Fall 2012: Compensation philosophy and practice · Fall 2012: Compensation philosophy and practice...

20

COMPENSATION COMMITTEE LEADERSHIP NETWORK ViewPoints December 13, 2012 TAPESTRY NETWORKS, INC · WWW.TAPESTRYNETWORKS.COM · +1 781 290 2270 Fall 2012: Compensation philosophy and practice On November 7 and 8, 2012, the Compensation Committee Leadership Network (CCLN) convened in New York City for its 18th meeting. Over two days, members discussed a number of topics, including long-term incentive plans, share ownership guidelines, and compensation peer groups. The group was joined by two distinguished guests: David Chun, the CEO of Equilar, and Charles Elson, the Edgar S. Woolard, Jr., chair of the John L. Weinberg Center for Corporate Governance at the University of Delaware. For a list of participants, see Appendix 1 on page 12. Executive summary Long-term incentive plans (Page 1) Long-term incentive (LTI) plans have changed considerably over the past decade and over the last year. This ever-changing environment prompted members to evaluate recent trends in LTI design, particularly the declining use of stock options and the corresponding rise in other forms of equity compensation. Members also discussed how to select the right metrics for evaluating individual and company performance, focusing on the importance of metrics linked closely to successful execution of corporate strategy. Members stressed the importance of board discretion in LTI decision making and the value of regularly evaluating past LTI plan performance. Share ownership guidelines (Page 6) Virtually all CCLN companies set requirements for how much stock certain executives must hold and what they need to do before selling it. The share ownership guidelines are functioning well at most CCLN member companies, with executives holding far more stock than is required under company policy or outsiders’ views of best practice, but members did identify several tactical challenges surrounding their policies, such as how stock price volatility can create noncompliance. Members also discussed the fundamental purpose of share ownership policies: creating a culture of ownership. Members considered how the company, particularly the CEO, can help create a company its employees want to own. Compensation peer groups: challenges and opportunities (Page 8) Members discussed Charles Elson and Craig Ferrere’s new research, “Executive Superstars, Peer Groups, and Overcompensation: Cause, Effect and Solution,” with Mr. Elson. Members agreed that peer groups should not be used mechanistically, but several disagreed with the paper’s thesis that compensation committees over-rely on compensation peer groups when setting executive pay. Members also discussed Equilar’s market-based peer algorithm with Equilar CEO David Chun, finding that it produced superior peer groups to other automated models, such as those used by Institutional Shareholder Services (ISS). Long-term incentive plans Developing long-term incentives (LTIs) for executives is among the most important and challenging duties of a compensation committee, members said. Members were aware that over the past 10 or so years the task

Transcript of Fall 2012: Compensation philosophy and practice · Fall 2012: Compensation philosophy and practice...

COMPENSATION COMMITTEE LEADERSHIP NETWORK

ViewPoints

December 13, 2012 TAPESTRY NETWORKS, INC · WWW.TAPESTRYNETWORKS.COM · +1 781 290 2270

Fall 2012: Compensation philosophy and practice On November 7 and 8, 2012, the Compensation Committee Leadership Network (CCLN) convened in New York City for its 18th meeting. Over two days, members discussed a number of topics, including long-term incentive plans, share ownership guidelines, and compensation peer groups.

The group was joined by two distinguished guests: David Chun, the CEO of Equilar, and Charles Elson, the Edgar S. Woolard, Jr., chair of the John L. Weinberg Center for Corporate Governance at the University of Delaware. For a list of participants, see Appendix 1 on page 12.

Executive summary

Long-term incentive plans (Page 1)

Long-term incentive (LTI) plans have changed considerably over the past decade and over the last year. This ever-changing environment prompted members to evaluate recent trends in LTI design, particularly the declining use of stock options and the corresponding rise in other forms of equity compensation. Members also discussed how to select the right metrics for evaluating individual and company performance, focusing on the importance of metrics linked closely to successful execution of corporate strategy. Members stressed the importance of board discretion in LTI decision making and the value of regularly evaluating past LTI plan performance.

Share ownership guidelines (Page 6)

Virtually all CCLN companies set requirements for how much stock certain executives must hold and what they need to do before selling it. The share ownership guidelines are functioning well at most CCLN member companies, with executives holding far more stock than is required under company policy or outsiders’ views of best practice, but members did identify several tactical challenges surrounding their policies, such as how stock price volatility can create noncompliance. Members also discussed the fundamental purpose of share ownership policies: creating a culture of ownership. Members considered how the company, particularly the CEO, can help create a company its employees want to own.

Compensation peer groups: challenges and opportunities (Page 8)

Members discussed Charles Elson and Craig Ferrere’s new research, “Executive Superstars, Peer Groups, and Overcompensation: Cause, Effect and Solution,” with Mr. Elson. Members agreed that peer groups should not be used mechanistically, but several disagreed with the paper’s thesis that compensation committees over-rely on compensation peer groups when setting executive pay. Members also discussed Equilar’s market-based peer algorithm with Equilar CEO David Chun, finding that it produced superior peer groups to other automated models, such as those used by Institutional Shareholder Services (ISS).

