Experiences in the administration of co-operative credit and marketing societies in northern Nigeria

13

EXPERIENCES IN THE ADMINISTRATION OF CO-OPERATIVE CREDIT AND MARKETING SOCIETIES IN NORTHERN NIGERIA* ROGER KING Department of Agricultural Economics, University of Reading, Earley Gate, Reading, RG6 2AT, Great Britain (Received:21 April, 1975) INTRODUCTION The principles behind co-operatives were first, developed by nineteenth century industrial workers in England as an alternative to the existing capitalism. Their vision was to replace ownership by the few with group ownership and authoritarian decisions with democracy, and to make the participation of members the basis for distribution of profits-that is, to supply the services of the co-operative to members at cost. This paper is concerned with the experience of introducing this type of institution into the very different social conditions of the peasant farming communities of northern Nigeria. The first part of the paper looks at co-operatives in the general terms of a government policy to promote institutional change. Next the blueprint on which northern Nigerian farmers’ co-operatives are based is described, followed by a description of how co-operatives have evolved in practice. Comparison of the blueprint on which co-operative development has been based and the very different existing reality holds some lessons on the administration of change in village society and is the subject of the final section. (In this paper there is no attempt to quantify the benefits accruing from the government’s co-operative policy, only to describe the experience of its administration.) CO-OPERATIVES AND INSTITUTIONAL CHANGE Institutions are simply the way things are done in society. By making promotion of co-operatives part of its policies, a government is indicating that it is not satisfied * The information in this paper was collectedby the author while he was Research Fellow at the Institute for Agricultural Research, Ahmadu Be110 University, 1972-74. The opinions expressed do not necessarily reflect those of the Institute. 195 Agricultural Administration (2) (1975)--O Applied Science Publishers Ltd, England, 1975 Prmted in Great Britain

-

Upload

roger-king -

Category

Documents

-

view

214 -

download

0

Transcript of Experiences in the administration of co-operative credit and marketing societies in northern Nigeria

EXPERIENCES IN THE ADMINISTRATION OF CO-OPERATIVE CREDIT AND MARKETING

SOCIETIES IN NORTHERN NIGERIA*

ROGER KING

Department of Agricultural Economics, University of Reading, Earley Gate, Reading, RG6 2AT, Great Britain

(Received: 21 April, 1975)

INTRODUCTION

The principles behind co-operatives were first, developed by nineteenth century industrial workers in England as an alternative to the existing capitalism. Their vision was to replace ownership by the few with group ownership and authoritarian decisions with democracy, and to make the participation of members the basis for distribution of profits-that is, to supply the services of the co-operative to members at cost. This paper is concerned with the experience of introducing this type of institution into the very different social conditions of the peasant farming communities of northern Nigeria.

The first part of the paper looks at co-operatives in the general terms of a government policy to promote institutional change. Next the blueprint on which northern Nigerian farmers’ co-operatives are based is described, followed by a description of how co-operatives have evolved in practice. Comparison of the blueprint on which co-operative development has been based and the very different existing reality holds some lessons on the administration of change in village society and is the subject of the final section. (In this paper there is no attempt to quantify the benefits accruing from the government’s co-operative policy, only to describe the experience of its administration.)

CO-OPERATIVES AND INSTITUTIONAL CHANGE

Institutions are simply the way things are done in society. By making promotion of co-operatives part of its policies, a government is indicating that it is not satisfied

* The information in this paper was collected by the author while he was Research Fellow at the Institute for Agricultural Research, Ahmadu Be110 University, 1972-74. The opinions expressed do not necessarily reflect those of the Institute.

195 Agricultural Administration (2) (1975)--O Applied Science Publishers Ltd, England, 1975 Prmted in Great Britain

196 ROGER KING

with the way certain things are being done and thinks they could be done better by utilising co-operatives. For example, promotion of co-operatives which made loans to farmers and sold their produce would indicate that the government considered the traditional credit and marketing arrangements to be unsatisfactory. It might also indicate that the traditional methods of decision-making and the distribution of economic power in rural communities were unacceptable to the government who wished to replace them with the principles of democracy and shared owner- ship inherent in co-operatives.

