External financial reporting and management information: a survey of U.K. management accountants

21

Management Accounting Research , 1996, 7, 73–93 External financial reporting and management information: a survey of U.K. management accountants Nathan Joseph,* Stuart Turley,* John Burns,* Linda Lewis,† Robert Scapens* and Alan Southworth* The interaction between external financial reporting requirements and management information has been a topic of debate both in the literature of management accounting, associated with the ideas of ‘relevance lost’, and in the literature of accounting regulation, where managerial action has been seen as one source of potential economic consequences. This paper presents the results of a postal questionnaire survey which collected the views of professionally qualified man- agement accountants working in U.K. industrial and commercial firms. The paper documents the results from the survey on issues such as the respondents’ beliefs about the influence of requirements for external financial accounting reports on internal systems design and decision-making within organizations. The paper also presents findings on areas of regulatory change having greatest impact on U.K. companies and reporting of information within these organizations. The survey is an initial part of a larger study in which the primary investigation is being undertaken through longitudinal case studies within a number of U.K. companies. ÷ 1996 Academic Press Limited Key words: survey; U.K. management accountants; external financial reporting; internal accounting; relevance lost; accounting regulation. 1. Introduction In recent years, there has been much interest in the impact of external financial reporting on the internal (management) accounting and decision making processes of companies. Kaplan (1984, p. 409) suggested that ‘the internal management accounting function has now become subservient to the external financial reporting function in U.S. firms’. From this perspective, it is claimed that generally accepted accounting practices which were primarily developed for periodic external reporting appear to dominate internal accounting—at least as far as U.S. firms are concerned. Indeed, it has been suggested that this dominance of external reporting has ef fectively reduced innovation in management accounting (Kaplan, 1984). In addition, from a financial reporting perspective, there has been an interest in the possible economic consequences of accounting regulation through information inductance ef fects on management decisions (Prakash and Rappaport, 1977; Zef f, * Department of Accounting and Finance, University of Manchester, Manchester, U.K., correspondence to N. Joseph. † Shef field University Management School. 10455–5005 / 6 / 010073 1 21 $18.00 / 0 ÷ 1996 Academic Press Limited

-

Upload

nathan-joseph -

Category

Documents

-

view

213 -

download

1

Transcript of External financial reporting and management information: a survey of U.K. management accountants

Management Accounting Research , 1996 , 7 , 73 – 93

External financial reporting and management information : a survey of U .K . management accountants

Nathan Joseph ,* Stuart Turley ,* John Burns ,* Linda Lewis , † Robert Scapens* and Alan Southworth*

The interaction between external financial reporting requirements and management information has been a topic of debate both in the literature of management accounting , associated with the ideas of ‘relevance lost’ , and in the literature of accounting regulation , where managerial action has been seen as one source of potential economic consequences . This paper presents the results of a postal questionnaire survey which collected the views of professionally qualified man- agement accountants working in U . K . industrial and commercial firms . The paper documents the results from the survey on issues such as the respondents’ beliefs about the influence of requirements for external financial accounting reports on internal systems design and decision-making within organizations . The paper also presents findings on areas of regulatory change having greatest impact on U . K . companies and reporting of information within these organizations . The survey is an initial part of a larger study in which the primary investigation is being undertaken through longitudinal case studies within a number of U . K . companies .

÷ 1996 Academic Press Limited

Key words : survey ; U . K . management accountants ; external financial reporting ; internal accounting ; relevance lost ; accounting regulation .

1 . Introduction

In recent years , there has been much interest in the impact of external financial reporting on the internal (management) accounting and decision making processes of companies . Kaplan (1984 , p . 409) suggested that ‘the internal management accounting function has now become subservient to the external financial reporting function in U . S . firms’ . From this perspective , it is claimed that generally accepted accounting practices which were primarily developed for periodic external reporting appear to dominate internal accounting—at least as far as U . S . firms are concerned . Indeed , it has been suggested that this dominance of external reporting has ef fectively reduced innovation in management accounting (Kaplan , 1984) . In addition , from a financial reporting perspective , there has been an interest in the possible economic consequences of accounting regulation through information inductance ef fects on management decisions (Prakash and Rappaport , 1977 ; Zef f ,

* Department of Accounting and Finance , University of Manchester , Manchester , U . K ., correspondence to N . Joseph . † Shef field University Management School .

10455 – 5005 / 6 / 010073 1 21 $18 . 00 / 0 ÷ 1996 Academic Press Limited

74 N . Joseph et al.

1978) . Thus , although starting from dif ferent concerns , researchers in both financial reporting and management accounting have raised questions about the extent to which the internal accounting function serves the needs of decision makers .

In this study , we examine the links between management accounting and external financial reporting through the views of 308 qualified management accountants working in U . K . industrial and commercial firms . A postal questionnaire survey was used to collect opinions on this subject and evidence about the areas of interaction between internal systems and external reporting requirements in the respondents’ organizations .

The remaining sections of the paper are as follows : the next section provides a brief background to the study while Section 3 describes the survey methodology employed . Section 4 presents the main general results on perceptions of external reporting and internal accounting . Section 5 attempts to identify whether responses to the questionnaire are associated with particular organizational or work back- grounds of survey participants . In the last section a summary of the results and a discussion of their implications is provided .

2 . Background to the study

The notion that management accounting may be subservient to financial accounting is not entirely new . This can be inferred from the work of Clark (1923 , p . 68) where he advocates the development of a system of cost analysis separate from the ‘formal books of account’ in which it would be possible to examine ‘dif ferential cost and cost as a normal supply-price , without being tied down by the rules that are legitimate and necessary in financial accounting’ . Further , Solomons (1965 , p . 38) notes that ‘Recent pronouncements on the postulates and principles of accounting have , for the most part , been directed to the problems of reporting company results to stockholders’ and that when accounting fundamentals are under consideration , ‘ . . . little attention tends to be given to the question of whether accounting rules appropriate to the needs of stockholders are also appropriate to the needs of management’ .

Many writers , including Clark , have advocated the separation of financial and management accounting . In this form , the dif ferent profit figures derived from the two sets of accounts could be reconciled . However , the emergence of integrated accounting systems , aided by sophisticated data processing facilities , can perpetuate a bias towards a particular user of accounting information .

