Explicit and Implicit Incentives: Longitudinal Evidence … research does not distinguish between...

31

Explicit and Implicit Incentives: Longitudinal Evidence from NCAA Football Head Coaches Employment Contracts Presented by Dr Brian Cadman Assistant Professor University of Utah # 2013/14-17 The views and opinions expressed in this working paper are those of the author(s) and not necessarily those of the School of Accountancy, Singapore Management University.

Transcript of Explicit and Implicit Incentives: Longitudinal Evidence … research does not distinguish between...

Explicit and Implicit Incentives:

Longitudinal Evidence from NCAA Football Head Coaches Employment Contracts

Presented by

Dr Brian Cadman

Assistant Professor University of Utah

# 2013/14-17

The views and opinions expressed in this working paper are those of the author(s) and not necessarily those of the School of Accountancy, Singapore Management University.

Explicit and Implicit Incentives: Longitudinal Evidence from NCAA Football Head

Coaches Employment Contracts

Brian Cadman

David Eccles School of Business, University of Utah

Gavin Cassar

INSEAD

Early draft: Please do not distribute

Abstract

We study the role of explicit and implicit incentives in a competitive labor market with no

internal promotion opportunities. We find that explicit incentives explain only a small fraction of

the total incentives, as the likelihood of new employment on better terms and renegotiation of

current employment on better terms increases following good performance. We also find the

likelihood of renegotiation versus changing employment on better terms is dependent on the

institutional characteristics and their willingness to pay in the market for labor. Our findings

demonstrate the role of renegotiation and the relative strength of labor market forces compared to

ex-ante pay-for-performance in the presence of strong external labor market incentives. Further,

our results suggest that conclusions regarding the optimal use of explicit incentives in pay-for-

performance may be substantially overstated when not considering the role of external labor

market incentives.

2

―The manager of a firm, like the coach of any team, may not suffer any immediate gain

or loss in current wages from the current performance of his team, but the success or failure of

the team impacts his future wages, and this gives the manager a stake in the success of the team.‖

Fama (1980) Journal of Political Economy, p.292.

1. Introduction

Explicit (contractible) and implicit (non-contractible) incentives motivate an agent’s

effort. For example, CEOs can be incentivized by ex-ante specified explicit bonus terms, or

implicitly incentivized by expectations of being ex-post settled-up by the board after observed

performance or by the presence of external labor markets that offer better future employment

terms. While understanding of the mix of total incentives is critical, outside of some notable

exceptions (e.g., Gibbons and Murphy, 1992; Rajgopal, Shevlin and Zamora, 2006), much of the

prior research does not distinguish between ex-ante and ex-post determined compensation or

consider the role of implicit external labor market incentives when determining the optimal use

of explicit incentives. Evidence on the importance of explicit and implicit incentives is limited

due to a lack of observability of explicit incentives and subsequent renegotiation (Gillan, Hartzell

and Parrino, 2009: 1630), difficulty to observe career outcomes beyond current employment, and

a lack of precision of expected implicit incentives associated with career concerns. To provide

evidence on implicit incentives in contracting, we use the labor market for National Collegiate

Athletic Association (NCAA) football head coaches. We investigate how the implicit incentives

from external labor market forces affect the use and importance of explicit incentives in

compensation.

We report three important findings. First, we document the characteristics and magnitude

of explicit incentives in head coaches’ contracts. We observe the mean (median) maximum

explicit incentives for head coaches to be 36% (29%) of the total fixed component of

3

compensation. Inconsistent with the arguments of Gibbons and Murphy (1992), we find no

evidence that the relative magnitude of explicit incentives is greater when implicit incentives

from external hiring are weakest.

Second, we compare the actual change in head coach compensation with the explicit

compensation change specified in the employment contract. Examining coaches that remain in

their current employment, a common research design choice used by researchers when

examining CEO total incentives, we find the mean (median) actual change in year-to-year

compensation to be 24% (3%). However, we find substantial differences in compensation driven

by successful head coaches either accepting new employment or renegotiating their existing

employment contract on better terms, which occurs 26% and 33% on average each coach-year,

respectively. For example, coaches who renegotiate their existing contract experience a mean

(median) actual change in compensation of 75% (33%) compared to a mean (median) change of

-1% (1%) for those that do not renegotiate. More striking, when we examine coaches who move

to other institutions, we find these coaches experience a mean (median) actual change in

compensation of 264% (257%). Therefore, we demonstrate that excluding head coaches that do

not remain in their current employment year-to-year substantially understates the true

relationship between performance and pay.

Third, we model the likelihood of a head coach voluntarily terminating their current

employment to accept higher paid employment or renegotiating their existing employment

contract on better terms. We find that renegotiation is more likely when the team performs well

(high winning percentage or appearing in the national championship game in previous year) and

when the college is large (BCS institution, higher salary rank) and therefore has limited

competitors that would dominate their willingness to pay for the coach’s talent. This evidence is

4

consistent with Gibbons and Murphy (1992: 470) conjecture that renegotiation mimics one of the

effects of labor market competition. We observe the probability of higher paid employment

(institution change) is also significantly more likely when the coaches’ team performs well (high

winning percentage); however, the likelihood of institution change decreases with college size

(stadium capacity). Taken together, this suggests that relatively smaller colleges are less able or

willing to increase pay sufficiently (renegotiate) to retain better performing coaches, and that a

equilibrium exists where institutions that reap the greatest returns to performance attract and

retain the most talented coaches. We examine three alternative arguments to this small

college/large college equilibrium pay explanation: 1) that departing coaches are lesser paid in

their original employment; 2) that new colleges overpay for head coaches from other colleges;

and 3) that the original colleges would have provided this pay increase. We find no support for

any of these alternative explanations. Overall, our results show how implicit incentives become

reflected in agent compensation – either within the firm or through the external labor market – is

dependent on the characteristics of the institution that employ the coach and the market for their

labor.

Our findings provide insight on a fundamental question of labor contracting in the

presence of only external labor market incentives (no promotion opportunities). We show that in

the presence of strong external labor market incentives, explicit pay-for-performance is of

limited importance. Our evidence provides bounds for workers in other labor markets with no

internal promotion opportunities, such as CEOs, where data availability inhibit empirical

investigation of labor market contracting. Overall, we demonstrate that in the presence of strong

external incentives and renegotiation that implicit incentives (limited explicit pay-for-

5

performance) can optimally incentive workers, where a small college/large college equilibrium

exists for agent talent.

2. Research Question and Setting

2.1 Related literature

Agent effort is motivated through total incentives, which can consist of ex-ante specified

explicit or contractible incentives, and implicit or non-contractible incentives, such as the

expectation of being ex-post settled-up (compensated) by the principal after observed

performance, or an improvement of the likelihood of future promotion or better employment

terms within the firm or in the external market for labor. Yet, almost all evidence of agent

incentives, particularly CEOs, is predominately limited to the relation between organizational

performance and observable changes in wealth experienced by the agent, which may be an

outcome of explicit or implicit incentives. Further, researchers generally exclude agents that

either choose to leave or are fired from their employment – as agents must be observed in

consecutive periods to estimate the performance-pay relation within current employment – and

even for those agents that remain in their current employment, researchers generally do not

observe when explicit performance is rewarded, ex-post settling up has occurred, or

renegotiation has taken place. The primary reason for the lack of empirical investigation of the

mix of total incentives is the difficulty in observing these forces in most labor market settings.

