Fair Lending Risk Management - UBA Conference/Marty_Mitchell... · Fair Lending Risk Management...

38

Fair Lending Risk Management Presented by: Martin (Marty) Mitchell, CRCM Managing Director, ProBank Austin Robert J. (Bob) Mullenbach, CRCM Managing Director, Compliance Division Deputy, ProBank Austin

Transcript of Fair Lending Risk Management - UBA Conference/Marty_Mitchell... · Fair Lending Risk Management...

Fair Lending Risk Management

Presented by:

Martin (Marty) Mitchell, CRCM

Managing Director, ProBank Austin

Robert J. (Bob) Mullenbach, CRCM

Managing Director, Compliance Division Deputy, ProBank Austin

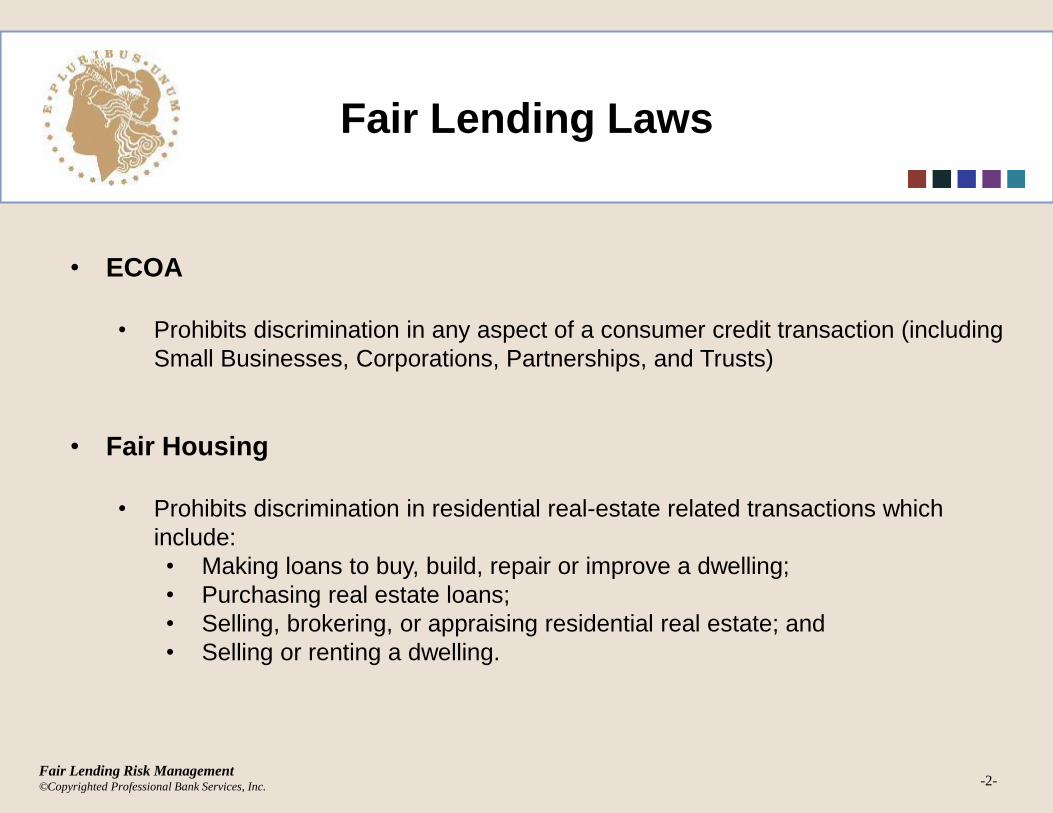

Fair Lending Laws

• ECOA

• Prohibits discrimination in any aspect of a consumer credit transaction (including

Small Businesses, Corporations, Partnerships, and Trusts)

• Fair Housing

• Prohibits discrimination in residential real-estate related transactions which

include:

• Making loans to buy, build, repair or improve a dwelling;

• Purchasing real estate loans;

• Selling, brokering, or appraising residential real estate; and

• Selling or renting a dwelling.

