Facing the Interview

331

Facing Interview? 2011 Page 1 Team SBLC Patna 2011 Facing Interview? This preparation guide for interview is a voluntary effort in the direction of collating past and general experiences of candidates who have appeared for interviews in our Bank in various scales & grades. Coupled with this, an effort has also been made to capture the latest & significant happenings in various domains of Banking & Finance World. The questions that have been compiled are only indicative and candidates can expect additional derivative questions based on these indicative questions. Here and there, indicative answers are also given and we suggest our esteemed aspirants to refer our SBLC’s promotion materials for further details. In order to assist our readers in obtaining answers/information on the topics highlighted, information index of “what is available where” is also provided. We are sure that all this will be very useful to our esteemed aspirants. WE wish the prospective candidates ALL THE BEST. Compiled By: Pramod Kumar Mishra Chief Manager, Training State Bank Learning Centre, Patna 0612-2592980

-

Upload

nottathpradeep -

Category

Documents

-

view

329 -

download

58

description

come on face it...

Transcript of Facing the Interview

Facing Interview? 2011 Page 1

T

eam

SB

LC

Pat

na

20

11

Fa

cin

g I

nte

rvie

w?

This preparation guide for interview is a voluntary effort in the direction of collating past and general experiences of candidates who have appeared for interviews in our Bank in various scales & grades. Coupled with this, an effort has also been made to capture the latest & significant happenings in various domains of Banking & Finance World. The questions that have been compiled are only indicative and candidates can expect additional derivative questions based on these indicative questions. Here and there, indicative answers are also given and we suggest our esteemed aspirants to refer our SBLC’s promotion materials for further details. In order to assist our readers in obtaining answers/information on the topics highlighted, information index of “what is available where” is also provided. We are sure that all this will be very useful to our esteemed aspirants. WE wish the prospective candidates

ALL THE BEST.

Compiled By: Pramod Kumar Mishra Chief Manager, Training

State Bank Learning Centre, Patna 0612-2592980

Facing Interview? 2011/Team SBLC Patna/PKM Page 2

(“ctrl+click” on the link will take you to the topic of your choice and “to Index” will again

redirect you to Index page)

INDEX

SL. Topics Description Page No.

1 General Guidelines

Suggested readings, Study materials

03

2 Personality/ Self

Personality related questions 06

3 Career Test

Career related questions

08

4 Assignments / work

Current & previous assignments

Promotion Appraisal Formats (for preparing

your answers around PAF)

10

5 Our Bank

SBI specific questions , Vision, Mission &

values, Awards & Recognition, List of Directors

on the Central Board of State Bank of India

34

6 General awareness

General questions relating to Economy

& Financial System 38

7 Banking Scenario

General Banking related questions with

special emphasis on Indian Banking 46

8 Readings

Chairman’s statement & interviews. Important articles that have appeared in Bank’s official publications/Newspapers

48

9 Circulars

“e-Circulars” – Index of Important Circulars (Gist of e Circulars: Hyperlinked)

61

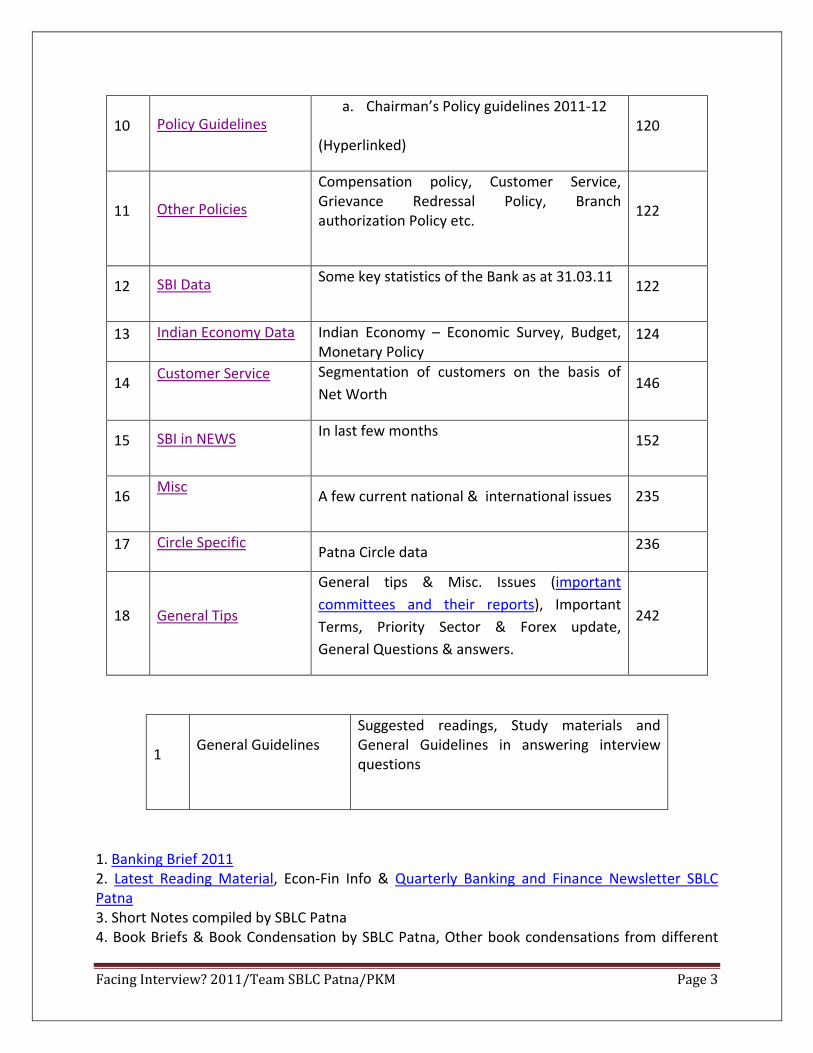

Facing Interview? 2011/Team SBLC Patna/PKM Page 3

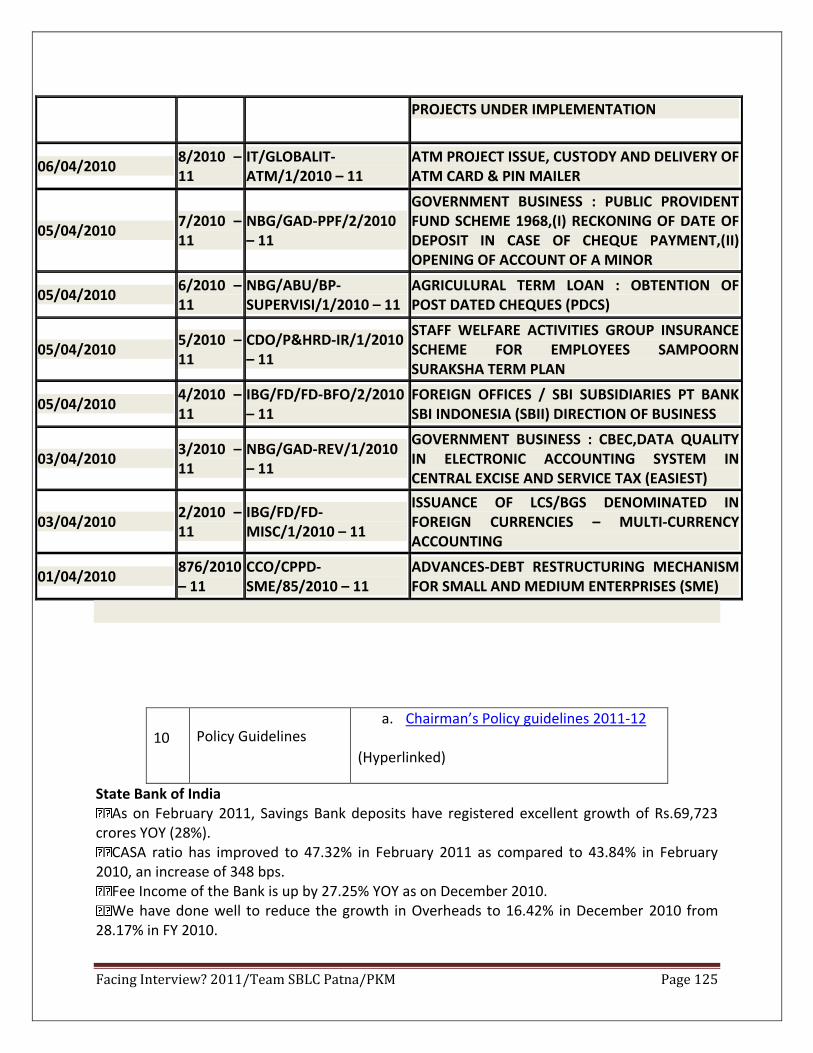

10 Policy Guidelines

a. Chairman’s Policy guidelines 2011-12 (Hyperlinked)

120

11 Other Policies

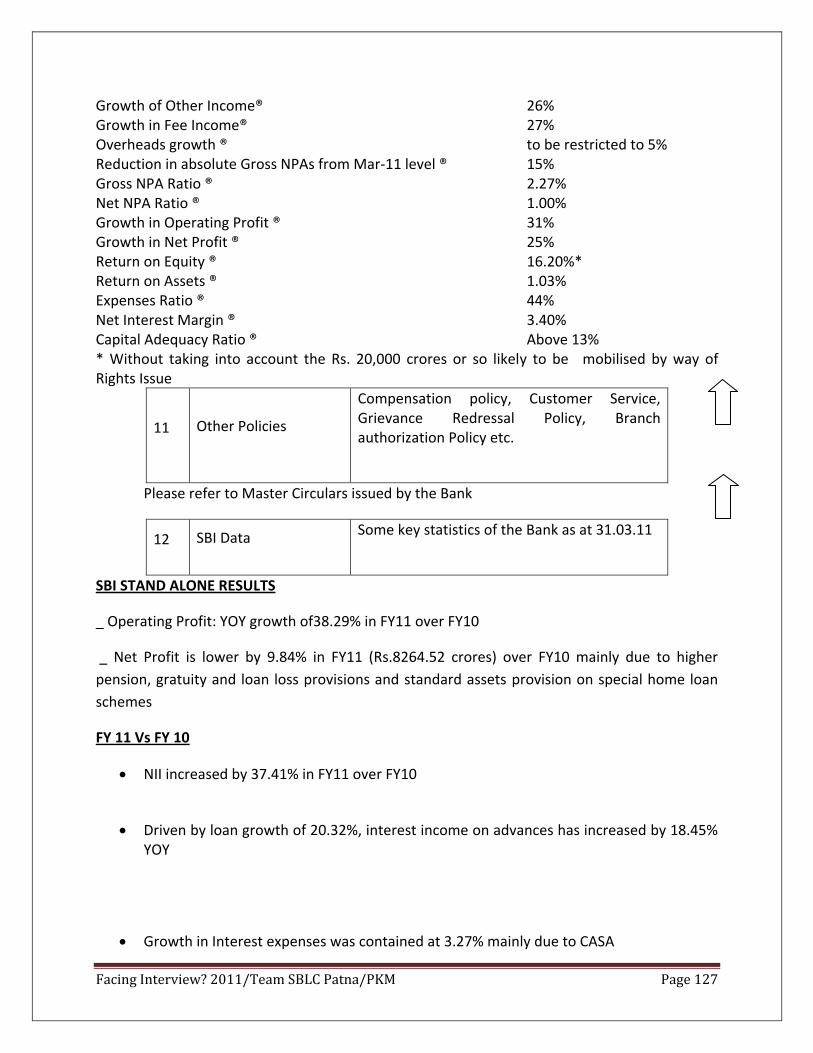

Compensation policy, Customer Service, Grievance Redressal Policy, Branch authorization Policy etc.

122

12 SBI Data

Some key statistics of the Bank as at 31.03.11

122

13 Indian Economy Data

Indian Economy – Economic Survey, Budget, Monetary Policy

124

14 Customer Service

Segmentation of customers on the basis of

Net Worth 146

15 SBI in NEWS

In last few months

152

16 Misc

A few current national & international issues 235

17 Circle Specific

Patna Circle data 236

18 General Tips

General tips & Misc. Issues (important

committees and their reports), Important

Terms, Priority Sector & Forex update,

General Questions & answers.

