Exploring impacts of the revised edl and associated policies

12

New Game New Opportunities New Direction Exploring Impacts of the Revised EDL and Associated Policies IMS Consulting Group April 2013 Developed by:Meng Zhang Jordan Liu Jimmy Lu Sherry Zhang WHITE PAPER CHINA

-

Upload

ims-health-asia-pacific -

Category

Business

-

view

370 -

download

0

Transcript of Exploring impacts of the revised edl and associated policies

New Game New Opportunities New Direction

Exploring Impacts of the Revised EDL and Associated Policies

IMS Consulting GroupApril 2013

Developed by:Meng Zhang Jordan Liu Jimmy Lu Sherry Zhang

WHITE PAPER CHINA

WHITE PAPER CHINA

IMS CONSULTING GROUP Exploring Impacts of the Revised EDL and Associated Policies

Content

Executive Summary………………………………………………………………………………………………………………………………… 3

1. Background on the Essential Drug System…………………………………………………………………………………………… 3

2. Comparing lists: the 2009 and 2012 Essential Drug Lists………………………………………………………………………… 4

2.1 Summary analysis of 2009 and 2012 NEDLs………………………………………………………………………………… 4

2.2 Market analysis of the 2009 and 2012 NEDLs……………………………………………………………………………… 4

2.3 Restricted provincial supplements to the NEDL…………………………………………………………………………… 5

Summary……………………………………………………………………………………………………………………………………… 5

3. 2012 EDL Implementation and Evolving Supporting Policies…………………………………………………………………… 6

3.1 EDL Implementation Scope and Usage Requirements…………………………………………………………………… 6

3.2 Changes in EDL Tendering Mechanisms……………………………………………………………………………………… 6

Towards an Improved “Two-Envelop” Model………………………………………………………………………………… 6

An Emerging Trend: Quality Classification…………………………………………………………………………………… 6

Shifting Priorities: Weight of the Quality Evaluation Score……………………………………………………………… 7

The Ripple Effect: Linkage of Provincial Tendering Results……………………………………………………………… 7

Winner Takes All: Granting Exclusive Access to One Supplier………………………………………………………… 7

3.3 EDL Pricing and Reimbursement Policies…………………………………………………………………………………… 8

4. Anticipated Impact of the New NEDL to MNCs……………………………………………………………………………………… 8

4.1 Impact of EDL Adjustments………………………………………………………………………………………………………… 8

4.2 Impact of EDL Policy Evolvement………………………………………………………………………………………………10

5. MNC’s Coping Strategies………………………………………………………………………………………………………………………10

Adjust tendering strategies according to new tendering policy environment…………………………………………10

Develop marketing strategies based on the needs of the new EDL market………………………………………………10

Explore methods to maintain favorable national price…………………………………………………………………………10

6. IMSCG is the perfect partner to pharma companies to succeed in the EDL market………………………………………11

7. End Remark…………………………………………………………………………………………………………………………………………11

Appendix:RDPAC Member Company List………………………………………………………………………………………………11

3

WHITE PAPER CHINA

IMS CONSULTING GROUP Exploring Impacts of the Revised EDL and Associated Policies

2020Nov 2010

Apr 2011 March 2013 March 2013

• 1st Essential drug list for PMIs & policy released

• National ceiling price was set based on current price of local generics

• 77.36% of primary institutions in China has implemented EDS

• State Council's suggestions on better establishment of EDS(No.14 Document) was published

• The guideline for essential drug procurement (No.56 Document) was published,indicating the establishment of essential drug system

• National average purchasing price was set ofr local reference

• The implementation scope of NEDL is expanded to 520 molecules

• Implementation scope of EDL is expanded to level 2&3 hospitals

• Essential drug system will be completely established by 2020

Aug 2009

The Establishment Plan of Essential Drug System

Source: Government publications, IMS interviews and analysis

In March 2013, China's Ministry of Health (MOH) released the new essential drug list (the “2012 EDL”). Significant changes are outlined in the newly released document; such change will undoubtedly assert great influence over future development prospects of multinational corporations (MNCs) in China. To help MNCs understand and navigate the newly announced policies, IMS Consulting Group has executed a deep-dive analysis of EDL updates and supporting policy evolvements and explored their impact to MNCs.

In this study, MNCs refer to 34 member companies of R&D-based Pharmaceutical Association Committee (RDPAC). Sales data of tier 2 & 3 hospitals comes from IMS MIDAS database (which collects hospital purchasing information from hospitals with 100+ beds and projects to national tier with advanced statistical models)

Executive Summary

1. Background on the Essential Drug System

Since its inception in 2009, the Essential Drug System (EDS) has been a top priority for policymakers at the central and provincial tiers. With the overall goal of establishing a comprehensive system which facilitates access and ensures affordable care for all citizens by 2020, the EDS and its associated policies have been supplemented and strengthened over the years.