-2-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

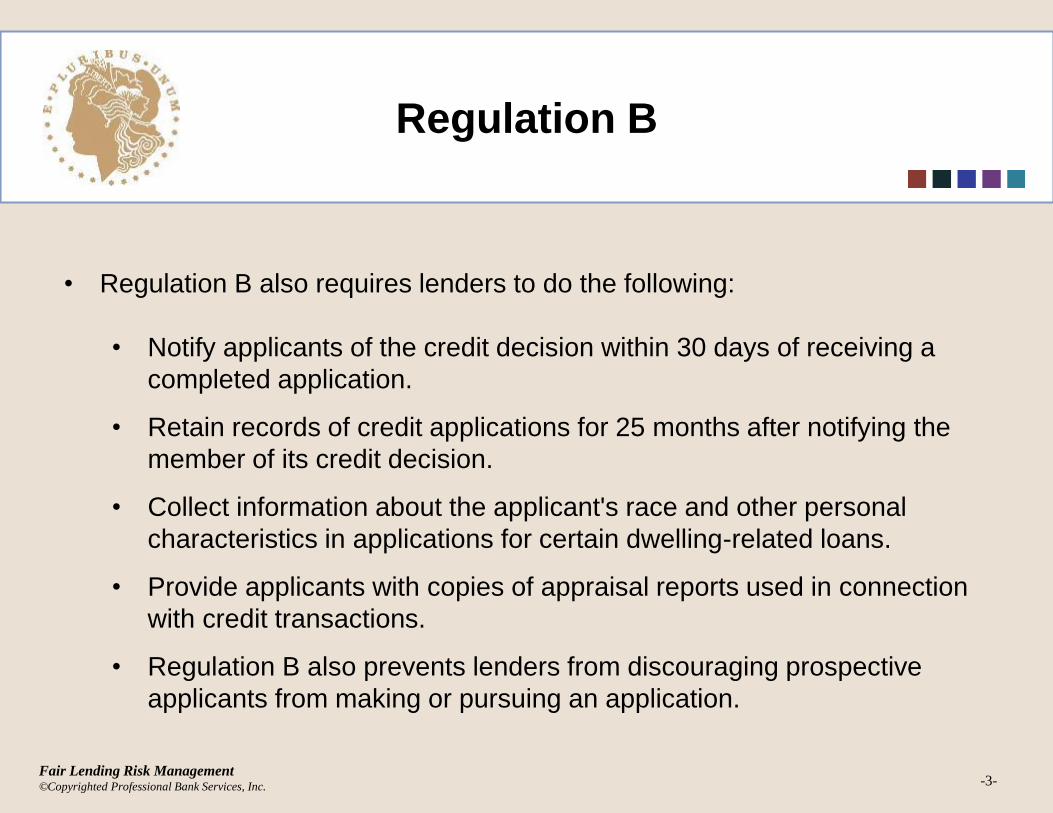

Regulation B

• Regulation B also requires lenders to do the following:

• Notify applicants of the credit decision within 30 days of receiving a

completed application.

• Retain records of credit applications for 25 months after notifying the

member of its credit decision.

• Collect information about the applicant's race and other personal

characteristics in applications for certain dwelling-related loans.

• Provide applicants with copies of appraisal reports used in connection

with credit transactions.

• Regulation B also prevents lenders from discouraging prospective

applicants from making or pursuing an application.

-3-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

Applicability

• ECOA and Fair Housing cover all phases of the lending process:

• Applications;

• Loan closings; and

• Post loan closing – including servicing and loss mitigation

activities.

• ECOA and Fair Housing apply to financial institutions and any

third parties engaged by financial institutions.

-4-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

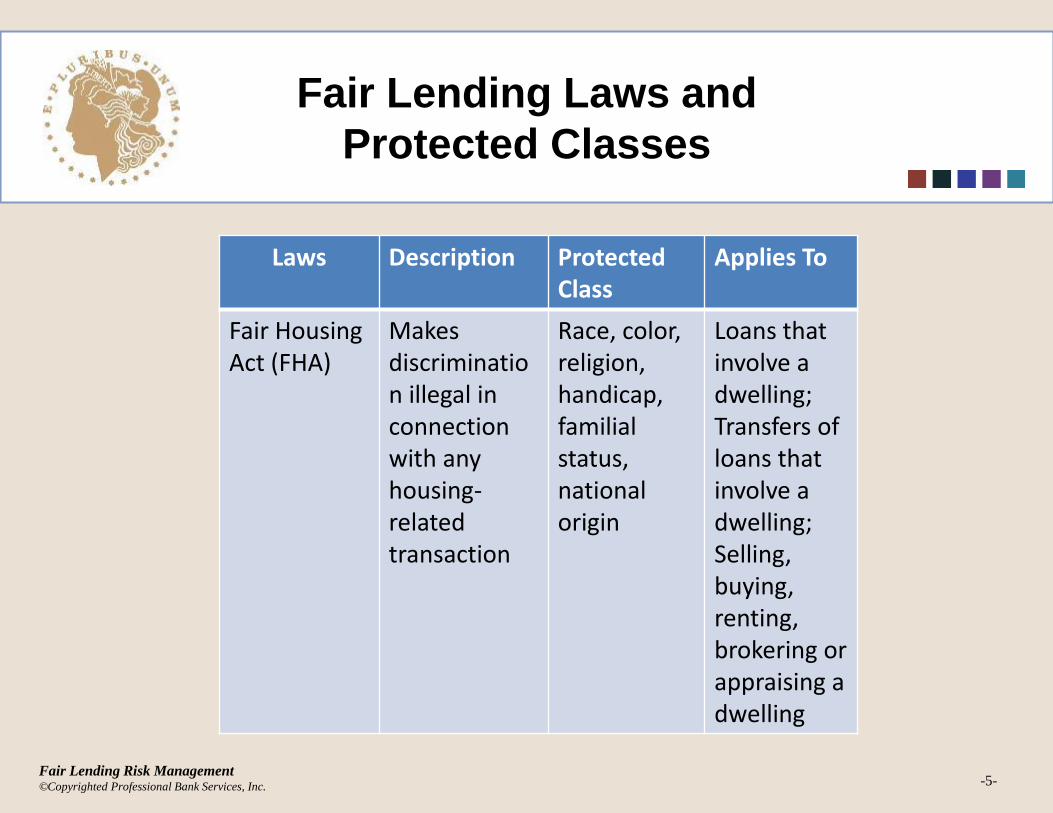

Fair Lending Laws and

Protected Classes

-5-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

Laws Description Protected Class

Applies To

Fair Housing Act (FHA)

