F. Gori - INVESTMENTS AND TARGETS CHANGING THE GAME

28

INVESTMENTS AND TARGETS CHANGING THE GAME Francesco Gori Chief Operating Officer

-

Upload

pirelli-official-slideshare-network -

Category

Investor Relations

-

view

322 -

download

0

Transcript of F. Gori - INVESTMENTS AND TARGETS CHANGING THE GAME

INVESTMENTS AND TARGETS CHANGING THE GAME

Francesco GoriChief Operating Officer

2

AGENDA

INVESTMENT ALLOCATION

TYRE MARKET VALUE

PLAN ORGANIZATION: A TIGHT MATRIX

PIRELLI BY REGION

TYRE MARKET VOLUME AND INDUSTRY INVESTMENTS

STRATEGY IMPLEMENTATION

PIRELLI TARGETS BY MATRIX

“WHAT IF” CONTINGENCY PLANS

3

WORLD TYRE MARKET TREND

Source: Tire Business reports for 2000-2009

+9%+9%

-10.0%-10.0%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

70 6972

8093

103112

128

140

126

4

CAGR

$/bln

Michelin

Bridgestone

Goodyear

WORLD MARKET SHARE TREND

Source: Tire Business reports for 2000-2009

70 69 7280

93

112

128

140

126

-

20

40

60

80

100

120

140

2000 2001 2002 2003 2004 2005 2006 2007 2008 20090%

5%

10%

15%

20%

25%

Market Share %

5

$/bln

Total Market

-5.8

-3.4

-3.4

Continental -0.7

Pirelli +0.7

WORLD TYRE MARKET: 5-YEAR FORECAST

Source: 2010-2015 Global Insight, Pirelli Estimates

>190

10%10%

+7%+7%

2009 2010 2011 2012 2013 2014 2015

126140 ~150

6

$/bln

Total Market

CAGR

PIRELLI ESTIMATES MATCH INDUSTRY ANNOUNCEMENTS IN THE TYRE MARKET FOR CARS

7

~50% ~20%~30%

In 2015, China will represent

~20% of world capacity

2011-2015 ADDITIONAL INDUSTRY CAPACITY

CAGR

1.5

+3.6%+3.6%+4.7%+4.7%

CAR TYRES

LATAM+APAC

EMEA+NAFTA

bln/pieces

1.2

1.4

46%44%

2010 2013

2015

Source: Global Insight, Pirelli Estimates

+6.6%

+2.3%+2.3%

No foreseen overcapacity

China India Others Total

56% 54%

41%

59%

~300 mln pcs Net Capex for 15 $/bln

(-30 mln pcs divested)

Source: Pirelli Estimates based on tyre manifactures announcements

AND FOR TRUCKS

8

~40%~40%

~20%

~40 mln pcs Net Capex for 10 $/bln

(-2 mln pcs divested)

China India Others Total

No foreseen overcapacity

+5.3%+5.3%

+6.2%+6.2%

mln/pieces (All Steel)

2010 2013 2015+7.5%

+2.1%+2.1%

124

70%

148

164

2011-2015 ADDITIONAL INDUSTRY CAPACITYTRUCK TYRES

LATAM+APAC

EMEA+NAFTA

In 2015, China will represent

~50% of world capacity

30%

67%

73%

27%33%

CAGRSource: Global Insight, Pirelli Estimates Source: Pirelli Estimates based on tyre manifactures announcements