Long-term incentive plans

Developing long-term incentives (LTIs) for executives is among the most important and challenging duties of a compensation committee, members said. Members were aware that over the past 10 or so years the task

COMPENSATION COMMITTEE LEADERSHIP NETWORK

ViewPoints

Fall 2012: Compensation philosophy and practice 2

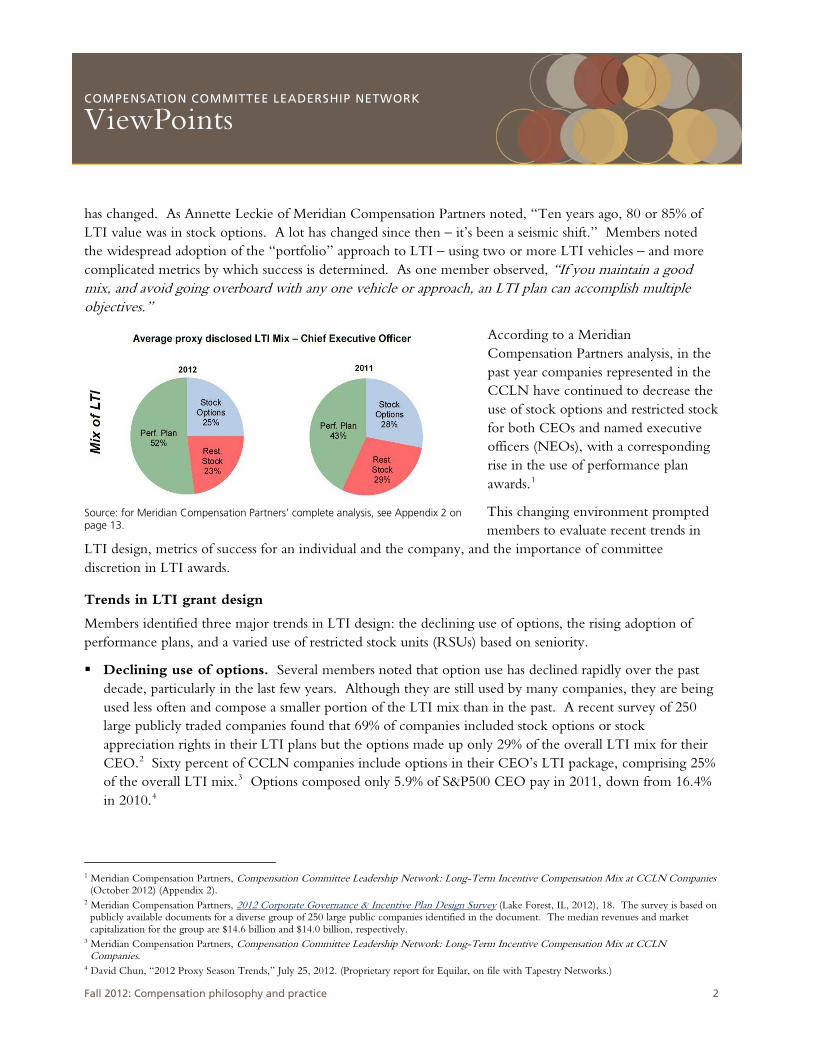

has changed. As Annette Leckie of Meridian Compensation Partners noted, “Ten years ago, 80 or 85% of LTI value was in stock options. A lot has changed since then – it’s been a seismic shift.” Members noted the widespread adoption of the “portfolio” approach to LTI – using two or more LTI vehicles – and more complicated metrics by which success is determined. As one member observed, “If you maintain a good mix, and avoid going overboard with any one vehicle or approach, an LTI plan can accomplish multiple objectives.”

