Fannie Mae DESKTOP UNDERWRITER LOAN...

14

DESKTOP UNDERWRITER LOAN PROSPECTOR 1. PRODUCT DESCRIPTION • Conventional Conforming fixed rate mortgage • DU Version 9.2 • 10 to 30 year term in annual increments • Fully amortizing • Qualified Mortgage (QM) Safe Harbor loans are permitted • Qualified Mortgage (QM) Rebuttable Presumption loans are permitted –see the Qualified Mortgage (QM) Rebuttable Presumption section for requirements. • Conventional Conforming fixed rate mortgage • 10 to 30 year term in annual increments • Fully amortizing • Qualified Mortgage (QM) Safe Harbor loans are permitted • Qualified Mortgage (QM) Rebuttable Presumption loans are permitted –see the Qualified Mortgage (QM) Rebuttable Presumption section for requirements. 2. INDEX 3. MARGIN 4. ANNUAL ADJUSTMENT 5. LIFE CAP 6. RATE AT ADJUSTMENT 7. TEMPORARY BUYDOWN 8. QUALIFYING RATE AND RATIOS Qualifying Rate • Qualify using the note rate Ratios • DU Approve/Eligible – Follow DU Qualifying Rate • Qualify using the note rate Ratios • LP Accept – 45% DTI 9. TYPES OF FINANCING Please note that this is not a client offer or solicitation for all loan products listed. All loans submitted for purchase to Stockton Mortgage must be eligible for purchase by Stockton Mortgage and be in full compliance with the Stockton Mortgage Loan Product Matrix, Agency Selling Guide and Client Contract for each approved client. Fannie Mae Purchase Mortgage Rate & Term Refinance (Limited Cash-Out Refinance) • Loans submitted to LP when the previous mortgage was a purchase money transaction • Existing mortgage must be seasoned at least 120 days, measured from previous note date to subject note date • Loan amount may include: • Pay off the outstanding principal balance of existing first loan (including existing HELOC in first lien position) plus any required per diem interest • Pay off of the outstanding principal balance of any existing subordinate liens that were used in whole to acquire the subject property • HUD-1 Settlement Statement(s) required from any prior transaction. The subject loan is considered a cash-out refinance if • The previous transaction combined a first and non-purchase money subordinate lien into a new first or subsequent refinance of that loan within the past 6 months • The current transaction pays off a first mortgage and a subordinate lien not used to acquire the subject property Not permitted N/A N/A N/A N/A N/A

Transcript of Fannie Mae DESKTOP UNDERWRITER LOAN...

DESKTOP UNDERWRITER LOAN PROSPECTOR

1. PRODUCTDESCRIPTION

• Conventional Conforming fixed rate mortgage• DU Version 9.2• 10 to 30 year term in annual increments• Fully amortizing• Qualified Mortgage (QM) Safe Harbor loans are permitted• Qualified Mortgage (QM) Rebuttable Presumption loans are permitted –see the Qualified Mortgage (QM) Rebuttable Presumption section for requirements.

• Conventional Conforming fixed rate mortgage• 10 to 30 year term in annual increments• Fully amortizing• Qualified Mortgage (QM) Safe Harbor loans are permitted• Qualified Mortgage (QM) Rebuttable Presumption loans are permitted –see the Qualified Mortgage (QM) Rebuttable Presumption section for requirements.

2. INDEX3. MARGIN4. ANNUAL ADJUSTMENT 5. LIFE CAP6. RATE AT ADJUSTMENT7. TEMPORARY BUYDOWN8. QUALIFYING RATEAND RATIOS

Qualifying Rate• Qualify using the note rate

Ratios• DU Approve/Eligible – Follow DU

Qualifying Rate• Qualify using the note rate

Ratios• LP Accept – 45% DTI

9. TYPES OF FINANCING

Please note that this is not a client offer or solicitation for all loan products listed. All loans submitted for purchase to Stockton Mortgage must be eligible for purchase by Stockton Mortgage and be in full compliance with the Stockton Mortgage Loan Product Matrix, Agency Selling Guide and Client Contract for each approved client.