The quantity of resources a government would want to devote to changing existing institutions by introducing co-operatives depends on the cost of administer- ing the change and the benefits that are expected from the reforms. The controversy surrounding co-operative policy usually originates at this point because benefits can be assessed differently from different viewpoints. Co-,operatives can be judged strictly in terms of commercial,efficiency but, to many people, they also contain the virtues of community involvement and a more socially just form of economic organisation. In addition they may be seen as -an institution which facilitates administration of government policy in rural communities.

It is the last consideration which probably gives most impetus to co-operative policy. Faced with a very large number of small farmers spread over a wide area and a critical limitation of skilled administrators, governments usually try self-help among farmers as an aid to agricultural development. Essentially this means that farmers themselves undertake some of the management required in providing the necessities for a modernising agriculture-for example, supply of improved inputs, better marketing channels, agricultural extension and credit. Frequently co- operatives are the institution chosen as the vehicle for mobilising the managerial abilities of farmers in order to promote agricultural development policies.

The next section of this paper describes how co-operative policy objectives have aimed at incorporating farmers’ managerial ability into independently viable businesses which also promote agricultural development and community ideals.

THE BLUEPRINT FOR CO-OPERATIVES IN NORTHERN NIGERIA

The basis for the co-operative movement in northern Nigeria is similar to that introduced by the British in other parts of the world. The description given below is specific to Co-operative Credit and Marketing Societies (CCMS’s) which account for the majority of farmers’ co-operatives in northern Nigeria.

The nature of co-operatives is spelled out in the Co-operative Societies Law, and the subsidiary legislation made under the Co-operative Societies Law- Northern Region Co-operative Societies Regulations (Section 58), which came into force in 1956.’ The individual societies are free to make their own bye-laws subject to the approval of the Registrars of Co-operatives, but in fact a high degree

CO-OPERATIVE CREDIT SERVICES IN NORTHERN NIGERIA 197

of uniformity exists and the following description of rules guiding co-operative operations includes those from the standard book of bye-laws provided by the Co-operative Registrar’s office.’

The Co-operative Law establishes a registered co-operative as a ‘body corporate’ with a life of its own and the ability to enter into contracts and be subject to other legal obligations. To be eligible for registration by the Registrar of Co-operatives, who heads each state’s Co-operative Division, a co-operative should have at least ten members over the age of eighteen within its area of operation. The area of operation is usually a village and surrounding hamlets. Membership is voluntary and open to all farmers subject to the approval of existing members. A condition of membership is the purchase of a minimum number of shares in the society. No member can purchase more than 20% of the total shares issued.

Once a member of a Co-operative Credit and Marketing Society, a farmer can take part in its economic activities. He can deposit savings, receive loans (interest limited to 20% pa), and sell his produce to the co-operative which resells it at the best possible price. The member also becomes eligible for a share of the profits arising from the society’s activities. A proportion of the profits must be deposited in the society’s ‘reserve fund’ but the rest is distributed on the basis of business done (bonus) or shares held (dividends).

Bank Government Cooperative Dwision

Secondary Society (Umon)

Unton provides Primary socletles Invest m the union

” representatwes

Pr~mory Society

The elected committee approve Members odd

by regular sowng

I lndwdual Members of the Primary Society

Fig. 1. A blueprint for the organisation of co-operative credit. There are variations on this blueprint which would also be consistent with co-operative laws and regulations. This figure shows

a simple form of co-operative organisation.

