Family Solutions Presentation

41

HAVE YOU FOUND A SOLUTION FOR YOUR FAMILY’S FINANCIAL GOALS?

-

Upload

additya-dubey -

Category

Documents

-

view

217 -

download

1

Transcript of Family Solutions Presentation

HAVE YOU FOUND A SOLUTION FOR YOUR FAMILY’S FINANCIAL GOALS?

ARE YOU SAVING ENOUGH?

3

YOUR CURRENT INCOME MAY NOT MATCH LIFE’S NEEDS

Can you ignore planning and investing for your future?

BIRTH & EDUCATION

Marriage Child Car House Child’s Education

Child’s Marriage

RETIREMENT

Are your investments growing adequately to meet your future needs?

Assuming Inflation @ 6% for years 2020 and 2030

4

BASIC EXPENSES WILL KEEP GROWING OVER TIME

5

Your ability to save falls due to higher demands on your income. Is your investment working hard enough for you?

YESTERDAY’S LUXURIES ARE TODAY’S NECESSITIES

ITEMS 1991 TODAY

Cable TV / Dish No Yes

LCD TV No Yes

Mobile No Yes

Washing Machine / Microwave No Yes

Branded Watches / Clothes No Yes

Bike / Car / Second Car No Yes

Home Theatre System No Yes

6

Mandatory expenses that make a demand on your household’s income are growing from changes in lifestyle and inflation

You need a plan to ensure that you save for the future and you put your savings to work, to meet those future goals

Do you have a plan to meet large

expenses of the future?

Are you saving enough with a

specific purpose or goal in mind?

Is your savings working hard enough

to meet those goals?

YOUR FUTURE NEEDS

WE ALL HAVE DREAMS FOR OUR FAMILIES

7

But the big challenge is how do we achieve these goals?

FAILING TO PLAN IS PLANNING TO FAIL

THREE FACETS OF THE INVESTMENT DECISION

Mutual Funds can offer a one-stop solution for all the three questions

Invest in a diversified portfolio that is managed professionally

HOW DO YOU INVEST?

WHERE YOU

INVEST?

Invest in a mix of assets that provide income and growth

WHEN DO YOU INVEST?

Invest systematically with discipline and patience

9

Your investments have to be tuned by allocating carefully across different types of assets

WHERE TO INVEST?

Each one comes with its return, risk and time horizon: – Equity offers better long term return, but higher short term volatility

– Debt offers steady income but limited long term appreciation

10

A diversified portfolio across asset classes can works best

equity short term debt

long term debt

commodities gold international assets

real estate

art

Spread your risks: Diversify by asset class

No country will always be the best performer year-after-year

WHERE TO INVEST?

11

A diversified portfolio across geographies can work best

Winners Rotate: Diversify by geography

“Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria” – Sir John Templeton

HOW TO INVEST?

12

Don’t let the cycle of market emotions rule you

HOW TO INVEST?

13

Don’t let the cycle of market noise rule you

A diversified portfolio works best for investors

14

HOW TO INVEST? A professional investment manager

is better equipped to take care of your investments!

15

Timing can be harmful to your investment

It is tough to time the market

WHEN TO INVEST?

Perfect market timing requires: the right exit point and the right re-entry point