Fannie Mae

Purchase MortgageRate & Term Refinance (Limited Cash-Out Refinance)• Loans submitted to LP when the previous mortgage was a purchase money transaction

• Existing mortgage must be seasoned at least 120 days, measured from previous note date to subject note date• Loan amount may include:

• Pay off the outstanding principal balance of existing first loan (including existing HELOC in first lien position) plus any required per diem interest• Pay off of the outstanding principal balance of any existing subordinate liens that were used in whole to acquire the subject property

• HUD-1 Settlement Statement(s) required from any prior transaction. The subject loan is considered a cash-out refinance if• The previous transaction combined a first and non-purchase money subordinate lien into a new first or subsequent refinance of that loan

within the past 6 months• The current transaction pays off a first mortgage and a subordinate lien not used to acquire the subject property

Not permittedN/AN/AN/AN/AN/A

DESKTOP UNDERWRITER LOAN PROSPECTOR

9. TYPES OF FINANCING (cont.)

Fannie Mae

• Closing costs and prepaids • Prepayment penalties associated with the existing mortgage • Cash-out limited to the lesser of 2% of the principal amount of the new loan or $2000• Delinquent real estate taxes may not be included in the loan amount. • See Agency Selling Guide for Continuity of Obligation definition and guideline requirements• Subject property may be currently listed for sale, subject to the following • Property must be taken off the market before the note date of the new mortgage • Borrower provides written confirmation of intent to occupy if a primary residence

Cash-Out Refinance• Power of Attorney not permitted• Ownership • One borrower must have held title to the subject property for at least 6 months, measured from previous note date to subject note date, with the following exceptions • Delayed Financing • Borrower legally awarded the property (divorce, separation, dissolution of a domestic partnership) • Inherited property (DU only) • LP loans: holding title for 6 months is not waived for a cash-out refinance • See Agency Selling Guide for details • For a manufactured home, one borrower must have held title to both the manufactured home and land for at least 12 months, measured from previous note date to subject note date. No exceptions.• See Agency Selling Guide for Continuity of Obligation definition and guideline requirements• Properties that have been listed for sale within the last 6 months permitted subject to the following • LTV/CLTV/HCLTV <=70% • Property has been taken off the market before the note date • Borrower provides written confirmation of the intent to occupy if primary residence

Please note that this is not a client offer or solicitation for all loan products listed. All loans submitted for purchase to Stockton Mortgage must be eligible for purchase by Stockton Mortgage and be in full compliance with the Stockton Mortgage Loan Product Matrix, Agency Selling Guide and Client Contract for each approved client.

DESKTOP UNDERWRITER LOAN PROSPECTOR

10. LOAN AMOUNT

11. LTV/CLTVLIMITATIONS AUTOMATED UNDERWRITING

Fannie Mae

Please note that this is not a client offer or solicitation for all loan products listed. All loans submitted for purchase to Stockton Mortgage must be eligible for purchase by Stockton Mortgage and be in full compliance with the Stockton Mortgage Loan Product Matrix, Agency Selling Guide and Client Contract for each approved client.

DESKTOP UNDERWRITER LOAN PROSPECTOR

11. LTV/CLTVLIMITATIONS AUTOMATED UNDERWRITING (cont.)

12. LTV/CLTVLIMITATIONS MANUFACTURED HOUSING

Fannie Mae

1 LTV>95%• Purchase- At least one borrower must be a first-time home buyer (must not have owned any residential property in the past three years)• Rate & Term Refinance –Existing loan being refinanced must be owned by Fannie Mae. Documentation may come from one of the following and must be retained in the loan file: • Fannie Mae’s Loan Lookup tool • Servicing System • The current servicer (if the lender is not the servicer)2 Maximum 105% CLTV with Community Second3 DU Approve Eligible - Borrowers with five to ten financed properties; see Limitations on Other R.E. Owned section for additional guidelines• See Agency Selling Guide for parents who want to provide housing for their physically handicapped or developmentally disabled adult child or children who want to provide housing for parents who are unable to work or do not have sufficient income to qualify (DU only)• See MI company eligibility guideline requirements for LTV >80%

Please note that this is not a client offer or solicitation for all loan products listed. All loans submitted for purchase to Stockton Mortgage must be eligible for purchase by Stockton Mortgage and be in full compliance with the Stockton Mortgage Loan Product Matrix, Agency Selling Guide and Client Contract for each approved client.

