Factor-Based Investing - Risk · characteristics – for instance ... Aon Hewitt Factor-Based...

8

Aon Hewitt Retirement and Investment Risk. Reinsurance. Human Resources. Factor-Based Investing

Transcript of Factor-Based Investing - Risk · characteristics – for instance ... Aon Hewitt Factor-Based...

Aon HewittRetirement and Investment

Risk. Reinsurance. Human Resources.

Factor-Based Investing

Aon Hewitt Factor-Based Investing 2

Summary

The right equity portfolio for an investor depends on their risk and return objectives, investment beliefs, cost constraints and governance resource.

Risk-adjusted returns are often considered when setting asset allocation, but can be overlooked

when constructing an equity portfolio, as some equity investors follow market capitalisation

strategies without considering any other approaches beforehand.

There are a number of widely available alternative “factor” based indices using different stock

weighting techniques (often known as “Smart Beta” strategies) which can be attractive in a

number of different scenarios for investors who:

• want to reduce sensitivity to equity market movements through low-volatility investments;

• are seeking different sources of returns but may have governance or cost constraints or

have an aversion to significant active risk;

• are looking to improve potential long-term risk-adjusted returns of an equity portfolio by

investing in a combination of factors.

Market cap doesn’t always fitMarket capitalisation based equity portfolios provide exposure

to each company in weights equal to the value of the shares

available to investors. For a number of reasons passive equity

investments constructed in this way remain popular. They are

easy for investors to understand and can provide liquid

exposure to global equity markets at a relatively low cost.

However, both active managers and supporters of factor

investing question why investors should hold more of an asset

just because it is large in size, or has performed well recently.

Capturing a factorThere are a number of different ways to construct equity indices

which do not follow a market capitalisation weighting method,

which have been designed to keep fairly constant exposure to a

specific factor using a rules-based approach. These include

approaches which weight stocks based on certain

characteristics – for instance company accounting ratios or

stocks which have exhibited low volatility.

In this paper we focus on two factors, “value” and “low

volatility” and it is the exposure to a particular factor which

drives performance from this type of investing. Selecting and

combining appropriate factors can also provide the benefits of

capturing the long-term risk premium for each factor, whilst

dampening volatility over shorter periods.

The right approach will depend on an investor’s circumstances

and we have helped a number of clients tailor their equity

allocations based on their objectives. The following scenarios

illustrate how factor investing can be used to achieve this.

Factor-Based Investing

Aon Hewitt Factor-Based Investing 3

Scenario 1: Risk reductionAn investor who requires the outperformance associated with

equities, but with an objective to reduce equity portfolio

volatility, could consider one of the low volatility approaches.

The relative liquidity and low cost of a low volatility equity

portfolio compared to some alternative asset classes can be

attractive. This can be particularly important for pension

schemes which have implemented a structured de-risking

plan involving a gradual reduction in exposure to higher

returning asset classes.

The “Minimum Variance” method is a common approach to

low volatility investing. Minimum Variance portfolios allocate to

companies which are not necessarily low volatility stocks in

isolation but, when combined in a portfolio, achieve an

aggregate reduction in volatility.

This is illustrated below, by comparing the volatility of the MSCI

World Minimum Volatility index (a minimum variance approach)

to the MSCI World index (a market capitalisation index) over 15

calendar years.

1 As at 31 December 2015

Ann

ual V

olat

ility

(%

)

20

15

10

5

02001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Board

Calendar year volatility

MSCI Index: MSCI World Minimum Volatility-ND MSCI Index: MSCI World-ND

The graph below also demonstrates how a minimum variance

approach has the potential to protect during equity market

downturns over the same period.

The fall in value (“drawdown”) associated with the minimum

variance approach is lower than a comparable market

capitalisation index.