Specifically, over the course of the past three years, significant process has been made as a result of coordinated development and decentralized efforts to address region-specific issues. Nevertheless, several issues have emerged in relation to the 2009 NEDL: ① The 2009 National Essential Drug List (NEDL), which includes 307 Western and Chinese medications, has not sufficiently met patients’ basic medical needs; ② The previously well-regarded Anhui two-envelope tendering model has been questioned with respect to its ability to ensure drug safety and overall patient health; ③ The NEDL, to date, has only been adopted in primary healthcare institutions, which account for a small proportion of all healthcare institutions. Due to lack of NEDL implementation in non-primary healthcare institutions (i.e. tier 2 and above hospitals), a unique and troubling phenomena of “Same City Different Price” has surfaced - notably, price variations for the same drug depending on institution.

In order to further China’s healthcare reforms, the government has recently made a slew of announcements: in February 2013, the State Council’s general office published its suggestions for the consolidation and improvement of EDS, as well as for the development of primary healthcare institutions (Document 14). This was closely followed by the Ministry of Health’s March release of the “National Essential Drug List 2012”.

Implementation of these new policies holds significant implications for the future of healthcare-focused companies in China. The pharmaceutical market will witness considerable change, bringing unprecedented opportunities and challenges that cannot be overlooked by MNCs.

4

WHITE PAPER CHINA

IMS CONSULTING GROUP Exploring Impacts of the Revised EDL and Associated Policies

2. Comparing lists: the 2009 and 2012 Essential Drug Lists

2.1 Summary analysis of 2009 and 2012 NEDLs

The 2012 edition of the Essential Drug List has numerous changes from the 2009 edition. The revised list includes a significant increase in the total number of molecules, but also specifies formulations, an inclusion criteria not detailed in the 2009 version. Notable changes are detailed below:

2.2 Market analysis of the 2009 and 2012 NEDLs

So what are the expected market implications of the expanded EDL? We took a first step towards answering this question by looking at 2012 tier 2 and 3 hospital sales for molecules included on the old and revised lists (chemical and biological drugs only). Our preliminary analysis shows that the essential drugs market, as a result of the newly expanded 2012 EDL, has significantly increased market share in both value and volume.

Note: Market share calculated by hospital purchase value or volume (2012); data collected from hospitals>100 beds

Source: IMS CHPA data and analysis

2009 NEDL WesternDrugs - 205 Molecules

2012 NEDL WesternDrugs - 317 Molecules

EDL Drugs Non-EDL Drugs

88.5%

11.5%

83.8%

16.2%

Value Share Comparison

2009 NEDL WesternDrugs - 205 Molecules

2012 NEDL WesternDrugs - 317 Molecules

EDL Drugs Non-EDL Drugs

Value Share Comparison

57.4%

42.6%

66.8%

33.2%

Source: Government publications, IMS interviews and analysis

2009 NEDL 2012 NEDL Notable change

Total number of molecules 307 520 +213

Number of Western drugs 205 317 +112

Number of Traditional Chinese Medicine (TCM

102 203 +101

Formulation and pack-specific? No Yes Formulation now specified

Number of formulations (Western drugs)

780+ 850+ + 70

Number of different packs (Western drugs)

2600+ 1400+ -1200

Therapeutic focus Basic needsAdditional

therapeutic focusAdded oncology, blood,

pediatric drugs

5

WHITE PAPER CHINA

IMS CONSULTING GROUP Exploring Impacts of the Revised EDL and Associated Policies