The recent debate on the possible subservient role of management accounting and its potentially harmful ef fects on international competitiveness has been due in a large part to Kaplan and his colleagues (see , for example , Kaplan , 1984 ; Johnson and Kaplan , 1987) . Although their claims rest mainly on anecdotal evidence among U . S . firms , their critique has attracted much international attention . Johnson and Kaplan (1987) assert that although advances in management accounting , designed to motivate and evaluate the ef ficiency of key (internal) operating activities , emerged in the U . S . by the middle of the nineteenth century , these advances ended by 1925 and since then , cost accountants have failed to develop new information processing procedures for controlling diverse product and process technologies . They argue

External Financial Reporting and Management 75

that the failure of cost accountants to develop new information processing procedures has limited the usefulness of product costing and operational cost control , and that this can be partly ‘attributed to the dominance of the external financial accounting statements during the twentieth century’ (Johnson and Kaplan , 1987 , p . 13) .

There is now a large body of management accounting literature from which the relative ef fectiveness and relevance of cost accounting methods can be inferred , but which provide conflicting evidence . For example , in case studies concerned with firms characterized by new technologies and high growth rates , Coates and Longden (1989 , p . 2) note that there was ‘considerable dif ficulty’ in the acceptance of modest changes to long-established management accounting practice for U . S . and U . K . firms . However , Innes and Mitchell (1989 , p . 2) found that management accounting practices have changed among U . K . firms where the management accounting function is not a purely centralized service function , and exists ‘to provide an information service for operational management’ . Similar results have been found for Japanese firms in that management accounting systems are designed to support ‘continuous innovation’ (see , Hiromoto , 1991) . Other related work has been mainly concerned with setting the framework for discussion (see , Choudhury , 1986 ; Ezzamel et al . , 1990 ; Hopper 1994) . Such work emphasizes the interrelation- ship of human performance with both the internal and external reporting environ- ments and the need for more research to aid our understanding of the relationship between accounting knowledge and social and economic forces .

There is research evidence which indicates that management accounting techni- ques are increasingly being used for decision making . In a U . K . study , Jones (1986) reported that 90 percent of companies which did not operate a budgetary control system in 1975 had introduced such a system by 1981 . He further recorded a tendency for U . K . firms to emphasize greater financial control and report budgetary results over shorter time horizons .

The increasingly competitive environment in which firms operate implies internal accounting systems and reporting procedures may need to be modified to provide better information for decision-making . Drury et al . (1993) indicate that U . K . firms are placing more emphasis on accurate product costing methods and profitability analysis . Further , some U . K . firms appear to be adopting new manufacturing technologies and implementing activity-based costing for more accurate cost control . On a priori grounds , therefore , we would expect a clear distinction between the roles of internal accounting and external financial reporting . Indeed , Allen (1989) has suggested that for many firms , the internal accounting and external financial reporting systems are completely separate in order to provide relevant information to management . In contrast , other writers have claimed that the accounting information needs of external users are essentially consistent with those of internal management (Institute of Chartered Accountants of Scotland , 1988) .

Discussions about the relevance of management accounting for decision making have to a large extent relied on anecdotal evidence and intuition rather than on large scale empirical work . In an interview-based study of six U . K . firms , Hopper et al . (1992) found no clear evidence of a belief that external reporting requirements dominate management accounting , even though most of the firms studied had a single system of data capture . In another study among academic and practising accountants , Emmanuel and Edwards (1990) found no agreement among the two

76 N . Joseph et al.

groups on the relative importance of various management accounting research issues . Although this latter study implies that there is a need for coordination of research and dissemination of ideas among the two groups , it does not suggest an obvious dominance of financial reporting . It is with this latter issue that this study is concerned .

3 . Methodology

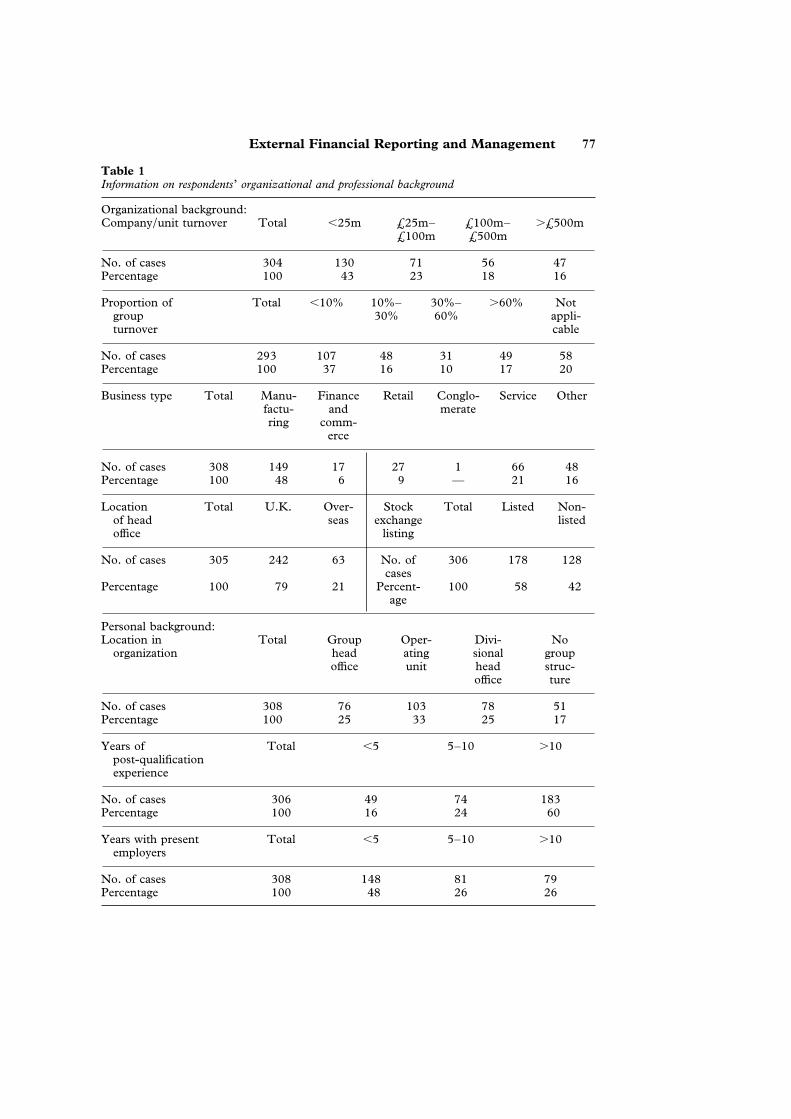

The investigation was pursued by means of a postal questionnaire conducted during the autumn of 1993 . The questionnaire was addressed to qualified members of the Chartered Institute of Management Accountants (CIMA) who were employed by U . K . industrial and commercial firms . The questionnaire was mailed to 1000 individuals , and a follow up reminder was sent after 4 weeks . Overall , 308 (31%) of the questionnaires were satisfactorily completed , a response rate which compares favourably with other survey studies of management accounting practice . Tests involving comparison between the earlier and later responses to the survey revealed no evidence of any non-response bias in the sample of questionnaires received . 1 An analysis of the responses by industry , company size , length of service of respondent with current employer and length of post-qualification experience is indicated in Table 1 . The respondents were employed in a diversity of industries . About 60 percent of the respondents had been qualified accountants for more than 10 years and 48 percent had been employed with their present employers for the last 5 years . The profile of the respondents suggests that our results may be fairly representative of the views held by U . K . management accountants .

