FAQ-6

3

In 2012 research firm Celent reported that only 4 percent of online banking customers at the top 50 banks were active users of personal financial management (PFM). Selling you a product that no one will use is not a sustainable business model. MX believes that PFM is dead. MX has pioneered the move into a new category, data-driven money management (DMM). DMM keeps your users coming back, whether analyzing their spending or cash flow, revising monthly budgets or charting progress toward a long term financial goal. We accomplish this with a world-class user interface, multi-source aggregation that ensures constant connectivity to one's financial data and superior cleansing and categorization of transactions, providing an accurate view of one's financial picture. Adoption How does MX define and measure adoption? We identify the percentage of users created in MX out of total online banking users. In the past many FIs utilized a tabbed approach where users opted in but MX is driving more deployments where all users are pre-loaded, enabling them to immediately start using data-driven money management. This takes adoption off the table as a worry since everyone can immediately use DMM. Mountain America Credit Union (MACU) experienced great success through a full integration, where all users were pre-loaded and an MX mini widget — sharing a user's spending breakdown — was integrated into the main online banking homepage to supercharge engagement. Tabbed PFM was almost hidden and siloed whereas data-driven money management is front and center. How Do You Measure Adoption And Engagement? FAQ:

-

Upload

jeff-meredith -

Category

Documents

-

view

45 -

download

0

Transcript of FAQ-6

In 2012 research firm Celent reported that only 4 percent of online banking customers at the top 50 banks were active users of personal financial management (PFM). Selling you a product that no one will use is not a sustainable business model. MX believes that PFM is dead.

MX has pioneered the move into a new category, data-driven money management (DMM). DMM keeps your users coming back, whether analyzing their spending or cash flow, revising monthly budgets or charting progress toward a long term financial goal. We accomplish this with a world-class user interface, multi-source aggregation that ensures constant connectivity to one's financial data and superior cleansing and categorization of transactions, providing an accurate view of one's financial picture.

Adoption

How does MX define and measure adoption? We identify the percentage of users created in MX out of total online banking users.

In the past many FIs utilized a tabbed approach where users opted in but MX is driving more deployments where all users are pre-loaded, enabling them to immediately start using data-driven money management. This takes adoption off the table as a worry since everyone can immediately use DMM.

