FALLING FORWARD: REAL OPTIONS REASONING …business.illinois.edu/josephm/badm 545_spring...

19

* Academy of Management Review 1999, Vol. 24. No. 1. 13-30. FALLING FORWARD: REAL OPTIONS REASONING AND ENTREPRENEURIAL FAILURE RITA GUNTHER MCGRATH Columbia University Although failure in entrepreneurship is pervasive, theory often reflects an equally pervasive antifailure bias. Here, I use real options reasoning to develop a more balanced perspective on the role of entrepreneurial failure in wealth creation, which emphasizes managing uncertainty by pursuing high-variance outcomes but investing only if conditions are favorable. This can increase profit potential while containing costs. I also offer propositions that suggest how gains from entrepreneurship may be maximized and losses mitigated. Schumpeter linked wealth creation directly to the entrepreneurial process, through which "new combinations" of factors of production are introduced into an economic system (1950: 83). Entrepreneurship creates new processes, puts underutilized resources to new uses, initiates the formation of new industries, and otherwise unleashes "gales of creative destruction" (Schumpeter, 1950: 83). It has been linked to cre- ation of employment, increases in productivity, and improvement of living standards, and to economic growth in general (Baumol, 1993; Birch, 1979). Consequently, scholars often regard entrepreneurship as quite a good thing (see Bir- ley, 1986, and Lumpkin & Dess, 1998). Embracing entrepreneurship, however, implies accepting all that goes with it, particularly the recognition of a priori irreducible uncertainty (Venkatara- man, 1997). One manifestation of uncertainty is highly variable—or risky—returns (Lubatkin & Chatterjee, 1994: 110). Risk can become manifest in failure (Miller & Reuer, 1996). Comments from Eric Abrahamson, Edward H. Bowman, Joel Brockner, Melissa Cardon, Ian C. MacMiUan, S. Venkat- araman, and four anonymous AMR reviewers were ex- tremely helpful in developing the ideas presented here. This research was partially funded by the proceeds from an award for Best Conceptual Paper, bestowed by Entrepie- neurship. Theory & Practice ai the 1996 annual meeting of the Academy of Management, and by the ECLIPSE (Entrepre- neurial Careers, Learning and Investment Patterns) project at the Columbia University Graduate School of Business. I am also grateful for the support of the Sol C. Snider Entre- preneurial Center at The Wharton School. The popular (and sometimes the scholarly) en- thusiasm for risk taking in the entrepreneurial process wanes considerably at the prospect of failure (Baker, Aldrieh, Langton, & Cliff, 1997). Researchers mourn the cost of new business failure, attempt to root out its causes, and seek to determine how it can be avoided (e.g., Kets de Vries, 1985; Reynolds, 1987, Romanelli, 1989; Sta- tistics Canada, 1997). Social norms can render "losing" shameful (Tezuka, 1997), and expensive public policies help new firms avoid failing by providing them with resources. In short, a ten- dency to view failure negatively introduces a pervasive bias in entrepreneurship theory and research. As March and Shapira observe, "Soci- ety values risk taking, but not gambling, and what is meant by gambling is risk taking that turns out badly" (1987: 1413). My objective is to offer ideas that might help redirect the theoretical focus in entrepreneur- ship from a preoccupation with achieving suc- cess and avoiding failure to a more integrated view of how the two phenomena are related (see also Aldrieh & Fiol, 1994). I begin by character- izing entrepreneurial initiatives not as varia- tions, random mutations, or bold new adven- tures but as real options, whose value is fundamentally influenced by uncertainty. I show how an options lens can reveal the condi- tions under which an antifailure bias can hinder understanding of the systemic relationship be- tween success and failure, leading to unin- tended negative consequences. Real options reasoning, moreover, allows more of failure's possible benefits to be captured and the most egregious of its costs to be contained. I apply these ideas at the economy and firm levels. 13

Transcript of FALLING FORWARD: REAL OPTIONS REASONING …business.illinois.edu/josephm/badm 545_spring...

* Academy of Management Review1999, Vol. 24. No. 1. 13-30.

FALLING FORWARD: REAL OPTIONSREASONING AND ENTREPRENEURIAL FAILURE

RITA GUNTHER MCGRATHColumbia University

Although failure in entrepreneurship is pervasive, theory often reflects an equallypervasive antifailure bias. Here, I use real options reasoning to develop a morebalanced perspective on the role of entrepreneurial failure in wealth creation, whichemphasizes managing uncertainty by pursuing high-variance outcomes but investingonly if conditions are favorable. This can increase profit potential while containingcosts. I also offer propositions that suggest how gains from entrepreneurship may bemaximized and losses mitigated.

Schumpeter linked wealth creation directly tothe entrepreneurial process, through which"new combinations" of factors of production areintroduced into an economic system (1950: 83).Entrepreneurship creates new processes, putsunderutilized resources to new uses, initiatesthe formation of new industries, and otherwiseunleashes "gales of creative destruction"(Schumpeter, 1950: 83). It has been linked to cre-ation of employment, increases in productivity,and improvement of living standards, and toeconomic growth in general (Baumol, 1993;Birch, 1979). Consequently, scholars often regardentrepreneurship as quite a good thing (see Bir-ley, 1986, and Lumpkin & Dess, 1998). Embracingentrepreneurship, however, implies acceptingall that goes with it, particularly the recognitionof a priori irreducible uncertainty (Venkatara-man, 1997). One manifestation of uncertainty ishighly variable—or risky—returns (Lubatkin &Chatterjee, 1994: 110). Risk can become manifestin failure (Miller & Reuer, 1996).

Comments from Eric Abrahamson, Edward H. Bowman,Joel Brockner, Melissa Cardon, Ian C. MacMiUan, S. Venkat-araman, and four anonymous AMR reviewers were ex-tremely helpful in developing the ideas presented here. Thisresearch was partially funded by the proceeds from anaward for Best Conceptual Paper, bestowed by Entrepie-neurship. Theory & Practice ai the 1996 annual meeting of theAcademy of Management, and by the ECLIPSE (Entrepre-neurial Careers, Learning and Investment Patterns) projectat the Columbia University Graduate School of Business. Iam also grateful for the support of the Sol C. Snider Entre-preneurial Center at The Wharton School.

The popular (and sometimes the scholarly) en-thusiasm for risk taking in the entrepreneurialprocess wanes considerably at the prospect offailure (Baker, Aldrieh, Langton, & Cliff, 1997).Researchers mourn the cost of new businessfailure, attempt to root out its causes, and seekto determine how it can be avoided (e.g., Kets deVries, 1985; Reynolds, 1987, Romanelli, 1989; Sta-tistics Canada, 1997). Social norms can render"losing" shameful (Tezuka, 1997), and expensivepublic policies help new firms avoid failing byproviding them with resources. In short, a ten-dency to view failure negatively introduces apervasive bias in entrepreneurship theory andresearch. As March and Shapira observe, "Soci-ety values risk taking, but not gambling, andwhat is meant by gambling is risk taking thatturns out badly" (1987: 1413).

My objective is to offer ideas that might helpredirect the theoretical focus in entrepreneur-ship from a preoccupation with achieving suc-cess and avoiding failure to a more integratedview of how the two phenomena are related (seealso Aldrieh & Fiol, 1994). I begin by character-izing entrepreneurial initiatives not as varia-tions, random mutations, or bold new adven-tures but as real options, whose value isfundamentally influenced by uncertainty. Ishow how an options lens can reveal the condi-tions under which an antifailure bias can hinderunderstanding of the systemic relationship be-tween success and failure, leading to unin-tended negative consequences. Real optionsreasoning, moreover, allows more of failure'spossible benefits to be captured and the mostegregious of its costs to be contained. I applythese ideas at the economy and firm levels.

13

14 Academy of Management Review January

A REAL OPTIONS PERSPECTIVE ONENTREPRENEURIAL FAILURE

I define the entrepreneurial process here asthe set of activities through which innovationschange existing combinations of factors of pro-duction, in both the manufacturing and the ser-vice sectors. The most widely recognizedsources of inspiration for entrepreneurship aremarket inefficiencies (Kirzner, 1979) and techno-logical progress (Schumpeter, 1950; see alsoShane, 1996). An entrepreneurial initiative, thus,is a specific effort by an existing firm or newentrant to introduce a new combination of re-sources. An initiative can be said to have failedwhen it is terminated as a consequence of ac-tual or anticipated performance below a criticalthreshold (see Gimeno, Folta, Cooper, & Woo,1997). In other words, failure is the termination ofan initiative that has fallen short of its goals.

Those goals are idiosyncratic. Consistent withbehavioral decision theory (Cyert & March, 1963)and theories of individual decision making(Kahneman & Tversky, 1979), failure thresholdsinvolve subjective assessments of alternatives.Hence, an entrepreneur might disband an eco-nomically profitable business if other activitiesappear more lucrative or interesting, if his or herinterests change, or if it seems that long-rungrowth is limited. That is, adverse opportunitycosts deter continuation of the current initiative(Gimeno et al., 1997). In contrast, as Meyer andZucker (1989) argue, organizations whose perfor-mance is economically poor may be sustainedby self-interested stakeholders, resulting in"permanently failing," underachieving organi-zations. It is the idiosyncratic judgment of whatconstitutes failure that makes real options rea-soning attractive.