The use of a questionnaire survey should be seen in the context of the overall project of which it is a part . This survey is an initial stage of a larger study in which the primary investigation is being undertaken through longitudinal case studies within a number of U . K . companies . Management accountants’ opinions are unlikely to reveal clear evidence of the kind of interactions between financial reporting and management information which may be deeply imbedded in organiza- tional practices . However , this does not mean that the views of management accountants are not of interest and it was felt appropriate to examine how this managerial constituency perceived some of the issues with which the research is concerned , both to provide base information about the kind of views that are prevalent in U . K . companies before embarking upon the case studies and to elicit

1 The questionnaire responses were received as follows :

25 Oct – 29 Oct : 1 Nov – 30 Nov : 1 Dec – 31 Dec :

122 137 49

—— 308 ——

40% 44% 16% ——–

100% ——–

The Kruskal – Wallis test was used to compare early and late responses by first splitting the sample into two halves . This process was repeated by splitting the sample into two-thirds and one-third . The null hypothesis was accepted that the subsamples were not significantly dif ferent at a 0 . 10 level .

External Financial Reporting and Management 77

Table 1 Information on respondents ’ organizational and professional background

Organizational background : Company / unit turnover Total , 25m £25m –

£100m £100m – £500m

. £500m

No . of cases Percentage

304 100

130 43

71 23

56 18

47 16

Proportion of group turnover

Total , 10% 10% – 30%

30% – 60%

. 60% Not appli- cable

No . of cases Percentage

293 100

107 37

48 16

31 10

49 17

58 20

Business type Total Manu- factu- ring

Finance and

comm- erce

Retail Conglo- merate

Service Other

No . of cases Percentage

308 100

149 48

17 6

27 9

1 —

66 21

48 16

Location of head of fice

Total U . K . Over- seas

Stock exchange

listing

Total Listed Non- listed

No . of cases

Percentage

305

100

242

79

63

21

No . of cases

Percent- age

306

100

178

58

128

42

Personal background : Location in

organization Total Group

head of fice

Oper- ating unit

Divi- sional head of fice

No group struc- ture

No . of cases Percentage

308 100

76 25

103 33

78 25

51 17

Years of post-qualification experience

Total , 5 5 – 10 . 10

No . of cases Percentage

306 100

49 16

74 24

183 60

Years with present employers

Total , 5 5 – 10 . 10

No . of cases Percentage

308 100

148 48

81 26

79 26

78 N . Joseph et al.

potential fruitful avenues to be pursued within individual organizations . The views of CIMA members may not , of course , be representative of other groups involved in management accounting and financial reporting . It may therefore be necessary to survey other groups of accountants as well as undertake longitudinal case studies to assess any potential bias which may result from our sample .

The questionnaire was structured to collect three types of information : 2 man- agement accountants’ opinions on the general interaction between external report- ing and internal accounting and decision-making ; evidence about the links between these variables in the respondents’ own organizations ; and information on the participants’ organizational and professional background to allow testing of certain variables which might have an impact on their views and experiences . The questionnaire was pre-tested with a sample of eight individuals and adjusted to incorporate their comments before being mailed to the full sample . 3

While the study has employed survey data to assess the extent to which external reporting requirements af fect internal accounting , this approach has certain impor- tant limitations . The questionnaire largely collected information about the percep- tions of management accountants which may not reflect fully the interaction between external reporting and internal accounting in practical situations . The results are reported in general terms only and may not identify the full extent of specific relationships for which alternative approaches may be more appropriate . Further , the survey only allows a static comparative analysis of the ways external reporting and internal accounting are linked . The results alone , therefore , may not be indicative of change and development in organizations . The current economic environment in which the respondents and firms operate and the professional capacity of the respondents may also have some influence on the responses received . These limitations entail a cautious interpretation of our results . However , this study contributes to the current debate on the possible subservient role of management accounting by documenting the survey results from a large sample on respondents’ beliefs about the influence of external financial reporting requirements on internal systems design and decision-making . This approach contrasts with the anecdotal evidence currently found in the literature .

4 . Survey results

The results of the questionnaire on three aspects of the research problem are reported in this section of the paper : views on the general relationship between internal (management) accounting and external financial reporting ; views on the importance of dif ferent types of information in dif ferent decision contexts ; and evidence on the nature of the interaction between internal and external accounting in the respondents’ own organizations .

2 Formal hypotheses are not listed here as it was felt that this would lead to a cumbersome presentation . Where appropriate , reference is made to the ef fective testing of hypotheses and all significant results are reported . In all instances , the null hypothesis is rejected in favour of the alternative if the statistical test employed yielded a value whose associated probability ( a ) of occurrence under the null is # 0 . 10 . 3 Copies of the questionnaire are available from N . Joseph at the University of Manchester .

External Financial Reporting and Management 79

Internal accounting and external financial reporting Using a scale of 1 (strongly agree) to 7 (strongly disagree) , respondents to the questionnaire were asked to indicate their views on nine assertions concerning the general relationship between internal accounting and external financial reporting . The results are reported in Table 2 , which shows not only the mean response but also the strength of opinion associated with each assertion as reflected in the proportion of respondents who recorded their views with the two strongest scores at either end of the scale . The figures in Table 2 exhibit a clear balance of opinion on six of the nine assertions and suggest a number of points worth noting .