242

1 General Guidelines

Suggested readings, Study materials and General Guidelines in answering interview questions

1. Banking Brief 2011 2. Latest Reading Material, Econ-Fin Info & Quarterly Banking and Finance Newsletter SBLC Patna 3. Short Notes compiled by SBLC Patna 4. Book Briefs & Book Condensation by SBLC Patna, Other book condensations from different

Facing Interview? 2011/Team SBLC Patna/PKM Page 4

ATIs/SBLCs. 5. SBIRD weekly brief: Atleast 6 months since 6. Master Circulars ( SBI): latest 7. Master Circulars ( RBI): latest (July 2010) 8. Loan Policy 2009 (Modifications): if you are dealing in advances. 9. Credit Management (SBSC Hyd.) : if you are dealing in advances. 10. Lectures / Speeches (especially for higher level promotions): if required, please contact. 11. Internal Magazines published by different ATIs/ Departments: available on SB times 12. Magazine & Reading Materials from IIBF: iibf.or.in : if required , please contact

General Guidelines for answering Interview Questions

First of all please prepare:

(Please structure your answers in a notebook/diary. Let it have some relation with your self-

appraisal for the last 4 yrs.)

1. Profile: Self & Branch/Unit (in detail), Region, Circle & Bank (Basic details)

2. SWOT analysis: Self & Branch/Unit (in detail), Region, Circle & Bank (Basic details)

IMPORTANT TIPS Be in yourself; do not try to imitate anyone. Bearing: Walk erect and with confidence. Maintain eye contact with the interview board Chairman and members while talking. Irrespective of the fact who has asked the question, maintain eye contact with every board member with special emphasis on Chairman of the board. Smile and be pleasant. Be enthusiastic and interested. You must be lively, keen and cheerful. Let your optimism and energy radiate. Conduct: Politeness pays. Be empathetic and attentive. Observe meticulously the code of manners and etiquette. Never be rude, argumentative or offensive. Do not neglect to pay compliments. Speech: Talk slowly deliberately and audibly. You should neither shout nor mumble. Pronounce your words clearly and crisply. Never be dull or monotonous with your words. Avoid use of phrases such as, you see, I say, of course I mean, etc. Dress: Choose your dress with care. It must be comfortable and befitting for the occasion. Smart and trendy look is not required; you must look sober. Choose your dress wisely and invest some amount, if required. Use shoes with laces and it must shine from the back side, too. Take special care on top 12 inches & bottom 12 inches, as well. Personal Hygiene: Be neat, tidy and clean. See that you are well groomed.

Facing Interview? 2011/Team SBLC Patna/PKM Page 5

Self control: Do not become emotional or get nervous. Be confident and patient. Check unnecessary movements. The Board may deliberately try to provoke you and see how easily you could be upset. Never lose your temper, whatsoever may be the situation. Do not bluff: State only what you know to be correct. Do not hazard guesses unless you are asked to do so. No beating in the bushes, please. Say politely that you are not very sure and you will try to know that. Shooting lions and boasting will land you in trouble. Do not try to be too clever. Remember, the board has years of experience and has interviewed several candidates. Own up your mistakes: If the board points out that you had made a mistake and you realize it to be fact, then be courageous and own it up. Never try to cover it up. The Board will respect you for your honesty. Initiative: Use your initiative but watch the reactions of the Board. Also, be conscious of your limitations. Do not over shoot. Do not draw conclusions. Be discreet when you talk about your own accomplishments. They should be conveyed subtly and tactfully. Criticism and Arguments: Do not criticize. Never try to find faults. As far as possible, stress the good point of others. It is better to be silent than to criticize. Do not get involved in unproductive arguments. You have not gone to the interview to win a verbal battle but to have a meaningful conversation. See how you can agree rather than to disagree. As a last resort, you may agree or disagree. Always remember one thing, you may win an argument but then chances of winning interview would be bleak. Listen and Observe: Keep your eyes and ears open. Study their reactions. You will know when to stop talking and when to listen. As a rule, do not interrupt. If the other person wishes to talk, let him do so. In fact, encourage him to talk. Be an attentive and enthusiastic listener. Practice: Practice, practice and practice. You must have as much practice as possible. Enlist the goodwill and co-operation of your friends, colleagues, elders and family members and have practice sessions with them. The more practice you have, the better it will prove. It will guarantee your SUCCESS. Try to frame your best possible answer for probable questions. IMPORTANT TIPS FOR FACING INTERVIEWS CONFIDENTLY You do need to be aware about your surroundings and this includes familiarity with current affairs. Banking industry specific questions are common. In addition, there are certain questions you may encounter during the interview, in one form or the other. These relate to questions about yourself, what you have been doing and what you want to do in future. In fact, many a times interview starts with personal sort of questions like “Tell me about yourself” or “your SWOT analysis”, etc. It is a good idea to sit for mock interviews with your friends or colleagues. Remember, practice makes a man perfect. Practice how you are going to enter into and exit from the interview

Facing Interview? 2011/Team SBLC Patna/PKM Page 6

room. If it makes you comfortable, take a few deep breaths before entering into the room and pray the deity you worship and faith most. There is no standard correct answer as such. What you need to do is to answer these questions calmly. Even during real interview, you should think before answering the questions. Prepare a diary of probable questions and answers and practice it as many times as you can. You need to pause before answering to collect your ideas as it will help you put together all the points, substantiating your response. Though you should not gloss over your weaknesses, you need to focus on your success and your achievements/strengths. You need to convince the interviewer that you are the most suitable person for the higher position. Like for Scale IV & V the traits which are considered as:

a. Ability for proactive action b. Variety of assignments c. Vision & execution capabilities d. Problem solving & decision making e. Team building & motivation f. Customer & marketing orientation

So, you must prepare yourself based on these traits. We are providing hereunder some questions, the Interview Board may not ask the same

question but preparation of it will make you comfortable in answering all type of questions.

2 Personality/ Self

Personality related questions

1. What are the goals in your life?

2. Let us know something about yourself that we don’t know?

3. What is the significance of your name or surname?

4. Let us know something about your birthplace, place of living, workplace. Please, remember special features of the place, like, if you belong to Nalanda, you are supposed to know about the Nalanda Vishwavidyalaya, Rajgir & Pawapuri, if you belong to Jamshedpur, you must know the full name of TISCO and unique features of the city etc.

Facing Interview? 2011/Team SBLC Patna/PKM Page 7

5. Let us know something about your academic background.

6. Once the above question is asked, you may expect some questions on your subject of Post Graduation/Graduation/area of specialization.

7. What were your subjects in College? (Once this is asked, 2 or 3 subject related

questions may be expected)

8. In case you have specialization in fields not directly related to banking, say – electronics,

engineering, etc., then you can expect questions like how relevant has been your specialization background helpful in your current banking career.

9. Your Branch/unit/self Profile.

10. If you were to make a SWOT ANALYSIS of yourself, what do you think your assessment

would be?

11. How do you balance your professional and personal life?

12. When you face difficult situations/criticism, how do you respond?

13. What are the most 3 important events in your life?

14. Who has / have influenced the most in your life? Why?

Facing Interview? 2011/Team SBLC Patna/PKM Page 8

15. Have you changed over the years? If so, how & why?

16. Do you consider yourself as a leader or a follower? What are the qualities required in a

leader?

17. Who are your role models? Why are they role models?

18. What are your hobbies? (One or two questions relating to hobby(ies) may be expected)

19. How do you spend your leisure time?

a. Which magazines and newspapers do your read regularly?

What do you like about these magazines and newspapers? What columns or sections do you like in these magazines and

newspapers? Who are the editors of the magazines? Any special feature attached to that newspaper?

b. What were the headlines of today’s newspapers?

c. Do you read books? Which are your favourite books? Who are your favourite

authors?

(If you indicate that you like literature, you can expect related questions on recent happenings like who is the winner of Nobel Prize for literature, Booker Prize etc. for the latest year )

d. If you happen to say, you enjoy watching cricket, you can expect questions like:

Do you think Indian Cricket team is playing well? Are we experimenting too much? What are the suggested measures to improve cricket? Why is cricket popular in India? About World Cup, IPL & T-20.

e. If you happen to say, you enjoy watching TV, you can expect questions like:

Facing Interview? 2011/Team SBLC Patna/PKM Page 9

Which TV serial you like most? Why do you like the particular TV serial? About TV related awards. What is TRP? How to calculate TRP etc.

20. Lady candidates can expect questions like:

How do you balance your career and family needs? Are you ready to be transferred to remote places, different assignments? List out the names of ladies who have made it to the top in the recent past in

different fields?

3 Career Test

Career related questions

1. List out 5 major accomplishments / highlights of your career.

2. List out your major accomplishments during the last 5 years? Especially if posted as BM then achievements during your tenure.

(Let it have some relevance to your Self-Appraisal Report or let it not contradict your report submitted earlier)

3. What are the difficult assignments handled by you in your career? Why do you think

they were difficult? How did you handle it?

4. What skills have you developed over the period in the Bank?

5. Why do you think you deserve promotion?

6. Are you ready to work anywhere in India? Ready to be transferred anywhere? Ready to

be posted for any assignments?

7. What do you think about yourself in the Bank?

a) 5 years hence b) 10 years hence c) Your peak career advancement in the Bank and reasons for your answer.

Facing Interview? 2011/Team SBLC Patna/PKM Page 10

8. In case you become part of the Top Management today, list out your priorities and

concerns? Few reasons for your priorities.

9. What is your wish list for the Bank?

10. What kind of assignments would you like to deal within the Bank? According to you,

which is the best & worst assignment in the Bank? Reasons for your choice.

11. What traits do you think are required to become successful in one’s career? What is

OLQ’s (Officer like qualities).

12. Do you feel Bank has given you due recognition till now? If yes, how? If not, why?

13. If you have a lucrative career option outside the Bank, what factors will you take into

consideration for continuing or switching over?

14. How was your Branch Manager’s assignment experience? What do you think are

the ideal qualities of a Branch Manager? How independent were you in discharging your duties? What were the pressures borne by you? In your opinion Branch Manager’s assignment is easier or tougher now-a-days than in earlier times? Give reasons to support your answer.

15. What do you think is your level of self-motivation? Do you think there is an enabling

environment in the Bank for you to realize your full potential? Do you think, Bank has given you ample opportunity for growth?

16. What is leadership? How many types of leaders are there? Which Leadership Style

you like & follow? And why?

Facing Interview? 2011/Team SBLC Patna/PKM Page 11

17. Can you recollect any humorous, important, momentous incidence or touching

moments in your career / life?

18. SWOT Analysis- Self, Assignment, Region, Circle, Bank.

19. Your concerns- Official, personal & others.

20. Your greatest achievements – Job related achievements in your personal life.

4 Assignments / work

Current & previous assignments

This is your domain and, therefore, you are the best judge. Needless to say, the candidates are expected to be thorough, knowledgeable and presentable in this area. Sit quietly for two or three hours and jot down as many questions as possible in these and other related areas. For example, the candidate may be in a forex dealing branch and handling exports related seat. The expectation here would be that he knows everything about Foreign Exchange. Also, he will be expected to know what is happening at the macro level especially for SMGS & TEGS level promotion, though it may not have a direct bearing on his seat. Hence, develop quickly the domain related knowledge. Be very clear about your assignment, role, targets, constraints, challenges, opportunities and future plans. It is recommended that, everyone should go through the questions suggested for a particular assignment. Emphasis may be more on present assignment related questions but for complete view, it is required to have a look at all the questions. Go carefully through your self-appraisal report. If you are in a Branch, go through MIS , P-Report, Branch Dossier, recent highlights of your Branch (Proposals handled, new business booked, etc.),Inspection & Audit Reports , highlights of your city, town, etc. In the interaction during interviews, mainly the focus ranges from job knowledge to attitudinal aspects, from potential to performance and from banking history to emerging banking scenario. Bankers are expected to be conversant with all the changes taking place in the financial services sector. Interview is an opportunity for you to present your personality consisting of your attitude, views and awareness level before the interview board, so that the potential in “You” is appropriately judged by the members of the Interview Board, who are learned and experienced people in their own field of specialization.

