FATCA Definitions, Terminology, and Criticisms

14

The Foreign Account Tax Compliance Act (FATCA) FATCA Definitions, Terminology, and Criticisms SESSION 2 Training Programme FATCA for LATAM Firms 23-24 February 2015 (Panama City), 25-26 February 2015 (Santo Domingo) Rodrigo Zepeda Independent Consultant

-

Upload

rodrigo-zepeda-llb-llm-acsi -

Category

Law

-

view

275 -

download

0

Transcript of FATCA Definitions, Terminology, and Criticisms

The Foreign Account Tax Compliance Act (FATCA)

FATCA Definitions, Terminology, and Criticisms

SESSION 2

Training ProgrammeFATCA for LATAM Firms

23-24 February 2015 (Panama City), 25 -26 February 2015 (Santo Domingo)

Rodrigo ZepedaIndependent Consultant

Section 1: FATCA Definitions

Section 2: FATCA Terminology

Section 3: FATCA Criticisms

FATCA DefinitionsSE CT ION 1

3

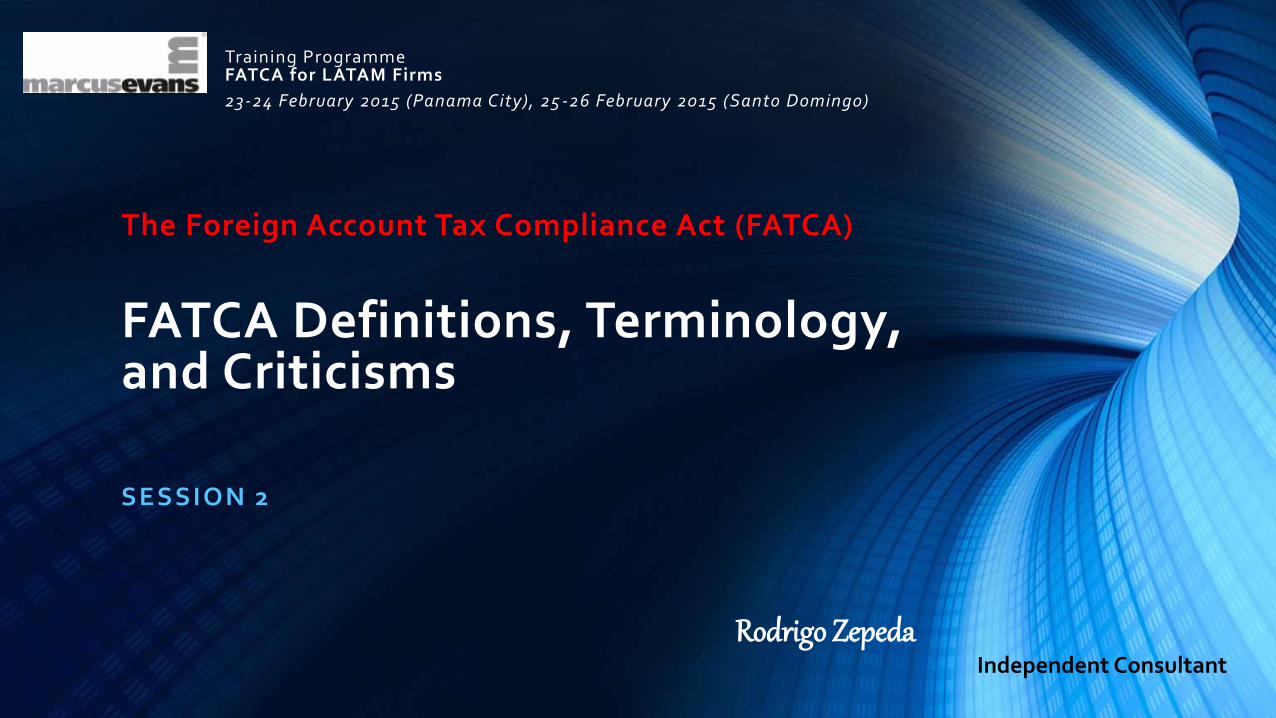

FATCA Definitions

OUTLINE DEFINITIONS (followed by RoundTable Session In-Depth Discussion of Further Definitions)

• FFI: Foreign Financial Institution means a foreign entity that is a financial institution as defined in theUnited States (U.S.) FATCA Final Regulations. It generally includes any one of five categories of FFI,namely specified: (1) depositary institutions; (2) custodial institutions; (3) investment entities; (4)insurance companies or holding companies of insurance companies that issue cash value insurance orannuity contracts; and (5) holding companies and treasury centres of groups that include anotherfinancial entity.

