Explain Changes in Net Position © Dale R. Geiger 20111.

51

Explain Changes in Net Explain Changes in Net Position Position © Dale R. Geiger 2011 1

-

Upload

avice-hunt -

Category

Documents

-

view

219 -

download

1

Transcript of Explain Changes in Net Position © Dale R. Geiger 20111.

Explain Changes in Net PositionExplain Changes in Net Position

© Dale R. Geiger 2011 1

Terminal Learning ObjectiveTerminal Learning Objective• Task: Explain Changes in Net Position Over a

Period of Time • Condition: You are a cost advisor technician with

access to all regulations/course handouts, and awareness of Operational Environment (OE)/Contemporary Operational Environment (COE) variables and actors

• Standard: With at least 80% accuracy:• Prepare Statement of Budgetary Resources• Demonstrate proprietary reporting• Prepare basic proprietary financial statements

© Dale R. Geiger 2011 2

Do federal agencies keep two sets of Do federal agencies keep two sets of books?books?

© Dale R. Geiger 2011 3

Two Types of AccountsTwo Types of Accounts

• Budgetary Accounts track budgetary activities and resources• Appropriations, Obligations, Expenditures

• Proprietary Accounts track financial activities and resources• Liabilities and payment of liabilities• Assets and payments received• Expenses and revenues

© Dale R. Geiger 2011 4

Budgetary ReportingBudgetary Reporting

• Statement of Budgetary Resources

• Budgetary Resources consist of:• Prior Year Unobligated Balance• Current Year Appropriations• Collections

Expenditures + OpenObligations

+ UnobligatedBalance

Appropriations& Other

=

Budgetary Resources = Status of Budgetary Resources

© Dale R. Geiger 2011 5

Budgetary ReportingBudgetary Reporting

• Statement of Budgetary Resources

• Budgetary Resources consist of:• Prior Year Unobligated Balance• Current Year Appropriations• Collections

Expenditures + OpenObligations

+ UnobligatedBalance

Appropriations& Other

=

Budgetary Resources = Status of Budgetary Resources

© Dale R. Geiger 2011 6

Statement of Budgetary ResourcesStatement of Budgetary Resources

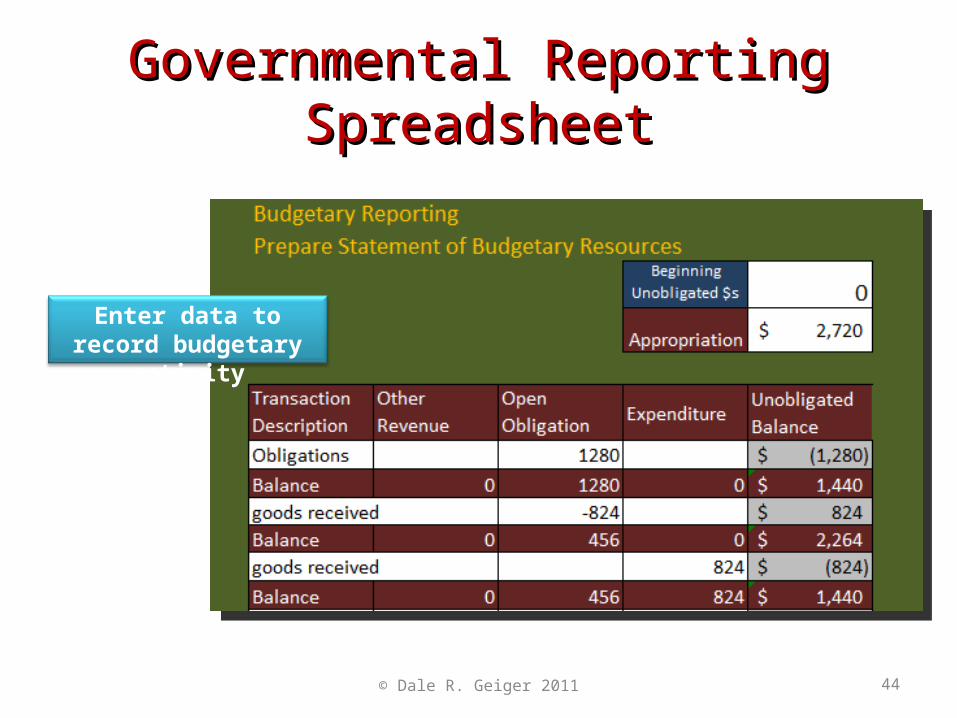

• The fictional Training Appropriation Fund received appropriations of $2720

• Purchase orders in the amount of $1280 were issued

• Goods received were $824 (estimated and actual)

• Task: Prepare the Statement of Budgetary Resources

© Dale R. Geiger 2011 7

Statement of Budgetary ResourcesStatement of Budgetary Resources

• What items represent the Budgetary Resources?