Facing Interview? 2011/Team SBLC Patna/PKM Page 12

In order to judge your potential, evaluation of your performance in the recent past, operating style, team building capabilities, effectiveness, neutral judgment level, transparency in dealings, initiatives, attitude, leadership qualities, your conflict management techniques, your pressure management techniques, your vision and ability to see beyond the boundaries are some noteworthy attributes. For junior level promotions, knowledge about bank’s scheme and ability for future growth is a must, but for fairly higher grade promotions what is needed is your leadership qualities, your negotiation skills, your ability to handle difficult and conflicting situations, your visioning ability, your practical strategy for future development of the organization and also for the self is a pre-requisite. Although, you should focus on current assignment, you may be asked some questions from your earlier assignments. Assignment related important questions:

A. If the candidate is from a Branch: 1. Your priority areas? 2. Location of your Branch. 3. Achieved budget? Reasons, if not achieved; strategies adopted, if achieved.( all

parameters). Business performance of the branch vis-à-vis budget. Growth achieved during your tenure vis-à-vis prior to yours.

4. If you are from a Super Circle of Excellence branch: what is the difference between your and other general branches? How could you justify that?

5. How do you motivate employees of your branch? 6. Special characteristics of your branch? 7. What is the scope of business in your area of operation? 8. Is Dynamic Budgeting Method better than old budget settlement one? Give reasons for

your answer. 9. What is your branch’s market share in the district? Is it improving or declining?

Reasons? 10. Who are your competitors? Your business strategies to beat competition? 11. Top 5 Borrowers, Depositors & NPA accounts of your branch. Your strategies regarding

all these three? Also, name five top non-customers in your area of the branch. 12. Misc. business & misc. income in your branch and your strategies to increase it. 13. Why fee based income is assuming importance in recent years? 14. Which are the 5 big proposals handled by your branch? 15. Any special achievement of your Branch? 16. Your strategy to reduce NPA of your branch? 17. How do you involve staff in business development? Whether bank has also taken any

steps in this regard? 18. What is meant by ‘money laundering, smurfing & money mule’? 19. What are the latest KYC guidelines? Is KYC a hindrance to business development? 20. Is BPR system/ SWO system working effectively in your branch? 21. Is your branch is in operating profit? If yes, your strategy. If not, reason?

Facing Interview? 2011/Team SBLC Patna/PKM Page 13

22. Efficiency ratios of the branch? GRR of the branch? Increase/decrease in which ratio is considered better?

23. Is IBTS working well in your branch? 24. Are you working on “LOS”? Is it better than “Dream Home”? if so, how? 25. Do you get full cooperation from your controller? Any example to substantiate? 26. Instructions regarding Note Refund Rules. 27. Recent instructions regarding Lockers, Nomination, Inoperative accounts, transfer of

accounts, etc. 28. Do you think we should promote RTGS, NEFT? Reasons for your answer. 29. Your practical strategies for overall development of the branch? How it is different from

others? 30. Your strategy to improve inspection rating of your branch? 31. Newly created BPR posts: your opinion about their effectiveness. 32. Do you think BPR is stabilized? BPR is helping you or creating problems? Reasons for

your answer. 33. Growing NPA is because of BPR outfits? Your opinion? 34. Effect of ADWDR on loan recovery scenario in agricultural finance? 35. Budget should be the responsibility of CPCs also. Your view? 36. Creation of CPCs has helped branches or not? 37. How do you handle coordination issues with CPCs? 38. ‘Post BPR, branch manager and branch people have nothing to do’. Justify your role vis-

à-vis the statement? 39. Do you think we have more products than required? 40. Biggest challenge/ hurdle branches/staff are facing now a days? Your strategy to deal

with the issue. 41. Your strategy to get the maximum from new recruits? 42. How do you ensure up-time/availability of ATMs of your branch? Present position? 43. Your views about SMS Unhappy, LMS etc. 44. In SBI, team is not working only individuals are. Your opinion and reasons for the

statement? 45. BC/BF/MRT and their effective utilization. 46. How you ensure to prevent frauds in your branch? 47. How to build committed teams? 48. How do you communicate to your staff? 49. Your strategy to improve and maintain harmonious inter-personal & intra-personal

relationship? 50. Customers are not always right. Your views in this regard? 51. Who is more important for you, your boss, employees or your customers? Reasons for

your answer. 52. What are the criteria for Chairman’s Club membership and the Incentive scheme? 53. Are we cross-selling in true sense and ethically? 54. How do you make people to listen your view point? 55. SBI Life is deriving more benefit from us than we derive out of them?

Facing Interview? 2011/Team SBLC Patna/PKM Page 14

56. Even after various alternate channels available to customers, we are unable to decongest our branches. Why? How to improve the situation?

57. Your practical strategy for crowd management. How it is different from others? Is it successful?

58. Customer’s expectations vis-a-vis our service standards: your opinion and reasons for your opinion.

59. There should be budgets for strategic business units also like SMEBU,PBBU in order to

achieve goals of the operation units. Your opinion and Bank’s instructions in this regard.

B. If the candidate is from an Administrative Office/ Regional Business Office:

If you are from Vigilance Deptt: About whistle blowing, vigilance angle, the alertness award, type of vigilances, DPD & Vig. Procedure, Preventive Vigilance leave etc.

If you are from Inspection Deptt.: about RFIA, Various ratings and their details, how do you help branches in improving rating? What is your role actually, position of branch ratings in the Circle, latest guidelines, etc.

If you are from HR wing: how do you justify your role, what is your role actually (controller or enabler)? Difference between P&HRD & HRD?, Any new initiative taken by you in your area of operation, how to motivate employees? About REMBS, Silver Jubilee Award, HRD philosophy, Training Philosophy, how do you assess training needs, how to contain attrition rate? New HRD initiatives of the Bank in recent past; Maternity leave, Special leave to join spouse abroad etc.

Like that please prepare yourself in your core area of operation. You must be thorough in your own field. Prepare yourself on the basis of “MSC principle”, Must: yourself and your domain, Should: about surroundings, related areas, Branch/Unit, Region, Circle, Bank, Could: Banking & Finance World.

- There should be budgets for strategic business units too, like SMEBU,PBBU in order to

achieve goals of the operation units. Your opinion and bank’s instructions regarding this.

- Considering the large-scale changes taking place in the Bank, what do you think should be the role of Administrative Offices? Do you feel present structure of Circle and Regions are good as compared to the earlier structure? Give suitable reasons.

- Several Regional offices have been shifted to their area of operations- effective or creating problems? Elaborate your answer.

- Opening of new branches – beneficial or burden? Reasons for your answer.

- Financial Inclusion: Boon or Bane?

Facing Interview? 2011/Team SBLC Patna/PKM Page 15

- Your comments on the workings of different cells (SMECCC, RCPC, RACPC, CPC etc). Coordination issues- your experience and strategies?

- Utilisation of BCs/BFs/MRTs members, effective? Give reasons for your answer.

- Do you think growing NPA is a concern in your region? If so, reasons and remedial measures, your strategy? If not, how you tackled the issue?

- Your strategy to reduce operating expenses and earning more misc. income?

- Strategies for overall development of the region.

- Biggest challenge your region is facing? Your strategy?

- Affect of ADWDRS in your region? Recovery position in your region?

- Are we fulfilling the role we are undertaking?

- Do you think that Administrative Offices are over-staffed? SBI is top heavy?

- What changes have taken place in our administrative set-up during the last few years?

What are the changes proposed?

- Administrative offices are profit centers or cost centers?

- Do you think we are spending more time than required at our workplaces? What are

Facing Interview? 2011/Team SBLC Patna/PKM Page 16

the ways in which we can reduce our time at our workplace?

- As a Controller, when you visit a Branch, what are the things you will give priorities to

take care of the Branch’s smooth & safe functioning? Is there any specific instruction regarding Branch Visit/Inspection?

- What is your strategy to take care of branches and how you derive maximum output

from the branch people?

C. If the candidate is from BPR cell:

- Are we fulfilling this role?

- Do you feel satisfied with your work output/job conditions?

- Do you feel that BPR cells are working as per Bank’s need and as per the needs of the operations? If yes, please explain in brief. If no, suggest measures for improvement.

- Do you feel existence of knowledge gap at BPR cells, branches?

- What measures will you undertake if you have the authority to increase overall

efficiency and working condition of a particular cell?

- What would you suggest for better performance of the operating units?

- Do you think on account of creation of various cells, customer ownership is missing?

- Do you feel there should be budget for CPCs also? If so, how? If not, why? Give reasons to substantiate your views.

Facing Interview? 2011/Team SBLC Patna/PKM Page 17

- Your opinion and experience about the functioning of BCs/BFs/MRTs/MPST/HLST etc., reasons for your response?

- Do you think growing NPA is due to improper functioning of BPR cells?

- Coordination issues; intra-cell and inter-operations? Your practical strategies for improvement?

- Do you think BPR cells are now well stabilized? Reasons for your opinion. - Dream Home software is better than “LOS”: your opinion & reasons for your opinion. - “LOS” is a LOSS or gain: your opinion and reasons for your opinion.

- Are you satisfied with the pace of development that is going on in the bank? D. If the candidate is from HR wing/ATIs/SBLCs: - Am I fjustifying the present role which I am currently undertaking?

- Impact/Effect of Citizen SBI programme/UDAAN. Give reasons for your reply. Any

memorable event during Citizen SBI programme/UDAAN, please describe. - Difference between a Facilitator, Trainer, Mentor, Coach? You are what among these?

- Is SBI a learning organisation? If yes, how? If no, furnish reasons and your practical

strategies for making SBI a learning organisation. - ATIs/SBLCs are profit centers or cost centers? Give reasons for your answer. - ATIs/SBLCs should be converted into profit centres. If not, why? If yes, how? - Specialization of SBLCs/Trainers is the need of the hour, justify. - What is “SME” in training? ( Subject Matter Expert) - Lateral recruitment of trainers is the need of the hour, justify. - SBLCs are playing their role? Strategies for future roles. - Difference between Knowledge & Learning?

- Details about STU and its impact? New initiatives taken by STU? Difference in Training

system & training imparted, after formation of STU.

Facing Interview? 2011/Team SBLC Patna/PKM Page 18

- Your strategy to assess & fulfill the needs of the operations/employees. - How do you ensure effectiveness of your sessions? - If any trainee is not giving ear to your words or not listening you, what would be your

strategy? - Credibility of the trainers and training system. - Integration of training system with operations- your practical strategy? - SWOT analysis of HR/Training System. - You are taking sessions on which topics or you are SME in? Expect some questions in

depth from topics of your sessions specially the practical aspect of it. Like, if you say, I take sessions on Marketing, you may expect question on Marketing & Selling, difference between the two terms, what is cross-selling, Up-selling, mis-selling, down-selling?

- When & how you get time to update yourself? - Your special initiatives ? if any. - What is your prescription to the trainees specially the new ones? - How do you maintain discipline during sessions? If one participant is coming late despite

your repeated requests, what would you do? - Profile of Training System & your ATI/SBLC. - How do you calculate capacity utilization? Capacity utilization of your ATI/SBLC for the

last three years? Reasons for rise & fall in it over years. - How do you ensure nomination & deputation of participants for any training

programme? - Do you think STRAPS is sufficient? How & why? - How do you motivate trainees for “eLearning” & how do you ensure they take interest

for the same. - Posting at ATIs/SBLCs is not a challenging assignment: your opinion? - Are you enjoying your assignment/role? How? - How have you added value in your role? - It’s a cozy posting. How you have managed this posting? - About the Project works, Case studies, Book-reviews & Book Condensations, etc. - Training methodology you have adopted and how do you decide which methodology is

better for any particular session and group of trainees. - Trainer-Trainee ratio in your Circle, what is optimum? Your view on this. - How to develop a caring organisation? - Attrition rate is higher in case of new entrants. Your strategy to retain the talent and the

challenges attached to it. - Extent of frauds & corruption in the Banking system. How to deal with the situation,

especially in the light of mass level recruitment, new branch openings and technological advancements.

- Role of HR/ATIs/SBLCs in the present scenario. Your strategies in this regard?

Facing Interview? 2011/Team SBLC Patna/PKM Page 19

- HRMS – boon or bane? Strategy? - Your strategy to groom new entrants as future leaders? - Mass recruitment- requirement or burden? How to get most from the young

generation? - Emotional & Career counseling of the employees, especially of the young generation? - Integration of new entrants with the culture, ethics & environment of SBI? Your

practical strategy? - Work-life balance: your practical strategy. - Do you think training system is overburdened? If yes, why? How to improve the

situation? If no, justify with special works done by you.