-45.0%

-40.0%

-35.0%

-30.0%

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

Jan

01

Jan

02

Jan

03

Jan

04

Jan

05

Jan

06

Jan

07

Jan

08

Jan

09

Jan

10

Jan

11

Jan

12

Jan

13

Jan

14

Jan

15

Jan

16

Cumulative drawdown

MSCI World Min Volatility MSCI World

Aon Hewitt Factor-Based Investing 4

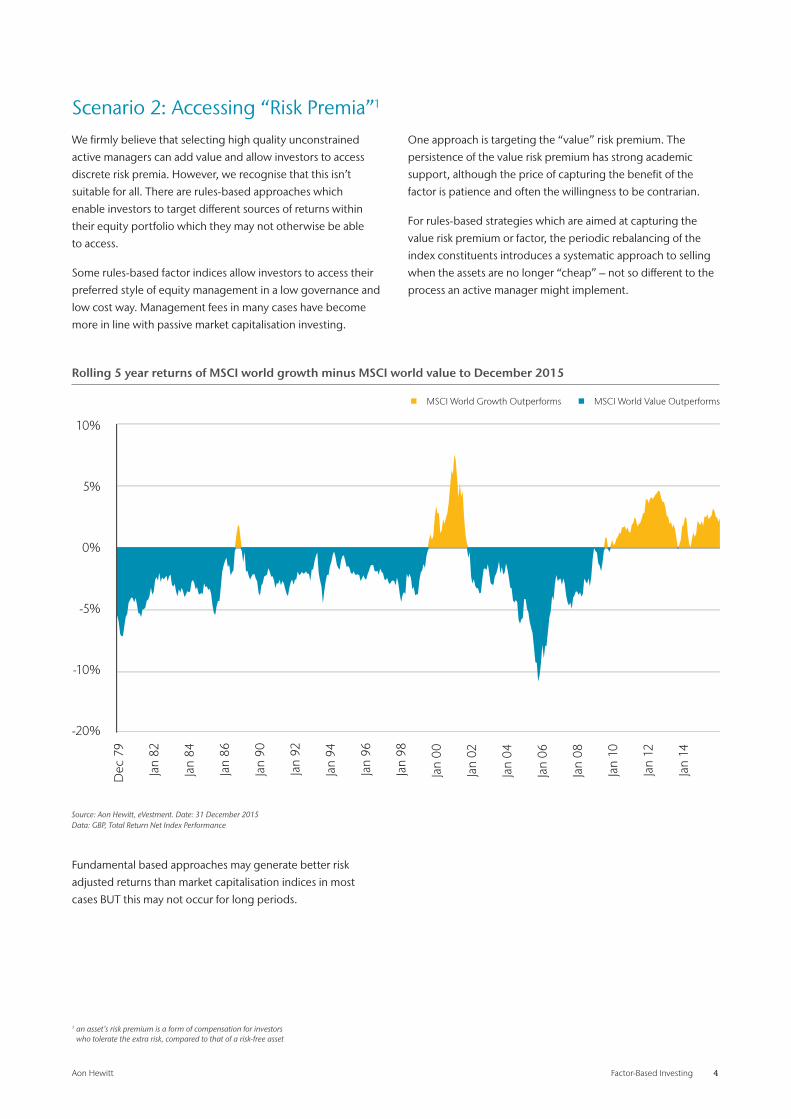

Scenario 2: Accessing “Risk Premia”1

We firmly believe that selecting high quality unconstrained

active managers can add value and allow investors to access

discrete risk premia. However, we recognise that this isn’t

suitable for all. There are rules-based approaches which

enable investors to target different sources of returns within

their equity portfolio which they may not otherwise be able

to access.

Some rules-based factor indices allow investors to access their

preferred style of equity management in a low governance and

low cost way. Management fees in many cases have become

more in line with passive market capitalisation investing.

One approach is targeting the “value” risk premium. The

persistence of the value risk premium has strong academic

support, although the price of capturing the benefit of the

factor is patience and often the willingness to be contrarian.

For rules-based strategies which are aimed at capturing the

value risk premium or factor, the periodic rebalancing of the

index constituents introduces a systematic approach to selling

when the assets are no longer “cheap” – not so different to the

process an active manager might implement.

