Exam Techniques for CIMA F2 Techniques for CIMA F2 ... Time management Application to F2 ... . 14

F2 Advanced Financial Reporting

Module: 08

Associates

1. Introduction

Inter-corporate investments

A business combination is where a parent will acquire 50% or more of the

shares in a subsidiary. However, this control-based classification can be

extended to other kinds of investment.

Using % ownership, inter-corporate investments can be classified as

financial assets, associates and business combinations. There is also

another classification known as a joint venture. The diagram shows how

these are broken down:

You'll note that a joint venture is a little different from the others as it's

typically where two or more entities have shared control of projects they are

working on together rather than joint ownership of company shares.

Group accounts – CIMA F1 to CIMA F2

Group accounting for associates is studied both in CIMA F1 and CIMA F2.

This chapter examines the basics of how to account for associates as

already studied in CIMA F1. If you're confident in this material, please feel

free to skim through it quickly as a recap. If it's been a while since your F1

exam, or you simply want to a recap of the basics before tackling the new

material then please do work through this chapter in full.

2. What is an associate?

Definition of associate

An associate is an entity over which the investor has significant influence

and which is neither a subsidiary nor an interest in a joint venture.

Significant influence

Significant influence is the power to participate in the financial and

operating policy decisions of the investee, but does not constitute

control or joint control over those policies.

To put it simply, if entity E was an investor in associate A, then E could turn up

to A's meetings to have a say, but E doesn't get the final say because they

lack the ownership to establish control.

IAS 28 states that this could be in the form of board representation,

participation in policy making etc. but for examination purposes,

significant influence is based on a percentage ownership of 20% to

50%.

3. Associates: accounting treatment

Equity accounting

As ownership for an associate is less than 50% it cannot be treated as a single

business entity (i.e. a group with a parent and subsidiary). Therefore, it cannot be consolidated. Consolidation requires line by line aggregation of

the parent and subsidiary financial statements (the acquisition method).

Instead, an associate is accounted for using the equity method. This is

less onerous than that used for subsidiaries as it only requires one new line

of entries in each of the financial statements those being:

• group share of net assets, and;

• group share of net income.

Rules

Let's take a look at some of the key rules for associate companies. We've

seen many of these rules for subsidiaries before, so the question is how we

deal with each of these key issues for associates. As you'll see it's a lot

easier!

Area Treatment

Intra-group balances and

transactions and

unrealised profits

The transactions themselves are not eliminated as

associates (as they were for subsidiaries).

However if there are unrealised profits those are

adjusted for.

Impairment of investment

value

If the value of the associate goes down, the

amount by which it is impaired is taken off of the

investment in the associate in the group's

accounts.

Associate profits &

dividends from associates

Dividends received from associates are excluded

from consolidated income statement and the

group's share of the associates profit is included

instead.

If you understand those rules you are doing very well! It can be hard to know

what's going on without seeing them applied to an example.

We'll cover each of these rules using examples throughout this chapter, but

let's start by considering an example of the last two of these three issues:

impairment of investment value and associate profits.