198 ROGER KING

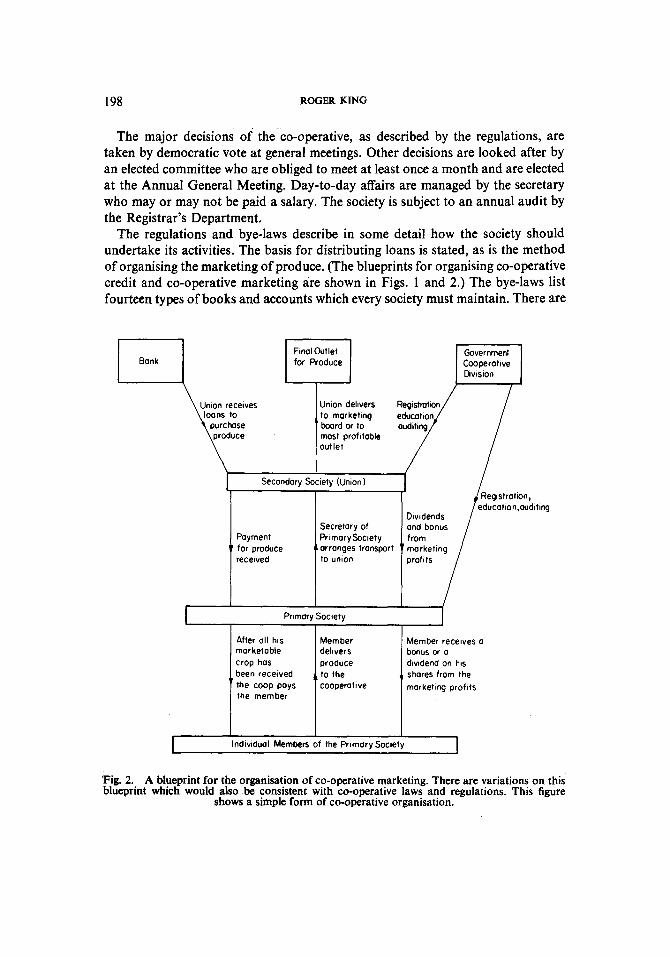

The major decisions of the co-operative, as described by the regulations, are taken by democratic vote at general meetings. Other decisions are looked after by an elected committee who are obliged to meet at least once a month and are elected at the Annual General Meeting. Day-to-day affairs are managed by the secretary who may or may not be paid a salary. The society is subject to an annual audit by the Registrar’s Department.

The regulations and bye-laws describe in some detail how the society should undertake its activities. The basis for distributing loans is stated, as is the method of organising the marketing of produce. (The blueprints for organising co-operative credit and co-operative marketing are shown in Figs. 1 and 2.) The bye-laws list fourteen types of books and accounts which every society must maintain. There are

Umon delwers to marketmg

” board or to most profltoble outlet

Secondary Society (Umon)

Payment 1 for produce

recewed

Secretory of PrlmorySoclety

ri arronges transport ” marketing to union

I Primary Society

After all his marketoble crop has been recewed the coop pays the member

Member dehvers produce to the L cooperotwe I

I lndwidual Members of the Primary Socle ,JY -

Member recewes a bonus or a dwtdend on hc shares from the morketq profats

‘Fig. 2. A blueprint for the organisation of co-operative marketing. There are variations on this blueprint which would also be consistent with co-operative laws and regulations. This figure

shows a simple form of co-operative organisation.

CO-OPERATIVE CREDIT SERVICES IN NORTHERN NIGERIA 199

procedures laid down for resolving most of the disputes which might occur. Frequently, as for example in applying for an extension of the loan repayment period, members are required to follow a written procedure.

In addition to the primary societies described above, there is provision for secondary societies, or co-operative unions, providing services,to member societies.

The objectives stated in the bye-laws also reveal a number of additional under- lying aims to the business operation described above. These include encouragement of improved methods of agriculture by supplying expert advice and improved inputs. Members are, in fact, legally obliged to use loans received only for agri- cultural purposes. In addition to the emphasis on agricultural development, the societies are supposed to encourage ‘the spirit and practice of thrift, mutual help and self-help’ (Bye-laws, page 1, paragraph 4 (viii)) and ‘to promote co-operative spirit among the members, to work for the improvement of local educational and living standards, and to encourage the development of the Co-operative Movement in the Northern Region of Nigeria’ (Bye-laws, page 2, paragraph 4 (ix).)

The blueprint is therefore of a well-defined organisation which can operate with near independence. Ideally, the economies of scale arising from the group effort should result in loans to farmers at interest rates below those of alternative sources and in increased incomes from lowering the cost of produce marketing.

