Federalism - CREBAcreba.ph/pdf/Federalism-ProfOlivar.pdf · Philippines has been left behind...

35

Federalism TUNAY NA PAGBABAGO 25 th CREBA Annual National Convention Baguio City,14 October 2016

Transcript of Federalism - CREBAcreba.ph/pdf/Federalism-ProfOlivar.pdf · Philippines has been left behind...

Federalism T U N A Y N A P A G B A B A G O

2 5 t h C R E B A A n n u a l N a t i o n a l C o n v e n t i o n

B a g u i o C i t y , 1 4 O c t o b e r 2 0 1 6

Presentation Outline

1. How are we doing? 2. Where should we go? 3. How do we get there? 4. Implications for PH real estate sector

Left behind

Country

Rank (1= poorest, 185 = richest)

Singapore 183

Brunei 182

Malaysia 141

Thailand 106

Indonesia 83

Philippines 63

Vietnam 60

Laos 58

Myanmar 55

Cambodia 43

Other Asian countries have progressed steadily, while the Philippines has been left behind by one after another of its neighbors. •2015 Rankings on Gross Domestic Product (GDP) based on purchasing-power-parity (PPP) per Capita. Posted by Global Finance

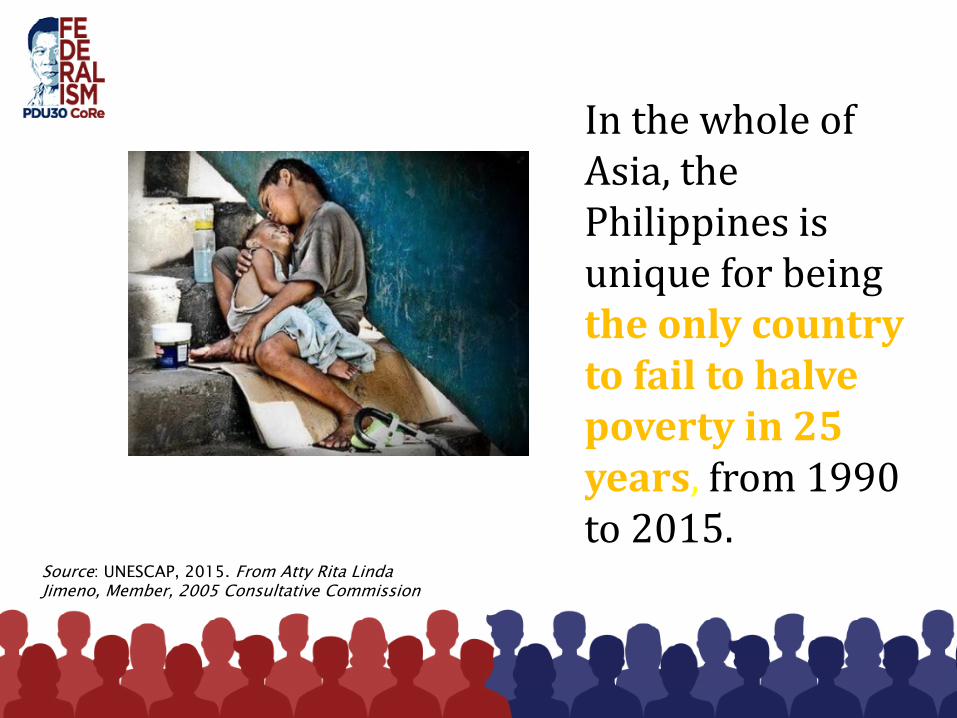

In the whole of Asia, the Philippines is unique for being the only country to fail to halve poverty in 25 years, from 1990 to 2015.

