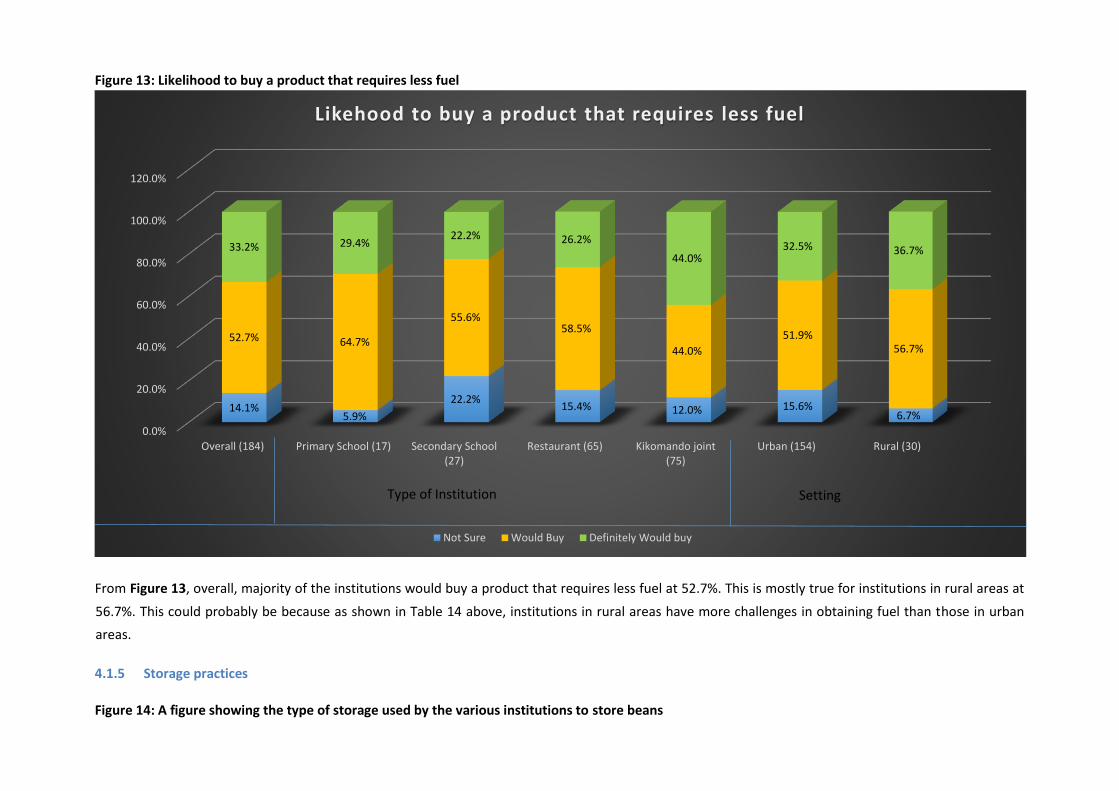

obtaining fuel used by various institutions ...... 34 Figure 13: Likelihood to buy a product that requires less fuel ................................................................................ 34

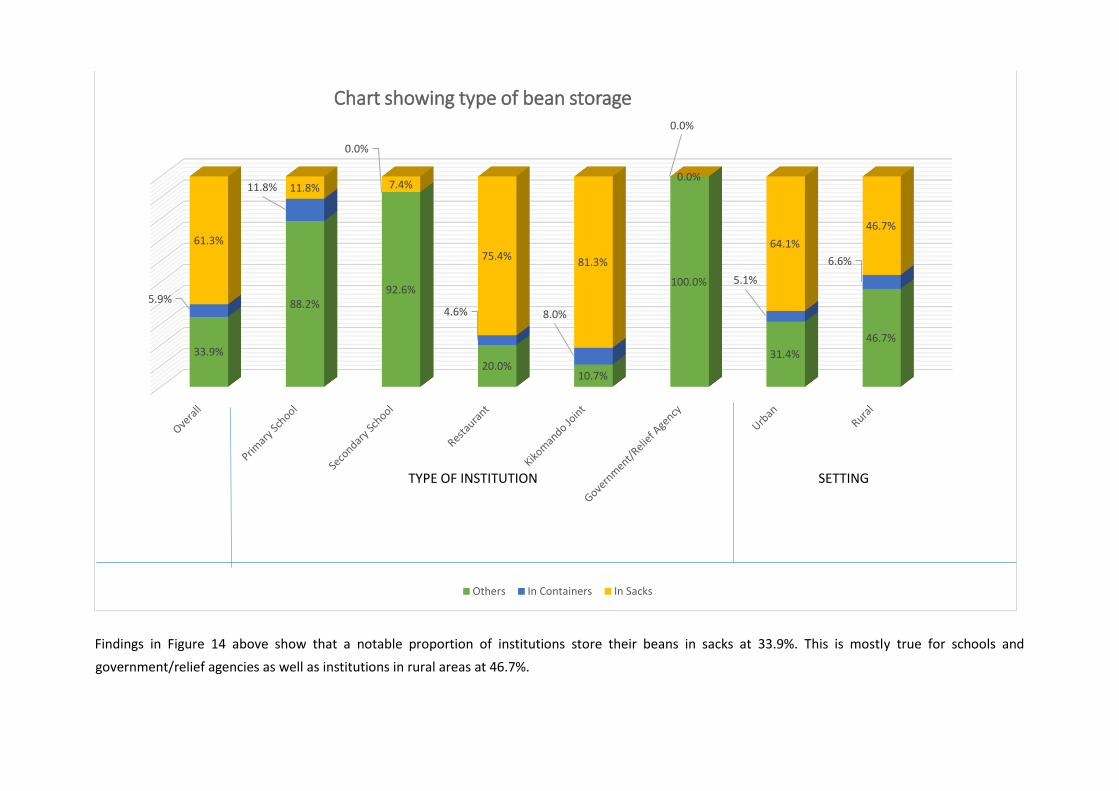

Figure 14: A figure showing the type of storage used by the various institutions to store beans ......................... 35 Figure 15: A figure showing mode of delivery to

business premises ...................................................................... 35 Figure 16: A figure showing challenges faced in obtaining the required labour force

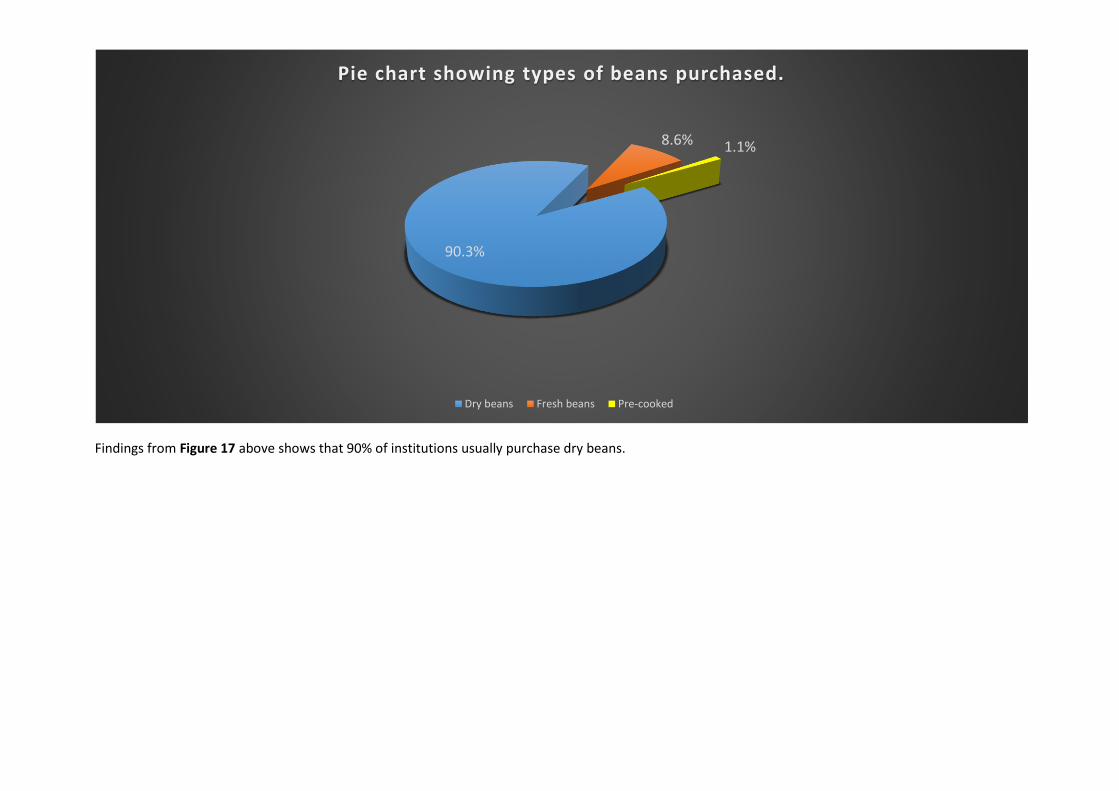

........................................... 36 Figure 17: A graph showing types of beans purchased ........................................................................................... 39 Figure 18: Reasons

for bean type preference ......................................................................................................... 40 Figure 19: A bar graph showing factors that determine the quantity of