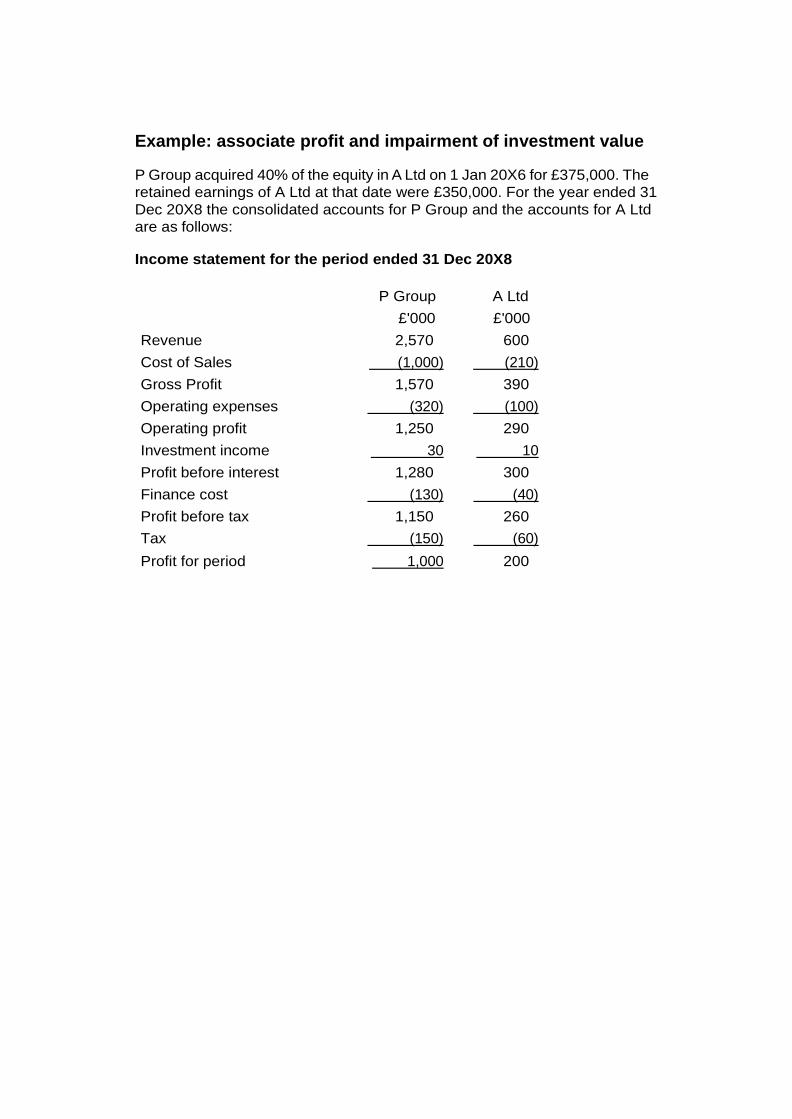

Example: associate profit and impairment of investment value

P Group acquired 40% of the equity in A Ltd on 1 Jan 20X6 for £375,000. The

retained earnings of A Ltd at that date were £350,000. For the year ended 31

Dec 20X8 the consolidated accounts for P Group and the accounts for A Ltd

are as follows:

Income statement for the period ended 31 Dec 20X8

P Group A Ltd

£'000 £'000

Revenue 2,570 600

Cost of Sales (1,000) (210)

Gross Profit 1,570 390

Operating expenses (320) (100)

Operating profit 1,250 290

Investment income 30 10

Profit before interest 1,280 300

Finance cost (130) (40)

Profit before tax 1,150 260

Tax (150) (60)

Profit for period 1,000 200

Statement of financial position as at 31 Dec 20X8

ASSETS

P Group

£’000

A Ltd

£’000

Non-current assets

Property, plant and equipment 2,000 600

Investment in associate 375 -

Current assets 100 300

2,475 900

EQUITY AND LIABILITIES

Equity

Share capital (£1 shares) 500 250

Retained earnings 1,875 550

2,375 800

Current liabilities 100 100

2,475 900

A Ltd paid a dividend of £50,000 in the year. P group's share of this is shown

as part of investment income in P Group.

The goodwill in A Ltd has impaired by 20% at the year end.

Prepare the consolidated statement of financial position and consolidated

income statement for P Group for the year end 31 Dec 20X8.

Answer

Method

Step 1. Share of profit of associate

For associates we recognise the share of the associate's profit in the

income statement, so the first step is to calculate the group share of the

associate’s profit after tax and add that to the income statement.

That increase is then shown as an increase in value of the investment in the

associate. In this case:

£’000 £’000

Associate profit after tax 200

Group share 40% 80

So we need to increase the investment in the associate by £80,000 to show

the investment has effectively gone up in value, and show an extra £80,000

of income. That extra income is shown both in the income statement and

also in the reserves (as the extra income is effectively transferred to

reserves at the end of the year).

