FAC2602 - gimmenotes.co.zagimmenotes.co.za/.../2017/01/FAC2602-Study-guide.pdf · ... Consolidation...

284

MO001/3/2017 Selected Accounting Standards and Simple Group Structures FAC2602 Semesters 1 & 2 Department of Financial Accounting IMPORTANT INFORMATION: This document contains the tutorial matter of your learning units.

Transcript of FAC2602 - gimmenotes.co.zagimmenotes.co.za/.../2017/01/FAC2602-Study-guide.pdf · ... Consolidation...

MO001/3/2017

Selected Accounting Standards and Simple Group Structures

FAC2602

Semesters 1 & 2

Department of Financial Accounting

IMPORTANT INFORMATION:

This document contains the tutorial matter of your learning units.

2

CONTENTS

Page

1. Introduction 3

2. Lecturers and contact details 3

3. Learning Unit 1 4

4. Learning Unit 2 13

5. Learning Unit 3 31

6. Learning Unit 4 47

7. Learning Unit 5 73

8. Learning Unit 6 91

9. Learning Unit 7 107

10. Learning Unit 8 162

11. Learning Unit 9 202

12. Topic B: Learning Unit 1 258

3

INTRODUCTION

Dear Student,

Attached please find the following learning units:

Learning unit 1 – Provisions in respect of companies in a group context

Learning unit 2 – Consolidation of a wholly-owned subsidiary at date of acquisition

Learning unit 3 – Consolidation of a partly-owned subsidiary at date of acquisition

Learning unit 4 – Consolidation of a wholly-owned subsidiary after date of acquisition

Learning unit 5 – Consolidation of a partly-owned subsidiary after date of acquisition

Learning unit 6 – Acquisition of an interest in a subsidiary during the year

Learning unit 7 – Elimination of intragroup transactions

Learning unit 8 – Treatment of dividends during consolidation

Learning unit 9 – Treatment of preference shares during consolidation

Topic B: Learning unit 1 – Statements of cash flows

LECTURERS AND CONTACT DETAILS

Your FAC2602 lecturers and their offices are as follows: Ms C Wolfaardt - AJH van der Walt Building 2-43 Ms S Gani - AJH van der Walt Building 2-45 Ms R Grobler - AJH van der Walt Building 2-67 Ms MM Pholo - AJH van der Walt Building 2-44 Our contact details are as follows:

Telephone: 012 429 4234 Fax: 012 429 3335 E-mail: [email protected]

4

FAC2602

Introduction to group annual

financial statements

PROVISIONS IN RESPECT

OF COMPANIES IN A

GROUP CONTEXT

LEARNING UNIT 1

FAC2602 / Learning unit 1

5

LEARNING OUTCOME

Students should be able to identify and define a business combination, a parent and subsidiary

company as well as simple groups in relation to International Financial Reporting Standards (IFRS).

OVERVIEW

The learning unit is divided into the following:

1.1 INTRODUCTION ............................................................................................................ 6

1.2 BUSINESS COMBINATION, PARENT AND SUBSIDIARIES ....................................... 6

1.3 ACCOUNTING FOR GROUPS .................................................................................... 10

1.4 GENERAL PRINCIPLES .............................................................................................. 11

1.5 EXERCISES ................................................................................................................. 11

SELF-ASSESSMENT ............................................................................................................. 12

KEY CONCEPTS

Business combination

Acquire

Entity

Parent

Subsidiary

Sub-subsidiary

Control

Share capital

Simple group

Complex group

FAC2602 / Learning unit 1

6

ASSESSMENT CRITERIA

After studying this learning unit, you should be able to

define a business combination

define a parent

define a subsidiary

explain the difference between simple and complex groups

describe the provisions regarding accounting and disclosure as they relate to

group financial statements of companies

1.1 INTRODUCTION

The first learning unit, which deals with group financial statements, is mainly background

knowledge. As you progress through the course, you will come to understand the purpose

that this background knowledge serves. We refer back to certain concepts and principles

discussed here in subsequent learning units, so they should become clearer to you later on in

the module.

1.2 BUSINESS COMBINATION, PARENT AND SUBSIDIARIES

Over the years, the tendency in the business world has been to form bigger and bigger

enterprises. Sole proprietors combined to form partnerships, which in turn amalgamated to

form yet bigger partnerships. However, these bigger partnerships posed one problem: all the

partners were not equally involved. Some partners merely contributed capital, whereas others

were more actively involved in managing the enterprise on a daily basis. The result was the

formation of companies to limit the liability of the inactive partners.

Companies also began to combine with other companies to form larger companies and groups

of companies.

IFRS 3 Business combinations regulates business combinations. We can define a business

combination as a transaction or other event in which an acquirer obtains control of one or more

businesses.

FAC2602 / Learning unit 1

7

EXAMPLE

The following is an example of such a group:

P Ltd

75% of the control by

means of 75% of the

share capital

S Ltd

a) P Ltd is the parent. (P Ltd holds more than half of the issued share capital and it is

assumed also more than half the voting rights in S Ltd.)

b) S Ltd is the subsidiary.

Where a parent is linked with a subsidiary to form a larger economic unit, it is customary to

refer to the entity as a group.

IFRS 10 Consolidated Financial Statements (issued May 2011) defines a group as a parent

and all its subsidiaries. In such a group, the management of the different independent parent

and subsidiary entities would co-ordinate their efforts on a central and unified basis to serve

the interests of the group as a whole. It is possible for management to operate on a unified

basis because of the control that the parent exercises over its subsidiaries.

IFRS 10 determines that an investor (in this case the parent) controls an investee (the

subsidiary) when the investor is exposed or has rights to variable returns from its involvement

with the investee and has the ability to affect those returns through its power over the

investee.

The above is an example of a simple group. Although you will only have to deal with accounting

and disclosure for simple groups in this course, we would like to introduce you to the concept of

complex groups so that it will not be an entirely new or foreign concept to you in future.

FAC2602 / Learning unit 1

8

EXAMPLE

The following are two examples of complex groups:

1. P Ltd

80% of the control through 60% of the control through

80% of the share capital 60% of the share capital

S1 Ltd S2 Ltd

a) P Ltd is the parent.

b) S1 Ltd and S2 Ltd are the subsidiaries.

c) P Ltd, S1 Ltd and S2 Ltd collectively form a complex group (horizontally).

2.

P Ltd

75% of the control through

75% of the share capital

S1 Ltd

80% of the control through

80% of the share capital

S2 Ltd

a) P Ltd is the parent.

b) S1 Ltd is the subsidiary, and S2 Ltd is the sub-subsidiary.

c) P Ltd, S1 Ltd and S2 Ltd collectively form a complex group (vertically).

It should be clear to you from the above that simple groups have only one subsidiary where

complex groups have more than one subsidiary.

The following definitions are important in the light of the above explanation:

FAC2602 / Learning unit 1

9

Business combination

A business combination is defined as a transaction or another event in which an acquirer

obtains control of one or more businesses.

Parent

A parent is an entity that controls one or more other entities (subsidiaries).

Subsidiary

A subsidiary is an entity that is controlled by another entity (the parent).

Sub-subsidiary

A sub-subsidiary is a subsidiary of another subsidiary.

Control

An investor (parent) controls an investee (subsidiary) when the investor (parent) is exposed or has rights to variable returns from its involvement with the investee (subsidiary) and has the ability to affect those returns through its power over the investee (subsidiary).

An investor (parent) controls an investee (subsidiary) only if all of the following is true for the investor:

It has power over the investee (subsidiary).

It has exposure or rights to variable returns from its involvement with the investee.

It has the ability to use its power over the investee (subsidiary) to affect the amount of the investor's returns.

Please note that in FAC2602 we will assume that an investor obtains control by possessing 50% or more of the shares and voting rights of a company.

The issued share capital of a company may consist of both ordinary and preference shares.

Shares do not have a nominal or par value in terms of the Companies Act 71 of 2008. All

shares of the same class have the same rights, and each share has one voting right, except

when the company's memorandum of incorporation provides otherwise (e.g. the voting rights

of preference shares may be excluded).

It should now be clear to you that a parent can obtain control over a subsidiary when the

parent holds the majority of the shares in the subsidiary.

In the examples we use, the percentages of shareholding and voting rights usually

correspond, since each share normally carries one vote. However, it is important to know that

this is not always the case in practice and that the percentage of voting rights would

determine the percentage of equity if there are no other factors influencing control.

In learning unit 3, we will explain the calculation of the percentage interest in more detail.

FAC2602 / Learning unit 1

10

1.3 ACCOUNTING FOR GROUPS

The essence of consolidations is that the parent is able to control the policy and management

of the subsidiary. Therefore, the group should be seen as an economic unit.

Although the parent shows investments in its subsidiaries on its statement of financial position,

it is highly probable that the value of the investments may have changed considerably since the

investments were made. The statements may therefore not be an accurate reflection of the

activities of the group.

For this reason, it is in the interest of the shareholders of the parent to have a single set of

annual financial statements drawn up for the group to give the shareholders an idea of the

earnings per share and the assets and liabilities of the group. We also call this set of

statements the consolidated statements, group annual financial statements or group

statements. Briefly, these are a combination of all the statements of the companies in the

group. They indicate that the investment represented in the parent's statements has been

replaced by the assets and liabilities of the subsidiary which represent this investment.

However, we need to make certain adjustments to represent these combined values

realistically as a single economic unit, which we will explain to you in the next learning unit.

IFRS 10 requires parent companies to consolidate their investments in subsidiaries and to

include all their subsidiaries in the consolidated financial statements. This implies that

consolidated financial statements are compulsory when a parent-subsidiary relationship

exists.

Group annual financial statements may include the following consolidated financial

statements: statement of profit or loss and other comprehensive income, statement of

changes in equity, statement of financial position, statement of cash flows and notes to the

consolidated financial statements.

When are group statements not required?

IFRS 10 however allows a parent not to present consolidated financial statements only if it

meets all of the following conditions:

The parent itself is a wholly-owned subsidiary, or the parent is a partially-owned sub-

sidiary of another entity and has informed its owners, including those not otherwise

entitled to vote, that it will not present consolidated financial statements, and its owners

do not object to this.

The parent's debt or equity instruments are not traded in a public market.

The parent did not file its financial statements with a securities commission or other

regulatory organisation for the purpose of issuing any class of instruments in a public

market, nor is in the process of doing so.

The ultimate or any intermediate parent of the parent produces consolidated financial

statements available for public use that comply with International Financial Reporting

Standards (IFRS).

FAC2602 / Learning unit 1

11

A parent that elects in terms of the above-mentioned not to present consolidated financial

statements may present separate financial statements as its only financial statements.

1.4 GENERAL PRINCIPLES

Group statements should be a fair reflection of the state of affairs of the parent and its

subsidiaries as at the accounting date.

Eliminate profits or losses that have arisen as a result of transactions within the group

and that have not been realised outside the group.

Eliminate all intragroup balances when determining the total assets and liabilities of the

group.

Eliminate the carrying amount of the parent's investment in the subsidiary.

1.5 EXERCISES

We end the learning unit with a few revision questions. For your own sake, try to answer them

by referring to the notes before you look at the proposed solutions.

QUESTION 1

Explain the following concepts:

a) Parent

b) Subsidiary

c) Wholly-owned subsidiary

QUESTION 2

Distinguish between simple and complex groups and give a schematic representation of each.

QUESTION 3

When are consolidated annual financial statements not required?