Getting even one of these wrong can affect returns

Mathematically, the odds are heavily against perfectly timing the market

16

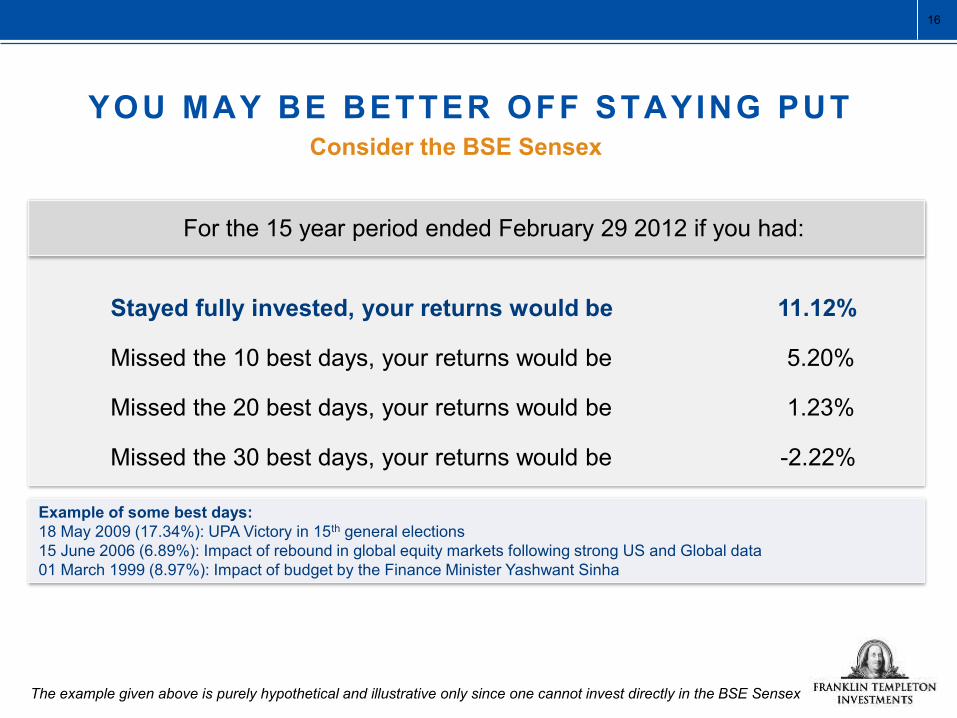

YOU MAY BE BETTER OFF STAYING PUT

For the 15 year period ended February 29 2012 if you had:

Stayed fully invested, your returns would be 11.12%

Missed the 10 best days, your returns would be 5.20%

Missed the 20 best days, your returns would be 1.23%

Missed the 30 best days, your returns would be -2.22%

Consider the BSE Sensex

The example given above is purely hypothetical and illustrative only since one cannot invest directly in the BSE Sensex

Example of some best days: 18 May 2009 (17.34%): UPA Victory in 15th general elections 15 June 2006 (6.89%): Impact of rebound in global equity markets following strong US and Global data 01 March 1999 (8.97%): Impact of budget by the Finance Minister Yashwant Sinha

TWO CRITICAL FACTORS TO SUCCESSFUL FINANCIAL PLANNING

START EARLY

18

Time is your friend when it comes to investing

The earlier you start investing, the more time you give your money to grow

The earlier you start, the lesser you need to save

19

STARTING EARLY CAN MAKE A DIFFERENCE TO YOUR WEALTH

Retirement corpus at age 60 assuming a return of 10%

on their investments

INR 70.4 lac

INR 2.0 crore

20

THE MORE THE DELAY, THE MORE THE NEED TO MAKE UP

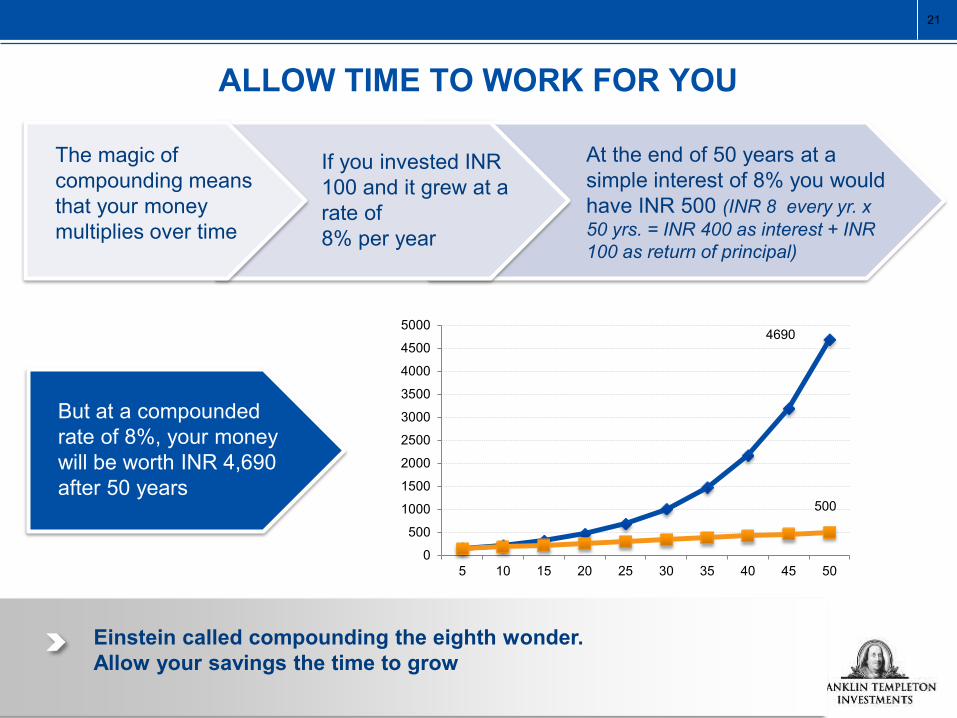

ALLOW TIME TO WORK FOR YOU

21

Einstein called compounding the eighth wonder. Allow your savings the time to grow