E. Specially for TEGS / SMGS:-

- Operating expenses: position and your strategy to reduce them. What are latest

instructions in this regard? - Technology and Financial inclusion are the need of the hour. Your opinion and

reasons for the same. - “Worst is yet to come”: Your view considering present Indian economic condition. - With mass level retirement in banking sector and in SBI, what would be your

strategy for the future? - Going GREEN is the new mantra. Please discuss Bank’s strategy and your opinion in

this regard. - DGM’s should be posted on locale: Your views & reasons for your views. - New initiatives taken by bank for employees’ satisfaction. - How will you groom new entrants as future leaders? Specially in the light of mass

level recruitments and retirement. - Growth at the cost of bottom-line: your view. - Corporate Social Responsibility: Statutory requirement, Social commitment or

Voluntary effort? Bank’s strategy and your opinion. - “BANCOM” Summit 2011. - Small centers are performing better than the metros. Your opinion in SBI’s context. - BPR cells are the reason for growing instances of NPAs. Your opinion and reasons

behind the opinion. - Monetary Policy highlights: 2011-12, recent review.

- Roadmap for Access to Banking Facility in Every Village by 2012: Committee’s report

& your opinion. SBI’s financial inclusion plan?

- Economic Survey: 2010-11.

- Chairman’s Policy Guidelines: 2011-12.

- Deposit insurance: should it be linked with ‘Risk Profile’ of the Banks?

- BASEL III: are we prepared?

- Budget 2011-12: highlights.

Facing Interview? 2011/Team SBLC Patna/PKM Page 20

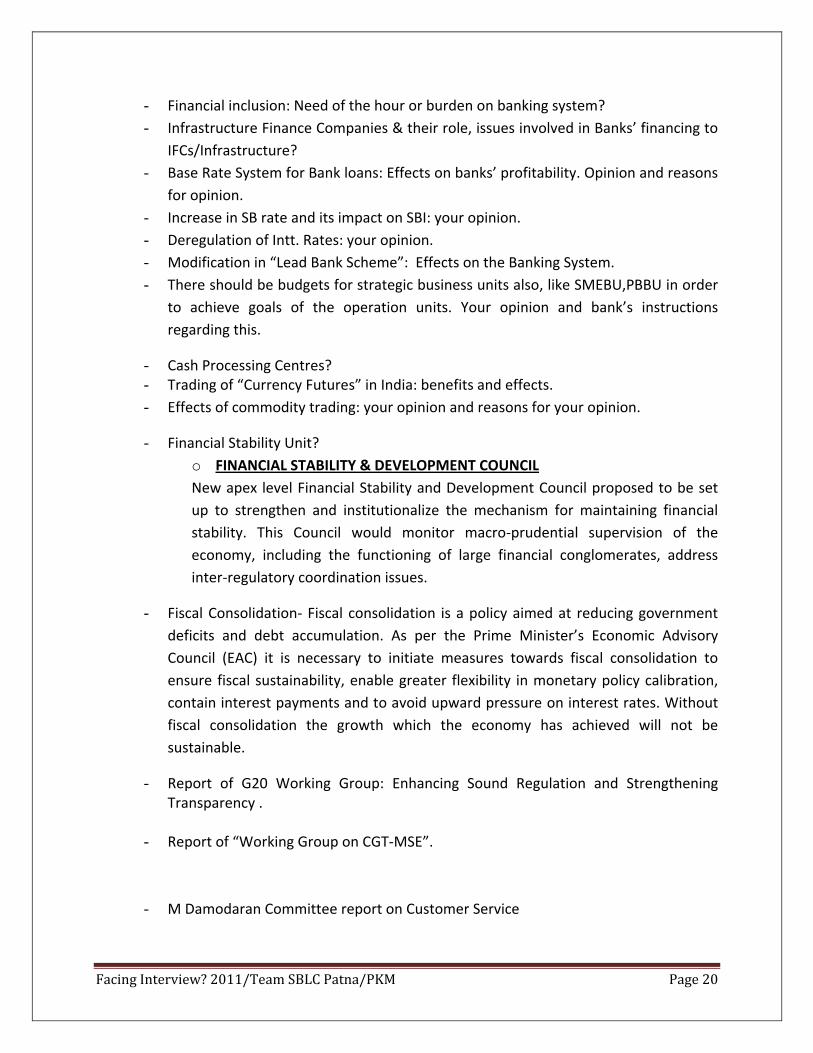

- Financial inclusion: Need of the hour or burden on banking system?

- Infrastructure Finance Companies & their role, issues involved in Banks’ financing to

IFCs/Infrastructure?

- Base Rate System for Bank loans: Effects on banks’ profitability. Opinion and reasons

for opinion.

- Increase in SB rate and its impact on SBI: your opinion.

- Deregulation of Intt. Rates: your opinion.

- Modification in “Lead Bank Scheme”: Effects on the Banking System.

- There should be budgets for strategic business units also, like SMEBU,PBBU in order

to achieve goals of the operation units. Your opinion and bank’s instructions

regarding this.

- Cash Processing Centres? - Trading of “Currency Futures” in India: benefits and effects.

- Effects of commodity trading: your opinion and reasons for your opinion.

- Financial Stability Unit?

o FINANCIAL STABILITY & DEVELOPMENT COUNCIL

New apex level Financial Stability and Development Council proposed to be set

up to strengthen and institutionalize the mechanism for maintaining financial

stability. This Council would monitor macro-prudential supervision of the

economy, including the functioning of large financial conglomerates, address

inter-regulatory coordination issues.

- Fiscal Consolidation- Fiscal consolidation is a policy aimed at reducing government

deficits and debt accumulation. As per the Prime Minister’s Economic Advisory

Council (EAC) it is necessary to initiate measures towards fiscal consolidation to

ensure fiscal sustainability, enable greater flexibility in monetary policy calibration,

contain interest payments and to avoid upward pressure on interest rates. Without

fiscal consolidation the growth which the economy has achieved will not be

sustainable.

- Report of G20 Working Group: Enhancing Sound Regulation and Strengthening Transparency .

- Report of “Working Group on CGT-MSE”.

- M Damodaran Committee report on Customer Service

Facing Interview? 2011/Team SBLC Patna/PKM Page 21

- A K Khandelwal committee (on HR issues) report and its likely impact on banking

industry.

- IT Vision :2011-17

- SBI Amendment Bill 2010- salient features.

- “UID” project- AADHAR? Swabhimaan?

- Should SBI charge royalty from its associates/subsidiaries?

- KYC guidelines: recent changes?

- IFRS: impact & benefit. Also CFSA?

- Need for “STU”? Impact of it.

- Revamp of training system in SBI: required?

- We have launched/started many initiatives but implementation thereof is not up to

the mark. Why? Your opinion.

- Concerns of the Bank for FY 2011-12?

- Your strategy to make SBI one among top 50 banks in the World?

- Training centers should be investment centres or profit centres?

- Outsourcing of training activities: required? Useful?

Facing Interview? 2011/Team SBLC Patna/PKM Page 22

- What is “CAFRAL”: (Centre for Advanced Financial Research & Learning)

- Effect of teaser rates on SBI. Should it be continued? Your opinion.

- It is difficult to keep high morale of the employees, especially in the light of

perceived inadequate salary package: your opinion.

- Technology – enabler or a big challenge, in the context of SBI.

- Is SBI a learning organisation? If yes, how? If not, reason and your strategy to make

it so.

- Merger of Associate Banks with SBI- need of the hour or burden? Banks view and

your opinion on this.

- Infrastructure lending – responsible for ALM mismatch. Your view on employees’

knowledge & skill up-gradation for infrastructure lending.

- Everybody is giving thrust on CASA. What level of CASA is sufficient for the bank?

- Are you satisfied with the way we are doing cross-selling? Or is it mis-selling?

- What is “Volker Rule”? (Separation of investment & commercial banking). Is it

suitable for India?

- STRIPS? –(Separately Traded Registered Interest and Payment Securities).

PROMOTION APPRAISAL FORM (PAF)

Promotion to : SMGS-V

BIO-DATA

Name in full: ___________ ________________ ____________

PF Index Number: __________

(Surname) (first name) (Middle name)

Date of Birth : ________ Age as on prescribed date : Yrs___ Mths ___

(dd/mm/yyyy) (eg:01-04-.... for PY ......)

SC/ST/OBC/Mino/Gen _____________ If Religious Minority specify: ______________

Academic Qualifications: _____________________ Position regarding CAIIB : ________

Other professional Qualifications: ___________________________

Entered the Bank as : _____________ on : ______________

Facing Interview? 2011/Team SBLC Patna/PKM Page 23

Entered Officer’s cadre as :_______________ on : ______________

Extension in Service; Date when last due : sanctioned upto

Statement of Assets & Liabilities submitted upto : 31st of March _______

Present Grade : _____________ Since ______________

No. of Chances :

(Beginning from promotion year .............) Certified having entered in service sheet.

Period Served in various Assignments

Rural : Years ______ Months _____ Semi-Urban : Years ______ Months _____

Line : Years ______ Months _____ Independent Line : Years ______ Months______

Exemption, if any permitted, from rural/semi-urban/line/operational assignments :

Period for which exemption permitted Assignment exempted

Foreign Assignment : Years ____ Months ___

Assignments held, from current to backwards (covering at least 5 years)

S.No Assignment/Designation Branch/Office From To date

1

2

3

Extra-ordinary leave on loss of pay

Period of leave Reasons for leave

- counting for service : ___________ __________________________

- not counting for service : ___________ __________________________

Sick Leave taken since last promotion :

Facing Interview? 2011/Team SBLC Patna/PKM Page 24

Year Number of Days (Full Pay) Nature of Illness (to be indicated only where

period of leave exceeds 14 days on one occasions

Present State of Health : NORMAL/__________________

Whether health wise able to proceed on transfer : Yes/No

Details of pending/contemplated Vigilance/ Disciplinary Case(s)/ Adverse features, if any

(Please give brief details of the case and the date when initiated)

Sealed Cover Procedure

5. Date since when the officers promotion is under sealed cover procedure :

6. Date of charge-sheet/suspension :

7. Nature of irregularities/ lapses attributed to the officer :

8. Present position of the enquiry/ disciplinary proceedings :

Any Special Achievements since previous promotion :

Appropriate Authority’s Special Remarks/recommendations, if any

Summary of Annual Appraisal Report

(Best 4 AARFs of the last 5 years but of the same grade, starting backwards from promotion

year)

Years Reporting Approval Reckoned as best 4(Y/N)

1

2

3

4

5

TOTAL OF THE REPORTS CONSIDERED (Max 400) ‘A’

Effective weight for promotion : [ (A * 40/400) ] (Max. 40) ‘B’

Facing Interview? 2011/Team SBLC Patna/PKM Page 25

Reasons for major variations, if any, in AARFS in score awarded by

Reporting/review/approving authorities :

It is certified that reviewed AARFs of the above years are properly drawn up and no

inconsistencies observed therein.