DESKTOP UNDERWRITER LOAN PROSPECTOR

13. SECONDARY FINANCING

Please note that this is not a client offer or solicitation for all loan products listed. All loans submitted for purchase to Stockton Mortgage must be eligible for purchase by Stockton Mortgage and be in full compliance with the Stockton Mortgage Loan Product Matrix, Agency Selling Guide and Client Contract for each approved client.

Fannie Mae

• See LTV/CLTV Limitations section• See Agency Selling Guide for eligibility guidelines• Down Payment Assistance Programs (DPA) are eligible when the following Community Seconds Program requirements are met • 30 Yr Fannie Fixed with Community Second only • DU Approve • Primary Residence • Purchase and Rate &Term Refinance only • Manufactured homes not permitted • May be funded by a federal agency, municipality, state, county or local housing finance agency, non-profit organization, a regional Federal Home Loan Bank or an employer • Stockton Mortgage must approve subordinate financing programs and mortgage documents, and any subsequent changes in advance. • Maximum 105% CLTV • May be used to fund all or part of the down payment, closing costs • The more restrictive down payment requirement between the product and the second mortgage will apply. • Income limits imposed by the Community Seconds provider apply • No reporting requirements permitted • See Agency Selling Guide

Eligible Property Types• 1-4 units• Condo • See the Fannie Mae or Freddie Mac Condo-PUD Matrices for: • Appraisal and warranty requirements • LTV/CLTV /HCLTV for Fannie Mae DU Limited Review established attached condos. • LP loans eligible with the following LP condo warranty project reviews: • Detached review • Established Condo Project review • New Condo Project review • 2-4 unit Condo Project review • Streamlined Review with an LTV/CLTV/HCLTV <=80%. Freddie Mac LP Streamlined Review with an LTV/CLTV/HCLTV >80% is not permitted • Condo warranty valid for 180 days prior to the note date• Leasehold Estates• Manufactured Homes (DU only) • Max 95% LTV/CLTV/HCLTV• Primary residence and second homes• Properties located in Condo/PUD projects not eligible• Properties on a leasehold are not eligible• The borrower must have owned both the manufactured home and land for at least 12 months preceding the date of the loan application for cash-out refinance transactions.• The manufactured home must be classified and titled as real property.• Properties permanently installed on a site for less than 12 months are eligible only if borrower is the second purchaser of the property and the seller is not the builder-contractor or manufactured housing dealer who installed MH unit on site.• Modular, Precut, Panelized Housing• PUD

Ineligible Property Types• 2-4 unit PUD• Condo Hotel• Co-op

14. PROPERTY TYPES

DESKTOP UNDERWRITER LOAN PROSPECTOR

15. OCCUPANCY

16. GEOGRAPHIC LOCATIONS

17. STATE SPECIFIC REQUIREMENTS18. ASSUMPTIONS19. ESCROW WAIVERS

20. PREPAYMENT PENALTY21. APPROVAL AUTHORITY

22. UNDERWRITING/AUS DECISIONS

Not permitted

Fannie Mae

• Primary Residence• Second Homes• Investment PropertiesAlabama, Florida, Georgia, Indiana, Kentucky, Mississippi, North Carolina, Ohio, Tennessee, and Texas

N/A

Please note that this is not a client offer or solicitation for all loan products listed. All loans submitted for purchase to Stockton Mortgage must be eligible for purchase by Stockton Mortgage and be in full compliance with the Stockton Mortgage Loan Product Matrix, Agency Selling Guide and Client Contract for each approved client.

• Higher Priced Mortgage Loans (HPML)• Primary residence loans must maintain an escrow account for a minimum of 5 years.