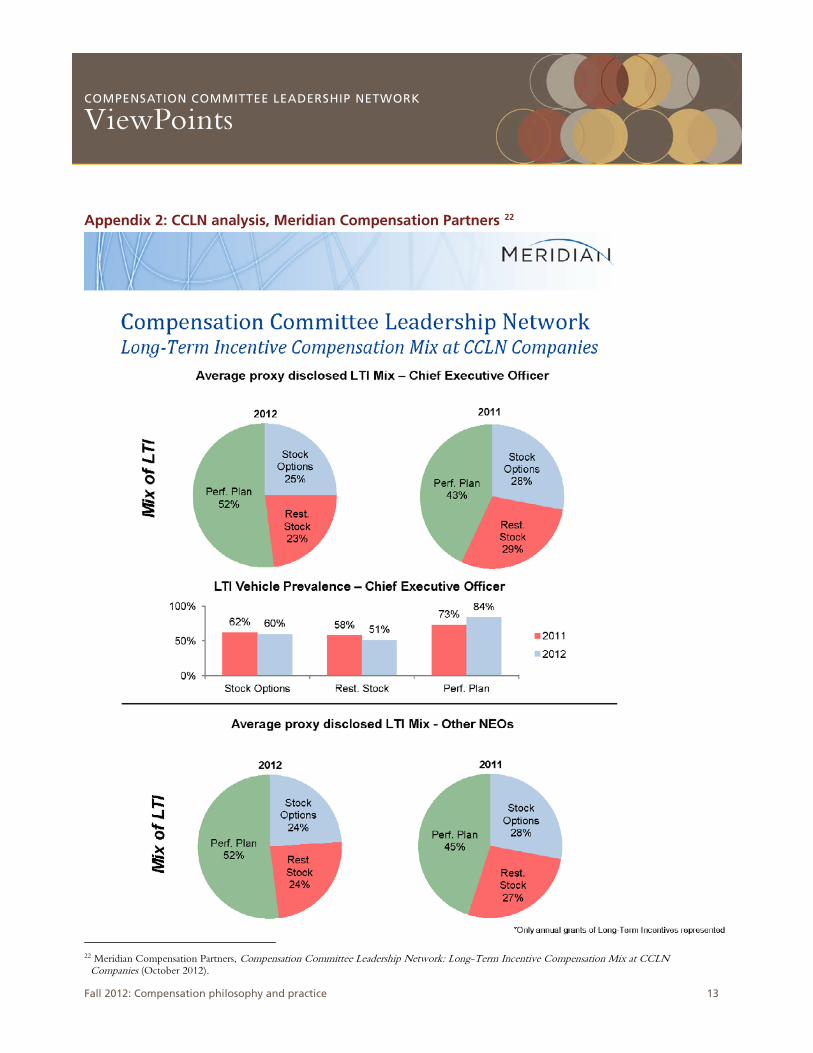

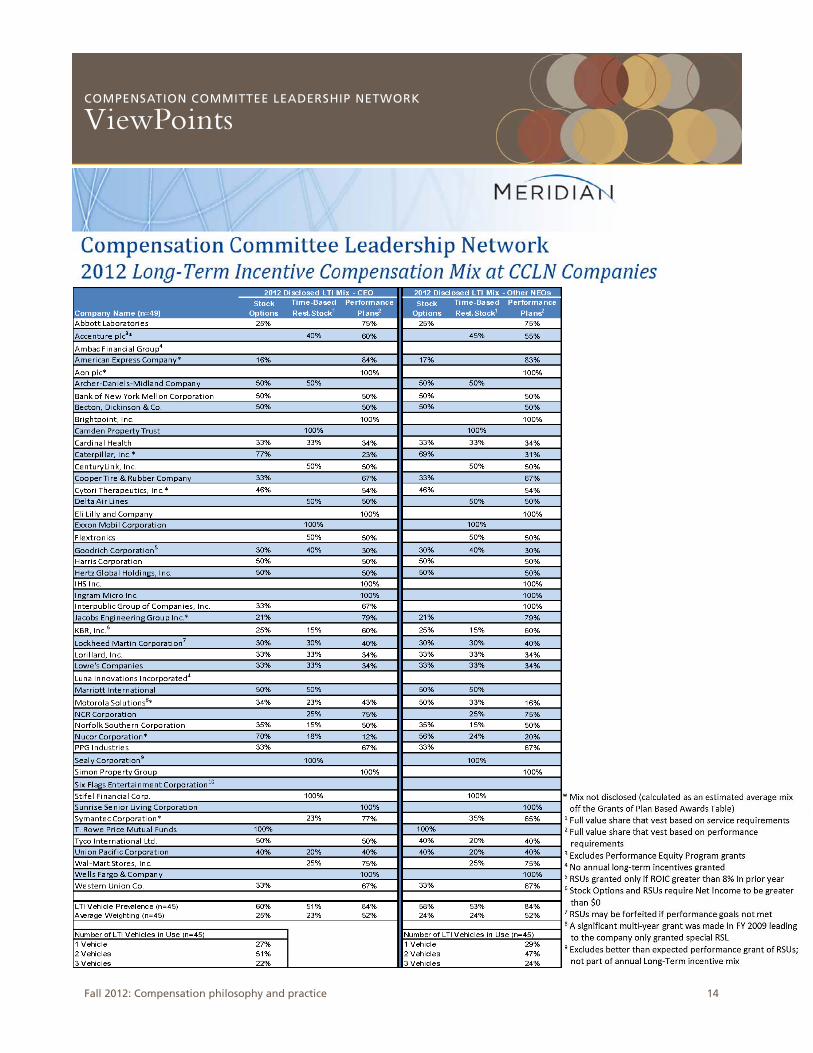

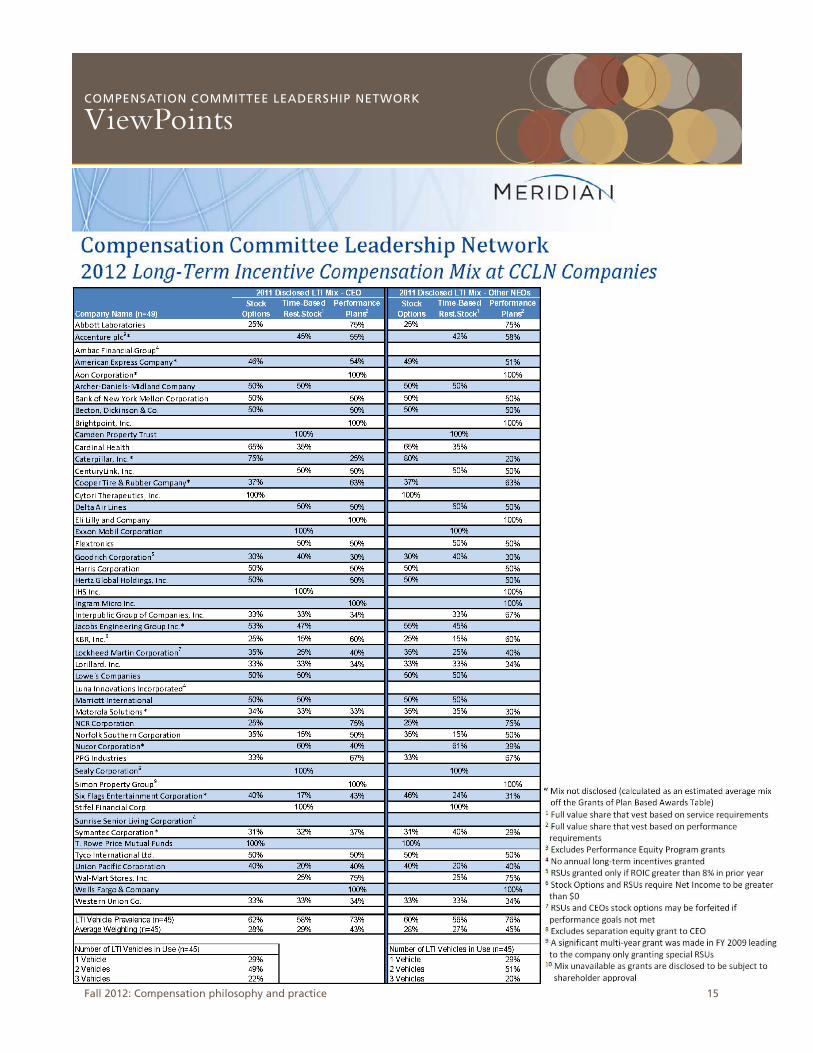

According to a Meridian Compensation Partners analysis, in the past year companies represented in the CCLN have continued to decrease the use of stock options and restricted stock for both CEOs and named executive officers (NEOs), with a corresponding rise in the use of performance plan awards.1

This changing environment prompted members to evaluate recent trends in

LTI design, metrics of success for an individual and the company, and the importance of committee discretion in LTI awards.