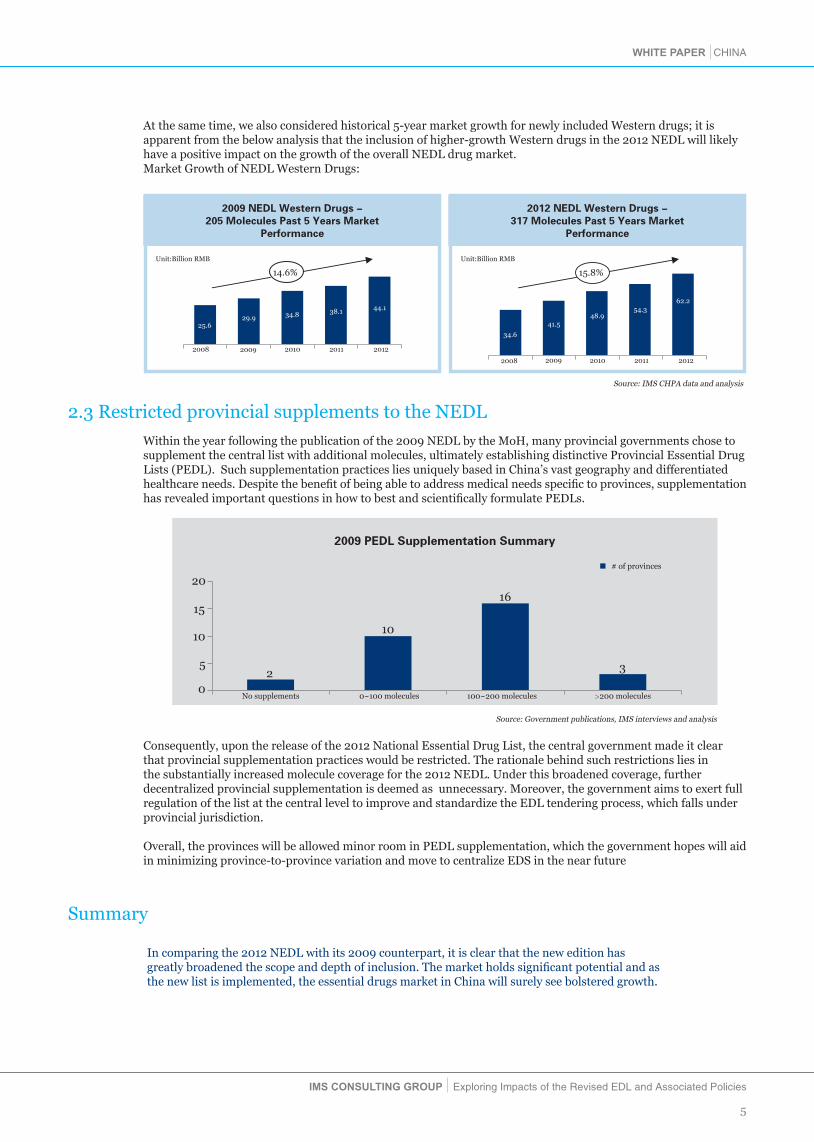

At the same time, we also considered historical 5-year market growth for newly included Western drugs; it is apparent from the below analysis that the inclusion of higher-growth Western drugs in the 2012 NEDL will likely have a positive impact on the growth of the overall NEDL drug market. Market Growth of NEDL Western Drugs:

Source: IMS CHPA data and analysis

2.3 Restricted provincial supplements to the NEDL

Within the year following the publication of the 2009 NEDL by the MoH, many provincial governments chose to supplement the central list with additional molecules, ultimately establishing distinctive Provincial Essential Drug Lists (PEDL). Such supplementation practices lies uniquely based in China’s vast geography and differentiated healthcare needs. Despite the benefit of being able to address medical needs specific to provinces, supplementation has revealed important questions in how to best and scientifically formulate PEDLs.

Summary

In comparing the 2012 NEDL with its 2009 counterpart, it is clear that the new edition has greatly broadened the scope and depth of inclusion. The market holds significant potential and as the new list is implemented, the essential drugs market in China will surely see bolstered growth.

Source: Government publications, IMS interviews and analysis

No supplements 0~100 molecules 100~200 molecules >200 molecules

2009 PEDL Supplementation Summary

# of provinces

02

10

16

35

10

15

20

Consequently, upon the release of the 2012 National Essential Drug List, the central government made it clear that provincial supplementation practices would be restricted. The rationale behind such restrictions lies in the substantially increased molecule coverage for the 2012 NEDL. Under this broadened coverage, further decentralized provincial supplementation is deemed as unnecessary. Moreover, the government aims to exert full regulation of the list at the central level to improve and standardize the EDL tendering process, which falls under provincial jurisdiction.

Overall, the provinces will be allowed minor room in PEDL supplementation, which the government hopes will aid in minimizing province-to-province variation and move to centralize EDS in the near future

Unit:Billion RMB

2009 2010 2011 2012

34.8 38.1 44.1

14.6%

2008

25.629.9

2009 NEDL Western Drugs -205 Molecules Past 5 Years Market

Performance

Unit:Billion RMB

2012 NEDL Western Drugs -317 Molecules Past 5 Years Market

Performance

2008 2009 2010 2011 2012

41.548.9

54.362.2

15.8%

34.6

6

WHITE PAPER CHINA

IMS CONSULTING GROUP Exploring Impacts of the Revised EDL and Associated Policies

