FATCA AND TRUSTS - STEP · A Brief Overview of FATCA II. FATCA and Trusts III. ... and securities...

27

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden. FATCA AND TRUSTS JOHN STAPLES BURT, STAPLES & MANER STEP MIAMI – 4 th ANNUAL SUMMIT May 31, 2013 Friday, May 17, 13

Transcript of FATCA AND TRUSTS - STEP · A Brief Overview of FATCA II. FATCA and Trusts III. ... and securities...

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

FATCA AND TRUSTS

JOHN STAPLESBURT, STAPLES & MANER

STEP MIAMI – 4th ANNUAL SUMMITMay 31, 2013

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

2

Agenda

I. A Brief Overview of FATCAII. FATCA and TrustsIII. FATCA AlternativesIV. Implementation Considerations

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

3

FATCA as a Reporting Regime FATCA stands for the “Foreign Account Tax

Compliance Act” which was incorporated into the HIRE Act that became law on March 18, 2010. Final FATCA regulations (“Regulations”) – Jan. 17, 2013

The goal of FATCA is to require foreign financial institutions (“FFIs”) and non-financial foreign entities (“NFFEs”) to provide information to the IRS identifying U.S. persons invested in non-U.S. bank and securities accounts. In Model 1 “intergovernmental agreement” (“IGA”)

jurisdictions the reporting goes to the local government for exchange with the IRS.

The policy of FATCA is to reduce U.S. tax evasion by improving the information available to the IRS about the offshore accounts of U.S. persons.

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

FATCA’s Teeth = Withholding FATCA’s lever to achieve this goal is a

NEW 30% withholding tax levied on “withholdable payments” made to non-participating FFIs and NFFEs.

“Withholdable payments” include all U.S. source income (“FDAP”) and gross proceeds from the sale or disposition of any property of a type that can produce interest or dividends from U.S. sources.

Withholding may also apply to non-U.S. source payments because of the “passthru payment” concept (reserved in the Regulations).

4

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

5

FFIs Broad definition that includes any non-

U.S. entity that:Accepts deposits;Holds financial assets for the account of

others;Acts as an “investment entity;” or,Engages in certain insurance businesses.

The “investment entity” concept is particularly important with regard to the proper FATCA classification