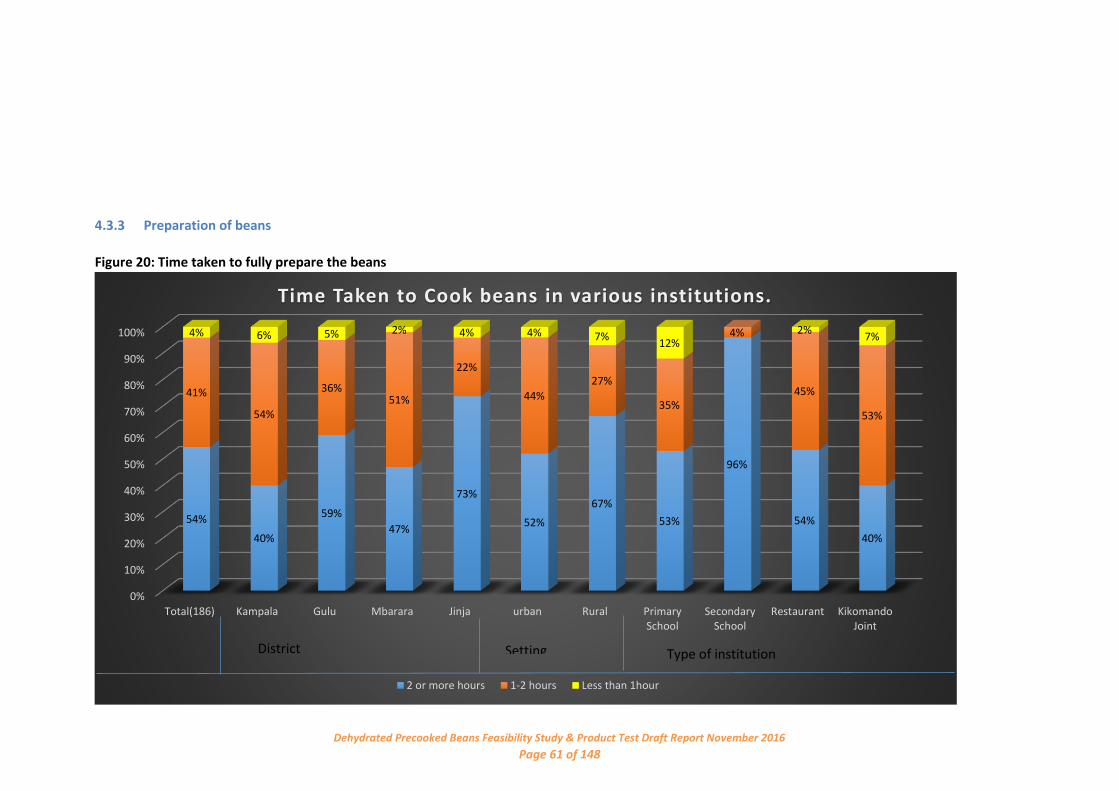

beans cooked per day ............................ 41 Figure 20: Time taken to fully prepare the beans ................................................................................................... 43 Figure

21: A graph showing how institutions handle their leftovers ...................................................................... 44 Figure 22: A figure showing institutional knowledge on

the nutritional value of beans ........................................ 45 Figure 23: A graph showing knowledge of and likelihood to purchased fortified foods

........................................ 46 Figure 24: A graph showing purchase consideration for fortified foods by institution and setting ....................... 46 Figure 25: A figure

showing responsiveness to the various problems faced with the beans by the institutions ... 48 Figure 26: A bar graph showing solutions to the problems faced with

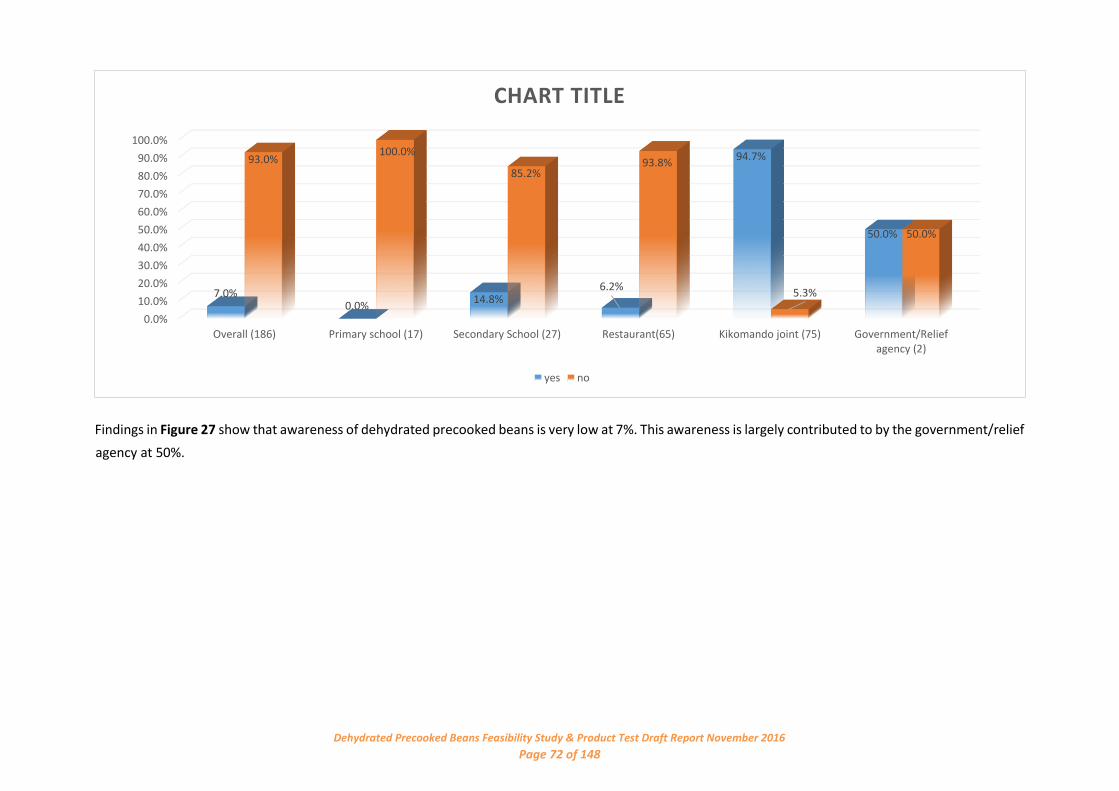

current beans ........................................... 48 Figure 27: Awareness of dehydrated precooked beans .......................................................................................... 49

Dehydrated Precooked Beans Feasibility Study& Product Test Draft Report Page x of 94

Figure 28: A graph showing likelihood to buy a bean product that has a long shelf life, free of pests…. .............. 50 Figure 29: A figure showing respondents` initial

thoughts and perceptions on dehydrated precooked beans ..... 51 Figure 30: A figure showing respondents` feedback on the appearance of the dehydrated

precooked beans

before preparation .................................................................................................................................................. 51

Figure 31: A figure showing respondents` feedback on the smell of the dehydrated precooked beans before

preparation .............................................................................................................................................................. 53

Figure 32: A figure showing a rating of respondent`s thoughts on the dehydrated precooked beans .................. 54 Figure 33: A bar graph showing respondents`

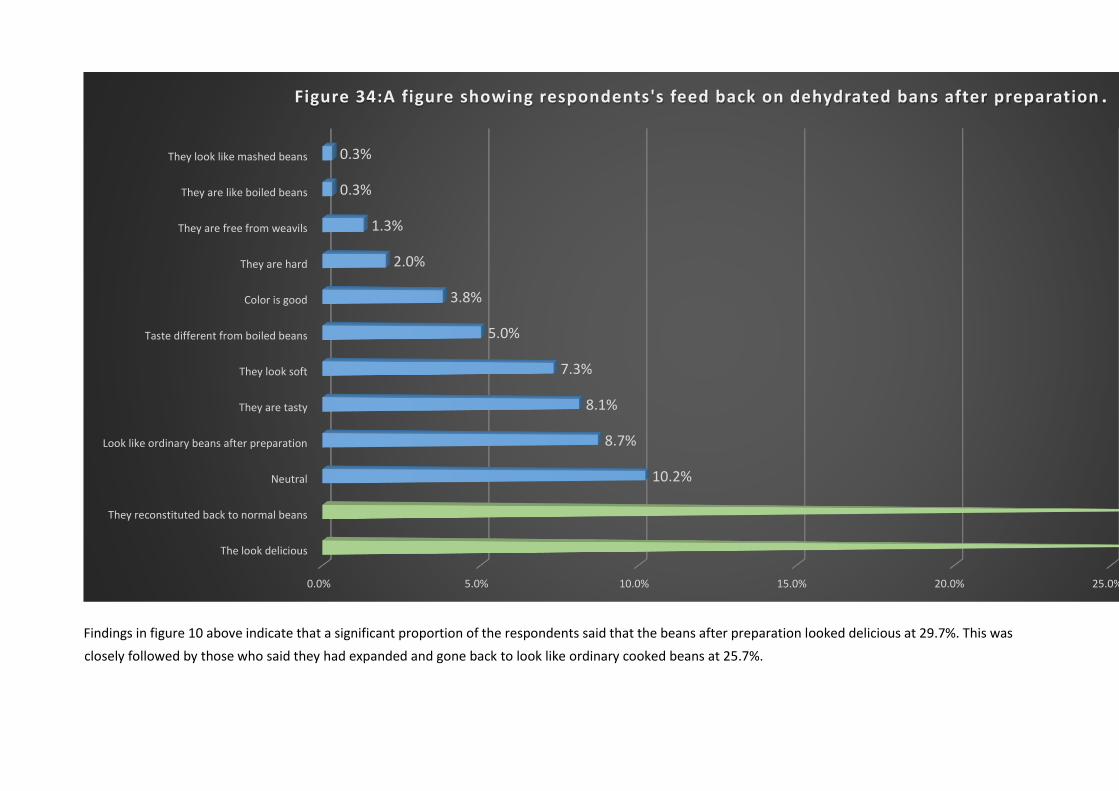

feedback on the appearance of the beans after preparation .... 59 Figure 34: A figure showing respondents` feedback on the appearance of the dehydrated

precooked beans after

preparation .............................................................................................................................................................. 60