None

DESKTOP UNDERWRITER LOAN PROSPECTOR

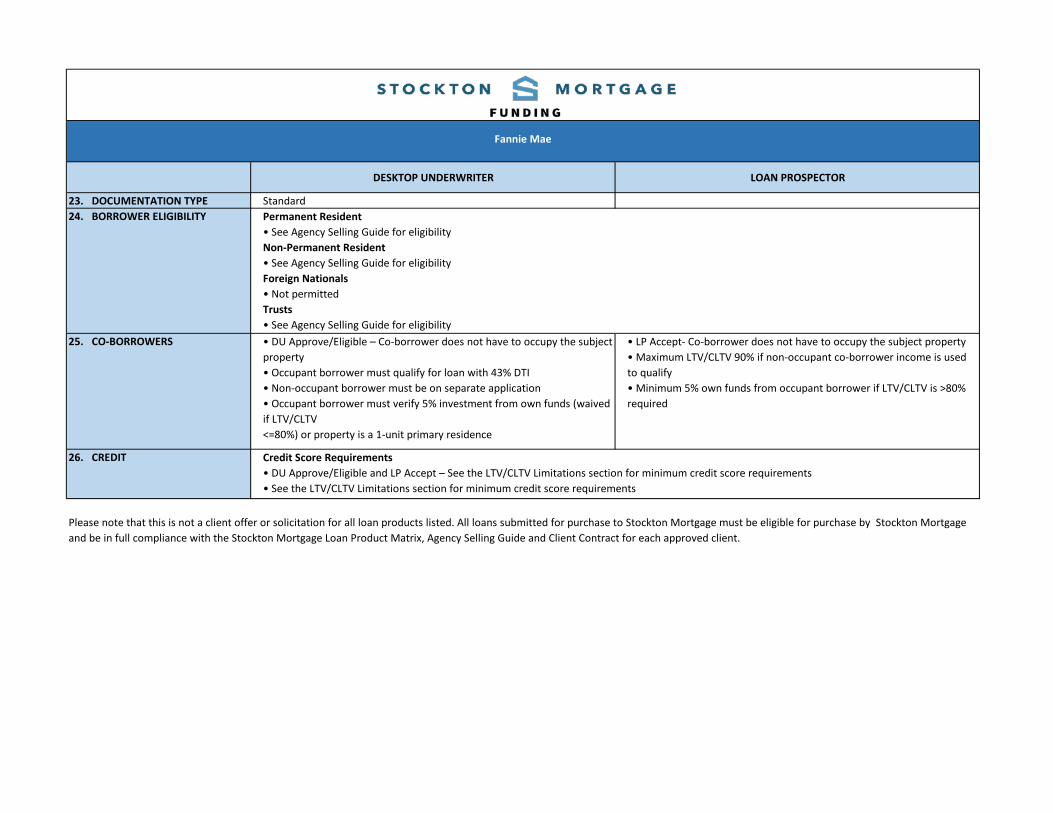

23. DOCUMENTATION TYPE Standard24. BORROWER ELIGIBILITY

25. CO-BORROWERS • DU Approve/Eligible – Co-borrower does not have to occupy the subject property• Occupant borrower must qualify for loan with 43% DTI• Non-occupant borrower must be on separate application• Occupant borrower must verify 5% investment from own funds (waived if LTV/CLTV<=80%) or property is a 1-unit primary residence

• LP Accept- Co-borrower does not have to occupy the subject property• Maximum LTV/CLTV 90% if non-occupant co-borrower income is used to qualify• Minimum 5% own funds from occupant borrower if LTV/CLTV is >80% required

26. CREDIT

Fannie Mae

Permanent Resident• See Agency Selling Guide for eligibilityNon-Permanent Resident• See Agency Selling Guide for eligibilityForeign Nationals• Not permittedTrusts• See Agency Selling Guide for eligibility

Credit Score Requirements• DU Approve/Eligible and LP Accept – See the LTV/CLTV Limitations section for minimum credit score requirements• See the LTV/CLTV Limitations section for minimum credit score requirements

Please note that this is not a client offer or solicitation for all loan products listed. All loans submitted for purchase to Stockton Mortgage must be eligible for purchase by Stockton Mortgage and be in full compliance with the Stockton Mortgage Loan Product Matrix, Agency Selling Guide and Client Contract for each approved client.