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

6

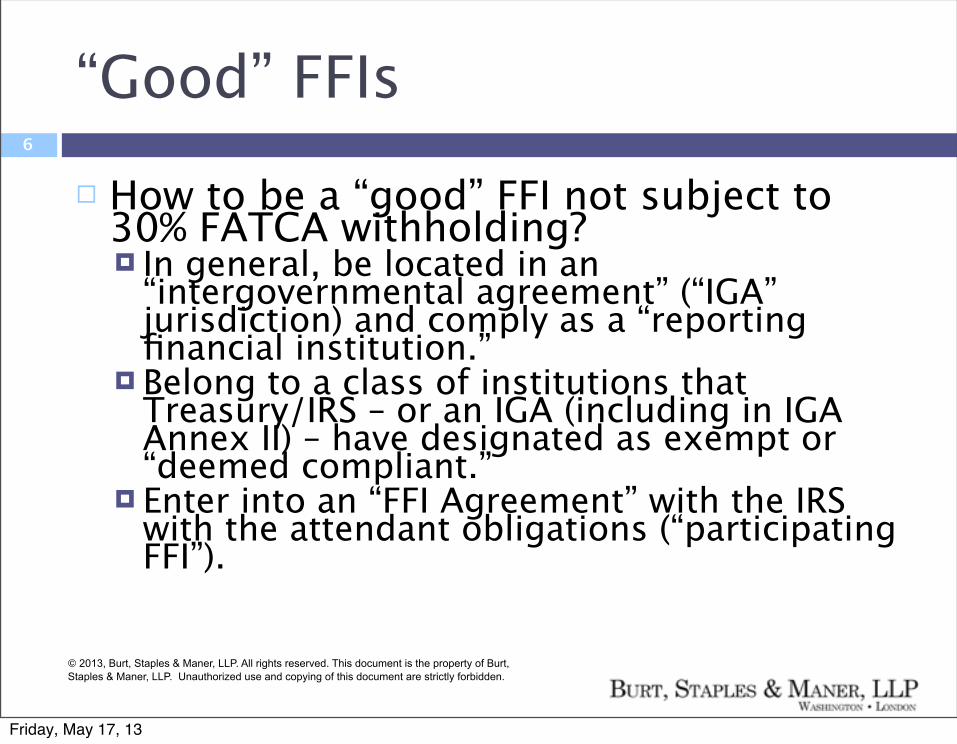

“Good” FFIs How to be a “good” FFI not subject to

30% FATCA withholding? In general, be located in an

“intergovernmental agreement” (“IGA” jurisdiction) and comply as a “reporting financial institution.”

Belong to a class of institutions that Treasury/IRS – or an IGA (including in IGA Annex II) – have designated as exempt or “deemed compliant.”

Enter into an “FFI Agreement” with the IRS with the attendant obligations (“participating FFI”).

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

7

NFFEs Non-financial Foreign Entities (“NFFEs”) are non-U.S.

entities that are not FFIs. Under the Regulations, the goal is to find

“substantial U.S. owners” of these entities. “Substantial” means >10% U.S. owners of non-U.S.

corporations or partnerships and >10% beneficiaries of non-U.S. trusts.

A U.S. grantor of a grantor trust is always considered a “substantial U.S. owner.”

Under the IGAs, identify any “controlling persons” who are U.S. (an AML/KYC concept based on local FATF implementation).

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

8

“Good” NFFEs How to be a “good” NFFE not subject to

30% FATCA withholding: Belong to a class of NFFEs that Treasury/IRS or

an IGA designate as per se “good” and not subject to FATCA withholding;

Engage in an “active business”; Certify to the withholding agent that the NFFE

has no substantial (or controlling) U.S. owners; or

Provide the names, addresses, and U.S. taxpayer identification numbers (“TINs”) of substantial (or controlling) U.S. owners to be reported to the IRS.

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

Why Should You Care About FATCA? If You Are a Trust/PIC Service Provider (e.g.,

Trust Company: It is highly likely that you will be considered a

financial institution. That means that you have substantial new due

diligence, withholding and reporting obligations. Failure to meet these obligations can lead to

withholding on all U.S. source amounts paid to you, penalties and significant reputational risk.

If You Provide Advice To Trusts (e.g., Investment Advisors): Same results as for trust service providers.

9

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

Why Should You Care About FATCA? If you are a Trust or PIC:

If such entities are actively managed, they will be considered FFIs and must either enter into agreements with the IRS or satisfy one of the alternative regimes whereby a trust service provider or withholding agent takes on FATCA responsibilities for them.

If they are not so managed, they must provide certifications to withholding agents that they do not have substantial U.S. owners or provide information regarding such owners or face FATCA withholding.

In either case, new documentation and information must be provided to avoid FATCA withholding.

If you are a Trust/PIC Advisor: Attorneys and accountants providing tax advice to affected

entities must be familiar with highly technical rules governing the respective obligations of trusts/PICs, trust service providers, and withholding agents.

10

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

“Investment Entity” – Providing

The investment entity definition has three parts, two of which are of primary interest to trusts and trust service providers.

First, a foreign entity is an “investment entity” and hence an FFI if it conducts as a business any of the of following activities or operations “for or on behalf of a customer” – Trading in money market instruments (checks, bills,

[CDs], derivatives, etc.); foreign currency; foreign exchange, interest rate and index instruments; transferable securities; or commodity futures;

Individual or collective portfolio management; Otherwise investing, administering, or managing

11

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

“Investment Entity” – Providing

Any entity providing services to trusts will satisfy the “for or on behalf of a customer” part of the definition.

Accordingly, it is crucial to determine if any of the listed activities and/or operations are being performed for trusts or other passive investment vehicles.

If yes, then the service provider is a “financial institution” even if it typically would not consider itself as such.

12

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

“Investment Entity” –

Second, a foreign entity is considered an FFI if “the entity’s gross income is primarily

attributable to investing, reinvesting or trading in financial assets …and the entity is managed by a [bank, custodial institution or insurance company] OR [an entity described above]….An entity is managed by another entity if the managing entity performs directly or through another third party service provider, any of the activities [described above] on behalf of the managed entity.