• P-FFI: Participating Foreign Financial Institution means an FFI (including a Reporting Model 2 FFI(RM2-FFI)) that has voluntarily agreed to comply with the terms of a Foreign Financial InstitutionAgreement (FFI Agreement) entered into with the U.S. IRS.

• DC-FFI: Deemed-Compliant Foreign Financial Institution means any of three specified types of FFI: (1)Registered Deemed-Compliant FFI (RDC-FFI); (2) Certified Deemed-Compliant FFI (CDC-FFI); and (3)Owner-Documented FFI (OD-FFI).

• NFFE: Non-Financial Foreign Entity means any non-U.S. entity that is not treated as a FinancialInstitution. NFFEs are sub-classified as either an 'Active NFFE' (A-NFFE) or a 'Passive NFFE' (P-NFFE).

45

FATCA Definitions (continued)

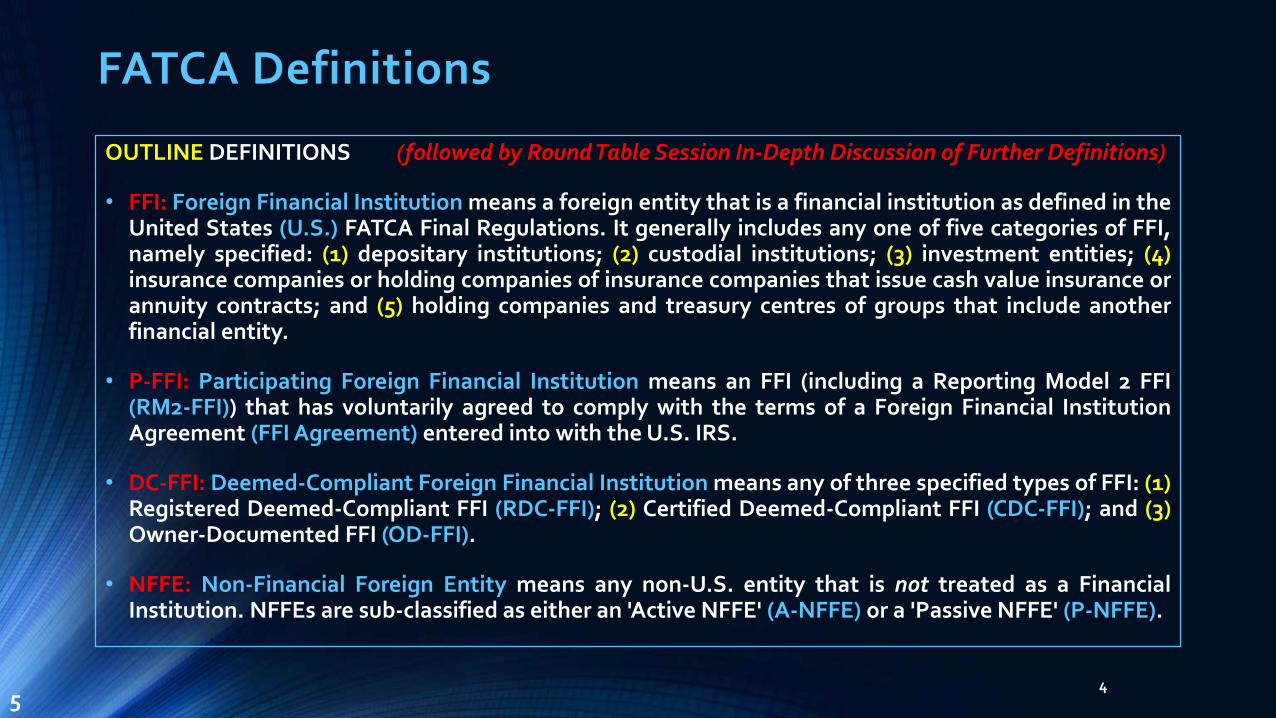

OUTLINE DEFINITIONS

• IRS: Internal Revenue Service means a government agency which is a bureau of the U.S. Departmentof Treasury, and which is the revenue service for the U.S. Federal Government responsible forcollecting taxes and administering the U.S. Internal Revenue Code 1986 (IRC) (as amended).

• GIIN: Global Intermediary Identification Number means a specified and unique identification numberthat is assigned to a P-FFI or a RDC-FFI by the U.S. Internal Revenue Service (IRS).