(Dy. General Manager & CDO/ Head of the Department for CC/establishments)

Date :_________________

Place__________________________

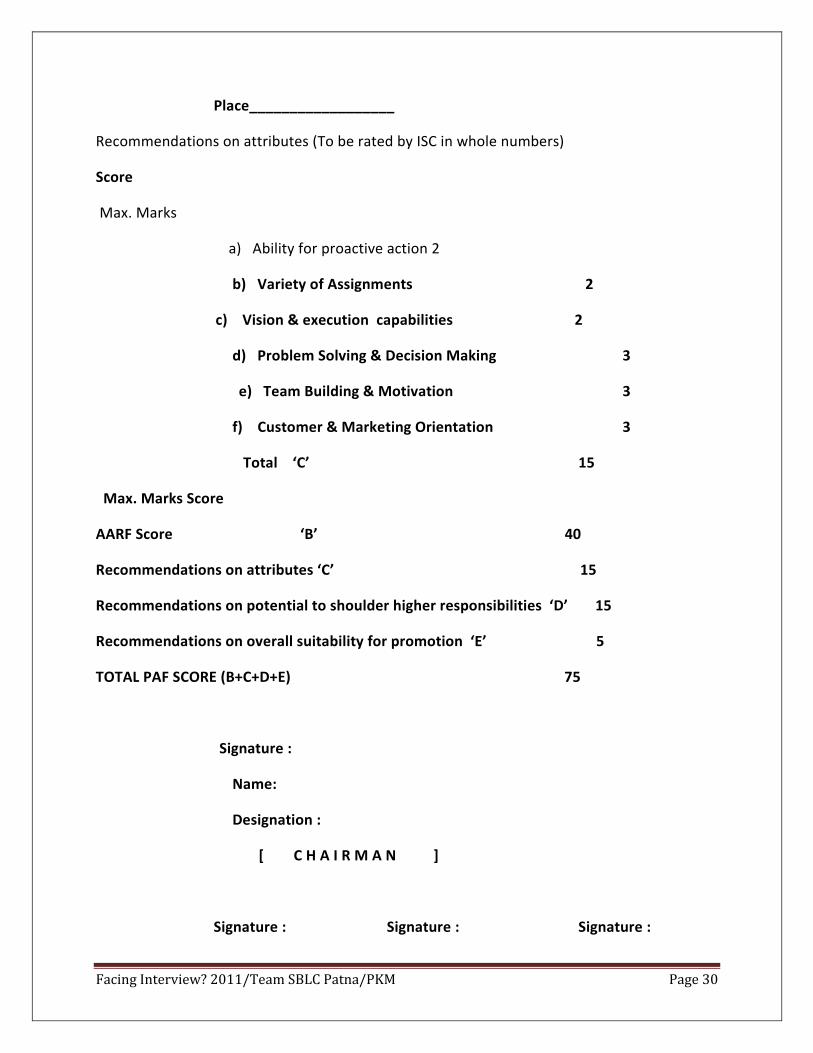

Recommendations on attributes (To be rated by ISC in whole numbers)

Score

Max. Marks

a) Ability for proactive action 2

b) Variety of Assignments 2

c) Vision & execution capabilities 2

d) Problem Solving & Decision Making 3

e) Team Building & Motivation 3

f) Customer & Marketing Orientation 3

Total ‘C’ 15

Max. Marks Score

AARF Score ‘B’ 40

Facing Interview? 2011/Team SBLC Patna/PKM Page 26

Recommendations on attributes ‘C’ 15

Recommendations on potential to shoulder higher responsibilities ‘D’ 15

Recommendations on overall suitability for promotion ‘E’ 5

TOTAL PAF SCORE (B+C+D+E) 75

Signature :

Name:

Designation :

[ C H A I R M A N ]

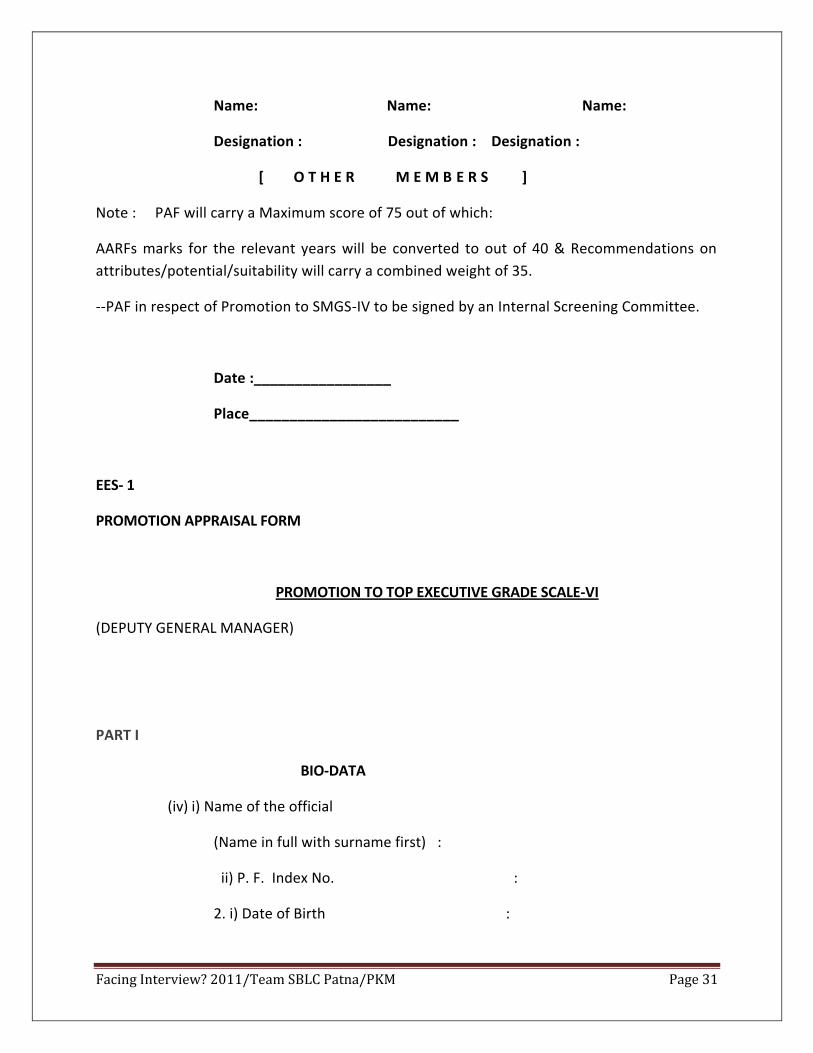

Signature : Signature : Signature :

Name: Name: Name:

Designation : Designation : Designation :

[ O T H E R M E M B E R S ]

Note : PAF will carry a Maximum score of 75 out of which:

AARFs marks for the relevant years will be converted to out of 40 & Recommendations on

attributes/potential/suitability will carry a combined weight of 35.

PAF in respect of Promotion to SMGS-V to be signed by an Internal Screening Committee.

Facing Interview? 2011/Team SBLC Patna/PKM Page 27

Date :_________________ Place__________________________

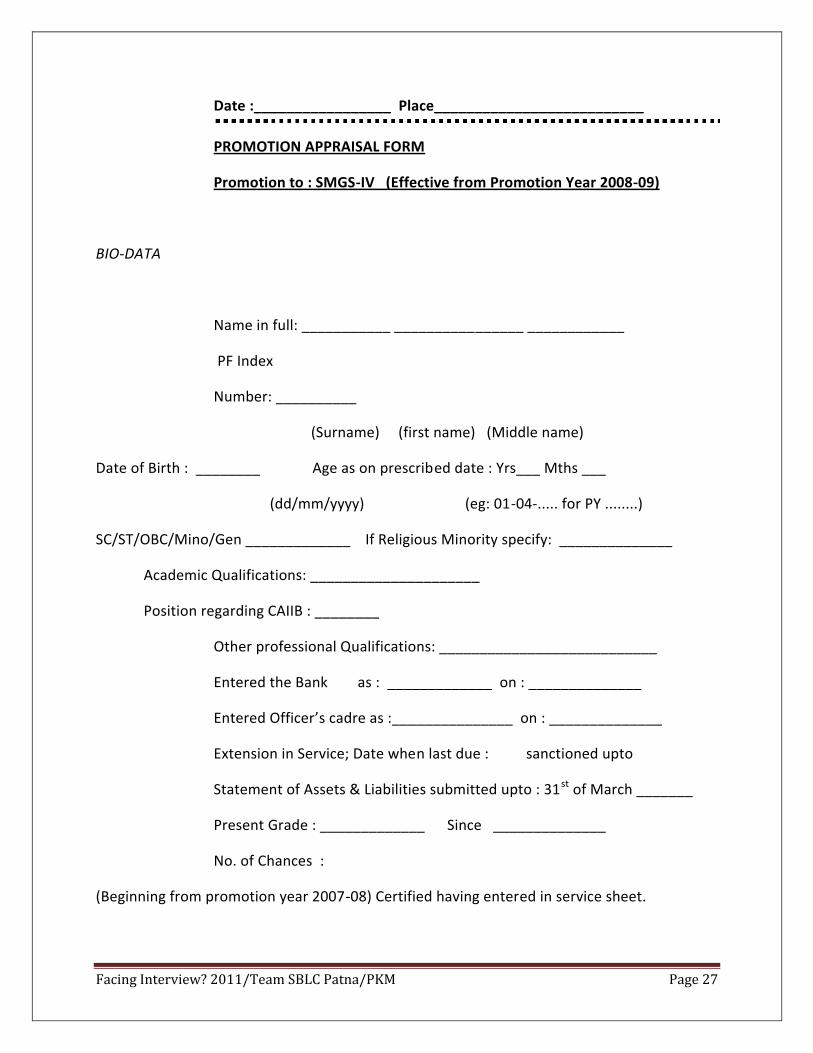

PROMOTION APPRAISAL FORM

Promotion to : SMGS-IV (Effective from Promotion Year 2008-09)

BIO-DATA

Name in full: ___________ ________________ ____________

PF Index

Number: __________

(Surname) (first name) (Middle name)

Date of Birth : ________ Age as on prescribed date : Yrs___ Mths ___

(dd/mm/yyyy) (eg: 01-04-..... for PY ........)

SC/ST/OBC/Mino/Gen _____________ If Religious Minority specify: ______________

Academic Qualifications: _____________________

Position regarding CAIIB : ________

Other professional Qualifications: ___________________________

Entered the Bank as : _____________ on : ______________

Entered Officer’s cadre as :_______________ on : ______________

Extension in Service; Date when last due : sanctioned upto

Statement of Assets & Liabilities submitted upto : 31st of March _______

Present Grade : _____________ Since ______________

No. of Chances :

(Beginning from promotion year 2007-08) Certified having entered in service sheet.

Facing Interview? 2011/Team SBLC Patna/PKM Page 28

Period Served in various Assignments

Rural : Years ______ Months _____ Semi-Urban : Years ______ Months _____

Line : Years ______ Months _____ Independent Line : Years ______ Months______

Exemption, if any permitted, from rural/semi-urban/line/operational assignments :

Period for which exemption permitted Assignment exempted

Foreign Assignment : Years ____ Months ___

Assignments held, from current to backwards(covering at least 5 years)

S.No Assignment/Designation Branch/Office From To

1 Current To date

2

3

4

5

Extra-ordinary leave on loss of pay

Period of leave Reasons for leave

- counting for service : ___________ __________________________

- not counting for service : ___________ __________________________

Sick Leave taken since last promotion :

Year Number of Days (Full Pay) Nature of Illness (to be indicated only where

period of leave exceeds 14 days on one occasions

Present State of Health : NORMAL/__________________

Whether health wise able to proceed on transfer : Yes/No

Details of pending/contemplated Vigilance/ Disciplinary Case(s)/ Adverse

features, if any

Facing Interview? 2011/Team SBLC Patna/PKM Page 29

(Please give brief details of the case and the date when initiated)

Sealed Cover Procedure

1. Date since when the officers promotion is under sealed cover

procedure :

2. Date of charge-sheet/suspension :

3. Nature of irregularities/ lapses attributed to the officer :

3. Present position of the enquiry/ disciplinary proceedings :

4. Any Special Achievements since previous promotion:

Appropriate Authority’s Special Remarks/recommendations, if any:

Summary of Annual Appraisal Report

(Best 3 AARFs of the last 4 years but of the same grade, starting backwards from promotion

year)

Years Reporting Approval Reckoned as best 3 (Y/N)

1

2

3

4

TOTAL OF THE REPORTS CONSIDERED (Max 300) ‘A’

Effective weight for promotion : * (A*40/300) + (Max. 40) ‘B’

Reasons for major variations, if any, in AARFS in score :

awarded by Reporting/review/approving authorities

It is certified that reviewed AARFs of the above years are properly drawn up and no

inconsistencies observed therein.

(Dy. General Manager & CDO/ Head of the Department for CC/establishments)

Date :_________________

Facing Interview? 2011/Team SBLC Patna/PKM Page 30

Place__________________

Recommendations on attributes (To be rated by ISC in whole numbers)

Score

Max. Marks

a) Ability for proactive action 2

b) Variety of Assignments 2

c) Vision & execution capabilities 2

d) Problem Solving & Decision Making 3

e) Team Building & Motivation 3

f) Customer & Marketing Orientation 3

Total ‘C’ 15

Max. Marks Score

AARF Score ‘B’ 40

Recommendations on attributes ‘C’ 15

Recommendations on potential to shoulder higher responsibilities ‘D’ 15

Recommendations on overall suitability for promotion ‘E’ 5

TOTAL PAF SCORE (B+C+D+E) 75

Signature :

Name:

Designation :

[ C H A I R M A N ]

Signature : Signature : Signature :

Facing Interview? 2011/Team SBLC Patna/PKM Page 31

Name: Name: Name:

Designation : Designation : Designation :

[ O T H E R M E M B E R S ]

Note : PAF will carry a Maximum score of 75 out of which:

AARFs marks for the relevant years will be converted to out of 40 & Recommendations on

attributes/potential/suitability will carry a combined weight of 35.