13

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

“Investment Entity” – The “Managed by” Demarcation The “managed by” concept essentially

determines which trusts and other passive investment vehicles are FFIs and which are NFFEs. If the trust is “managed by” another entity,

then it is an FFI in its own right. If the trust is not so managed, then it is an

NFFE. Why did Treasury take this approach?

To essentially force the more sophisticated service provider into taking on the FATCA

14

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

Alt. 1: Certified Sponsored Entity A “sponsoring entity” (e.g., a trust service

provider) can agree to perform all due diligence, withholding, reporting, and other requirements that the “sponsored entity” (e.g. a trust) otherwise would have to do. The sponsored entity may have no more than 20

individual owners of its debt and equity (other than certain FATCA-compliant FFIs) – that is, this works for smaller trusts and passive investment vehicles.

The sponsoring entity must register with the IRS and get a “global intermediary identification

15

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

Alt. 2: Registered DC Sponsored

The registered deemed-compliant requirements are largely the same as for the certified variety of sponsored entity EXCEPT: The “20 individual owners” rule does not

apply (so it can apply to larger trusts or passive entities);

At present it appears that the sponsored entity must register with the IRS and get a GIIN although the IRS apparently has this under consideration; and

16

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

Alt. 3: Owner Documented FFIs

Either the managing entity or another “designated withholding agent” (“DWA”) such as a bank or custodian can agree to collect all underlying owner information (e.g, all grantor and beneficiaries of trusts) and report annually on any U.S. persons to the IRS.

However, there are a large number of requirements and special rules associated with this alternative that makes it more complicated than the sponsored entity

17

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

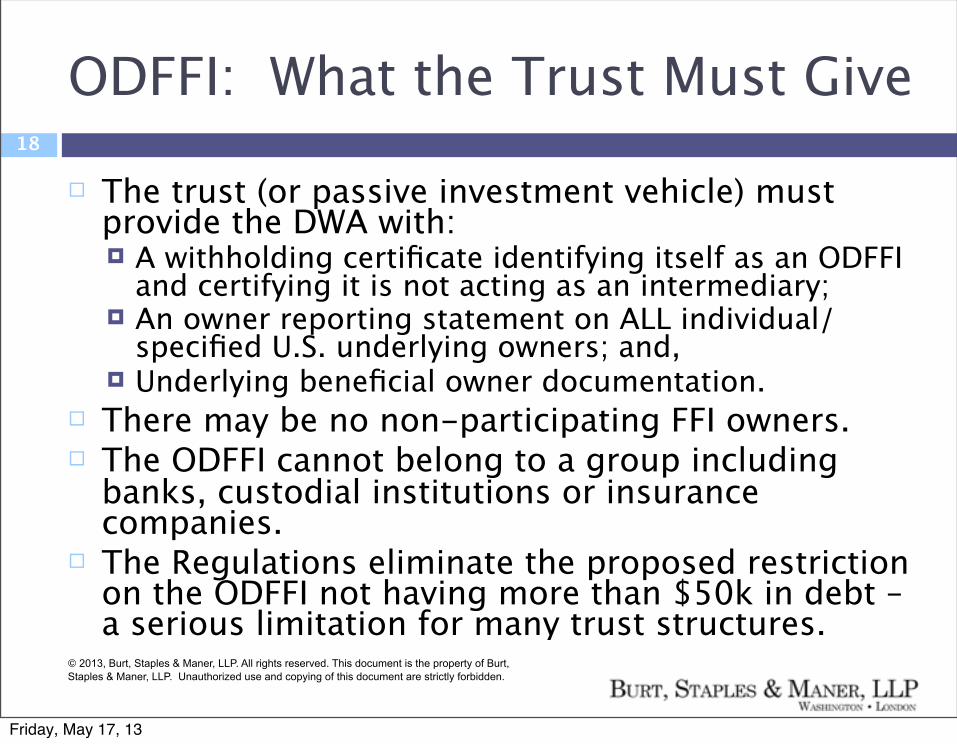

ODFFI: What the Trust Must Give

The trust (or passive investment vehicle) must provide the DWA with: A withholding certificate identifying itself as an ODFFI

and certifying it is not acting as an intermediary; An owner reporting statement on ALL individual/

specified U.S. underlying owners; and, Underlying beneficial owner documentation.