2010 2013

2015

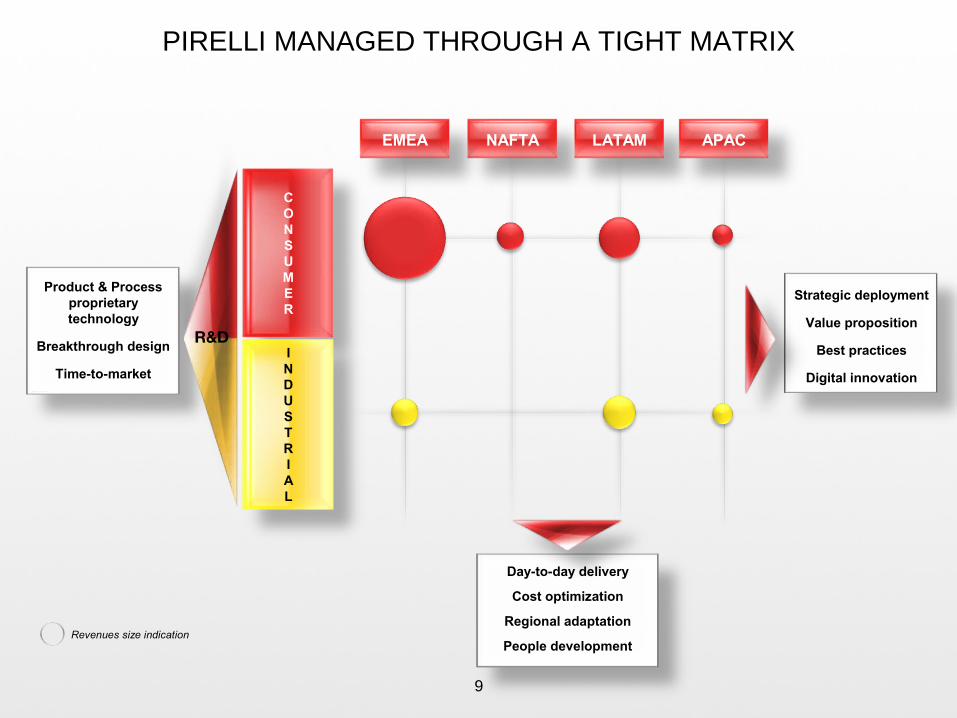

PIRELLI MANAGED THROUGH A TIGHT MATRIX

Strategic deployment

Value proposition

Best practices

Digital innovation

9

EMEA NAFTA LATAM APAC

Product & Process proprietary technology

Breakthrough design

Time-to-market

Day-to-day delivery

Cost optimization

Regional adaptation

People developmentRevenues size indication

CONSUMER

INDUSTRIAL

R&D

PIRELLI STRATEGIC IMPLEMENTATION

10

EMEA NAFTA LATAM APAC

Improve focus

Streamline operations

Increase efficiency

Keep lean

Improve scale economies

Stay regional

Time-to-market and Premium customization

Platform and component

standardization

Innovative material

solutions and processing

Revenues size indication

CONSUMER

INDUSTRIAL

R&D

KEY LEVER WILL BE THE INCREASE IN PIRELLI INVESTMENT RATE

1.2 0.7

15 11

1.35

1.4(net)

11

Capex (€/bln)

Additional capacity (mln pieces)

2011-13 2014-152006-10

INVESTMENT ALLOCATIONINVESTMENTS

Consumer

Industrial

14% 56%

3% 27%

MatureLATAM &

RDE

EMEA MARKET GROWTH AND PIRELLI STRATEGY

12

EBIT margin:

from mid-single digit to double digit by 2013

80%

464 484 501

81%

452

2.1%2.1%

Consumer Tyre Market (Car)

mln/pieces

OE

Repl.

2011 2013 20152010

19% 20%

80% 80%

87% 83%

29 30 3335

3.7%3.7%

83%87%

Industrial Tyre Market (Truck)

mln/pieces

OE

Repl.

2011 2013 20152010

13% 17%

Focus on premium fast growing segments

Consolidate leadershipin the Motorbike segment

Russia production focused on Winter

Selective approach to OEM

Low cost/premium capacity increase

Further cost efficiencies

Source: Global Insight, Pirelli Estimates

Pirelli Revenue Growth

MEA

EU

+6%+6%

2,5002,800

21%2,35020%

€/mln

2011E 2013E2010E

2,10019%

2009A

20%

13% 17%

20% 20%

79%81% 80% 80%

EMEA EBIT INDEX BRIDGE 2010-2013

Depreciation/ others

EfficienciesPrice/mix Raw materials

& cost of inputs

Volume EBIT 2013EBIT 2010

index “200”(30)

100

90

index “100”50

(110)

13

Index”100” = EBIT EMEA 2010

Focus on Premium Consumer segments

Focus on specialized dealer channel

Volume and Premium mix growth supported by new plant in Mexico

M/H Truck tyre sales restricted to Mexico

Selective approach to European OEM transplants

Strong brand appreciation from end-users as shown by 2010 JD Power study with Pirelli best OE tyre in the performance/sport segment

NAFTA MARKET GROWTH AND PIRELLI STRATEGY

14

EBIT margin:from single digit to

double digit by 2013

2.6%2.6%

22 23 2421

83% 80% 79%84%

Industrial Tyre Market (Truck)

2011 2013 20152010

OE

Repl.

mln/pieces

16% 17% 20% 21%

81% 81% 81%82%

3.0%3.0%

334 354 370318

Consumer Tyre Market (Car)

2011 2013 20152010

OE

Repl.

mln/pieces

18% 19% 19% 19%

Source: Global Insight, Pirelli Estimates

410 440

Pirelli Revenue Growth

2011E 2013E2010E

335

2009A

+8%(+10% in

USD)

+8%(+10% in

USD)520

€/mln

€/$ 1.33 in 2010; 1.40 in 2011/13

YUCATAN

CHIAPAS

TABASCOCAMPECHE

AGS.