While the relative importance of explicit and implicit incentives is generally excluded

from empirical investigations of pay and performance, there have been some notable exceptions

that have considered the interplay between explicit and implicit incentives. Gibbons and Murphy

(1992) posit and find that explicit incentives are stronger for CEOs nearing retirement, as the

6

implicit incentives from career concerns are weakest for these CEOs. Rajgopal, Shevlin and

Zamora (2006) find evidence consistent with the Oyer (2004) model that more talented CEOs

will have greater pay sensitivity to market-wide factors as they have greater external labor

market opportunities. Ederhof (2011) find that explicit bonus-based incentives are greater for

mid-level managers that face weaker implicit incentives from internal promotion. Again, while

these and other investigations provide insight into explicit and implicit incentive trade-offs, this

research does not consider the relative importance of alternative incentives or differences

between explicit incentives and ex-post settling up, nor do they consider agents that self-select

for better employment outside the firm. To provide insight into these important issues, we

examine a well-defined labor market where performance is more easily observable, contract

terms that link pay with performance are measurable, the labor market is more clearly defined,

and talent transfers across organizations more easily.

2.2 The labor market for NCAA head coaches

Sports labor markets have several empirical advantages to investigate incentives over

other labor markets, such as the market for CEOs (Kahn, 2000). First, unlike CEOs, almost all

NCAA coaches’ contracts are publicly observable (Gillian, Hartzell and Parrino, 2009), which

allows us to empirically distinguish between the ex-ante explicit incentives and any ex-post

settling up from renegotiation in actual pay outcomes (Fee, Hadlock and Pierce, 2006). By

observing renegotiation we do not require the commonly used assumption that employment

contracts are renegotiation proof (Gibbons and Murphy 1992: 470). Further, unlike CEOs,

coaches do not own stock in their institutions, which allows for more precise estimation of total

incentives in compensation and the separation of ownership and control is transparent.

7

Second, NCAA coaches are in a well-defined competitive labor market, which allows for

more accurate estimations of career concerns from labor market-based incentives. Within this

market we can observe coaches career outcomes over time, including transfer between colleges

and professional leagues, which is relatively common as coaches possess transferable talent with

limited institution-specific capital (Dutta, 2008). This longer period of observation recognizes

that several years are necessary to capture the dynamics in the pay-performance relation

(Boschen and Smith, 1995). While there is some research on job outcomes following

employment, such as senior officers of public firms (e.g., Brickley, Linck, and Coles, 1999;

Chang, Dasgupta and Hilary, 2010; Fee and Hadlock, 2004), it is difficult to observe the

employment terms for the majority of these workers.

Third, the performance metrics are well-defined and easy to observable, resulting in less

information asymmetry in the labor market and by researchers. Further, the timing of observed

performance and labor market outcomes (e.g., almost all turnover and renegotiation occurs at the

end of the football season) allows researchers to observe clear causal associations between

performance and compensation.

Finally, another important advantage of examining NCAA head coaches is an alternative

setting to CEOs to investigate incentives and contracting. The super majority of all empirical

research on incentives is based on the most senior officers of the largest publicly listed firms.

While significant focus on these officers’ incentives can be motivated by the importance of these

firms to the economy, there is lack of evidence from alternative settings, particularly settings that

are absent of regulation that affects organizations’ choice of incentives used. For example,

section 162(m) of the internal revenue code limits the tax deductibility of salaried compensation

to $1 million for senior officers of US publicly listed firms. This regulation makes it more costly

8

for these firms to use greater salaried compensation to incentivize workers, which likely distorts

the mix of incentives absent of this regulation.

3. Sample Selection and Variable Measurement

3.1 Sample

We examine employment contracts for head coaches of the NCAA Football Bowl

Subdivision (FBS). The FBS consists of 120 universities aligned in 11 conferences that each

range from 10-14 members and four independent teams with no conference affiliation (e.g. the

University of Notre Dame). Our sample spans contracts for the academic years beginning each

fall from 2006 to 2010, and include 107, 108, 110, and 109 teams in each year, respectively. The

omission of teams from the sample is due to the non-disclosure of employment contracts by

private institutions and a small subset of public institutions (e.g. the University of Southern

California). We collect several details from the contracts including annual salaried compensation

and explicit incentive bonuses, in addition to other contract terms, such as the contract length and

termination clauses.

Limiting the analysis to a homogenous labor market and setting removes heterogeneity in

the quality of available successors and ability to accurately assess coach performance (Parrino,

1997). Further, by focusing solely on head coaches we remove heterogeneity in decision-making

authority, variation in the extent of monitoring and any implicit incentives related to internal

promotion that may influence the use of explicit incentives (Ederhof, 2011). The lack of internal

promotion, in addition to other features, mirrors the implicit incentives in the labor market for

CEOs.

3.2 Compensation, Performance and Institution Measures

9

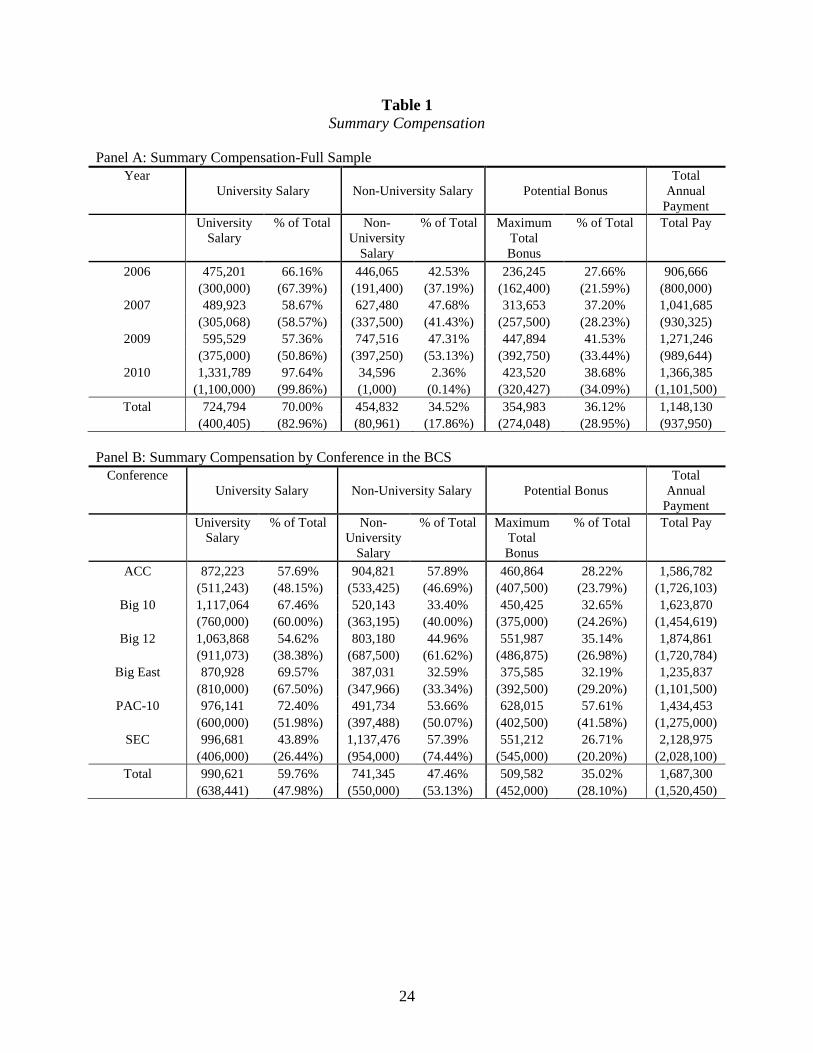

Table 1 Panel A provides summary statistics of annual compensation and the maximum

bonus the coach can earn. The mean (median) annual salary is $1,148,000 ($937,950), of which

70% (83%) is university-paid with the remaining sourced from other affiliates such as corporate

sponsors, university support groups or media organizations. The maximum bonus that an average

(median) coach can earn in a season is $354,983 ($274,048), which equates to a mean (median)

maximum potential bonus of 36% (29%) of their total salary. These bonuses include explicit

incentives associated with on-field performance (e.g. win-loss record, bowl appearances, national

and conference rankings) and off-field performance (e.g. graduation rates, attendance, etc.).