Table 2 Interaction between internal accounting and external financial reporting

n Mean Stan- dard devi- ation

Per- centage rating 1 or 2

Per- centage rating 6 or 7

(a) Externally imposed accounting standards for published financial statements influence management decisions

307 3 . 818 1 . 694 26 . 4 21 . 8

(b) Internal accounting systems are designed primarily to provide information for published financial statements

308 5 . 185 1 . 478 7 . 1 53 . 9

(c) External auditors have significant influence on companies’ choices of accounting policies

308 3 . 977 1 . 583 21 . 4 19 . 8

(d) External auditors have considerable influence on the design of internal accounting systems

308 5 . 182 1 . 450 5 . 2 51 . 3

(e) Companies can influence the market perception of their financial performance and position through their choice of accounting policies

308 2 . 701 1 . 261 51 . 6 3 . 2

(f) Companies on occasions change their accounting policies simply to influence stock market perception of performance

308 2 . 701 1 . 259 49 . 4 2 . 9

(g) Investors can usually see through attempts to use accounting policies simply to improve the published financial statements

308 4 . 140 1 . 507 16 . 2 20 . 8

(h) Internal accounting systems are designed primarily to meet management information needs independently from the requirements for published financial statements

307 2 . 642 1 . 504 62 . 2 7 . 5

(i) Management decisions to allocate resources to particular activities are based primarily on internal accounting reports

307 2 . 730 1 . 539 57 . 0 8 . 8

80 N . Joseph et al.

Allen (1989) argues that for many firms , the information demands of managers cannot be met from an internal accounting system which is constrained by the requirements of external financial reporting . There is little evidence of a belief amongst respondents to this survey that internal systems are dominated by the needs of external reporting . There was clearly disagreement with the suggestion that internal accounting systems are designed primarily to provide information for published financial statements [item (b) in Table 2 , mean 5 . 185 , with 53 . 9% recording a 6 or 7 rating] and agreement that they are designed to meet management information needs independently from the requirements of published financial statements [item (h) , mean 2 . 642 , with 62 . 2% recording a rating of 1 or 2] . Tests of the association between these two items indicated a relationship which , although moderate , is negative , suggesting consistency in the way responses were made to the two assertions . 4

The above results are also consistent with the views expressed about the influence of external auditors on the design of internal accounting systems , where there was marked disagreement with the suggestion that auditors have considerable influence (mean 5 . 182 , with 51 . 3% expressing disagreement at the two strongest points on the scale) .

There was agreement with the suggestion that management decisions concerned with the allocation of resources to activities are based primarily on internal accounting reports (57% recording 1 or 2) . By contrast , there was little agreement on the influence which externally imposed accounting standards have on man- agement decisions [item ( a )] ; only 26 . 4% of respondents recorded a rating of 1 or 2 , compared with 21 . 8% who recorded a rating of 6 or 7 . This latter result should also be contrasted with the responses to items (b) and (h) . Thus although there was general agreement about the purpose of internal accounting systems , the lack of agreement as to the influence of externally imposed accounting standards suggests some uncertainty .

One interesting issue raised in the literature is the extent to which the information needs of external decision makers are met by published financial reports . Innes and Moyes (1991) indicate that some of the participants in their study felt that the firm’s long-term performance was being compromised by financial market pressure to produce short-term results . Items (e) and (f) in Table 2 provide some evidence of a belief in management’s ability to use financial reporting to influence external parties . There was strong agreement both that companies’ choice of accounting policies can influence market perceptions of performance and position , and that companies do change accounting policies to influence the stock market (mean of 2 . 701 on both items , with 51 . 6 and 49 . 4% respectively scoring at 1 or 2) . Tests for the association between responses on these two assertions revealed a moderate association . 5 The belief that management can influence external parties through accounting policy choice may indicate the potential for interaction between

4 The χ 2 test was performed to test the association between responses to items (b) and (h) in Table 2 and rejected the null hypothesis ( χ 2 value 179 . 251 , probability value , a 5 0 . 000) that there was no connection between the responses . Although the Cramer coef ficient , C indicated a moderate association ( C 5 0 . 312) , the Spearman rank order correlation , r s indicates that the relationship was negative ( r s 5 2 0 . 449 , a 5 0 . 000) . 5 The χ 2 test rejected the null hypothesis that there was no association between responses to these two assertions ( χ 2 value 272 . 955 , a 5 0 . 000) . However the association was moderate ( C value 0 . 384 , a 5 0 . 000) , and the Spearman rank order correlation was positive .

External Financial Reporting and Management 81

Table 3 Interaction between internal accounting and external financial reporting factor matrix : Varimax orthogonal rotation 1

Factor 1 Factor 2 Factor 3

(c) External auditors have significant influence on companies’ choices of accounting policies

0 . 7479

(d) External auditors have considerable influence on the design of internal accounting systems

0 . 6276

(a) Externally imposed accounting standards for published financial statements influence management decisions

0 . 2894

(e) Companies can influence the market perception of their financial performance and position through their choice of accounting policies

0 . 8782

(f) Companies on occasions change their accounting policies simply to influence stock market perception of performance

0 . 6676

(g) Investors can usually see through attempts to use accounting policies simply to improve the published financial statements

2 0 . 3258

(b) Internal accounting systems are designed primarily to provide information for published financial statements

2 0 . 4333

(h) Internal accounting systems are designed primarily to meet management information needs independently from the requirements for published financial statements

0 . 9831

(i) Management decisions to allocate resources to particular activities are based primarily on internal accounting reports

0 . 4701

Percentage variance explained 15 . 9 18 . 3 9 . 7

1 Only the variables with the largest loadings on each factor are shown .

external reporting and internal decisions as in this circumstance management will have an incentive to maximize and exploit the opportunity for flexibility in external accounting . Yet there may be important limitations to this flexibility since the respondents could not agree on the extent to which externally imposed accounting standards influence management decisions .

To understand the common underlying independent dimension(s) of the results , maximum likelihood factor analysis was applied to the variable scores for initial factor extraction . The factor loadings were rotated using a varimax rotation . The resulting factor loadings are presented in Table 3 . The association between the responses on the nine assertions suggest three main factors , which account for about 44% of the variation in the data . Since each factor loading is the correlation between the responses to individual assertions and the factor , the factor loadings reflect ‘groups’ of assertions on which the respondents expressed consistent views . The factor analysis indicates that similar responses were made on the relationship between external financial reporting , internal accounting and decision-making in respect of the following three factors : (i) external regulation and use of financial statements policies ,

(ii) internal accounting systems and decision making , (iii) external auditors’ influence .

82 N . Joseph et al.

Importance of types of information in dif ferent decision contexts There is some disagreement in the literature on the extent to which the information needs of managers and external users of published financial reports are perceived to be similar . It has often been assumed that external and internal users of financial reports have dif ferent needs (see , for example , Carsberg , 1980) , but other writers have suggested that the information needs of both groups are similar (see Lee , 1988) . Indeed , Bhimani (1993 , p . 22) states that the performance measures reported to external users by U . K . firms ‘tended to be a subset—and often a considerably reduced subset—of those calculated for internal purposes’ .

To investigate some aspects of this issue , the participants in the survey were asked to assess the importance of certain information variables in three contexts—two involving boards of directors and one concerning investors (using a scale of 1 5 of vital importance , 7 5 of no importance) . The results are summarized in Table 4 . They indicate that respondents believe that cash flow is the most important information variable for boards of directors when reviewing past performance , followed by earnings per share . The assessment of the importance of cash flow was significantly dif ferent from those for share price and deviation from plans . Similarly , the rating for earnings per share was significantly dif ferent from both share price and deviations from plan . 6 In the context of boards of directors deciding future strategy , cash flow was again assessed as having greatest importance , followed by earnings per share . Comparison of the variables using the t -statistic produced similar results to those referred to above for the review of past performance .