• What items represent the Status of Budgetary Resources?

• How much are the expenditures? • How much of the obligations was left

outstanding?• What is the unobligated balance?

© Dale R. Geiger 2011 8

Statement of Budgetary ResourcesStatement of Budgetary Resources

Budgetary Resources:Appropriations $2720

Status of budgetary resources:Obligations (unfilled orders) $456Expended appropriations 824Unobligated Balance 1440

Total $2720

© Dale R. Geiger 2011 9

Statement of Budgetary ResourcesStatement of Budgetary Resources

Budgetary Resources:Appropriations $2720

Status of budgetary resources:Obligations (unfilled orders) $456Expended appropriations 824Unobligated Balance 1440

Total $2720The purpose of this report is to show that

all budgetary resources are accounted for

© Dale R. Geiger 201110

Check on LearningCheck on Learning

• What is the basic equation for the Statement of Budgetary Resources?

• What items represent the Status of Budgetary Resources?

© Dale R. Geiger 2011 11

Proprietary ReportingProprietary Reporting

• Statement of Net CostCosts – Earned Revenues = Net Cost

• Statement of Changes in Net PositionFinancing Sources – Net Cost = Change in Net Position

• Balance SheetAssets = Liabilities + Net Position

• Uses the Accrual Basis of Accounting

© Dale R. Geiger 2011 12

Proprietary ReportingProprietary Reporting

• Statement of Net CostCosts – Earned Revenues = Net Cost

• Statement of Changes in Net PositionFinancing Sources – Net Cost = Change in Net Position

• Balance SheetAssets = Liabilities + Net Position

• Uses the Accrual Basis of Accounting

© Dale R. Geiger 2011 13

Proprietary ReportingProprietary Reporting

• Statement of Net CostCosts – Earned Revenues = Net Cost

• Statement of Changes in Net PositionFinancing Sources – Net Cost = Change in Net Position

• Balance SheetAssets = Liabilities + Net Position

• Uses the Accrual Basis of Accounting

© Dale R. Geiger 2011 14

Proprietary ReportingProprietary Reporting

• Statement of Net CostCosts – Earned Revenues = Net Cost

• Statement of Changes in Net PositionFinancing Sources – Net Cost = Change in Net Position

• Balance SheetAssets = Liabilities + Net Position

• Uses the Accrual Basis of Accounting

© Dale R. Geiger 2011 15

Proprietary ReportingProprietary Reporting

• Statement of Net CostCosts – Earned Revenues = Net Cost

• Statement of Changes in Net PositionFinancing Sources – Net Cost = Change in Net Position

• Balance SheetAssets = Liabilities + Net Position

• Uses the Accrual Basis of Accounting

© Dale R. Geiger 2011 16

Other Financing SourcesOther Financing Sources

• Increase Net Position • Prevent Revenues and Expenditures from

being counted twice in the same entity• Transfers of cash from other funds in the same

government• Unreimbursed services provided by another

governmental segment or entity

• Cash inflows from long term borrowing

© Dale R. Geiger 2011 17

Proprietary vs. BudgetaryProprietary vs. Budgetary

• The budgetary accounts use the budgetary basis:

Once the goods are received, the budgetary accounting process is finished and the proprietary accounts take over

Plan Order ConsumeReceive Pay

Commitment Obligation Expenditure

© Dale R. Geiger 2011 18

Proprietary vs. BudgetaryProprietary vs. Budgetary

• The proprietary accounts use the accrual basis:

• When goods are received liability recorded• When payment is made liability satisfied• When goods are consumed expense