3. 2012 EDL Implementation and Evolving Supporting Policies

3.1 EDL Implementation Scope and Usage Requirements

After the release of 2009 EDL, all government-based primary healthcare institutes were required, by the MoH, to restrict drug utilization to only EDL-listed molecules (a core pillar of the essential drug system). As of April 2011, only 77.36% of primary healthcare institutions have fully implemented EDS. Moreover, procurement and utilization of EDL drugs have not followed central policies: in some areas, primary healthcare institutes can still procure non-EDL drugs. In contrast, there are no requirements or restrictions regarding EDL usage in tier 2 & 3 hospitals, thus highlighting large implementation loop holes and scope differences in the old system.In early 2013, Chen Zhu, Minister of MOH, indicated that after the release of new EDL, all primary healthcare institutions are required to only supply EDL drugs. In addition, volume and revenue ratio of EDL drug in tier 2 hospitals should reach 40%~50% with tier 2 hospitals in designated pilot counties to achieve a ratio of 50%. Lastly, revenue ratio of EDL drug in level 3 hospitals should be 25%~30%.In reality, 2012 IMS tier 2&3 hospitals purchase data indicates that the sales of 317 western drug molecules included in the 2012 NEDL accounts for only 16% of the overall sales, highlighting a significant gap between the actual and the required utilization ratio (25% for tier 3 hospitals and 40% for tier 2 hospitals). In the case that published hospital EDL utilization rations are enforced, it is rational to conclude that prescription volume of EDL drugs in tier 2&3 hospitals will see significant increase. (Sales volumes are expected to undergo greater growth if Chinese traditional medicines are considered)

3.2 Changes in EDL Tendering Mechanisms

Since implementation of EDS, provinces have launched exploratory and experimental efforts in identifying the optimal EDL tendering mechanism. The outcome of such efforts cumulatively amounts to lowered drug prices, reduced patient out-of-pocket spending, ensured quality and supply for the primary healthcare sector. Moving into the future, with the publication of document no. 14 by the General Office of the State Council, provinces are facing new challenges in EDL tendering.

Towards an Improved “Two-Envelop” Model

Firstly, document no. 14 clearly states that the “two-envelope” model will be continuously adopted in EDL tendering, but with renewed determination to further improve the model’s main assessment modules – notably, quality and price. Within the quality module, drug quality, manufacturer’s services and credentials will be highlighted as critical metrics. Moreover, the 2010 GMP will be featured as a core pillar of the improved model. On the other hand, within the pricing module, excessively low-priced drugs will be subjected to composite scoring, with the main goal of avoiding unsustainable pricing competition and to encourage manufacturers’ prioritization and maintenance of drug quality. Secondly, in past rounds of provincial tendering, some provinces have proceeded with a new variation of the “two-envelop” model. For instance, in the last Beijing EDL tender, to prevent lower priced, and therefore assumed to be lower quality products, from dominating, the quality evaluation score was weighted and become a part of a more holistic approach to evaluating tenders.

An Emerging Trend: Quality Classification

The 2009 EDL was thoroughly known as a list used for primary healthcare institution, meant to meet basic healthcare needs. As such, in past rounds of provincial tendering, only a few provinces – namely Shanghai and Jiangsu - has incorporated quality classification, a tendering tactic meant to reward manufactures’ investments in assuring quality. On the other hand, most other provinces failed to implement this tiered approach, choosing instead to use a bundled, one-size-fits-all approach to EDL procurement. Lastly, although Shanghai and Jiangsu took the stance to insist on quality, the then utilized evaluation system was far from perfect – lower priced drugs were still favored, leading to the phenomena of “lower priced contender takes all”. For now, public opinion does not seem to favor mandated implementation of quality evaluation. Instead it continues to be perceived that EDL tenders will remain unchanged and price-centric. For MNCs, this presents as a critical time and opportunity to change public and central government opinions: the 2012 new EDL is no longer restricted to just primary healthcare institutions, instead it is being transformed into a broad healthcare initiative with mandated usage in higher-tier hospitals. As such, the mechanism by which this goal is realized - the provincial tender – should stand to satisfy the needs of healthcare institutions of all levels. Moreover, with broaden scope of impact and the number of lives affected, an increased reliance falls on the tender mechanism to satisfy patient needs of all types, but most of all, to protect all patient rights.