FAC2602 / Learning unit 1

12

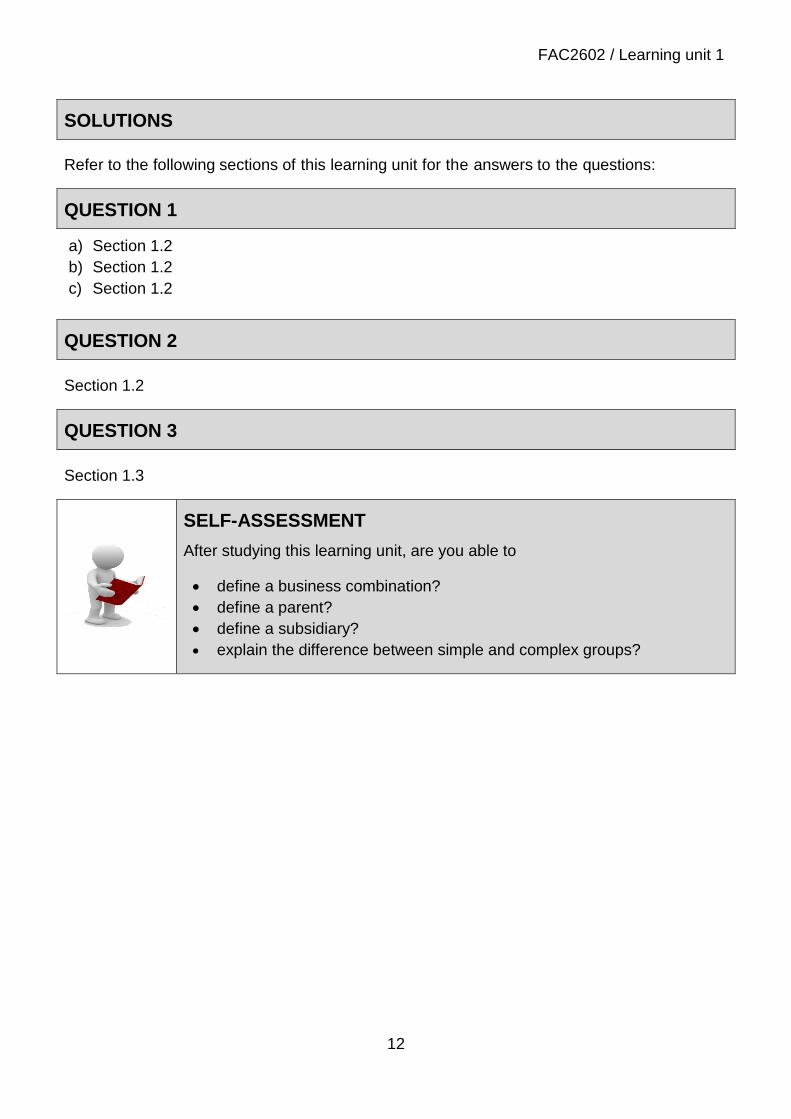

SOLUTIONS

Refer to the following sections of this learning unit for the answers to the questions:

QUESTION 1

a) Section 1.2

b) Section 1.2

c) Section 1.2

QUESTION 2

Section 1.2

QUESTION 3

Section 1.3

SELF-ASSESSMENT

After studying this learning unit, are you able to

define a business combination?

define a parent?

define a subsidiary?

explain the difference between simple and complex groups?

13

FAC2602

Introduction to group annual

financial statements

CONSOLIDATION OF A

WHOLLY-OWNED

SUBSIDIARY AT DATE OF

ACQUISITION

LEARNING UNIT 2

FAC2602 / Learning unit 2

14

LEARNING OUTCOME

Students should be able to consolidate the financial statements of a group of companies at the date of

acquisition if a subsidiary is wholly-owned in accordance with International Financial Reporting Stan-

dards (IFRS).

OVERVIEW

The learning unit is divided into the following:

2.1 INTRODUCTION .......................................................................................................... 15

2.2 BASIC CONSOLIDATION TECHNIQUES ................................................................... 15

2.3 CONSOLIDATION OF THE STATEMENT OF FINANCIAL POSITION OF A WHOLLY-

OWNED SUBSIDIARY AT THE DATE OF ACQUISITION ......................................... 20

2.4 EXERCISES ................................................................................................................. 24

SELF-ASSESSMENT ............................................................................................................. 30

KEY CONCEPTS

Net asset value

Premium

Discount

Intragroup items

Common items

Goodwill

Gain from a bargain purchase

FAC2602 / Learning unit 2

15

ASSESSMENT CRITERIA

After studying this learning unit, you should be able to

draft the consolidated annual financial statements of a parent and its wholly-

owned subsidiary at the date of acquisition in accordance with International

Financial Reporting Standards (IFRS).

calculate intragroup items and common items

calculate goodwill and a gain from a bargain purchase at the acquisition of a

subsidiary

do the pro-forma consolidation journal entries

2.1 INTRODUCTION

As we explained in learning unit 1, the consolidated statements of a group are in principle

merely the combined statements of all the companies in the group. However, we will have to

make certain adjustments to the statements before we can refer to them as consolidated

statements.

We can represent consolidations schematically as follows:

A Ltds

financial

statement

B Ltds

financial

statement

Group consolidated

Financial statementsAdjustments to

A Ltd drafts its financial statements from its financial records, as does B Ltd. Once the

individual statements have been completed, the accountant use the information from these

statements to make the necessary consolidation adjustments and only then compiles the

consolidated statements. Note that the original financial statements of A Ltd and B Ltd are

never amended during the consolidation process. This process repeats itself year after year,

and the adjustments have to be made afresh every year. You will understand this better as

you study the following learning units.

2.2 BASIC CONSOLIDATION TECHNIQUES

Please follow the following basic steps when compiling consolidated annual financial state-

ments:

Eliminate common items.

Eliminate intragroup items.

Consolidate the remaining items.

FAC2602 / Learning unit 2

16

2.2.1 Eliminating common items

One of the first adjustments the accountant should make to the consolidated statements is to

eliminate the investment in the parent's records and the owners' equity section in the

subsidiary's records as at the date when the investment was made. We do this because we

need to eliminate all intragroup transactions since the group is regarded as one economic

entity and cannot enter into transactions with itself.

Note:

In this module, we only deal with cases where the investment in the subsidiary is carried (in the

records of the parent) at the original cost price, which is assumed to be its fair value. For the

sake of simplicity, it is assumed that the fair value remains unchanged from the original cost

price.

EXAMPLE 1

The following example illustrates the elimination of investment in the parent's books at the

date of acquisition:

STATEMENTS OF FINANCIAL POSITION AS AT 28 FEBRUARY 20.5

ASSETS

A Ltd

R

B Ltd

R

Investment in B Ltd - at fair value 10 000 -

Cash and cash equivalents 10 000 10 000

20 000 10 000

EQUITY AND LIABILITIES

Share capital - ordinary shares (20 000/10 000 shares)

20 000

10 000

Draft the consolidated statement of financial position for the A Ltd Group at

28 February 20.5. Assume that A Ltd acquired its interest on that date. B Ltd was

incorporated on 28 February 20.5.

FAC2602 / Learning unit 2

17

SOLUTION 1

Pro-forma consolidated journal entry

Dr

Cr

R

R

Share capital of B Ltd 10 000

Investment in B Ltd

10 000

Elimination of owners' equity of B Ltd at acquisition

The group consolidated statement of financial position would now be drafted as follows:

A LTD GROUP

CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 28 FEBRUARY 20.5

ASSETS

R

Cash and cash equivalents (10 000 + 10 000)

20 000

EQUITY AND LIABILITIES

Share capital

20 000

EXAMPLE 2

The following example illustrates the elimination of investment in the parent's records a few

years after acquisition:

STATEMENTS OF FINANCIAL POSITION AS AT 28 FEBRUARY 20.9

ASSETS

A Ltd R

B Ltd R

Investment in B Ltd - at fair value (cost price: R10 000) 10 000 - Trade and other receivables 12 000 8 000 Cash and cash equivalents 14 000 10 000

36 000 18 000

EQUITY AND LIABILITIES Share capital - ordinary shares (20 000/10 000 shares) 20 000 10 000 Retained earnings 16 000 8 000

36 000 18 000

FAC2602 / Learning unit 2

18

REQUIRED

Draft the consolidated statement of financial position of the A Ltd Group at

28 February 20.9 in compliance with the requirements of International Financial

Reporting Standards (IFRS). Assume that A Ltd acquired its interest on

28 February 20.5 when B Ltd was incorporated.

SOLUTION 2

Pro-forma consolidated journal entry

Dr

Cr

R

R

Share capital of B Ltd 10 000 Investment in B Ltd

10 000

Elimination of owners' equity of B Ltd at acquisition

A LTD GROUP Consolidated statement of financial position as at 28 February 20.9

ASSETS

R

Current assets

Trade and other receivables (12 000 + 8 000)

20 000 Cash and cash equivalents (14 000 + 10 000)

24 000

Total assets

44 000 EQUITY AND LIABILITIES

Total equity Share capital

20 000

Retained earnings (16 000 + 8 000)

24 000 Total equity and liabilities

44 000

With reference to the previous two examples, we can deduce the following:

The journal entry for the elimination of the investment and the owners' equity at the date of

acquisition will remain unchanged from one year to the next.

The share capital on the consolidated statement of financial position is always only that of

the parent.

The profits the subsidiary made after the date of acquisition become part of the retained

earnings of the group and are shown as such in the consolidated statements. We will

discuss this principle at greater length in learning unit 4.

The profits the subsidiary made before the date of acquisition cannot form part of the

retained earnings of the group. The parent pays for such profits. We will also take a closer

look at this principle in learning unit 4.

Since the parent obtained its interest in the subsidiary at the date of incorporation (the date

on which the company was established), there could not have been any retained earnings

in the records of B Ltd.

FAC2602 / Learning unit 2

19

2.2.2 Eliminating intragroup items

It is common practice for companies in the same group to sell inventories and assets to one

another.

The following schematic representation is an example of this:

A Ltd Timber to public

Sells Sells

machine timber

B Ltd Wooden wagons to the public

The actual profit the group made from the sale of goods was the profit made from sales to the

public only, since all the other sales took place within the group. Sales within a group are

known as intragroup sales and therefore have to be eliminated during consolidations.

A Ltd may lend a sum of money or sell an asset to B Ltd. We also have to eliminate these

transactions. In learning unit 7, we will study intragroup transactions in detail.

2.2.3 Consolidating remaining items

Once we have eliminated all common and intragroup items, we can draw up the consolidated

statement of financial position, the consolidated statement of profit or loss and other

comprehensive income, the consolidated statement of changes in equity and the consolidated

statement of cash flows. In this module, we expect you to be able to do all relevant pro-forma

consolidation journal entries for consolidation purposes and to draft the consolidated state-

ment of financial position, consolidated statement of profit or loss and other comprehensive

income and consolidated statement of changes in equity.

FAC2602 / Learning unit 2

20

2.3 CONSOLIDATION OF THE STATEMENT OF FINANCIAL POSITION OF A WHOLLY-OWNED SUBSIDIARY AT THE DATE OF ACQUISITION

We account for all business combinations on the purchase or acquisition method, and this

method involves the following four steps:

identifying the acquirer

determining the acquisition date

recognising and measuring the identifiable assets acquired, the liabilities assumed and any

non-controlling interest in the acquiree

recognising and measuring goodwill or a gain from a bargain purchase

The following three situations may arise if a parent obtains an interest in a subsidiary:

The price paid by the parent for the interest/investment in the subsidiary is equivalent to the

fair value of assets and liabilities acquired. An acquisition of this kind is known as an

acquisition at net asset value.