Plan Order ConsumeReceive Pay

Asset & Liability Remove Liability Expense

© Dale R. Geiger 2011 19

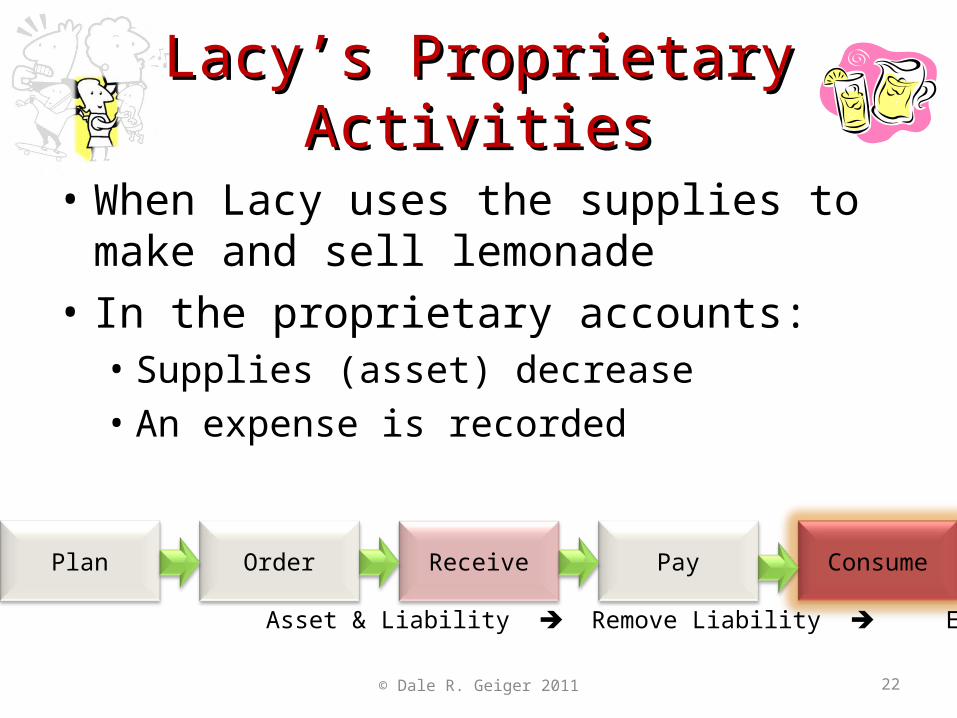

Lacy’s Proprietary ActivitiesLacy’s Proprietary Activities

• Lacy purchases supplies on account at the grocery store (she RECEIVES GOODS)

• The EXPENDITURE is the final activity in the budgetary accounts

• In the proprietary accounts:• An asset is recorded: Supplies represent future

benefit – they can be used to make and sell lemonade• A liability is recorded: Lacy has an obligation to pay

the bill in the future

© Dale R. Geiger 2011 20

Lacy’s Proprietary ActivitiesLacy’s Proprietary Activities

• When Lacy pays the grocery bill:• In the proprietary accounts:• Cash (an asset) decreases• The liability is removed because Lacy has satisfied

her obligation

© Dale R. Geiger 2011 21

Lacy’s Proprietary ActivitiesLacy’s Proprietary Activities

• When Lacy uses the supplies to make and sell lemonade

• In the proprietary accounts:• Supplies (asset) decrease• An expense is recorded

Plan Order ConsumeReceive Pay

Asset & Liability Remove Liability Expense

© Dale R. Geiger 2011 22

Check on LearningCheck on Learning

• What activity ends the involvement of the budgetary accounts in the purchasing process?

• What activity constitutes an expense in the proprietary accounts?

© Dale R. Geiger 2011 23

Statement of Net CostStatement of Net Cost

• Most federal agencies generate revenues that are insignificant in comparison to expenses

• Revenues are generally reimbursements for costs incurred on behalf of other federal agencies

• Expenses – Revenues = Net Cost

© Dale R. Geiger 2011 24

Statement of Net CostStatement of Net Cost

• Salaries and personnel costs for the fictional Training Appropriation Fund for the year were $398

• Other expenses amounted to $40• Miscellaneous revenues of $186 were

collected • Task: Prepare the Statement of Net Cost

© Dale R. Geiger 2011 25

Statement of Net CostStatement of Net Cost

Salaries and personnel costs $398Other expenses 40Total Costs $438Less: Miscellaneous revenues 186Net Cost $252

© Dale R. Geiger 2011 26

Statement of Net CostStatement of Net Cost

Salaries and personnel costs $398Other expenses 40Total Costs $438Less: Miscellaneous revenues 186Net Cost $252

The purpose of this statement is to show the cost to the government of providing this program or service.

© Dale R. Geiger 2011 27

Statement of Change in Net PositionStatement of Change in Net Position

• Shows how the activities of the period affect the Net Position of the entity

• Net Position consists of:Cumulative Results of Operations

+Unexpended Appropriations

• The changes in the two categories are calculated separately

© Dale R. Geiger 2011 28

Statement of Change in Net PositionStatement of Change in Net Position

Cumulative Results of Operations:

Appropriations used+ Other financing sources- Net Cost= Net Change+ Beginning= Ending

Unexpended Appropriations:

Appropriations received - Appropriations used= Net Change+ Beginning= Ending

© Dale R. Geiger 2011 29

Statement of Change in Net PositionStatement of Change in Net Position

Cumulative Results of Operations:

Appropriations used+ Other financing sources- Net Cost= Net Change+ Beginning= Ending

Unexpended Appropriations:

Appropriations received - Appropriations used= Net Change+ Beginning= Ending

Proprietary activity© Dale R. Geiger 2011 30

Statement of Change in Net PositionStatement of Change in Net Position

Cumulative Results of Operations:

Appropriations used+ Other financing sources- Net Cost= Net Change+ Beginning= Ending

Unexpended Appropriations:

Appropriations received - Appropriations used= Net Change+ Beginning= Ending

Budgetary activity© Dale R. Geiger 2011 31

Statement of Change in Net PositionStatement of Change in Net Position

• The fictional Training Appropriation Fund is a new entity, so beginning net position is zero

• Appropriations were $2720, and Expenditures were $824 (from Statement of Budgetary Resources)

• Net cost of operations is $252 (from Statement of Net Cost)

© Dale R. Geiger 2011 32

Statement of Change in Net PositionStatement of Change in Net Position

© Dale R. Geiger 2011 33

Statement of Change in Net PositionStatement of Change in Net Position

© Dale R. Geiger 2011 34

Statement of Change in Net PositionStatement of Change in Net Position

Cumulative Results of Operations

Unexpended Appropriations

Appropriations -- $2720Appropriations Used $824 (824)Less: Net Cost (252) --Net change 572 1896Add Beginning: -0- -0-Ending: $572 $1896

© Dale R. Geiger 2011 35

Statement of Change in Net PositionStatement of Change in Net Position

Cumulative Results of Operations

Unexpended Appropriations

Appropriations -- $2720Appropriations Used $824 (824)Less: Net Cost (252) --Net change 572 1896Add Beginning: -0- -0-Ending: $572 $1896

© Dale R. Geiger 2011 36

Balance SheetBalance Sheet

• Similar to the Statement of Financial Position• Assets = Liabilities + Net Position• If Assets < Liabilities, Net position will be

negative• Net position = Unexpended appropriations +

cumulative results of operations

© Dale R. Geiger 2011 37

Balance SheetBalance Sheet

• The fictional Training Appropriation Fund has $2600 in its balance with the Treasury

• Equipment (net of depreciation): $380• Liabilities: $512• From Statement of Change in Net Position:• Cumulative results of operations: $572• Unexpended Appropriations: $1896

• Task: Prepare the Balance Sheet

© Dale R. Geiger 2011 38

Balance SheetBalance SheetAssets:Balance with the Treasury $2600 Equipment (net of depreciation) 380Total Assets $2980

Liabilities and Net Position:Liabilities $512Unexpended Appropriations 1896 Cumulative results of Operations 572Total Liabilities and Net Position $2980

© Dale R. Geiger 2011 39

Balance SheetBalance SheetAssets:Balance with the Treasury $2600 Equipment (net of depreciation) 380Total Assets $2980

Liabilities and Net Position:Liabilities $512Unexpended Appropriations 1896 Cumulative results of Operations 572Total Liabilities and Net Position $2980

This statement lists the assets of the entity and shows how they were financed:

(borrowing)

(appropriations)

(operations)

© Dale R. Geiger 2011 40

Check on LearningCheck on Learning

• Which statement shows the cost to the government of providing a particular program or service?

• Which statement explains the changes in the Net Position of the entity?

© Dale R. Geiger 2011 41

Why is it important to be familiar with Why is it important to be familiar with External Reports?External Reports?

• External Reporting is the primary objective of most accounting systems

• Cost accounting information is drawn from the same accounting system

• Understanding the basis of the accounting data permits a meaningful translation to useful cost information

© Dale R. Geiger 2011 42

Issues with Budgetary AccountingIssues with Budgetary Accounting

• Focus is on obligations and expenditures• Ordering and receiving goods do not reflect actual

use of resources

• 99.9% philosophy of financial management• All of the money will be spent, yet does not

necessarily reflect the true cost of operations

© Dale R. Geiger 2011 43

Governmental Reporting SpreadsheetGovernmental Reporting Spreadsheet

Enter data to record budgetary activity

© Dale R. Geiger 2011 44

Governmental Reporting SpreadsheetGovernmental Reporting Spreadsheet

Prepare the Statement of Budgetary Resources

© Dale R. Geiger 2011 45

Governmental Reporting SpreadsheetGovernmental Reporting Spreadsheet

Budgetary Resources equal

Status of Budgetary Resources

© Dale R. Geiger 2011 46

Governmental Reporting SpreadsheetGovernmental Reporting Spreadsheet

Prepare Statement of Net Cost

© Dale R. Geiger 2011 47

Governmental Reporting SpreadsheetGovernmental Reporting Spreadsheet

Net cost flows into the Statement of Change in Net Position, Cumulative Results of Operations

© Dale R. Geiger 2011 48

Governmental Reporting SpreadsheetGovernmental Reporting Spreadsheet

The Statement of Change in Net Position shows changes in both Cumulative Results of Operations

and Unexpended Appropriations

© Dale R. Geiger 2011 49

Governmental Reporting SpreadsheetGovernmental Reporting Spreadsheet

The Balance Sheet shows Assets and Liabilities as well

as the new balances in Unexpended Appropriations

and Cumulative Results of Operations

© Dale R. Geiger 2011 50

Practical ExercisePractical Exercise

© Dale R. Geiger 2011 51