7

WHITE PAPER CHINA

IMS CONSULTING GROUP Exploring Impacts of the Revised EDL and Associated Policies

Shifting Priorities: Weight of the Quality Evaluation Score

Document no.64, a critical guidance document for EDL tenders, clearly states that “the weight of the quality evaluation score should not be less than 50% of the total score.” In actual practices, differences in the definition of quality has resulted in clinically-based attributes being utilized less than required. In the past few years of trial and error, various government departments have realized the importance of quality evaluation, as a critical defense against lower- priced products dominating tenders, further exasperating quality-related adverse events and supply shortages. Document no. 14 also states that, when assessing the quality evaluation score, passing the 2010 GMP should be considered as a key assessment criteria, complemented by product quality, manufacturers’ services and credentials. Manufacturers should move swiftly to comply with policy terms, engage provincial tendering departments and officers in deeper discussion, and further optimize internal tendering and market access strategies.

The Ripple Effect: Linkage of Provincial Tendering Results

“Top-to-bottom” and “left-to-right” linkage of provincial tendering results are not new to the public. This rings especially true for price referencing between provinces, otherwise known as “left-to-right” price reference. As of today, provincial tender price referencing has become a mainstream initiative. Consequently, manufacturers have to critically assess the potential fall-out as winning tender prices are published nation-wide, impacting commercial operations on an unimaginable scale. Moreover, ramifications may extend far beyond just tenders to government-imposed cuts to price ceilings, which largely observe tender prices and falls under the jurisdiction of the NDRC. “Top-to-bottom” linkage refers to the direct application of wining EDL tender prices, targeted for primary healthcare institutions, to tier 2 and 3 hospitals. The implication for “top-to-bottom” linkage is that manufacturers cannot choose to forfeit the primary (EDL) market, which up until now, has been a strategy chosen by many MNCs. As such, as “top-to-bottom” linkage is implemented across provinces, manufacturer choosing not to participate in EDL tenders could stand to lose the entire tier 2 and 3 hospital market as well. This is without saying, a loss too huge to bear, even if off-cycle procurement is possible. For future round of tenders, “left-to-right” linkage will be present with an unquestioned forced, the only challenge left to resolve will remain with how to identify a reasonable number of and exact reference provinces. Similarly, expanded roll-out for ‘top-to-bottom’ linkage is also expected in the future. Under the expanded EDL and broadened scope of application to tier 2 and 3 hospitals, there will be renewed efforts to unify price within a province. As such, with rising command of overall market share and linkage to the larger tier 2 and 3 hospital sector, MNCs need to take a critical re-assessment internal EDL tendering capabilities, as it becoming harder and harder to forfeit the primary market.

Winner Takes All: Granting Exclusive Access to One Supplier

One of the most criticized initiatives observed in previous rounds of provincial tenders is “winner takes all” – the practice of granting the right to supply an entire province to a lone manufacturer. Although this practice provides ammunition to lower prices, it also serves as a ticking time-bomb with respect to product quality and steady supply – consequences most felt by patients and consumers. Provinces are slowing waking up to the dire repercussions afforded by this dangerous practice, and have made revision accordingly. In the last Beijing provincial tendering, this commitment was indeed lifted: two manufacturers are now able to win the bid for a single formulation of a tendered molecule, one with highest overall score and one with the lowest bid price. In recent contact with provincial tendering officers, we received directional messages to indicate in future tenders, the total number of manufacturers permitted to win the bid will vary depending on the total number of manufacturers participating in the tender. Furthermore, up to 3 manufacturers, at most, can be bid winners. So it seems, with enough industry voice, that the detrimental practice of “winner takes all” may be nullified after all.

8

WHITE PAPER CHINA

IMS CONSULTING GROUP Exploring Impacts of the Revised EDL and Associated Policies