NCAA coaches’ compensation is increasing over our sample period, with the mean (median)

salaried compensation rising from $906,666 ($800,000) in 2006 to $1,366,385 ($1,101,500) in

2010. The nominal maximum potential bonus is also increasing over time such that the

proportion of maximum bonus to total salary increases slightly over the sample period.

Table 1 Panel B presents the summary compensation by athletic conference. We denote

the six Bowl Champion Series (BCS) conferences (ACC, Big 12, Big East, Big 10, Pac 10, and

SEC) that have greater access to more prestigious bowls and lucrative media rights compared to

the non-automatically qualifying (non-AQ) conferences. Consistent with BCS conference teams

attracting more talented coaches with greater reservation wages and a greater investment by the

University in the program, the mean (median) total salary for coaches of BCS teams of

$1,687,300 ($1,520,450) is significantly greater than the mean (median) total salary for non-AQ

coaches of $511,421 ($390,603). Despite the significant differences in salary between BCS and

non-AQ universities the maximum bonus as a percentage of total salary is not significantly

different, with the mean (median) bonus being 35% (28%) for BCS institutions and 37% (30%)

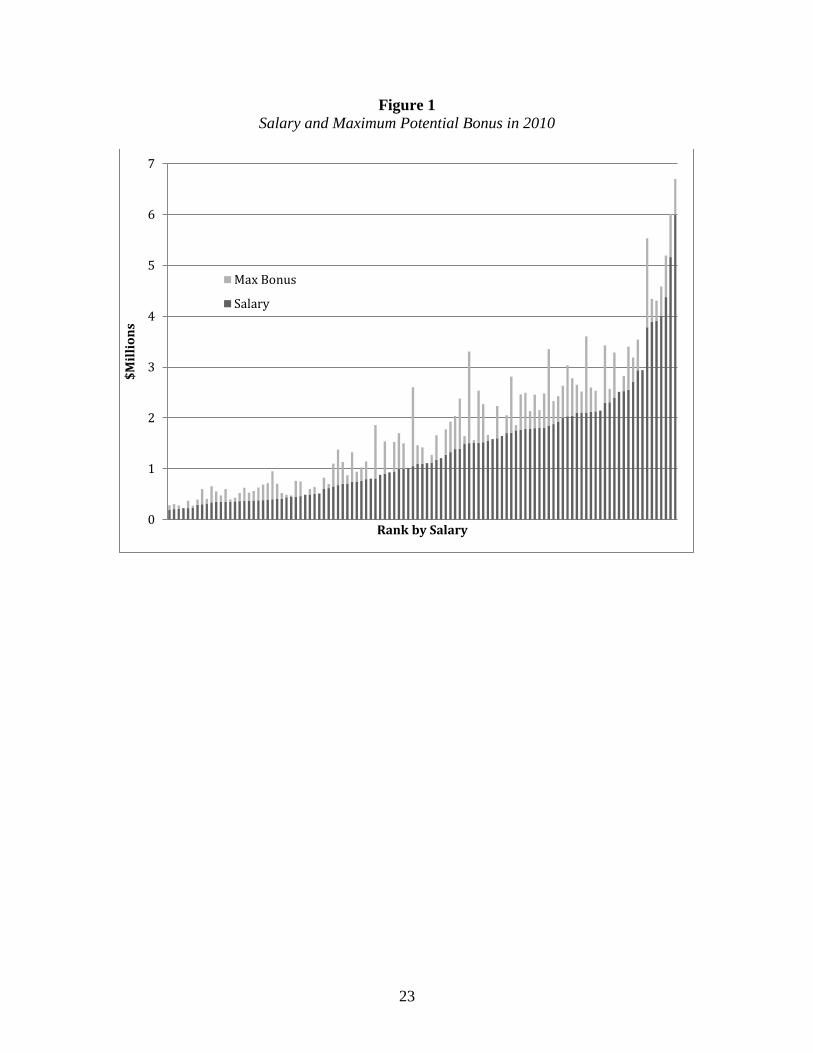

for non-AQ institutions. Figure 1 provides the salary and maximum bonus for all our coaches in

10

our most recent sample year (2010) ranked by total salary. This figure shows convexity in the

labor market salaries of NCAA football coaches. In fact, the average Pearson correlation

between total salary and the ranked salary for the NCAA football coach labor market in our

sample period is 0.98.

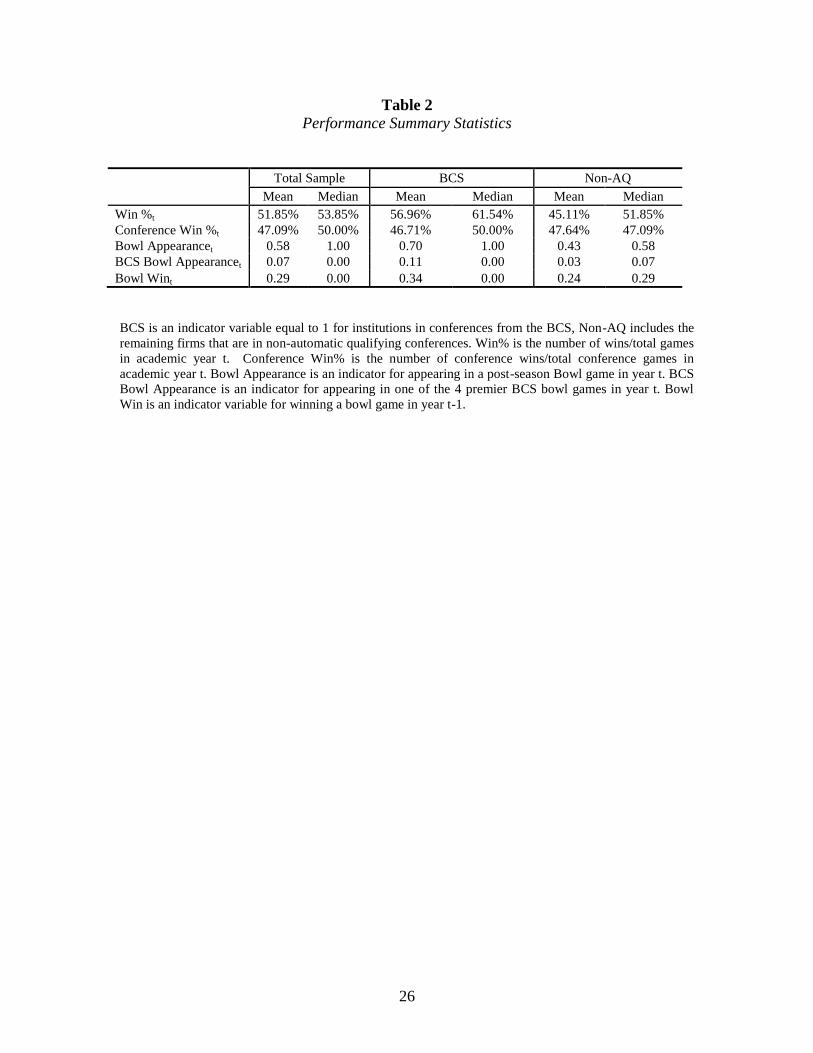

Table 2 provides the summary statistics of our performance measures. We obtain the

winning percentage, conference winning percentage, playing in a bowl game, playing in a BCS

bowl game, winning a bowl game, and appearing in the national championship game. Our

performance measures are motivated by their explicit use in our head coaches’ employment

contracts and by published research on football coach compensation, promotions and firings

(Fee, Hadlock, Pierce, 2006; Holmes, 2011). Consistent with BCS teams performing better than

Non-AQ teams, on average, the winning percentage of BCS teams is more than 10% greater than

non-AQ teams., In addition, BCS teams appear in post-season bowl games 70% of the time,

while non-AQ teams appear in a bowl game 43%. BCS teams also appear in BCS bowls and win

their bowl game more frequently than non-AQ teams.