The price paid by the parent for the interest is higher than the fair value of assets and

liabilities acquired. This is known as acquisition at a premium. This premium should be

treated as goodwill.

After initial recognition, the parent must measure the goodwill acquired in a business

combination at cost less any accumulated impairment losses. We do not amortise

goodwill. Instead, the parent must test it for impairment annually, or more frequently if

events or changes in circumstances indicate that it might be impaired in accordance with

IAS 36 Impairment of Assets.

In this module, we will not be dealing with impairment losses, but will assume the initial cost

price of goodwill to be equal to current fair value.

The price paid by the parent is lower than the fair value of assets and liabilities acquired.

This is known as the acquisition of a subsidiary at a discount, which is also referred to as

a gain from a bargain purchase and is recognised at the acquisition date in profit or loss.

For the purpose of this module, note that a gain from a bargain purchase is a possibility

when acquiring a subsidiary. However, we will deal with this in Accounting III modules.

The following examples illustrate the possible situations which could arise:

FAC2602 / Learning unit 2

21

EXAMPLE 1

Acquisition of a subsidiary at net asset value

The following represent the abridged statements of financial position of A Ltd and its wholly-

owned subsidiary, B Ltd, at 31 December 20.5, which is the date on which A Ltd acquired its

interest in B Ltd.

STATEMENTS OF FINANCIAL POSITION AS AT 31 DECEMBER 20.5

A Ltd

R

B Ltd

R

ASSETS

Investment in B Ltd - at fair value (cost price: R90 000) 90 000 -

Bank 30 000 55 000

Trade and other receivables 60 000 35 000

180 000 90 000

EQUITY AND LIABILITIES

Share capital - ordinary shares (100 000/50 000 shares) 100 000 50 000

Retained earnings 80 000 40 000

180 000 90 000

SOLUTION 1

Calculations

1. Analysis of owners' equity of B Ltd

Total

R

At

R

Since

R

Share capital 50 000

50 000

–

Retained earnings 40 000

40 000

–

90 000

90 000

–

Purchase difference –

–

Consideration 90 000

90 000

–

Therefore, it is clear that the price A Ltd paid for the investment in B Ltd is equal to the

nett assets acquired. (90 000 = 50 000 + 40 000)

FAC2602 / Learning unit 2

22

2. Pro-forma consolidated journal entry

Dr

R

Cr

R

Share capital (B Ltd) 50 000

Retained earnings (B Ltd) 40 000

Investment in B Ltd

90 000

Elimination of owners' equity of B Ltd at

acquisition

The price paid by A Ltd for the investment in B Ltd is equal to the value of the net assets

acquired. (90 000 = 50 000 + 40 000)

A LTD GROUP

CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 31 DECEMBER 20.5

R

ASSETS

Current assets

Cash and cash equivalents (30 000 + 55 000) 85 000

Trade and other receivables (60 000 + 35 000) 95 000

Total assets 180 000

EQUITY AND LIABILITIES

Equity attributable to owners of the parent

Share capital 100 000

Retained earnings 80 000

Total equity 180 000

EXAMPLE 2

Acquisition of a subsidiary at a premium

The following represent the abridged statements of financial position of A Ltd and its wholly-

owned subsidiary B Ltd at 31 December 20.5. This is also the date on which A Ltd acquired

its interest in B Ltd. Note that the information is the same as in the previous example, except

for the investment, which is now R100 000 instead of R90 000.

FAC2602 / Learning unit 2

23

STATEMENTS OF FINANCIAL POSITION AS AT 31 DECEMBER 20.5

ASSETS

A Ltd

R

B Ltd

R

Investment in B Ltd - at fair value (cost price: R100 000) 100 000 -

Bank 20 000 55 000

Trade and other receivables 60 000 35 000

180 000 90 000

EQUITY AND LIABILITIES

Share capital - ordinary shares (100 000/50 000 shares)

100 000

50 000

Retained earnings 80 000 40 000

180 000 90 000

SOLUTION 2

Calculations

1

Analysis of owners' equity of B Ltd

Total R

At R

Since

R

Share capital 50 000

50 000

–

Retained earnings 40 000

40 000

–

90 000

90 000

–

Equity represented by goodwill ─ parent 10 000

10 000

–

Consideration 100 000

100 000

–

2

Pro-forma consolidated journal entry

Dr R

Cr R

Share capital (B Ltd) 50 000

Retained earnings (B Ltd) 40 000

Goodwill 10 000

Investment in B Ltd

100 000

Elimination of owners' equity of B Ltd at acquisition

A LTD GROUP

CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 31 DECEMBER 20.5

R

ASSETS

Non-current assets

Goodwill

10 000

10 000

Current assets

Cash and cash equivalents (20 000 + 55 000)

75 000

Trade and other receivables (60 000 + 35 000)

95 000

170 000

Total assets

180 000

FAC2602 / Learning unit 2

24

EQUITY AND LIABILITIES

Equity attributable to owners of parent

Share capital

100 000

Retained earnings

80 000

Total equity and liabilities

180 000

COMMENTS

In this example, the parent paid more than the net asset value for its interest in the subsidiary,

which means that a premium (goodwill) was paid at acquisition. Goodwill is regarded as an

intangible asset and should be shown as a non-current asset in the consolidated statement of

financial position. In this module, we determine the goodwill at acquisition only. We are not

concerned with future changes in the value of goodwill, which will be dealt with on third-year level.

According to IFRS 3, the two options for calculating goodwill are as follows:

a) The partial method (the method used in this MO001)

b) The full goodwill method (which uses the non-controlling interest at fair value to determine

goodwill). However, this method will be dealt with later on third-year level.

EXAMPLE 3

Acquisition of a subsidiary at a discount

COMMENTS

This is when the parent pays less than the net asset value for its interest in the subsidiary. We will

deal with this on third-year level.

2.4 EXERCISES

To see whether you are able to apply the content of this learning unit, answer the following

questions. It is important to calculate the answers before looking at the suggested solutions.

FAC2602 / Learning unit 2

25

QUESTION 1

You receive the following statements of financial position of P Ltd and S Ltd as at 30 June 20.6:

STATEMENTS OF FINANCIAL POSITION AS AT 30 JUNE 20.6

P Ltd

R

S Ltd

R

ASSETS

Investment in S Ltd - 100 000 shares at fair value

(cost price: R145 000)

145 000 -

Current assets 40 000 115 000

185 000 115 000

EQUITY AND LIABILITIES

Share capital - 100 000 ordinary shares 100 000 100 000

Retained earnings 85 000 15 000

185 000 115 000

REQUIRED

Draft the consolidated statement of financial position of the P Ltd Group as

at 30 June 20.6 in compliance with the requirements of International

Financial Reporting Standards; if P Ltd acquired its interest in S Ltd at

30 June 20.6.

FAC2602 / Learning unit 2

26

QUESTION 2

You receive the following trial balances:

TRIAL BALANCES AT 31 MARCH 20.5

P Ltd

Dr/(Cr)

R

S Ltd

Dr/(Cr)

R

Share capital - ordinary shares (100 000/50 000 shares) (100 000) (50 000)

Retained earnings (80 000) (20 000)

Trade and other receivables 40 000 15 000

Inventories 20 000 35 000

Trade and other payables (15 000) (18 000)

Long-term borrowings (100 000) -

Loan – S Ltd 80 000 -

Investment in S Ltd – 50 000 shares at fair value

(cost price: R80 000)

80 000 -

Loan – P Ltd - (80 000)

Bank 25 000 58 000

Property, plant and equipment 50 000 60 000

REQUIRED

Draft the consolidated statement of financial position of the P Ltd Group as at

31 March 20.5 in compliance with the requirements of International Financial

Reporting Standards; if P Ltd acquired its interest in S Ltd at 31 March 20.5.

SOLUTIONS

QUESTION 1

You should have followed the following steps:

Step 1 - determining the percentage interest

Investment in S Ltd

=

100 000 shares

x 100

Ordinary shares of S Ltd 100 000 shares

= 100% (therefore wholly-owned subsidiary)

FAC2602 / Learning unit 2

27

Note that the interest in S Ltd is determined by the amount of shares held in S Ltd and not

the rand value. You must use 100 000 shares and not R145 000.

Step 2 - Draft the analysis of owners' equity of S Ltd:

Analysis of owners' equity of S Ltd

Total

R

At

R

Since

R

Share capital 100 000 100 000 -

Retained earnings 15 000 15 000 -

115 000 115 000 -

Equity represented by goodwill - parent 30 000 30 000 -

Consideration 145 000 145 000 -

Step 3 - eliminating all common items

Pro-forma consolidated journal entry

Dr

Cr

R

R

Share capital – S Ltd 100 000

Retained earnings – S Ltd 15 000

Goodwill 30 000

Investment in S Ltd

145 000

Elimination of owners' equity of S Ltd at acquisition

Step 4 – drafting the consolidated statement of financial position

P LTD GROUP

CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 30 JUNE 20.6

ASSETS R

Non-current assets

Goodwill 30 000

Current assets (40 000 + 115 000) 155 000

Total assets 185 000

FAC2602 / Learning unit 2

28

EQUITY AND LIABILITIES

Equity attributable to owners of the parent

Share capital 100 000

Retained earnings 85 000

Total equity and liabilities 185 000

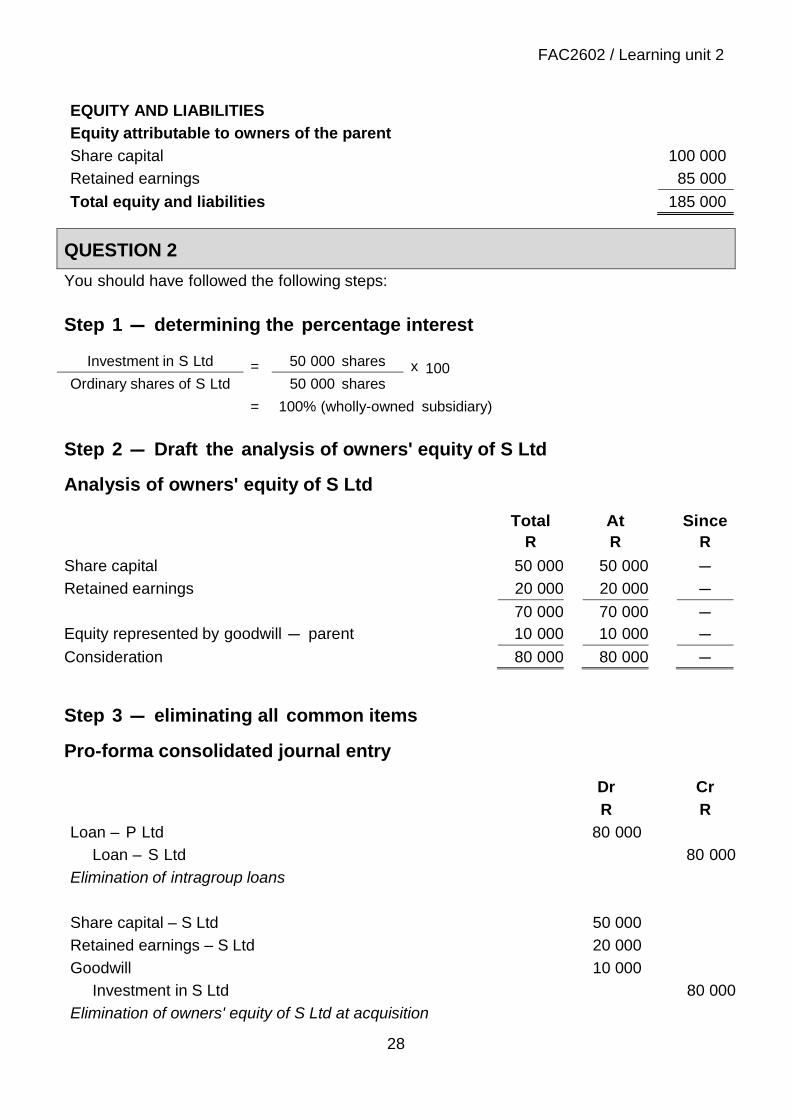

QUESTION 2

You should have followed the following steps:

Step 1 - determining the percentage interest

Investment in S Ltd = 50 000 shares x 100

Ordinary shares of S Ltd 50 000 shares

= 100% (wholly-owned subsidiary)

Step 2 - Draft the analysis of owners' equity of S Ltd

Analysis of owners' equity of S Ltd

Total

R

At

R

Since

R

Share capital 50 000 50 000 -

Retained earnings 20 000 20 000 -

70 000 70 000 -

Equity represented by goodwill - parent 10 000 10 000 -

Consideration 80 000 80 000 -

Step 3 - eliminating all common items

Pro-forma consolidated journal entry

Dr

Cr

R

R

Loan – P Ltd 80 000

Loan – S Ltd 80 000

Elimination of intragroup loans

Share capital – S Ltd 50 000

Retained earnings – S Ltd 20 000

Goodwill 10 000

Investment in S Ltd

80 000

Elimination of owners' equity of S Ltd at acquisition

FAC2602 / Learning unit 2

29

Step 4 - drafting the consolidated statement of financial position

P LTD GROUP

CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 31 MARCH 20.5

31 MARCH 20.5

ASSETS

Non-current assets

Property, plant and equipment (50 000 + 60 000) 110 000

Goodwill 10 000

120 000

Current assets

Trade and other receivables (40 000 + 15 000) 55 000

Inventories (20 000 + 35 000) 55 000

Cash and cash equivalents (25 000 + 58 000) 83 000

193 000

Total assets 313 000

EQUITY AND LIABILITIES

Equity attributable to owners of the parent

Share capital 100 000

Retained earnings 80 000

Total equity 180 000

Non-current liabilities

Long-term borrowings 100 000

Current liabilities

Trade and other payables (15 000 + 18 000) 33 000

Total liabilities 133 000

Total equity and liabilities 313 000

FAC2602 / Learning unit 2

30

COMMENTS

You will note that in our proposed solutions to the assignments, we give the consolidated

statement of financial position followed by the calculations. We will not criticise the format of your

answer, but please ensure that you answer the question in full.

It would be perfectly acceptable to give some of the easier calculations in brackets, as in our

proposed solutions.

Note that this question included intragroup loans. We eliminated both the parent's and subsidiary's

debit and credit loans against each other.

SELF-ASSESSMENT

After studying this learning unit, are you able to

draft the consolidated annual financial statements of a parent and its wholly-

owned subsidiary at date of acquisition in accordance with International Financial

Reporting Standards?

calculate intragroup and common items?

calculate goodwill and a gain from a bargain purchase at the acquisition of a

subsidiary?

do the pro-forma consolidation journal entries?

31

FAC2602

Introduction to group annual

financial statements

CONSOLIDATION OF A

PARTLY-OWNED

SUBSIDIARY AT DATE OF

ACQUISITION

LEARNING UNIT 3

FAC2602 / Learning unit 3

32

LEARNING OUTCOME

Students should be able to consolidate the financial statements of a group of companies at the date of

acquisition if a subsidiary is wholly-owned in accordance with International Financial Reporting Stan-

dards.

OVERVIEW

The learning unit is divided into the following:

3.1 INTRODUCTION .......................................................................................................... 33

3.2 CONSOLIDATION OF THE STATEMENT OF FINANCIAL POSITION OF A PARTLY-

OWNED SUBSIDIARY AT THE DATE OF ACQUISITION ........................................ 33

3.3 EXERCISES ................................................................................................................. 40

SELF-ASSESSMENT ............................................................................................................. 46

KEY CONCEPTS

Partly-owned subsidiary

Outside owners

Non-controlling owners

Non-controlling interests (NCI)

ASSESSMENT CRITERIA

After studying this learning unit, you should be able to

calculate the percentage applicable to non-controlling owners

draft the consolidated annual financial statements of a group with a partly-owned

subsidiary at the date of acquisition in accordance with International Financial

Reporting Standards

do the pro-forma consolidation journal entries

FAC2602 / Learning unit 3

33

3.1 INTRODUCTION

In learning unit 2, we dealt only with wholly-owned subsidiaries, in other words, where the

parent has acquired the entire issued share capital of the subsidiary.

However, there may be various reasons why it could be impossible for the parent to take up

all the shares in the subsidiary. Some of the owners may not be prepared to sell their shares

to the parent, or the parent may not have sufficient funds to purchase all the shares. The

other owners of the subsidiary are known as non-controlling or outside owners. Non-

controlling owners may consist of ordinary owners and preference owners. We will deal with

subsidiaries with preference shares in learning unit 9.

3.2 CONSOLIDATION OF THE STATEMENT OF FINANCIAL POSITION OF A PARTLY-OWNED SUBSIDIARY AT THE DATE OF ACQUISITION

The same rules apply for consolidation purposes, except that we now have to make provision

for the non-controlling owners' interest in the profit of the subsidiary.

EXAMPLE

P Ltd

80% of voting rights

20% of voting rights

S Ltd Non-controlling owners

To make provision for the non-controlling owners' interest in the profit of the subsidiary, it is

important to know how to calculate the percentage interest in the subsidiary.

FAC2602 / Learning unit 3

34

EXAMPLE 1

The following represent the condensed statements of financial position of A Ltd and its subsi-

diary, B Ltd:

STATEMENTS OF FINANCIAL POSITION AS AT 30 JUNE 20.6

SOLUTION 1

We calculate the parent's interest in the subsidiary as follows:

Investment in B Ltd =

80 000 shares x 100 = 80%

Issued shares of B Ltd 100 000 shares

Therefore, A Ltd has an 80% interest in B Ltd, and the non-controlling owners of B Ltd only

have a 20% interest in B Ltd.

A Ltd

R

B Ltd

R

ASSETS

Property, plant and equipment

Investment in B Ltd

150 000

200 000

– 80 000 ordinary shares at fair value (cost price: R90 000) 90 000 -

Current assets 110 000 10 000

350 000 210 000

EQUITY AND LIABILITIES

Share capital - ordinary shares (200 000/100 000 shares)

200 000

100 000

Retained earnings 50 000 30 000

Long-term borrowings 100 000 80 000

350 000 210 000

FAC2602 / Learning unit 3

35

EXAMPLE 2

The following represent the condensed statements of financial position of P Ltd and S Ltd:

STATEMENTS OF FINANCIAL POSITION AS AT 31 JULY 20.4

P Ltd

R

S Ltd

R

ASSETS

Property, plant and equipment

Investment in S Ltd

150 000

200 000

- 35 000 ordinary shares at fair value (cost price: R75 000) 75 000 -

Current assets 125 000 10 000

350 000 210 000

EQUITY AND LIABILITIES

Share capital - ordinary shares (100 000/50 000 shares)

200 000

100 000

Retained earnings 50 000 30 000

Long-term borrowings 100 000 80 000

350 000 210 000

SOLUTION 2

We calculate the parent's interest in the subsidiary as follows:

Investment in S Ltd =

35 000 shares x 100 = 70%

Issued shares of S Ltd 50 000 shares

As for wholly-owned subsidiaries, the following three situations may occur when a parent

acquires an interest in a partly-owned subsidiary:

Acquired at net asset value

Acquired at a premium (goodwill)

Acquired at a discount (gain from a bargain purchase)

Examples 3 to 5 below illustrate the three situations that may arise:

FAC2602 / Learning unit 3

36

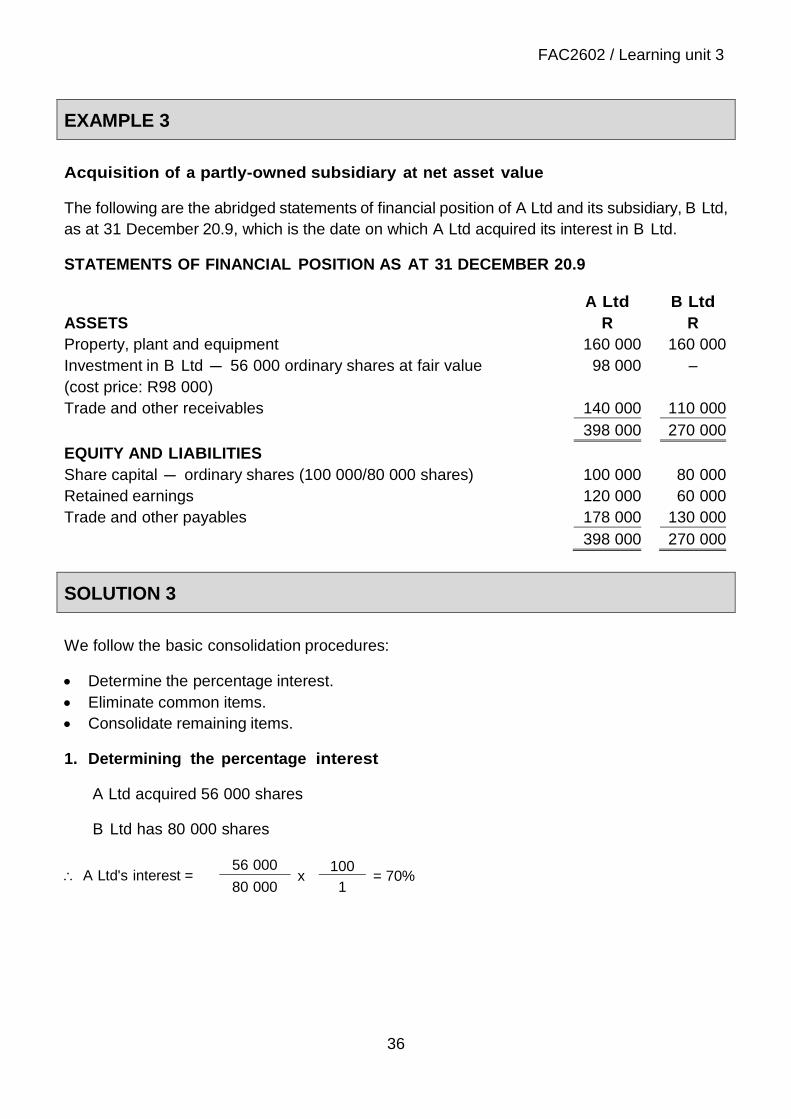

EXAMPLE 3

Acquisition of a partly-owned subsidiary at net asset value

The following are the abridged statements of financial position of A Ltd and its subsidiary, B Ltd,

as at 31 December 20.9, which is the date on which A Ltd acquired its interest in B Ltd.