The fulfilment of such a blueprint requires qualities among the members which may initially be in short supply in rural areas. These include an understanding and appreciation of democratic decision-making, the managerial ability to run a credit programme on a bureaucratic basis, the sophistication to deal with urban institu- tions such as banks, and the ability to build up the trading links essential to efficient marketing. A minimum of literacy among members and the availability of a skilled secretary are essential. Elected officials must embrace an ethic of selfless business honesty which village society has previously given them little opportunity to develop.

The government co-operative officials receive a training which emphasises the rules and principles of the blueprint. They then have the unenviable task of approximating the blueprint in societies where few of the qualities essential for its achievement are immediately available. The following section looks at the result of the interaction between co-operative policy and the village community.

THE ADMINISTRATION OF CO-OPERATIVE CREDIT AND MARKETING SOCIETIES IN PRACTICE

The co-operative movement in northern Nigeria has had problems in the past which were not directly attributable to the aims or the administration of co- operative policy. In terms of increase in numbers the greatest period of growth for the co-operative movement was during the 1960s. In 1972 there were 250,000 members in 2700 registered societies. (Data collected by the author from the

200 ROGER KING

Registrar’s office of the six northern states between January and March, 1973.) Some societies were not formed on a genuine basis, but were inspired by political groups who used them for collecting and distributing patronage. There are many stories of money loans being distributed to hastily-formed societies who felt no obligation to repay, or of members repaying in good faith only to find later that there was no record of their repayment. In addition to undermining the concept of a co-operative among farmers, the interference was partly responsible for the accumulation of a N2,776,870 (f I ,388,435) (reference 10, p. 2) debt by 1970. At this point most of the loans to farmers were halted by the newly-formed state governments pending a review of co-operative activities. The withdrawal of government guaranteed production credit effectively halted co-operative activity in the primary societies. In recent years a number of states have cautiously resumed distributing production credit to those co-operative societies which have achieved the best repayment records in the past. It is revitalised societies in Kano and North Eastern State that form the .basis of this section of the present paper. (Three primary co-operative societies and one union in each of the states were studied in detail. All the societies had been registered more-than eight years and had received production credit for the last two years at the time of the study (1973-74))

The farmers involved in the six primary Co-operative Credit and Marketing Societies which form the basis of the study were engaged in a hoe agriculture and farmed. an average of 3 ha. per family in the Kano state villages’and 4 ha. per family in the North Eastern state villages. The main food staples were millet and sorghum, the main cash crop, groundnuts. The average size of the societies was about 100 members, varying from 40 in the smallest to 200 in the largest.