You can see these amendments in step 1 in the consolidation matrix shown

later. It's worth taking a look at this now so you can see how the adjustment

works on the face of the financial statements.

Step 2. Dividend from associate

In step 1 we added in the share of profits of the associates. We have a

problem though. In the parent's accounts we've already shown some income

from the associate as dividends received. We're effectively double counting

and so these dividends need to be removed.

Next then, we eliminate the dividend received from the associate from

the P Group income statement, and reduce the carry value of the

investment in the associate by the same amount.

£’000 £’000

Associate dividend paid 50

Group share 40% 20

You can see this adjustment in step 2 in the consolidated matrix shown later.

You might wonder why the £20,000 dividend is taken off the investment in

this stage. In step 1 we added £80,000 of associate profit to the investment in

the associate. However of that £80,000, £20,000 has effectively already

been paid out as a dividend meaning the net increase in investment should

only be £60,000. Taking off the £20,000 here means that the net figure is

correctly shown.

Step 3. Goodwill impairment

The question noted that goodwill had impaired by 20%, meaning the value

had reduced by 20%.

The first thing to do here is calculate the goodwill on acquisition which is the

difference between the amount paid and the fair value of the equity

purchased (which we'll assume is the book value).

£’000 £’000

Consideration paid 375

Net assets acquired:

Share capital 250

Retained earnings at acq'n date 350

600

Group share (40% x 600 = 240) 40% (240)

Goodwill on acquisition 135

According to the question impairment is 20% of this value = £27,000.

This is recognised as a loss in the income statement in the year, as the value

of the asset has reduced. The carry value of the investment in the associate is

also marked down.

DR Operating expenses £27,000

CR Investment in associate £27,000

Note that since the profit fell by £27,000 the retained earnings also fell too,

and that's also adjusted for in this step in the statement of financial position.

You can see this adjustment in step 3 in the consolidated matrix shown later.

Step 4

An easy step to finish.

Incorporate the associate into the group accounts by taking the parent's

statements and adding the amendments as per steps 1 to 3.

Note that there's no need to add anything from the associate, so this is

different from what we did with subsidiaries.

Consolidation matrix: Income statement

P Group

Earnings

Step 1

Dividend

Step 2

Goodwill

Step 3

Step 4

P Group

£'000 £'000 £'000 £'000 £'000

Revenue 2,570 2,570

Cost of Sales (1,000) (1,000)

Gross Profit 1,570 1,570

Op. expenses (320) (27) (347)

Op. profit 1,250 1,223

Inv income 30 (20) 10

PBIT 1,280 1,233

Finance cost (130) (130)

Share of

1,150 1,103

associate 80 80

Profit Before Tax 1,150 1,183

Tax (150) (150)

Profit After Tax 1,000 1,033

Consolidation matrix: SoFP

Goodwill Dividend Earnings

Step 1 Step 2 Step 3 Step 4

P Group

(W1) (W2) (W3) P Group

ASSETS

£’000 £'000 £'000 £'000 £'000

Non-current assets

PPE 2,000 2,000

Inv in associate 375 80 (20) (27) 408

Current assets 100 100

2,475 2,508

EQUITY AND LIABILITIES

Equity

Share capital 500 500

Retained earnings 1,875 80 (20) (27) 1,908

2,375 2,408

Current liabilities 100 100

2,475 2,508

Let's sum up our final consolidated statements with supporting notes.