We also measure the size of the college as it relates to their investment in the football

program. To measure the relative size of the college and its capacity to pay we use whether the

college is in a BCS or non-AQ conference, where BCS conference teams are generally larger

teams with greater investments in the program. We also measure stadium capacity, where larger

stadiums are generally associated with larger universities that invest more in their football

program. In unreported tests, the stadium capacity of BCS teams is significantly larger than non-

AQ teams.

4. Tests of Explicit and Implicit Incentives

11

4.1 Use of explicit incentives

Agent effort is motivated through the sum of explicit and implicit incentives. Implicit

incentives related to career concerns can be borne from the expectation of internal promotion

(Ederhof, 2011) or hiring outside the firm (Gibbons and Murphy, 1992). Given the lack of

internal promotion, head coaches’ implicit incentives are primarily driven by external labor

market opportunities. As implicit incentives are not a choice variable of colleges, explicit

incentives are selected after considering the implicit incentives from the labor market. Therefore,

the use of explicit incentives should be greater when the head coaches’ implicit incentives from

external hiring are weakest.

Our measure of implicit incentives from external hiring is college size. As coaches of

larger schools have less external employment options that can provide similar or better

compensation, explicit incentives should be positive associated with college size (Gibbons and

Murphy, 1992: 487). College size is captured in our analysis by total compensation, being a BCS

affiliated college, and stadium capacity.

Table 3 reports our model of explicit incentives use, as measured by the maximum

potential bonus divided by salaried compensation. With the exception of stadium capacity,

inconsistent with the arguments of Gibbons and Murphy (1992), we find little evidence that the

relative magnitude of explicit incentives is greater when implicit incentives from external hiring

are weakest. In fact, we find that bonus is a lower proportion of pay for coaches that earn more

total compensation as evidenced by a negative coefficient on total compensation and salary rank.

This puzzling finding has two potential explanations. First, the labor market for NCAA football

head coaches is broader than the college head coach positions. Specifically, the National Football

League (NFL) may provide implicit incentives to NCAA coaches, which reduces the need for

12

larger colleges to explicitly incentivize coaches. One rebuttal to this explanation is the salaries of

the high paid college coaches are generally equivalent to NFL head coaches’ salaries. Second,

the explicit incentives are of relatively minor importance in total incentives; and therefore,

examining the proportion of the bonus to total salary captures substantial noise. We explore this

latter explanation in the following section.

4.2 Change in annual compensation

While ex-ante contracted wages and explicit incentives motivate agent effort, the

contracted terms will not likely reflect the actual agent compensation in the presence of

renegotiation and external labor markets. Specifically, given the presence of a labor market for

coaches, the head coach can use observed performance to obtain better employment terms from

another college, or the current college may increase compensation to retain the coach in their

current employment. The extent explicit incentives reflect the total change of compensation

provides the importance of contractible incentives relative to renegotiation and external career

concerns. Empirical investigation of the relative importance of explicit incentives is limited

given data availability, particularly regarding observation of the ex-ante and any renegotiated

contract, performance and future employment outcomes. We use our setting and data to provide

novel empirical evidence on the importance of ex-ante incentives relative to ex-post settling up

on labor market outcomes.

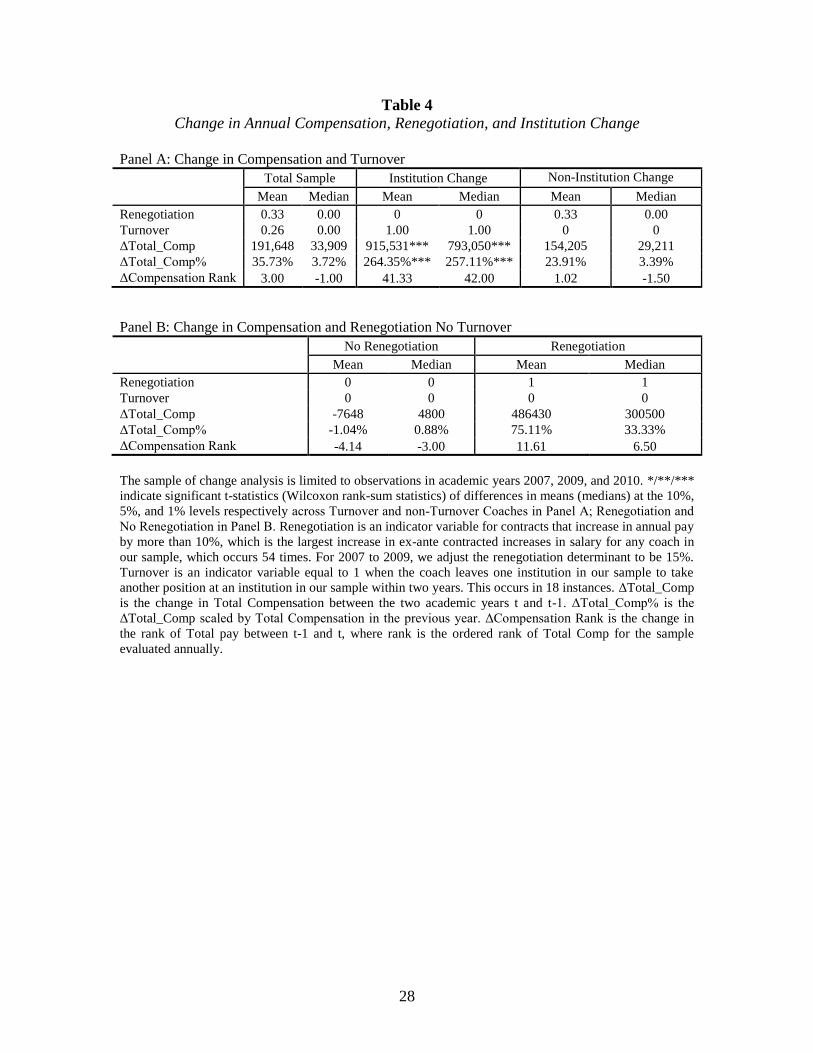

To provide a baseline in change in pay we focus in the changes in pay for coaches that

remain in our sample, either with the same institution, or a different one. The total compensation

increases on average by $191,647 or 35%. In addition, the average coach increases in ranking of

pay by 3 spots, where pay rank is an annual rank ordering of the sample based on total salary

13

paid to the coach. The median pay rank is -1 indicating that the median coach drops one place in

the pay ranking.

4.2.1 Change in annual compensation due to renegotiation

Because all contracts in our sample are ―multiple year‖ contracts we can identify

contracts that are renegotiated. Specifically, we identify renegotiations by comparing the terms

of the contract in the previous year with the following year and by also examining the execution

date of most recent coach’s employment contract. In cases where the new contract varies from

the terms of the prior contract in length or salary, we label the contract as renegotiated. For the

243 coach-institutions in our sample that remain over multiple seasons, we identify 121

renegotiations (approximately 50%).

Table 4 reports changes in compensation for our sample and several sub-groups.

Examining coaches that remain in their current employment, a common research design choice

used by researchers when examining CEO total incentives, we find the mean (median) actual

change in year-to-year compensation to be 24% (3%), which equates to a mean (median)

increase in salary of $154,205 ($29,210). However, this mean change masks significant variation

in compensation changes across these coaches. As shown in Table 4 Panel B, coaches who

renegotiate their existing contract experience a mean (median) actual change in compensation of

75% (33%) compared to a mean (median) change of -1% (1%) for those that do not renegotiate.