Entrepreneurial Initiatives As Real Options

Real options theory concerns classes of in-vestments in real assets that are similar to fi-nancial options in structure (Bowman & Hurry,1993; Dixit & Pindyck, 1994). Just as the purchaseof an option contract conveys the right but notthe obligation to purchase the underlying asseton which the contract is written, investment in areal option conveys the opportunity to continueinvestment. If investments are staged so thatexpenditures end under poor conditions, lossescan be contained. The cost of failure, in other

words, is limited to the cost of creating the realoption, less any remaining option value (Dixit &Pindyck, 1994; Mitchell & Hamilton, 1988; Roberts& Weitzman, 1981). Should conditions prove fa-vorable, further investments may be made,which is referred to as exercising the option.

Scholars applying a real options frameworkhave emphasized its advantages over conven-tional approaches (such as net present valuecalculations) under conditions of uncertainty(Dixit & Pindyck, 1994; Hurry, Miller, & Bowman,1992; Kogut, 1991; Kogut & Kulatilaka, 1994; Tri-georgis, 1996). It has also been described as auseful lens for viewing entrepreneurship(McGrath, 1996).

In financial options theory, increased volatil-ity of the underlying asset increases the value ofthe option, because the potential gains aregreater while the costs to access them remainthe same. The upside becomes greater, but po-tential losses become no worse (Fama & Miller,1972). So, too, is the case with real options, forwhich potential variance of expected returns isakin to volatility (McGrath, 1997). Ex ante uncer-tainty, thus, is an important driver of optionvalue. If their present value is held constant,projects with greater variance of potential out-come have higher option value.

In this model failure is related directly to un-certainty, from which the value of the entrepre-neurial option is derived (Knight, 1921). Entre-preneurial rents (Rumelt, 1987) can be earned bythose who take out real options on opportunitiesthat are not obvious to others and that, therefore,are undervalued.

Real Options in Bundles

Understanding what leads to the success orfailure of a specific initiative, however, tells usonly a small part of the story of entrepreneurialwealth creation, which is a combinative processof interrelated advances and setbacks (see Ven-kataraman. Van de Ven, Buckeye, & Hudson,1990). Because of spillover and learning effects,it is often more useful to evaluate the collectivecontribution of entrepreneurial initiatives towealth creation than to assess each initiative onits own. The initiative that fails may still im-prove knowledge or methods of production. Con-sider Osborne's introduction of the first portable(some said "luggable") personal computer withbundled software—both innovations that were

t999 McGrath 15

imitated by later entrants. The benefits remainlong after the demise of the company that pio-neered them.

On a larger scale, failed first movers are as-sociated with the emergence of entirely newindustries (Aldrich & Fiol, 1994). Speech recog-nition technology is a current example. Techno-logical development is being driven by well-known research laboratories (including those atCarnegie Mellon University, the MassachusettsInstitute of Technology, Stanford Engineering,SRI International, and Lucent Technologies' BellLabs) and a clutch of startups (with names suchas Dragon Systems, Nuance Communications,and Applied Language Technologies). Shouldspeech recognition systems become ubiquitous,pundits argue that profits will flow to those whomake products and deliver services—not to thestartups developing the technology (Gross,Judge, Port, & Wildstrom, 1998). The startups,however, will have played an important role in aprocess expected to fundamentally alter theway people transmit information, use comput-ers, and offer services. Even if the startups even-tually fail, their contribution will have been pro-found (Garud & Van de Ven, 1992).

Entrepreneurial Initiatives and WealthCreation

Entrepreneurship attracts scholarly attentionbecause it is strongly associated with growth foran economy and with prosperity for individualfirms, as illustrated above.

Economy-level impacts. The technical andother advances generated by entrepreneurialactivity long have been associated with eco-nomic growth, because they allow increasing—not diminishing—returns to the deployment ofcapital (Knight, 1944; Romer, 1987). In what Barro(1997) terms "endogenous" growth theories, en-trepreneurial initiatives are seen as experi-ments in which hypotheses about the utility of anew combination of resources relative to exist-ing combinations and relative to other new al-ternatives are tested (Starr & MacMillan, 1990).This hypothesis testing generates improve-ments in technologies and increases economicresilience (Hayek, 1945).

Governments can influence the process of en-dogenous growth through "taxation, mainte-nance of law and order, provision of infrastruc-ture services, protection of intellectual property

rights, and regulation of international trade, fi-nancial markets, and other aspects of the econ-omy" (Barro, 1997: 6). In options terms, govern-ment policies can have a significant influenceon which options are taken out, which are exer-cised, and which are abandoned, as well as bywhom.

Firm-level impacts. At the level of the firm,entrepreneurial orientation (Lumpkin & Dess,1996) is the propensity of the firm to sponsorinitiatives that reconfigure and renew its re-source base. Much of the real options literatureto date has focused on firm-level initiatives, of-ten calling them "ventures," "projects," or "pro-posed investments" (Dixit & Pindyck, 1994;McGrath, 1997; Stewart, 1991).

With financial options, uncertainty regardingthe price of the underlying stock eventually isresolved by the passage of time. The value of theunderlying asset accessed through the acquisi-tion of a real option, however, is not as easy toascertain, since real options generally are noteasy to trade, nor do they have defined expira-tion dates. Moreover, real options also cannotalways be valued on their own. The investmentmade in one real option may pay off by resolv-ing issues surrounding other real options, evenif the first was a failure.

Thus, a complete accounting of a real option'sworth requires an understanding of the otheroptions in play. For instance, Maidique and Zir-ger (1985) show that new product failures likethe Edsel and the IBM Stretch computer dramat-ically and idiosyncratically reduced technicaland market uncertainties in ways that led tospectacularly successful subsequent productlaunches, such as Ford's Mustang and IBM'sSystem 360. Initiatives may be pursued with theexplicit recognition that they are likely to fail(Lynn, Morone, & Paulson, 1997) or may beviewed as part of an entire portfolio of newbusiness development activities (Collins & Por-ras, 1994: 140-168). What matters is that theyenhance the firm's accumulated resource andknowledge base by reducing uncertainty, in-creasing variety, and expanding the search foropportunity (March, 1991).

Just as national policies influence the struc-ture of payoffs to entrepreneurs at a societallevel, business policies influence the rewardsand sanctions for entrepreneurship within afirm. Senior executives influence entrepreneur-ial effort through their policies, including pro-

16 Academy of Management Review January

motion, pay, and recognition, as well as throughtheir disposition of firm-controlled assets, suchas physical facilities and capital (Hambrick &Mason, 1984).

Implications of using real options reasoning.Four observations regarding a real options ap-proach apply across both the societal and thefirm levels of analysis. First, options are bestvalued as part of a "bundle." Second, uncertain-ty—and hence potential variance—is key to thevalue of an option. Third, failures can have pos-itive consequences. Fourth, preventing failurecan mean sacrificing opportunity. If one under-stands these commonalities, one can use realoptions reasoning to develop a more balancedtheoretical perspective on failure.

Note that I do not mean to suggest that failureis desirable in and of itself. It can be painful andcostly, can generate vicious cycles of discour-agement and decline, and can obviously be mis-managed. These well-known drawbacks tend,however, to distort how failure is conceived. Theconsequent antifailure bias can lead to the lossof many of failure's most important lessons andto unanticipated negative consequences.

ADDRESSING ANTIFAILURE BIASES THROUGHREAL OPTIONS REASONING

Real options reasoning suggests that the keyissue is not avoiding failure but managing thecost of failure by limiting exposure to thedownside while preserving access to attractiveopportunities and maximizing gains. A highfailure rate can even be positive, provided thatthe cost of failing is bounded. For instance,"churn" (high rates of business founding andexiting) is associated with economic vibrancy(Birch, 1979).

Changing one's perception of failure can re-quire adjusting fundamental assumptions re-garding performance. As March and Shapira(1987) observe, failure as manifested in risk tak-ing that goes badly is considered undesirable.Therefore, people seek success and avoid fail-ure, and those efforts can introduce errors inlearning and interpretation processes. Paradox-ically, such errors often make failure more likelyor more expensive than it need have been (seeLevinthal & March, 1993). Errors fall into threebroad categories: (1) errors caused by extrapo-lating to the future from past success, (2) errorsowing to cognitive bias, and (3) errors intro-

duced through interventions to avoid the occur-rence or appearance of failure. Table 1 providesa summary.