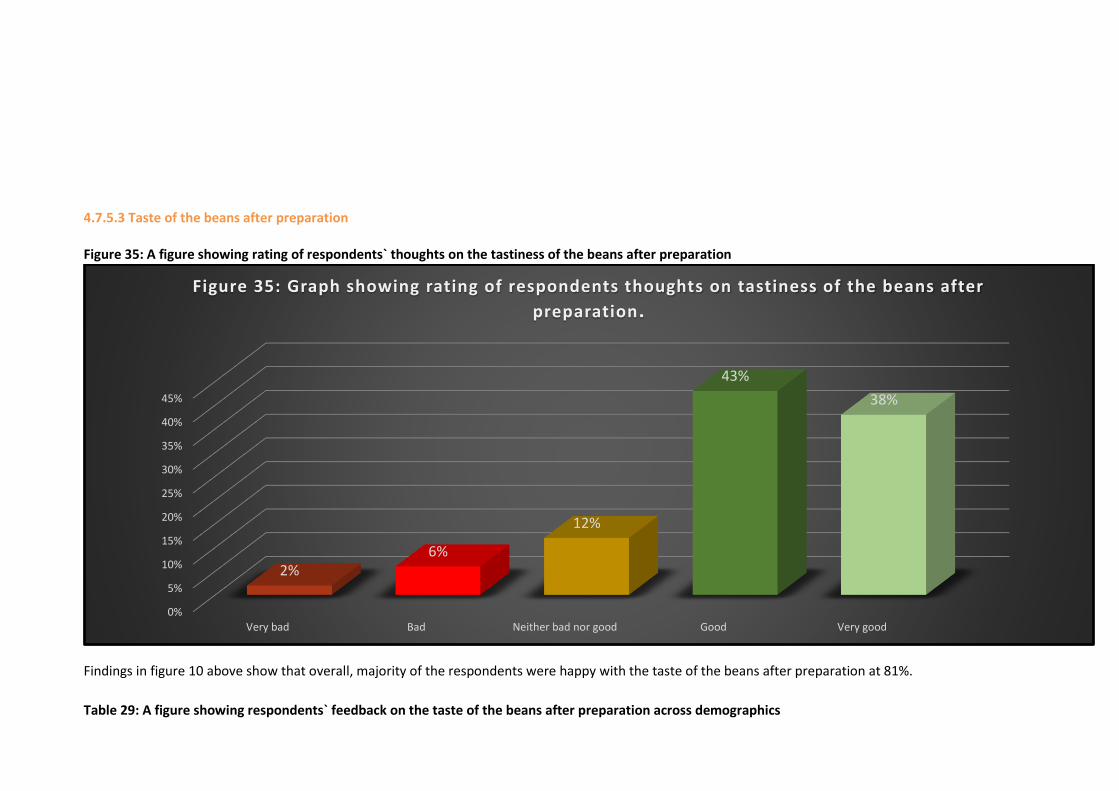

Figure 35: A figure showing rating of respondents` thoughts on the tastiness of the beans after preparation .... 61 Figure 36: A figure showing respondent`s feedback

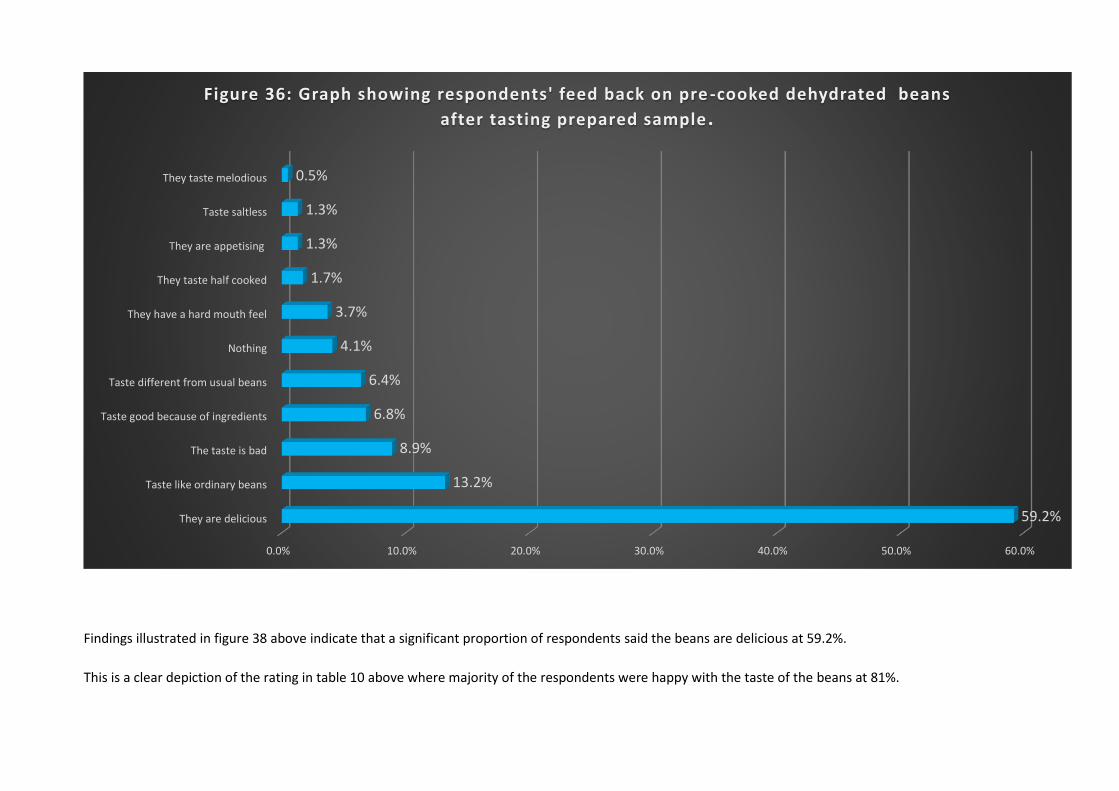

on the taste of the beans after preparation ........................ 62

Figure 37: A figure showing respondents rating of the color of the beans after preparation .............................. 62 Figure 38: A figure showing respondents` feedback

on the color of the dehydrated precooked beans after

preparation .............................................................................................................................................................. 63

Figure 39: A figure showing respondents` feedback on the aroma of the dehydrated precooked beans after

preparation .............................................................................................................................................................. 64

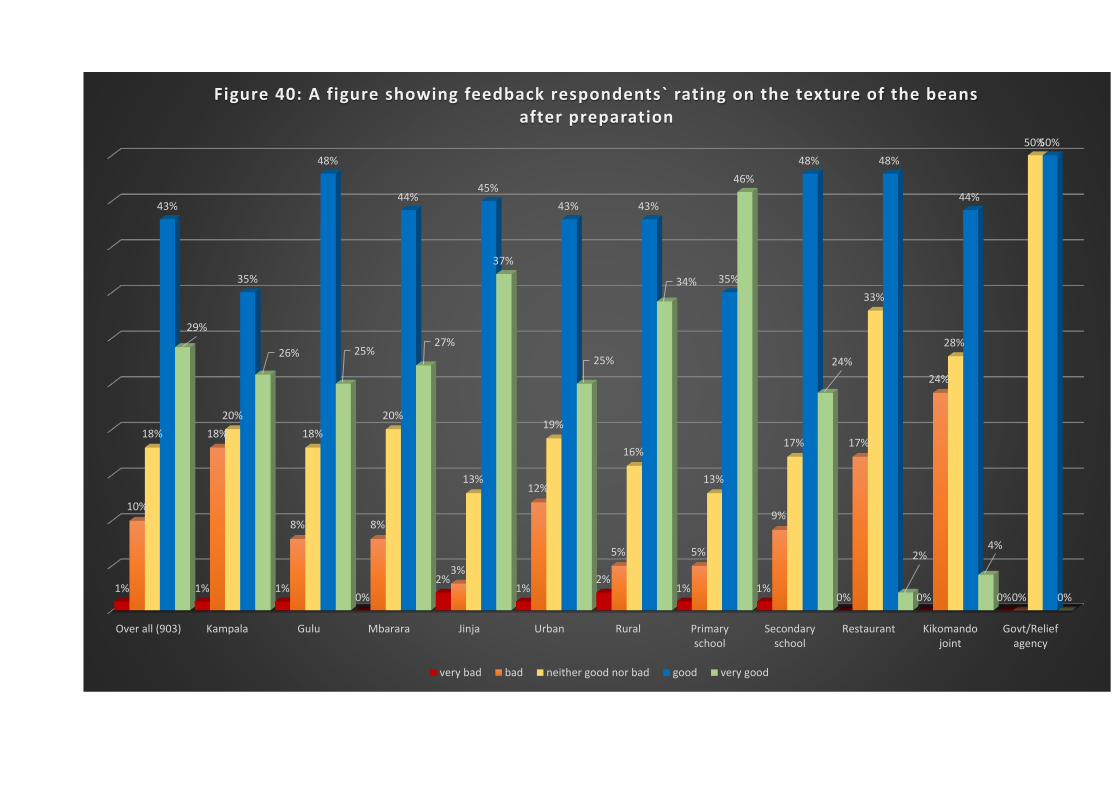

Figure 40: A figure showing feedback respondents` rating on the texture of the beans after preparation .......... 65 Figure 41: A figure showing respondents feedback

on the texture of the dehydrated precooked beans after

preparation .............................................................................................................................................................. 65

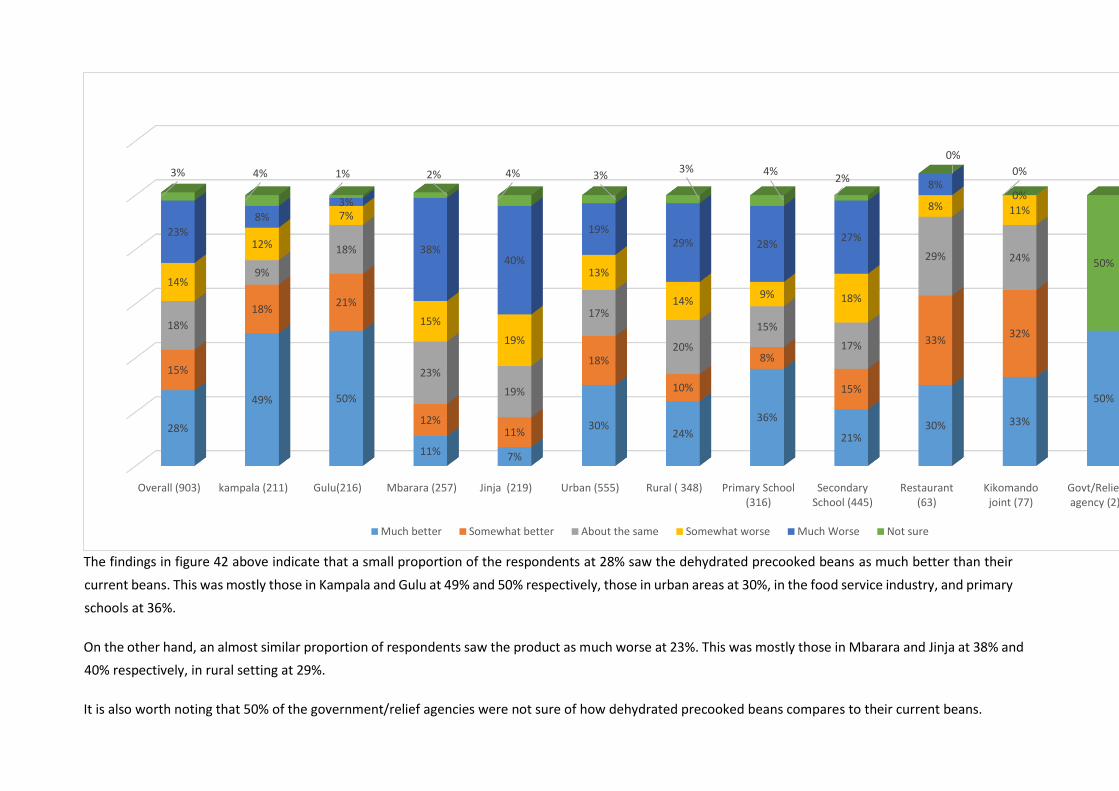

Figure 42: A figure showing respondents` comparison of dehydrated precooked beans to the current beans they

consume/purchase .................................................................................................................................................. 66