Coaches that renegotiate their existing employment terms increase their mean (median)

compensation by $486,430 ($300,500) and increase their pay ranking in the NCAA head coach

labor market by 12 (7) mean (median) places.

14

4.2.2 Change in annual compensation due to institution change

An important advantage of the football coaches labor market over more commonly

investigated settings, such as CEOs, is the observation of agents’ employment outcomes after

their current employment. This limitation of other labor market settings almost always requires

researchers to deliberately exclude agents that leave their current employment in the following

year. For example, when investigating CEO pay-for-performance relations, CEOs that leave their

current employment due to being fired, hired at another firm or retired are removed from the

sample. This common research design choice that is driven by lack of data availability could

substantially distort the true relation between pay and performance.

We observe coaches changing institutions 20% of the time for 84 turnovers. Of the 84

turnovers in our sample, the coach moves to another institution in our sample within 1 season in

9 cases and moves to another institution within our sample in another 9 cases. In 14 cases, the

coach leaves their existing institution to join an organization in the National Football League. In

the remaining cases, the coach is either out of the market, or it takes longer than two years before

landing a coaching job at another FBS institution.

Table 4 Panel B shows that when coaches that change institutions to another head coach

position in our sample within two years they experience a mean (median) actual change in

compensation of 264% (257%), which equates to an increase in salary of $915,000 ($793,050)

and an increase in salary rank in the labor market by 41 (42) places.

Together, the results in changes in pay and turnovers support the conjecture that the labor

market is a strong source of incentives. That is, large increases in pay exist when coaches move

institutions. These findings demonstrate that in a labor market setting with a non-trivial

likelihood of external hiring and/or termination of employment the common research design

15

choice of excluding agents that do not remain in the same organization in consecutive years

substantially understates the true relation between pay-for-performance. Therefore, research that

does not consider how these sample choices distort the observed pay-for-performance may

substantially under-report the true convexity from total incentives. Overall, we find substantial

differences in compensation driven by successful head coaches either accepting new

employment or renegotiating their existing employment contract on better terms, which occurs

26% and 33% on average each coach-year, respectively. We explore the likelihood of these

outcomes in the following section.

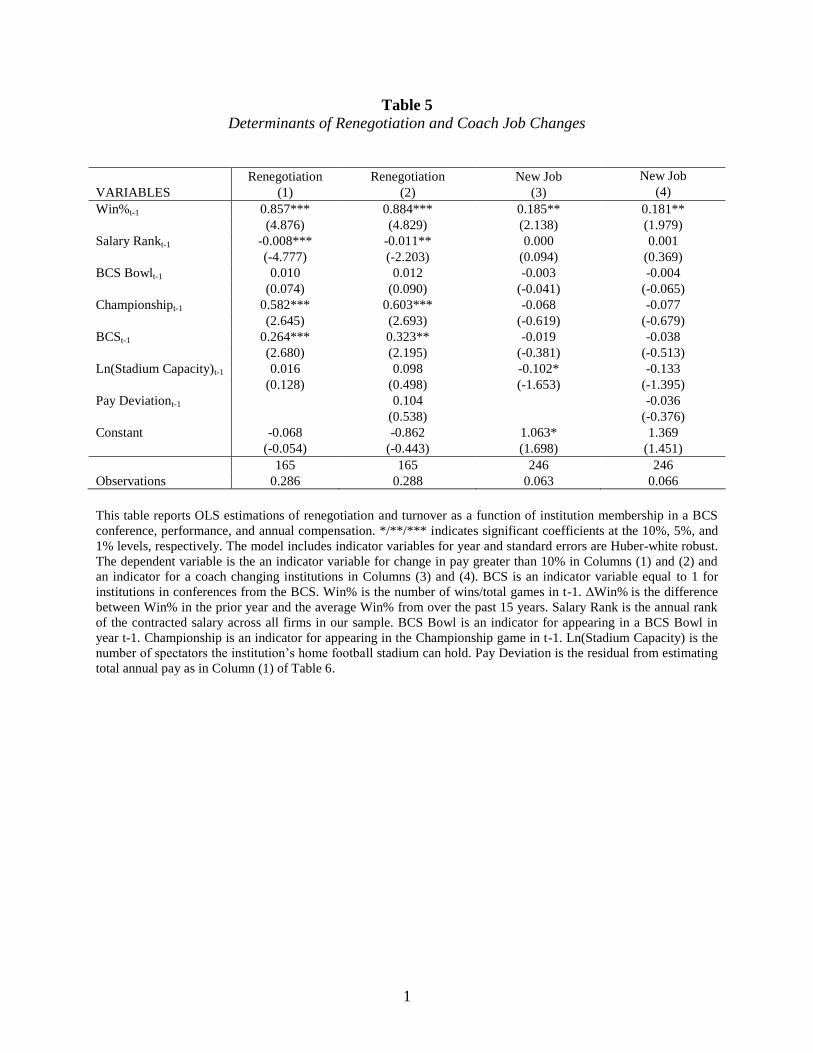

4.3 Likelihood of higher paid employment and renegotiation

We model both the likelihood of a head coach movement to higher paid employment or

renegotiating their existing employment contract on better terms as a function of the coach’s

team performance and college characteristics. Table 5 shows that the likelihood of renegotiation

is more likely when the coaches’ team has a higher winning percentage or appears in the national

championship game in the previous year. This evidence is consistent with Gibbons and Murphy

(1992: 470) conjecture that renegotiation mimics one of the effects of labor market competition.

We also find that likelihood of renegotiation is increasing in the size of the college, as

represented by the college being in a BCS conference and having a lower salary rank. This

evidence is consistent with renegotiation being more likely when the college has limited

competitors for the coach’s talent. At the same time, renegotiation is negatively related with the

salary rank. This suggests there is a ceiling in the market for coaches, where coaches at the

highest pay scale do not renegotiate their contracts even after strong performance.

Table 5 column 3 shows that the likelihood of higher paid employment (institution

change) is also significantly more likely when the coaches’ team performs well (higher winning

16

percentage in the previous year). However, the likelihood of institution change decreases with

college size (stadium capacity). Taken together, this suggests separating equilibrium across the

labor market where relatively smaller colleges are less able or willing to increase pay sufficiently

(renegotiate) to retain better performing coaches; and consequently, better performing coaches

leave for higher paying jobs in colleges that have greater capacity to pay. This suggests that

better performing coaches are more likely to leave current employment if there are more external

labor market opportunities to improve their employment terms. Overall, our results show how

implicit incentives become reflected in agent compensation – either within the firm or through

the external labor market – is dependent on the agent’s firm characteristics in the market for their

labor.

4.3.1 Alternative explanations

We examine three alternative explanations to this small college/large college equilibrium

pay story: 1) that departing coaches are lesser paid in their original employment; 2) that new

colleges overpay for head coaches from other colleges; and 3) that the original colleges would

have provided this pay increase.

First, we calculate the deviation in the coach’s salary from a model of expected total

compensation. Specifically, we estimate expected compensation for the coach in the year before

renegotiation or institution change, to determine if the coach’s action was in part due to being

relatively under paid in their original employment.

Table 6 Model 1 presents results from estimating expected compensation as a function of

performance in the prior year and college characteristics. Consistent with the univariate statistics,

we find total compensation is greater for college coaches in BCS conferences, coaches of

colleges with greater stadium capacity and those coaches that have a higher winning percentage

17

in recent years. The coefficient of 0.629 suggests that coaches of BCS teams earn $293,000 more

in annual compensation than coaches of teams that are non-AQ. Turning to performance, we find

that overall winning percentage is positively related to annual pay. Inspecting the coefficients

indicates that winning one more game in the regular season, which increases the winning

percentage by about 10% for a 10-game season is related to an increase in pay of $238,000, on

average. However, other measures of performance including bowl appearances and wins do not

relate to compensation levels. The overall explanatory power of our expectation model of total

compensation is reasonable, with an r-squared of 0.73.