Unintended Negative Consequences of anAntifailure Bias

Extrapolating to the future from past success.Economic systems are like others in that theyoversample success and undersample failure(Levinthal & March, 1993: 110). Hence, generaliz-ing from observation can be a poor guide forfuture action (see Sitkin, 1992: 255). Further, sinceroutines are used for most ongoing operations,those not associated with failure are likely to beretained. These are then applied to new situa-tions, whether or not they are appropriate (Nel-son & Winter, 1982). A related phenomenon is thecompetence trap. Unless management deliber-ately takes countermeasures, success in the ap-plication of one routine or technology tends todecrease an organization's willingness and ca-pacity to adopt a new one, even if the new oneoffers long-term performance benefits (Levitt &March, 1988). The sad fate of incumbents con-fronting innovations introduced by newcomersillustrates this point (Tushman & Anderson,1986). In short, a major unintended consequenceof seeking success and avoiding failure is atendency to bring into the future not only thevaluable lessons learned from the past but alsothe distortions of those lessons.

Cognitive biases. Well-known psychologicalphenomena, such as the confirmation bias (seeKahneman, Slovic, & Tversky, 1982), systemati-cally lead people to reject information thatmight indicate that their current assumptionsare incorrect. When making decisions, individ-uals may see information with negative conno-tations as less vivid, plausible, visible, or avail-able, whereas they readily accept informationwith positive connotations (Kiesler & Sproull,1982). By implication, many judgments on costs,revenues, opportunities, and outcome distribu-tions are likely to be wrong. Furthermore, en-trants in a new area often behave like lem-mings. If they conclude that growing marketsare attractive, they may overlook the fact thatmany other players may be making an identicalevaluation. One inadvertent result is an in-crease in the probability of failure for any givenentrant. For example, in the early days of theWinchester disk drive industry, over a hundred

1999 McGiath 17

TABLE 1Examples of the Unintended Consequences of an Antifailure Bias

Antecedent EffectPotential BiasesIntroduced

Potential UnintendedConsequences

Examples from theEntrepreneurial Process

Extrapolating to the future from past success

Oversamplingsuccess andundersamplingfailure (Levinthal &March, 1993).

Successes are morewidely representedin survivor samplesthan failures are.Samples are leftcensored (Aldrich &Fiol, 1994).

Routinization, inwhich practicesperceived to beassociated withadequateperformance areretained andrepeated, whereaspractices perceivedto be associatedwith inadequateperformance(failure) areavoided.

Incorrect inferenceswhen generalizingfrom observedbehavior. Success isseen as more likelythan it really is;failures are seen asless likely than theyreally are; factors thatpowerfully predictperformance are seenas weaker than theyreally are.

Responses to theenvironment areselected from anarrow range ofpath-dependentlyacquired routines—not from allpossible choices.These, further,have many tacitelements,rendering theirfunctioning difficultto understand andreplicate.

Misspecification ofcausal relations, as insuperstitious learningbased on spuriouscorrelations ordownward bias infactors that actuallydo drive performance.

New situations areapproached the wayprevious ones were,regardless of thecausal structure thatunderlay the oldroutine (Nelson &Winter, 1982).

Routines that wereeffective in a knowncontext fail whenapplied to a new oneor are continued to thepoint at which theygenerate what Starrand Bygrave term the"liabilities ofstaleness, sameness,priciness, andcostliness" (1992: 353).

Gimeno et al.'s (1997)study, in whichspurious correlationsfrom biased survivorsamples make it seemthat intrinsicallymotivatedentrepreneurs havelower performance.The correctinterpretation, theyargue, is that thosewho are intrinsicallymotivated are willingto accept lowerperformance.

Blockbuster Video'sventure into Germany,in which establishedpractices that work inthe United Statesproved not to appealto sufficient numbersof German consumers.For instance.Blockbuster stocksonly familyentertainment andmovie classics,whereas one-third ofGermany's $510million rental marketis composed of movieswith sexual or violentthemes. Blockbusterwithdrew from theGerman market inNovember 1997.

Improvement andimitation. Likeroutinization, theseprocesses decreasethe variety ofroutines available(Levinthal & March,1993; Levitt &March, 1988; Meyer,1997).

Increasingcompetence atachieving knownresults;development ofspecializedroutines andcospecializedassets.

Decreased variety andabsorptive capacity;greater "simplicity"(Ashby, 1956; Miller,1993). Existing levelsof competence becomethe standard;alternatives that mayrepresent a betterlong-run solution arerejected in the short

Competence traps and"core rigidities," inwhich success at theapplication of aninferior technologyinhibits the adoptionof a superior one(Levitt & March, 1988)or creates inertia(Leonard-Barton, 1992).Increasedvulnerability of thesystem to a change inconditions.

A tendency for thosewho enter early intoan arena to lose out tolater entrants (Aldrich& Fiol, 1994). This iscommon in the case of"competence-destroying"innovations (Tushman& Anderson, 1986).

18 Academy of Management Review January

TABLE 1(Continued)

Antecedent EffectPotential BiasesIntroduced

Potential UnintendedConsequences

Examples from theEntrepreneurial Process

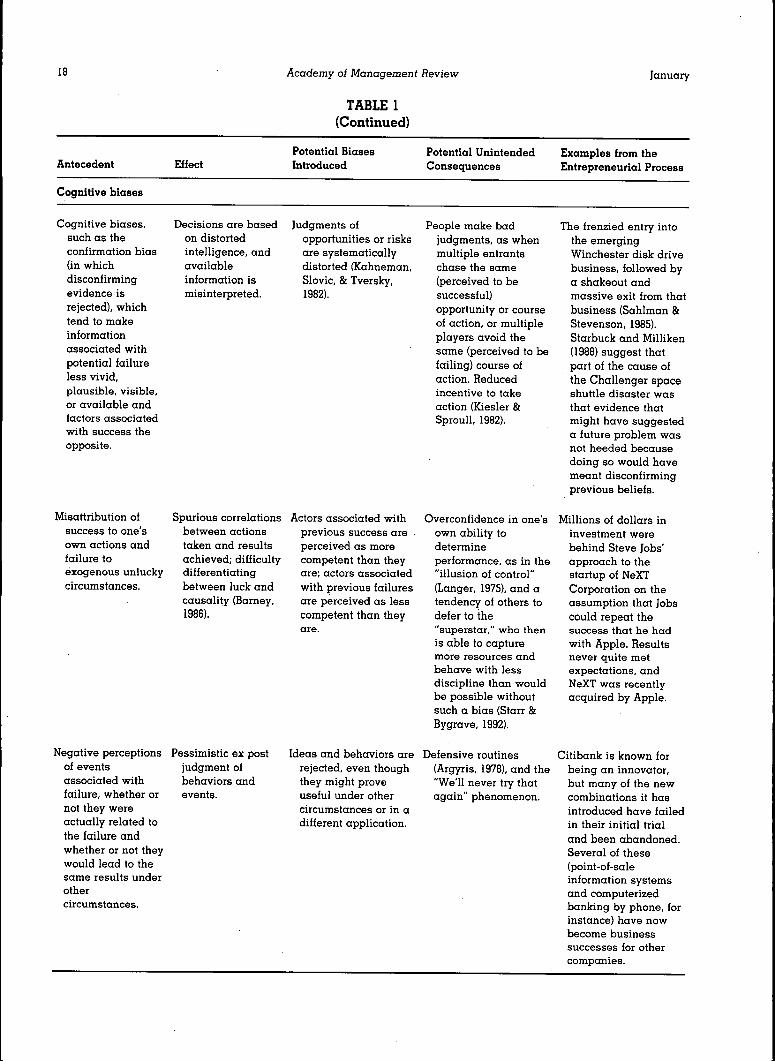

Cognitive biases

Cognitive biases,such as theconfirmation bias(in whichdisconfirmingevidence isrejected), whichtend to makeinformationassociated withpotential failureless vivid,plausible, visible,or available andfactors associatedwith success theopposite.

Misattribution ofsuccess to one'sown actions andfailure toexogenous unluckycircumstances.

Decisions are basedon distortedintelligence, andavailableinformation ismisinterpreted.

Spurious correlationsbetween actionstaken and resultsachieved; difficultydifferentiatingbetween luck andcausality (Barney,1986).

Negative perceptionsof eventsassociated withfailure, whether ornot they wereactually related tothe failure andwhether or not theywould lead to thesame results underothercircumstances.

Pessimistic ex postjudgment ofbehaviors andevents.

Judgments ofopportunities or risksare systematicallydistorted (Kahneman,Slovic, & Tversky,1982).

Actors associated withprevious success areperceived as morecompetent than theyare; actors associatedwith previous failuresare perceived as lesscompetent than they

Ideas and behaviors arerejected, even thoughthey might proveuseful under othercircumstances or in adifferent application.

People make badjudgments, as whenmultiple entrantschase the same(perceived to besuccessful)opportunity or courseof action, or multipleplayers avoid thesame (perceived to befailing) course ofaction. Reducedincentive to takeaction (Kiesler &Sproull, 1982).

Overconfidence in one'sown ability todetermineperformance, as in the"illusion of control"(Langer, 1975), and atendency of others todefer to the"superstar," who thenis able to capturemore resources andbehave with lessdiscipline than wouldbe possible withoutsuch a bias (Starr &Bygrave, 1992).