Source: UNESCAP, 2015. From Atty Rita Linda Jimeno, Member, 2005 Consultative Commission

Unsettled times

UNSETTLED POLITICAL SITUATION:

• Insurgency • Moro Rebellion • Social Unrest (due to injustice, poverty, corruption, political

warlords and dynasties, and failed agrarian reform)

HukBaLaHap/HMB CPP/NPA Political Warlords Failed Agrarian Reform

Real GRDP/Capita (in millions PhP) 2009 2010 2011 2012 2013 2014 Average

Region

2009-2014

NCR 162.32 171.44 173.06 181.75 195.07 203.13 181.13

Luzon 45.16 47.24 47.49 48.82 50.60 52.51 48.64

Visayas 37.33 39.53 40.76 41.68 43.35 44.75 41.23

Mindanao 33.79 34.91 35.52 37.67 39.35 41.51 37.12

Average 69.65 73.28 74.21 77.48 82.09 85.48

High 162.32 171.44 173.06 181.75 195.07 203.13

Low 33.79 34.91 35.52 37.67 39.35 41.51

Source: PSA, ChartPoints and Bloomberg

Real GRDP/capita (in millions PhP)

-

50.00

100.00

150.00

200.00

250.00

200

9

201

0

201

1

201

2

201

3

201

4

200

9

201

0

201

1

201

2

201

3

201

4

200

9

201

0

201

1

201

2

201

3

201

4

200

9

201

0

201

1

201

2

201

3

201

4

NCR Luzon Visayas Mindanao

Presentation Outline

1. How are we doing? 2. Where should we go? 3. How do we get there? 4. Implications for PH real estate sector

Change is coming.

Rodrigo Duterte wins on promise of real change

One proposed change: from Unitary to Federal

Malacañan decides how much to give to local

governments.

In Federalism, states can make decisions with little

interference from national government.

What is Federalism?

A form of government where sovereignty is constitutionally shared between a central authority and states or regions National government focuses on national interests such as foreign relations, national security, and monetary policy

Autonomous regions or states will be responsible for delivery of public goods and social services and local economic development.

Constitutional basis

1) EMPOWERMENT : It will empower our citizens

to become more involved in government decisions at the local level. They will be more willing to pay taxes to finance government programs and services that they can directly create and oversee.

AdvAdvantages of “the federal idea”

2) BETTER DECISION-

MAKING : It will improve the ability

of local government executives to quickly make decisions that respond to their unique circumstances. Over time, we will bring up a better class of leadership.

AdvAdvantages of “the federal idea”

3) GREATER

ACCOUNTABILITY: It will bring government

officials closer to their constituencies, strengthening oversight. Over time, platform and performance will replace personality-based politics.

AdvAdvantages of “the federal idea”

4) HEALTHY

COMPETITION: States or regions will have

to compete with each other to attract domestic and foreign trade, investment and credit. Over time, good performers and policies will prevail over bad ones.

AdvAdvantages of “the federal idea”

6) DIVERSITY AMID UNITY: The federal idea ensures a just and enduring framework for peace among the various ethnic, religious, and cultural communities. The legitimate interests of Moros and other indigenous peoples will be addressed and protected.

AdvAdvantages of “the federal idea”

6) DECONGEST METRO MANILA: Manila will become decongested as the different regions catch up in economic growth and employment opportunities. This catching-up will also propel us for the first time towards genuine self-sustaining growth as a country.

AdvAdvantages of “the federal idea”

Presentation Outline

1. How are we doing? 2. Where should we go? 3. How do we get there? 4. Implications for PH real estate sector

Modes of charter change

People’s Initiative Constitutional Convention

Constituent Assembly

x ?

Source: Centrist Democratic Party (CDP)

Advantages of the Federal System of Government

In a federal system of government, states (or

regions) will have the power to exercise taxation and

keep the revenues for themselves, remitting only

their respective contributions to the national government.