Makes discrimination illegal in connection with any housing-related transaction

Race, color, religion,handicap,familialstatus, national origin

Loans that involve a dwelling;Transfers of loans that involve a dwelling;Selling, buying, renting, brokering or appraising a dwelling

Fair Lending Laws and

Protected Classes

-6-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

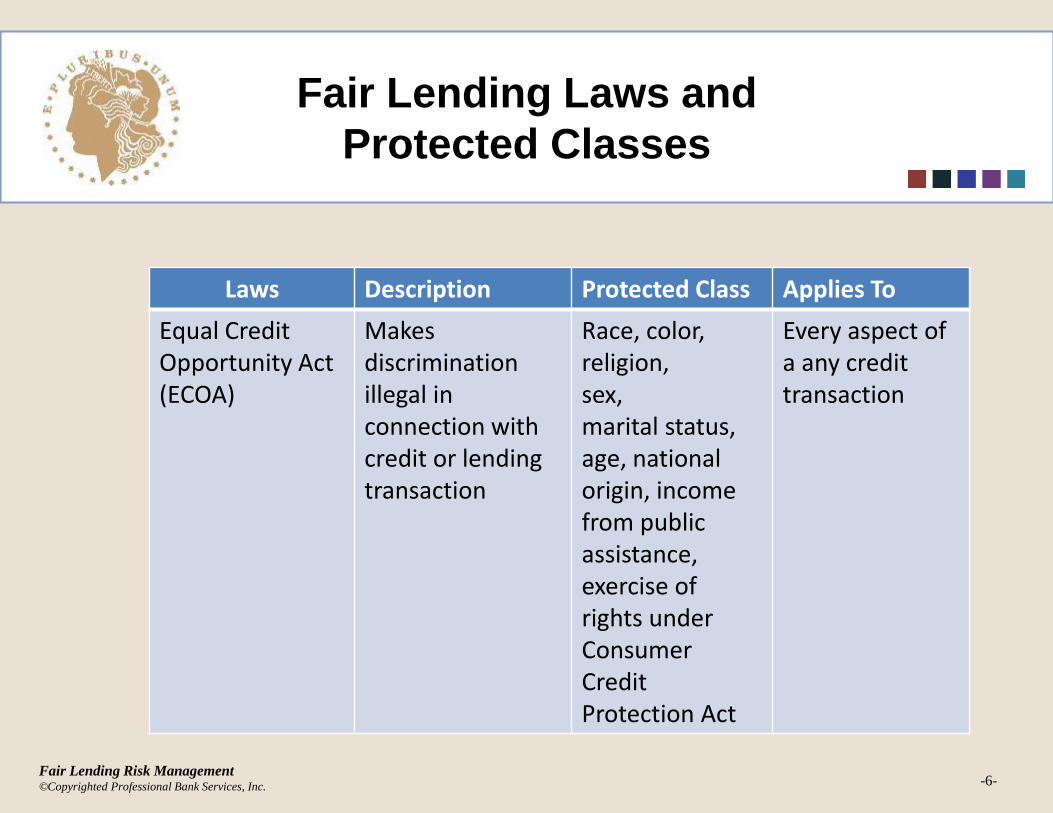

Laws Description Protected Class Applies To

Equal Credit Opportunity Act(ECOA)

Makes discrimination illegal in connection with credit or lending transaction

Race, color, religion,sex,marital status, age, national origin, income from public assistance, exercise of rights under Consumer Credit Protection Act

Every aspect of a any credit transaction

Fair Lending Laws and

Protected Classes

-7-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

Laws Description Data Points Applies To

Home Mortgage Disclosure Act(HMDA)

Requiresreporting of residential lending data

Race, ethnicity,sex, income, action taken, HOEPA, lien status, rate spread, property location