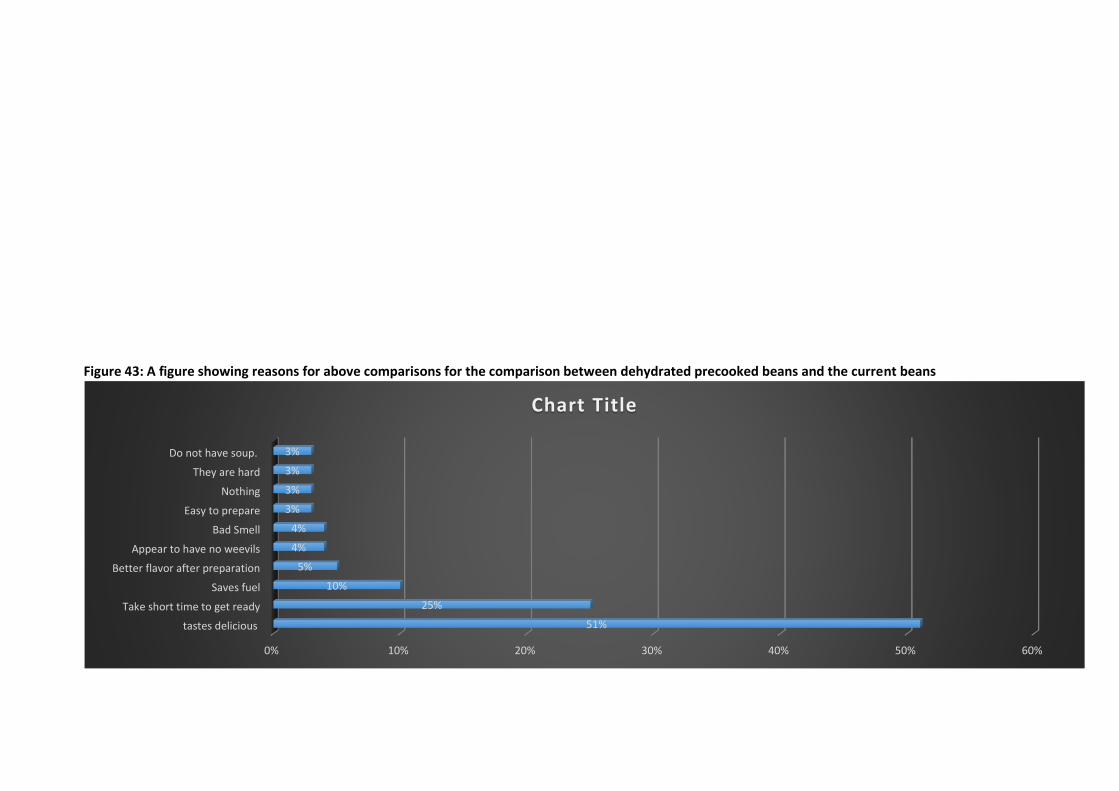

Figure 43: A figure showing reasons for above comparisons for the comparison between dehydrated precooked

beans and the current beans ................................................................................................................................... 67 Figure 44: A figure showing the various likes for

dehydrated precooked beans .................................................... 68 Figure 45: A figure showing the various dislikes for dehydrated precooked beans

............................................... 68 Figure 46: A figure showing respondents` suggestions for improvement of dehydrated precooked beans.......... 69 Figure 47: A figure

showing the institutional need for dehydrated precooked beans ........................................... 70 Figure 48: A figure showing respondents` intent to purchase dehydrated

Dehydrated Precooked Beans Feasibility Study& Product Test Draft Report Page xi of 94

precooked beans ............................... 71 Figure 49: A figure showing reasons for purchase/consumption intent ................................................................. 71 Figure 50:

A figure showing average price respondents are willing to pay for 1 kg of dehydrated precooked beans

................................................................................................................................................................................. 73

ACRONYMS

Measure Definition

FAO Food and Agriculture Organisation

FTF-CPM Feed the Future Uganda Commodity Production and Marketing Activity

RWI Research World International

MAAIF Ministry of Agriculture, Animal Industry and Fisheries

USAID United States Agency for International Development

UNDP United Nations Development Programme

Dehydrated Precooked Beans Feasibility Study& Product Test Draft Report Page xii of 94

DEFINITION OF KEY TERMS Term Definition

Kikomando Joint A roadside kitchen stall where basic foods are prepped and sold to passers by

Relief Agency An organization that provides aid for people in need, especially in disaster areas

Government body An established organization or foundations, especially one dedicated to education, public

service, or culture run by government.

Institution In this case it refers to all the target respondents in the survey which include a primary school,

a secondary school, a restaurant, Kikomando Joints, Relief Agency and Government body.

Dehydrated precooked

beans These are beans that have been fully cooked and dehydrated to remove moisture up to less

than 10 degrees Celsius.

Learners As used in this report, these refer to students and pupils.

Caterers Someone who arranges the delivery, preparation and presentation of food for consumers

Dehydrated Precooked Beans Feasibility Study& Product Test Draft Report Page xiii of 94

EXECUTIVE SUMMARY

Feed the Future Commodity Production and Marketing Activity (FTF-CPM) commissioned Research World International Limited in the month of May 2016 to conduct

a feasibility study and product test for dehydrated precooked beans in Kampala, Jinja, Mbarara, and Gulu districts of Uganda.

The overall objective of this assignment was to establish the availability of market for dehydrated precooked beans in Uganda`s institutional markets and to assess

consumers’ willingness to buy the dehydrated precooked beans product.

This survey was conducted using quantitative methods of sampling, data collection and analysis study. Face-to face Personal interview approach was used during

collection of data. The survey was single phased and encompassed both the feasibility study component as well as the product test component. The target respondents

interviewed were 44 schools, 1 relief agency, 1 government institutions, 65 restaurants and 75 Kikomando joints. In some cases we employed random sampling

techniques, while in other cases where targeted institutions were difficult to find or locate, purposive and snowballing techniques was used.

The key findings and recommendations of the study were that: 91% of institutions are likely to buy dehydrated precooked beans especially among retail shops which

is where they should be sold and distributed; Suppliers of beans need to produce enough quantities of dehydrated precooked that can meet the demand of beans,

especially in schools, government and relief agencies; In order for suppliers of beans to be competitive, they need to be aware of current bean prices on the market

so that they can provide affordable competitive prices to their customers; 52.7% of institutions are yearning to buy precooked beans since they use less fuel especially

in rural areas; most institutions prefer yellow beans while others prefer Kanyeebwa and Nambaale; Major problems found with beans is that they take long to cook,

they have weevils while the dehydrated precooked beans are hard and they smell bad. There is need to put in place solutions to overcome these problems.

Dehydrated Precooked Beans Feasibility Study& Product Test Draft Report Page ii of 94

Conclusion and the way forward is that the suppliers of dehydrated precooked beans should proceed with their production and distribution especially among schools

and government institutions/agencies as that is where there is ready market for them. However, there is need to improve on the various gaps that have been

highlighted in this report concerning the dehydrated precooked beans.

CHAPTER 1 – INTRODUCTION

1.1 Introduction

Feed the Future Commodity Production and Marketing Activity (FTF-CPM) commissioned Research World International Limited to conduct a feasibility study

and product test for dehydrated precooked beans in Kampala, Jinja, Mbarara, and Gulu districts of Uganda.

This document serves as a draft report of the findings from the survey. It is divided into four chapters known as; Chapter one consisting of the introduction

which is largely what was agreed upon at inception of the survey, Chapter two consisting of review of past literature, Chapter three comprising of summary of

the findings, while Chapter four contains the recommendations and conclusions.

1.2 Background

Feed the Future Commodity Production and Marketing Activity`s (FTF-CPM) key objective is to achieve sustainable increase in the production and marketing

of high quality maize, beans and coffee in the 34 FTF focus districts. In support of the beans value chain, the activity partnered with Gryphon Group to introduce

a dehydrated pre-cooked bean product to Uganda`s institutional market. However, before any investments are made into the complete production of the

product, they saw it necessary to carry out a feasibility study and product test in the primary, secondary and tertiary markets. Results from the survey will be

used in formulating a viable business strategy and a product that is tailor made for the institutional market.

Following a competitive process and negotiations, FTF-CPM contracted Research World International to implement a survey amongst schools, relief agencies,

government institutions and the food service industry aimed at establishing the availability of a market for dehydrated precooked beans in the institutional

markets.

1.3 Survey Objectives

1.3.1 Overall objective

The overall objective of this assignment was to establish the availability of a market for dehydrated precooked beans in Uganda`s institutional markets and to

assess consumers’ willingness to buy the dehydrated precooked beans product.

1.3.2 Specific objectives

The specific objectives of this assignment were categorised into two as shown below;

A. Feasibility study for dehydrated precooked beans:-

• To gather data on the nutrition standard preferences for the various institutions

• To gather data on current bean consumption and usage

• To determine constraints faced with the current bean product

• To establish bean category preferences

• To determine the size and scope of the institutional market for dehydrated precooked beans in Uganda

• To gauge the acceptability of a dehydrated precooked bean product

B. Product test for dehydrated precooked bean product:-

• To gather spontaneous thoughts and perceptions on the product

• To establish likes and dislikes, and suggestions for improvement on proposed product

• To determine likelihood to purchase the product and at what prices

CHAPTER 2 – LITERATURE REVIEW

Given the importance of beans, it is necessary to understand what the situation of the bean sub-sector in Uganda is in terms of production, marketing and

consumption. This chapter presents a review of past literature from a number of studies and elaborates the theoretical basis for the study.