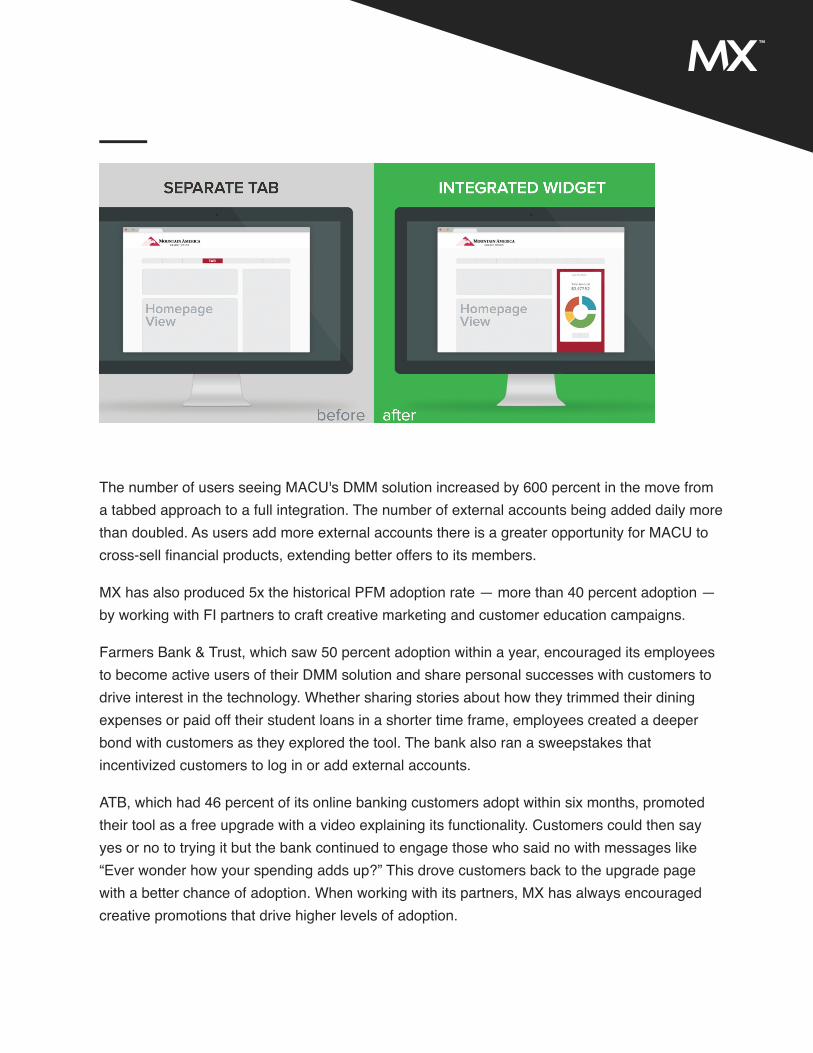

Mountain America Credit Union (MACU) experienced great success through a full integration, where all users were pre-loaded and an MX mini widget — sharing a user's spending breakdown — was integrated into the main online banking homepage to supercharge engagement. Tabbed PFM was almost hidden and siloed whereas data-driven money management is front and center.

How Do You Measure Adoption And Engagement?

FAQ:

The number of users seeing MACU's DMM solution increased by 600 percent in the move from a tabbed approach to a full integration. The number of external accounts being added daily more than doubled. As users add more external accounts there is a greater opportunity for MACU to cross-sell financial products, extending better offers to its members.

MX has also produced 5x the historical PFM adoption rate — more than 40 percent adoption — by working with FI partners to craft creative marketing and customer education campaigns.

Farmers Bank & Trust, which saw 50 percent adoption within a year, encouraged its employees to become active users of their DMM solution and share personal successes with customers to drive interest in the technology. Whether sharing stories about how they trimmed their dining expenses or paid off their student loans in a shorter time frame, employees created a deeper bond with customers as they explored the tool. The bank also ran a sweepstakes that incentivized customers to log in or add external accounts.

ATB, which had 46 percent of its online banking customers adopt within six months, promoted their tool as a free upgrade with a video explaining its functionality. Customers could then say yes or no to trying it but the bank continued to engage those who said no with messages like “Ever wonder how your spending adds up?” This drove customers back to the upgrade page with a better chance of adoption. When working with its partners, MX has always encouraged creative promotions that drive higher levels of adoption.

Engagement

Banks commonly use a 60 or 90 day term when referring to active users and engagement. Here are some of the ways we measure engagement at MX:

What percentage of users are going into online banking and visiting the master widget (or opening up MoneyDesktop in a tab)? What percentage of users are aggregating external, or held away, accounts? This is a crucial piece for FIs wishing to view a customer's held away accounts — be it a mortgage, credit card or auto loan — and compete for that business.

Aggregated accounts per user. If a user on the MX platform has added at least one external account, we find that they average 5.2 accounts. This suggests that once you get users to aggregate, they don't just stop at one account and call it quits; it's easy to make the addition of external accounts a repeatable process. The more successful you are in getting your users to add accounts, the greater opportunity you'll have to win their business.

Sessions by product type, be it master widget, mobile or alerts widget.

Feature visits: This would include visits across accounts, transactions, spending, budgets, trends, debts, net worth and goals. FIs are eager to see which features are proving most helpful for their account holders in managing their financial lives.

Monthly active users, defined as users who've loaded a piece of MoneyDesktop, be it mobile app or widgets. Some FIs seek to measure engagement within the tighter monthly time frame vs using 60 or 90 day intervals.

Sessions per active user per month. While overall engagement levels are important, even a smaller number of power users who are hooked on DMM can speak to the success of your implementation. Javelin Strategy & Research notes that DMM is a "magnet for consumers who monitor and manage their finances vigilantly. That list is topped by Moneyhawks, who actively use online banking, mobile banking and pay bills through their primary FI." Moneyhawks represent the most profitable account holders for an FI; more than half of the consumers who use bank money management tools are Moneyhawks. While they only account for 13 percent of the population, Moneyhawks control a staggering 41 percent of deposits and a third of investable assets.

Total users and total mobile users. FIs frequently compare online vs mobile usage as they seek to understand their customers' preferred channels and how they are trending over time.