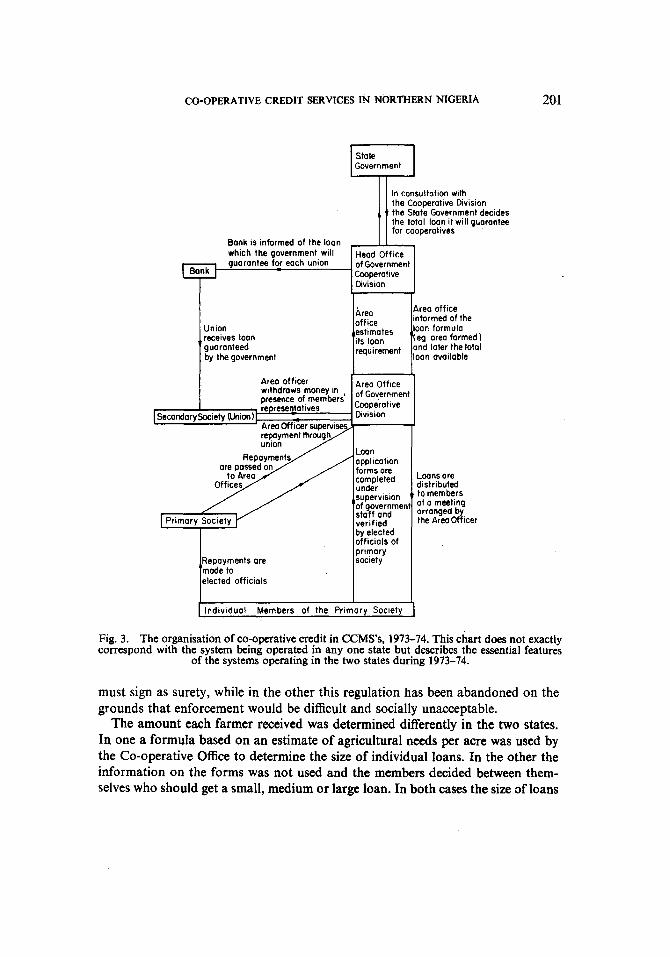

Co-operative credit The co-operative credit operation (Fig. 3) consists of the annual distribution of

pre-season loans and collection of repayments at harvest time. In one of the two states studied, part of the loan was given halfway through the growing season. Towards the end of the dry season, after satisfactory repayment of the previous year’s loan, a meeting is called by the government Co-operative Officer to complete the loan application forms for the next farming year. Usually every member applies for, and receives, a loan. The information included on the forms varies from state to state but includes area farmed, crops grown and the previous year’s harvest. Government Co-operative Inspectors necessarily assist in this process as very few of the farmers can read or write and sometimes the forms are in unfamiliar English rather than the local Hausa. In the past the estimates of farmed area, expressed in acres, have often been wildly inaccurate as most farmers have no concept of an acre nor any alternative area measure.

The application form is signed with the member’s thumb print and verified as accurate by the society’s president and treasurer. In one state an additional person

CO-OPERATIVE CREDIT SERVICES IN NORTHERN NIGERIA 201

State L-J Government

In consultation with the Cooperative Division the State Government decides the totol loan it will guarantee

Bank is informed of the loan

I Union receives loan guaranteed by the governmenl

Aren officer

/l appllcotion I

I,,.,“,,

Rep0 lymeny

primaryy?p ,

Repoyments are

I made to elected officials

individual Members of the Primary Society

Fig. 3. The organisation of co-operative credit in CCMS’s, 1973-74. This chart does not exactly correspond with the system being operated in any one state but describes the essential features

of the systems operating in the two states during 1973-74.

must sign as surety, while in the other this regulation has been abandoned on the grounds that enforcement would be difficult and socially unacceptable.

The amount each farmer received was determined differently in the two states. In one a formula based on an estimate of agricultural needs per acre was used by the Co-operative Office to determine the size of individual loans. In the other the information on the forms was not used and the members decided between them- selves who should get a small, medium or large loan. In both cases the size of loans

202 ROGER KING

was limited by the total amount allocated to that society by the local Co-operative Office which, in turn, was limited by the total amount allocated to the local co-operative union by the Headquarters of the Co-operative Division. Similarly, the total credit programme of the Co-operative Division itself is limited by the decision of the state government.

This control over co-operative credit by the government is possible because the co-operatives are dependent on government financing. Contrary to the blueprint (Fig. 1) the societies have been unable to collect savings, accumulate profits or become creditworthy in their own right. The finance for the loans is from govern- ment guaranteed bank overdrafts and the state governments bear the cost if co- operative members do not repay their loans.

The continuing existence of a co-operative credit society is most directly dependent on its ability to collect repayments from its members. It is here that the institution makes its greatest contribution. The six societies studied in detail were among those which historically had good repayment records. The repayment system is for the elected officials of the primary societies to collect money from members whenever they can. The secretary of the society issues receipts, but, as nearly all members are illiterate, the essential basis for the system is one of memory, and trust in the leaders.

The ability of a society to enforce repayment and receive the trust of the members seemed to be dependent on the authority of one or two leaders. This was certainly true for the four most rural societies where in three cases the authority could be traced to the village head. In the fourth village, the head was young and distrusted (and excluded from the co-operative), and the co-operative president, a respected village elder, was regarded as an alternative leader in the village. The basis for success in the two societies located in small towns was not so clear. Probably these societies, whose members are relatively cosmopolitan, are less dependent on tradi- tional authority. Traders who stood to personally gain by becoming co-operative produce buyers (see later) were prominent among the leaders of these societies.