Cash flow was regarded as more important in assessing future strategy than in reviewing past performance (mean rating 2 . 030 and 2 . 444 , respectively) but in both of these decision contexts for boards of directors , the rankings show cash flow as being of greater importance than earnings .

In contrast , when asked to indicate the importance of information variables to investors when assessing corporate performance , respondents rated both earnings per share and the price earnings ratio as more important than cash flow . The least important variable in this context was deviations from forecast . The dif ference between the ratings for the earnings variables compared to cash flow were statistically significant , as was the dif ference between the responses for earnings per share and price earnings ratio . 7 The respondents therefore placed significantly dif ferent interpretations on the importance of all the variables to investors when assessing corporate performance .

6

Boards reviewing past performance t -statistic a

Cash flow compared to share price Cash flow compared to deviation from plan EPS compared to share price EPS compared to deviation from plan

2 7 . 11 2 6 . 04 2 8 . 04 2 3 . 81

0 . 000 0 . 000 0 . 000 0 . 000

7

Investors assessing corporate performance t -statistic a

EPS compared to cash flow Price earnings ratio compared to cash flow EPS compared to price earnings ratio

2 7 . 23 2 3 . 12 2 5 . 66

0 . 000 0 . 000 0 . 000

External Financial Reporting and Management 83

Table 4 Relative importance of decision variables to board of directors and investors

n Mean Standard devation

Rank

Boards of public companies reviewing past performance :

Earnings per share Share price Cash flow Deviations from plan

303 304 304 303

2 . 594 3 . 303 2 . 444 3 . 069

1 . 464 1 . 505 1 . 521 1 . 619

2 4 1 3

Boards of public companies deciding future strategy :

Ef fects on earnings per share Ef fects on share price Ef fects on cash flow

304 304 305

2 . 451 2 . 918 2 . 030

1 . 309 1 . 490 1 . 351

2 3 1

Investors assessing corporate performance :

Earnings per share Price earnings ratio Cash flow Deviations from forecast

305 305 305 305

2 . 089 2 . 479 2 . 823 3 . 328

1 . 324 1 . 400 1 . 401 1 . 499

1 2 3 4

These results indicate that the respondents do not perceive that the information variables are of similar importance to both the board of directors and to investors . Cash flow was seen as most important to management and earnings to investors . Using the t -statistic , comparisons of the earnings per share and cash flow variables in the board of director contexts with their counterparts in the investor context indicated that the rating dif ferences are statistically significant . Although it is likely that management may emphasize cash flow more strongly in a period of economic recession , the dif ferent rating for investors does have important implications for the contents of published financial statements , in that their preparation may be influenced by a concern for earnings .

In addition to rating certain specified information variables , respondents were asked to indicate the most important information not currently disclosed in financial statements . A total of 297 suggestions were made , covering a wide range of types of information . A summary classification of these suggestions is provided in Table 5 . It is notable that respondents included non-financial information , information about the future , and analytical information (including segmental analysis) as well as suggestions relating to the contents of the financial statements .

Experience in respondents ’ organizations The questionnaire also included some questions asking more specifically for evidence about the interaction between internal accounting and external reporting in the respondents’ own organizations . The results of the relevant questions are shown in Tables 6 , 7 and 8 .

Table 6 reports views on the extent of integration of the reporting processes and data capture systems used for internal and external purposes (measured on a 7

84 N . Joseph et al.

Table 5 A classification of information indicated as important but not currently contained in financial statements

Types of information seen as important No . of requests Notes

Non-financial information Past information on balance sheet Past information on income statement Future / projected information Additional segmental information Financial analysis

33 31 16 14 12 7

1 2 3 4 — —

There were 297 suggestions received in total for addiitonal information to be disclosed in financial statements . Many of the suggestions made were not repeated in suf ficient numbers to be included in the above table . Some of these less frequently suggested categories include information on audit , of f balance sheet items , internal control statements , resource utilisation , daily shipments , value bases and accounting policies .

Notes : 1 Non-financial information covered a wide range of information sources , including market information , head counts and employee turnover , customer dependency and training policy . 2 Past information on balance sheets included (in order of designated importance) information on working capital , fixed assets , finance , intangibles and contingent liabilities . 3 Past information on income statements included (in order of designated importance) operating costs , management remuneration , provisions and pricing . 4 Future / projected related information , for example , to forecasts profits and turnover , cash flow , costs and investment plans .

point scale where 1 5 totally integrated and 7 5 totally independent) . The responses indicate a general tendency towards integration not only of the recording of information to provide the basis for reports , which might be expected given the capacity of computerized data capture , but also of the forms of internal and external reports on performance , albeit to a lesser extent . 8

Further , Table 7 shows that for organizational units that are part of a group , there is little flexibility over the choice of either internal accounting systems or

Table 6 Extent of integration of information systems for published financial statements and internal accounting reports

n Mean Standard deviation

Per- centage 1 or 2

Per- centage 6 or 7

Published financial statements and in- ternal accounting reports

307 3 . 182 1 . 635 40 . 1 10 . 7

Data capture systems used to provide information for preparing the pub- lished financial statements and the management reports

305 2 . 748 1 . 418 50 . 5 4 . 3

8 The χ 2 test rejected the null hypothesis that there was no association between the responses on these two questions ( χ 2 value 255 . 468 , a 5 0 . 000) , although the relationship was moderate ( C 5 0 . 374) .

External Financial Reporting and Management 85

Table 7 Policy on accounting within the group

Types of information seen as important No . of cases

Percentage

(a) Group accounting rules determine both internal accounting systems and accounting policies used for published financial statements

128 52

(b) Group accounting rules determine internal systems but not the accounting policies used for published financial statements

28 12

(c) Group accounting rules determine policies used for pub- lished financial statements but not internal accounting systems

89 36

245 100 (d) Company not part of a group 62

307

accounting policies for external reporting . A total of 64% of respondents within group structures indicated that the design of internal systems is determined at group level [items (a) plus (b) in Table 7] , with this figure rising to 88% for accounting policies [items (a) plus (c)] .

One of the motivations for including these questions was that in an earlier pilot study (reported in Hopper et al . , 1992) , personnel in group head of fices had suggested that they were happy for staf f at organizational units to devise their own systems to provide the information which unit management felt was necessary to run their businesses , although periodic reports would be required in standard group format . The above results do not suggest that this approach is perceived to be the case by participants in this survey .