The magic of compounding means that your money multiplies over time

If you invested INR 100 and it grew at a rate of 8% per year

At the end of 50 years at a simple interest of 8% you would have INR 500 (INR 8 every yr. x 50 yrs. = INR 400 as interest + INR 100 as return of principal)

4690

500

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

5 10 15 20 25 30 35 40 45 50

But at a compounded rate of 8%, your money will be worth INR 4,690 after 50 years

MANTRAS FOR SUCCESS

22

You need a one-point solution that enables you to define, plan and reach your goals

Understand the need to save for goals

PLAN BETTER FOR YOUR FUTURE

Set the time frame to save

Determine goal value and saving target

Monitor the progress

Motivate yourself to keep at it

23

Presenting

24

WHAT IS FAMILY SOLUTIONS?

A unique investment solution that helps

you plan for your life goals

THE NEW PARADIGM

25

KEY ELEMENTS OF FAMILY SOLUTIONS

THE NEW PARADIGM

PLANNER & GOAL SHEET

APPLICATION FORM

GOAL TRACKER

ACCOUNT STATEMENT

26

HOW DOES IT WORK?

THE NEW PARADIGM

Create a customized plan using the Family Solutions Planner

Submit filled up Family Solutions form and Goal Sheet to us

Receive a Welcome Letter and customized

Family Solutions Account Statement

Review and track progress of your

goals through your advisor

1

2 3

4

“Goal Sheet” needs to be submitted with the application form

27

FAMILY SOLUTIONS PLANNER AND GOAL SHEET

Planner is available both on our website and with your advisor

INPUT Goal details, target amount, timeframe, inflation and returns expectations (that determines portfolio style)

OUTPUT Amount to invest annually / monthly / one-time to reach the goals & FT funds allocation