We calculate the deviation in the coach’s salary from the Table 6 Model 1 of coaches

expected total compensation in the previous year to determine if it influences their career

outcomes. Examining the estimates from Table 5 column 2 and 4 we find no support that the

likelihood of renegotiation or institution change increases in the deviation from the expected

salary, suggesting that departing coaches are no lesser or better paid on average.

A second alternative to the separating equilibrium pay explanation is that colleges

overpay new coaches relative to optimal to entice them to leave their existing employment. To

test this explanation, in Column (2) we include an indicator for coach turnovers as an additional

covariate in the total compensation model. Specifically, if the coefficient on turnover is positive,

controlling for college characteristics and performance, this would suggest that colleges pay new

coaches greater than their expected pay to entice the coach to leave their original employment.

Examining the estimated coefficient for turnover, while the results found in Column (1) remain,

there is not a significant relation between annual pay and turnovers, This results suggests that

colleges compensate their coaches based on the economic determinants in a consistent manner

regardless of the stability of the coaching position.

18

A third alternative is that the increase in pay associated with turnover was likely to occur

regardless of the institution change, as the original institution would have ex-post settled up the

coach by paying a higher salary in future periods. To explore the relevance of this explanation

we model the change in coaches compensation as a function of the coach’s team’s recent

performance and college characteristics. If turnover, in and of itself, is not an important

determinant of change in coach pay we should not find an association between turnover and pay

change after controlling for recent performance. The results of this analysis are presented in

Table 6 column 3. Consistent with the univariate change in compensation, column 3 shows that

after controlling for the recent performance of the coach’s team, coaches that change institutions

experience a substantial increase in compensation. Therefore, we conclude our evidence is

consistent with large explicit incentives in the labor market for well-performing coaches.

5. Extensions

5.1 Explicit incentives

Our primary measure of explicit incentives is the maximum potential bonus divided by

annual salaried compensation. Obviously, it is infeasible for all coaches in our sample to receive

their maximum potential bonus, as most incentive bonuses are conditional on on-field

performance, such as winning games or championships. We selected this maximum bonus

measure to provide an upper bound of the importance of ex-ante explicit incentives, thereby

ensuring that our finding of explicit incentives being of limited importance was not driven by our

choice of estimating the likelihood of achieving various explicit bonuses. Therefore, while we

observe explicit incentives explain a small fraction of the total incentives, the expected explicit

component of total incentives is likely to be substantially smaller than reported.

19

In unreported results, we consider two alternative explicit incentive measures. First, we

consider an expectation model where all teams have an equal chance of winning every football

game, with all remaining unobservable off-field performance recorded at its maximum potential

bonus. Second, we consider an expectation model where teams’ likelihood of winning is based

on their historical performance over the previous 20 years. In unreported tests, all the cross-

sectional findings are invariant to using the alternative explicit incentive measures discussed

above.

5.2 Time horizon

Our main empirical results report the change in head coaches’ compensation in the year

following observed performance. Given the change in compensation observed is primarily driven

by the variation in coaches’ annual salaries – due to renegotiation or better employment – the

implications of the change in compensation is not limited to the following year. Rather, the

observed change influences all future year’s compensation both contractually and in expectation

(Gibbons and Murphy, 1992: 470). Therefore, the relative importance of implicit incentives is

likely to be greater than reported in this study. Future analysis can incorporate empirical

expectations of the likelihood of renegotiation, better employment, remaining on the existing

employment terms and involuntary termination with the distribution of expected compensation

for each of these job outcomes.

6. Conclusion

We provide novel evidence of the importance of explicit and implicit incentives in

contracting. We find that explicit pay-for-performance is of limited importance in the presence of

strong external implicit labor market incentives. Using the empirical advantages of the labor

20

market for NCAA head football coaches, we capture significant variation in agent compensation

and incentives not previously observed in pay-for-performance research. Specifically, by

observing agents’ renegotiation following good performance and their career outcomes after

current employment, we document substantial convexity in the pay-for-performance relation

driven predominantly by implicit incentives.

Our findings provide insight on a fundamental question of labor contracting in the

presence of external labor market incentives excluding internal promotion opportunities.

Obviously, the relative importance of ex-ante explicit incentives and ex-post settling up through

contract renegotiation will vary across labor markets conditional on many factors, including the

observability and noise of performance, transferability of human capital and the convexity in the

distribution of labor market compensation. Therefore, in settings where performance

observability is low and noise greater, there is limited transferable (greater institutional specific)

human capital and minimal pay convexity in the labor market, the importance of implicit

incentives should be reduced. In this regard, our evidence provides bounds for other labor

markets with no internal promotion opportunities, such as CEOs, where data availability inhibit

empirical investigation of labor market contracting. Overall, we demonstrate that in the presence

of strong external incentives and renegotiation that limited explicit pay-for-performance can

optimally incentivize workers.

21

References:

Boschen, J. F. and Smith, K. J. 1995. You can pay me now and you can pay me later: The

dynamic response of executive compensation to firm performance. Journal of Business

68(4): 577-608.

Brickley, J. A., Linck, J. S., and Coles, J. L. 1999. What happens to CEOs after they retire? New

evidence on career concerns, horizon problems, and CEO incentives. Journal of Financial

Economics 52(3): 341-377.

Chang, Y. Y., Dasgupta, S., and Hilary, G. 2010. CEO ability, pay, and firm performance.

Management Science 56(10): 1633-1652.

Ederhof, M. 2011. Incentive compensation and promotion-based incentives of mid-level

managers: Evidence from a multinational corporation. The Accounting Review 86(1): 131-

153.

Fama, E. F. 1980. Agency problems and the theory of the firm. Journal of Political Economy

88(2): 288-307.

Fee, C. E. and Hadlock, C. J. 2004. Management turnover across the corporate hierarchy.

Journal of Accounting and Economics 37(1): 3-38.

Fee, C. E., Hadlock, C. J., and Pierce, J. R. 2006. Promotions in the internal and external labor

market: Evidence from professional football coaching careers. Journal of Business 79(2):

821-850.

Gibbons, R. 2005. Incentives between firms (and within). Management Science 51(1): 2-17.

Gibbons, R. and Murphy, K. T. 1992. Optimal incentive contracts in the presence of career

concerns: Theory and evidence. Journal of Political Economy 100(3): 468-505.

Gillan, S. L., Hartzell, J. C., and Parrino, R. 2009. Explicit versus implicit contracts: Evidence

from CEO employment agreements. Journal of Finance 64(4): 1629-1655.

Hall, B. J. and Liebman, J. B. 1998. Are CEOs really paid like bureaucrats? Quarterly Journal of

Economics 113(3): 653-691.

Holmes, P. 2011. Win or go home: Why college football coaches get fired. Journal of Sports

Economics 12(2): 157-178.

Holmstrom, B. 1982. Managerial incentives schemes—a dynamic perspective. In Essays in

Economics and Management in Honor of Lars Wahlbeck. Helsinki: Swenska

Handelsho¨gkolan.

22

Inoue, Y., Plehn-Dujowich, J. M., Kent, A. and Swanson, S. 2012. Roles of performance and

human capital in college football coaches’ compensation. Journal of Sports Management

27(1): 73-83.

Kahn, L. M. 2000. The sports business as a labor market laboratory. Journal of Economic

Perspectives 14(3): 75-94.