--PAF in respect of Promotion to SMGS-IV to be signed by an Internal Screening Committee.

Date :_________________

Place__________________________

EES- 1

PROMOTION APPRAISAL FORM

PROMOTION TO TOP EXECUTIVE GRADE SCALE-VI

(DEPUTY GENERAL MANAGER)

PART I

BIO-DATA

(iv) i) Name of the official

(Name in full with surname first) :

ii) P. F. Index No. :

2. i) Date of Birth :

Facing Interview? 2011/Team SBLC Patna/PKM Page 32

ii) Residual service as on the 1st April of the :

promotion year

3. Qualifications

i) Academic :

ii) Professional (including CAIIB) :

4. i) Joined the Bank as :

on :

ii) Entered Officers. Cadre as :

on :

iii) Date when last extension : was due and granted up to:

iv) Asset & Liability Statement submitted up to :

(v) i) Date of promotion to SMGS-V :

ii) Channel under which promoted to SMGS-V :

(Normal/Fast Track/Appeal)

iii) Total service in the present grade :

iv) Number of chances availed including for the

current promotion year

(vi) Period served in qualifying assignment(s):

Assignment Grade From

To

Facing Interview? 2011/Team SBLC Patna/PKM Page 33

7.i. (a) Sick leave availed by the official since last promotion:

Period Ailment

(vii) (b) Details of extra-ordinary leave sanctioned during entire service (counting

for service/not counting for service):

Period Reasons

ii) Comments upon status of health of the Officer33 with specific reference to his/her being

able to proceed on transfer upon promotion:

(viii) Assignments held:

(covering all assignments in the grade, minimum 4 assignments – current position backwards):

Sr. No. Position Branch/Office From To

9. Details of pending/contemplated vigilance/disciplinary cases, if any:

PART II

SUMMARY OF AARFs

Year Reported Reviewed Total (out of 100)

III/IIIA IV/IVA III/IIIA IV/IVA

2007-08

2006-07

2005-06

2004-05

TOTAL OF 4 YEARS (OUT OF 400)

Facing Interview? 2011/Team SBLC Patna/PKM Page 34

(TOTAL EQUIVALENT MARKS (OUT OF 40)

(USE CONVERSION FACTOR *0.10) (A)

General Comments (Section B Form IV/IV-A of AARF)

Year IV As on 31.03.2008

Year III As on 31.03.2007

Year II As on 31.3.2006

Year I As on 31.03.2005

A. ADVERSE REMARKS/FEATURES, IF ANY, IN AARFs:

i) Advised to the officer (details of correspondence to be provided):

ii) Not advised to the officer:

B. BRIEF REPORT ON EXCEPTIONAL PERFORMANCE/ACHIEVEMENT/RECOGNITION:

Certified that all Annual Appraisal Reports compiled for the relevant years have been duly

taken into consideration. All reports are drawn up properly and no inconsistencies observed

therein.

Deputy General Manager & Circle Development Officer/ Head of the Department*

Date: _________________ Place: _____________________

* For officers posted in Corporate Centre/its establishments

PART III

REPORT ON MANAGERIAL CAPABILITIES

(To be rated by the Internal Screening Committee, on a Five-point scale: 5-

Exemplary, 4-Excellent,

3-Good, 2-Above average, 1-AvNumerical marks

1.Creativity/Innovation and Achievement Orientation:

2. Analytical ability and decision making:

Facing Interview? 2011/Team SBLC Patna/PKM Page 35

3. Communication:

4. Leadership qualities and team building:

5.Inter-personalrelations:

6.Industrial Relations and Human Resources Management:

7. Corporate Image Building and Public Relations:

8. Environmental Awareness and Marketing Skills:

9. Emotional Strength:

10. Role in CMC/CirCC and other Structural Committees:

Total marks (Out of 50)

Total Equivalent Marks (Out of 15) (B)

(Use Conversion Factor *0.30)

PART IV

GENERAL COMMENTS ON POTENTIAL OF THE OFFICER TO SHOULDER HIGHER

RESPONSIBILITIES WITH SPECIFIC COMMENTS ON LEADERSHIP QUALITIES

(To be rated by the Internal Screening Committee, on a Five-point scale: 10-Excellent Potential,

8-very good potential, 6- Good potential 4-Capable, Zero-not capable)

COMMENTS:

MARKS FOR POTENTIAL & LEADERSHIP (OUT OF 10) I

PART V

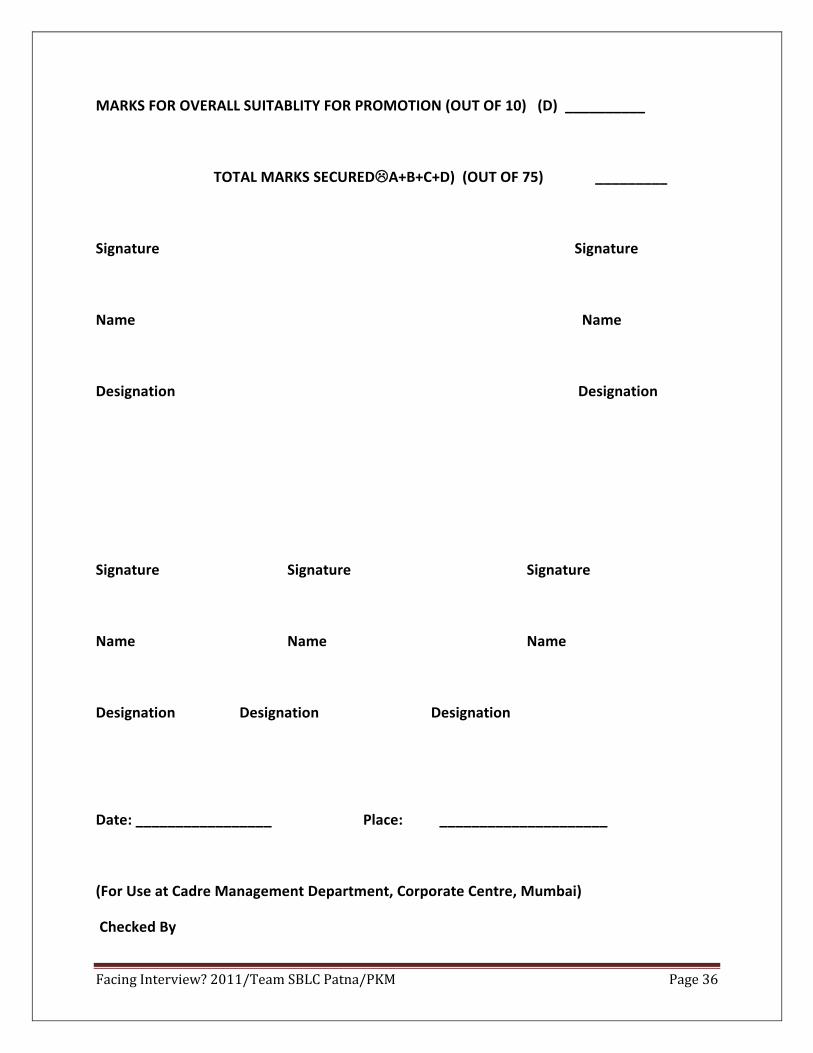

RECOMMENDATIONS ON THE OVERALL SUITABILITY FOR PROMOTION

(To be rated by the Internal Screening Committee, on a Five-point scale: 10-Eminently

Suitable, 8-Most Suitable, 6-Suitable, 4-Marginally Suitable, Zero-Unsuitable)

Facing Interview? 2011/Team SBLC Patna/PKM Page 36

MARKS FOR OVERALL SUITABLITY FOR PROMOTION (OUT OF 10) (D) __________

TOTAL MARKS SECUREDA+B+C+D) (OUT OF 75) _________

Signature Signature

Name Name

Designation Designation

Signature Signature Signature

Name Name Name

Designation Designation Designation

Date: _________________ Place: _____________________

(For Use at Cadre Management Department, Corporate Centre, Mumbai)

Checked By

Facing Interview? 2011/Team SBLC Patna/PKM Page 37

Date of Receipt

Entered in Computer by Verified by

GAPs, if any

5 Our Bank

SBI specific questions , Vision, Mission &

values, Awards & Recognition, List of Directors

on the Central Board of State Bank of India

Some of the highlights / recent developments in the recent past in SBI are listed below, and as bankers, we are expected to keep a close tab on these developments:

1. What is “Centre for Advanced Quantitative Finance” : it is being established for imparting training on quantitative finance for handling risks. Going forward, this will merge with SBI leadership initiatives.

2. “SBI Youth for India” initiative. 3. Organisational changes.

4. Annual Report – Various parameters. Analysis of the result.

5. Chairman’s Policy Guidelines.

6. Augmenting Capital.

7. SBI Heritage.

8. BPR – New initiatives taken. Usefulness of the initiatives.

Facing Interview? 2011/Team SBLC Patna/PKM Page 38

9. Technology Developments – New Products & initiatives/campaigns.

10. Human Resources, Job family, Performance linked incentive schemes, Huge Recruitment

drive, Employees participation, HRMS, Silver Jubilee Award, the Alertness Award and Chairman Club etc.

11. Productivity Excellence and leadership development programme.

12. New products introduced in Agriculture, PBBU and SMEBU segments.

13. Operations Risk Policy, Business Continuity Plan, Disaster Recovery Plan, Outsourcing Policies, Acceptable Usage Policies, Compensation Policy etc.

14. Project SME Gyanshala, Krishi-Gyan, NRI Nipun etc.

15. Productivity Excellence Programme, Udaan, Citizen SBI , Jagriti, Parivartan – I & II

16. What is “Banker to every Indian” & “Proud to be an Indian”? Justify this.

17. STU? Communicate………….Collaborate ……………..Change……..(but how?).

18. New business started by the Bank: Wealth Management, Financial Planning, SBI Pension

Fund Pvt. Ltd., SBI Custodial Services, General Insurance business etc.

19. Your Vision for SBI? Your strategy to achieve it.

Facing Interview? 2011/Team SBLC Patna/PKM Page 39

20. Bank’s New Vision , Mission& Value statement (Co-created by SBI employees in 2008)

VISION

My SBI.

My Customer first.

My SBI: First in customer satisfaction

MISSION

We will be prompt, polite and proactive with our customers.

We will speak the language of young India.

We will create products and services that help our customers achieve their goals.

We will go beyond the call of duty to make our customers feel valued.

We will be of service even in the remotest part of our country.

We will offer excellence in services to those abroad as much as we do to those in India.

We will imbibe state of the art technology to drive excellence.

VALUES

We will always be honest, transparent and ethical.

We will respect our customers and fellow associates.

We will be knowledge driven.

We will learn and we will share our learning.

We will never take the easy way out.

We will do everything we can to contribute to the community we work in.

We will nurture pride in India

21. HRD philosophy of SBI

Facing Interview? 2011/Team SBLC Patna/PKM Page 40

Our HRD philosophy aims at enabling every member of the staff to work as part

of an effective team and to activate his potential with the objective of achieving

the Banks’ goal.

22. Training philosophy of SBI

Training in SBI is a Pro-active, Planned & Continuous process, as an integral part

of the organizational development. It seeks to impart knowledge, improve skill

and re-orient attitudes for individual growth and organizational effectiveness.

23. Bank Day Pledge

24. Evolution of SBI

25. Awards & Recognition

26. Today we have lots of achievements (Rewards& Recognitions). According to you, which are the most important achievements of the Bank? Give reasons for your answer.

27. Is SBI a Learning organisation? If yes, how? If no, your strategy for making SBI a learning

organisation.

28. Reasons for marginal growth in net profit of the Bank in FY2009-10.

29. Concerns of the Bank for FY2010-11.

30. Your strategy to control overheads?

31. Latest Awards & Recognitions received by State Bank of India? Which one is most important in your view? And why that is most important?