2.1 Overview of the Beans Subsector

Beans are the most important legume for human consumption in the world. According to (FAO, 2011), the most important legume in Uganda is beans, followed

by ground nuts, soya bean, cowpea, and pigeon pea. While beans are considered a low status food, the “meat of the poor”, they provide the second most

important source of protein after maize and the third most important source of calories after maize and cassava (Pachico, 1993). It is estimated that about 20

million MT of beans are produced annually with a market value of US $10 billion. The leading countries in the production of beans in 2010 by volume were

India, Brazil, Myanmar, USA and China (FAOSTAT, 2012).

In the East African Community (EAC) Region, Uganda is ranked second to Tanzania in the production of common beans also known as Phaseolus Vulgaris

(UNDP, 2013)1. In Uganda, beans provide 25% of the total dietary calorie intake and 45% of the protein intake and with their short growing cycle and

adaptability to a wide range of growing conditions they are a vital source of income for many families, contributing up to 9% of household income in some

areas. As a traditional staple food, beans are a major source of affordable protein, complex carbohydrates, essential micronutrients, dietary fiber, vitamin B

and antioxidants in the nutritionally challenged diets of both the rural and urban poor.

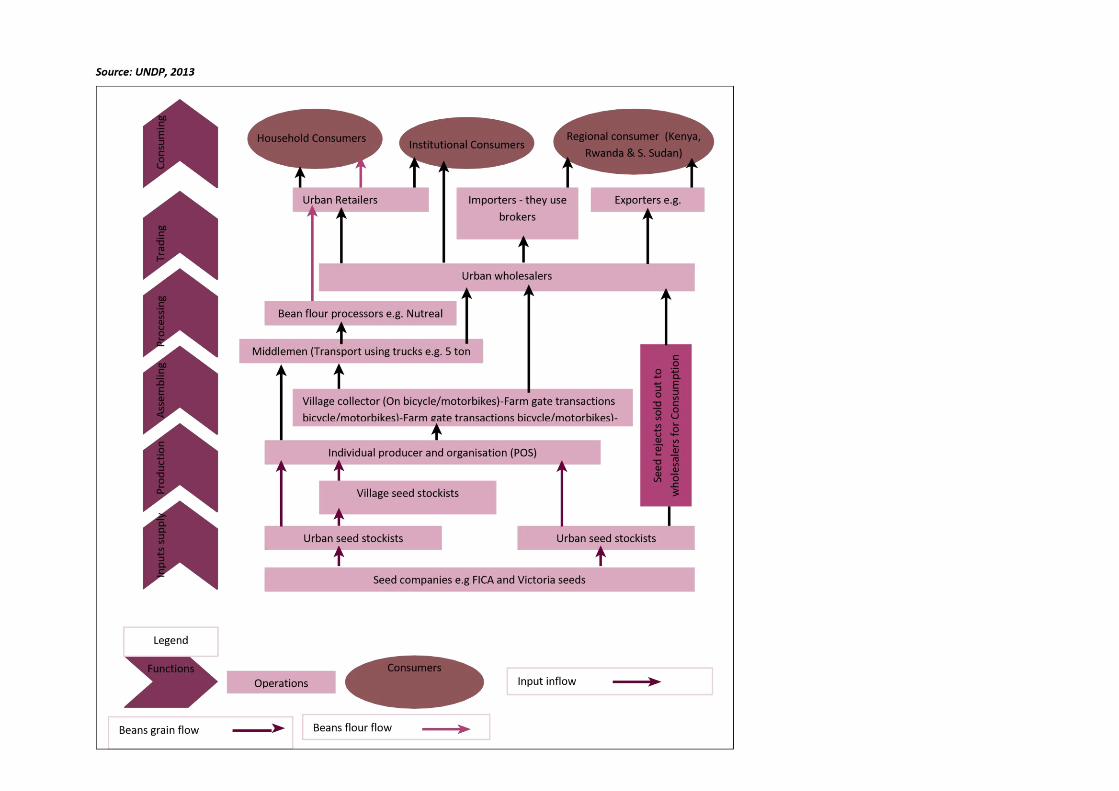

2.2 Value chain of beans in Uganda

The value chain of bean grain and bean seed as shown below is a map of the key micro-level actors of the bean grain value chain. These are the input suppliers,

producers, assemblers, processors, traders and consumers. Bean consumption is through three channels of households, institutions and regional trade.2

1 http://ussp.ifpri.info/files/2011/10/bean-marketing-in-uganda-nkonya-2001.pdf

2 United National Development Programme. (n.d.). United National Development Programme Home page . Retrieved 11 20, 2016, from United National Development

Programme Uganda Website

2.3 Beans Production in Uganda

The common bean (Phaseolus vulgaris) is a basic constituent to the traditional diet of most Ugandans. Beans are grown in two seasons (March to June, and

September to November). The September to November season records high yields due to the high amount of rainfall. For instance, in 2008/2009 growing

season, 59% of all the beans produced was during this season (MAAIF, 2010). Productivity of beans in Uganda recorded a sharp decline in 2006 from 478,000

metric tonnes to 424,000 metric tonnes. However, between 2004 and 2010, production increased by 2% (MAAIF, 2010)3. This increase in production was

associated with the increasing population. Uganda has been ranked the second producer of beans after Tanzania in the East African Community.

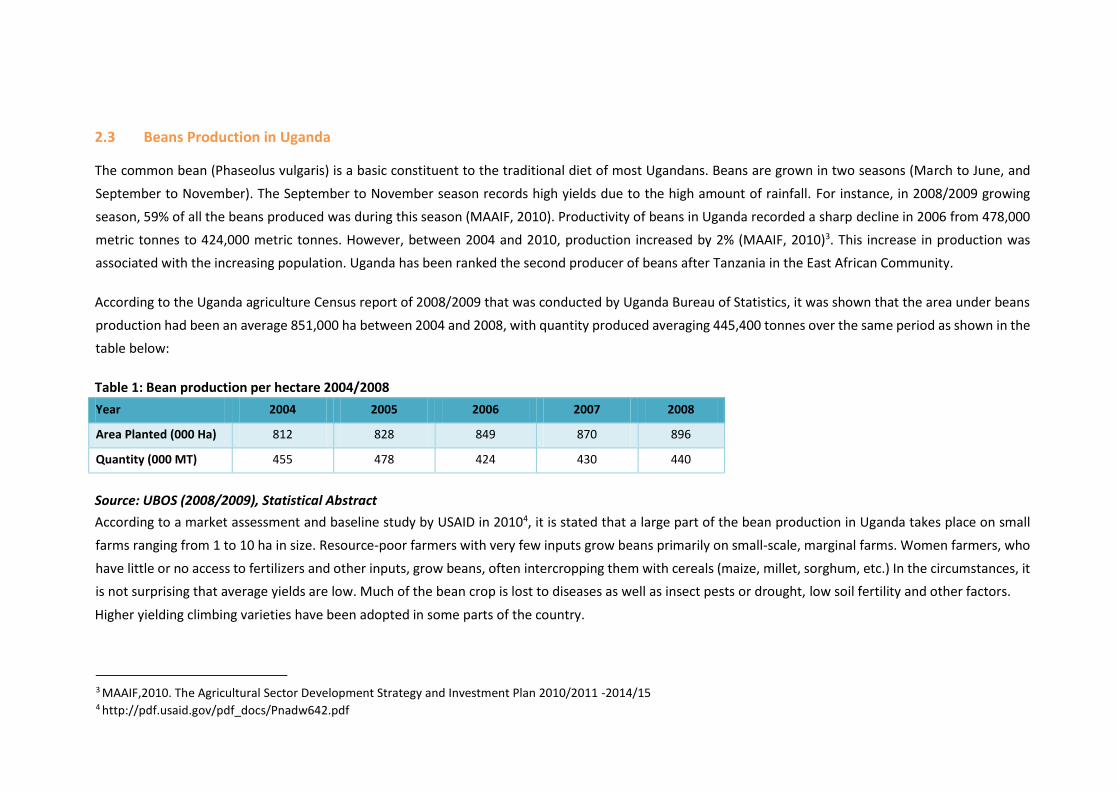

According to the Uganda agriculture Census report of 2008/2009 that was conducted by Uganda Bureau of Statistics, it was shown that the area under beans

production had been an average 851,000 ha between 2004 and 2008, with quantity produced averaging 445,400 tonnes over the same period as shown in the

table below:

Table 1: Bean production per hectare 2004/2008

Source: UBOS (2008/2009), Statistical Abstract

According to a market assessment and baseline study by USAID in 20104, it is stated that a large part of the bean production in Uganda takes place on small

farms ranging from 1 to 10 ha in size. Resource-poor farmers with very few inputs grow beans primarily on small-scale, marginal farms. Women farmers, who

have little or no access to fertilizers and other inputs, grow beans, often intercropping them with cereals (maize, millet, sorghum, etc.) In the circumstances, it

is not surprising that average yields are low. Much of the bean crop is lost to diseases as well as insect pests or drought, low soil fertility and other factors.

Higher yielding climbing varieties have been adopted in some parts of the country.

3 MAAIF,2010. The Agricultural Sector Development Strategy and Investment Plan 2010/2011 -2014/15

4 http://pdf.usaid.gov/pdf_docs/Pnadw642.pdf

Year 2004 2005 2006 2007 2008

Area Planted (000 Ha) 812 828 849 870 896

Quantity (000 MT) 455 478 424 430 440

2.3.1 Bean varieties grown in Uganda

A number of bean varieties are grown in Uganda with notable diversity in terms of seeds type and adaptation. Local market preferences and variances in

climatic and agronomic conditions generally dictate which varieties are popular. There is some bias towards the large-seeded types in Uganda where farmers

grow and maintain seed mixtures of all sizes and colors. The grain is an important cash crop and the leaves are also an important vegetable in some parts of

the country.