SONORACHIHUAHUA

BA

JA C

ALIFO

RN

IA N

OR

TE

BA

JA C

ALIFO

RN

IA SU

R

SIN

ALO

A

DURANGO

NAYARIT

ZACATECAS TAMPS.

VERACRUZ

COLIMA

GUERREROOAXACA

JALISCO

COAHUILA

Nuevo

Leon

MEXICO CITY

BUILDING A PLATFORM FOR GROWTH IN NAFTA

Estabilishment of a new plant in Mexico with a yearly production capacity of ~5 mln car tyres by 2015

100% Premium tyres Dedicated to serve NAFTA countries, in

particular the USA

Key benefits

Better service and lower delivery times to NAFTA clients

Competitive manufacturing costs Lower logistic costs and no import duties

Key Investment returns Initial investment: 210 mln USD Value accretive already < 2013

15

NAFTA corridor

LATAM MARKET GROWTH AND PIRELLI STRATEGY

16

Regional Profitability:

no significant change (mid two-digit)

76%76%

10

77%77%

1112

14

6.8%6.8%

2011 2013 20152010

Industrial Tyre Market (Truck)

mln/pieces

OE

Repl.

23% 23% 24% 24%

6.5%6.5%

7889 98

72

73% 74% 74%73%

2011 2013 20152010

Consumer Tyre Market (Car)

mln/pieces

OE

Repl.

27% 27% 26% 26%

Consolidate Regional leadership

Keep expanding Pirelli exclusive tyre dealer network in best locations

Exploit growing Premium OEM fitments’ pull-through on after market sales

Increase local-for-local content

Source: Global Insight, Pirelli Estimates

>1.7

>2.2>1.8

2011E 2013E2010E

Pirelli Revenue Growth

1.33

2090A

€/$ 1.33 in 2010; 1.40 in 2011/13

+10%(+11% in

USD)

+10%(+11% in

USD)

€/bln

brand, dealer exclusivity and product range

an historical presence in terms of local production

a leading market share in all business segment

LATAM

0.9

2005 2007 2009

1.2 1.3

2010E

1.7

… and over 11,000 employees

Campinas

7 plants

Santo André

Gravatai

Sumaré

No.1 BrandTop-of-mind brand in MercosurElected no. 1 brand in all sectors

Strongest dealers network

Best rangeNo. 1 local OEM strategic supplierThe only full range player: from 2 wheels to

Truck to Agro

17

A success story of regional leadership, with sales exceeding 1.7 bln €

#1 #1 #1 #1

Feira de Santana

Merlo

Guacara

€/bln

ASIA – PACIFIC MARKET GROWTH AND PIRELLI STRATEGY

Focus on China Premium consumer market

OEM selection among premium (EU transplants)

Leverage on F1 to enhance brand awareness across the region

China factory becoming high-end full range: Truck, Car, Moto, Steelcord

Export hub also for MEA and Nafta markets (not only APAC)

Regional Profitability:

from single digit to double digit by 2013

18

OE

Repl.

mln/pieces

55%

55%

7.2%7.2%

412474

536

378

2011 2013 20152010

54%54%

Consumer Tyre Market (Car)

46% 46% 45% 45%

mln/pieces

OE

Repl.80%

79%78%

63

81%

8091

69

7.6%7.6%

2011 2013 20152010

Industrial Tyre Market (Truck)

19% 20% 21% 22%

Source: Global Insight, Pirelli Estimates

€/mln

2011E 2013E2010E

270

470

310

Pirelli Revenue Growth

2009A

231

+20%(+22% in

USD)

+20%(+22% in

USD)