Kahn, L. M. 2007. Markets: Cartel behavior and amateurism in college sports. Journal of

Economic Perspectives 21(1): 209-226.

Oyer, P. 2004, Why do firms use incentives that have no incentive effects? Journal of Finance

59(4): 1619–1649.

Parrino, R. 1997. CEO turnover and outside succession: A cross-sectional analysis. Journal of

Financial Economics 46(2): 165-197.

Rajgopal, S., Shevlin, T. and Zamora, V. 2006. CEOs’ outside employment opportunities and the

lack of relative performance evaluation in compensation contracts. Journal of Finance 61(4):

1813-1844.

23

Figure 1

Salary and Maximum Potential Bonus in 2010

0

1

2

3

4

5

6

7

$M

illi

on

s

Rank by Salary

Max Bonus

Salary

24

Table 1

Summary Compensation

Panel A: Summary Compensation-Full Sample

Year

University Salary Non-University Salary Potential Bonus

Total

Annual

Payment

University

Salary

% of Total Non-

University

Salary

% of Total Maximum

Total

Bonus

% of Total Total Pay

2006 475,201 66.16% 446,065 42.53% 236,245 27.66% 906,666

(300,000) (67.39%) (191,400) (37.19%) (162,400) (21.59%) (800,000)

2007 489,923 58.67% 627,480 47.68% 313,653 37.20% 1,041,685

(305,068) (58.57%) (337,500) (41.43%) (257,500) (28.23%) (930,325)

2009 595,529 57.36% 747,516 47.31% 447,894 41.53% 1,271,246

(375,000) (50.86%) (397,250) (53.13%) (392,750) (33.44%) (989,644)

2010 1,331,789 97.64% 34,596 2.36% 423,520 38.68% 1,366,385

(1,100,000) (99.86%) (1,000) (0.14%) (320,427) (34.09%) (1,101,500)

Total 724,794 70.00% 454,832 34.52% 354,983 36.12% 1,148,130

(400,405) (82.96%) (80,961) (17.86%) (274,048) (28.95%) (937,950)

Panel B: Summary Compensation by Conference in the BCS

Conference

University Salary Non-University Salary Potential Bonus

Total

Annual

Payment

University

Salary

% of Total Non-

University

Salary

% of Total Maximum

Total

Bonus

% of Total Total Pay

ACC 872,223 57.69% 904,821 57.89% 460,864 28.22% 1,586,782

(511,243) (48.15%) (533,425) (46.69%) (407,500) (23.79%) (1,726,103)

Big 10 1,117,064 67.46% 520,143 33.40% 450,425 32.65% 1,623,870

(760,000) (60.00%) (363,195) (40.00%) (375,000) (24.26%) (1,454,619)

Big 12 1,063,868 54.62% 803,180 44.96% 551,987 35.14% 1,874,861

(911,073) (38.38%) (687,500) (61.62%) (486,875) (26.98%) (1,720,784)

Big East 870,928 69.57% 387,031 32.59% 375,585 32.19% 1,235,837

(810,000) (67.50%) (347,966) (33.34%) (392,500) (29.20%) (1,101,500)

PAC-10 976,141 72.40% 491,734 53.66% 628,015 57.61% 1,434,453

(600,000) (51.98%) (397,488) (50.07%) (402,500) (41.58%) (1,275,000)

SEC 996,681 43.89% 1,137,476 57.39% 551,212 26.71% 2,128,975

(406,000) (26.44%) (954,000) (74.44%) (545,000) (20.20%) (2,028,100)

Total 990,621 59.76% 741,345 47.46% 509,582 35.02% 1,687,300

(638,441) (47.98%) (550,000) (53.13%) (452,000) (28.10%) (1,520,450)

25

Panel C: Summary Compensation by Conference in the non-AQ

Conference University Salary Non-University Salary Potential Bonus

Total

Annual Pay

University

Salary

% of Total Non-

University

Salary

% of Total Maximum

Total

Bonus

% of Total Total Pay

CUSA 507,172 71.54% 232,325 29.96% 238,173 35.57% 721,758

(379,000) (85.68%) (64,400) (16.70%) (232,167) (34.55%) (560,060)

Independent 630,668 88.89% 57,143 14.29% 250,000 62.50% 675,113

(640,851) (100.00%) (0) (0.00%) (225,000) (56.25%) (640,851)

MAC 243,315 89.07% 33,032 11.16% 162,207 58.12% 275,673

(200,850) (95.23%) (12,250) (5.70%) (140,000) (52.75%) (269,062)

MWC 599,681 75.18% 188,175 27.53% 270,209 36.69% 772,264

(500,000) (97.51%) (75,000) (15.96%) (171,625) (31.23%) (700,000)

Sun Belt 248,183 89.26% 26,837 11.06% 56,998 20.82% 274,254

(225,750) (96.23%) (8,650) (3.81%) (50,000) (18.75%) (261,000)

WAC 474,375 81.60% 100,707 18.92% 140,950 25.94% 572,285

(371,546) (90.43%) (46,810) (9.71%) (110,000) (15.85%) (390,663)

Total 409,293 82.16% 108,000 18.86% 171,135 37.44% 511,421

(305,822) (95.27%) (23,250) (8.77%) (125,000) (29.57%) (390,603)

The sample consists of …

University Salary is the Annual compensation paid by the University, Non-University Salary includes compensation

paid by corporate sponsors, media, and other organizations that are involved with the University and pay a portion

of the coache’s salary directly. Potential Bonus is the maximum bonus the coach can earn in a year for achieving

performance goals such as winning percentage, conference championships, bowl appearance, and national rankings.

Total Annual Pay is the sum of University and Non-University Salary. Panel A includes all teams in our sample

separated by academic year. Panel B reports summary statistics for each conference included in the Bowl

Championship Series. Panel C reports summary statistics for universities in conferences that are not automatic

qualifiers, but remain in the Football Championship Series (FBS).

26

Table 2

Performance Summary Statistics

Total Sample BCS Non-AQ

Mean Median Mean Median Mean Median

Win %t 51.85% 53.85% 56.96% 61.54% 45.11% 51.85%

Conference Win %t 47.09% 50.00% 46.71% 50.00% 47.64% 47.09%

Bowl Appearancet 0.58 1.00 0.70 1.00 0.43 0.58

BCS Bowl Appearancet 0.07 0.00 0.11 0.00 0.03 0.07

Bowl Wint 0.29 0.00 0.34 0.00 0.24 0.29

BCS is an indicator variable equal to 1 for institutions in conferences from the BCS, Non-AQ includes the

remaining firms that are in non-automatic qualifying conferences. Win% is the number of wins/total games

in academic year t. Conference Win% is the number of conference wins/total conference games in

academic year t. Bowl Appearance is an indicator for appearing in a post-season Bowl game in year t. BCS

Bowl Appearance is an indicator for appearing in one of the 4 premier BCS bowl games in year t. Bowl

Win is an indicator variable for winning a bowl game in year t-1.

27

Table 3

Determinants of Explicit Incentives as Measured by Bonus

Bonus% Bonus% Bonus%

VARIABLES (1) (2) (3)

Bowl Wint-1 0.005 0.005 0.007

(0.125) (0.110) (0.159)

Win%t-1 -0.261*** -0.136 -0.138

(-2.637) (-1.371) (-1.396)

Championshipt-1 -0.113 -0.068 -0.095

(-0.753) (-0.464) (-0.653)

BCS Bowlt-1 -0.040 -0.014 -0.015

(-0.494) (-0.182) (-0.186)

Ln(Stadium Capacity)t -0.020 0.250*** 0.242***

(-0.328) (3.757) (3.710)

BCSt-1 0.022

(0.428)

Ln(Total Comp)t -0.187***

(-4.916)

Salary Rankt -0.005***

(-4.916)

Constant 0.615 0.168 -2.002***

(0.989) (0.372) (-2.996)

Observations 384 384 384

R-squared 0.057 0.081 0.082

This table reports OLS estimations of Bonus% as a function of institution membership in a BCS

conference, performance, and annual compensation. */**/*** indicates significant coefficients at the 10%,

5%, and 1% levels, respectively. The model includes indicator variables for year and standard errors are

Huber-white robust. The dependent variable is the maximum potential bonus scaled by the total annual pay

excluding bonus in year t. Ln(Stadium Capacity) is the number of spectators the institution’s home football

stadium can hold. BCS is an indicator variable equal to 1 for institutions in conferences from the BCS.