Trends in LTI grant design

Members identified three major trends in LTI design: the declining use of options, the rising adoption of performance plans, and a varied use of restricted stock units (RSUs) based on seniority.

Declining use of options. Several members noted that option use has declined rapidly over the past decade, particularly in the last few years. Although they are still used by many companies, they are being used less often and compose a smaller portion of the LTI mix than in the past. A recent survey of 250 large publicly traded companies found that 69% of companies included stock options or stock appreciation rights in their LTI plans but the options made up only 29% of the overall LTI mix for their CEO.2 Sixty percent of CCLN companies include options in their CEO’s LTI package, comprising 25% of the overall LTI mix.3 Options composed only 5.9% of S&P500 CEO pay in 2011, down from 16.4% in 2010.4

1 Meridian Compensation Partners, Compensation Committee Leadership Network: Long-Term Incentive Compensation Mix at CCLN Companies (October 2012) (Appendix 2).

2 Meridian Compensation Partners, 2012 Corporate Governance & Incentive Plan Design Survey (Lake Forest, IL, 2012), 18. The survey is based on publicly available documents for a diverse group of 250 large public companies identified in the document. The median revenues and market capitalization for the group are $14.6 billion and $14.0 billion, respectively.

3 Meridian Compensation Partners, Compensation Committee Leadership Network: Long-Term Incentive Compensation Mix at CCLN Companies.

4 David Chun, “2012 Proxy Season Trends,” July 25, 2012. (Proprietary report for Equilar, on file with Tapestry Networks.)

Source: for Meridian Compensation Partners’ complete analysis, see Appendix 2 on page 13.

COMPENSATION COMMITTEE LEADERSHIP NETWORK

ViewPoints

Fall 2012: Compensation philosophy and practice 3

Some members lamented the loss of options. One member said, “Stock options are the ultimate shareowner-friendly risk-reward tool.” But criticism of options, particularly by ISS, meant that it was “just not worth it,” in the words of one member, to use them. A different member supported a move away from options: “Options are inefficient with the volatility in the market. If they’re underwater, they’re not making anyone happy, and they are expensive and dilutive. That’s the primary reason they are used less.”

Rising adoption of performance share plans. Performance shares were the most common LTI vehicle in 2012 at CCLN companies5 and a broader sample of public companies.6 Their growth has been rapid. Performance share plans were used by 73% of CCLN companies in 2011 and 84% in 2012.7 Although there are difficulties, particularly in selecting the right metrics for such plans, members generally agreed with one member’s sentiment: “Options may have been simpler, but performance-based shares work well.”

Some members cautioned against evaluating all performance plans the same way. “Certain stock awards are categorized as performance based but have performance requirements with a lower threshold. Such awards may take the place of restricted shares, enabling tax deductibility.”

Varied use of RSUs based on seniority. In an earlier meeting, CCLN members noted that lower-level executives typically appreciate restricted stock awards more than the CEO.8 That has not changed. “Most employees would prefer the certainty of an RSU,” one member said. But restricted stock is being used less frequently for CEOs at CCLN companies – it was used by 58% of companies in 2011 and 51% in 2012.9

Metrics for evaluating individual and company success

Members agree that the most challenging and important aspect of LTI design is choosing the metrics that reflect successful execution on the strategic plan and position the company for long-term, sustainable growth. “We have to identify what is right for this company right now. That’s not going to be right for other companies or even this company in 10 years,” one member said.

Members identified three major categories of metrics: financial, qualitative, and strategic.

Financial metrics. Historically, performance plan success has often been based on financial metrics. Meridian’s 2012 survey of 250 large public companies found that 58% of surveyed companies used earnings metrics such as earnings per share, operating income, net income, and others. Other financial metrics, such as total shareholder return and cash flow, are also frequently used.10 In addition, relative

5 Meridian Compensation Partners, Compensation Committee Leadership Network: Long-Term Incentive Compensation Mix at CCLN Companies.

6 Meridian Compensation Partners, 2012 Corporate Governance & Incentive Plan Design Survey. 7 Meridian Compensation Partners, Compensation Committee Leadership Network: Long-Term Incentive Compensation Mix at CCLN Companies.

8 Compensation Committee Leadership Network, “Executive Compensation in 2008: Never a Dull Moment,” May 22-23, 2008. 9 Meridian Compensation Partners, Compensation Committee Leadership Network: Long-Term Incentive Compensation Mix at CCLN Companies.

10 Meridian Compensation Partners, 2012 Corporate Governance & Incentive Plan Design Survey (Lake Forest, IL, 2012) 19.

COMPENSATION COMMITTEE LEADERSHIP NETWORK

ViewPoints

Fall 2012: Compensation philosophy and practice 4

financial metrics are popular; nearly half of companies use relative goals, most often relative total shareholder return (TSR).11

Members focused on the use of TSR. One member saw value in TSR, but suggested that it be used “as a qualifier. At certain points TSR would prevent you from earning more than target or from earning anything under an LTI plan. But it can’t be the only metric.”

Several members were concerned that TSR metrics had become too important. As one said, “TSR should not drive the process.” Another member said that TSR metrics “can make you too focused on the short term at the expense of prudent investments; that short-term focus isn’t in anyone’s interest.” One member suggested that moving away from TSR as a metric could lead to better returns for shareholders. “One competitor made all metrics purely internal – no TSR. The metrics were all based on sales volume and quality. And it was transformative, taking that company so far ahead of the rest of us. The end result is that they achieved that strategic mission and had exceptional TSR as a result.”

Qualitative metrics. Members are increasingly interested in other metrics, particularly qualitative metrics. “We have a mix of quantitative and qualitative goals. I don’t think everything needs to be financial … I have not given up the dream of qualitative measures,” one member said. In general, qualitative metrics are more likely to appear in annual performance plans than in long-term plans; 65% of companies use some type of qualitative measure in such plans.12 “We use softer metrics in our short-term plan – for example, employee safety. But we’re considering softer metrics in the long-term plan to help change the culture of the organization,” said one member.