CENTRAL

LGU

Rebalancing gov’t responsibilities

• Primary service responsibilities (National)

– What services can only be provided by the National

Government? (e.g. Defense)

• Secondary service responsibilities (Shared)

– What services does the National Government have a

significant interest in but are best delivered by a lower

unit of government? (e.g. Education, Health)

• Tertiary service responsibilities (Local)

– What services are of primary concern to local

communities? (e.g. Policing, Agriculture, Fire Protection)

DAI/Facilitating Public Investment (FPI) Project

22

Redefining taxation and fiscal transfers

• Primary National Government Services <= Federal Tax

• Secondary National Government Services <= Conditional Grants

• Tertiary National Government Services <= Block Grants

• Limited Scope Special Infrastructure Transfers

• Transfers to Improve Fiscal Management DAI/Facilitating Public Investment (FPI) Project

23

Another view on rebalancing

Source: LoGoDeF, 2016

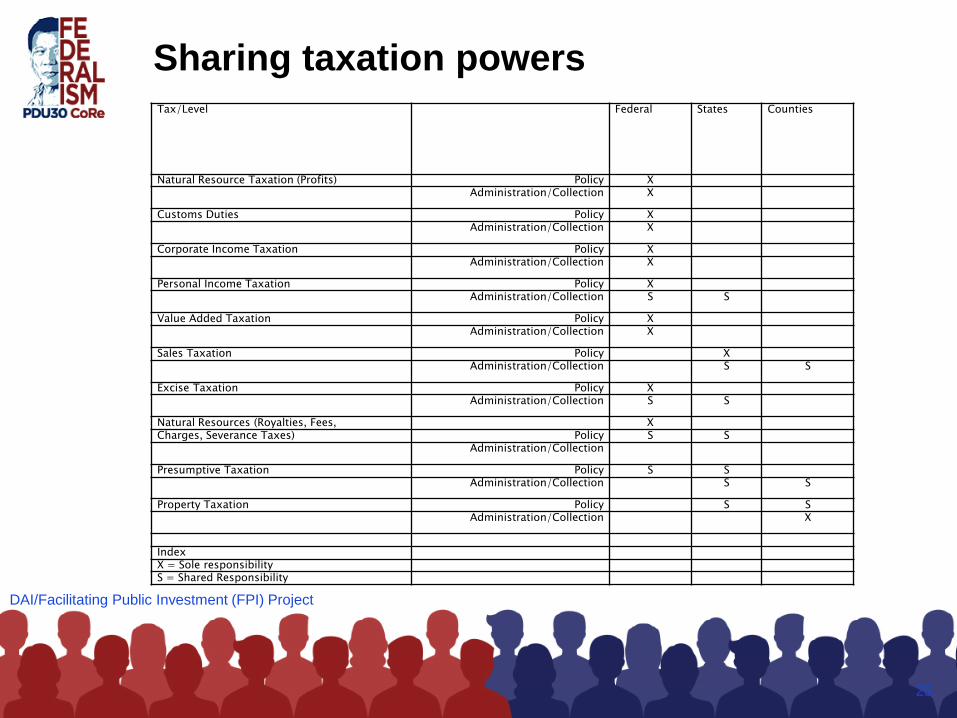

Sharing taxation powers Tax/Level Federal States Counties

Natural Resource Taxation (Profits) Policy X Administration/Collection X

Customs Duties Policy X Administration/Collection X

Corporate Income Taxation Policy X Administration/Collection X

Personal Income Taxation Policy X Administration/Collection S S

Value Added Taxation Policy X Administration/Collection X

Sales Taxation Policy X Administration/Collection S S

Excise Taxation Policy X Administration/Collection S S

Natural Resources (Royalties, Fees, X Charges, Severance Taxes) Policy S S Administration/Collection

Presumptive Taxation Policy S S Administration/Collection S S

Property Taxation Policy S S Administration/Collection X

Index X = Sole responsibility S = Shared Responsibility

DAI/Facilitating Public Investment (FPI) Project

25

Another view on sharing taxation powers

Source: LoGoDeF, 2016

Presentation Outline

1. How are we doing? 2. Where should we go? 3. How do we get there? 4. Implications for PH real estate sector

28

Issues

•Continuing restrictions on land ownership by

foreigners (not just in PH but also in other ASEAN

countries like Indonesia and Myanmar). These may

limit full positive impact from freer cross-border

investment flows post-ASEAN integration.