STATEMENTS OF FINANCIAL POSITION AS AT 31 DECEMBER 20.9

ASSETS

A Ltd

R

B Ltd

R

Property, plant and equipment 160 000 160 000

Investment in B Ltd - 56 000 ordinary shares at fair value

(cost price: R98 000)

98 000 –

Trade and other receivables 140 000 110 000

398 000 270 000

EQUITY AND LIABILITIES

Share capital - ordinary shares (100 000/80 000 shares) 100 000 80 000

Retained earnings 120 000 60 000

Trade and other payables 178 000 130 000

398 000 270 000

SOLUTION 3

We follow the basic consolidation procedures:

Determine the percentage interest.

Eliminate common items.

Consolidate remaining items.

1. Determining the percentage interest

A Ltd acquired 56 000 shares

B Ltd has 80 000 shares

A Ltd's interest = 56 000

x 100

= 70% 80 000 1

FAC2602 / Learning unit 3

37

2. Analysis of owners' equity of B Ltd at 31 December 20.9

Total

A Ltd 70 % NCI

30 %

At Since

At acquisition

Share capital

Retained earnings

R

80 000

60 000

R

56 000

42 000

R

R

24 000

18 000

Purchase difference

140 000

-

98 000

-

42 000

-

Consideration and NCI 140 000 98 000 42 000

COMMENT

In this question, the date of acquisition and the date of consolidation are the same, which is why

the statement of financial position does not include any of the subsidiary's other equity

components since these have been eliminated at acquisition (see pro-forma consolidated journal

entry).

Non-controlling interests are presented as a credit in the statement of financial position, as it

reflects what is owed to the non-controlling owners in terms of their share of the equity.

3. Pro-forma consolidated journal entry

Dr

R

Cr

R

NCI#

R

Share capital 80 000

Retained earnings 60 000

Investment in B Ltd

98 000

Non-controlling interests (statement of financial position)

42 000

42 000

Elimination of owners' equity of B Ltd at acquisition

42 000

# Please note: We only show this column to reflect the movement of non-controlling interests

(NCI). It is not a journal entry. We will do this in all the exercises that follow.

FAC2602 / Learning unit 3

38

A LTD GROUP

CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 31 DECEMBER 20.9

R

R

ASSETS

Non-current assets

Property, plant and equipment (160 000 + 160 000) 320 000

Current assets

Trade and other receivables (140 000 + 110 000) 250 000

Total assets 570 000

EQUITY AND LIABILITIES

Equity attributable to owners of the parent

Share capital 100 000

Retained earnings 120 000

220 000

Non-controlling interests 42 000

Total equity 262 000

Current liabilities

Trade and other payables (178 000 + 130 000) 308 000

Total equity and liabilities 570 000

EXAMPLE 4

Acquisition of a partly-owned subsidiary at a premium (goodwill)

The following are the abridged statements of financial position of A Ltd and its subsidiary,

B Ltd, as at 31 December 20.9, which is the date on which A Ltd acquired its interest in B Ltd.

STATEMENTS OF FINANCIAL POSITION AS AT 31 DECEMBER 20.9

ASSETS

A Ltd

R

B Ltd

R

Property, plant and equipment 160 000

160 000

Investment in B Ltd

– 64 000 ordinary shares at fair value (cost price: R140 000) 140 000

-

Trade and other receivables 98 000

110 000

398 000

270 000

EQUITY AND LIABILITIES

Share capital – ordinary shares (100 000/80 000 shares) 100 000 80 000

Retained earnings 120 000

60 000

Trade and other payables 178 000

130 000

398 000

270 000

FAC2602 / Learning unit 3

39

SOLUTION 4

Once again, we follow the basic consolidation procedures:

Determine the percentage interest.

Eliminate common items.

Consolidate remaining items.

1. Determine the percentage interest

A Ltd acquired 64 000 shares

B Ltd has 80 000 shares

A Ltd's interest = 64 000

x 100

= 80% 80 000 1

2. Analysis of owners' equity of B Ltd at 31 December 20.9

3. Pro-forma consolidated journal entry

Dr

R

Cr

R

NCI

R

Share capital 80 000

Retained earnings 60 000

Goodwill 28 000

Investment in B Ltd

140 000

Non-controlling interests (statement of financial position)

28 000

28 000

Elimination of owners' equity of B Ltd at acquisition

28 000

Total A Ltd 80% NCI

20% At Since

At acquisition

Share capital

Retained earnings

R

80 000

60 000

R

64 000

48 000

R

R

16 000

12 000

Equity represented by goodwill – parent

140 000

28 000

112 000

28 000

28 000

–

Consideration and NCI 168 000 140 000 28 000

FAC2602 / Learning unit 3

40

A LTD GROUP

CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 31 DECEMBER 20.9

20 .9

R

ASSETS

Non-current assets

Property, plant and equipment (160 000 + 160 000) 320 000

Goodwill 28 000

348 000

0 Current assets

Trade and other receivables (98 000 + 110 000) 208 000

Total assets 556 000

EQUITY AND LIABILITIES

Equity attributable to owners of the parent

Share capital 100 000

Retained earnings 120 000

220 000

Non-controlling interests 28 000

Total equity 248 000

Current liabilities

Trade and other payables (178 000 + 130 000) 308 000

Total equity and liabilities 556 000

EXAMPLE 5

Acquisition of a partly-owned subsidiary at a discount (gain from a bargain purchase)

We will deal with the acquisition of a subsidiary at a discount in detail at third-year level; it

does not form part of this course.

3.3 EXERCISES

We shall now conclude this learning unit with a few revision questions. It is in your own interest

to try to answer these questions by referring to the learning unit before you look at the

proposed solutions.

FAC2602 / Learning unit 3

41

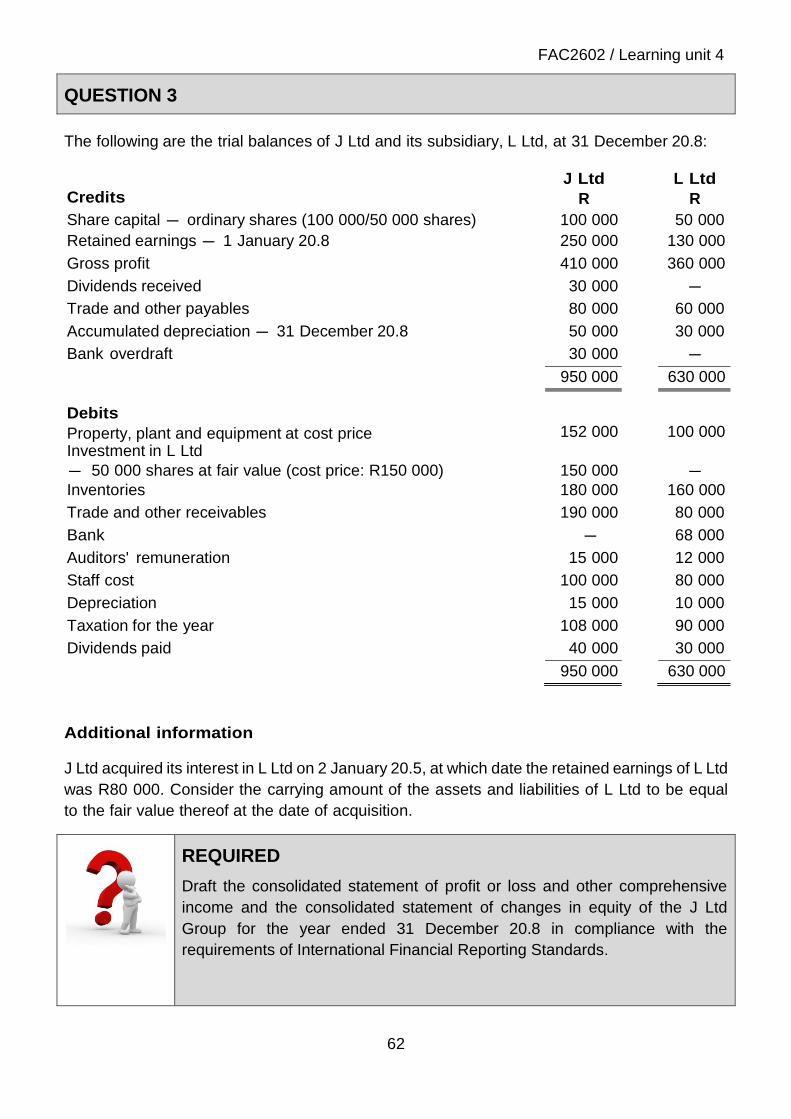

QUESTION 1

P Ltd acquired its interest in S Ltd on 30 June 20.5. Each share carries one vote. The following

represent the condensed trial balances of P Ltd and S Ltd at 30 June 20.5:

P Ltd S Ltd

R R

Debits

Property, plant and equipment 52 700 133 900

Investment in S Ltd

– 75 000 shares at fair value (cost price: R90 000) 90 000 –

– 10 000 debentures at fair value (cost price: R10 000) 10 000 –

Bank 2 500 –

Inventories 15 800 4 200

171 000 138 100

Credits

Share capital – ordinary shares (150 000/100 000 shares) 150 000 100 000

Retained earnings 12 200 11 300

Debentures (20 000 debentures) – 20 000

Trade and other payables 8 800 1 200

Bank overdraft – 5 600

171 000 138 100

REQUIRED

Draft the consolidated statement of financial position of the P Ltd Group as at

30 June 20.5 in compliance with the requirements of International Financial

Reporting Standards.

FAC2602 / Learning unit 3

42

QUESTION 2

P Ltd acquired 40 000 ordinary shares in S Ltd on 1 January 20.5, and each share carries one

vote.

The following represent the condensed statements of financial position of P Ltd and S Ltd at

1 January 20.5:

P Ltd

R

S Ltd

R ASSETS

Property, plant and equipment

103 200

157 300

Unsecured loan to P Ltd

-

20 000

Investment in S Ltd

– 40 000 ordinary shares at fair value (cost price: R180 000) 180 000

-

Current assets 44 000

15 500

327 200

192 800

EQUITY AND LIABILITIES

Share capital – ordinary shares (100 000/50 000 shares) 200 000

100 000

Revaluation of land and buildings -

50 000

Retained earnings 95 700

40 000

Long-term borrowing from S Ltd 20 000

–

Current liabilities 11 500 2 800

327 200

192 800

REQUIRED

Draft the consolidated statement of financial position of the P Ltd Group as at

1 January 20.5 in compliance with the requirements of International Financial

Reporting Standards.