Strategic metrics. Members are tying their plans more closely to their company’s competitive environment and strategic plan, with both quantitative and qualitative metrics. As one member said, “when the company changes, so too should the LTI. Moving from a stable dividend-producing company to a high-tech growth company requires a different LTI plan.”

One member noted, “We have set a plan that’s very specific to a [research and development challenge] at the company. If we had used financial measures, executives would have had no payouts for the last several years. We’re getting everyone focused on this single critical element of success. And it’s working. It’s been very exciting to see all of the smart people at our company trying to figure out this key challenge.”

11 Ibid., 20. 12 Meridian Compensation Partners, 2012 Trends and Developments in Executive Compensation, 11.

COMPENSATION COMMITTEE LEADERSHIP NETWORK

ViewPoints

Fall 2012: Compensation philosophy and practice 5

The importance of discretion in LTI awards

Designing the perfect LTI plan is virtually impossible, members said, because it would require the ability to predict the future. One member said, “We have a difficult enough time with setting the right three-year goals. And I’m not sure that there’s any world where three years can be considered ‘long term.’” It would be unfair to unduly penalize an executive of an agricultural company subject to an unprecedented drought; it would also be unfair to reward the executive of a company producing at-home electric generators whose sales skyrocketed because of a 100-year superstorm.

While discretion is viewed by some board critics with suspicion, CCLN members see the exercise of discretion as essential to effectively awarding long-term incentives and critical to board oversight of compensation. Members suggested ways that the committee can preserve some discretion while satisfying relevant stakeholder concerns.

Build a history of moving awards up and down as warranted. Careful tracking of past awards across business cycles can satisfy observers that discretion is carefully applied. Another member said, “We were able to demonstrate to [proxy advisors] that we were just as likely to adjust executive pay down as we were likely to push it up. Once you’ve demonstrated a willingness to do both, you earn your future exercises of discretion.”

Consider including realizable pay as part of the communication effort. One member pointed out that “if the move to realizable pay is adopted in a more widespread fashion, some of the concerns of ISS and others may diminish. It gets closest to communicating the reality of what a compensation plan really does and what the CEO actually gets.”

Earn the trust of executives by demonstrating the time and care that go into compensation decisions. “Accepting discretion requires trust,” one member said. “You’ll only have success with discretion if you have trust in those making the decisions.” Companies historically devote substantial time by their most senior leaders to determine and communicate pay; a practice that members believe is important to establish at all levels. According to one member, one CEO “would set these really daunting reach-goals for all his direct reports. But because there was trust that the efforts would be evaluated

Disclosure issues with strategic metrics

Some members expressed concern that Securities and Exchange Commission disclosure requirements made it

difficult to tie metrics too closely to corporate strategy. As one member said, “Disclosing goals for NEOs to

competitors is not a smart thing, so we obfuscate and use funky measures, something that we’re willing to

disclose, and that’s not ideal. [Disclosure requirements] have made compensation more of a blunt instrument.”

While some companies explicitly proclaim their long-term strategy through their compensation disclosures,

members said that a company need not publicize its plans if it wants to tie compensation to milestones on that

strategic plan. According to one, “You can communicate [interim milestones] with a narrative, prospective

description. You’re telling that story to investors already anyway.” As another member said, “Our goal is trying

to do the right thing, incentive the right behaviors. We can’t let disclosure rules lead us to do something that

isn’t right.”

COMPENSATION COMMITTEE LEADERSHIP NETWORK

ViewPoints

Fall 2012: Compensation philosophy and practice 6

against the difficulty of the task, the executives thought the process was ultimately fair – and it got the absolute best out of employees.” The same principle can apply to the use of discretion with the CEO by demonstrating how the compensation committee and board deliberately and equitably evaluate the CEO’s performance.

Reviewing how things have been done – and asking, “What if…?”

Members stressed the importance of regularly evaluating how the LTI plan has performed, looking back at historical payouts, and testing LTI plan changes on prior performance. One member said, “It’s important to calibrate how your company views ‘target.’ Many executives view being paid at target as a failure, and in some cases those companies will calibrate targets accordingly. In other words, 130% of target does not mean the same thing at two companies.” Another member said that a regular look back at the prior 10 years helped the board have better conversations with executives and outsiders: “We saw that over a 10-year period, we averaged 103% of target. That’s helpful to us when we have years that are significantly off of that target figure, in either direction.”

Another member suggested looking forward by challenging past performance: “What [would] we learn if we asked, ‘What if we could start from scratch?’ I think that if we were creating programs from scratch, thinking as owners, we’d do it differently. I’m an advocate of getting the compensation committee to have a boot camp where it thinks about how it might start from scratch. We think about the philosophy, evaluate every element against the philosophy and past practice, and evaluate how we think it will help us achieve in the future.”

Share ownership guidelines

Most companies maintain guidelines concerning the amount of company stock executives – and frequently directors – must hold, how long it must be held, and the process by which company stock may be sold. More than 90% of companies recently surveyed by Meridian maintained executive stock ownership guidelines;13 as of 2010, 95 of the Fortune 100 maintained such guidelines.14

“Setting the target as a multiple of salary is the most common approach, but a few companies still set the target as a particular number of shares or dollar value of holdings,” John Anderson said. “We have also seen guidelines trending upward. The average stock ownership requirement used to be three to five times a CEO’s annual salary. The overall average is now around five to six times salary, and more companies are setting a six-times-salary requirement for the CEO.”

Although members said that reviewing and updating share ownership guidelines was an important task, at most CCLN member companies, share ownership policies are functioning well. “For us, it does not really matter if it’s five or six times salary; our CEO holds so much more stock than that,” one member said. Most CCLN members saw share ownership guidelines ultimately as a means to a different end. As one member

13 Ibid., 2. 14 Shearman & Sterling, 2010 Corporate Governance of the Largest US Public Companies: Director & Executive Compensation (New York:

Shearman & Sterling, 2011), 30.