• GOs: Grandfathered Obligations generally refers to eligible debt instruments (including interestobligations) classified as debt for U.S. tax purposes and with stated maturities issued on or before1 July 2014 (including gross proceeds from the disposition of grandfathered obligations).

• IGA: Intergovernmental Agreement means a partnership agreement based on a ModelIntergovernmental Agreement template, between the U.S. and a FATCA Partner Jurisdiction, whichallows FFIs in FATCA Partner Jurisdictions to either report information on U.S. account holders: (1)directly to their national tax authorities who will then report to the IRS (Model 1 IGA) ; or (2) directlyto the IRS by entering into a FFI Agreement with the IRS (Model 2 IGA).

55

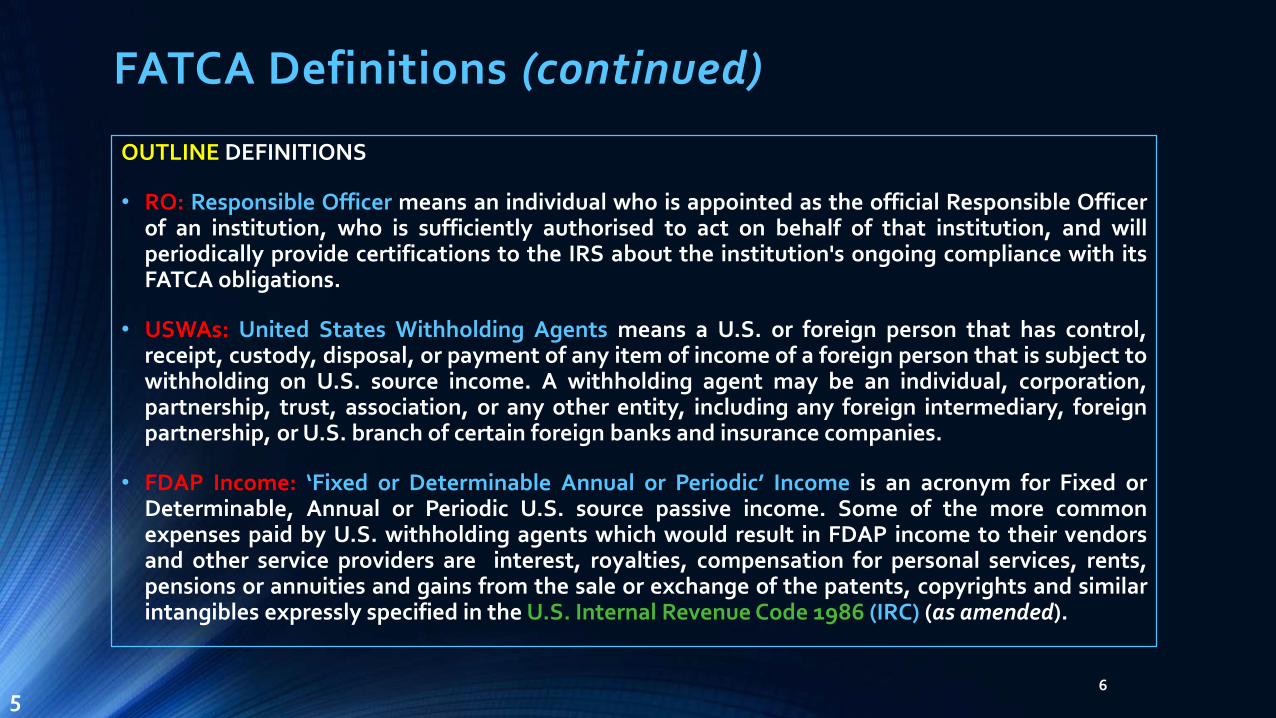

FATCA Definitions (continued)

6

OUTLINE DEFINITIONS

• RO: Responsible Officer means an individual who is appointed as the official Responsible Officerof an institution, who is sufficiently authorised to act on behalf of that institution, and willperiodically provide certifications to the IRS about the institution's ongoing compliance with itsFATCA obligations.

• USWAs: United States Withholding Agents means a U.S. or foreign person that has control,receipt, custody, disposal, or payment of any item of income of a foreign person that is subject towithholding on U.S. source income. A withholding agent may be an individual, corporation,partnership, trust, association, or any other entity, including any foreign intermediary, foreignpartnership, or U.S. branch of certain foreign banks and insurance companies.