P Group: Consolidated Income Statement for period end 31 Dec 20X9

P Group

£'000

Revenue 2,570

Cost of Sales (1,000)

Gross Profit 1,570

Operating expenses (347)

Operating profit 1,223

Investment income 10

Finance cost (130)

Share of associate 80

Profit before tax 1,183

Tax (150)

Profit for the period 1,033

P Group: Consolidation Statement of financial position as at 31 Dec 20X9

P Group

ASSETS

£'000

Non-current assets

Property, plant and equipment 2,000

Investment in associate (note 1) 408

Current assets 100

2,508

EQUITY AND LIABILITIES

Equity

Share capital 500

Retained earnings (note 2) 1,908

2,408

Current liabilities 100

2,508

The following notes simply show the workings we calculated earlier in the

consolidation matrix but in a neat tabular format. There are no new

calculations here for you to get your head around, although you might want to

double check that you understand each line to confirm your understanding

of our earlier calculations.

Note 1: Investment in associate

£’000 £’000

Cost of investment 375

Retained earnings of associate at

year end

550

Retained earnings at acquisition (350)

20

0

Share of post-acquisition profits 40% 80

Dividend received

(20)

Impairment of goodwill (27)

Investment in associate 408

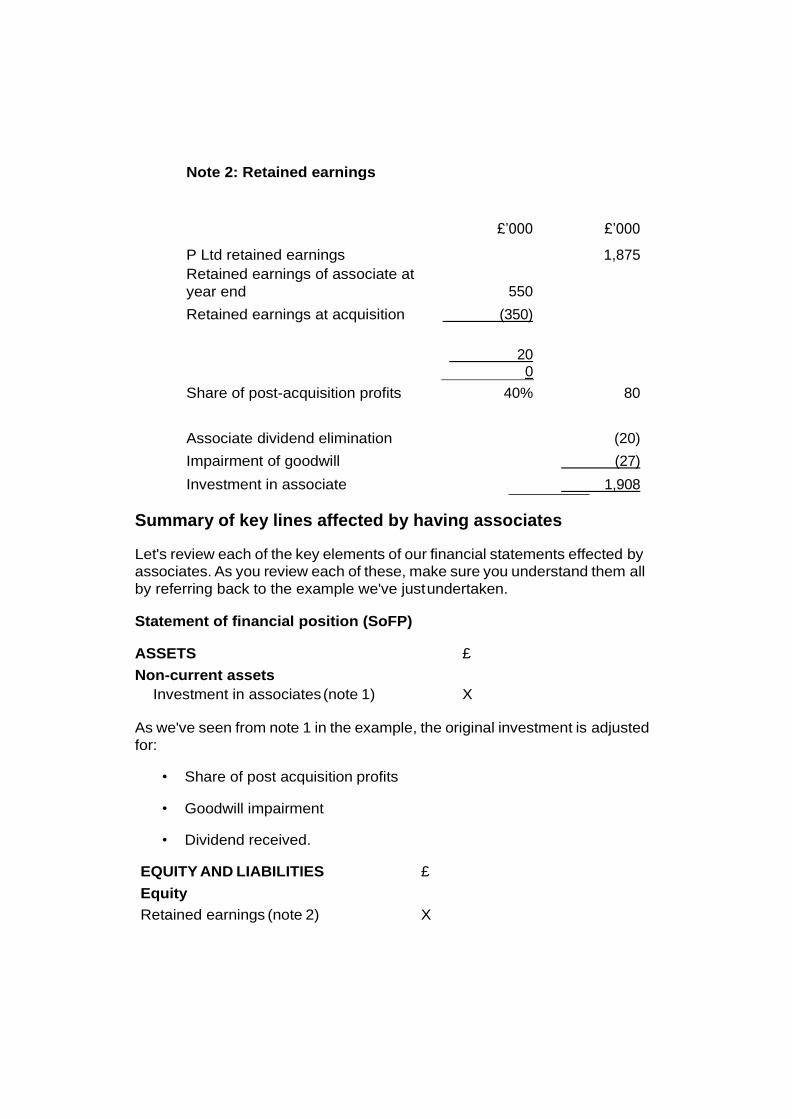

Note 2: Retained earnings

£’000

£’000

P Ltd retained earnings 1,875

Retained earnings of associate at

year end

550

Retained earnings at acquisition (350)

20

0

Share of post-acquisition profits 40% 80

Associate dividend elimination

(20)

Impairment of goodwill (27)

Investment in associate 1,908

Summary of key lines affected by having associates

Let's review each of the key elements of our financial statements effected by

associates. As you review each of these, make sure you understand them all

by referring back to the example we've just undertaken.