Turning directly to the issue of the influence of accounting policies for external

Table 8 Externally imposed accounting standards and internally selected accounting policies

n Mean Standard deviation

Per- centage rating 1 or 2

Per- centage rating 6 or 7

Frequency with which externally proposed accounting standards lead to changes in :

Company’s internal information system Content of reports to top management Decisions taken in the company

307 306 306

4 . 550 4 . 938 5 . 036

1 . 517 1 . 495 1 . 394

10 . 1 5 . 9

15 . 4

32 . 2 43 . 1 46 . 1

Frequency wich which internally selected accounting policies lead to changes in :

Company’s internal information system Content of reports to top management Decisions taken in the company

307 307 307

2 . 700 2 . 779 3 . 101

1 . 292 1 . 342 1 . 484

51 . 5 48 . 9 39 . 1

5 . 5 5 . 2 8 . 8

86 N . Joseph et al.

reporting on other aspects of the respondents’ organizations , Table 8 reports responses to questions about the ef fects of both policies that are externally imposed , for example through accounting standards , and those that result from discretionary management choice (measured on a 7 point scale where 1 5 frequently and 7 5 never) . The results suggest relatively strong and consistent views that the influence of discretionary choice is more frequent than that of externally imposed standards . It also appears that the likelihood of an ef fect is greatest in terms of changes in information systems , followed by changes in internal management reporting , and is least for decisions taken within the company . The respondents seem to perceive that the ef fects of external reporting change are mainly informa- tional rather than decision based . The figures in Table 8 show a polarity between the responses on the ef fects of internal policy choice and those on externally imposed standards . The t -statistic on the dif ference in the means for the same ef fects under the two influences was significant in all cases .

The fact that the questionnaire is collecting opinions about ef fects rather than actual impact is perhaps worth reiterating here , as the links between informational change and decision ef fects may be subtle and indirect , rather than explicit and acknowledged . As noted in the introduction , the possibility of decision con- sequences following from information inductance has been discussed in the literature on accounting standard setting (Prakash and Rappaport , 1977 ; Zef f , 1978 ; Wilner , 1982) , and the existence of such ef fects may not be captured in a survey of this kind .

5 . The influence of respondents’ organizational and professional background

There are good reasons to suggest that a number of demographic variables may have a significant ef fect on the beliefs of the respondents . For example , perceptions of the links between internal accounting and external financial reporting may have been influenced by the respondents’ location within the organization structure . The perceived importance of activities concerned with internal accounting and published financial statements may also be influenced by the circumstances of the organization . 9 Further , dif fering beliefs of the relative importance of performance measures to the board and investors could be associated with organizational features , 1 0 such as size or business type . The variation in responses associated with specific organizational or personal characteristics is discussed below , with reference to the same structure of issues as that used in the previous section .

Internal accounting and external financial reporting To assess the ef fects of demographic variables on the respondents’ beliefs about the relationship between internal accounting and external financial reporting , the non-parametric Kruskal – Wallis test was employed . The null hypothesis is that the

9 In an empirical study concerned with information systems , Santos (1989) indicates that key activities were prioritized depending on the internal and external circumstances of organizations and this led to dif ferences in the perceived importance of certain activities . 1 0 From interviews with some subsidiaries of 15 multinational companies , Coates et al . (1992 , p . 136) note : ‘the subsidiaires had greater awareness of the corporate financial objectives that had been set than of the corporate mission , and that this generated dif fering perceptions between the head of fice and subsidiary management’ .

External Financial Reporting and Management 87

Table 9 Results of pair - wise comparisons of demographic variables with ratings from interaction between internal accounting and external financial reporting using the Kruskal – Wallis tests 1

Company / unit

turnover

Years of post-

qualication experience

Years with

present employers

(a) Externally imposed accounting standards for published financial statements influence management decisions

(b) Internal accounting systems are designed primarily to provide information for published financial statements

5 . 173 (0 . 075)

(c) External auditors have significant influence on companies’ choices of accounting policies

6 . 710 (0 . 082)

7 . 189 (0 . 027)

(d) External auditors have considerable influence on the design of internal accounting systems

5 . 387 (0 . 068)

(e) Companies can influence the market perception of their financial performance and position through their choice of accounting policies

7 . 347 (0 . 025)

(f) Companies on occasions change their accounting policies simply to influence stock market perception of performance

6 . 499 (0 . 039)

(g) Investors can usually see through attempts to use accounting policies simply to improve the published financial statements

(h) Internal accounting systems are designed primarily to meet management information needs independently from the requirements for published financial statements

5 . 796 (0 . 055)

(i) Management decisions to allocate resources to particular activities are based primarily on internal accounting reports

1 The probability ( a ) value associated with the test statistic is shown in parenthesis . Only the cases with a # 0 . 10 are shown .

demographic variables have no ef fect on the beliefs of the respondents . The results for cases where a significant association was present are reported in Table 9 . The results indicate that the personal circumstances of the respondents appear to have a greater association with the respondents’ beliefs than the nature of the organization in which they are employed . In several cases the respondents’ length of service with their current organization and the number of years post-qualification experience have a significant ef fect on the views expressed . In particular , the results indicate that respondents with 10 or more years post-qualification experience as well as length of service with their present employers , disagreed more strongly (relative to other groups) with most assertions in Table 9] , except item (h) in which case those respondents agreed more strongly . The only significant ef fect associated with an organizational variable is that between turnover and the respondents’ perceptions of

88 N . Joseph et al.

the degree of influence exerted by external auditors on the companies’ choice of accounting policies . Respondents in smaller organizations disagreed more strongly that auditors have a significant influence . It is interesting to note that neither the nature of the main business of the company nor the location of the respondents in the organizational structure appears to influence the respondents’ views .

Importance of types of information in dif ferent decision contexts Our earlier results indicated that the perceived importance of various performance measures to dif ferent decision-makers varied . We tested the null hypothesis that the demographic variables have no ef fect on the perceived importance of the informa- tion variables . The results of the Kruskal – Wallis test for the association between demographic factors and views on the importance of information variables (with a null hypothesis of no association) are set out in Table 10 .