Bowl Win is an indicator variable for winning a bowl game in year t-1. Win% is the number of wins/total

games in t-1. Championship is an indicator for appearing in the Championship game in t-1. BCS Bowl is an

indicator for appearing in a BCS Bowl in year t-1. Ln(Total Comp) is the natural log of total salary in year

t. Salary Rank is the annual rank of the contracted salary across all firms in our sample.

28

Table 4

Change in Annual Compensation, Renegotiation, and Institution Change

Panel A: Change in Compensation and Turnover

Total Sample Institution Change Non-Institution Change

Mean Median Mean Median Mean Median

Renegotiation 0.33 0.00 0 0 0.33 0.00

Turnover 0.26 0.00 1.00 1.00 0 0

ΔTotal_Comp 191,648 33,909 915,531*** 793,050*** 154,205 29,211

ΔTotal_Comp% 35.73% 3.72% 264.35%*** 257.11%*** 23.91% 3.39%

ΔCompensation Rank 3.00 -1.00 41.33 42.00 1.02 -1.50

Panel B: Change in Compensation and Renegotiation No Turnover

No Renegotiation Renegotiation

Mean Median Mean Median

Renegotiation 0 0 1 1

Turnover 0 0 0 0

ΔTotal_Comp -7648 4800 486430 300500

ΔTotal_Comp% -1.04% 0.88% 75.11% 33.33%

ΔCompensation Rank -4.14 -3.00 11.61 6.50

The sample of change analysis is limited to observations in academic years 2007, 2009, and 2010. */**/***

indicate significant t-statistics (Wilcoxon rank-sum statistics) of differences in means (medians) at the 10%,

5%, and 1% levels respectively across Turnover and non-Turnover Coaches in Panel A; Renegotiation and

No Renegotiation in Panel B. Renegotiation is an indicator variable for contracts that increase in annual pay

by more than 10%, which is the largest increase in ex-ante contracted increases in salary for any coach in

our sample, which occurs 54 times. For 2007 to 2009, we adjust the renegotiation determinant to be 15%.

Turnover is an indicator variable equal to 1 when the coach leaves one institution in our sample to take

another position at an institution in our sample within two years. This occurs in 18 instances. ΔTotal_Comp

is the change in Total Compensation between the two academic years t and t-1. ΔTotal_Comp% is the

ΔTotal_Comp scaled by Total Compensation in the previous year. ΔCompensation Rank is the change in

the rank of Total pay between t-1 and t, where rank is the ordered rank of Total Comp for the sample

evaluated annually.

1

Table 5

Determinants of Renegotiation and Coach Job Changes

Renegotiation Renegotiation New Job New Job

VARIABLES (1) (2) (3) (4)

Win%t-1 0.857*** 0.884*** 0.185** 0.181**

(4.876) (4.829) (2.138) (1.979)

Salary Rankt-1 -0.008*** -0.011** 0.000 0.001

(-4.777) (-2.203) (0.094) (0.369)

BCS Bowlt-1 0.010 0.012 -0.003 -0.004

(0.074) (0.090) (-0.041) (-0.065)

Championshipt-1 0.582*** 0.603*** -0.068 -0.077

(2.645) (2.693) (-0.619) (-0.679)

BCSt-1 0.264*** 0.323** -0.019 -0.038

(2.680) (2.195) (-0.381) (-0.513)

Ln(Stadium Capacity)t-1 0.016 0.098 -0.102* -0.133

(0.128) (0.498) (-1.653) (-1.395)

Pay Deviationt-1

0.104

-0.036

(0.538) (-0.376)

Constant -0.068 -0.862 1.063* 1.369

(-0.054) (-0.443) (1.698) (1.451)

165 165 246 246

Observations 0.286 0.288 0.063 0.066

This table reports OLS estimations of renegotiation and turnover as a function of institution membership in a BCS

conference, performance, and annual compensation. */**/*** indicates significant coefficients at the 10%, 5%, and

1% levels, respectively. The model includes indicator variables for year and standard errors are Huber-white robust.

The dependent variable is the an indicator variable for change in pay greater than 10% in Columns (1) and (2) and

an indicator for a coach changing institutions in Columns (3) and (4). BCS is an indicator variable equal to 1 for

institutions in conferences from the BCS. Win% is the number of wins/total games in t-1. ΔWin% is the difference

between Win% in the prior year and the average Win% from over the past 15 years. Salary Rank is the annual rank

of the contracted salary across all firms in our sample. BCS Bowl is an indicator for appearing in a BCS Bowl in

year t-1. Championship is an indicator for appearing in the Championship game in t-1. Ln(Stadium Capacity) is the

number of spectators the institution’s home football stadium can hold. Pay Deviation is the residual from estimating

total annual pay as in Column (1) of Table 6.

2

Table 6

Determinants of Total Compensation and the Effect of Changing Institutions

Total_Compt Total_Compt ΔLn(Total_Comp)t

VARIABLES (1) (2) (3)

Bowl Wint-1 0.028 -0.028 -0.131**

(0.540) (-0.487) (-2.296)

Win%t-1 0.627*** 0.606*** 0.382***

(5.348) (4.466) (2.654)

Championshipt-1 0.098 0.062 0.236

(0.602) (0.333) (1.326)

BCS Bowlt-1 0.115 0.190* 0.071

(1.239) (1.872) (0.699)

BCSt 0.629*** 0.657*** 0.040

(10.518) (9.740) (0.545)

Ln(Stadium Capacity)t 0.790*** 0.765*** -0.029

(11.131) (9.627) (-0.342)

Turnovert -0.045 1.011***

(-0.771) (8.761)

Constant 4.234*** 4.923*** 0.221

(5.762) (5.991) (0.250)

Observations 412 310 174

R-squared 0.728 0.733 0.394

This table reports OLS estimations of annual compensation as a function of institution membership in a BCS

conference, performance, and whether the coach recently moved to the institution. */**/*** indicates significant

coefficients at the 10%, 5%, and 1% levels, respectively. The model includes indicator variables for year and

standard errors are Huber-white robust. The dependent variable in Columns (1) and (2) is the Ln(Total Annual pay

(excluding bonus)) in year t. The dependent variable in Column (3) is the difference in the natural log of annual pay

for the coach in year t-1 and year t. If the coach changes institutions, the pay at the prior firm is included as Total

Compensation in t-1. Column (1) includes all observations in our sample, Column (2) is restricted to observations

after the first year of our sample, 2006 so that we can observe turnovers. Column (3) is limited to coaches that

remain in our sample for at least two years (regardless of the institution) so that the change in pay can be measured.

BCS is an indicator variable equal to 1 for institutions in conferences from the BCS. Bowl Win is an indicator

variable for winning a bowl game in year t-1. Win% is the number of wins/total games in t-1. Championship is an

indicator for appearing in the Championship game in t-1. BCS Bowl is an indicator for appearing in a BCS Bowl in

year t-1. Ln(Stadium Capacity) is the number of spectators the institution’s home football stadium can hold.

Turnover is an indicator for coaches that moved from one institution in our sample to another over the past year.