Source: IMS data, IMS Analysis

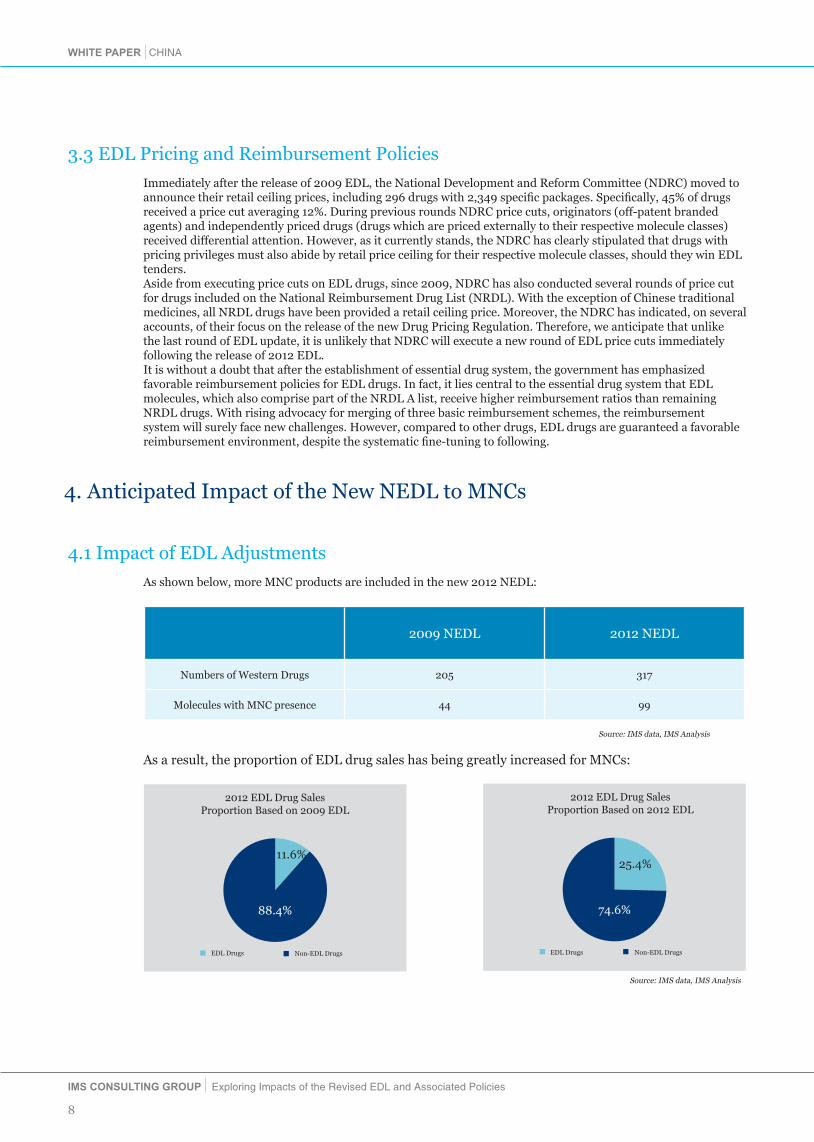

4. Anticipated Impact of the New NEDL to MNCs

4.1 Impact of EDL Adjustments

As shown below, more MNC products are included in the new 2012 NEDL:

As a result, the proportion of EDL drug sales has being greatly increased for MNCs:

88.4%

11.6%

2012 EDL Drug Sales Proportion Based on 2009 EDL

EDL Drugs Non-EDL Drugs

2012 EDL Drug Sales Proportion Based on 2012 EDL

EDL Drugs Non-EDL Drugs

74.6%

25.4%

Source: IMS data, IMS Analysis

3.3 EDL Pricing and Reimbursement Policies

Immediately after the release of 2009 EDL, the National Development and Reform Committee (NDRC) moved to announce their retail ceiling prices, including 296 drugs with 2,349 specific packages. Specifically, 45% of drugs received a price cut averaging 12%. During previous rounds NDRC price cuts, originators (off-patent branded agents) and independently priced drugs (drugs which are priced externally to their respective molecule classes) received differential attention. However, as it currently stands, the NDRC has clearly stipulated that drugs with pricing privileges must also abide by retail price ceiling for their respective molecule classes, should they win EDL tenders.Aside from executing price cuts on EDL drugs, since 2009, NDRC has also conducted several rounds of price cut for drugs included on the National Reimbursement Drug List (NRDL). With the exception of Chinese traditional medicines, all NRDL drugs have been provided a retail ceiling price. Moreover, the NDRC has indicated, on several accounts, of their focus on the release of the new Drug Pricing Regulation. Therefore, we anticipate that unlike the last round of EDL update, it is unlikely that NDRC will execute a new round of EDL price cuts immediately following the release of 2012 EDL.It is without a doubt that after the establishment of essential drug system, the government has emphasized favorable reimbursement policies for EDL drugs. In fact, it lies central to the essential drug system that EDL molecules, which also comprise part of the NRDL A list, receive higher reimbursement ratios than remaining NRDL drugs. With rising advocacy for merging of three basic reimbursement schemes, the reimbursement system will surely face new challenges. However, compared to other drugs, EDL drugs are guaranteed a favorable reimbursement environment, despite the systematic fine-tuning to following.

2009 NEDL 2012 NEDL

Numbers of Western Drugs 205 317

Molecules with MNC presence 44 99

9

WHITE PAPER CHINA

IMS CONSULTING GROUP Exploring Impacts of the Revised EDL and Associated Policies

Molecules with MNC presence in 2012 NEDL have achieved much higher growth than those in 2009 NEDL.