Legal and

political

•BSP concern that industry is dominated by

conglomerates controlled by less than a dozen

families, most of whom have aggressively borrowed.

Industry

structure •Low-income housing deficit projected by SHDA to hit

5.8 MM by 2030.

•Possible oversupply at the high-end of residential

market. BSP supposed to release new “housing price

index” in 2015 to monitor overheating.

•Poor physical infrastructure hampers proper matching

of property supply and demand.

Supply-

demand

imbalances

Sources: Wall Street Journal; Lamudi; MyProperty.ph

Housing demand & supply

30

Outlook

•PH will lead ASEAN in real estate market growth.

•“There is no truth to the rumor that there will be a

real estate bubble!” – Eduardo Ong, Chair, Board of

Real Estate Service

Philippines

•MM dislodged Madrid to join JLL Top 30 list in 2014.

•From 28th largest city GDP in the world in 2010, MM

will rise to 25th place in 2020 and 18th place in 2030.

•MM far more geared to IT than its regional peers.

Ranked 10th in Tech-Rich Cities global index for

1Q’15, above San Diego, Osaka, Munich, and Beijing.

•MM real estate market has one of the highest

absorption rates in Asia, and is still one of the most

affordable in the world.

Metro Manila

Sources: CBRE 2015 APAC Real Estate Markets Outlook; PWC/ULI Asia Pacific Report 2015; JLL Global 300 Index report , 2014

31

Opportunities (2015)

• Puregold and Vista Land will invest Php 3.5 BN

and PhP 15 BN respectively to expand into

retail over the next 5 years.

• Megaworld has doubled to 20 the number of

township projects in its national portfolio

Investment

niches

• New “business hubs” like the PhP 1.5 BN

development in Palayan City, Nueva Ecija.

• Developers expanding into Cavite, Batangas,

Laguna, and other provincial cities as Metro

Manila becomes saturated.

Provincial cities

• Prospective new office demand from ASEAN

companies expanding into PH

• ASEAN brands entering PH retail market, eg

H&M’s first mall in 2014.

ASEAN

integration

Sources: Wall Street Journal; Lamudi; MyProperty.ph

Regionalization of real estate sector (1)

32

• One international airport per state?

• More seaports on long PH coastline

• Improvement in access infrastructure, eg “last

mile connectivity” from tourist access point to

tourist destination

Infrastructure buildout

• New provincial hubs will drive the creation of

interstate value chains, whether in agricultural

processing, manufacturing, or services sector

• Growth of suburbs

Business expansion

and demographic

shifts

• Will a new constitution allow states to permit

majority land ownership by foreigners?

• FDI policies could then become a competitive

tool of states

Lift foreign investment

restrictions

Regionalization of real estate sector (2)

33

• No more one-size-fits-all national land use code

that is hostile to real estate and commercial

development

• Land use policies become still another

competitive tool of states

Land use policies

and administration

• Strong and autonomous states can provide

credit support to mortgage instruments during

rollout of primary and secondary markets

• The Bangsa Moro state can serve as conduit for

other states into the billion-dollar regional

Islamic finance market

Mortgage finance

market

• More creative policy responses will come from

state- and lower-level housing development

agencies, eg exemption for low-income housing

bonds from state and municipal taxes

Low-cost housing

backlog

Thank you!

Gary B. Olivar Convenor

President Duterte Constitutional Reforms Towards Federalism

(PDu30 CoRe)

![Our [National] Federalism - Yale Law Journal · source: federalism now comes from federal statutes. It is “National Federalism”— statutory federalism, or “intrastatutory”](https://static.fdocuments.us/doc/165x107/5f84f6df3b712117dc60d34f/our-national-federalism-yale-law-journal-source-federalism-now-comes-from-federal.jpg)