In 2012 research firm Celent reported that only 4 percent of online banking customers at the top 50 banks were active users of personal financial management (PFM). Selling you a product that no one will use is not a sustainable business model. MX believes that PFM is dead.

MX has pioneered the move into a new category, data-driven money management (DMM). DMM keeps your users coming back, whether analyzing their spending or cash flow, revising monthly budgets or charting progress toward a long term financial goal. We accomplish this with a world-class user interface, multi-source aggregation that ensures constant connectivity to one's financial data and superior cleansing and categorization of transactions, providing an accurate view of one's financial picture.

Adoption

How does MX define and measure adoption? We identify the percentage of users created in MX out of total online banking users.

In the past many FIs utilized a tabbed approach where users opted in but MX is driving more deployments where all users are pre-loaded, enabling them to immediately start using data-driven money management. This takes adoption off the table as a worry since everyone can immediately use DMM.

Mountain America Credit Union (MACU) experienced great success through a full integration, where all users were pre-loaded and an MX mini widget — sharing a user's spending breakdown — was integrated into the main online banking homepage to supercharge engagement. Tabbed PFM was almost hidden and siloed whereas data-driven money management is front and center.

The number of users seeing MACU's DMM solution increased by 600 percent in the move from a tabbed approach to a full integration. The number of external accounts being added daily more than doubled. As users add more external accounts there is a greater opportunity for MACU to cross-sell financial products, extending better offers to its members.

MX has also produced 5x the historical PFM adoption rate — more than 40 percent adoption — by working with FI partners to craft creative marketing and customer education campaigns.

Farmers Bank & Trust, which saw 50 percent adoption within a year, encouraged its employees to become active users of their DMM solution and share personal successes with customers to drive interest in the technology. Whether sharing stories about how they trimmed their dining expenses or paid off their student loans in a shorter time frame, employees created a deeper bond with customers as they explored the tool. The bank also ran a sweepstakes that incentivized customers to log in or add external accounts.

ATB, which had 46 percent of its online banking customers adopt within six months, promoted their tool as a free upgrade with a video explaining its functionality. Customers could then say yes or no to trying it but the bank continued to engage those who said no with messages like “Ever wonder how your spending adds up?” This drove customers back to the upgrade page with a better chance of adoption. When working with its partners, MX has always encouraged creative promotions that drive higher levels of adoption.

Engagement

Banks commonly use a 60 or 90 day term when referring to active users and engagement. Here are some of the ways we measure engagement at MX:

What percentage of users are going into online banking and visiting the master widget (or opening up MoneyDesktop in a tab)? What percentage of users are aggregating external, or held away, accounts? This is a crucial piece for FIs wishing to view a customer's held away accounts — be it a mortgage, credit card or auto loan — and compete for that business.

Aggregated accounts per user. If a user on the MX platform has added at least one external account, we find that they average 5.2 accounts. This suggests that once you get users to aggregate, they don't just stop at one account and call it quits; it's easy to make the addition of external accounts a repeatable process. The more successful you are in getting your users to add accounts, the greater opportunity you'll have to win their business.

Sessions by product type, be it master widget, mobile or alerts widget.

Feature visits: This would include visits across accounts, transactions, spending, budgets, trends, debts, net worth and goals. FIs are eager to see which features are proving most helpful for their account holders in managing their financial lives.

Monthly active users, defined as users who've loaded a piece of MoneyDesktop, be it mobile app or widgets. Some FIs seek to measure engagement within the tighter monthly time frame vs using 60 or 90 day intervals.

Sessions per active user per month. While overall engagement levels are important, even a smaller number of power users who are hooked on DMM can speak to the success of your implementation. Javelin Strategy & Research notes that DMM is a "magnet for consumers who monitor and manage their finances vigilantly. That list is topped by Moneyhawks, who actively use online banking, mobile banking and pay bills through their primary FI." Moneyhawks represent the most profitable account holders for an FI; more than half of the consumers who use bank money management tools are Moneyhawks. While they only account for 13 percent of the population, Moneyhawks control a staggering 41 percent of deposits and a third of investable assets.

Total users and total mobile users. FIs frequently compare online vs mobile usage as they seek to understand their customers' preferred channels and how they are trending over time.