The results indicate that the respondents’ perceptions of the relative importance of the cash flow variable for reviewing past performance are influenced by their length of post-qualification experience . The location of the respondents within the organizational structure also appears to have a significant ef fect on views about the

Table 10 Results of pair - wise comparisons of demographic variables with importance of decision variables to board of directors and investors using the Kruskal – Wallis 1 test

Proportion of

group turnover

U . K . or overseas

head of fice

Listed or non-listed

Location in

organiz- ation

structure

Years of post- qualifi- cation

experience

Boards of public companies reviewing past performance

Earnings per share Share price Cash flow 6 . 670

(0 . 083) 8 . 905

(0 . 012) Deviations from plan 8 . 702

(0 . 069) 9 . 296

(0 . 026) Boards of public companies deciding future strategy

Ef fects on earnings per share

3 . 481 (0 . 062)

Ef fects on share price Ef fects on cash flow

4 . 057 (0 . 044)

Investors assessing corporate performance

Earnings per share 3 . 625 (0 . 057)

3 . 301 (0 . 069)

Price earnings ratio Cash flow 8 . 178

(0 . 042) Deviations from forecast 7 . 670

(0 . 053)

1 The probability ( a ) value associated with the test statistic is shown in parentheses . Only the cases with a # 0 . 10 are shown .

External Financial Reporting and Management 89

relative importance of information about cash flow and deviations from plans to the board when reviewing past performance , and to investors when assessing corporate performance . Respondents located at head of fices (relative to those located elsewhere) placed greater importance on these variables . Views on the importance of cash flow to future strategy appear not to be influenced by any of the demographic variables . The responses for earnings per share and share price measures , appear to be influenced by the fact that the companies are listed , but only in the context of boards deciding future strategy and investors assessing corporate performance . The main business of the company or group and the relative size (proportion of total group turnover) of the unit in which the respondents work , appear to have no significant ef fect on the perceived importance of the decision variables to the board when deciding future strategy , and investors when assessing corporate performance .

Accounting standards and accounting policies This section discusses the results of tests for association between the demographic variables and the findings included in Table 8 on the frequency with which externally imposed standards and internally imposed accounting policies to have led to changes in internal information systems , and decisions taken in companies .

The results , reported in Table 11 , indicate that size (measured by turnover) and relative size within the group have a significant association with the frequency with

Table 11 Results of pair - wise comparisons of demographic variables with externally imposed accounting standards and internally selected accounting policies using the Kruskal – Wallis test 1

Company / unit

turnover

Group turn- over

U . K . or overseas

head of fice

Listed or non- listed

Location in organi-

zation structure

Frequency with which externally imposed accounting standards lead to changes in :

Company’s internal information system

Content of reports to top management

Decisions taken in the company

8 . 163 (0 . 043) 11 . 953 (0 . 008) 10 . 639 (0 . 014)

9 . 623 (0 . 047) 10 . 889 (0 . 028)

5 . 783 (0 . 016)

5 . 494 (0 . 019) 4 . 510

(0 . 034) 4 . 218

(0 . 040)

6 . 561 (0 . 087) 16 . 447 (0 . 001) 12 . 206 (0 . 007)

Frequency with which internally selected accounting policies lead to changes in :

Company’s internal information system

6 . 595 (0 . 086)

Content of reports to top management

3 . 587 (0 . 058)

6 . 813 (0 . 078)

Decisions taken in the company

3 . 857 (0 . 050)

1 The probability ( a ) value associated with the test statistic is shown in parentheses . Only the cases with a # 0 . 10 are shown .

90 N . Joseph et al.

which externally imposed accounting standards have led to changes in the content of reports to top management and in decisions taken in the companies , and that size is further associated with the frequency of change in the company’s internal information system . Respondents in larger units and larger parts of a group indicated more frequent ef fects than those in smaller organizations . Whether the company is listed on the Stock Exchange or not had a similar significant association with the frequency of all three ef fects . However , few demographic variables appear to have a significant ef fect on the frequency of changes following internally selected accounting policies . In this case , the ef fects appear to be stronger for firms whose head of fices are located overseas . It therefore appears that larger size and listing are important factors associated with a perceived higher incidence of ef fects from external accounting regulation . Whether the respondent organization had a U . K . or overseas head of fice had a significant association with the frequency of ef fects on reports to top management—respondents with overseas organizations reported less frequent change resulting from externally imposed accounting standards albeit not for internally selected accounting policies . Finally , the position of the respondents in the organizational structure appears to be significantly associated with views about the frequency of change following both external accounting regulation and internally chosen policies—the greatest frequency of impact was recorded by respondents based at group head of fice .

6 . Summary of results and discussion

The research reported in this paper represents a preliminary and limited investiga- tion of the connection between external reporting requirements and internal accounting and decision-making , and thus conclusions must be stated with caution . Nevertheless , from the responses that have been obtained through this questionnaire survey , a number of clear patterns have been identified in the expressed perceptions of U . K . qualified management accountants .

The survey has disclosed little evidence of a generally held belief that external reporting dominates internal accounting . 1 1 While there was evidence of a belief that management can and do attempt to influence investors’ views through accounting policy choice , there were mixed findings regarding the impact of external reporting on management decisions . There tended to be agreement with the statement that management decisions to allocate resources to particular activities are based primarily on internal accounting reports [Table 2(i)] , but a range of opinion was expressed about the statement that externally imposed accounting standards for published financial statements influence management decisions [Table 2(a)] . This leaves some doubt about the views concerning the impact of external reporting on management decisions .

Information about cash flow and earnings per share was considered to be of dif fer- ing importance to internal and external decision-makers . For internal decision- makers cash flow information was regarded as most important , whereas for investors it was earnings which were perceived to be of most importance . This suggests a dif ferent decision-making emphasis and the possibiilty that internal decision-makers

1 1 This is consistent with a pilot study which found ‘no clear evidence of external reporting conventions or accounting standards being cited as adversely af fecting management accounting systems’ (see , Hopper et al . , 1992 , p . 310) .

External Financial Reporting and Management 91

will not be overly concerned with the information reported in the external reports . There was also a belief that non-financial and future oriented information not currently contained in financial statements is important for decision-making . In addition , the respondents indicated that discretionary accounting choice has had a more frequent impact on internal systems , reports and decisions than has externally imposed accounting regulations . This could well be consistent with the views that managers can influence their financial performance through their choice of accounting policies . If such accounting policy choices are regarded as important it is quite likely that they will be applied throughout the company and not just in the external financial reports .

The testing of organizational demographic variables indicated that the character- istics of the organization in which the respondents work was associated with variation in their experiences of the impact of internally decided and externally imposed accounting change . Larger size , a stock exchange listing , being part of a U . K . group and the fact that the respondent was based at head of fice resulted in higher frequencies of impacts being reported . These characteristics would seem to suggest that management accountants working at the head of fices of large , multi-divisional , quoted companies are most likely to see an impact of external reporting on their companies’ internal accounting systems and management decisions . Conversely , management accountants in small and medium sized privately owned companies , or in larger quoted companies but located away from head of fice are more likely to see little impact . The issue of size and stock market listing would seem to be important a priori , as large quoted companies are likely to be very conscious of the impact that their external financial reports have on their shareholders .