FAC2602 / Learning unit 3

43

SOLUTIONS

QUESTION 1

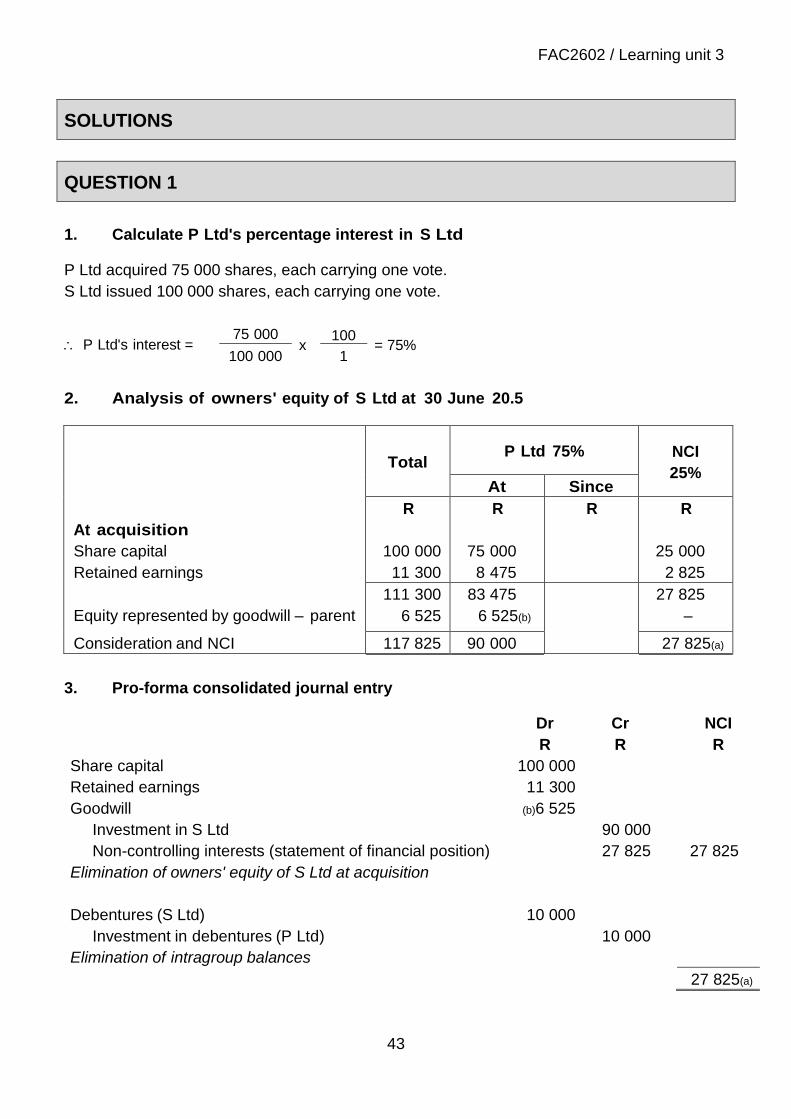

1. Calculate P Ltd's percentage interest in S Ltd

P Ltd acquired 75 000 shares, each carrying one vote.

S Ltd issued 100 000 shares, each carrying one vote.

P Ltd's interest = 75 000

x 100

= 75% 100 000 1

2. Analysis of owners' equity of S Ltd at 30 June 20.5

3. Pro-forma consolidated journal entry

Dr

R

Cr

R

NCI

R

Share capital 100 000

Retained earnings 11 300

Goodwill (b)6 525

Investment in S Ltd

90 000

Non-controlling interests (statement of financial position)

27 825

27 825

Elimination of owners' equity of S Ltd at acquisition

Debentures (S Ltd) 10 000

Investment in debentures (P Ltd) 10 000

Elimination of intragroup balances

27 825(a)

Total P Ltd 75% NCI

25% At Since

At acquisition

Share capital

Retained earnings

R

100 000

11 300

R

75 000

8 475

R

R

25 000

2 825

Equity represented by goodwill – parent

111 300

6 525

83 475

6 525(b)

27 825

–

Consideration and NCI 117 825 90 000 27 825(a)

FAC2602 / Learning unit 3

44

P LTD GROUP

CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 30 JUNE 20.5

R

ASSETS

Non-current assets

Property, plant and equipment (52 700 + 133 900) 186 600

Goodwill (b)6 525

193 125

Current assets

Inventories (15 800 + 4 200) 20 000

Cash and cash equivalents 2 500

22 500

Total assets 215 625

EQUITY AND LIABILITIES

Equity attributable to owners of the parent

Share capital 150 000

Retained earnings 12 200

162 200

Non-controlling interests (a)27 825

Total equity 190 025

Non-current liabilities

Debentures (20 000﹣10 000) 10 000

10 000

Current liabilities

Trade and other payables (8 800 + 1 200) 10 000

Bank overdraft 5 600

15 600

Total liabilities 25 600

Total equity and liabilities 215 625

COMMENT

Debit and credit bank balances may not be set off against each other upon consolidation.

Therefore, we show the parent's favourable bank balance and the subsidiary's bank overdraft

separately.

The balances can be offset against each other if the company with the favourable balance has

guaranteed the overdraft account, but only if both accounts are at the same bank.

FAC2602 / Learning unit 3

45

QUESTION 2

1. Calculate P Ltd's percentage interest in S Ltd

P Ltd acquired 40 000 shares, each carrying one vote.

S Ltd issued 50 000 shares, each carrying one vote.

P Ltd's interest = 40 000

x 100

= 80% 50 000 1

2. Analysis of owners' equity of S Ltd at 1 January 20.5

3. Pro-forma consolidated journal entry

Dr

R

Cr

R

NCI

R

Share capital 100 000

Revaluation surplus 50 000

Retained earnings 40 000

Goodwill (a)28 000

Investment in S Ltd

180 000

Non-controlling interests(statement of financial position)

38 000

38 000

Elimination of owners' equity of S Ltd at acquisition

Long-term loan from S Ltd (P Ltd) 20 000

Unsecured loan to P Ltd (S Ltd) 20 000

Elimination of intragroup loans

38 000(b)

Total P Ltd 80% NCI

20% At Since

At acquisition

Share capital

Retained earnings

Revaluation surplus

R

100 000

40 000

50 000

R

80 000

32 000

40 000

R

R

20 000

8 000

10 000

Equity represented by goodwill – parent

190 000

28 000

152 000

28 000(a)

38 000

–

Consideration and NCI 218 000 180 000 38 000(b)

FAC2602 / Learning unit 3

46

P LTD GROUP

CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 1 JANUARY 20.5

R

ASSETS

Non-current assets

Property, plant and equipment (103 200 + 157 300) 260 500

Goodwill (a)28 000

288 500

Current assets (44 000 + 15 500) 59 500

Total assets 348 000

EQUITY AND LIABILITIES

Equity attributable to owners of the parent

Share capital 200 000

Retained earnings 95 700

295 700

Non-controlling interests (b)38 000

Total equity 333 700

Current liabilities (11 500 + 2 800) 14 300

Total equity and liabilities 348 000

SELF-ASSESSMENT

After studying this learning unit, are you able to

calculate the percentage applicable to non-controlling owners?

draft the consolidated annual financial statements of a group with a partly-

owned subsidiary at the date of acquisition in accordance with International

Financial Reporting Standards?

do the pro-forma consolidation journal entries?

47

FAC2602

Introduction to group annual

financial statements

CONSOLIDATION OF A

WHOLLY-OWNED

SUBSIDIARY AFTER DATE

OF ACQUISITION

LEARNING UNIT 4

FAC2602 / Learning unit 4

48

LEARNING OUTCOME

Students should be able to consolidate the financial statements of a group of companies if the interest

in the wholly-owned subsidiary was acquired a few years ago in accordance with International Finan-

cial Reporting Standards.

OVERVIEW

The learning unit is divided into the following:

4.1 INTRODUCTION .......................................................................................................... 49

4.2 TREATMENT OF GOODWILL ARISING ON ACQUISITION ...................................... 49

4.3 CONSOLIDATION OF A WHOLLY-OWNED SUBSIDIARY AFTER THE DATE OF

ACQUISITION ............................................................................................................. 49

4.4 EXERCISES ................................................................................................................. 59

SELF-ASSESSMENT ............................................................................................................. 72

KEY CONCEPTS

Post-acquisition profits

ASSESSMENT CRITERIA

After studying this learning unit, are you able to

draft the consolidated annual financial statements of a group if the interest in

the wholly-owned subsidiary was acquired a few years ago in accordance with

International Financial Reporting Standards?

do the pro-forma consolidation journal entries?

FAC2602 / Learning unit 4

49

4.1 INTRODUCTION

In learning unit 2, we discussed the consolidation of a wholly-owned subsidiary at the date of

acquisition. In this learning unit, we deal with the compiling of consolidated annual financial

statements at any date after the acquisition of an interest in a subsidiary. We always eliminate

the owners' equity (share capital and other components) of a subsidiary that exist at the

acquisition of the subsidiary against the investment in the subsidiary. It does not form part of

the owners' equity (share capital and other components) of the group. The parent originally

paid for it. Refer to examples 1 to 3 in learning unit 2 if you need to make sure that you un-

derstand the above statement.

Therefore, all the profits the subsidiary makes after the date of acquisition become the profits

of the group and should be included as such in the consolidated statements. All components

of equity of a subsidiary which was formed after the date of acquisition form part of the total

equity of the group.

4.2 TREATMENT OF GOODWILL ARISING ON ACQUISITION

By now, you should be familiar with the term "goodwill". A parent may pay more or less than

the net asset value of the shares acquired with the purchase of the interest in the subsidiary.

This can be attributed to the following:

specific items which have a market value that is higher or lower than the carrying value

(e.g. property or plant)

the value of the undertaking as a whole

The goodwill that a parent pays for when acquiring a subsidiary represents the parent's

anticipation of future economic benefits. We reflect goodwill at cost price for the purposes of this

course. We will deal with future adjustments in value on third year level.

We will also deal further with the alternative option and methods in IFRS 3 regarding the

calculation of goodwill on third-year level.

4.3 CONSOLIDATION OF A WHOLLY-OWNED SUBSIDIARY AFTER THE DATE OF ACQUISITION

Where consolidation takes place at a date after the acquisition of the interest in the sub-

sidiary, we must consolidate both the statements of financial position and the statements of

profit and loss and other comprehensive income of the parent and the subsidiary.

We will still follow the same consolidation procedures:

Eliminate common items.

Eliminate intragroup items.

Consolidate remaining items.

FAC2602 / Learning unit 4

50

We now turn our attention to a new aspect, namely that we will have to deal with various periods

when analysing the owners' equity of the subsidiary. The following serves as an example of

this:

Suppose A Ltd acquired its 100% interest in B Ltd on 1 January 20.1, and you are required to

draft the consolidated financial statements for the year ended 31 December 20.8. You will

have to divide the analysis of owners' equity into three parts.

Analysis of owners' equity of B Ltd

Total

R

At

R

Since

R

At acquisition

1 January 20.1

Since acquisition to beginning of current year

2 January 20.1 to 31 December 20.7

Current year

1 January 20.8 to 31 December 20.8

As in the previous learning units, we will deal with the three situations that may arise when a

parent acquire shares in a subsidiary.