1 an asset’s risk premium is a form of compensation for investors who tolerate the extra risk, compared to that of a risk-free asset

Fundamental based approaches may generate better risk

adjusted returns than market capitalisation indices in most

cases BUT this may not occur for long periods.

10%

5%

0%

-5%

-10%

Dec

79

Jan

82

Jan

84

Jan

86

Jan

90

Jan

92

Jan

94

Jan

96

Jan

98

Jan

00

Jan

02

Jan

04

Jan

06

Jan

08

Jan

10

-20%

Jan

12

Jan

14

Rolling 5 year returns of MSCI world growth minus MSCI world value to December 2015

MSCI World Growth Outperforms MSCI World Value Outperforms

Source: Aon Hewitt, eVestment. Date: 31 December 2015 Data: GBP, Total Return Net Index Performance

Aon Hewitt Factor-Based Investing 5

Scenario 3: Better risk-adjusted returnsRisk-adjusted returns are often considered when setting asset

allocation, but can be overlooked when constructing an equity

portfolio – particularly for passively managed mandates.

For investors who recognise some of the limitations associated

with the market capitalisation approach, investing in

combinations of factor-based strategies has delivered higher

risk adjusted returns, at least over the longer term.

Some investors select an index fund under the impression that

this will always provide diversification at low cost, without

understanding possible risks, especially in small markets,such

as extreme concentration in a small number of stocks or to a

particular industry.

The market capitalisation approach invests a larger proportion

of the index to stocks which have been driven up to levels

which may not reflect their intrinsic value. Although investors

will benefit from the price increase, these are potentially the

holdings which may suffer the greatest losses when market

bubbles burst. One well-known historic example of this is the

“Dotcom Bubble” when equity market indices developed a

relatively high concentration to Technology, Media and

Telecommunications sectors.

Combining strategies can be a particularly effective way of

including rules-based factor indices in a portfolio. The chart

below demonstrates how a higher “Sharpe Ratio”, a common

measure of risk-adjusted returns, might be achieved by

combining exposure to different factors compared to an

investment in a market capitalisation index.

The portfolio below combines a minimum variance low volatility

approach and a value weighted index constructed using a

composite of company fundamentals in equal proportions.

Weight of the IT sector in the S&P 500 index

Weight of the IT sector in the S&P 500 Index

Source: Datastream

Ind

ex w

eig

ht

0%

10%

20%

30%

40%

50%

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Aon Hewitt Factor-Based Investing 6

Index risk return

MSCI World

Low Volatilty Value Weighted Fundamentals

50% Low Volatility / 50% Value Weighted

Fundamental

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

10.0% 11.0% 12.0% 13.0% 14.0% 15.0% 16.0% 17.0% 18.0%

An

nu

alis

ed R

etu

rn

Annualised Risk Source: Aon Hewitt, eVestment. MSCI, S&P, FTSE Data: GBP, Total Return Net Index Performance. 10 years to 31 December 2015.

MSCI World

50% Low Volatility / 50% Value Weighted Fundamentals

Return (% pa) 4.1 6.4

Risk (% pa) 14.8 12.9

Sharpe Ratio 0.1 0.3

It should be noted that the above combination is a backtest and

not a live portfolio implemented over the entire period shown.

We would not typically expect the observed level of

outperformance relative to a market capitalisation index

over all time periods.

Aon Hewitt Factor-Based Investing 7

ContactOliver Sample Associate Consultant+44 (0)113 291 [email protected]

ConclusionImplementing an equity allocation is an active decision and

market capitalisation indices may not always be the best fit.

The scenarios above demonstrate how equity portfolios

tailored towards specific factors have the potential to be

better suited to investors’ objectives.

Although factor-based investments can produce periods of

underperformance against market capitalisation indices over

the short to medium term, over the longer term, investing in

combinations of factors has the potential to deliver higher

risk adjusted returns.