According to Waluse (2012), specifically, Ugandan bean farmers traditionally grow varietal mixtures of variable growth habits. However, some production of

single varieties is also practiced, especially for urban markets. In Kalyebara (2008), it was found that farmers grow the traditional varieties for the household

consumption, and the improved varieties for commercial purposes. There are several varieties within the country, with most of the traditional varieties having

degenerated into what is commonly referred to as “local” varieties (Uganda’s grain subsector report, 2007). See appendix 1 for list of current common bean

varieties

2.3.2 Bean growing areas

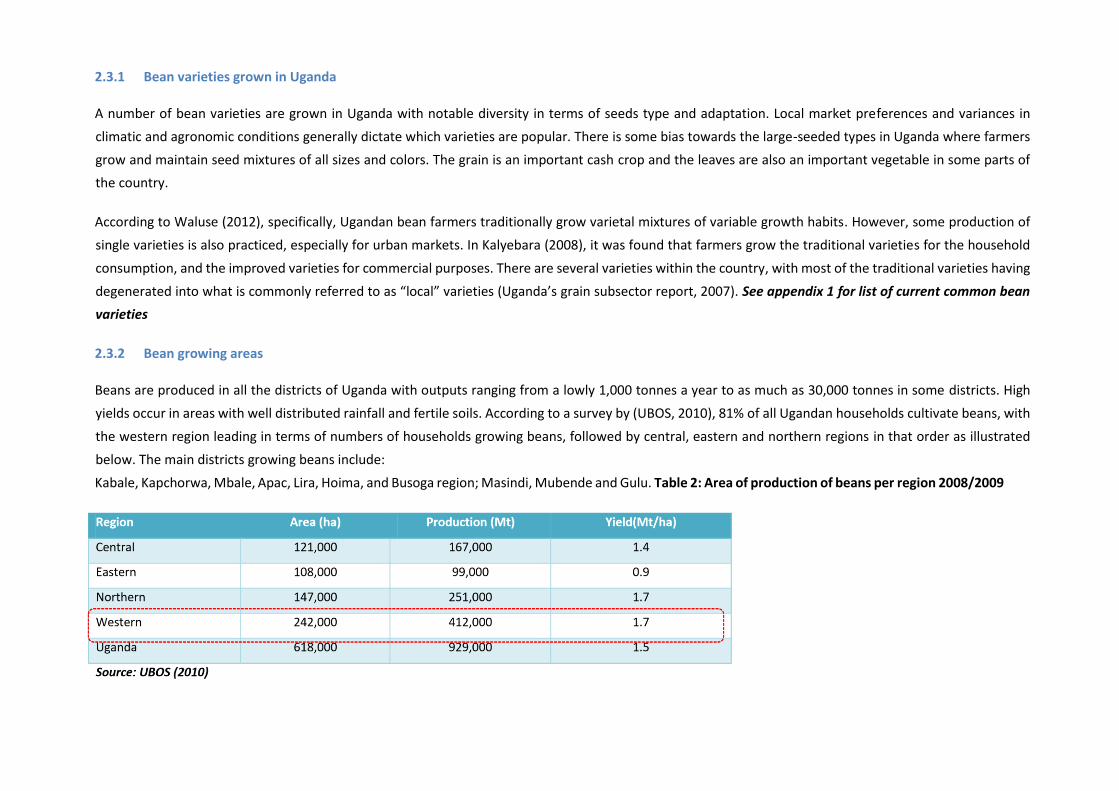

Beans are produced in all the districts of Uganda with outputs ranging from a lowly 1,000 tonnes a year to as much as 30,000 tonnes in some districts. High

yields occur in areas with well distributed rainfall and fertile soils. According to a survey by (UBOS, 2010), 81% of all Ugandan households cultivate beans, with

the western region leading in terms of numbers of households growing beans, followed by central, eastern and northern regions in that order as illustrated

below. The main districts growing beans include:

Kabale, Kapchorwa, Mbale, Apac, Lira, Hoima, and Busoga region; Masindi, Mubende and Gulu. Table 2: Area of production of beans per region 2008/2009

2.4 Beans consumption in Uganda

2.4.1 Domestic market

Beans are the most important legume for human consumption in the world. They are estimated to be the second most important source of dietary protein

and the third most important source of calories. They are an important staple food in sub-Saharan Africa, particularly in rural areas of Eastern Africa.

In Uganda, beans are a major staple and a key source of food security for both rural and urban populations. Consumer preferences for beans differ, depending

on seed types, color, shape, and brilliance or seed coat luster. However, many consumers prefer beans with the sweet taste and fast cooking attributes. There

is higher demand for bean varieties with these attributes than those which have very attractive seed appearance. Beans are often combined with such energy

sources as maize, plantains (matooke), or root crops (sweet potatoes, cassava, yams, etc). The high nutritional value of beans in terms of the percentage of

protein is an important complement to these starchy foods. In addition, the high mineral content of beans, especially iron and zinc, is advantageous in cases

of high prevalence of micronutrient deficiencies such as iron deficiency anemia.

The Uganda census on Agriculture of 2008/2009 established that out of the 929,000 MT of beans produced during the 2008/2009 seasons, 32% of the produce

was consumed, 23% was stored and 12% were used for other purposes (UBOS-UCA, 2010)5. The demand for common beans in Uganda in 2010 was estimated

to be 464,000 MT and it is projected that, it will rise to 641,000 MT by 2020 (Abate et al., 2011). Per capita consumption of beans in Uganda is estimated to be

19 Kg/Yr much of which is institutional demand (schools, World Food Program, prisons, Ministry of Defense, Police, Prime minister’s office for relief distribution)

and individual buyers. The key drivers of demand of these beans are mainly prices, population growth and availability.

According to Education Management Information System data sheet (2012) the total number of primary schools in Uganda is 22,501. Of these primary schools,

8,337,069 students are enrolled. Of which 4,168,931 are boys and 4,168,130 are girls. In addition, the data sheet shows that 7,097,382 of these students are

enrolled in government schools while 1,121,833 students are enrolled in private schools.

Ibid, (2012)6 states that the total number of secondary schools in Uganda is 3,038. Of these secondary schools, 1,240,437 students are enrolled. Of which,

669,334 are boys and 578103 are girls. In addition the data sheet states that 2,143 are government schools while 895 are private secondary schools. Further

details show that 590,801 students are enrolled in the private secondary schools while 656,636 students are enrolled in government secondary schools.

5 UBOS. & MAAIF. 2010. Uganda Census of Agriculture 2008/2009. Kampala: Uganda Bureau of Statistics and Ministry of Agriculture, Animal Industry and Fisheries.

6 EMIS Data sheet 2000-2012. Kampala: Ministry of Education and Sports

According to a survey conducted by UBOS in 2009, most beans produced are consumed locally. Out of the quantities produced between 2004 and 2008

generally over 90% is estimated to have been consumed locally with insignificant amounts being sold informally to neighboring countries. National annual

consumption of beans is estimated at about 58 kg per capita.

According to a study done on staple foods by USAID in 20107, it is stated that apart from the World Food Programme, the main buyers of beans are institutions

(schools, hospitals, police, prisons, restaurants, etc.), buying either from village stores or large urban traders. Volumes purchased differ according to the size

of the institution. Small institutions buy between 2 and 5 100-kg bags of beans every week, while large institutions procure big volumes of between 5-10 100-

kg bags of beans per week. Purchases are mainly done on credit basing on the ruling price in the market.

2.4.2 International market

There is a significant market for Ugandan beans within the region, but as noted earlier, most of the beans produced are consumed domestically. In spite of

this, however, some amounts are exported to the region. Exports are primarily in unprocessed form with little value added. Over 90% of Uganda`s bean market

is across the borders. Such trade is categorized into formal and informal operations.

The informal trade is particularly significant at the border points of Uganda and Kenya, Sudan, DRC, Tanzania, and Rwanda. According to a Market Assessment

that was done by USAID in 2010, it was estimated that about 90 –120 Kg bags of beans were ferried to Kenya through Busia border point. The major participants

in this trade were found to be youth who either carry their commodities on bicycles or cross the border points on foot. Beans are carried in small quantities of

up to 5 kilograms. The two groups involved in informal trade are the foreign buyers who travel from neighbouring countries into Uganda to purchase the beans

and Ugandan exporters, who include large scale producers, traders/ and companies who mainly export their beans formally through the border points.

The formal bean trade is still very small with World Food Programme being the largest exporter of beans from Uganda. Majority of beans are exported to the

neighbouring countries. WFP uses two procurement mechanisms namely; Agriculture and Marketing Support Programme, the WFP purchases beans mainly

from farmer groups who can supply at least 40 MT and by other community based organizations. WF`s Vulnerability and Assessment Unit ensures that farmer

groups are paid a fair price. Producer groups are also assisted with market information on commodity prices throughout the country. This programme is

working well in eastern, central and western Uganda, where farmers have good surpluses every year. The WFP also purchases from traders who can stock bulk

and/or supply at least 200 MT of beans. Kampala has the biggest bean traders with sufficient volumes for export.

7 http://pdf.usaid.gov/pdf_docs/Pnadw642.pdf

2.5 Nutritional standards

According to the US Dry bean council, dry beans and other legumes are some of the most widely available, inexpensive and nutritionally complete staple foods.

In the Dietary Guidelines for Americans 2010, scientists recommend that adults consume three cups of beans per week to promote health and reduce the risk

of chronic diseases.8

As both a vegetable and a non-meat protein source, beans contain nutrients found in both food groups. They are also a nutrient-rich source of complex

carbohydrates and contain dietary fiber, proven to reduce the risk of heart disease and some cancers and to aid in weight maintenance.

According to East Africa Community (2013), it is stated that dry beans for human consumption should meet the specifications set out in the East African

Standards for dry beans.9 These are can be summarized as the quality requirements, general requirements, specific requirements, contaminants, Hygiene,

packaging and labeling requirements.

2.6 Limitations to bean consumption

One of the biggest limiting factors to bean consumption is the time required to cook them and, consequently, the amount of fuel or firewood required for

cooking. According to UNDP 2010 report on the bean value chain, consumption has been marginal over the years due to the reduction in per capita

consumption of beans caused by:10

• The hard to cook characteristics of beans which require a lot of time to cook and consume a considerable amount of energy. This characteristic of

beans make urban consumer biased against bean based meals due to the inadequacy in the time they have to prepare food,

• The effect of flatulence on consumers causing discomfort to consumer

• A wrong perception has been assigned to bean meals branding them as inferior. This can be seen in some names given to beans such as ‘poor man’s

meat’ and the minimal attention on building consumers’ demand.

Other factors explaining slow development of the bean sub-sector include: under-developed bean markets as most of the trade is informal with very few

market off-takers and limited value addition

8 http://www.usdrybeans.com/nutrition/guidelines/

9 East African Community. 2013. Final Draft East African Standard :Dry beans specifications, East African Community

10 UNDP.2012. A Value Chain Analysis of the Dry Bean Sub-sector in Uganda

The low status accorded to beans by consumers is caused by the high infestation of beans with storage pests especially “bruchids” and Hard to cook effect

(HTC) as a result of inadequate postharvest handling and poor storage, poor storage also leads to high post-harvest losses of beans leading to increased prices

for the consumer and low returns for the producers, and the current inadequate value addition processing into bean-food-products is also caused by poor

post-harvest handling which reduces the quality of raw beans with respect to the basic requirements for processing.