• FDAP Income: ‘Fixed or Determinable Annual or Periodic’ Income is an acronym for Fixed orDeterminable, Annual or Periodic U.S. source passive income. Some of the more commonexpenses paid by U.S. withholding agents which would result in FDAP income to their vendorsand other service providers are interest, royalties, compensation for personal services, rents,pensions or annuities and gains from the sale or exchange of the patents, copyrights and similarintangibles expressly specified in the U.S. Internal Revenue Code 1986 (IRC) (as amended).

5

FATCA TerminologySE CT ION 2

7

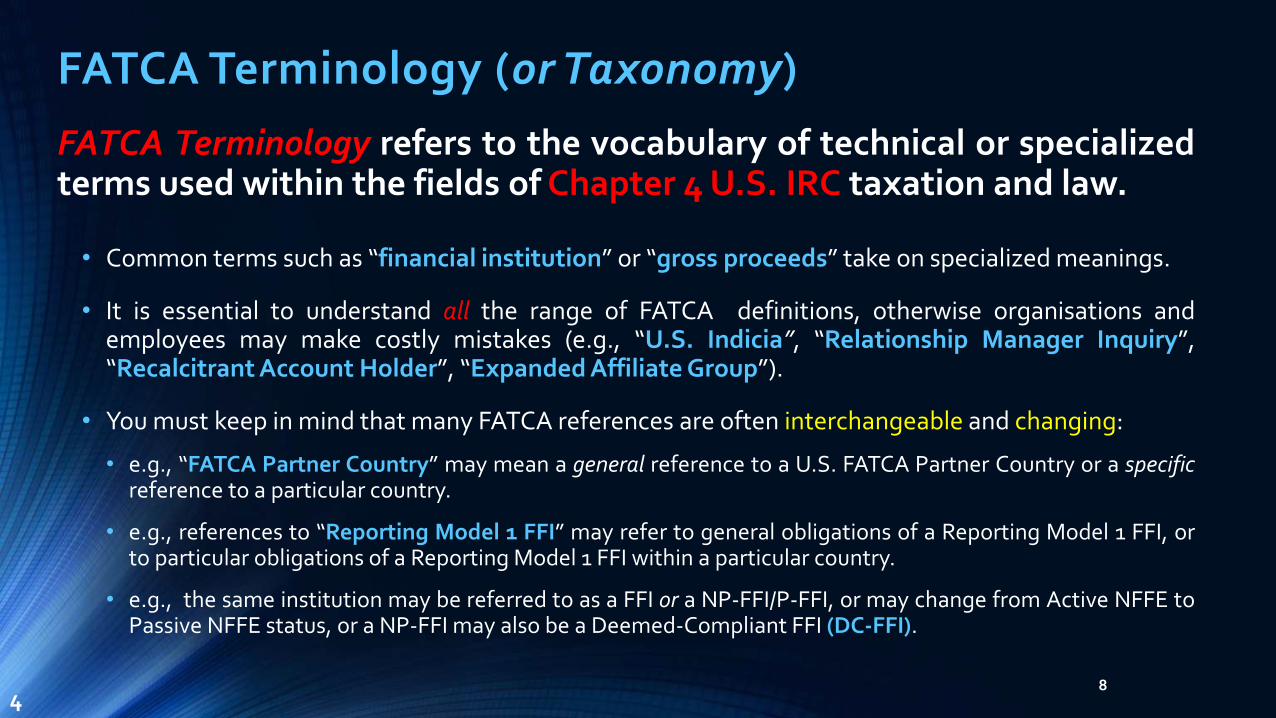

FATCA Terminology (or Taxonomy)

FATCA Terminology refers to the vocabulary of technical or specializedterms used within the fields of Chapter 4 U.S. IRC taxation and law.

• Common terms such as “financial institution” or “gross proceeds” take on specialized meanings.

• It is essential to understand all the range of FATCA definitions, otherwise organisations andemployees may make costly mistakes (e.g., “U.S. Indicia”, “Relationship Manager Inquiry”,“Recalcitrant Account Holder”, “Expanded Affiliate Group”).

• You must keep in mind that many FATCA references are often interchangeable and changing:

• e.g., “FATCA Partner Country” may mean a general reference to a U.S. FATCA Partner Country or a specificreference to a particular country.

• e.g., references to “Reporting Model 1 FFI” may refer to general obligations of a Reporting Model 1 FFI, orto particular obligations of a Reporting Model 1 FFI within a particular country.

• e.g., the same institution may be referred to as a FFI or a NP-FFI/P-FFI, or may change from Active NFFE toPassive NFFE status, or a NP-FFI may also be a Deemed-Compliant FFI (DC-FFI).