COMPENSATION COMMITTEE LEADERSHIP NETWORK

ViewPoints

Fall 2012: Compensation philosophy and practice 7

said, “The question is not whether our share ownership holding requirement should be 5 times salary or 5.2 times salary; this is a question about culture.”

Cultivating a culture of ownership

CCLN members want employees to think like owners. Directors play a role in cultivating a company’s ownership culture, but the prime mover is the company’s CEO. “The most important thing for an ownership culture is the tone at the top,” one member said. Members identified three ways that the CEO can set that tone:

Leading by example. Culture starts at the top, members said, and the CEO’s commitment to the company and to stock ownership is essential. Several members said that the CEO’s own stock ownership was very important to instilling a culture of ownership. “I think it says something important culturally if the CEO never sells company stock,” one member said. However, while there is value to a CEO exceeding the ownership requirement – “I think it would be disconcerting to see a CEO holding only exactly the minimum number of shares” – some members worried that a “never sell” mentality was not in anyone’s best interest. One member said, “I am in favor of a small but regular sale of stock awards. I think that’s generally good financial advice for anyone. I’m a big proponent of [Securities and Exchange Commission Rule] 10b5-1 share sale plans to accomplish such sales in a routine way.” Another member suggested, “Differentiating between what executives do with options versus restricted shares can help. With options, they should be able to do what they want.”

Speaking with executives before any stock sale. One member said, “I think that it’s a good idea for the CEO to have a conversation with each executive before a sale of stock. That’s a great opportunity to discuss the reason for the sale and the reasons to believe in the company.” Several members noted that their companies’ CEOs follow the same principle, discussing proposed stock sales with the compensation committee (or, at minimum, the chair).

Listen for – and report – any leading indicators of culture problems. Members noted that corporate culture can change more quickly that one might suspect. Attentiveness to a culture of ownership is important. In addition to learning about culture from discussions with executives who plan to sell company stock, the CEO should look for other indicators that ownership culture could be stronger. “You can hear interesting things,” one member said. “We found out that some executives may have been thinking about avoiding promotions to avoid the stock ownership requirements. That’s a problem.”

COMPENSATION COMMITTEE LEADERSHIP NETWORK

ViewPoints

Fall 2012: Compensation philosophy and practice 8

Compensation peer groups: challenges and opportunities

Members devote substantial board, human resources, and compensation consultant time to refining the methodologies by which they select peer groups and to explaining those judgments. In general, members find these tasks very important and nuanced.

CCLN members have considered peer groups at prior meetings.15 Then and now, members have challenged themselves and their boards to find even better ways to align pay and performance, thus increasing shareholder confidence in board oversight of executive compensation. Members are eager to consider new approaches to and alternative perspectives on perennial challenges like the construction and use of peer groups for executive compensation. For this reason, members were joined at the November meeting by David Chun, the CEO compensation research firm Equilar, and Charles Elson, the Edgar S. Woolard, Jr., chair of the John L. Weinberg Center for Corporate Governance at the University of Delaware and one author of a widely reviewed academic study, “Executive Superstars, Peer Groups, and Overcompensation: Cause, Effect, and Solution.”16

15 For example, Compensation Committee Leadership Network, “Fall 2011: going back to basics,” ViewPoints, October 27, 2011. 16 Charles M. Elson and Craig K. Ferrere, “Executive Superstars, Peer Groups and Overcompensation: Cause, Effect and Solution,” Journal of

Corporation Law, forthcoming.

Share ownership policy challenges and solutions

Stock price volatility. An executive could be at five times salary one day and four times salary the next if

company stock is volatile. Members offered several ways to avoid this complication, including creating a “safe

harbor” once the executive reaches the compliance point; evaluating the holding against market price and

either current market price or grant date price, whichever is higher; or reducing volatility by calculating the

holding value based on the average of a particular number of days.

Smaller straight stock grants. It may take new executives longer to reach holding requirements as

company incentive plans make more stock awards contingent on performance. Members offered two

solutions: providing a catch-up grant early in the executive’s tenure, or providing a threshold credit on the

performance shares.

Unusual personal circumstances for executives. One member’s company “had a particularly high number

of young executives – people who needed to tap into their equity to pay for their children to go to college.”

One option was to increase the percentage of compensation paid in cash. Another member suggested that

this situation may be rectified by pledging shares, but several members disagreed, noting that pledging shares

was a “red flag” issue for investors and analysts. Said one: “Even though this situation might make sense, I’m

not sure we want to put anyone in the position of being the morality police for when it is and is not

permissible to pledge shares.”

COMPENSATION COMMITTEE LEADERSHIP NETWORK

ViewPoints

Fall 2012: Compensation philosophy and practice 9

The costs and benefits of peer groups

In “Executive Superstars, Peer Groups, and Overcompensation: Cause, Effect and Solution,” Charles Elson and co-author Craig Ferrere suggest that an essential premise of competitive benchmarking by peer groups – an efficient and informed market for executive talent – is flawed.17

In the paper, Elson and Ferrere argue that the growth of peer groups is accidental and not based on sound research. CEOs are not themselves as mobile as some believe. CEOs very infrequently leave the organization at which they are chief executive to lead a different organization. The theory of the “superstar CEO” – an individual with general management and leadership expertise who can lead any organization to greatness – is fundamentally flawed; Elson and Ferrere note that success is more frequently based on accumulated knowledge of a company’s culture, strengths, weakness, and other internal-factors, leading those CEOs chosen from within a corporation’s ranks to outperform those hired from outside.

At the meeting Mr. Elson noted, “Historically, pay for executives has been based too much on external factors, particularly the pay at other companies. Those designing pay should focus more on internal metrics than external metrics – you’ll get more appropriate pay based on performance.”