We recommend talking to your usual Aon Hewitt contact

to discuss how factor-based investing can be employed

effectively within your strategy.

GlossaryMSCI minimum volatility index Minimum variance approach which weights portfolios to target

the lowest portfolio volatility for a given opportunity set and

under certain constraints.

Drawdown Measures the fall in cumulative return from a previously

reached peak in market value.

Value stocks Stocks which are priced cheaper than their company

fundamentals (earnings, sales etc.) would suggest.

Sharpe ratio Risk adjusted return measure, defined as the excess return

above a risk free return, per unit of volatility.

Value weighted fundamental indices

Illustrative portfolio in Scenario 3 uses a fundamental based

index which weights portfolios using a combination of

fundamental factors, including total cash dividends, free cash

flow, total sales and book equity value.

Aon Hewitt empowers organisations and individuals to secure a better future through innovative talent, retirement and health solutions. We advise, design and execute a wide range of solutions that enable clients to cultivate talent to drive organisational and personal performance and growth, navigate risk while providing new levels of financial security, and redefine health solutions for greater choice, affordability and wellness. Aon Hewitt is a global leader in human resource

solutions, with over 30,000 professionals in 90 countries serving more than 20,000 clients worldwide. For more information on Aon Hewitt, please visit: aonhewitt.com

Follow Aon on Twitter: twitter.com/Aon_plc

Sign up for News Alerts: http://aon.mediaroom.com/index.php?s=58

About Aon Hewitt

About Aon Aon plc (NYSE:AON) is a leading global provider of risk

management, insurance brokerage and reinsurance

brokerage, and human resources solutions and

outsourcing services. Through its more than 72,000

colleagues worldwide, Aon unites to empower results

for clients in over 120 countries via innovative risk

and people solutions. For further information on our

capabilities and to learn how we empower results for

clients, please visit: http://aon.mediaroom.com/

This document and any enclosures or attachments are prepared on

the understanding that it is solely for the benefit of the addressee(s).

Unless we provide express prior written consent, no part of this

document should be reproduced, distributed or communicated to

anyone else and, in providing this document, we do not accept or

assume any responsibility for any other purpose or to anyone other

than the addressee(s) of this document.

Notwithstanding the level of skill and care used in conducting due

diligence into any organisation that is the subject of a rating in this

document, it is not always possible to detect the negligence, fraud,

or other misconduct of the organisation being assessed or any

weaknesses in that organisation’s systems and controls or operations.

This document and any due diligence conducted is based upon

information available to us at the date of this document and takes no

account of subsequent developments. In preparing this document we

may have relied upon data supplied to us by third parties (including

those that are the subject of due diligence) and therefore no warranty

or guarantee of accuracy or completeness is provided. We cannot

be held accountable for any error, omission or misrepresentation of

any data provided to us by third parties (including those that are the

subject of due diligence). This document is not intended by us to

form a basis of any decision by any third party to do or omit to do

anything.

Any opinions or assumptions in this document have been derived

by us through a blend of economic theory, historical analysis and/or

other sources. Any opinion or assumption may contain elements of

subjective judgement and are not intended to imply, nor should be

interpreted as conveying, any form of guarantee or assurance by us of

any future performance. Views are derived from our research process

and it should be noted in particular that we can not research legal,

regulatory, administrative or accounting procedures and accordingly

make no warranty and accept no responsibility for consequences

arising from relying on this document in this regard.

Calculations may be derived from our proprietary models in use at

that time. Models may be based on historical analysis of data and

other methodologies and we may have incorporated their subjective

judgement to complement such data as is available. It should be

noted that models may change over time and they should not be

relied upon to capture future uncertainty or events.

Aon Hewitt Limited is authorised and regulated by the

Financial Conduct Authority. Registered in England & Wales.

Registered No: 4396810.

Registered Office:

The Aon Centre

The Leadenhall Building

122 Leadenhall Street

London EC3V 4AN

Copyright © 2016 Aon plc

aon.com

Risk. Reinsurance. Human Resources.