The frenzied entry intothe emergingWinchester disk drivebusiness, followed bya shakeout andmassive exit from thatbusiness (Sahlman &Stevenson, 1985).Starbuck and Milliken(1988) suggest thatpart of the cause ofthe Challenger spaceshuttle disaster wasthat evidence thatmight have suggesteda future problem wasnot heeded becausedoing so would havemeant disconfirmingprevious beliefs.

Millions of dollars ininvestment werebehind Steve Jobs'approach to thestartup of NeXTCorporation on theassumption that Jobscould repeat thesuccess that ho hadwith Apple. Resultsnever quite metexpectations, andNeXT was recentlyacquired by Apple.

Defensive routines Citibank is known for(Argyris, 1978), and the being an innovator,"We'll never try thatagain" phenomenon.

but many of the newcombinations it hasintroduced have failedin their initial trialand been abandoned.Several of these(point-of-saleinformation systemsand computerizedbanking by phone, forinstance) have nowbecome businesssuccesses for othercompanies.

1999 McGrath 19

TABLE 1(Continued)

Antecedent EffectPotential BiasesIntroduced

Potential UnintendedConsequences

Examples irom theEntrepreneurial Process

Negativeretrospectiverecollection ofevents associatedwith failure.

Events associatedwith a past failureare suppressed, nottalked about, oravoided.

Firms and individualsfail to learn from theirexperiences and mayrepeat the samemistakes over and

Negative feedback The Swiss watchdepresses estimates of industry repeated theorganizational .performance andpersonal effectiveness(March & Sutton, 1997:701).

same strategy ofmoving tosuccessively higher-quality, higher-pricedwatches in the face ofthe introduction ofdigital technology. Itlost the bulk of itsmarket and only .regained a strongposition in watcheswith a completelydifferent approach—the Swatch watch.

Direct interventions

Manipulation ofmetrics to producemeasures thatreflect success,regardless ofactual results(Meyer, 1997).

Diversion ofresources tosupportunderperforminginitiatives fornoneconomicreasons (Meyer &Zucker, 1989;Watson & Everett,1996).

The correlationbetween measuresand outcomesweakens; measuresthemselves lose .variance.

Delays or preventsexit (Gimeno et al.,1997); delays orprevents otherkinds ofunpleasant butpotentiallynecessary actions.

Distortion of the original Inability to adequatelymeaning or value ofmeasures; self-servingor unethicalmanipulation ofinformation to avoidthe appearance offailure.

Distorts information;weakens therelationship amongaspirations, slack, andperformance, whichcan distort incentivesfor search andimprovement (Cyert &March, 1963). Cancreate a false sense ofconfidence.

assess outcomes ortheir relationship toaspirations. Marketsbecome less efficient.

Intentionallymisinforminginvestors and otherstakeholders (seeCable & Shane, 1997).

Destroys economic valuefrom the shareholder'sperspective (Meyer &Zucker, 1989);encourages riskierbehavior owing toprotection from itscosts; createsopportunity costs asvaluable resourcesand talents aretrapped; limits searchfor better alternatives.

Practices of the Koreanchaeboi, in whichfunds are diverted tounderperforming unitsto mask performanceproblems (TheEconomist, 1998);practices ofgovernments andother assistanceprograms that helpsmall firms and bailout large ones.

Asymmetricallocation of thepenalties of failing.

Those who try andfail bear all thecosts; those whofail to try escapeunscathed.

Uninvolved actors canbenefit frominformation generatedby a failed attemptwhile incurring noneof its risks.

Creates a disincentivefor taking initiative;free riding andopportunism problemscan become pervasive(March & Shapira,1987).

The often-cited situationin large Japanesecompanies, in whichthe perception is thattaking initiative is notgoing to be rewarded(Tezuka, 1997).

new entrants developed the same optimisticscenarios and entered en masse. Few remainedafter a nasty shakeout (Sahlman & Stevenson,1985).

A second cognitive bias is the tendency toattribute success to one's own actions and fail-ure to bad luck (Staw, McKechnie, & Puffer, 1983).This results from difficulty distinguishing be-

20 Academy of Management Review January

tween luck and causality (Barney, 1986). Conse-quences include overconfidence in one's ownefficacy (Langer, 1975) and a tendency on thepart of others to assume that previous successimplies superior ability. Entrepreneurs whohave attained superstar status may not only be-lieve themselves to be more gifted than theyactually are, but they may also draw investmentand attention that they do not merit. For in-stance, consider the substantial backing thatflowed into Steve Jobs' NeXT software on thebasis of his previous substantial success at Ap-ple. As Starr and Bygrave (1992) argue, success-seeking supporters are unlikely to impose disci-pline or offer constructive criticism, ironicallyrendering disappointment more likely. DisneyCorporation's foray into Europe demonstrates asimilar phenomenon at the firm level.

The flip side of this bias is the perception thateverything associated with a failure is bad,whether causally related to the failure or not.Firms in the grips of this perception gain noth-ing from their failed attempts. One example isCitibank's venture into point-of-sale data re-cording. Citibank pioneered the use of an elec-tronic card to identify, by household, whatbrands of goods were being purchased in super-markets. Unfortunately, the bank did not opt fora gradual launch in some test markets, as realoptions reasoning might have suggested wouldmake sense. Instead, they launched nationally,making an investment of over $100 million.When the market did not materialize as quicklyas expected. Citibank terminated the venture.Real options reasoning suggests that the bank-ers should have redirected the effort to make useof the reduction of uncertainty that the launchallowed. Finally, because Citibank terminatedthe people and sold off the assets deployed inthe initiative, instead of recycling them, thebank was less able to capture benefits by reduc-ing the uncertainty its other ventures faced.Ironically, the lessons were not lost on Citi-bank's rivals, many of which have since enteredwhat is now seen as a profitable, high-growthbusiness.

Direct manipulation. Distaste for failure alsocan lead to behavior that seeks to avoid failureunscrupulously. Metrics can be manipulated.Meyer (1997) uses as his example teachers whotrain students to take tests (because good testscores are a measure of success), which reducesthe power of the test to indicate how much stu-

dents actually have learned. Populations fromwhich metrics are drawn also can be skewed.For example, business schools can reject stu-dents with low Graduate Management AptitudeTest (GMAT) scores to bolster their average re-ported GMAT. Less benign manipulations ofmetrics occur when entrepreneurs want to pro-vide incorrect or misleading information, as Ca-ble and Shane (1997) observe may plausibly bethe case when entrepreneurs deal with venturecapitalists.

Another form of failure avoidance occurswhen resources are diverted to support initia-tives that might otherwise be cancelled orclosed down. Important stakeholders may valuethe survival of the firm more than economic re-turns to shareholders, therefore causing it tosurvive (Meyer & Zucker, 1989). Some businessesare valued for reasons that are intrinsic or psy-chological, as when they represent a family tra-dition; are an extension of an enjoyable activity(e.g., a hobby); or reflect personal values, suchas independence, held by the entrepreneur (Gi-meno et al., 1997). Governments divert resourcesto bolster poorly performing businesses for avariety of reasons: to preserve or protect compe-tition in an industry (e.g., when the governmentrescued Chrysler Corporation), to sustain em-ployment (Storey, 1997), or to redress formerlydisadvantaged groups. Companies, too, some-times use cash flows from high-performing busi-nesses to support poorly performing ones. TheKorean chaebol have been criticized for takingthis to such an extreme as to make their finan-cial statements meaningless {The Economist,1998).

Finally, the systemic desire to avoid failuresometimes is manifested by individuals or firmsallocating all the penalties for failure to thosejudged to be responsible. This allows the unin-volved to benefit in two ways: (1) they avoid thecost of failing, and (2) they can potentially ben-efit from the new knowledge and insight createdby the failed attempt! Such an asymmetric allo-cation of costs reduces the incentive to engagein entrepreneurship; can deter future entrepre-neurial efforts; and (when those who fail exit)can cause loss of organizational memory, exac-erbating cognitive biases (March & Shapira,1987). Free riding and opportunism are relatedissues. A system in which it is better not to failthan to succeed has been blamed for a lack of

1999 McGiath 21

innovation in large Japanese companies (Te-zuka, 1997).

An antifailure bias can, in short, have coun-terintuitive negative effects. It can interfere sig-nificantly with people's ability to make senseout of experience. This, in turn, means that fail-ures are not (to borrow Sitkin's [1992] phrase)"intelligent." I hope to show that theory basedon real options reasoning can foster a more bal-anced view of the relationship between failureand wealth creation. The resulting policiesshould (1) generate increased variance, (2) allowoptions with poor prospects and little value tobe terminated, and (3) make action more attrac-tive than passivity, despite the possibility offailure.

Avoiding Unintentional Bias by IncreasingVariance

When people seek success in order to avoidthe downsides, they look for opportunities tolower variance. The somewhat counterintuitiveeffect is to decrease option value, because vari-ance is to a real option what volatility is to afinancial one (McGrath, 1997). The question is,how can entrepreneurial processes increasevariance in the face of powerful forces that seekto reduce it?