Mr. Elson added, “When we began this project, we were hoping to find a universally applicable internal metric to help set executive pay. We could not do this. And it’s fair to note that a weakness of the paper is the lack of a clear alternative.” Elson said that the research led him to suggest four changes:

1. Compensation discussion and analysis should not include peer group data.

2. Proxy advisors such as ISS should stop using peers as such a significant input to evaluate a company’s pay for performance.

3. Companies should continue to use peers for evaluating performance, but should use them only as one of several data points to define pay targets.

4. Pay itself should be set with careful attention to internal pay equity.

Some members noted areas of agreement with Elson and Ferrere’s work. Members agreed that peer groups should not be used mechanistically; the judgment of the board and its compensation committee is essential. Some members shared Elson and Ferrere’s concern that the use of peer groups had led to “pay ratcheting” – growth of executive pay not supported by corporate performance.

Members thought that talent was more transferable than Mr. Elson’s research suggested. “I appreciated hearing his explanation, but I found his argument fundamentally flawed… Certain leadership and management skills really are transferable,” one member said. “And when coupled with other useful knowledge – of the industry, the marketplace, global growth opportunities – outside candidates can be very attractive.”

During the discussion, Mr. Elson said that the data showed public company CEOs infrequently leave to lead another company. “Apart from a group of turnaround specialists, sitting public company CEOs rarely leave

17 ViewPoints does not comprehensively summarize Elson and Ferrere’s 50 page research study. For more information on Elson and Ferrere’s

research, readers are encouraged to review the study in full.

COMPENSATION COMMITTEE LEADERSHIP NETWORK

ViewPoints

Fall 2012: Compensation philosophy and practice 10

to become the CEO of another public company,” Mr. Elson said. 18 Members’ experiences differed; they believed CEOs do move and – perhaps more importantly – have considerable opportunity to move, if they are not unsatisfied with their current role. One member said, “I left one company when I was CEO and went to another. I know talent is transferable, because I did it.”

Members pointed out that there is no clear, objective, outcomes-oriented pay philosophy based solely on internal pay equity: “It’s another data point which can help to enrich the discussion. But as the only way [to set pay], it’s seriously flawed.” Mr. Elson agreed, but said that more emphasis could – and should – be placed on internal pay equity.

While it is incredibly challenging to create peer groups, members said that they were nonetheless useful for evaluating pay packages. In the words of one, “Peer groups help make sure you’re playing in the right sandbox instead of out on an open beach.” Another member said, “Peer groups give you a sanity check – are your salaries in the right ballpark?” And as one member said, “Management is going to refer to peer groups. I am not in favor of eliminating my use of any source of relevant data. It’s my job to weigh it appropriately.”

Creating better peer groups

Creating the right peer group for a given company and task requires substantial care and attention from the compensation committee, compensation consultant, and others. Each peer group is bespoke, with compensation committee members applying judgment about the reasons for including or excluding any

given company.

Members have previously acknowledged that it would be unreasonable for each of a company’s shareholders to devote the same time and attention to peer group construction. As a result, different systems for evaluating peer groups have emerged. In a prior meeting, members discussed peer group challenges with ISS president Gary Retelny.19 Members have been interested in finding better, scalable methods for investors and proxy advisors to evaluate peer groups.

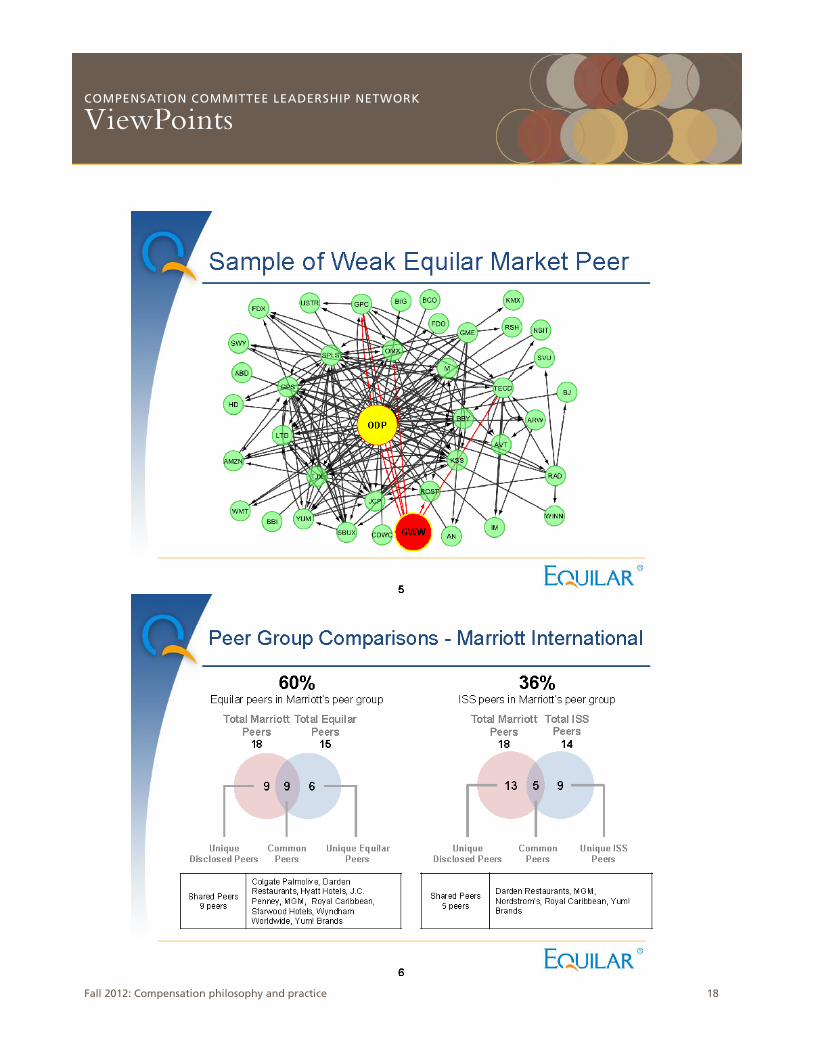

In November, members evaluated one such method – Equilar’s market-based peers. Mr. Chun explained the concept: “We’ve all seen the rapid growth and incredible power of social networking. Equilar decided to take that concept and apply it to executive compensation. Our hypothesis was that evaluating a company’s peers in a social way would be analytical and scalable, but fundamentally based on the reasoned discretion of directors.” 18 For more, see ibid. at 30-31. 19 Compensation Committee Leadership Network, “A Dialogue with Gary Retelny,” ViewPoints, August 10, 2012.