€/$ 1.33 in 2010; 1.40 in 2011/13

DEVELOPING PIRELLI PRESENCE IN THE CHINESE MARKET

Planned investments will raise Pirelli capacity to serve the fast

growing Chinese mkt

Truck tyres Car tyres

+40%

+100%

19

Optimal location: half way between seaside and metropolitan areas

Competitive labor cost

Competitive energy cost

Additional capacity by 2013

Largest and best located industrial compound among tyre peers

STRATEGIC SOURCING: FOUR KEY DIRECTIONS

Source: SICOM, oilnergy.com

20

GETTING CLOSER TO NATURAL RUBBER PLANTATIONS

OPEN INNOVATION WITH KEY SYNTHETIC RUBBER PLAYERS

DEVELOPING NEW BIOMATERIALS REPLACING NON-GREEN ONES

INCREASING STEEL CORD PRODUCTION TO MAINTAIN VERTICALIZATION

Brazil

Turkey

Cina

Romania

BrazilBrazil

Brazil

Italy

Germany

Russia Cina

Japan

Liberia

Vietnam

Indonesia

'2007 QI/08 QII/08 QIII/08 QIV/08 QI/09 QII/09 QIII/09 QIV/09 QI/10 QII/10 QIII/10 QIV/10

RAW MATERIAL TREND ASSUMPTION

NATURAL RUBBER

SYNTHETIC RUBBER

21

Avg 2007 = 100

SBR

2,060 $/ton

'2007 QI/08 QII/08 QIII/08 QIV/08 QI/09 QII/09 QIII/09 QIV/09 QI/10 QII/10 QIII/10 QIV/10

Avg 2007 = 100

TSR 20

2,153 $/ton

-200 -300

2011 2011-2013

Input costs headwind

Efficiencies vs 2010 ~+200+80

* *

* Raw materials cost variance vs 2010

Source: SICOM, CMAI

€/mln

PIRELLI PROFITABILITY TARGETS BY REGION

>40%>30%

>20%>30%

Rebalanced profitability between Regions

RDE (Except LATAM)

LATAM

MATURE

2010E 2013E 2015E

22

>50%

<20%

<30% <40% >30%

PIRELLI TARGETS BY SEGMENTS

€/Bln

> 6.0

> 4.7> 5.1

Ind.

Cons.

8%8%

32%32%

31%

2013E2010E 2011E 2013E2010E 2011E

>8.5%

9÷10%

11÷12%

30%

31%

33%Ind.

Cons.

Volumes +4% +5%

Price/Mix +4% +3%

23

PBIT (Post Restr.)Revenues

4.0

29%

2009A 2009A

7.7%

33%

2011 vs 2010

CAGR2010-2013

71% 69%68%

68%

67% 67%69%

70%

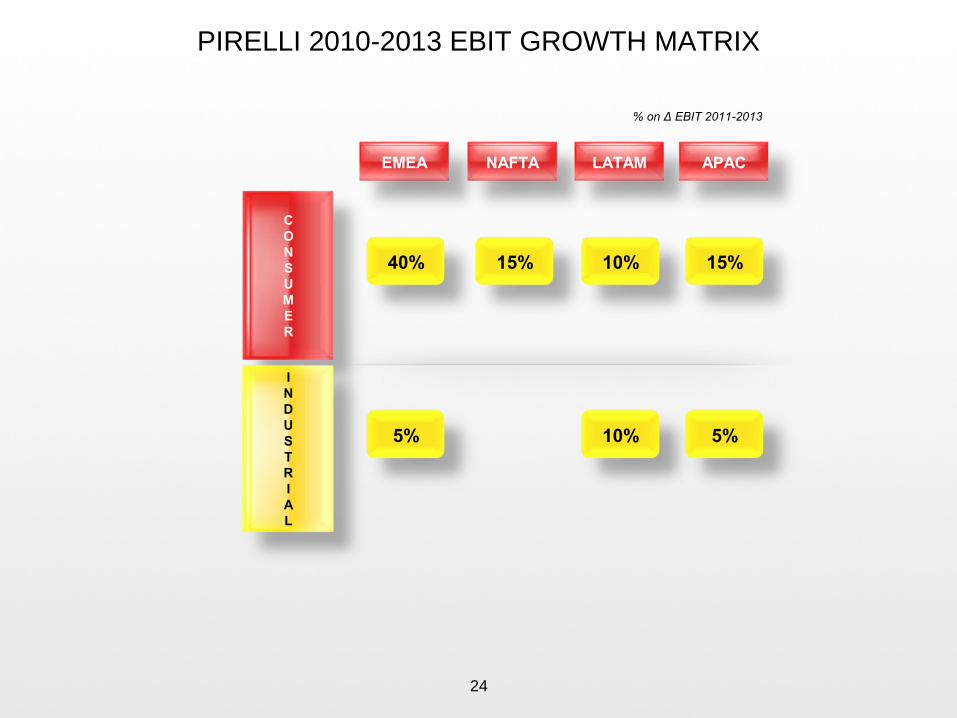

PIRELLI 2010-2013 EBIT GROWTH MATRIX

40% 15% 10% 15%

5% 10% 5%

24

% on Δ EBIT 2011-2013

EMEA NAFTA LATAM APAC

CONSUMER

INDUSTRIAL

TYRE EBIT INDEX BRIDGE 2010-2013

25

Index”100” = EBIT 2010

Depreciation/ others

Raw materials

& cost of inputs

EfficienciesPrice/mixVolume EBIT 2013EBIT 2010

Index “160”