According to conventional thought, motivationto pursue high-variance opportunities is a func-tion of the availability of resources, or slack(March & Simon, 1963: 146), and the perception ofa gap between current performance and somehigher aspiration (see March & Sutton, 1997: 701).Availability of slack, meaning resources not yetcommitted to other firm efforts, permits experi-mentation to occur, while performance not yet ataspiration levels induces search. Performancegaps can stem either from recent poor perfor-mance (threatening failure) or from the percep-tion of opportunity. In either case the availabil-ity of slack, coupled with the motivation forsearch, will intensify the search for variance,because in this condition experimentation withnew combinations of resources is possible andsearching in new, higher-variance directions isperceived as desirable.

Proposition 1: Other things beingequal, at the industry and firm levels,the higher the motivation for searchand the more slack available, the

greater the variance in returns thatwill be sought and the higher the re-sulting option value will be.

Where, however, does slack come from?Industry level. Aldrich and Fiol (1994) observe

that established institutional forces (such as thebehavior of incumbents, rules set up by stan-dards bodies, acceptance of dominant designs,government regulations, and so forth) dictatewhich factors of production used in which com-binations will be considered legal and legiti-mate. These limits establish boundary condi-tions of variance for an industry. Other thingsbeing equal, and assuming reasonably efficientcapital markets, in an established industry theamount of slack in the form of capital availablefor investment in new initiatives is likely to re-main within a range consistent with the ex-pected value and variance of returns in the in-dustry (Stewart, 1991). Further, new initiativesare apt to enter the industry near its mean per-formance level.

Disrupt established industry boundaries,however, and the pattern of risk and reward isdisrupted as well. This gives options-orientedinvestors (Schumpeter's [1934] "capitalists") theincentive to increase available slack in the formof investment funds in the pursuit of higher re-turns, and it gives entrepreneurs the incentive touse the capital for search in the altered industryspace. Consider the current frenzy of entry intoInternet-based businesses, into telecommunica-tions, and into such formerly moribund industryspaces as the recently deregulated electric util-ities industry. The perception of high-varianceopportunity has caused enormous diversion ofresources into these industries, permitting theformation of thousands of new firms. Thisgrowth has dramatically increased the variancein returns within each industry and, conse-quently, their option value.

As the examples suggest, although disruptionof industry boundaries is sometimes a functionof relatively exogenous Schumpeterian pro-cesses at the industry level, governments andother institutional actors often play a significantrole. When these actors restrict potential changein the industry, potential variance of opportuni-ties is limited, and the option value of the entireindustry is reduced. Aldrich and Fiol, for exam-ple, observe that state regulation of the funeralhome business suppressed founding rates and

22 Academy of Management Review January

"almost totally" suppressed the emergence ofcompeting industries (1994: 646). The importantpoint for our purposes is that, often, such vari-ance-restricting behavior is a function of thedesire of incumbents and their supporters toavoid challenges (and concomitant potentialfailure).'

Firm level. If high-revenue opportunities aresparsely scattered, policies .that encouragesearch over a wide area will tend to be morelikely to discover them than policies that focuson a circumscribed area. Unlike capital markets,however, which can rely to some extent on aninvisible-hand approach to the allocation ofslack to high-variance opportunities, firms usu-ally depend on managerial policy to accomplishthis. Only managerial policy is likely to over-come internal competition from lower-variance,more powerful, and often more immediatelyprofitable existing businesses and to allocateslack to new initiatives (see Block & MacMillan,1993). Moreover, the pursuit of success often ini-tiates a process of organizational simplification(Miller, 1993) that makes sustained pursuit ofvariance difficult.

Monsanto's entry into agricultural biotechnol-ogy highlights these problems. Beginning in thelate 1960s, a high-variance-seeking initiativeinto biology was undertaken by a few scientistsseeking to depart from the Agricultural Productsgroup's focus on chemicals. Throughout thecourse of the next three decades, the biologyprogram consumed over $2 billion. It risked ter-mination dozens of times, faced vicious compe-tition from other Monsanto programs, and washaunted by the possibility that government offi-cials would be leery of permitting geneticallyaltered plants to be farmed outdoors. Accordingto company documents, only strong support forthe program on the part of senior executivesenabled it to continue (Rogers, 1998). Ironically,although the biotechnology program has beenjudged a major success, management plans tosplit the firm into a chemicals company and alife sciences company, thereby decreasing the

' This is one oi the problems with the deliberate creationof entry barriers in traditional competitive strategy (Porter,1980). To the extent that entry barriers limit potential vari-ance within an industry, the option value of that industry isreduced, slack is likely to flow elsewhere, and the entiresystem can come to be increasingly vulnerable to invasionby another industry.

pursuit of high variance that the entry into bio-technology made possible in the first place.

As this example suggests, increasing thesearch for high variance within a firm is not atrivial problem. One solution, long proposed inthe corporate venturing and innovation litera-ture, is structural separation of variance-increasing subunits from variance-reducingones (see, for instance, Tushman & O'Reilly,1997). This has the effect of increasing the num-ber of choices the firm may make, in that it is fareasier to instill separate budgeting, control, andadministrative processes for different units.

One effect of such structural separation is tocreate more environments in which the liabili-ties of failure avoidance may be escaped. Theparent organization, for instance, may be able toavoid applying existing routines to new prob-lems and may create conditions in which unex-pected results can yield valuable reduction ofuncertainty. When Citibank entered the con-sumer credit card industry, for instance, the ini-tial idea was to cross-market credit cards tobranch banking customers. Disappointing re-sults led to an organizational move out of thebranches into a separately funded and man-aged initiative designed specifically to pursuenew business opportunities in nonbranch con-sumer markets. 'The initiative that eventuallybecame a spectacular success differed in signif-icant ways from retail branch banking (e.g., theideal credit card customer is not a saver but aborrower).

The point is that, absent high motivation,which was generated by a combination ofstrong corporate emphasis on innovation and awillingness to allocate available slack to a newstructure, early poor results could easily haveterminated the venture. In short, as Bowman andHurry (1993) observe, organizational structuresthat facilitate the opening and exercising of in-dividual options through the existence of differ-entiated subunits have the potential to generategreater potential variance in outcomes for a firm(see also Bowman & Moskowitz, 1998). This im-plies that large firms, in particular, should pur-sue multiple options in many subunits, ratherthan only a limited number of large opportuni-ties.

Proposition 2; Given motivation toisearch for high-vaiiance opportunitiesand allocation of slack at firm level, a

1999 McGiath 23

portfolio of options structured so thatindependent decisions can be made tosupport or withdraw from individualentrepreneurial initiatives will havegreater upside potential than a port-folio in which one choice affects mul-tiple entrepreneurial initiatives.

This brings us to the question of the cost offailure. So far, I have addressed the first impli-cation of real options reasoning—namely, thatthere are benefits to be gained from the pursuitof high-variance opportunities, even if that pur-suit increases the potential for failure. But whatof a second consideration in real options reason-ing, which is to contain the downside cost ofthose failures that occur? Next, I consider theimplications both for parsimony in the creationof new options and discipline in closing them.

Parsimony in the Pursuit of an OptionsStrategy

One of the key implications of real optionsreasoning is that investments should be madesequentially so that major commitments aremade only if circumstances are favorable(McGrath, 1997). This has strategic implications.First, initiatives that promise high upside vari-ance in potential profits are likely to havehigher option value by constraining levels ofcost. Consider, for instance. Block and Subba-Narasimha's conclusion with respect to corpo-rate ventures that "overall firm performance inventuring is most likely determined by the sizeof the losses in the losers, rather than percent-age of ventures that are profitable" (workingpaper, cited in Block & MacMillan, 1993: 334).Second, options must be extinguished ruthlesslywhen they no longer promise high upside poten-tial.

With financial options, decisions regardinginvestment and exercise are relatively straight-forward, in the sense that individuals can usemathematical models. Such decisions are moreproblematic for real options, because the esti-mation of future prospects is highly uncertain,the decision to terminate is often painful, andthe time by which the decision must be made isopen—there is no strike date for most real op-tions. These facts suggest that just as processesthat increase potential upside variance can in-crease option value, a complementing set of pro-

cesses that contain costs similarly can have apositive effect on the value of an entrepreneur-ial options portfolio.

Sitkin's (1992) distinction between failureswith little learning benefit and intelligent fail-ures is useful here. Intelligent failures are thosein which expectations are not met but some-thing useful for the future is learned. They resultfrom "thoughtfully planned action," in which re-sults can be compared with plans to achieveincreasing understanding. The process is equiv-alent to the systematic conversion of assump-tions to knowledge often advocated in the liter-ature on new business planning (Block &MacMillan, 1985; McGrath & MacMillan, 1995).