FAC2602 / Learning unit 4

51

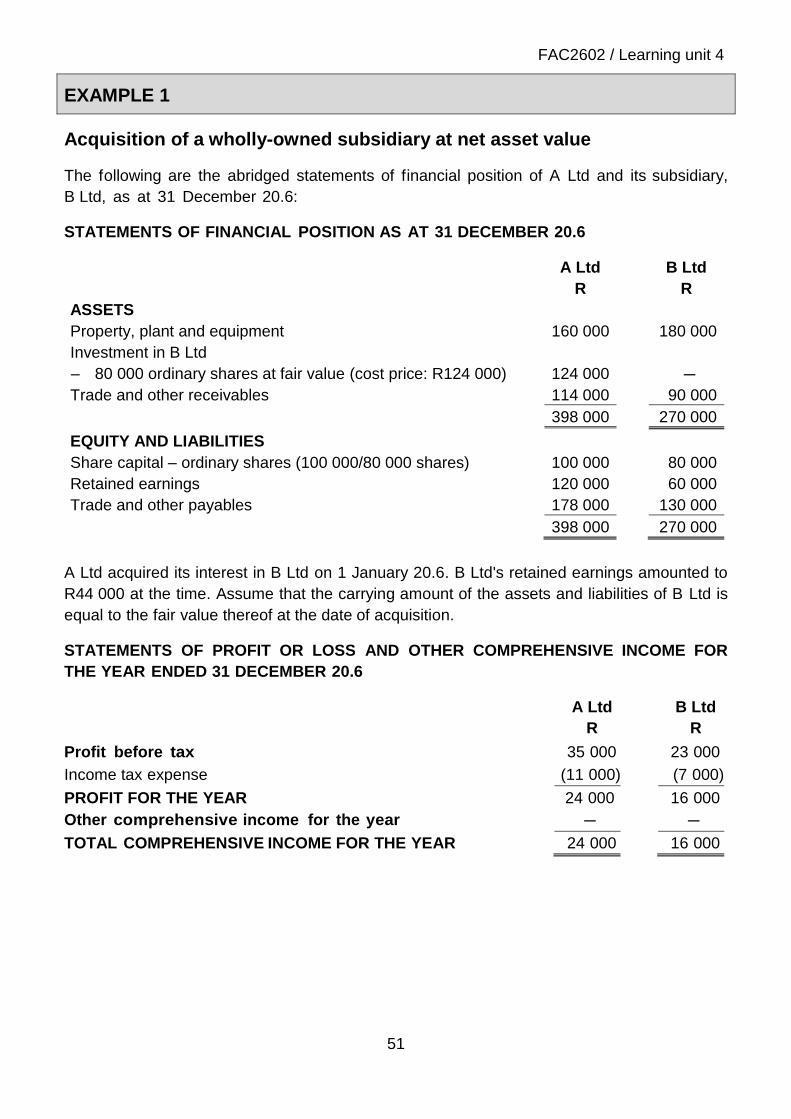

EXAMPLE 1

Acquisition of a wholly-owned subsidiary at net asset value

The following are the abridged statements of financial position of A Ltd and its subsidiary,

B Ltd, as at 31 December 20.6:

STATEMENTS OF FINANCIAL POSITION AS AT 31 DECEMBER 20.6

A Ltd

R

B Ltd

R

ASSETS

Property, plant and equipment 160 000

180 000

Investment in B Ltd

– 80 000 ordinary shares at fair value (cost price: R124 000) 124 000

-

Trade and other receivables 114 000

90 000

398 000

270 000

EQUITY AND LIABILITIES

Share capital – ordinary shares (100 000/80 000 shares) 100 000

80 000

Retained earnings 120 000

60 000

Trade and other payables 178 000

130 000

398 000

270 000

A Ltd acquired its interest in B Ltd on 1 January 20.6. B Ltd's retained earnings amounted to

R44 000 at the time. Assume that the carrying amount of the assets and liabilities of B Ltd is

equal to the fair value thereof at the date of acquisition.

STATEMENTS OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR

THE YEAR ENDED 31 DECEMBER 20.6

A Ltd

R

B Ltd

R

Profit before tax 35 000 23 000

Income tax expense (11 000) (7 000)

PROFIT FOR THE YEAR 24 000 16 000

Other comprehensive income for the year - -

TOTAL COMPREHENSIVE INCOME FOR THE YEAR 24 000 16 000

FAC2602 / Learning unit 4

52

STATEMENTS OF CHANGES IN EQUITY FOR THE YEAR ENDED 31 DECEMBER 20.6

Share capital Retained

earnings

Total

A Ltd B Ltd A Ltd B Ltd A Ltd B Ltd

R R R R R R

Balance at 1 January 20.6 100 000 80 000 96 000 44 000 196 000 124 000

Changes in equity for 20.6

Total comprehensive income for

the year

Profit for the year 24 000 16 000 24 000 16 000

Balance at 31 December 20.6 100 000 80 000 120 000 60 000 220 000 140 000

Suppose you have to draft the consolidated statement of profit or loss and other

comprehensive income, the consolidated statement of changes in equity and the consolidated

statement of financial position at 31 December 20.6.

SOLUTION 1

Before you draft these statements, you can do the following:

Analyse the owners' equity in B Ltd.

Do the pro-forma consolidation journal entries.

1. Analysis of owners' equity in B Ltd

At acquisition – 1 Jan

2 .6

Share capital

Retained earnings Purchase difference

Consideration and NCI

Since acquisition

• Current year

Profit for the year

Total A Ltd 1 00%

NCI

0% At Since

At acquisition - 1 Jan 20.6

Share capital

Retained earnings

R

80 000

44 000

R

80 000

44 000

R R

-

-

Purchase difference

124 000

-

124 000

-

16 000

-

- Consideration and NCI

124 000

16 000

124 000

-

-

Since acquisition

Current year

Profit for the year

140 000

16 000

-

FAC2602 / Learning unit 4

53

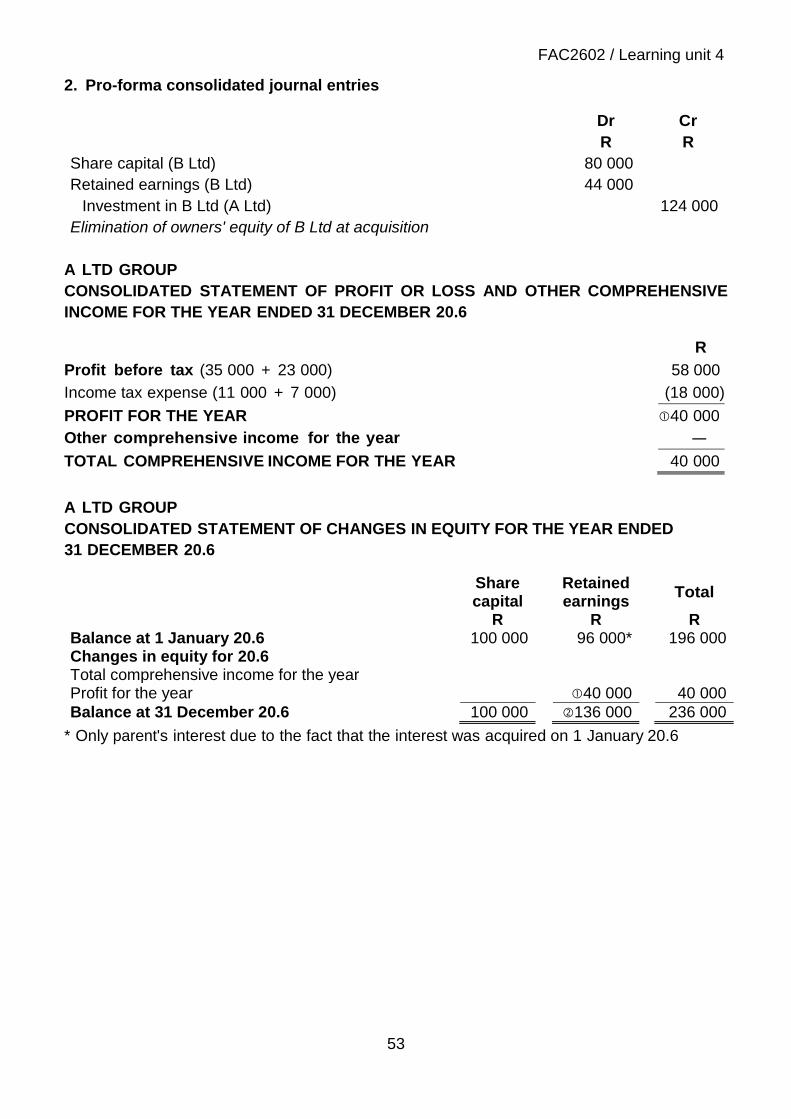

2. Pro-forma consolidated journal entries

Dr Cr

R R

Share capital (B Ltd) 80 000

Retained earnings (B Ltd) 44 000

Investment in B Ltd (A Ltd)

124 000

Elimination of owners' equity of B Ltd at acquisition

A LTD GROUP

CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE

INCOME FOR THE YEAR ENDED 31 DECEMBER 20.6

R

Profit before tax (35 000 + 23 000) 58 000

Income tax expense (11 000 + 7 000) (18 000)

PROFIT FOR THE YEAR 40 000

Other comprehensive income for the year -

TOTAL COMPREHENSIVE INCOME FOR THE YEAR 40 000

A LTD GROUP

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED

31 DECEMBER 20.6

Share capital

Retained earnings

Total

R

R

R

Balance at 1 January 20.6 100 000

96 000*

196 000 Changes in equity for 20.6

Total comprehensive income for the year Profit for the year 40 000

40 000

Balance at 31 December 20.6 100 000 136 000

236 000

* Only parent's interest due to the fact that the interest was acquired on 1 January 20.6

FAC2602 / Learning unit 4

54

A LTD GROUP

CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 31 DECEMBER 20.6

R

ASSETS

Non-current assets

Property, plant and equipment (160 000 + 180 000) 340 000

Current assets

Trade and other receivables (114 000 + 90 000) 204 000

Total assets 544 000

EQUITY AND LIABILITIES

Equity attributable to owners of the parent

Share capital 100 000

Retained earnings 136 000

Total equity 236 000

Current liabilities

Trade and other payables (178 000 + 130 000) 308 000

Total equity and liabilities 544 000

FAC2602 / Learning unit 4

55

EXAMPLE 2

Acquisition of a wholly-owned subsidiary at a premium

The following are the abridged statements of financial position of A Ltd and its subsidiary,

B Ltd, as at 31 December 20.6:

STATEMENTS OF FINANCIAL POSITION AS AT 31 DECEMBER 20.6

ASSETS

A Ltd

R B Ltd

R

Property, plant and equipment

Investment in B Ltd - 80 000 ordinary shares at fair value

(cost price: R148 000)

160 000

148 000

180 000

-

Trade and other receivables 90 000 90 000

398 000 270 000

EQUITY AND LIABILITIES

Share capital - ordinary shares (100 000/80 000 shares)

100 000

80 000

Retained earnings 120 000 60 000

Trade and other payables 178 000 130 000

398 000 270 000

A Ltd acquired its interest in B Ltd on 1 January 20.5, at which time B Ltd's retained earnings

amounted to R26 000. At the date of acquisition, consider the carrying amount of the assets

and liabilities of B Ltd to be equal to the fair value thereof.

STATEMENTS OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR

THE YEAR ENDED 31 DECEMBER 20.6

A Ltd

R B Ltd

R

Profit from operations 25 000 23 000

Dividends received from subsidiary 10 000 -

Profit before tax 35 000 23 000

Income tax expense (11 000) (7 000)

PROFIT FOR THE YEAR

Other comprehensive income for the year

24 000

- 16 000

-

TOTAL COMPREHENSIVE INCOME FOR THE YEAR 24 000 16 000

FAC2602 / Learning unit 4

56

STATEMENTS OF CHANGES IN EQUITY FOR THE YEAR ENDED 31 DECEMBER 20.6

Share capital Retained earnings

Total

A Ltd B Ltd A Ltd B Ltd A Ltd B Ltd

R R R R R R

Balance at 1 January 20.6 100 000 80 000 111 000 54 000 211 000 134 000

Changes in equity for 20.6 Total comprehensive income for the year Profit for the year 24 000 16 000 24 000 16 000

Dividend paid: ordinary (15 000) (10 000) (15 000) (10 000)

Balance at 31 December 20.6 100 000 80 000 120 000 60 000 220 000 140 000

REQUIRED

You are required to draft the consolidated statement of profit or loss and other

comprehensive income, the consolidated statement of changes in equity and the

consolidated statement of financial position at 31 December 20.6 in compliance with

the requirements of International Financial Reporting Standards.