Index “100”

40 (20)

60

70 (90)70

“WHAT IF” CONTINGENCY PLANS

If demand were to fall below our scenarios, a portfolio of contingency plans is ready

Decelerate investment programs

Reduce output and launch additional

restructuring

26

By region, if demand slowdown is localized

By segment, if cycle penalizes either B2B and/or B2C

Pirelli exposure to RDE markets softening volume reduction

Output contingent reduction in high-cost factories

Additional restructuring in higher cost factories

Program costs freeze as successfully implemented in 2009

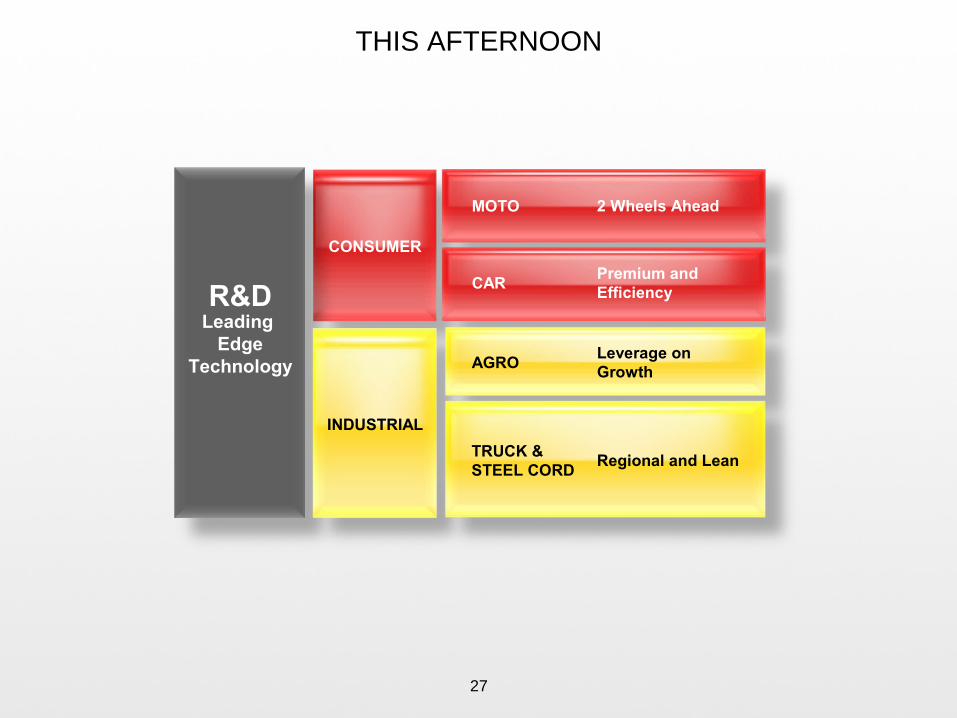

THIS AFTERNOON

27

Leading Edge

Technology

CONSUMER

R&D

INDUSTRIAL

MOTO 2 Wheels Ahead

CARPremium and Efficiency

AGROLeverage on Growth

TRUCK & STEEL CORD

Regional and Lean

DISCLAIMER

28

This presentation contains statements that constitute forward-looking statements based on Pirelli & C SpA’s current expectations and projections about future events and does not constitute an offer or solicitation for the sale, purchase or acquisition of securities of any of the companies mentioned and is directed to professionals of the financial community. These statements appear in a number of places in this presentation and include statements regarding the intent, belief or current expectations of the customer base, estimates regarding future growth in the different business lines and the global business, market share, financial results and other aspects of the activities and situation relating to the Company. Such forward looking statements are not guarantees of future performance and involve risks and uncertainties, and actual results may differ materially from those expressed in or implied by these forward looking statements as a result of various factors, many of which are beyond the ability of Pirelli & C SpA to control or estimate precisely. Consequently it is recommended that they be viewed as indicative only. Analysts are cautioned not to place undue reliance on those forward looking statements, which speak only as of the date of this presentation. Pirelli & C. SpA undertakes no obligation to release publicly the results of any revisions to these forward looking statements which may be made to reflect events and circumstances after the date of this presentation, including, without limitation, changes in Pirelli & C. SpA business or acquisition strategy or to reflect the occurrence of unanticipated events. The Manager mandated to draft corporate accounting documents of Pirelli & C. SpA. Francesco Tanzi, attests – as per art.154-bis. comma 2 of the Testo Unico della Finanza (D.Lgs. 58/1998) – that all the accounting information contained in this presentation correspond to the documented results, books and accounting of the Company.