To generate valuable insight, individualsplanning entrepreneurial initiatives might in-corporate the equivalent of clearly articulatedresearch hypotheses as assumptions, which cantheri be subject to disciplined assessment. Newinformation serves to improve assumptions.This approach introduces a perspective on devi-ations from plan that is quite different from re-garding deviations as mistakes, and it alsocounters several of the cognitive biases result-ing from the avoidance of failure. The approachcan counter escalating commitment, for in-stance, because it offers a way to identify whenthe provision of resources for noneconomic rea-sons is preventing failure (Meyer & Zucker, 1989;Ross & Staw, 1986), and it can mitigate suchbiases as the confirmation bias, because plan-ning to validate assumptions requires the sys-tematic acquisition of potentially disconfirminginformation. Through disciplined modeling, itcan reduce the tendency to draw conclusionsfrom spurious positive or negative correlations.

Proposition 3: At the firm level, plan-ning processes that treat deviations asvehicles for testing assumptions,rather than as failures, are more likelyto permit the early redirection of re-source inflows to or termination of anentrepreneurial initiative, thus con-taining costs and increasing the valueof the options portfolio.

Recognition that initial hypotheses are incor-rect and prompt redirection of strategy withoutadditional investment are consistent with theprinciple of "asset parsimony" (Hambrick &MacMillan, 1984). This principle suggests that,in uncertain environments, the benefits to be

24 Academy of Management Review January

gained by early containment of fixed costs andavoidance of irreversible investments are con-siderable. This applies even though total re-turns from a successful modified project may besomewhat less than returns from a successfulstrategy involving fixed assets and irreversiblecommitments—directly analogous to the situa-tion with real options reasoning, in which somepotential upside gain may be sacrificed in orderto capitalize on the option value of having alter-natives. By funding sequentially, and then put-ting in place mechanisms to spot signals of ad-verse changes in future value and adjustingexpenditure patterns accordingly, the price of areal entrepreneurial option may be contained.The fewer the resources absorbed by initiativeswith little option value, the more they are freedto pursue attractive opportunities.

Planning aside, other mechanisms are associ-ated, at both the firm and industry levels, withreducing the potential losses from entrepreneur-ial initiatives. At the industry level, those whoprovide slack to new ventures are well known toutilize mechanisms for containing their costs.Venture capitalists, for instance, typically se-quence rounds of financing contingent upon theachievement of milestone objectives agreed toin advance (Fast, 1981). Firms that seek to ac-quire capital through an initial public offeringface due diligence inquiries and the scrutiny offinancially interested parties, such as investors,investment banks, and analysts. Within a firm,those who provide resources for corporate entre-preneurial initiatives may employ similar tech-niques. They are likely to utilize such mecha-nisms as the timed release of funds and highhurdle rates to impose the discipline of assetparsimony upon internal ventures (Dixit & Pin-dyck, 1994: 47-48).

Proposition 4: Other things beingequal, the more the potentialdownside of each initiative in an op-tion portfolio is bounded by limitingfixed costs and irreversible invest-ments, the greater the bundled valueof the portfolio will be.

Just as the resource allocation process in anindustry or firm influences which options will beopened and at what cost, so the payoff structurehelps determine which will be terminated orpermitted to expire. The structure of payoffs is aterm used by Baumol (1993) to indicate the re-

wards and sanctions a society offers for variouskinds of economic activity. Here, the question ofhow much flexibility there is within a portfolioof options becomes important.

Consider an economy such as that of Korea,which is dominated by huge conglomeratefirms—the chaebol. From the perspective of pol-icy makers in Korea, each chaebol group repre-sents a single option on a portfolio of assets (aswell as a source of desperately desired employ-ment and other social goods). The policy alter-natives available should an entire chaebol ap-pear to be at risk are fairly straightforward: itcan be allowed to fail or it can be supported.Policy makers, in effect, have no choice. Giventhe trauma of repeatedly having entire conglom-erates fail, it is hardly surprising that resourcesare channeled into supporting the chaebol, evenin the face of clear evidence of poor performance(and international criticism).

Consider an alternative model, in which pol-icy makers could elect to support (or not) each ofthe member businesses on a separate basis.Such an approach represents a portfolio of op-tions, rather than a single option on a businessportfolio. The impetus to offer special protectionto any one of them is likely to be lower, and theability to contain the costs of supporting chosenbusinesses is likely to be greater as well. Thisapproach both increases flexibility and de-creases costs.

A similar argument can be made at the firmlevel. Companies that make huge, irreversibleinvestments as single attempts at innovationrisk suffering losses that are enormous, com-pared to losses risked by companies that en-gage in many smaller initiatives (consider Ex-xon's failed multibillion-dollar venture into oilshale, as compared to the continuous innova-tions introduced by 3M).

Proposition 5: In the long run, the dis-tribution of the cost of failure for in-vesting in and then foregoing the ex-ercise of options in a portfolio ofoptions will be much narrower thanthe distribution of the cost of failurefor investing the same amount andforegoing the exercise of single op-tions.

Investing with the goal of promoting intelli-gent failure aims at generating insights that canbe useful elsewhere. By taking this sort of ex-

1999 McGiath 25

perimental approach to entrepreneurial in-vestments, firms can reduce incentives to (inten-tionally or otherwise) distort, misuse, ormisunderstand lessons learned from past fail-ures. If executives manage failure intelligentlyby, for instance, conducting constructive post-mortems of option-oriented initiatives, the in-sights derived can be incorporated into a firm'sknowledge base. However, when failures arepainful and become undiscussible, the potentialfor a firm to learn from its mistakes is compro-mised. Indeed, as Lynn et al. (1997) discovered,proactive analysis of failure can sometimes bethe only mechanism by which firms discoverhow new technologies might meet needs thatfuture customers will have by giving these cus-tomers a tangible product to react to.

Action Made More Attractive than Passivity

With financial options, the greater the upsidepotential of the underlying asset on which anoptions contract is written, the greater the valueof the option. By analogy, the more substantialthe upside potential returns on an entrepreneur-ial investment, the more valuable options onthose returns are likely to be. This suggests away to tackle the problem of asymmetric distri-butions of costs and benefits to entrepreneurialactivity.

As I mentioned, Baumol (1993) has long arguedthat the incidence of entrepreneurship is relatedto the structure of payoffs, which is the set ofrules regarding the allocation of gains andlosses to entrepreneurial activities within a so-cial context. Under Baumol's example, societiesthat reward litigation rather than entrepreneur-ship will tend to encourage their brightest peo-ple to become litigators rather than entrepre-neurs.

One result of this is that the value of an en-trepreneurial option may be depressed by soci-etal limitations on upside gains. Many Scandi-navian countries, for example, impose highincome taxes on entrepreneurial proceeds,which has been associated with diminished en-trepreneurial drive in those countries (MacMil-lan, 1995). In many African countries social ob-ligations can cause funds to be channeled toimpoverished family members upon the firstsign of any returns, leading to difficulties insustaining entrepreneurship (Diomande, 1990).And in the United Kingdom the absence of

routes to exit and the illiquidity of funds in-vested in ventures also act to limit upside po-tential (Birley, 1997).

Within corporations, too, it can be difficult tocompensate venture champions adequately. Al-though this may not interfere with the prospectsof a particular venture, if successful championsfind their compensation to be inadequate rela-tive to external opportunities, then a corporationis likely to lose its talent (Block & Ornati, 1987).

By implication, a high level of entrepreneurialactivity is unlikely to be sustained if the upsidepotential rewards are limited and the potentialfor loss unlimited. In that situation doing noth-ing is a far more attractive alternative. To avoidencouraging passivity, a society or firm wouldbe better off using mechanisms that share thecosts of entrepreneurial failure, rather thanheaping financial and social sanctions uponthose who explore entrepreneurial options. Sim-ilarly, a sufficiently large upside must be avail-able to entrepreneurs to encourage the searchfor high-variance opportunities. Such optionlikepayoff structures for entrepreneurial effort trun-cate the downside, increase the expected payoff,and thus create a greater incentive for the en-trepreneur to take action. Such structures alsomake the payoff function more convex, allowingthe entrepreneur to increase expected value fur-ther by increasing his or her risk.̂

Proposition 6: The less the social costof failure in taking entrepreneurialaction, the greater the aggregate levelof entrepreneurial activity and thegreater the cumulative value of thenational portfolio of options will be.

Proposition 7: The greater the gainsfrom successful entrepreneurial ac-tion, the greater the aggregate level ofentrepreneurial activity in an econ-omy or firm and the greater the cumu-lative value of the entrepreneurial op-tions portfolio will be.

Propositions 6 and 7 address the conse-quences of an antifailure bias that discouragesentrepreneurship by penalizing those who tryand holding blameless those who do not. Obvi-ously, there are many mechanisms for institut-ing optionlike payoff structures, each of which

'' I thank an anonymous reviewer for this insight.

26 Academy of Management Review January

has a different cost to government and otherstakeholders in society. It would be worthwhilefor future research to explore such mechanisms.

DISCUSSION AND IMPLICATIONS

Although entrepreneurship in the form ofstartups in a population of firms differs fromentrepreneurship in the form of projects under-taken by a single firm, real options reasoningoffers a useful logic for understanding the im-portance and implications of failure at both lev-els of analysis. At both levels, seeking greaterpotential variance is correlated to greater optionvalue; at both levels, there is much to be gainedby processes through which costs can be con-tained; and at both levels, the incentive to en-gage in entrepreneurial activity increases whenpotential losses are limited and potential gainsare increased. As a theory of real options rea-soning continues to develop, it may become pos-sible to apply these concepts to additional lev-els of analysis. For instance, at the level of theindividual, human and social capital have prop-erties analogous to options investments.