DESKTOP UNDERWRITER LOAN PROSPECTOR

26. CREDIT (cont.)

27. ASSET/RESERVES

Fannie Mae

• Purchase or rate & term refinance• No self-employed borrowers• Maximum 36% DTI• No minimum reserve requirement• Maximum 95% LTV

Housing (Mortgage/Rental) Payment History (PITIA)• Inclusive of all liens regardless of position• Applies to all mortgages on all financed properties• DU Approve/Eligible and LP Accept – Evaluated by DU/LP

Significant Derogatory Credit• See Agency Selling Guide for• Bankruptcy• Foreclosure• Preforeclosure• Deed-in-lieu• Restructured Loans• Short Payoff

Seller ContributionsPrimary Residence and Second Homes• 3% for LTV/CLTV > 90%• See the Fannie Mae REO section for Primary Residence with an LTV/CLTV >90%• 6% for LTV/CLTV > 75% <= 90%• 9% for LTV/CLTV <= 75%Investment Properties• 2%

Please note that this is not a client offer or solicitation for all loan products listed. All loans submitted for purchase to Stockton Mortgage must be eligible for purchase by Stockton Mortgage and be in full compliance with the Stockton Mortgage Loan Product Matrix, Agency Selling Guide and Client Contract for each approved client.

DESKTOP UNDERWRITER LOAN PROSPECTOR

Please note that this is not a client offer or solicitation for all loan products listed. All loans submitted for purchase to Stockton Mortgage must be eligible for purchase by Stockton Mortgage and be in full compliance with the Stockton Mortgage Loan Product Matrix, Agency Selling Guide and Client Contract for each approved client.

Fannie Mae

Cash-Out Refinance – The cash out may not be used to meet the reserve requirements

27. ASSET/RESERVES (cont.)

DESKTOP UNDERWRITER LOAN PROSPECTOR

28. EMPLOYMENT/ INCOME

29. LIMITATIONS ON OTHER R.E. OWNED

Multiple Loans to the Same Borrower• DU Approve • New multiple loans must be underwritten simultaneously• See the Approval Authority section• See Agency Selling Guide for eligibility guidelines• Second Home & Investment Properties• Up to 10 financed properties, including the subject property. Borrowers with 5- 10 financed properties must meet the below eligibility requirements, including additional reserve requirements. See Reserves section for reserve requirements.• See Fannie Mae REO section for LTV/CLTV/HCLTV ratios on 2-4 unit• Investment property

Multiple Loans to the Same Borrower• LP Accept• New multiple loans must be underwritten simultaneously• See the Approval Authority section• See Agency Selling Guide for eligibility guidelines• Second Home & Investment Properties• Up to 4 financed properties, including the subject property• See Reserves section for reserve requirements.

Fannie Mae

• Follow DU/LP for income documentation• LP Accept where income is documented with tax returns must provide two years tax returns, regardless of the LP requirement.• LP Accept with Future Employment is not permitted• See Agency Selling Guide

Form 4506-T• Prior to Final Underwriting Decision(Non-delegated clients) or Prior to Funding (Delegated Clients)• 4506-T must be processed for each borrower. Obtain as appropriate:• tax return transcript (s) when the personal income tax return(s) are used for qualification (self-employment, rental income, >= 25% income earned from commission, etc.); or• W-2 or 1099 transcript(s) for salaried borrowers or for borrowers with other types of income not documented with tax returns (retirement, social security disability, etc.)• At Closing• 4506-T for each borrower whose income is used to qualify must be signed at closing• 4506 –T for the business tax return transcript(s) must be signed at closing when the business returns are in the file• See Agency Selling Guide for complete guidelines

Please note that this is not a client offer or solicitation for all loan products listed. All loans submitted for purchase to Stockton Mortgage must be eligible for purchase by Stockton Mortgage and be in full compliance with the Stockton Mortgage Loan Product Matrix, Agency Selling Guide and Client Contract for each approved client.