Homepurchase, home improve-ment,refinancing

Prohibited Bases

-8-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

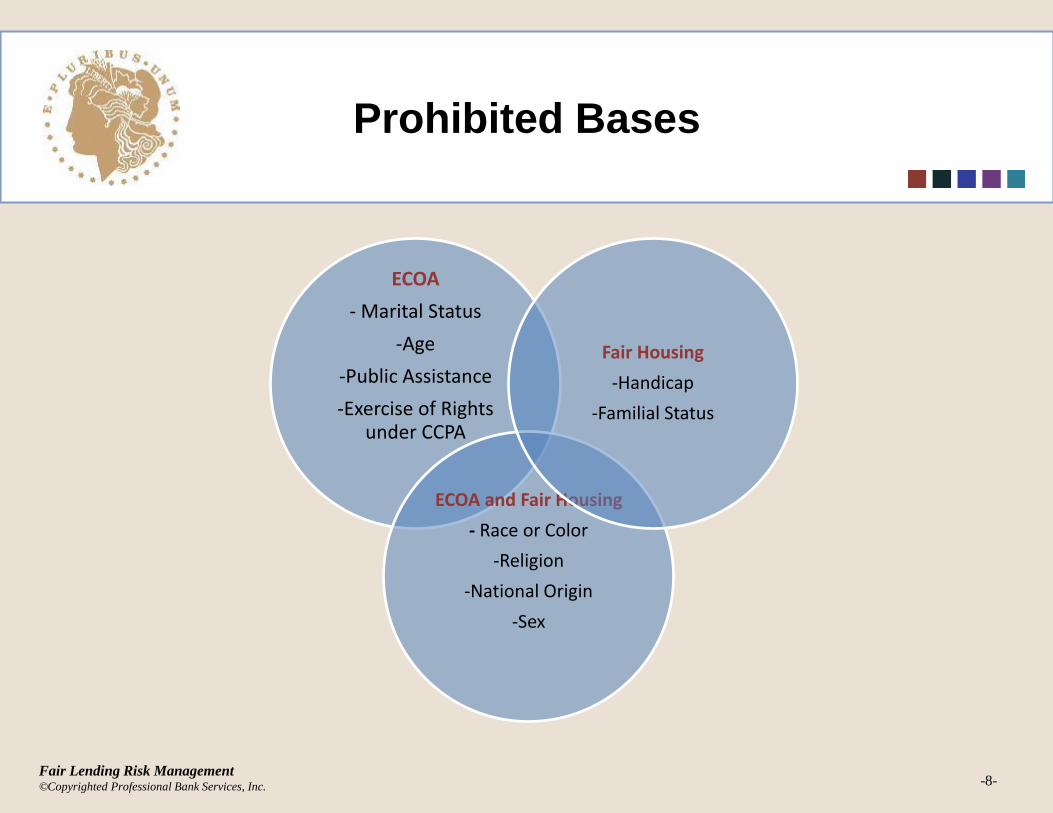

ECOA

- Marital Status

-Age

-Public Assistance

-Exercise of Rights under CCPA

ECOA and Fair Housing

- Race or Color

-Religion

-National Origin

-Sex

Fair Housing

-Handicap

-Familial Status

Prohibited Acts

-9-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

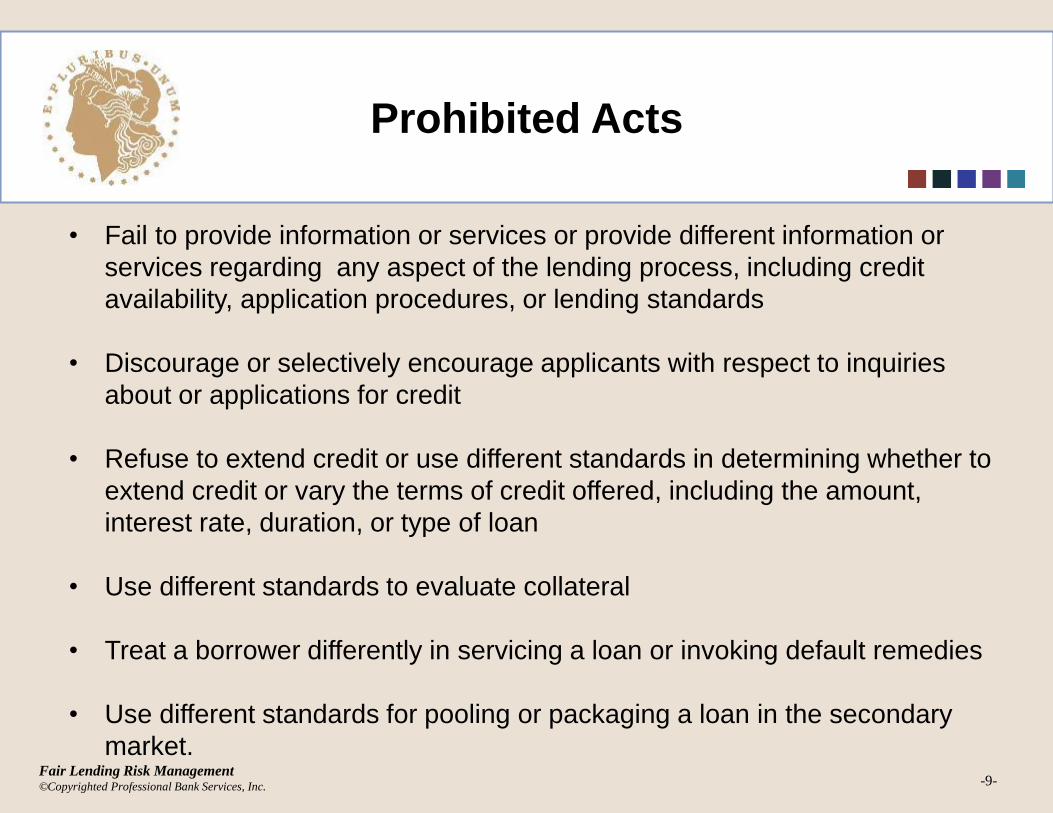

• Fail to provide information or services or provide different information or

services regarding any aspect of the lending process, including credit

availability, application procedures, or lending standards

• Discourage or selectively encourage applicants with respect to inquiries

about or applications for credit

• Refuse to extend credit or use different standards in determining whether to

extend credit or vary the terms of credit offered, including the amount,

interest rate, duration, or type of loan

• Use different standards to evaluate collateral

• Treat a borrower differently in servicing a loan or invoking default remedies

• Use different standards for pooling or packaging a loan in the secondary

market.