Source: for Equilar’s complete overview, see Appendix 3 on page 16.

COMPENSATION COMMITTEE LEADERSHIP NETWORK

ViewPoints

Fall 2012: Compensation philosophy and practice 11

Mr. Chun continued, “What we do is construct the full peer network – identifying which companies you list as peers; who those companies identify as peers; which other companies identify you as peers; and so on. And we weight the strength of relationships. Two companies that identify each other as peers – that’s a strong relationship. A peer of that company that you don’t list as a peer – that’s not quite as strong. By weighting these relationships, we identify the 15 strongest peers.”

Mr. Chun said, “We think it’s strong, scalable, and better than the alternatives.” Mr. Chun cited Yum! Brands as a good example of the contrast between Equilar’s methodology and that of ISS.

Members thought that the Equilar model was very intriguing. “At base, it’s an analysis of the meta-data of what all of our boards are doing,” one member said. Another wondered if “this approach might help mitigate

gaming. If a company includes very aspirational peers, it prompts the question, ‘Did they include you too?’” A third said, “It’s not perfect, but bravo. This is a great way to scan the pay universe.” Members were pleased to hear that Glass Lewis began using Equilar’s market-based peers algorithm in their proxy research in July 2012.20 Despite the perceived strengths, one member noted that, “At the end of the day peer groups are still a judgment call. We wouldn’t use anything that’s purely formulaic.”

Conclusion

CCLN members are frequently asked to evaluate challenging issues associated with executive compensation practices. Although time is limited and their ultimate focus is rightly on performance, pausing to consider the underlying philosophies of alternative approaches challenges committee chairs to think differently about perennial challenges. This careful and deliberate attention to complex, nuanced issues is the reason for affording compensation committees discretion with structuring and using LTI and share ownership plans and peer groups – and why such discretion will hopefully lead to stronger alignment of executive and shareholder interest and better functioning capital markets.

About this document The views expressed in this document represent those of the Compensation Committee Leadership Network. They do not reflect the views nor constitute the advice of network members, their companies, or Tapestry Networks. Please consult your counselors for specific advice.

This material is prepared by Tapestry Networks. It may be reproduced and redistributed in its entirety including all trademarks and legends.

20 Glass, Lewis & Co., “Pay for Performance,” accessed November 29, 2012, http://www.glasslewis.com/issuer/pay-for-performance/.

Source: for Equilar’s complete overview, see Appendix 3 on page 16.

COMPENSATION COMMITTEE LEADERSHIP NETWORK

ViewPoints

Fall 2012: Compensation philosophy and practice 12

Appendix 1: Contributing members 21

The following members participated in the discussion:

John L. Anderson, Meridian Compensation Partners

Jill M. Considine, Interpublic Group of Companies

Karen N. Horn, Eli Lilly and Company

Annette Leckie, Meridian Compensation Partners

Linda Fayne Levinson, NCR and The Western Union Company

Samuel C. Scott III, Bank of New York Mellon Corporation

Laurie Siegel, CenturyLink

Richard J. Slater, KBR

Kelvin R. Westbrook, Archer Daniels Midland Company

The following members took part in pre-meeting or post-meeting discussions:

Thomas A. Dattilo, Harris Corporation

Lloyd H. Dean, Wells Fargo

Thomas J. Donohue, Union Pacific Railroad Corporation

Victoria F. Haynes, Nucor Corporation

David R. Goode, Caterpillar and Delta Air Lines

Marshall O. Larsen, Lowe’s Companies

Richard C. Notebaert, Aon

Marjorie M. Magner, Accenture

Steven S. Reinemund, Marriott International

Daniel H. Schulman, Flextronics International

Anne Stevens, Lockheed Martin Corporation

21 The compensation committee leaders are identified by the compensation committee membership. John L. Anderson and Annette Leckie

participated in their capacity as compensation experts.

COMPENSATION COMMITTEE LEADERSHIP NETWORK

ViewPoints

Fall 2012: Compensation philosophy and practice 13

Appendix 2: CCLN analysis, Meridian Compensation Partners 22

22 Meridian Compensation Partners, Compensation Committee Leadership Network: Long-Term Incentive Compensation Mix at CCLN

Companies (October 2012).

COMPENSATION COMMITTEE LEADERSHIP NETWORK

ViewPoints

Fall 2012: Compensation philosophy and practice 14

COMPENSATION COMMITTEE LEADERSHIP NETWORK

ViewPoints

Fall 2012: Compensation philosophy and practice 15

COMPENSATION COMMITTEE LEADERSHIP NETWORK

ViewPoints

Fall 2012: Compensation philosophy and practice 16

Appendix 3: Overview of Market Peers, Equilar 23

23 Equilar, Inc., Overview of Equilar Market Peers: Compensation Committee Leadership Network (November 2012).

COMPENSATION COMMITTEE LEADERSHIP NETWORK

ViewPoints

Fall 2012: Compensation philosophy and practice 17

COMPENSATION COMMITTEE LEADERSHIP NETWORK

ViewPoints

Fall 2012: Compensation philosophy and practice 18

COMPENSATION COMMITTEE LEADERSHIP NETWORK

ViewPoints

Fall 2012: Compensation philosophy and practice 19

COMPENSATION COMMITTEE LEADERSHIP NETWORK

ViewPoints

Fall 2012: Compensation philosophy and practice 20