DESKTOP UNDERWRITER LOAN PROSPECTOR

Please note that this is not a client offer or solicitation for all loan products listed. All loans submitted for purchase to Stockton Mortgage must be eligible for purchase by Stockton Mortgage and be in full compliance with the Stockton Mortgage Loan Product Matrix, Agency Selling Guide and Client Contract for each approved client.

Fannie Mae

29. LIMITATIONS ON OTHER R.E. OWNED (cont.)

DESKTOP UNDERWRITER LOAN PROSPECTOR

30. FANNIE MAE REO When the transaction is Fannie Mae REO using one of the following enhancements, the file must be clearly marked as Fannie Mae REO and an approved exception must be in the loan file for delivery purposes.• Primary residence LTV/CLTV >90% may have Seller Contributions up to 6% (rather than the 3%), and• Multiple Financed REO: Max 75% LTV/CLTV/HCLTV for 2 to 4 unit subject investment property (rather than the standard 70% LTV/CLTV/HCLTV.)• Resale Restrictions• Fannie Mae REO resale restriction (property resold within 3 months of purchase) is eligible. An exception must be submitted with the loan file for delivery purposes.

N/A

31. APPRAISAL REQUIREMENTS

32. MORTGAGE INSURANCE

Please note that this is not a client offer or solicitation for all loan products listed. All loans submitted for purchase to Stockton Mortgage must be eligible for purchase by Stockton Mortgage and be in full compliance with the Stockton Mortgage Loan Product Matrix, Agency Selling Guide and Client Contract for each approved client.

Fannie Mae

Mortgage insurance is required for all loans over 80% LTV• Refer to the MI company requirements for additional eligibility guidelines• Discounted coverage requiring additional premium per AUS is not eligible• Include the calculation and rate factor used to determine mortgage insurance premium disclosed to the borrower on the initial application. Including the MI rate card with the factor will allow Stockton Mortgage to direct the loan to the appropriate MI partner• Financed MI is permitted for 1-unit primary residence and second home purchase and rate & term refinance transactions• The mortgage amount and LTV including the financed premium may not exceed the limitation set forth in the program guidelines• Mortgage insurance coverage is based on LTV excluding the financed premium. Rate lock pricing is based on mortgage amount including financed premium

• See Agency Selling Guide for complete requirements• DU Approve/Eligible – Follow DU• LP Accept• An Interior and Exterior Appraisal Report (Form 1004) is required• Re-use of an appraisal report is not permitted

DESKTOP UNDERWRITER LOAN PROSPECTOR

Fannie Mae

32. MORTGAGE INSURANCE (cont.)

Please note that this is not a client offer or solicitation for all loan products listed. All loans submitted for purchase to Stockton Mortgage must be eligible for purchase by Stockton Mortgage and be in full compliance with the Stockton Mortgage Loan Product Matrix, Agency Selling Guide and Client Contract for each approved client.