2.6 Opportunities in the beans sub-sector

According to the Uganda Investment Authority (UIA) report on the foods and beverages industry, market for dry beans exists, locally, regionally, and

internationally. Demand exists in East and Western Uganda, across borders within the region and for relief agencies (up to 300,000 MT per annum)11 with the

instability in the region fueling the demand. Within the region, beans could be canned for the local, regional and export markets.

2.7 The potential for dehydrated precooked beans

Beans are a key source of protein among low income households and institutions. In recent years, the rapid expansion of urban populations, rising incomes,

and high costs of energy have fuelled the demand for fast-cooking, processed foods. Canned or frozen beans are sometimes available, but are only affordable

to a minority of wealthy consumers. Developing affordable bean products is therefore increasingly important.

According to the Kenyan National Agricultural Research Organization, by engaging farmers and the private sector to introduce a range of precooked bean

products to suit different consumers, the East African precooked beans' project will impact in a number of ways farmers and consumers across East

Africa. This is further emphasized by the Director of National Crops Resources Research Institute (NaCRRI) as published in the Daily Monitor in 2015, that

processing pre-cooked beans there will improve nutrition content, incomes and conserve the environment in terms of saving on biomass energy as well as

boost farmer production of beans since there will be ready market provided by processing industries.

In a similar thought Ugen, M. (2014), emphasizes that developing a viable precooked bean industry requires reliable production of appropriate bean varieties,

effective marketing systems, and competitive food products acceptable to consumers.12 He further adds that dehydrated precooked beans if introduced will

have the following benefits;

11 UIA.2000. Investing in Uganda`s food and beverages Industry

12 Ugen, M. (2014). precooked beans for nutrition ,food and income in Uganda. Kampala, Uganda : National Agriculture Research Organization

• Increased availability of bean varieties with high nutritional content (protein, iron, and zinc) suitable for precooking, produced by 7,500 smallholder

farmers.

• Increased bean production at the household level, supported by increased market demand.

• Job creation in new agro-enterprises at various stages of the value chain (production, grading, bulking, packaging, transportation, and marketing),

especially for women and youth.

• Increased incomes at household level from the sale of beans.

• Greater consumption of beans by households in rural, urban, and peri-urban areas.

• Less wood used in cooking beans and less time spent by women collecting it.

• Empowerment of various social groups (women, men, and youth) engaged in adding value to beans.

The need to develop a bean product that will take a much shorter preparation time yet still affordable comes with a need for the private sector to collaborate

with farmers to boost the bean value chain. With a product in mind such as dehydrated precooked beans, that can possibly address these needs, there is a

need to first of all conduct a feasibility study for this product to establish whether it is viable to invest in its production and secondly to test the product with

the intended consumers to find out whether it will be accepted.

CHAPTER 3 – RESEARCH METHODOLOGY

3.1 Study Design

The design of this survey was formative in nature. This survey was conducted using quantitative methods of sampling, data collection and analysis study. Face-

to-face Personal interview approach was used during collection of data. The survey was single phased and encompassed both the feasibility study component

as well as the product test component. Described below were the survey procedures followed:

Survey Procedures

• The survey was done in schools, relief agencies, government bodies and food services industry (Kikomando joints and restaurants). These institutions were

sampled from the urban/rural setting of Kampala, Jinja, Mbarara, and Gulu.

• We used a single phased approach where both the feasibility study and product test were done concurrently.

• Due to the nature of the respondents, for all the interviews, appointments were set with the various in charges at each of the institutions prior to the time

of the interview and respondents informed of the need to take part in both the feasibility study as well as the product test. At this point, the in charges

were also informed of any assistance we needed from them in terms of space to carry out the product test as well as a list of potential respondents we

needed to take part in the survey. The in charges provided consent for the institution`s willingness to participate in the survey and also facilitated the

availability of other respondents.

• On the date of the interview, the interviewers were tasked with ensuring that the in charge avails them with the appropriate respondents and again obtain

individual consent from these respondents. for example in schools we interviewed the bursar/HM/Deputy Head teacher (i.e. any one of them that was

well versed with the purchase activities of the institution), a head cook, and 12 learners, in Kikomando joints & restaurants, we interviewed the business

owner or someone who managed the day-to-day running of the business, In relief agencies and government institutions, we interviewed the person in

charge of procurement.

• At each institution, an average interview of both feasibility study and product test took between 2 hours to two hours and 30 minutes.

3.2 Feasibility Study

We adopted the quantitative research approach. This approach entailed use of surveys that were intended to capture information on current product usage

and consumption; quantities purchased annually, challenges faced with current beans, storage practices, labour costs, fuel consumption, nutritional standards,

and acceptability of dehydrated precooked beans among others.

Information was gathered through face-to-face personal interviews with targeted primary and secondary markets. These included;

• Primary markets: School administrators

• Secondary markets: Administrators of Kikomando joints and restaurants and persons in charge of procurement/welfare in relief agencies and

government institutions.

3.2.1 Sampling

The survey took place in Kampala, Jinja, Mbarara, and Gulu. In some cases, we employed random sampling techniques, while in other cases where targeted

institutions were difficult to find or locate, purposive and snowballing techniques was used.

3.2.1.1 Schools

Within schools, the target population included the caterer/head cook who knows the amount of food cooked per day for each student/learner, the deputy

head teacher/ Head Teacher who is usually the one in charge of purchases, the school bursar who executes the purchase.

With the aid of district specific data for each of the districts, we categorised the schools as government aided and non-government aided, day and boarding,

primary and secondary, rural and urban. As such in each district, we targeted to achieve a sample of 16 schools.

Sample size

To arrive at the 16 schools, we adopted the formula for a sample size required for an experiment designed to investigate the behaviour of an unknown

population mean will be influenced by the following:

• value selected for α, the risk of rejecting a true hypothesis,

• value of β, the risk of accepting a false null hypothesis when a particular value of the alternative hypothesis is true,

• value of the population standard deviation

Assuming that α=0.05 and β=0.50 then this give us a value of 16 (you may refer to the table on

http://www.itl.nist.gov/div898/handbook/prc/section2/prc222.htm).

The number of schools per district was based on the assumption that we can able to calculate and compare means on been consumption per schools

Sampling frame

The sampling frame was a list of primary and secondary schools in the four districts of Kampala, Jinja, Mbarara and Gulu. The list got from Education

Management Information System in Uganda provided us with the data on the domains of selection that is boarding, rural and government or private. Our

sampling frame for schools the was obtained from the Ministry of Education

Sample design

Each school was taken as a cluster hence adopted cluster sampling design within the schools.

3.2.1.2 Restaurants

In each of the urban places at least three major markets were identified that serve low and middle income people in terms of meals. From each district 16

restaurant owners who manage the purchase of food were targeted to be interviewed using face-to-face approach.

3.2.1.3 Relief Agencies

The survey targeted 3 relief agencies in Kampala that invest a lot in purchasing food for relief. Individual staffs who are in charge of purchase of food for relief

in the selected agencies were the target key respondents. Out of the 3 relief agencies, only World Food programme accepted to participate in the study while

World Vision and Red Cross said they do not buy beans and were therefore unable to participate in the study. Both the two agencies indicated to us that they

are supplied beans by World Food Programme.

3.2.1.4 Government Institutions

The survey focused on institutions that purchase beans in bulk. We targeted to interview persons in charge of purchases/Welfare from 3 institutions in Kampala.

Out of the 3, only Office of the Prime Minister accepted to participate in the study while Uganda Police Force, Uganda Prisons Service, and Uganda People`s

Defence Forces (UPDF) said they can only participate in the study with permission from Ministry of Defence which required stretching of the timelines to

accommodate for securing such permission hence they were left out.

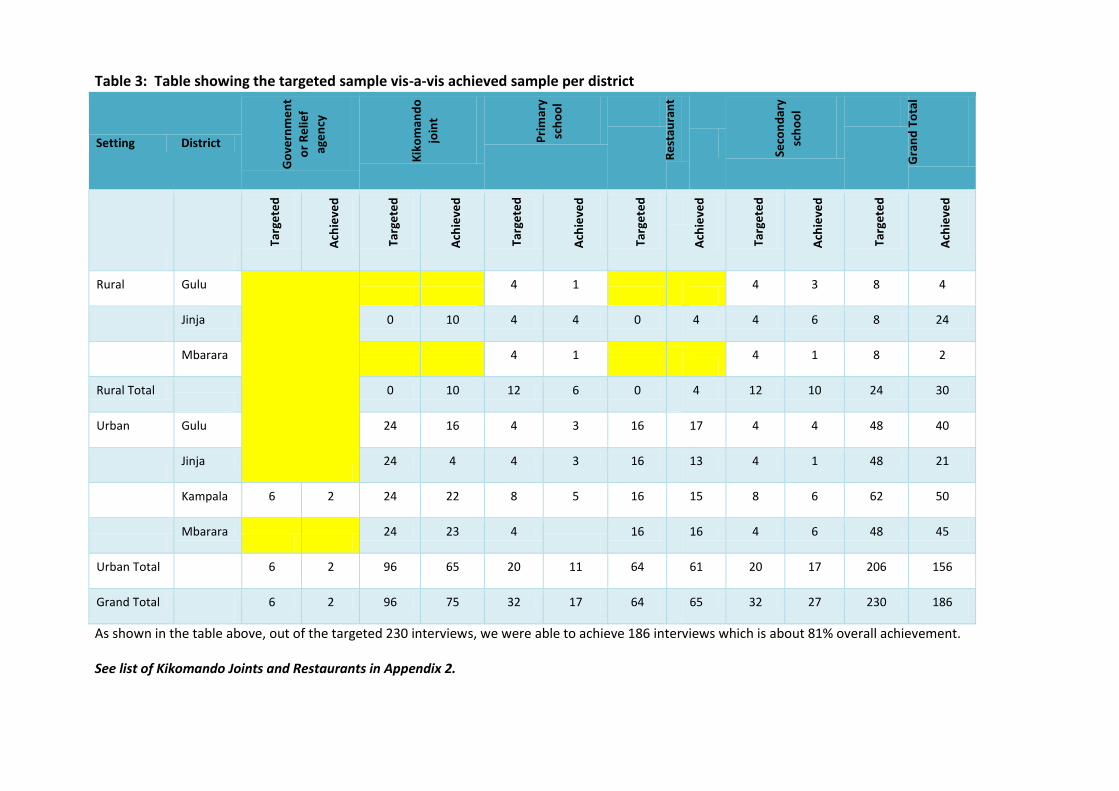

Table 3: Table showing the targeted sample vis-a-vis achieved sample per district

Setting District

Rural Gulu

4 1

4 3 8 4

Jinja 0 10 4 4 0 4 4 6 8 24

Mbarara

4 1

4 1 8 2

Rural Total

0 10 12 6 0 4 12 10 24 30

Urban Gulu 24 16 4 3 16 17 4 4 48 40

Jinja 24 4 4 3 16 13 4 1 48 21

Kampala 6 2 24 22 8 5 16 15 8 6 62 50

Mbarara

24 23 4

16 16 4 6 48 45

Urban Total

6 2 96 65 20 11 64 61 20 17 206 156

Grand Total 6 2 96 75 32 17 64 65 32 27 230 186

As shown in the table above, out of the targeted 230 interviews, we were able to achieve 186 interviews which is about 81% overall achievement.