Statement of financial position (SoFP)

ASSETS £

Non-current assets

Investment in associates (note 1) X

As we've seen from note 1 in the example, the original investment is adjusted

for:

• Share of post acquisition profits

• Goodwill impairment

• Dividend received.

EQUITY AND LIABILITIES £

Equity

Retained earnings (note 2) X

As we've seen from note 2 in the example, the original retained earnings are

also adjusted for:

• Share of post acquisition profits

• Goodwill impairment

• Dividend received.

Statement of comprehensive income (CIS)

Profit or loss

£

Share of associate X

This is calculated using:

£ £

Retained earnings of associate at year end X

Less: Retained earnings at acquisition (X)

X

Share of post-acquisition profits

(multiply by % owned)

X% X

‘Investment income’ is also adjusted to take out any dividends received

during the period. This is calculated as:

£

Investment income X

Associate dividends received (X)

X

4. Trading with associates: unrealised profit

Unrealised profit adjustment

Hopefully you remember that intra-group transactions are not allowed for

subsidiaries and are reversed out.

The treatment for associates is slightly different. The transactions

themselves are allowed for associates and do not need to be reversed,

but the investor's share in any unrealised profits does need to be

removed.

These rules are given in IAS 28 which states that: unrealised profits on

trading between the group and associate (A) should be removed based

on the investor’s share (i.e. the % owned by parent, P). This is given by:

Unrealised profit adjustment (PUPA) = A% x unrealised profit

How the unrealised profit adjustment is applied is dependent on whether the

parent (P) or the associate (A) is the seller and where the profit is made. In

the case of an inventory sale this would be:

Scenario Unrealised profit Overstated inventory

P sells to A In P’s books In A’s books

A sells to P In A’s books In P’s books

Treatment of unrealised profit: Parent sells to Associate

Let's say a parent sells a £100 item it makes £50 profit on. If the associate

then sells that product on, say for £120, it makes a further £20, and the

group as a whole makes £70. That's fine and no adjustment is needed

because the total group profit of £70 is fully realised. There is no 'unrealised

profit'.

What if the associate did not sell the item though? The parent has a £50

profit which is 'unrealised'. It's not a true profit. What's actually happened is

that that purchased item was carried over in the associate's closing inventory

and that's caused the profit for the group to be too high.

If the associate is 20% owned the adjustment made is then £10 (£50 x 20%).

Here are the adjustments needed:

DR Group cost of sales £10

CR Investment in associate £10

Cost of sales is increased to reduce the profits, and the investment in the

associate reduced to reflect the fact that inventory was too high.

Note that the reserves in the statement of financial position are also lower too

(as the profits were lower) so these need to be reduced by £10 too.

Example – Unrealised profits

P Ltd owns 30% of A Ltd. P Ltd has sold £200,000 worth of goods to A Ltd at a

price which is at a 25% mark-up i.e. price paid by A is £250,000 (£200,000 x

125/100).

50% of these items remained unsold at the end of the year. What is the

impact on the cost of investment in A Ltd in the year end Consolidated

Statement of Financial Position?

Answer

Profit on the sale = £50k (£250k- £200k).

Profit element in inventory of associate = £25k (= 50% x £50k).

This is the unrealised profit (PUP).

P Ltd’s share of the PUP is £7.5k (= 30% x £25k). This is the unrealised profit

adjustment that is required in the consolidated accounts. The unrealised

profit adjustment aims to reduce the group retained earnings and the carry

value of the associate due to the overstated inventory.