Prohibited Acts

-10-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

A lender may not express, orally or in writing, a preference based on prohibited factors

or indicate that it will treat applicants differently on a prohibited basis. A violation may

still exist even if a lender treated applicants equally.

A lender may not discriminate on a prohibited basis because of the characteristics of:

• An applicant, prospective applicant, or borrower

• A person associated with an applicant, prospective applicant, or borrower (for

example, a co-applicant, spouse, business partner, or live-in aide)

• The present or prospective occupants of either the property to be financed or

the characteristics of the neighborhood or other area where property to be

financed is located.

Persons With Disabilities

-11-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

The Fair Housing Act requires lenders to make reasonable accommodations for a

person with disabilities when such accommodations are necessary to afford the

person an equal opportunity to apply for credit.

Applications

-12-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

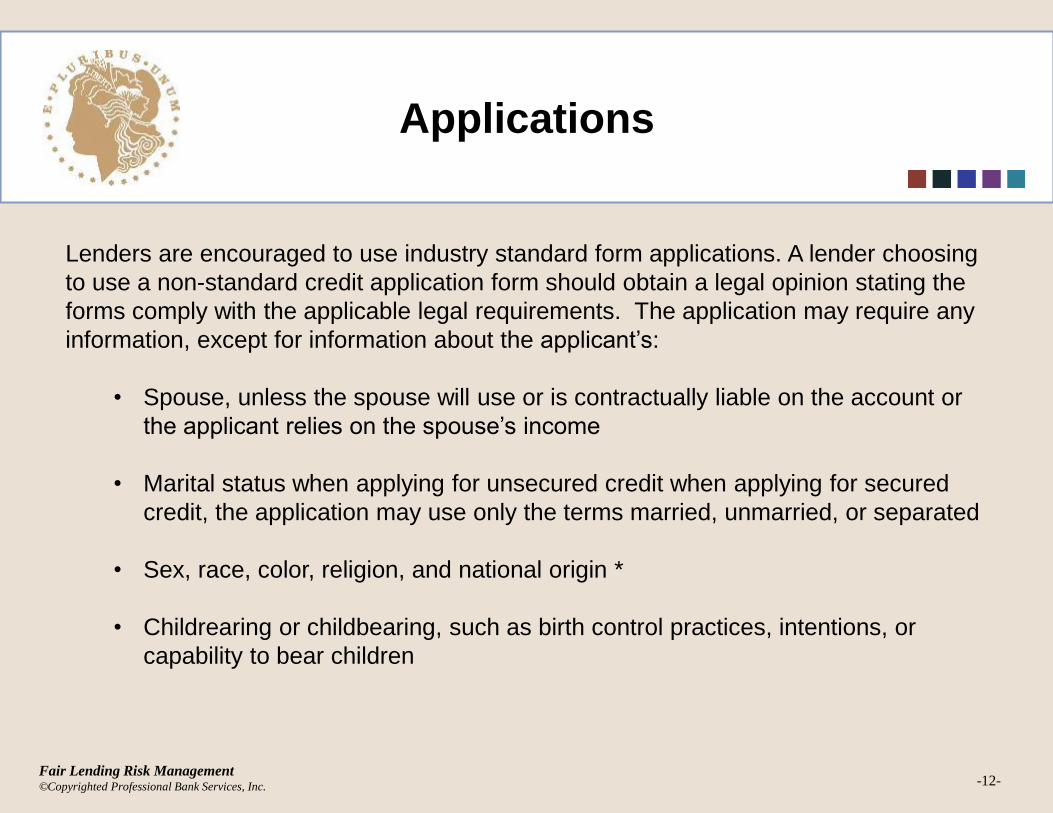

Lenders are encouraged to use industry standard form applications. A lender choosing

to use a non-standard credit application form should obtain a legal opinion stating the

forms comply with the applicable legal requirements. The application may require any

information, except for information about the applicant’s:

• Spouse, unless the spouse will use or is contractually liable on the account or

the applicant relies on the spouse’s income

• Marital status when applying for unsecured credit when applying for secured

credit, the application may use only the terms married, unmarried, or separated

• Sex, race, color, religion, and national origin *

• Childrearing or childbearing, such as birth control practices, intentions, or

capability to bear children

Examples of Overt Discrimination

-13-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

• Including explicit prohibited basis identifiers in the institution’s written or oral policies

and procedures (underwriting criteria, pricing standards, etc.)

• Collecting information, conducting inquiries or imposing conditions contrary to

express requirements of Regulation B.

• Including variables in a credit scoring system that constitute a basis or factor

prohibited by Regulation B or, for residential loan scoring systems, the FHA.