84

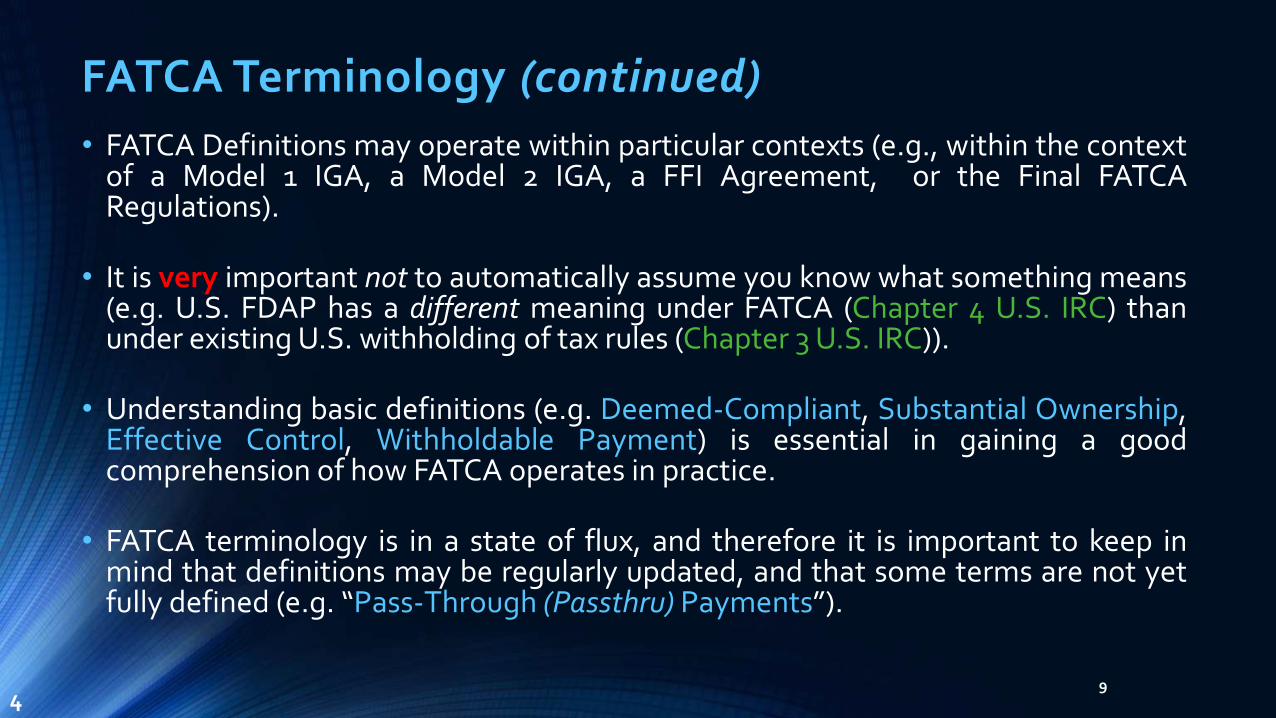

FATCA Terminology (continued)

• FATCA Definitions may operate within particular contexts (e.g., within the contextof a Model 1 IGA, a Model 2 IGA, a FFI Agreement, or the Final FATCARegulations).

• It is very important not to automatically assume you know what something means(e.g. U.S. FDAP has a different meaning under FATCA (Chapter 4 U.S. IRC) thanunder existing U.S. withholding of tax rules (Chapter 3 U.S. IRC)).

• Understanding basic definitions (e.g. Deemed-Compliant, Substantial Ownership,Effective Control, Withholdable Payment) is essential in gaining a goodcomprehension of how FATCA operates in practice.

• FATCA terminology is in a state of flux, and therefore it is important to keep inmind that definitions may be regularly updated, and that some terms are not yetfully defined (e.g. “Pass-Through (Passthru) Payments”).