Moreover, the market share of MNC products has also increased significantly:

Source: IMS data, IMS Analysis

2008 2009 2010 2011 2012

2012 NEDL MNC Presence – 99 MoleculePast 5 Years Market Performance

43%44%

45%45%

45%

27.6

32.9

38.342.3

48.6

57%56%

55%55%

55%

15.2%

Unit: billion RMB

MNC Proudect

MNC Proudect

Local Proudect

Local Proudect

2008 2009 2010 2011 2012

2009 NEDL MNC Presence – 44 MoleculePast 5 Years Market Performance

12.7%

22%

25.029.3

33.4 35.3

40.4

22%21%

20%18%

78%78%

79%80%

82%

Unit: billion RMB

Source: IMS data, IMS Analysis

A few star products are also listed in the 2012 NEDL, we have listed the top 10 MNC new additions, based on 2012

hospital purchase value, below:

Through the above analysis, we conclude that the new NEDL may pose substantial impact to MNCs. As such, it is

crucial for MNCs to invest more resources and energy into the EDL market, to drive future success in China.

NO. Product Name Company

1

2

3

4

5

6

7

8

9

10

PLAVIX

GLUCOBAY

AVELOX

NOVOLIN 30R

NORVASC

DIOVAN

DIPRIVAN

DIANEAL PD-2

ELOXATIN

VOLUVEN

Sanofi

Bayer

Bayer

Novo

Pfizer

Novartis

Astrazeneca

Baxter

Sanofi

Fresenius Kabi

Note:* AVELOX is not directly showed on the 2012 NEDL, it is classified in the group of antituberculotics

10

WHITE PAPER CHINA

IMS CONSULTING GROUP Exploring Impacts of the Revised EDL and Associated Policies

4.2 Impact of EDL Policy Evolvement

The development of the EDL market is highly contingent on the release of supporting policies and subsequent execution. IMS have identified the following policies that may significantly affect the EDL market:

•Tendering linkage with level 2 & 3 hospitals - In provinces implementing the tendering linkage, sales in higher-tier hospitals may be significantly impacted if MNC products lose EDL tenders. As a result, MNCs can no longer forfeit the primary market and must also win EDL tenders to save the more critical higher-tier hospital markets

• Requirements for EDL drug revenue ratio - In general, non-EDL drugs are more expensive than EDL drugs. To meet the required EDL drug revenue ratio, hospitals tends to prescribe much more EDL drugs, which will cause erosion of the non-EDL drug market.

• Application of new tendering mechanisms – Future evolution of the tendering arena, including changes in the “two-envelope” model, quality classification and scoring system will pose significant impact on tendering strategies and comes for MNC products. This, in-turn, will further affect market access outcomes for the entire province and country.

5. MNC’s Coping Strategies

As increasing number of MNC products are being included in the EDL, thus pinpointing the space as becoming an important portion of overall MNC business. However, due to uncertainties in policy environment and hurdles in market access, MNCs face significant challenges in the EDL market. In response, it is critical that MNCs adjust their marketing, sales, distribution, tendering, pricing as well as corporate strategies to meet these new challenges and opportunities.

Adjust tendering strategies according to new tendering policy environment

• Identify key stakeholders in the tendering process and understand his interpretation of current tendering policies and likely future trends, developing different communication strategies towards different key stakeholders

•Determine the advantages and values of MNC products compared to generics; preparation to demonstrate these value attributes points to key stakeholders through the use of concrete evidence

• Develop innovative tendering strategies to reduce potential impact from the harsh and uncertain future tendering environment

• Formulate unified national tendering and negotiation strategies to minimize potential negative impact of inter-provincial price referencing

Develop marketing strategies based on the needs of the new EDL market

• Gain a comprehensive understanding of the EDL market by analyzing trends and unmet needs of community- and county-level hospitals; generate differentiated forecasting models for different market segments

• Examine EDL policies’ impacts on MNC’s market positions; adjust understanding of therapeutic areas and market according to new market dynamics

• Analyze competitors’ EDL strategies in order to develop and implement coping strategies

Explore methods to maintain favorable national price

• Develop revenue forecast based on price and volume; explore short and long term impacts of price fluctuation on MNCs

•Closely follow NDRC’s development of pricing policies related to MNC products; actively engage key stakeholders involved in policy development to maintain independent and differential pricing status

11

WHITE PAPER CHINA

IMS CONSULTING GROUP Exploring Impacts of the Revised EDL and Associated Policies

6. IMSCG is the perfect partner to pharma companies to succeed in the EDL market

IMSCG PMA group has developed close relationship with NDRC, MoHRSS,MOH and many other government agencies. We have also collaborated with RDPAC to examine EDL tendering and pricing policies, and communicated industry recommendations to the government. We have more than 30 professional consultants with healthcare background and credentials from top universities in the world. With comprehensive understanding of China healthcare environment and rich experiences in pricing and market access projects, we could provide diverse and multi-layered consulting services focusing on client’s need.