• Statements made by the institution’s officers, employees or agents which

constitute an express or implicit indication that one or more such persons have

engaged or do engage in discrimination on a prohibited basis in any aspect of a

credit transaction.

• Employee or institutional statements that evidence attitudes based on

prohibited basis prejudices or stereotypes.

Three Types of Illegal Discrimination

Disparate Treatment

-14-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

• Occurs when a lender has neutral credit policies and criteria, but applies

them inconsistently, in a way that adversely impacts borrowers on a

prohibited basis.

• A bank requires automobile loan customers to have monthly debt

payments of less than 40 percent of gross monthly income. If the bank

denies a female applicant based on that rule, but makes a policy

exception and approves a male applicant in similar circumstances, this

may be disparate treatment.

• Lenders often have a legitimate, business-related reason to "bend the

rules" for a particular applicant. If this is the case, it is possible that no

violation of fair lending law occurred.

Three Types of Illegal Discrimination

Disparate Impact

-15-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

• Occurs when a lender adopts a neutral policy, applies it consistently, but the

policy causes a "disproportionate adverse impact" on a prohibited basis.

• A bank adopts a minimum loan amount for home mortgage loans. This

minimum is so high that few minority, single or elderly applicants qualify

for loans in the bank's market area due to their incomes or the local

home values. This may constitute disparate impact.

• A policy or practice that creates a disparity on a prohibited basis is not

necessarily proof of a violation. The apparent disparate impact may be

legal if there is a business necessity for the policy or practice, and there

is no alternative policy or practice that is less discriminatory.

Prohibited Practices

-16-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

A lender may not discriminate on a prohibited basis by considering the

characteristics of:

• An applicant, prospective applicant, or borrower;

• A person associated with an applicant, prospective applicant, or

borrower;

• The present or prospective residents of the property to be financed; or

• The neighborhood where the property to be financed is located.

How Discrimination Occurs

in Underwriting

-17-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

• Examiners compare credit-underwriting decisions to find apparent disparate

treatment.

• A lender that approves a loan to a married applicant with a two-year-old

bankruptcy, but denies applications from unmarried applicants with

much older bankruptcies.

• Examiners focus their review on "marginal" applicants, who are neither

clearly qualified, nor clearly unqualified, for credit. Lenders usually need

to exercise judgment or provide extra assistance to qualify marginal

applicants for credit, and discrimination may be more likely in these

cases.

Indicators of Discrimination

in Underwriting

-18-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

• Substantial disparities among the approval/denial rates for applicants by

monitored prohibited basis characteristic (especially within income

categories)

• Substantial disparities among the application processing times for

applicants by monitored prohibited basis characteristic (especially within

denial reason groups)

• Substantially higher proportion of withdrawn/ incomplete applications from

prohibited basis group applicants than from other applicants

• Vague or unduly subjective underwriting criteria

• Lack of clear guidance on making exceptions to underwriting criteria,

including credit scoring overrides

Indicators of Discrimination

in Underwriting

-19-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

• Lack of clear loan file documentation regarding reasons for any exceptions

to standard underwriting criteria, including credit scoring overrides

• Relatively high percentages of either exceptions to underwriting criteria or

overrides of credit score cutoffs

• Loan officer or broker compensation based on loan volume (especially

loans approved per period of time)

• Consumer complaints alleging discrimination in loan processing

How Discrimination Occurs

Terms and Conditions

-20-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

• If a financial institution approves a loan but imposes higher interest rates or

excessive fees on a prohibited basis, the financial institution may have

violated the Equal Credit Opportunity Act (ECOA) or the Fair Housing Act

(FHA).

• The examiner will need to investigate whether a nondiscriminatory

reason, such as risk-based pricing, accounts for the difference.

• The Justice Department has settled several ECOA and FHA lawsuits

with lenders, often citing discriminatory credit pricing.

Indicators of

Pricing Discrimination

-21-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

• Financial incentives for loan officers or brokers to charge higher prices:

interest rate, fees, points.

• Financial incentives are accompanied by broad pricing discretion such as

through the use of overages or yield spread premiums.

• Presence of broad discretion in loan pricing (including interest rate, fees

and points), such as through overages, underages or yield spread

premiums. Such discretion may be present even when institutions

provide rate sheets and fees schedules, if loan officers or brokers are

permitted to deviate from those rates and fees without clear and objective

criteria.

Indicators of

Pricing Discrimination

-22-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

• Use of risk-based pricing that is not based on objective criteria or applied

consistently

• Substantial disparities among prices being quoted or charged to applicants

who differ as to their monitored prohibited basis characteristics

• Consumer complaints alleging discrimination in residential loan pricing.

• In mortgage pricing, disparities in the incidence or rate

• A loan program that contains only borrowers from a prohibited basis group,

or has significant differences in the percentages of prohibited basis groups.

Redlining General Concepts

-23-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

• The avoidance of segments of the bank’s market area in providing banking

products and services.

• A complete absence of activity is not the standard – disproportionately

lower levels will raise concerns during reviews.

• Within the Context of the Bank’s Defined Market Areas, examiners will look

for:

• Lending Patterns

• Branch Structure

• Advertising

• Reverse Redlining – high percentage of loans with less advantageous

features in high minority areas

Steering

-24-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

• Steering is the placement of a customer in a product.