Facing Interview? 2011/Team SBLC Patna/PKM Page 41

List of Directors on the Central Board of State Bank of India

(As on 19th April 2011)

Sr.

No.

Name Designation Under Section of

SBI Act 1955

1 Shri Pratip Chaudhuri Chairman 19 (a)

2 Shri R. Sridharan Managing Director 19 (b)

3 Shri Hemant Contractor Managing Director 19(b)

4 Shri A. Krishna Kumar Managing Director 19(b)

5 Shri Diwakar Gupta Managing Director (CFO) 19(b)

6 Dr. Ashok Jhunjhunwala Director 19 I

7 Shri Dileep C. Choksi Director 19 I

8 Shri S. Venkatachalam Director 19 I

9 Shri D. Sundaram Director 19 I

10 Shri G. D. Nadaf Officer Employee Director 19 (cb)

11 Dr. Rajiv Kumar Director 19 (d)

12 Shri Shashi Kant Sharma Director 19 (e)

13 Smt. Shyamala Gopinath Director 19 (f)

6 General awareness

a. General questions relating to Economy

& Financial System

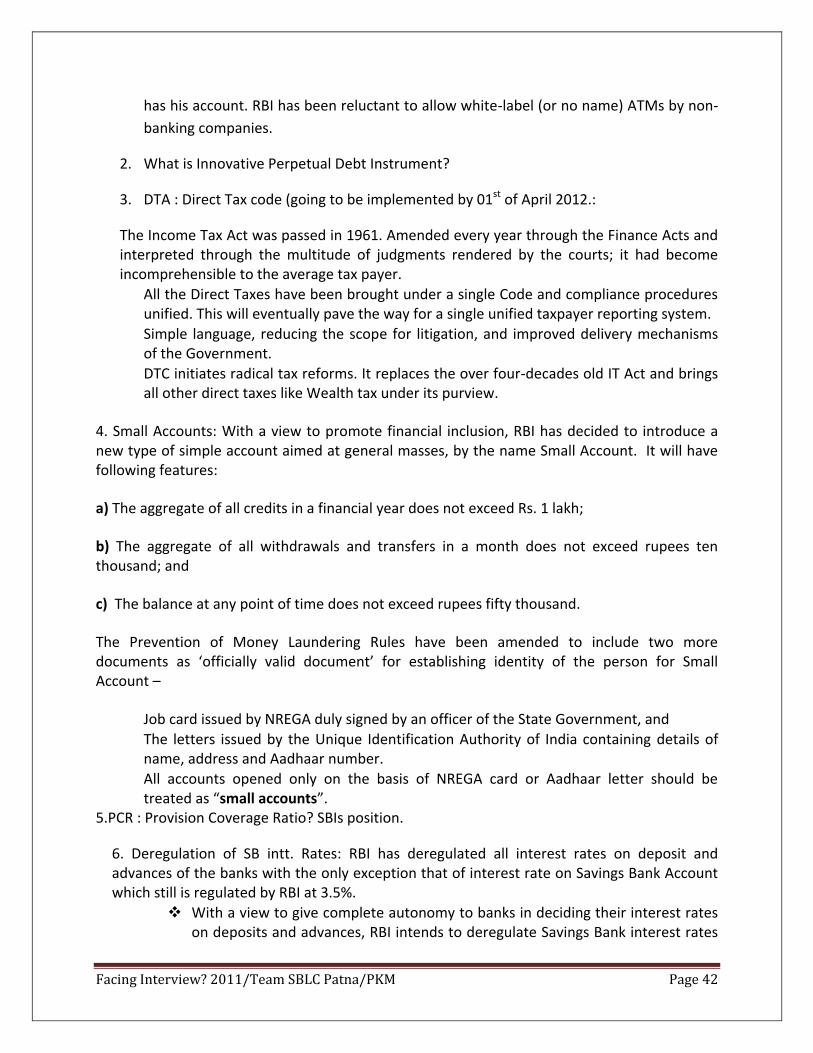

1. What is “White Label ATM”? : Customers from any bank can deposit or withdraw money

from ‘white-label ATMs’. Their banks then pay for the service. Also, such ATMs are

invariably owned by a third-party, not a bank. At present, under RBI guidelines, ATMs

can only belong to a particular bank. Transactions of customers from other banks are

settled by paying Rs 14 as the charge per transaction by the bank in which the customer

Facing Interview? 2011/Team SBLC Patna/PKM Page 42

has his account. RBI has been reluctant to allow white-label (or no name) ATMs by non-

banking companies.

2. What is Innovative Perpetual Debt Instrument?

3. DTA : Direct Tax code (going to be implemented by 01st of April 2012.:

The Income Tax Act was passed in 1961. Amended every year through the Finance Acts and interpreted through the multitude of judgments rendered by the courts; it had become incomprehensible to the average tax payer.

All the Direct Taxes have been brought under a single Code and compliance procedures unified. This will eventually pave the way for a single unified taxpayer reporting system.

Simple language, reducing the scope for litigation, and improved delivery mechanisms of the Government.

DTC initiates radical tax reforms. It replaces the over four-decades old IT Act and brings all other direct taxes like Wealth tax under its purview.

4. Small Accounts: With a view to promote financial inclusion, RBI has decided to introduce a new type of simple account aimed at general masses, by the name Small Account. It will have following features:

a) The aggregate of all credits in a financial year does not exceed Rs. 1 lakh;

b) The aggregate of all withdrawals and transfers in a month does not exceed rupees ten thousand; and

c) The balance at any point of time does not exceed rupees fifty thousand.

The Prevention of Money Laundering Rules have been amended to include two more documents as ‘officially valid document’ for establishing identity of the person for Small Account –

Job card issued by NREGA duly signed by an officer of the State Government, and

The letters issued by the Unique Identification Authority of India containing details of name, address and Aadhaar number.

All accounts opened only on the basis of NREGA card or Aadhaar letter should be treated as “small accounts”.

5.PCR : Provision Coverage Ratio? SBIs position.

6. Deregulation of SB intt. Rates: RBI has deregulated all interest rates on deposit and advances of the banks with the only exception that of interest rate on Savings Bank Account which still is regulated by RBI at 3.5%.

With a view to give complete autonomy to banks in deciding their interest rates on deposits and advances, RBI intends to deregulate Savings Bank interest rates

Facing Interview? 2011/Team SBLC Patna/PKM Page 43

also. The RBI has released a discussion paper on the de-regulation of the rate of interest on saving deposit.

This de-regulation will give rise to more healthy competition amongst banks and this will lead to improvement in efficiency.

As savings deposits are comparatively stable the banks may link them to medium term deposit rates and offer higher rates, thus benefiting the customer.

In the short run, banks may offer comparatively higher rates, however, in the long run they are likely to settle around 5% or so; in tune with 15-45 days term deposit rates.

7. BASEL III Guidelines: The Basel standards are developed by the Basel Committee on Banking Supervision (BCBS), a group within the Bank for International Settlements (BIS) in Basel, Switzerland to ensure safety, soundness and solvency of the banking system. Basel – III is a set of standards and practices developed for internationally active banks to ensure that they maintain adequate capital to sustain themselves during periods of economic crisis. The key objective of Basel III is to tighten the already existing international rules on financial regulation (“Basel I” and “Basel II”), which failed to provide sufficient protection against the financial turmoil. Basel III will require banks to build up extra capital reserves in good times to be used in troubled markets and lessen the need for government bailouts.

Problems with Basel II

a) Capital requirements were too low;

b) There was too much reliance on credit ratings;

c) Banks could use internal models to measure risk;

d) Banks could get around the rules by setting up off-balance-sheet entities;

e) It lacked any kind of liquidity requirements.

Basel- III: Basel III establishes more stringent capital requirements, tripling the amount of

capital that the banks must keep on hand to absorb losses during financial crisis. It requires

banks to maintain higher common equity than before, including a capital conservation buffer of

2.5% of their assets.

8. CERSAI: Pursuant to the announcement made by the Finance Minister in the budget speech for 2011-12, Government of India, Ministry of Finance notified the establishment of the Central Registry. The objective of setting up of Central Registry is to prevent frauds in loan cases involving multiple lending from different banks on the same immovable property. This Registry has become operational on March 31, 2011. The Central Registry of CERSAI, a Government Company licensed under Section 25 of the Companies Act 1956 has been incorporated for the purpose of operating and maintaining the Central Registry under the provisions of the Securitisation and Reconstruction of Financial Assets & Enforcement of Security Interest Act, 2002 (SARFAESI Act).

Facing Interview? 2011/Team SBLC Patna/PKM Page 44

Some of the highlights / recent developments during the last one year are listed below, and as bankers, we are expected to keep a close tab on these and related developments in the economy. So candidates can expect questions in these areas:

1. GST: Goods and Services Tax (GST) is a comprehensive tax levy on manufacture, sale and consumption of goods and services at a national level. It is collected on value-added goods and services at each stage of sale or purchase in the supply chain, by implementing a tax management software at all levels. The system allows the set-off of GST paid on the procurement of goods and services against the GST which is payable on the supply of goods or services. However, the end consumer bears this tax as he is the last person in the supply chain. Implementation of GST will lead to the abolition of other taxes such as octroi, Central Sales Tax, State-level sales tax, entry tax, stamp duty, telecom license fee, turnover tax, tax on consumption or sale of electricity, taxes on transportation of goods and services etc., thereby avoiding multiple layers of taxation that currently exist in India. However, crude petroleum, diesel, petrol, aviation turbine fuel, natural gas and alcohol for human consumption have been kept out of the GST ambit.

2. India’s success story in present financial crisis position of the world- Sustained growth rate and tasks ahead.

3. GOI , RBI & Banks initiatives to overcome crisis.

4. 11th Five Year Plan (2007-2012). The home loan and may have been

5. Economic & Financial Reforms, Technology, Market and Supervision related reforms.

6. Special Economic Zones, SPZs

7. Comparison between China and India. BASIC Countries?

8. BPLR/Base Rate and its relation to Intt. Rate, Inflation & Economy.

Facing Interview? 2011/Team SBLC Patna/PKM Page 45

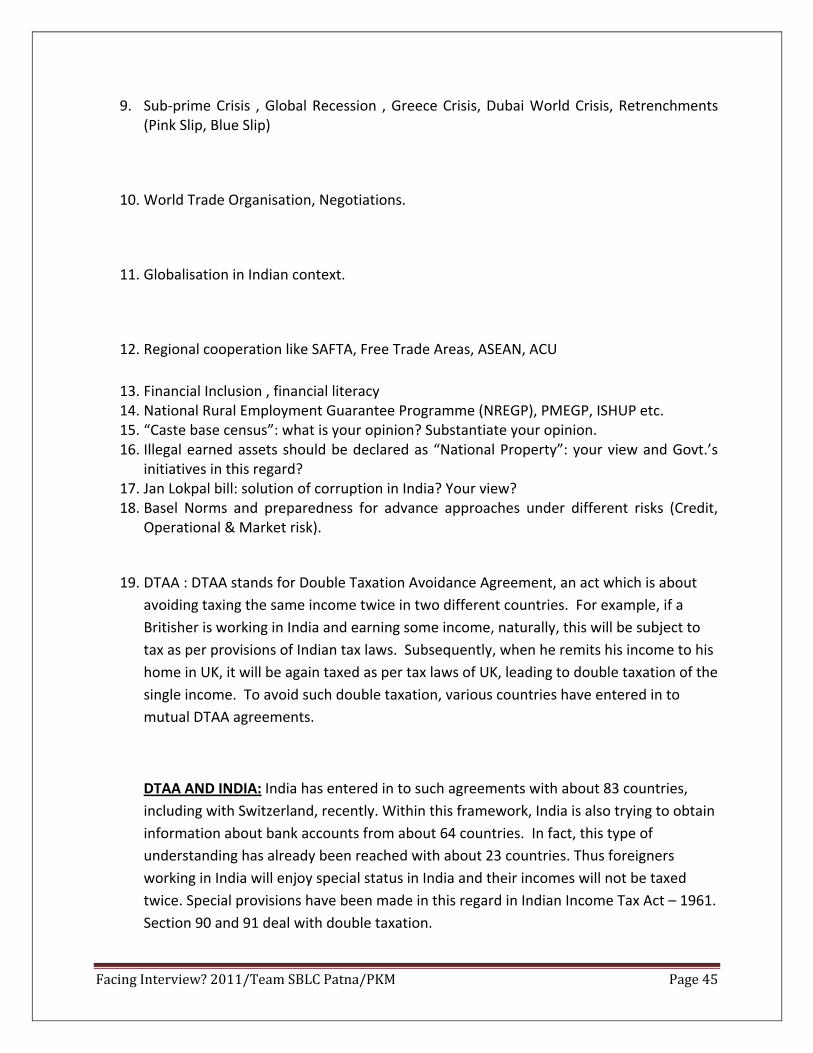

9. Sub-prime Crisis , Global Recession , Greece Crisis, Dubai World Crisis, Retrenchments (Pink Slip, Blue Slip)

10. World Trade Organisation, Negotiations.

11. Globalisation in Indian context.

12. Regional cooperation like SAFTA, Free Trade Areas, ASEAN, ACU

13. Financial Inclusion , financial literacy 14. National Rural Employment Guarantee Programme (NREGP), PMEGP, ISHUP etc. 15. “Caste base census”: what is your opinion? Substantiate your opinion. 16. Illegal earned assets should be declared as “National Property”: your view and Govt.’s

initiatives in this regard? 17. Jan Lokpal bill: solution of corruption in India? Your view? 18. Basel Norms and preparedness for advance approaches under different risks (Credit,

Operational & Market risk).