DESKTOP UNDERWRITER LOAN PROSPECTOR

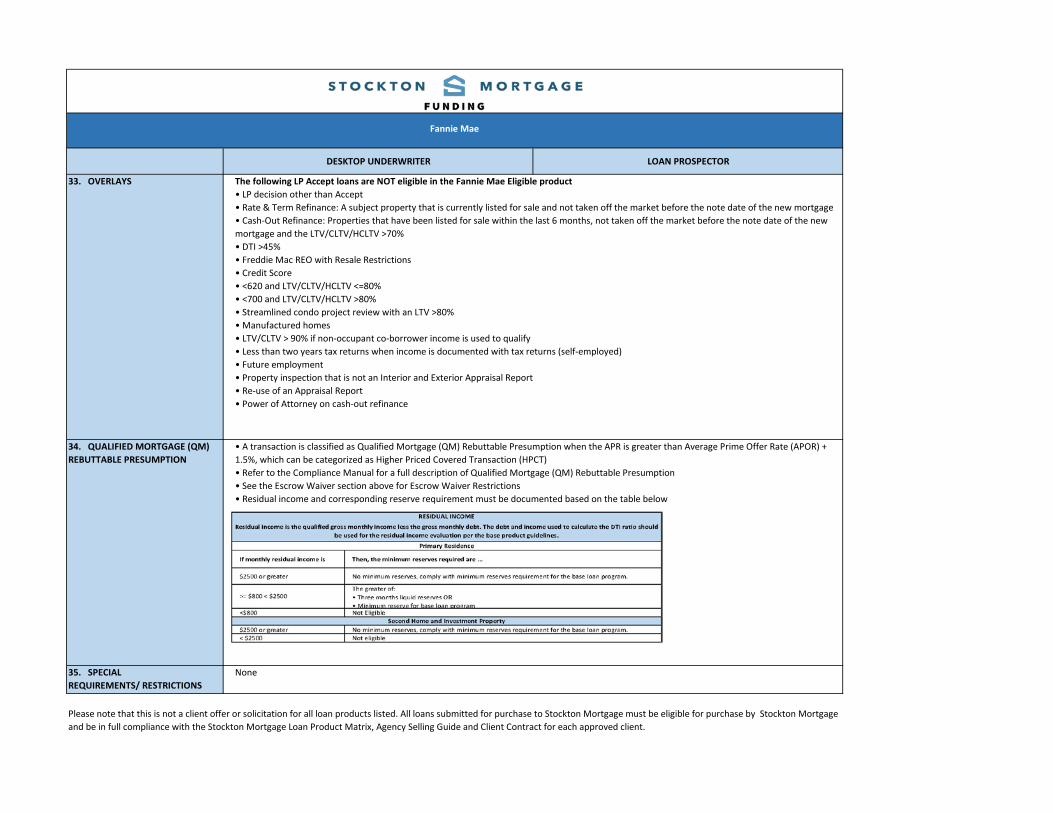

33. OVERLAYS

34. QUALIFIED MORTGAGE (QM) REBUTTABLE PRESUMPTION

35. SPECIALREQUIREMENTS/ RESTRICTIONS

Please note that this is not a client offer or solicitation for all loan products listed. All loans submitted for purchase to Stockton Mortgage must be eligible for purchase by Stockton Mortgage and be in full compliance with the Stockton Mortgage Loan Product Matrix, Agency Selling Guide and Client Contract for each approved client.

Fannie Mae

The following LP Accept loans are NOT eligible in the Fannie Mae Eligible product• LP decision other than Accept• Rate & Term Refinance: A subject property that is currently listed for sale and not taken off the market before the note date of the new mortgage• Cash-Out Refinance: Properties that have been listed for sale within the last 6 months, not taken off the market before the note date of the new mortgage and the LTV/CLTV/HCLTV >70%• DTI >45%• Freddie Mac REO with Resale Restrictions• Credit Score• <620 and LTV/CLTV/HCLTV <=80%• <700 and LTV/CLTV/HCLTV >80%• Streamlined condo project review with an LTV >80%• Manufactured homes• LTV/CLTV > 90% if non-occupant co-borrower income is used to qualify• Less than two years tax returns when income is documented with tax returns (self-employed)• Future employment• Property inspection that is not an Interior and Exterior Appraisal Report• Re-use of an Appraisal Report• Power of Attorney on cash-out refinance

• A transaction is classified as Qualified Mortgage (QM) Rebuttable Presumption when the APR is greater than Average Prime Offer Rate (APOR) + 1.5%, which can be categorized as Higher Priced Covered Transaction (HPCT)• Refer to the Compliance Manual for a full description of Qualified Mortgage (QM) Rebuttable Presumption• See the Escrow Waiver section above for Escrow Waiver Restrictions• Residual income and corresponding reserve requirement must be documented based on the table below

None

![[Superior + Subordinate] or [Superior - Illinois State Universitymy.ilstu.edu/~llipper/com495/examples_cs/NCA Superior-Subordinate... · Superior-Subordinate 2 Abstract The relationship](https://static.fdocuments.us/doc/165x107/5ad250647f8b9a92258cfbfd/superior-subordinate-or-superior-illinois-state-llippercom495examplescsnca.jpg)