NOTE: Steering can occur even if it doesn’t involve a less favorable product.

NOTE: May occur when the institution offers the same product in various lending

channels that price or underwrite the product differently, i.e., portfolio vs.

mortgage subsidiary products.

How Discrimination Occurs

Steering

-25-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

• "Steering" generally occurs when a lender refers applicants to a less favorable

credit product than they qualify for.

• May raise fair lending concerns if it puts prohibited-basis customers at a

disadvantage.

• Lenders steer minority customers to FHA home mortgage loans even

when they should qualify for lower-priced conventional credit.

• Examiners review the institution's policies and practices for referring

customers to various products. If individual lenders can refer customers to

different credit products, examiners evaluate whether the lenders use their

discretion in a nondiscriminatory manner.

ECOA Targeted Review

-26-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

• Generally focus on a specific product; e.g. mortgages or auto lending.

• Statistical analysis

• File review

Indirect Auto Lending

-27-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

• Other than a home, a car or truck is often one of the largest purchases a

consumer makes in his or her lifetime.

• Third largest market in terms of loans outstanding in the consumer financial

marketplace, behind only mortgages and student loans. In 2013, outstanding

auto loan balances were approximately $863 billion, with over $355 billion

originated during 2013.

• Auto lenders fall under the CFPB’s supervisory or enforcement jurisdiction.

This includes financial institutions, like banks, credit unions, captive auto

lenders, and certain nonbank companies.

HMDA Data Integrity Review

-28-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

• Essentially, HMDA compliance examination.

• Inaccurate HMDA data may lead to resubmission of HMDA data for one or

more years.

• May also lead to fair lending enforcement action.

Fair Lending Risk Assessment

-29-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

• Program – Procedures - Practices

Fair Lending Risk Assessment

-30-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

• Program:

• Clear written policies and procedures

• Management oversight

• Consistent with FFIEC Interagency Fair Lending

Examination Procedures

Board and Management

Oversight

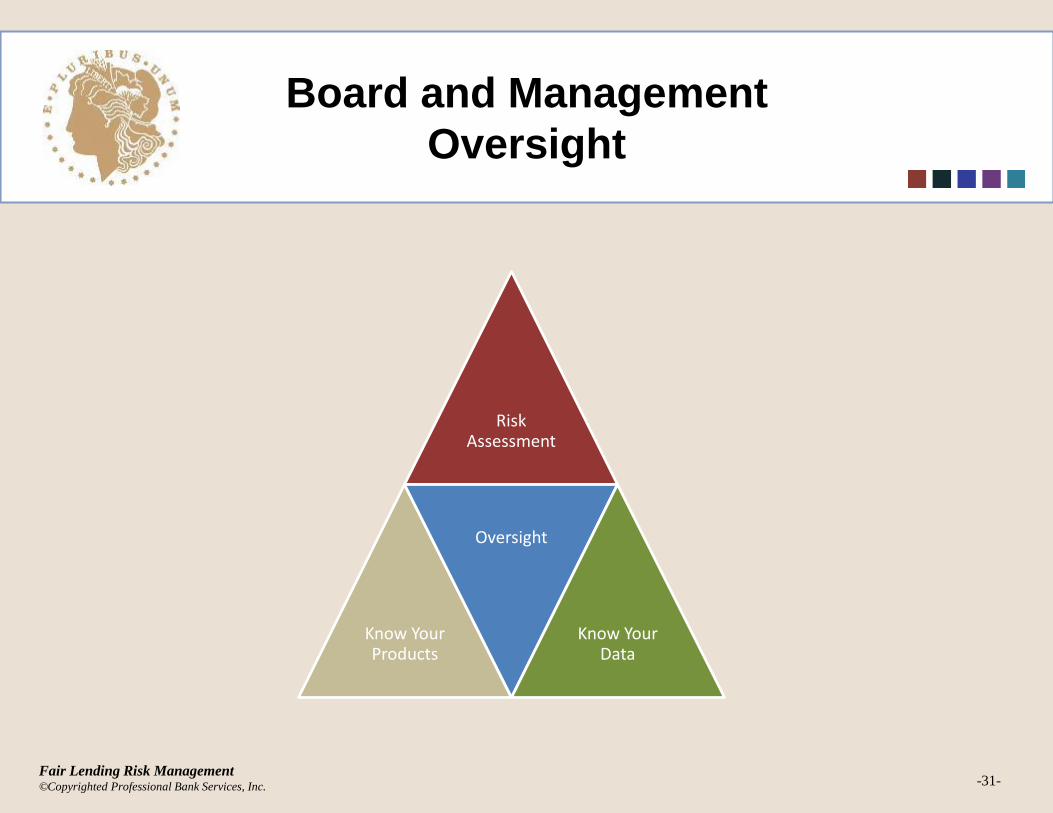

-31-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

Risk Assessment

Know Your Products

Oversight

Know Your Data

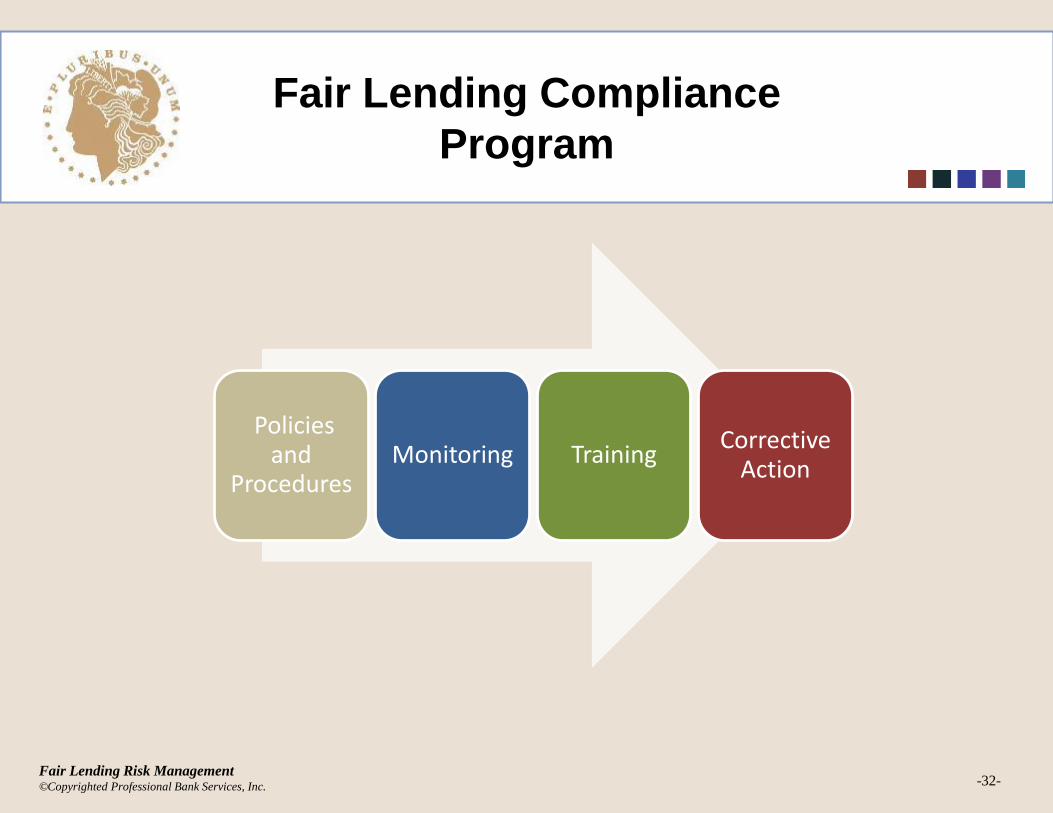

Fair Lending Compliance

Program

-32-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

Policies and

ProceduresMonitoring Training

Corrective Action

Monitoring

-33-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

• Compliance audits should include a process to:

- Report findings to appropriate leadership and managers,

- Respond to exceptions,

- Implements corrective action, and monitors the results of

corrective action.

• Self-evaluations and Self tests

- Recommended for most banks as a way to review the results of

lending activities to identify any risk indicators or areas of

concern.

Training

-34-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

• Best practices include a formal fair lending training program,

tailored to the institution that includes:

- Board of Directors

- New employees

- Third-party providers

- Programs specific to employee function

- Applications, closings, foreclosures and debt resolution

- Marketing, advertising and signage

Common Violations

-35-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

• Making loans with different pricing and terms to similarly situated

applicants with no apparent explanation

• Failing to establish/update/comply with board-approved

underwriting and pricing standards

• Lack of centralized underwriting/local decision-making authority

with inadequate oversight

• No secondary review process

• Overt or misstatements in lending policies

• Redlining

• Steering

Common Violations

-36-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

• HMDA violations that can lead to a targeted fair lending exam:

• Failure to collect government monitoring information (GMI)

• Requesting information about the applicant’s spouse when not

applying for joint credit

• Failure to include alimony, child support, public assistance, and

other separate maintenance when calculating applicant income

• Data errors

• ECOA/ Reg B - failure to provide adverse action notices in a timely

manner

Conclusion

-37-Fair Lending Risk Management©Copyrighted Professional Bank Services, Inc.

• Equal treatment of loan applicants is a serious issue for the

regulators and should be a serious issue for all lending institutions.

• Significant liability can be incurred through unintentional illegal

discrimination.

• Multicultural awareness, race, gender, and handicap sensitivity

training is not a joke and institutions that expect to survive and

thrive should takes proactive steps to make this part of their

corporate culture and identity.

• The “tone at the top” is crucial to success.

Martin (Marty) Mitchell, CRCM

Managing Director, ProBank Austin

6200 Dutchmans Lane, Suite 305

Louisville, Kentucky 40205

(800) 523-4778, Ext. 258

www.probank.com

Robert J. (Bob) Mullenbach, CRCM

Managing Director, Compliance Division

Deputy, ProBank Austin

6200 Dutchmans Lane, Suite 250

Louisville, Kentucky 40205

(800) 523-4778, Ext. 258

www.probank.com