See list of Kikomando Joints and Restaurants in Appendix 2.

3.2.2 Secondary Data

Secondary data has been gathered to validate and fill any gaps from the primary data. The RWI team of consultants has conducted desk review that has given

us the opportunity to further understand the bean market. This has been put as a separate section called Literature review. See section 2

3.3 Product Test

We adopted the quantitative research approach. This approach entailed use of surveys that were intended to capture information on the sensory reaction,

spontaneous thoughts, perceptions, likes and dislikes, pricing, acceptability of the proposed product during the product test.

Information was gathered through central location tests (CLT) with targeted primary, secondary market in Kampala, Jinja, Mbarara, and Gulu with an

urban/rural split.

Central Location Tests

This technique is appropriate in instances where contact with the product being tested is necessary. Participants were recruited at the various institutions to

participate in the research at a central, convenient and spacious location like at the cafeteria or a room recommended by the institution; the product test

was conducted and questionnaire completed at that time. Since the research required us to test one product for all the respondents, we employed the

monadic test scenario.

This scenario is used in situations where a new product is yet to be launched or is being developed for a particular set of target consumers in order to find out

whether the product will be accepted by the intended consumers.

Target respondents

We targeted the primary, secondary as explained below:-

Primary market: The targets were learners and administrators in the sampled schools within the four districts in both rural and urban setting.

Secondary market: We targeted business owners/managers in the institutions in the food service industry like Kikomando joints and restaurants, Procurement

Managers with in the relief agencies and government institutions in the urban areas of the four districts.

The criteria for inclusion will be based on the following criteria:

Should be an institution in the 4 districts where the survey is being conducted

Should have a procurement/purchase decision maker available and consenting to be interviewed/participate in this survey.

The criteria for exclusion will be failure to meet all the above criteria.

Respondent Recruitment Criteria

We targeted institutions that purchase beans more regularly and in large quantities. For a respondent to qualify for this research they had to fall in any of the

following categories; schools, institutions in the food service industry like Kikomando Joints and restaurants, relief agencies and government institutions.

Respondent Recruitment

The very institutions used for the feasibility study were given priority for the product test. To minimise on recruitment time, recruitment for the feasibility

study and product test took place at the same time implying that a respondent gave consent to participate in both studies at once.

In all institutions, upon getting consent, while the interview for the feasibility study was going on, the set up for the product test was also happening at the

same time. This was aimed at minimising time spent within an institution.

In schools, we liaised with selected teachers regarding the selection of students to participate. Students were selected from various class levels except in

schools where at the time of visit only one class was available. Upon identifying the learners and a venue, set up for the product test was done.

3.3.1 Sampling

The same institutions sampled for the feasibility study were considered for the product test. While the same administrators/owners/chefs in the institutions

sampled above took part in the product test, in the schools, we also recruited learners who are the consumers of beans.

Sample size for the learners The number of learners per school was determined using the formula below

The Kish (1965) formula was used for the sample size determination. The formula is as stated below

Where

N required sample size

z is the 95% Confidence interval, Z=1.96, e is the permissible error = 5% p is proportion of the total population who are knowledgeable on

the indicator of interest 50% q is the proportion of the total population who are not knowledgeable on the indicator of interest

100-p=50% deff design effect taken as 2

Substituting in the formula we get n=768

This was the targeted minimum number of learners to be interviewed. Since we proposed to go to 16 schools per district that is 16X4=64, then we collected

data from 12 learners per school (768/64=12.0005).

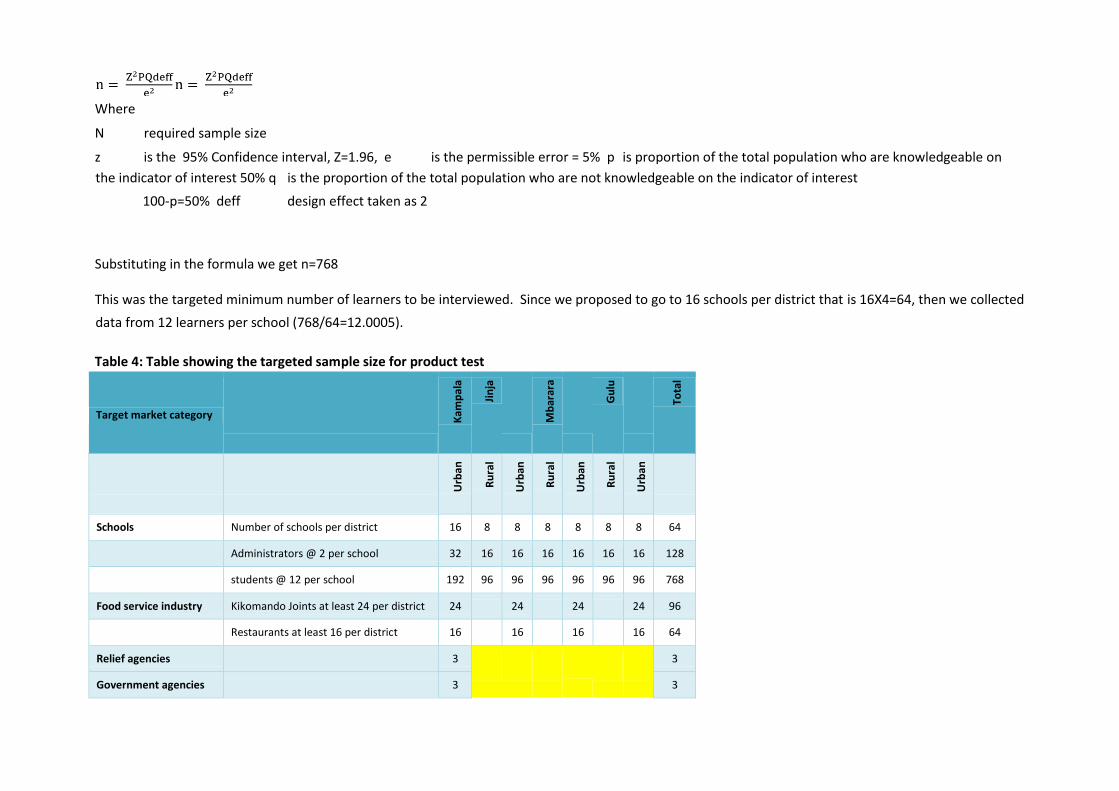

Table 4: Table showing the targeted sample size for product test

Target market category

Schools Number of schools per district 16 8 8 8 8 8 8 64

Administrators @ 2 per school 32 16 16 16 16 16 16 128

students @ 12 per school 192 96 96 96 96 96 96 768

Food service industry Kikomando Joints at least 24 per district 24 24 24 24 96

Restaurants at least 16 per district 16 16 16 16 64

Relief agencies 3

3

Government agencies 3 3

Targeted sample size 1,126

Table 5: Table showing the achieved sample size for product test

District Business of organization

Gulu Kikomando joint 16 16

Primary school 40

30 70

Restaurant 17 17

Secondary school 84

29 113

Gulu Total

124 92 216

Jinja Kikomando joint

10 4 14

Primary school 69 30 99

Restaurant 4 13 17

Secondary school 75 14 89

Jinja Total

158 61 219

Kampala Government or Relief agency

2 2

Kikomando joint 22 22

Primary school 95 95

Restaurant 15 15

Secondary school 77 77

Kampala Total

211 211

Mbarara Kikomando joint

25 25

Primary school 40

12 52

Restaurant 14 14

Secondary school 26

140 166

Mbarara Total

66 191 257

Grand Total 348 555 903

3.3.2 Product that was tested

The dehydrated precooked beans that were tested were provided by Gryphon Group who is in partnership with Feed the Future Uganda Commodity

Production and Marketing Activity. Every institution selected had an opportunity to test the product.

3.3.3 Order of rotation

At the end of the exercise, our objective was to ensure that each target respondent has a chance to test the product. Since it was one product, we adopted

the monadic testing where all respondents were given the opportunity to test this product.

3.4 Data Collection Procedures, Methods and Instruments

3.4.1 Tool development

We designed one tool encompassing both the feasibility study questions and product test questions. Since there were some questions that were specific to

particular institutions, we further split it into two; one tool was for schools and food service industry while the second tool was for Relief agencies and

Government institutions. These were designed in conjunction with Feed the Future Uganda Commodity Production and Marketing Activity.

3 .3.4 Beans Preparation

Light charcoal stove and bring

water to boil

Soak the product

in hot water for about 15 - 20 minutes such that it can reconstitute

Prepare your ingredients

including cooking oil, onions,

tomatoes green pepper, curry

powder, and any other spices as may be desired

In a pre - heated sauce pan, add

oil, then onions, green pepper , tomatoes, salt

and any other

spices as may be desired. After the spice mixture is ready, add your

reconstituted beans/maize. Add

an appropriate amount of water and leave to boil for 5 - 10 minutes

Thereafter, serve the

sauce with any type of

food.

Questionnaire

This was used to collect data during both the feasibility study capturing current bean consumption, usage, fuel used, constraints with current product, bean

category preferences, preferred nutritional standards, acceptability of a dehydrated pre-cooked bean product, an estimate of size and scope of the proposed

product, acceptability of dehydrated precooked beans and the product test capturing spontaneous thoughts and perceptions towards the product, likes and

dislikes likelihood to purchase and prices.