Consolidated Statement of Financial Position adjustment:

Reduce group retained earnings by £7,500

Reduce investment in associate by £7,500

Treatment of unrealised profit: Associate sells to Parent

If the sale is the other way around, the associate selling to the parent, and

again the inventory is unsold at the year end, then the unrealised profit

adjustment aims to reduce the profit made unfairly by the associate and

also reduce the overstated group inventory.

DR Share of associate’s profit

CR Group inventory

Let's see this in action using the same example as before.

Example - Impact on financial statements

Using the same example as before, what is the impact on the cost of

investment in A Ltd in the year end Consolidated Statement of Financial

Position if A Ltd made the sale to P Ltd?

Answer

In this case, the profit element would be included in A Ltd’s books and P Ltd

would hold the overstated inventory. The unrealised profit adjustment aims to

reduce the profit made from the associate and reduce the overstated group

inventory.

The unrealised profit adjustment (PUPA) remains the same at £7,500 but the

adjustment is different.

Reduce group retained earnings by £7,500

Reduce group inventory by £7,500

The cost of investment in A Ltd is not affected by the unrealised profit

adjustment.

5. Summary rules

At the start of the chapter we covered the key rules for associate companies.

Let's review these again. Hopefully in hindsight you'll understand each of

these a little better now than when we first presented them. If not then you'll

need to review the various sections again to ensure you are fully on top of

them.

Area Treatment

Intra-group balances and

transactions and

unrealised profits

The transactions themselves are not eliminated as

associates (as they were for subsidiaries).

However if there are unrealised profits those are

adjusted for.

Impairment of investment

value

If the value of the associate goes down, the

amount by which it is impaired is taken off of the

investment in the associate in the group's

accounts.

Associate profits &

dividends from associates

Dividends received from associates are excluded

from consolidated income statement and the

group's share of the associates profit is included

instead.

Subsidiary vs Associates – apply the right set of rules

As you've seen throughout this chapter, associates are treated very

differently from subsidiaries. When you are doing questions your first key

step must always be to identify whether the company is a subsidiary (>50%

ownership) or an associate (20%-50% ownership) so that you then apply the

correct rules.

Practise questions

Group accounting is a complicated topic. On the positive side it's just follows

a set of rules that if you learn and apply systematically are the same each

time. Make sure you learn the rules carefully therefore and then practise as

many questions as you can. That way you should then find this complex

topic becomes one you fully understand and can do well in your exam.

6. Chapter summary

• An associate relationship exists where there is significant influence.

This is indicated where a parent holds between 20% and 50% of the voting shares. Associates are accounted for using the equity method.

This requires only presenting the share of net assets and profits.

• Significant influence is the power to participate in the financial and

operating policy decisions. Significant influence is presumed (for examination purposes) where a parent holds 20% to 50% of voting

shares.

• Associate is not a group member (ownership below 50%) therefore

cannot be consolidated using the acquisition method.

• An associate is accounted for by using the equity method. This

requires:

◦ a one line entry in the statement of financial (‘investment in

associate’) and

◦ two lines in the statement of comprehensive income (‘share of

associate’ and ‘share of associate’s other comprehensive

income’).

• ‘Investment in associate’ is shown as a non-depreciating non-current

asset. It is calculated as cost of the investment plus the share of the

post acquisition profits less impairment losses.

• ‘Share of associate’ is shown before group profit before tax. It is

calculated as associate’s profit for the year x group % less the

associate’s impairment to date.

• The following rules apply when using the equity method:

◦ Do not cancel:

▪ Intra-group balances and transactions.

◦ Eliminate:

▪ Unrealised profits;

▪ Dividends from associate.

◦ Adjustments:

▪ Fair value adjustments are made where associate's net assets

are not at fair value;

▪ Group reserves: add the group share of the post-acquisition

profit;

▪ Impairment (e.g. goodwill in share of associate).

• Key reporting standard guiding accounting treatment is IAS 28

(Investments in Associates and Joint Ventures).