FAC2602 / Learning unit 4

57

SOLUTION 2

Calculations

1. Analysis of owners' equity of B Ltd

At acquisition - 1 Jan 20.5

Share capital

Retained earnings

Equity represented by goodwill

- parent

Consideration Since acquisition

• To beginning of current year

Retained earnings

(54 000 31/12/20.5 -

26 000 1/1/20.5)

• Current year

Profit for the year

Dividend paid

Total A Ltd 100%

NCI

0% At Since

R

80 000

26 000

R

80 000

26 000

R R

106 000

42 000

106 000

42 000(1)

28 000(2)

16 000

(10 000)

148 000

28 000

16 000

(10 000)

148 000

182 000

148 000

34 000

2. Pro-forma consolidated journal entries

Dr

Cr

R

R

Share capital (B Ltd) 80 000

Retained earnings (B Ltd) 26 000

Goodwill 42 000(1)

Investment in B Ltd (A Ltd)

148 000

Elimination of owners' equity of B Ltd at acquisition

Dividend received (A Ltd) 10 000(4)

Dividend paid (B Ltd)

10 000

Elimination of intragroup dividend

FAC2602 / Learning unit 4

58

A LTD GROUP

CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE

INCOME FOR THE YEAR ENDED 31 DECEMBER 20.6

A LTD GROUP

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED

31 DECEMBER 20.6

R

Profit before tax (35 000 – 10 000(4) + 23 000) 48 000

Income tax expense (11 000 + 7 000) (18 000)

Profit for the year

Other comprehensive income for the year

(3)30 000

-

TOTAL COMPREHENSIVE INCOME FOR THE YEAR 30 000

Share

capital

R

Retained

earnings

R

Total

R

Balance at 1 January 20.6

Changes in equity for 20.6

Total comprehensive income for the year

Profit for the year

100 000

139 000#

(3)30 000

239 000

30 000

Dividends paid: ordinary (15 000) (15 000)

Balance at 31 December 20.6 100 000 154 000 254 000

# [111 000 + 28 000(2)]

FAC2602 / Learning unit 4

59

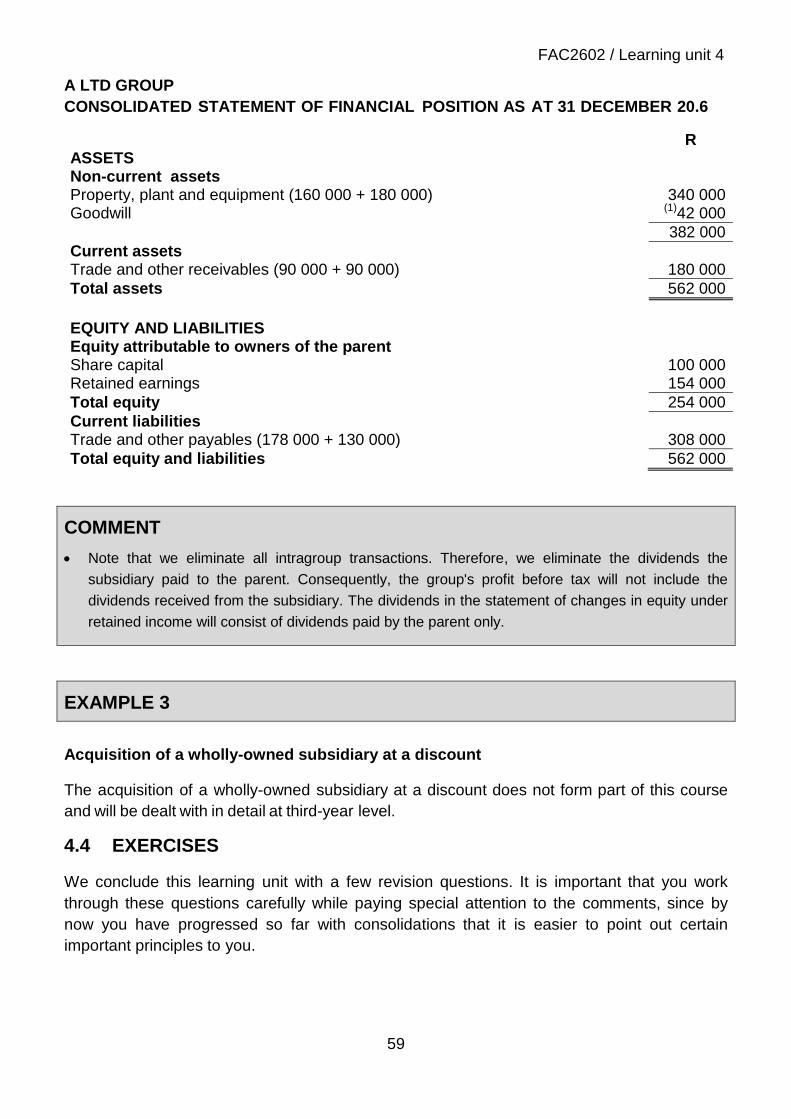

A LTD GROUP

CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 31 DECEMBER 20.6

R

ASSETS

Non-current assets

Property, plant and equipment (160 000 + 180 000) 340 000 Goodwill (1)42 000

382 000

Current assets

Trade and other receivables (90 000 + 90 000) 180 000

Total assets 562 000

EQUITY AND LIABILITIES

Equity attributable to owners of the parent

Share capital 100 000 Retained earnings 154 000

Total equity 254 000

Current liabilities

Trade and other payables (178 000 + 130 000) 308 000

Total equity and liabilities 562 000

COMMENT

Note that we eliminate all intragroup transactions. Therefore, we eliminate the dividends the

subsidiary paid to the parent. Consequently, the group's profit before tax will not include the

dividends received from the subsidiary. The dividends in the statement of changes in equity under

retained income will consist of dividends paid by the parent only.

EXAMPLE 3

Acquisition of a wholly-owned subsidiary at a discount

The acquisition of a wholly-owned subsidiary at a discount does not form part of this course

and will be dealt with in detail at third-year level.

4.4 EXERCISES

We conclude this learning unit with a few revision questions. It is important that you work

through these questions carefully while paying special attention to the comments, since by

now you have progressed so far with consolidations that it is easier to point out certain

important principles to you.

FAC2602 / Learning unit 4

60

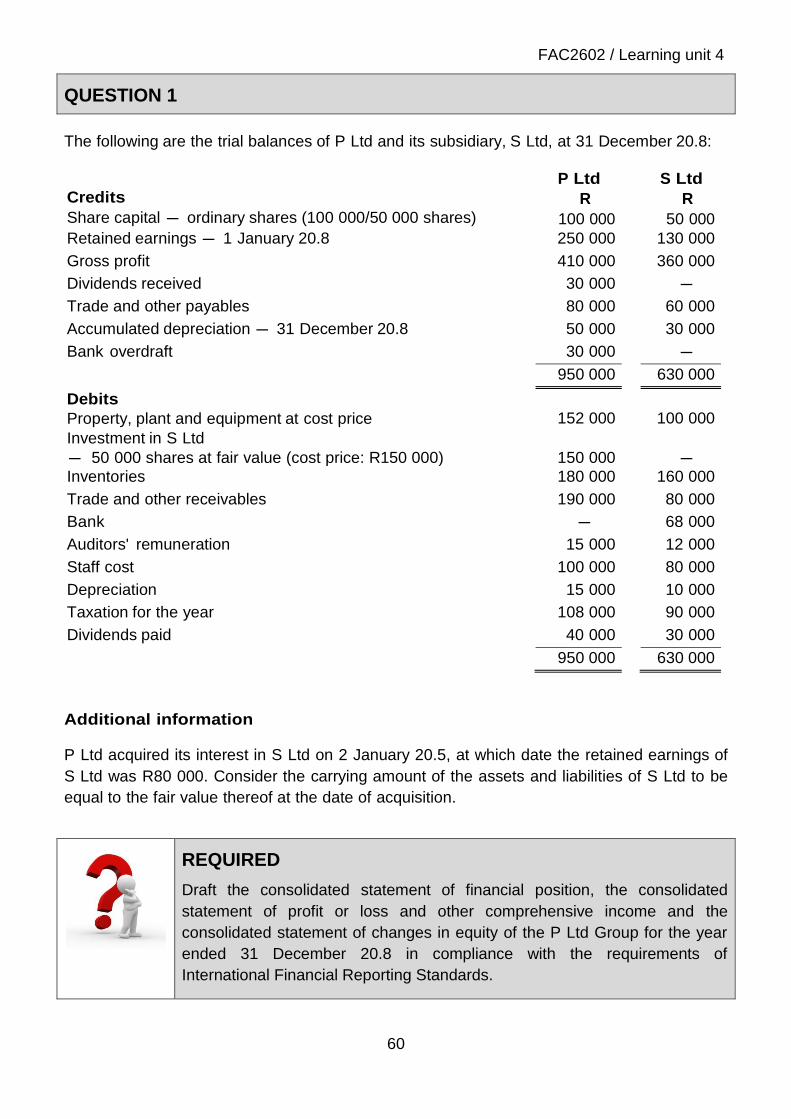

QUESTION 1

The following are the trial balances of P Ltd and its subsidiary, S Ltd, at 31 December 20.8:

Credits

Share capital - ordinary shares (100 000/50 000 shares)

P Ltd

R

100 000

S Ltd

R

50 000

Retained earnings - 1 January 20.8 250 000 130 000

Gross profit 410 000 360 000

Dividends received 30 000 -

Trade and other payables 80 000 60 000

Accumulated depreciation - 31 December 20.8 50 000 30 000

Bank overdraft 30 000 -

950 000 630 000

Debits

Property, plant and equipment at cost price

152 000

100 000

Investment in S Ltd

- 50 000 shares at fair value (cost price: R150 000)

150 000

-

Inventories 180 000 160 000

Trade and other receivables 190 000 80 000

Bank - 68 000

Auditors' remuneration 15 000 12 000

Staff cost 100 000 80 000

Depreciation 15 000 10 000

Taxation for the year 108 000 90 000

Dividends paid 40 000 30 000

950 000 630 000

Additional information

P Ltd acquired its interest in S Ltd on 2 January 20.5, at which date the retained earnings of

S Ltd was R80 000. Consider the carrying amount of the assets and liabilities of S Ltd to be

equal to the fair value thereof at the date of acquisition.

REQUIRED

Draft the consolidated statement of financial position, the consolidated

statement of profit or loss and other comprehensive income and the

consolidated statement of changes in equity of the P Ltd Group for the year

ended 31 December 20.8 in compliance with the requirements of

International Financial Reporting Standards.

FAC2602 / Learning unit 4

61

QUESTION 2

The following are the trial balances of A Ltd and its subsidiary, B Ltd, at 31 December 20.8:

Credits

A Ltd

R B Ltd

R

Share capital - ordinary shares (100 000/50 000 shares) 100 000 50 000

Retained earnings - 1 January 20.8 250 000 130 000

Gross profit 410 000 360 000

Dividends received 30 000 -

Trade and other payables 80 000 60 000

Accumulated depreciation - 31 December 20.8 50 000 30 000

Bank overdraft 30 000 -

950 000 630 000

Debits

Property, plant and equipment at cost price

152 000

100 000

Investment in B Ltd

- 50 000 shares at fair value (cost price: R150 000)

150 000 -

Inventories 180 000 160 000

Trade and other receivables 190 000 80 000

Bank - 68 000

Auditors' remuneration 15 000 12 000

Staff cost 100 000 80 000

Depreciation 15 000 10 000

Taxation for the year 108 000 90 000

Dividends paid 40 000 30 000

950 000 630 000

Additional information

A Ltd acquired its interest in B Ltd on 2 January 20.5, and at that date the retained earnings of