I hope I have demonstrated that real optionsreasoning has the potential to help scholars de-velop a more balanced perspective on the role offailure. Let me now highlight implications ofthis discussion for theory and research in entre-preneurship and the related fields of technolog-ical change and innovation.

First, real options reasoning can provide theconceptual foundation for a new perspective onthe dynamics of performance, survival, andchoice in entrepreneurship. Consider the resultsattained by Gimeno et al. (1997), which showempirically that firms with similar levels of per-formance may experience different exit rates,owing not to exogenous environmental selectioneffects but to the recognition of increased valuefor the founder in exercising options other thancontinuing to invest in the firm. What is good oradequate performance for a firm at one time, byextension, may be seen at a later date as inferiorto the performance that other options generate.Thus, contrary to assertions made by many (par-ticularly in population ecology) that selectionenvironments exert more or less uniform pres-sure to exit, the exit decision is, in fact, to someextent a choice among options with uncertainfuture values. When uncertainties are resolved,alternative options to continuation may be exer-

cised. In future work dealing with organization-al mortality, scholars should, therefore, apply amore discriminating lens to exit and termina-tion.

Second, populations matter, as does the mech-anism through which uncertainty regarding fu-ture outcome distributions is resolved. We mustavoid the same trap that work attempting toexplain performance differentials through theidea of "fitness" (see Drazin & Van de Ven, 1985)must avoid. Just as observed fitness or lackthereof may only mask what is going on at an-other level of analysis, so, too, observed successmay be understood inadequately in studies thatcompare only two, or only surviving, firms. Ineffect, in such studies researchers look only atthe period after uncertainty is resolved, hopingthereby to gain insight useful for guiding invest-ment in the period prior to this resolution. But, aswe have seen, uncertainty reduction for a suc-cessful initiative may come from investmentsmade in a failed one—investments that are notvisible without a population-level lens.

Further, the potential to avoid downsidelosses may be fundamentally related to the typeand number of other initiatives being pursuedsimultaneously. The pursuit of opportunities bymany entrepreneurs at once may result in keyuncertainties becoming resolved more rapidlyand less expensively (on a per firm basis) than ifonly a few entrepreneurs are engaged. In otherwords, if many entrepreneurs are operating, thecost for a given entrepreneur to resolve certaincritical uncertainties can be reduced. This pro-cess cannot be understood simply by studyingthe strategy of the surviving or successful firms.

Third, this discussion suggests that it may beworth pursuing comparative entrepreneurshipresearch, particularly into differences in payoffstructures in different industries and cultures.Real options reasoning suggests that the more apayoff structure involves low or containable riskand the potential for high rewards for the entre-preneur, the more likely it will be to motivateentrepreneurship. The risk component is directlyrelated to institutional and legal structures thatdeal with failure. For instance, in what Hofstede(1980) terms "coUectivist" cultures, bankruptcyoften has a devastating social and economicimpact on the entrepreneur. We can expect in-dividuals in such cultures to assess the poten-*tial downside loss associated with the entrepre-neurial option as far greater than it would be for

1999 McGrath 27

their counterparts in cultures in which failure iseasier to overcome. In an "individualistic" cul-ture such as the United States, for instance, fail-ures are "professionally forgiven" (Petzinger,1997). This reduces potential downside loss,while a tax system that permits the accumula-tion of vast wealth offers a compelling potentialupside. This design maximizes option value forentrepreneurs in the United States.

Fourth, because the value of a real optiondepends to some extent upon subjective judg-ments regarding what is likely to happen in anuncertain future, real options reasoning sug-gests a point of intersection between economicforces and psychological ones. Consider reac-tance. Reactance is a process whereby a personbecomes more motivated to overcome setbacksafter experiencing one. If the subsequent at-tempt is also unsuccessful, reactance can turninto "learned helplessness"—a loss of faith inone's ability to conquer adversity (Brockner etal., 1983). Reactance may have less magnitudeand shorter duration in a culture in which fail-ing is extremely costly than in a culture thattolerates failure better, which, in turn, will influ-ence the number and nature of options opened.

Fifth, in future research scholars might fruit-fully investigate how interfering with the so-called natural processes by which failures occurhas either beneficial or detrimental effects. Ifartificial support allows a high-variance-seeking firm to survive its initial ordeal, theeffects for society can be viewed as positive ornegative: positive, if this assistance allows pro-ductive firms to overcome the vulnerable startupstage and subsequently succeed on their own;negative, if it has the effect of preserving less"fit" firms in the population to underperform andto set a bad example for others. Real optionsreasoning is useful for work of this nature, be-cause it highlights where external interventionhas unintended negative effects and makes po-tential benefits clear.

If, for example, governmental intervention al-lows a failing firm to take out a loan to stave offcertain bankruptcy, what has happened fromsociety's point of view is that this entrepreneur-ial option has just become more expensive.Other things being equal, the increased ex-pense reduces the expected value to be ob-tained from the option—a point that real optionsreasoning would show unambiguously. The realoptions approach reveals that without a con-

comitant increase in the expected gains, suchinterventions are a bad idea. However, govern-ment intervention intended to increase slackavailable to high-variance-seeking initiativesmight be analyzed as a worthwhile investment,even if the new firms experience a high failurerate.

This leads directly to a sixth implication ofthis discussion—namely, that real options rea-soning offers a useful perspective from which toview such governmental policies as regulation.As Aldrich and Fiol (1994) point out, some poli-cies can have the effect of reducing the optionvalue of an entire industry. Loosen the con-straints, as when formerly regulated industriesare deregulated, and an explosion of entrepre-neurial activity often ensues (a current examplebeing the telecommunications and electric util-ity industries).

Similarly, real options reasoning suggests thelimitations in conventional perspectives on vari-ance-reducing competitive behavior by firms.For instance, exploiting dominance in an indus-try with high entry barriers is a relatively low-variance position with limited option value. Areal options view shows that exploiting domi-nance creates vulnerability over the long run,because forces that reduce external (industry-level) variance are likely also to reduce the pos-sible range of organizational responses tocompetitive threat or environmental shift. Cor-respondingly, within a firm, policy decisions areneeded to create greater variety, even in rela-tively stable, oligolopolistic industries. Seniorexecutives may wish to focus greater energy ondeliberate variance generation in the allocationof resources.

CONCLUSION

I began this article with the hope of develop-ing a more balanced theoretical perspective onfailure in the entrepreneurial process. Real op-tions reasoning, which explicitly links economicvalue and uncertainty, offers a useful toolwhereby failure can be reconceptualized. Its pri-mary benefit is its systematic method of linkingpositive and negative outcomes, from which op-erationalizable propositions can be derived forcreating value through entrepreneurship—without the distortions of obsessive failureavoidance.

28 Academy of Management Review January

Real options reasoning suggests that if thepoint of studying entrepreneurship is to under-stand wealth creation, then examining failurerates and individual stories of success and fail-ure stories may miss the heart of the matter. Itmatters relatively little if many inexpensive op-tions expire, provided that returns are substan-tial for the ones that survive. By the same token,high failure rates for entrepreneurial busi-nesses do not really matter, provided that thecost of failing is contained and that the busi-nesses that do succeed enjoy substantialgrowth.

One reason why failure offers benefits is be-cause it is often easier to pinpoint why a failurehas occurred than to explain a success, makingfailure analysis a powerful mechanism for re-solving uncertainty (Sitkin, 1992). By carefullyanalyzing failures instead of focusing only onsuccesses, scholars can begin to make system-atic progress on better analytical models of en-trepreneurial value creation. Such work prom-ises to bring to entrepreneurship research thekind of progress that better valuation modelshave brought to the world of financial options(Black & Scholes, 1973). Indeed, just as a clearerunderstanding of the nature of volatility andrisk has spawned an explosion of instrumentsand products for managing their effects better,so, too, a direct and unflinching look at thedownside of entrepreneurship will create con-siderable opportunities. Perhaps, in entrepre-neurial scholarship to come, intelligent failureswill even be celebrated.

REFERENCES

Aldrich, H., & Fiol, M. 1994. Fools rush in? The institutionalcontext of industry creation. Academy of ManagementReview, 19: 645-670.

Argyris, C. 1978. Strategy, change, and defensive routines.Boston: Pitman Publishing.

Ashby, W. R. 1956. An introduction to cybernetics. London:Chapman and Hall.

Baker, T., Aldrich, H., Langton, A., & Cliff, J. E. 1997. Temperedby the flame: What do entrepreneurs leam from failure?Paper presented at the annual meeting of the Academyof Management, Vancouver, British Columbia.

Barney, J. B. 1986. Strategic factor markets: Expectations,luck, and business strategy. Managemenf Science, 32:1231-1241.