KEY ELEMENTS: PLANNER AND GOAL SHEET

28

WELCOME SCREEN

KEY ELEMENTS: PLANNER AND GOAL SHEET

29

INPUT SCREENS

Choose to plan for either one or all of the three goals

Basic details are captured

KEY ELEMENTS: PLANNER AND GOAL SHEET

30

Goal wise details entered basis your objectives / needs and

expectations

KEY ELEMENTS: PLANNER AND GOAL SHEET

31

GOAL DETAILS

Goal wise output on how much to invest and which funds to

invest in

KEY ELEMENTS: PLANNER AND GOAL SHEET

32

GOAL SUMMARY SHEET

KEY ELEMENTS: PLANNER AND GOAL SHEET

Option to add more goals View Goal Sheet to get your

customized plan

33

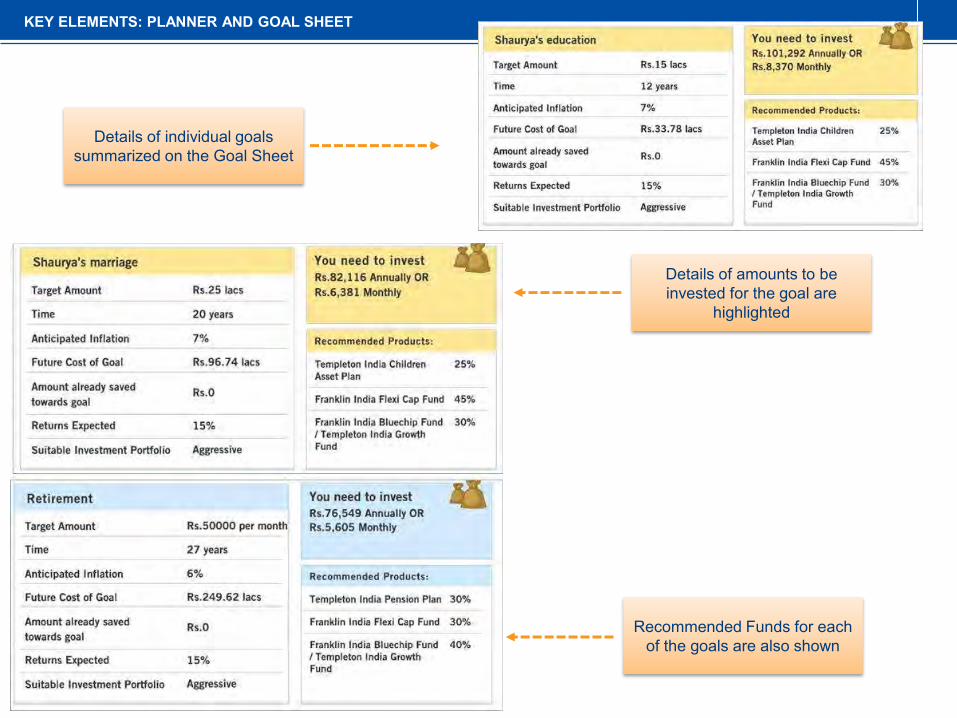

GOAL SHEET (OUTPUT)

The Goal Sheet is a summary

of your goals and the

recommended plan

KEY ELEMENTS: PLANNER AND GOAL SHEET

Details of individual goals summarized on the Goal Sheet

Details of amounts to be invested for the goal are

highlighted

Recommended Funds for each of the goals are also shown

KEY ELEMENTS: PLANNER AND GOAL SHEET

35

APPLICATION FORM

Facility of multiple goals in one form

Convenience of single cheque across multiple funds / goals in a form

Flexibility of investing lump-sum (regular), SIP or combination of both

Flexibility for existing FT investors to move into Family Solutions with current investments

Transaction rules on load, minimum application amount, etc. same as that at the underlying scheme level

SIP ECS form for multiple goals / schemes in each form

KEY ELEMENTS: APPLICATION FORM

36

APPLICATION FORM

KEY ELEMENTS: APPLICATION FORM

Single table for multiple schemes across multiple goals

Option of Single Cheque across all funds (if lump-sum)

37

SIP ECS FORM

KEY ELEMENTS: APPLICATION FORM

Single ECS form for upto 4 schemes

38

ACCOUNT STATEMENT

Family Solutions details will be shown at a goal level

KEY ELEMENTS: ACCOUNT STATEMENT

Funds are segmented Goal wise as per your specific goals

Current value of the goal is available

39

BENEFITS TO YOU

THE NEW PARADIGM

TO PLAN • Planner helps plan for life goals in simple,

organized and customized way

• Saves the trouble of choosing from 100s of funds with varied objectives

TO INVEST

• You fill up a single form for all your goals and pay through a single cheque

TO MONITOR

• Customized account statement gives details of goals, schemes invested in and the value of the investments

• Track the progress of your goals through your advisor anytime you wish

ARE YOU READY FOR THE NEW PARADIGM?

PRESENTING FAMILY SOLUTIONS

41

RISK FACTORS

Disclaimer: Setting up the goals, planning of investment and taking informed investment decision might require professional expert advice. You are advised to consult your advisor prior to arriving at the investment decision. There is no assurance or guarantee that the goals planned for will be achieved and the same is subject to the investment performance of the schemes. Past performance of the schemes is neither an indicator nor a guarantee of future performance, and may not be considered as the basis for future investment decisions. The recommendation given above is based on the inputs provided by you regarding your anticipated rate of returns and rate of inflation, the investment goals including the target amount and investment horizon.

Risk Factors: Mutual Fund investments are subject to market risks, read all scheme related documents carefully. The NAVs of the schemes may go up or down depending upon the factors and forces affecting the securities market including the fluctuations in the interest rates and there can be no assurance that the schemes’ investment objectives will be achieved. The past performance of the mutual funds managed by the Franklin Templeton Group and its affiliates is not necessarily indicative of future performance of the schemes. The names of the schemes do not in any manner indicate the quality of the schemes, their future prospects or returns. The Mutual Fund is not guaranteeing or assuring any dividend under any of the schemes and the same is subject to the availability and adequacy of distributable surplus and the investment performance of the schemes. The investments made by the schemes are subject to external risks. Subscription in tax saving schemes are subject to lock-in period specified in the respective scheme information document and the investor cannot redeem, transfer, assign or pledge the units during the lock-in period.