There may be no non-participating FFI owners. The ODFFI cannot belong to a group including

banks, custodial institutions or insurance companies.

The Regulations eliminate the proposed restriction on the ODFFI not having more than $50k in debt – a serious limitation for many trust structures.

18

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

ODFFI: What the Trust Must Give

Instead of the owner reporting information and underlying documentation, the ODFFI can provide the DWA with a letter from a U.S. audit firm confirming that the ODFFI meets the Regulatory requirements. Must be signed no more than 4 years before a

payment. DWA can rely on it until “reason to know” it is

incorrect. If there are U.S. owners, then the ODFFI must

supply an owner reporting statement only for them and W-9s.

19

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

ODFFI – Preexisting Account

An DWA can forgo the normal documentation rules for accounts opened before 12/31/13 and for payments prior to 1/1/17 – thus this is a transitional rule only. Rely on AML/KYC information that has been

collected within last four years if it is sufficient to: (1) Identify U.S. and individual direct/indirect

owners and (2) Report with respect to U.S. owners.

Must have no knowledge/reason to know that

20

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

Do the Investment Entity

There has been some question whether an IGA entity can serve as either a sponsoring entity or a DWA under the ODFFI rules.

It appears that this is possible in Model 1 IGA jurisdictions given that the definition of “reporting financial institution” includes the deemed compliant definitions in the Regulations. IRS officials have publicly agreed to this. Caution: All Regulatory requirements must

be met even if in an IGA jurisdiction.

21

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

Determining “Substantial

A “substantial U.S. owner” typically owns more than 10% of the NFFE. For trusts, every grantor is a substantial

owner and any more than 10% beneficiary is a substantial owner.

Attribution rules apply in determining the thresholds INCLUDING the section 267 attribution rules for family relations.

If a grantor trust is wholly owned by U.S. persons then only those persons, and not the beneficiaries, are considered to have an interest in the trust.

22

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

“Substantial Owners” (Cont’d) The Regulations provide that only two kinds of

trust interests are relevant for determining whether reporting applies: Discretionary Distribution Test – the person

received (directly or indirectly) only discretionary distributions and the FMV exceeds either 10% of the total value of all annual distributions or 10% of the value of the assets held by the trust at year end.

Mandatory Distribution Test – the person is entitled to receive only mandatory distributions and the value of the interest in the trust exceeds 10% of the value of all trust assets.

Combination Test – the person is entitled to either of the above kinds of distribution and either is exceeded.

23

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

FATCA Classification of “Active

Trust Engaged in Profit-Making Business While such an entity may have “trust” in its name,

it is taxed and treated as a business entity for U.S. tax purposes.

Treat as active NFFE (no owner documentation required)

Trust Owns a Company with a Profit-Making Business Treat company as active NFFE. Trust owns stock and should be treated either as

a passive NFFE or an FFI depending upon

24

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

FATCA Classification of “Active

Trust Owns Tangible Property For example, personal property, artwork,

private jet, etc. Treat as passive NFFE.

Trust Owns Company that Owns Tangible Property Company is a passive NFFE. Trust can be either a passive NFFE or an FFI

depending upon circumstances.

25

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

Some Final Thoughts Multinational FIs need to determine how they are

interacting with trusts in each business line. For example, custody/banking versus providing

managerial services. An appropriate communication/customer contact

strategy should be strongly considered since many of the options discussed above require significant interaction with trust customers.

Remember that there may be business opportunities involved.

The following systems and procedures will need to be revised and updated for FATCA: (1) client on-boarding; (2) due diligence and document

26

Friday, May 17, 13

© 2013, Burt, Staples & Maner, LLP. All rights reserved. This document is the property of Burt, Staples & Maner, LLP. Unauthorized use and copying of this document are strictly forbidden.

27

Contact Details John M. Staples

[email protected] +1 202 783-1500

Please visit our websites for up-to-date information on FATCA: www.bsmlegal.com or www.cticompliance.com.

Friday, May 17, 13