19. DTAA : DTAA stands for Double Taxation Avoidance Agreement, an act which is about

avoiding taxing the same income twice in two different countries. For example, if a

Britisher is working in India and earning some income, naturally, this will be subject to

tax as per provisions of Indian tax laws. Subsequently, when he remits his income to his

home in UK, it will be again taxed as per tax laws of UK, leading to double taxation of the

single income. To avoid such double taxation, various countries have entered in to

mutual DTAA agreements.

DTAA AND INDIA: India has entered in to such agreements with about 83 countries,

including with Switzerland, recently. Within this framework, India is also trying to obtain

information about bank accounts from about 64 countries. In fact, this type of

understanding has already been reached with about 23 countries. Thus foreigners

working in India will enjoy special status in India and their incomes will not be taxed

twice. Special provisions have been made in this regard in Indian Income Tax Act – 1961.

Section 90 and 91 deal with double taxation.

Facing Interview? 2011/Team SBLC Patna/PKM Page 46

Other questions that may be expected: i) What is the growth rate India has achieved in recent years? a) Overall b) Agriculture Sector c) Manufacturing Sector d) Services Sector e) Technology ii) What is the targeted growth rate during the next 5 year Plan? Last year revised estimate & this year projections? Do you think this is achievable in present scenario? iii) India’s performance in World Economy? iv) What are the roadblocks for achieving high-targeted growth rate? v) What do you think are the reasons behind India’s economic stability? vi) How does our growth story compared with that of China & other BRIC/BASIC countries? vii) What are our strong points and weak point’s vis-à-vis China? viii) Foreign Trade Policy viii) What is Gross Domestic Product?

- What is Gross National Product? - What is the Difference between Gross Domestic Product and Gross National Product?

ix) What is Per Capita Income Growth Rate? Per Capita Income? x) Literacy Rate? xi) Poverty Line? xii) India’s position in World in “PPP”, Country rating? xiii) How are Inflation and Interest Rate Related? xiv) What is Revenue Deficit? xv) What is Fiscal Deficit? xvi) What are Ways and Means Advances? What is Market Stabilization Scheme?

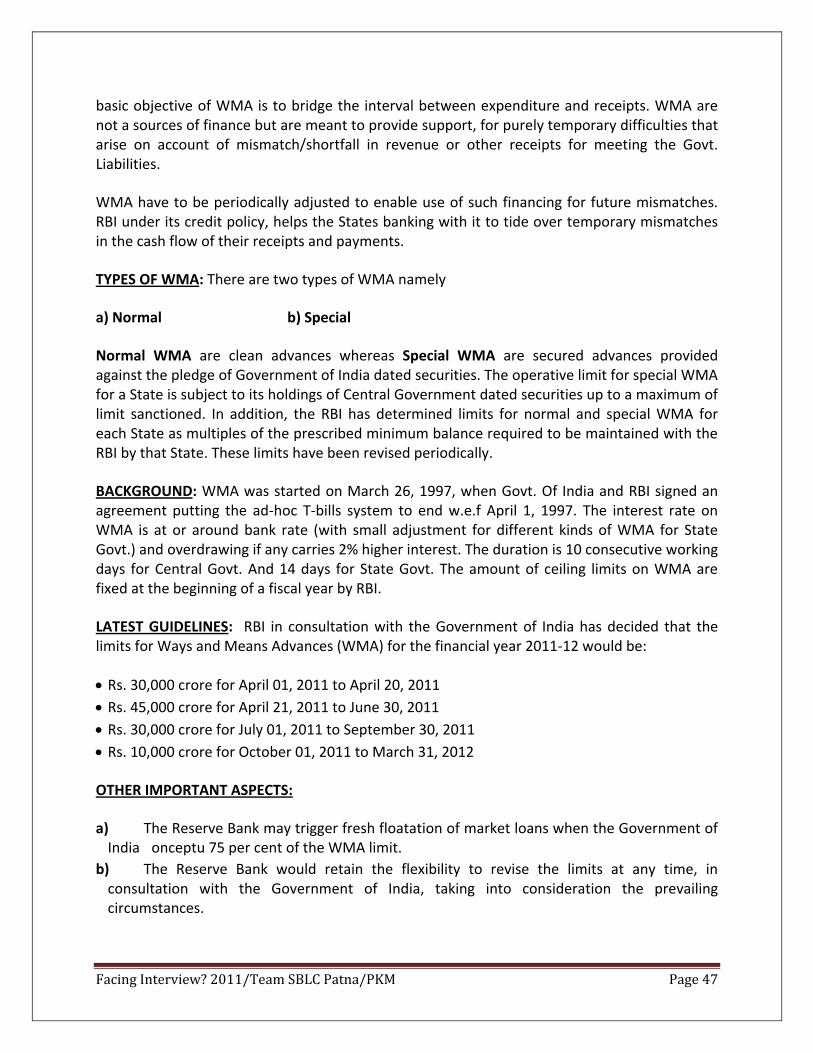

Ways and Means Advances (WMA) are temporary advances (overdrafts) extended by RBI to the Govt. Section 17(5) of RBI Act allows RBI to make WMA both to the Central and State Govt. The

Facing Interview? 2011/Team SBLC Patna/PKM Page 47

basic objective of WMA is to bridge the interval between expenditure and receipts. WMA are not a sources of finance but are meant to provide support, for purely temporary difficulties that arise on account of mismatch/shortfall in revenue or other receipts for meeting the Govt. Liabilities.

WMA have to be periodically adjusted to enable use of such financing for future mismatches. RBI under its credit policy, helps the States banking with it to tide over temporary mismatches in the cash flow of their receipts and payments.

TYPES OF WMA: There are two types of WMA namely

a) Normal b) Special

Normal WMA are clean advances whereas Special WMA are secured advances provided against the pledge of Government of India dated securities. The operative limit for special WMA for a State is subject to its holdings of Central Government dated securities up to a maximum of limit sanctioned. In addition, the RBI has determined limits for normal and special WMA for each State as multiples of the prescribed minimum balance required to be maintained with the RBI by that State. These limits have been revised periodically.

BACKGROUND: WMA was started on March 26, 1997, when Govt. Of India and RBI signed an agreement putting the ad-hoc T-bills system to end w.e.f April 1, 1997. The interest rate on WMA is at or around bank rate (with small adjustment for different kinds of WMA for State Govt.) and overdrawing if any carries 2% higher interest. The duration is 10 consecutive working days for Central Govt. And 14 days for State Govt. The amount of ceiling limits on WMA are fixed at the beginning of a fiscal year by RBI.

LATEST GUIDELINES: RBI in consultation with the Government of India has decided that the limits for Ways and Means Advances (WMA) for the financial year 2011-12 would be:

Rs. 30,000 crore for April 01, 2011 to April 20, 2011

Rs. 45,000 crore for April 21, 2011 to June 30, 2011

Rs. 30,000 crore for July 01, 2011 to September 30, 2011

Rs. 10,000 crore for October 01, 2011 to March 31, 2012

OTHER IMPORTANT ASPECTS:

a) The Reserve Bank may trigger fresh floatation of market loans when the Government of India onceptu 75 per cent of the WMA limit.

b) The Reserve Bank would retain the flexibility to revise the limits at any time, in consultation with the Government of India, taking into consideration the prevailing circumstances.

Facing Interview? 2011/Team SBLC Patna/PKM Page 48

c) The interest rate on WMA/overdraft will be: i) Ways and Means Advances: Repo Rate; ii) Overdraft: Two percent above the Repo Rate

d) The minimum balance required to be maintained by the Government of India with the Reserve Bank of India will not be less than Rs.100 crore on Fridays, on the date of closure of Government of India’s financial year and on June 30, i.e., closure of the annual accounts of the RBI and not less than Rs.10 crore on other days.

e) As per the provisions of the agreement dated March 26, 1997 between the Government of India and the RBI, overdrafts beyond ten consecutive working days will not be allowed.

MONITORING OF WMA: The position of WMA actually onceptu and overdrafts of various States is closely monitored in the Internal Debt Management Cell (IDM Cell), RBI, on a daily basis on receipt of the position from Central Accounts Section (CAS). When a State avails of WMA in excess of 75 per cent of the aggregate limit (aggregate = normal plus operative limit for special WMA), the State is cautioned to take remedial measures to avoid emergence of overdraft in its account. Whenever a State, after availing of normal and special WMA, emerges in overdraft, the IDM Cell conveys the position of its overdraft to the concerned State on a daily basis, with a request to clear it within a period not exceeding ten consecutive working days. If the account of a State continues to be overdrawn on the eleventh continuous working day, the RBI suspends payments on behalf of the State until the overdraft is cleared.

SURPLUS INVESTMENTS: The RBI acts as the sole agent for investment of the State’s surplus funds. Surplus cash balance of a State beyond a level indicated by it is automatically invested in 14-day intermediate Treasury bills. The States are also free to participate in 14-day and 91-day Treasury bills auctions as non-competitive bidders for investment of their durable surplus.

xvii) What is the Concept of SEZ? From which country have we borrowed this model? xviii) What is Infrastructure Finance Company (IFC)? xix) What are the norms for funding IFCs? xx) What is LPG in the context of Economy? Ans: LPG stands for Liberalisation, Privatisation and Globalisation

- What is Liberalisation?

- What is Privatisation?

- What is Globalisation?

Facing Interview? 2011/Team SBLC Patna/PKM Page 49

xxi) What is Glocalisation? Indicative Answer: Thinking Globally and Acting Locally. xxii) What is BSE index, NSE, MCDEX, NASDAQ? How many shares does BSE index constitute of? What is Bankex ? xxiii) What is Demutualisation? Indicative Answer: It is the process of changing a mutual or cooperative association (say a Mutual Fund or Stock Exchange) into a Public Company by converting the interest of members into shareholding. Such shares can be traded like the shares of the company. Note: Bombay Stock Exchange demutualised itself for today’s structure. xxiv) What are the reasons behind the current share prices movement in the Market? xxv) What is Currency Future/ Interest rate future? xxvi) What is a Green Shoe Option? xxvii) What is a Red Herring Prospectus? xxviii) What is a Green Field Project? What is a Brown Field Project? xxix) What is Exchange Traded Fund? xxx) What is Book Building? xxxi) What is IRR ? xxxii) What is Price Earning Ratio? xxxiii) What is Yield? xxxiv) What is Yield to Maturity? xxxv) New Project of TATAs & impact on Indian Car market. xxxvi) What is leveraged buyout? (This is how Tata’s acquisition of Corus was structured). It is a transaction where the cash flow or assets (or both) of the company that is being acquired is leveraged, i.e., money is borrowed against these – to take over the firm. LBOs can be done if the acquirer takes a major stake in the company, meaning over 51%. Consider a $500 million buyout. In a common LBO structure, the acquirer floats a Special Purpose Vehicle (SPV) overseas and chips in with, say, $150 million as equity and borrows the rest. The company being taken over is a subsidiary of the SPV. Later, the SPV or the holding

Facing Interview? 2011/Team SBLC Patna/PKM Page 50