Barro, R. J. 1997. Determinants of economic growth: A cross-country empirical study. Cambridge, MA: MIT Press.

Baumol, W. J. 1993. Entrepreneurship, management and thestructure of payoffs. Cambridge, MA: MIT Press.

Birch, D. 1979. The job generation process. Cambridge, MA:MIT Program on Neighborhood and Regional Change.

Birley, S. 1986. The role of new firms: Births, deaths and jobgeneration. Strategic Management lournal, 7: 361-376.

Birley, S. 1997. Entrepreneurship in ihe U.K. Paper presentedat the Waseda University Entrepreneurial Research Unit1997 International Symposium, Tokyo, Japan.

Black, F., & Scholes, M. 1973. The pricing of options andcorporate liabilities. lournal of Political Economy, 81:637-654.

Block, Z., & MacMillan, 1. C. 1985. Milestones ior successfulventure planning. Harvard Business Review, 63(5): 184-196.

Block, Z., & MacMillan, I. C. 1993. Corporate venturing: Cre-ating new businesses within the firm. Cambridge, MA:Harvard Business School Press.

Block, Z., & Ornati, O. 1987. Compensating corporate venturemanagers. Journal of Business Venturing, 2: 41-51.

Bowman, E. H., & Hurry, D. 1993. Strategy through the optionlens: An integrated view of resource investments andthe incremental-choice process. Academy of Manage-ment Review, 18: 760-782.

Bowman, E. H., & Moskowitz, G. 1998. A heuristics approachto the use of options anal/sis in strategic decision maJr-ing. Working paper. The Wharton School, University ofPennsylvania, Philadelphia.

Brockner, J., Gardner, M., Bierman, J., Mahan, T., Thomas, B.,Weiss, W., Winters, L., & Mitchell, A. 1983. The roles ofself-esteem and self-consciousness in the Wortman-Brehm Model of Reactance and learned helplessness.Joumal of Personality and Social Psychology, 45: 199-209.

Cable, D. M., & Shane, S. 1997. A prisoner's dilemma ap-proach to entrepreneur-venture capitalist relationships.Academy of Management Review, 22: 142-176.

Collins, J. C, & Porras, J. I. 1994. Built to last: Successfulhabits of visionary companies. New York: HarperCol-lins.

Cyert, R. M., & March, J. G. 1963. A behavioral theory of thefirm. Englewood Cliffs, NJ: Prentice-Hall.

Diomande, M. 1990. Business creation with minimal re-sources: Some lessons from the African experience.Working paper, Sol C. Snider Entrepreneurial Center,University of Pennsylvania, Philadelphia.

Dixit, A., & Pindyck, R. 1994. Investment under uncertainty.Princeton, NJ: Princeton University Press.

Drazin, R., & Van de Ven, A. H. 1985. Alternative forms of fit incontingency theory. Administrative Science Quarterly,30: 514-539.

The Economist. 1998. Kill or cure? January 10: 13-14.

Fama, E. F., & Miller, M. H. 1972. The theory of finance. NewYork: Holt, Rinehart, and Winston.

Fast, N. D. 1981. Pitfalls of corporate venturing. Research-Technology Management, 20(March): 21-24.

1999 McGrafh 29

Garud, R., & Van de Ven, A. H. 1992. An empirical evaluationof the internal corporate venturing process. StrategicManagement Journal 13: 93-109.

Gimeno, J., Folta, T. B., Cooper, A. C, & Woo, C. Y. 1997.Survival of the fittest? Entrepreneurial human capitaland the persistence of underperforming firms. Adminis-trative Science Quarterly, 42: 750-783.

Gross, N., Judge, P. C, Port, O., & Wildstrom, S. H. 1998. Let'stalk: Speech technology is the next big thing in comput-ing. Will it put a PC in every home? Business Week,February 23: 61-80.

Hambrick, D. C, & MacMiUan, I. C. 1984. Asset parsimony-managing assets to manage profits. Sloan ManagementReview, 25(2): 67-74.

Hambrick, D. C, & Mason, P. 1984. Upper echelons: Theorganization as a reflection of its top managers. Acad-emy of Management Review, 9: 193-206.

Hayek, F. 1945. The use of knowledge in society. AmericanEconomic Review, 35: 519-530.

Hofstede, G. 1980. Culture's consequences; /nternationa7 dif-ferences in wori-rela(ed values. Beverly Hills, CA: Sage.

Hurry, D., Miller, A. T., & Bowman, E. H. 1992. Calls on high-technology: Japanese exploration of venture capital in-vestments in the United States. Strategic ManagementJournal, 13: 85-101.

Kahneman, D., Slovic, P., & Tversky, A. 1982. Judgment underuncertainty: Heuristics and biases. Cambridge, MA:Cambridge Press.

Kahneman, D., & Tversky, A. 1979. Prospect theory: An anal-ysis of decision under risk. Econometrica, 47: 263-292.

Kets de Vries, M. 1985. The dark side of entrepreneurship.Harvard Business Review, 63(6): 160-167.

Kiesler, S., & Sproull, L. 1982. Managerial responses tochanging environments: Perspectives on problem sens-ing from social cognition. Administrative Science Quar-terly, 27: 548-570.

Kirzner, I. 1979. Perception, opportunity and entreprensur-ship. Chicago: University of Chicago Press.

Knight, F. H. 1921. (Reprinted in 1971.) flisi, uncertainty andprofit. Chicago: University of Chicago Press.

Knight, F. H. 1944. Diminishing returns from investment./our-nai of Political Economy, 52: 26-47.

Kogut, B. 1991. Joint ventures and the option to expand andacquire. Management Science, 37: 19-33.

Kogut, B., & Kulatilaka, N. 1994. Operating flexibility, globalmanufacturing, and the option value of a multinationalnetwork. iVfanagement Science. 40: 123-139.

Langer, E. J. 1975. The illusion of control. Journal of Person-ality and Social Psychology, 32: 311-328.

Leonard-Barton, D. 1992. Core capabilities and core rigidi-ties: A paradox in managing new product development.Strategic Management Journal, 13: 111-126.

Levinthal, D., & March, J. G. 1993. The myopia of learning.Strategic Management Journal, 14: 95-112.

Levitt, B., & March, J. G. 1988. Organizational learning. An-nual Review of Sociology, 14: 319-340.

Lubatkin, M., & Chatterjee, S. 1994. Extending modern port-folio theory into the domain of corporate diversification:Does it apply? Academy of Management Journal, 37:109-136.

Lumpkin, G. T., & Dess, G. G. 1998. Clarifying the entrepre-neurial orientation construct and linking it to perfor-mance. Academy of Management Review, 21: 135-172.

Lynn, G. S., Morone, J. G., & Paulson, A. S. 1997. Marketingand discontinuous innovation: The probe and learn pro-cess. In M. Tushman & P. Anderson (Eds.), Managingstrategic innovation and change: 353-375. New York:Oxford University Press.

MacMillan, I. C. 1995. Supporting entrepreneurship in differ-ent countries and regions. Paper presented at theWaseda University Entrepreneurial Research Unit 1995International Symposium, Tokyo, Japan.

Maidique, M. A., & Zirger, B. J. 1985. The new product learn-ing cycle. Research Policy, 14: 299-313.

March, J. G. 1991. Exploration and exploitation in organiza-tional learning. Organization Science, 2: 71-87.

March, J. G., & Shapira, Z. 1987. Managerial perspectives onrisk and risk taking. Management Science, 33: 1404-1418.

March, J. G., & Simon, H. 1963. (Reprinted in 1993.) Organiza-tions. New York: Wiley.

March, J., & Sutton, R. 1997. Organizational performance as adependent variable. Organization Science, 8: 698-706.

McGrath, R. G. 1996. Options and the entrepreneur: Towardsa strategic theory of entrepreneurial wealth creation.Proceedings of the Academy of Management: 101-105.

McGrath, R. G. 1997. A real options logic for initiating tech-nology positioning investments. Academy of Manage-ment Review, 22: 974-996.

McGrath, R. G., & MacMillan, I. C. 1995. Discovery-drivenplanning. Harvard Business Review, 73(July-August): 44-54.

Meyer, M. 1997. Dilemmas of performance measurement.Working paper. The Wharton School, University of Penn-sylvania, Philadelphia.

Meyer, M., & Zucker, L. 1989. Permanently failing organiza-tions. Newbury Park, CA: Sage.

Miller, D. 1993. The architecture of simplicity. Academy ofManagement Review, 18: 116-138.

Miller, K. D., & Reuer, J. J. 1996. Measuring organizationaldownside risk. Strategic Management Journal, 17: 671-692.

Mitchell, G. R., & Hamilton, W. F. 1988. Managing R&D as astrategic option. flesearch-Technoiogy i^^anagement,27(3): 15-22.

Nelson, R. R., & Winter, S. J. 1982. An evolutionary theory ofeconomic change. Cambridge, MA: Harvard UniversityPress.

Petzinger, T. 1997. The front lines: She failed. So what? An

30 Academy of Management Review January