The most common individual variables associated with variation in the responses were length of post-qualification experience and length of service with current employer . Both of these variables may be associated with seniority in the organization . Hence , it should not be surprising that such people had very clear and identifiable views on the issues explored in the questionnaire and especially opinions on the interaction between internal accounting and external financial reporting .

Putting the findings from the dif ferent parts of the questionnaire together suggests an interesting implication . The apparently widely held belief that internal account- ing is not dominated by external accounting requirements would seem to be in conflict with the reported integration of systems of data capture and uniform reporting procedures and with the lack of discretion at the unit level in both internal and external information and reporting processes . Although the management accountants who responded to the survey do not seem to believe that management accounting is dominated by financial reporting , they use integrated financial accounting and management accounting systems and have little discretion in the content of their management reports . The latter being dictated by the requirements of financial reporting to head of fice .

Such seemingly contradictory findings may be due to managers and management accountants perceiving management information needs in terms which reflect a financial accounting view of the organization and of its performance . In other words , the lack of a belief that external reporting dominates internal accounting may simply be a reflection of the success with which external requirements have become an established part of the routines of information gathering and reporting within

92 N . Joseph et al.

organizations and an essential part of management thinking on appropriate information for decision making . Issues of this nature , however , cannot be investigated using the survey methods of the research reported here .

Future research As a questionnaire survey this research has provided evidence about the perceptions of one group , U . K . qualified management accountants , regarding the interactions between external financial reporting and management information and decision- making . Such perceptions are important to understanding how accounting and decision-making is viewed in practice . The nature and mechanics of the interactions themselves , however , cannot be elicited through surveys of opinions . They are likely to be complex in most organizations and will rarely be explicitly articulated . They may be deeply imbedded in organizational procedures and may often be ‘subcon- scious’ to many participants . Research using in depth and preferably longitudinal case studies will be more appropriate for exploring the processes of accounting and decision-making within organizations .

There are many issues concerning the practical routines surrounding both internal and external reporting , and their inter-relationships , which require further research . For example , the role of accounting information and systems in organizations which are beginning to attach particular importance to non-financial key performance measures is a subject in need of further study . In addition , there are questions concerning the performance of accounting functions and who undertakes such traditional accounting tasks as cost monitoring and control . Is it the accountants or the operational managers who are primarily involved in cost management? How do managers cope with requirements for continual cost improvement? Such issues raise questions concerning the way in which an understanding of business performance is constructed , which is at the heart of the investigation of how external reporting shapes the thinking of managers and accountants , and influences the processes of management reporting .

Acknowledgements : This paper was presented at the European Accounting Association Annual Congress in Venice in April 1994 . The authors gratefully acknowledge the financial support granted by the Chartered Institute of Management Accountants for carrying out this research project .

References

Allen , D ., 1989 . Creating Value — The Financial Management of Brands , London . Chartered Institute of Management Accountants .

Bhimani , A ., 1993 . Performance measures in UK manufacturing companies : the state of play , Management Accounting , December , 20 – 22 .

Carsberg , B ., 1980 . Chapter 1 , in Arnold , J ., Carsberg , B . and Scapens , R ., (eds) Topics in Management Accounting , Oxford . Philip Allan .

Choudhury , N ., 1986 . In search of relevance in management accounting research , Accounting and Business Research , Winter , 21 – 32 .

Clark , J ., 1923 . The Economics of Overhead Costs , Chicago , IL , The University of Chicago Press .

Coates , J ., Davis , E ., Emmanuel , C ., Longden , S . and Stacy , R ., 1992 . Multinational companies performance measurement systems : international perspectives , Management Accounting Research , 3 , 133 – 150 .

External Financial Reporting and Management 93

Coates , J . and Longden , S ., 1989 . Management Accounting : The Challenge of Technological Innovation , London , The Chartered Institute of Management Accountants , 1 .

Drury , C ., Braund , S ., Osborne , P . and Tayles , M ., 1993 . A Survey of Management Accounting Practices in UK Manufacturing Companies , London , The Chartered Association of Certified Accountants , Certified Research Report 32 .

Emmanuel , C . and Edwards , K ., 1990 . Exploring the relevance gap , Management Accounting ( UK ) , November , 44 – 46 .

Ezzamel , M ., Hoskin , K . and Macve , R ., 1990 . Managing it all by numbers : a review of Johnson & Kaplan’s ‘Relevance Lost’ , Accounting and Business Research , 20(78) , 153 – 166 .

Hiromoto , T ., 1991 . Restoring the relevance of management accounting , Journal of Management Accounting Research , Fall , 1 – 15 .

Hopper , T ., 1994 . Activity based costing : a critical commentary . Fukuaka University , Review of Commercial Sciences , November , 479 – 511 .

Hopper , T ., Kirkham , L ., Scapens , R . and Turley , S ., 1992 . Does financial accounting dominate management accounting—a research note , Management Accounting Research , 3 , 307 – 311 .

Innes , J . and Mitchell , F ., 1989 . Management Accounting : The Challenge of Technological Innovation , London , The Chartered Institute of Management Accountants , 2 .

Innes , J . and Moyes , J ., 1991 . Management Information and External Reporting — Six case studies , Edinburgh , The Institute of Chartered Accountants of Scotland .

Institute of Chartered Accountants of Scotland (ICAS) , 1988 . Making Corporate Reports Valuable , London , Kogan Page Limited .

Johnson , H . and Kaplan , R ., 1987 . Relevance Lost : The Rise and Fall of Management Accounting , Boston , MA , Harvard Business School Press .

Jones , C . J ., 1986 . Financial planning and control practices in U . K . companies : a longitudinal study , Journal of Business Finance and Accounting , Summer , 161 – 185 .

Kaplan , R . S ., 1984 . The evolution of management accounting , The Accounting Review , July , 390 – 418 .

Lee , T ., 1988 . The information needs of management , in Making Corporate Reports Valuable — The Literature Survey , Edinburgh , Institute of Chartered Accountants of Scotland , 183 – 215 .

Prakash , P . and Rappaport , A ., 1977 . Information inductance and its significance for accounting , Accounting Organisations and Society , 2(1) , 29 – 38 .

Santos , B ., 1989 . Information systems : similarities and dif ferences across organisations , OMEGA Internatinal Journal of Management Science , 17(1) , 9 – 20 .

Solomons , D ., 1965 . Divisional Performance : Measurement and Control , Chicago , IL , Richard D . Irwin .

Wilner , N ., 1982 . SFAS8 and information inductance—an experiment , Accounting Organisa- tions and Society , 7(1) , 43 – 52 .

Zef f , S ., 1978 . The rise of economic consequences , Journal of Accountancy , December , 56 – 63 .