94

FATCA CriticismsSE CT ION 3

10

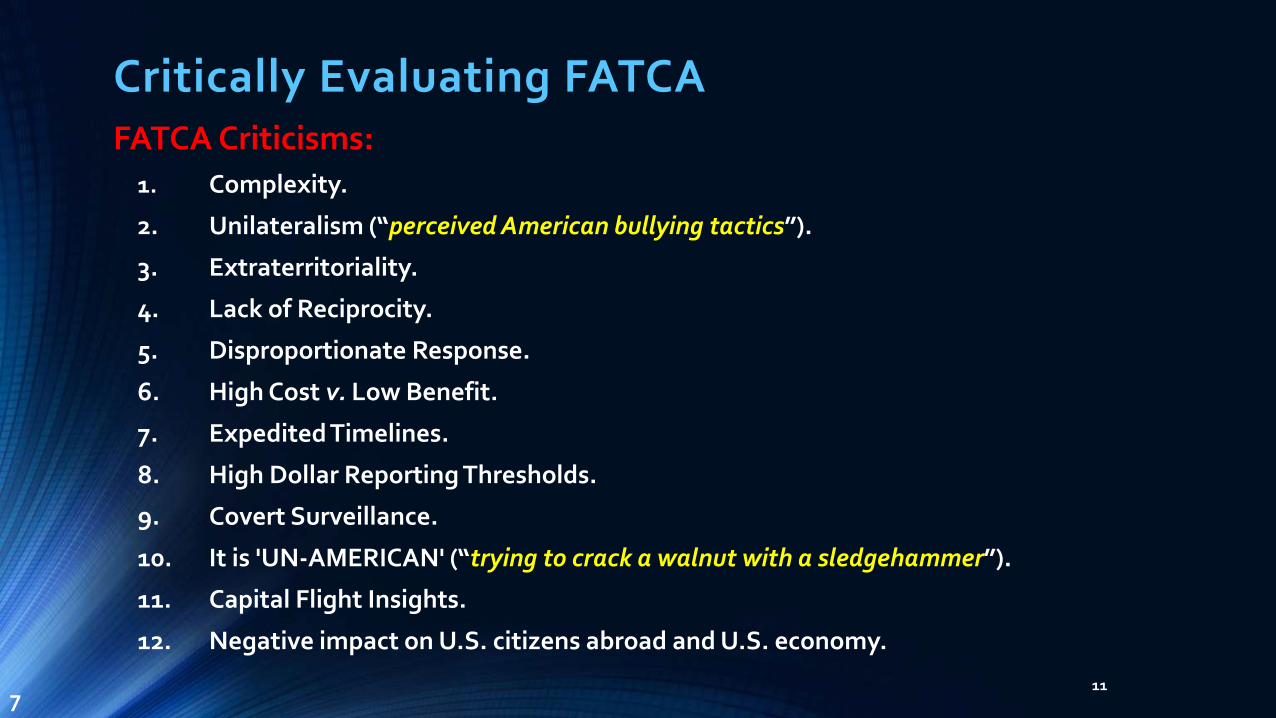

Critically Evaluating FATCAFATCA Criticisms:

1. Complexity.

2. Unilateralism (“perceived American bullying tactics”).

3. Extraterritoriality.

4. Lack of Reciprocity.

5. Disproportionate Response.

6. High Cost v. Low Benefit.

7. Expedited Timelines.

8. High Dollar Reporting Thresholds.

9. Covert Surveillance.

10. It is 'UN-AMERICAN' (“trying to crack a walnut with a sledgehammer”).

11. Capital Flight Insights.

12. Negative impact on U.S. citizens abroad and U.S. economy.

117

12

13

Presentation Information

DECLARATION OF CONFLICTING INTERESTSThe author declares that to the best of his knowledge he has no potential conflicts of interest with respect to the research orauthorship of this presentation.

ABOUT THE PRESENTERRodrigo Zepeda is an independent consultant who specialises in derivatives and financial services law, regulation, andcompliance. He holds a LLM Masters degree in International and Comparative Business Law, has been an Associate of theChartered Institute for Securities and Investment since 2004, and has passed the New York Bar Examination. He has alsopublished widely in leading industry journals such as the Capco Institute’s Journal of Financial Transformation, the Journal ofInternational Banking Law and Regulation, as well as e-books on derivatives law. Noted publications include “Optimizing RiskAllocation for CCPs under the European Market Infrastructure Regulation”; “The ISDA Master Agreement 2012: A MissedOpportunity”; “The ISDA Master Agreement: The Derivatives Risk Management Tool of the 21st Century?”; and “To EU, or not toEU: that is the AIFMD question”.

CONTACT DETAILSEmail: [email protected]: http://www.linkedin.com/in/rodrigozepedaMobile: UK + (0)7592457373

The Foreign Account Tax Compliance Act (FATCA)

FATCA Definitions, Terminology, and Criticisms

SESSION 2

Training ProgrammeFATCA for LATAM Firms

23-24 February 2015 (Panama City), 25 -26 February 2015 (Santo Domingo)

Rodrigo ZepedaIndependent Consultant