In 2012 research firm Celent reported that only 4 percent of online banking customers at the top 50 banks were active users of personal financial management (PFM). Selling you a product that no one will use is not a sustainable business model. MX believes that PFM is dead.

MX has pioneered the move into a new category, data-driven money management (DMM). DMM keeps your users coming back, whether analyzing their spending or cash flow, revising monthly budgets or charting progress toward a long term financial goal. We accomplish this with a world-class user interface, multi-source aggregation that ensures constant connectivity to one's financial data and superior cleansing and categorization of transactions, providing an accurate view of one's financial picture.

Adoption

How does MX define and measure adoption? We identify the percentage of users created in MX out of total online banking users.

In the past many FIs utilized a tabbed approach where users opted in but MX is driving more deployments where all users are pre-loaded, enabling them to immediately start using data-driven money management. This takes adoption off the table as a worry since everyone can immediately use DMM.

Mountain America Credit Union (MACU) experienced great success through a full integration, where all users were pre-loaded and an MX mini widget — sharing a user's spending breakdown — was integrated into the main online banking homepage to supercharge engagement. Tabbed PFM was almost hidden and siloed whereas data-driven money management is front and center.

The number of users seeing MACU's DMM solution increased by 600 percent in the move from a tabbed approach to a full integration. The number of external accounts being added daily more than doubled. As users add more external accounts there is a greater opportunity for MACU to cross-sell financial products, extending better offers to its members.

MX has also produced 5x the historical PFM adoption rate — more than 40 percent adoption — by working with FI partners to craft creative marketing and customer education campaigns.

Farmers Bank & Trust, which saw 50 percent adoption within a year, encouraged its employees to become active users of their DMM solution and share personal successes with customers to drive interest in the technology. Whether sharing stories about how they trimmed their dining expenses or paid off their student loans in a shorter time frame, employees created a deeper bond with customers as they explored the tool. The bank also ran a sweepstakes that incentivized customers to log in or add external accounts.

ATB, which had 46 percent of its online banking customers adopt within six months, promoted their tool as a free upgrade with a video explaining its functionality. Customers could then say yes or no to trying it but the bank continued to engage those who said no with messages like “Ever wonder how your spending adds up?” This drove customers back to the upgrade page with a better chance of adoption. When working with its partners, MX has always encouraged creative promotions that drive higher levels of adoption.

Engagement

Banks commonly use a 60 or 90 day term when referring to active users and engagement. Here are some of the ways we measure engagement at MX:

What percentage of users are going into online banking and visiting the master widget (or opening up MoneyDesktop in a tab)? What percentage of users are aggregating external, or held away, accounts? This is a crucial piece for FIs wishing to view a customer's held away accounts — be it a mortgage, credit card or auto loan — and compete for that business.

Aggregated accounts per user. If a user on the MX platform has added at least one external account, we find that they average 5.2 accounts. This suggests that once you get users to aggregate, they don't just stop at one account and call it quits; it's easy to make the addition of external accounts a repeatable process. The more successful you are in getting your users to add accounts, the greater opportunity you'll have to win their business.

Sessions by product type, be it master widget, mobile or alerts widget.

Feature visits: This would include visits across accounts, transactions, spending, budgets, trends, debts, net worth and goals. FIs are eager to see which features are proving most helpful for their account holders in managing their financial lives.

Monthly active users, defined as users who've loaded a piece of MoneyDesktop, be it mobile app or widgets. Some FIs seek to measure engagement within the tighter monthly time frame vs using 60 or 90 day intervals.

Sessions per active user per month. While overall engagement levels are important, even a smaller number of power users who are hooked on DMM can speak to the success of your implementation. Javelin Strategy & Research notes that DMM is a "magnet for consumers who monitor and manage their finances vigilantly. That list is topped by Moneyhawks, who actively use online banking, mobile banking and pay bills through their primary FI." Moneyhawks represent the most profitable account holders for an FI; more than half of the consumers who use bank money management tools are Moneyhawks. While they only account for 13 percent of the population, Moneyhawks control a staggering 41 percent of deposits and a third of investable assets.

Total users and total mobile users. FIs frequently compare online vs mobile usage as they seek to understand their customers' preferred channels and how they are trending over time.