√ IMSCG could help our clients to gain insights regarding future policy dynamics through our extensive

networks with P&MA decision-makers, assisting our clients to engage key government officials and shape future policy development

√ IMSCG is the gold standard in market measurement and sales data, which could help MNCs to track and

analyze performance of generics and competitors comparing with MNC products in different regions, hospitals and markets

√ IMSCG could help MNCs to forecast sales and explore the impacts of EDL pricing and tendering

policies as well as requirements on EDL drug sales ratio on product performances in primary care medical institutes

√ IMSCG has collaborated with clinical physicians on numerous market research projects regarding

prescription behaviors/habits and unmet needs of physicians and county hospitals, well positioned to assist MNCs to develop commercial and marketing strategies targeting the EDL market

7. End Remark

Upon release of the new EDL, MNCs should re-examine the EDL market. It is no longer a market that could be avoided. Performance in the EDL market will influence market access and sales of products, even company annual performance and future development. Therefore, MNCs should carefully interpret EDL policies and actively respond to the new policy environment, adjusting product and corporate strategies to meet new challenges and opportunities.

Abbott Allergan Astellas AstraZenecaBaxter Bayer Healthcare Biogen Boehringer-IngelheimBristol-Myers Squibb CSL Biotherapies Celgene EISAIDaiichi Sankyo Eli Lilly Freseniuskabi GE HealthcareGlaxoSmithKline Gedeon Richter Ipsen LEO PharmaH. Lundbeck A/S Merck Serono MSD MundipharmaNovartis Novo Nordisk Pfizer RocheSanofi Santen Servier UCB Takeda Dainippon Sumitomo Xian-Janssen Genzyme Chugai Pharmaceutical

Appendix:RDPAC Member Company List

WHITE PAPER CHINA

IMS CONSULTING GROUP Exploring Impacts of the Revised EDL and Associated Policies

GLOBAL PERSPECTIVE & LOCAL INTELLIGENCE

IMSCG P&MA will assist you to achieve excellence in China!

IMS Cousulting Group

Pricing & Market Acess Meng Zhang Senior Principale-mail : [email protected]

Shanghai Office: 41/F The Center,No.989 Changle Road +86(21)3325-2288

Beijing Office:26/F Central Tower, China Overseas Plaza, No.8 Guanghuadongli, Jianguomenwai Avenue, Chaoyang District+86(10)8567-4500

IMSCG Pricing & Marketing Access (IMSCG P&MA) is the largest consulting group dedicating on drug pricing and market access. Professional industry consulting team, experienced intelligence and peculiar global perspective will help you achieve excellence and win-win aspiration

Professional Consultant

There are more than 30 professional consultants in IMS P&MA team, most of whom are with medical related background graduated from world top universities. They concentrate on analyzing China’s healthcare policy landscape, possess extensive project experience on drug pricing and market access, and provide comprehensive services based on clients’ demands

Extensive Industry Cooperationt

With concentration on and love of pharma industry, IMSCG P&MA becomes the leader among consulting groups. Sustainable cooperation with famous MNCs has been generated. Abundant deep-dive investigations has been conducted authorized by industry associations to assess China’s policy environment, and the results has been agreed and appreciated by most industry experts

Statistics support

As the leader of medical data supplier, IMS has been providing the most perfect medical reports and suggestions to healthcare industry for more than 55years covering 100+ countries around the world. Leveraging the data advantage, IMSCG P&MA provides more comprehensive and accurate analysis of China’s medical market

Well Developed Relationship

In China, IMS P&MA has built up strong relationships and long term communication scheme with related gov’t authorities, such as NRDC, MoHRSS, and MoH etc. And most of the suggestions provided by P&MA, representing the industry voice, have been accepted by the gov’t, which has made outstanding contributions to the development of pharma industry

Distinctive Global Perspective

IMSCG P&MA has branches in Europe, Africa, Asia and America providing consulting services in over 100 countries. International mature consulting tools, scientific analysis approach and extensive management experience could bring local clients the global perspectives and international concepts and help develop market access strategies

Comprehensive policy analysis

Rooted in the China market for years, IMSCG P&MA possesses thorough understanding of China policy environment, knows well about relevant government authorities, and develops profound and distinctive policy insights. Valuable messages and recommendations are delivered to help local clients to adapt to evolving environment and seize opportunities.

IMSCG Pricing & Market Access Team