Comparison of Figs. 1 and 3 shows clearly the way the government Co-operative Office has come to play a much more central role than is suggested by the blueprint. Rather than supervising co-operative activities through society organisation it has come to control many decisions because of the societies’ dependence on govern- ment financing. In extending its control the Co-operative Division has built direct links between itself and members, and has undertaken much of the administration which the blueprint makes the responsibility of the society. The co-operative union has no life of its own, all its decisions being made by the Co-operative Office.

In reality the co-operative pre-season loan operation is not very different from a typical government-sponsored group credit scheme. The system of decision-making outlined in the co-operative blueprint (Fig. 1) is hardly utilised. Success seems to be mostly dependent on respect for traditional authority, or the forcefulness of a few modern thinking personalities who may be partly motivated by the opportunity the co-operative offers for personal gain.

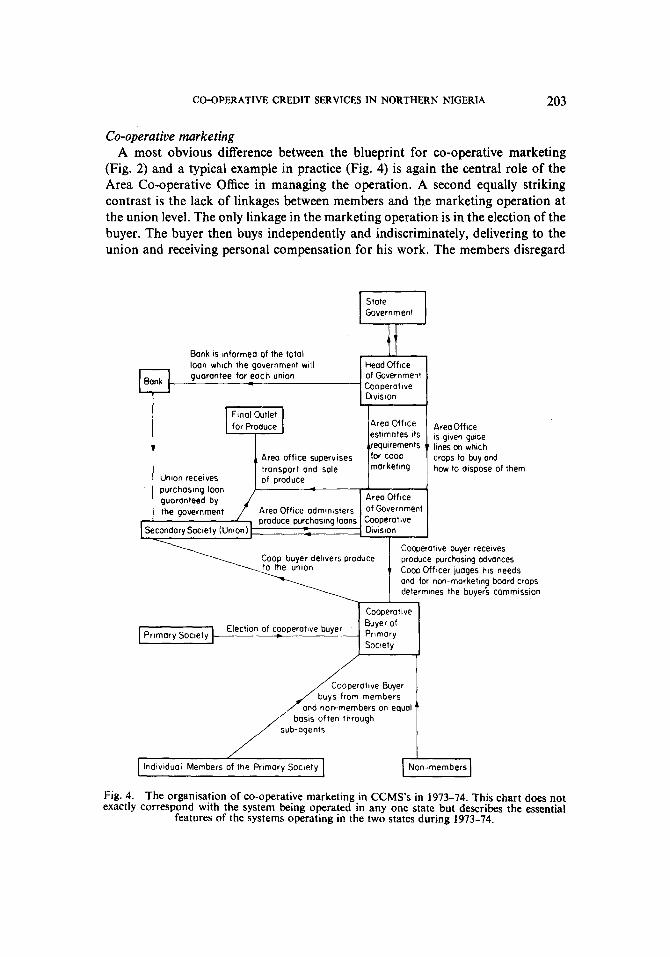

CO-OPERATIVE CREDIT SERVICES IN NORTHERN NIGERIA 203

Co-operative marketing A most obvious difference between the blueprint for co-operative marketing

(Fig. 2) and a typical example in practice (Fig. 4) is again the central role of the Area Co-operative Office in managing the operation. A second equally striking contrast is the lack of linkages between members and the marketing operation at the union level. The only linkage in the marketing operation is in the election of the buyer. The buyer then buys independently and indiscriminately, delivering to the union and receiving personal compensation for his work. The members disregard

State I Government

p Area Offlce I I Area Offxe estimates Its requirements

IS gwen gutde lmes on which

Umon recewes

,/ Area offlce supervIses for coop crops to buy and tronsport and sole marketmg how to dispose of them of produce

SecondarySocIety (Umon)

Cooperatwe buyer recewes produce purchosmg advances

11 Coop Officer judges his needs and for non-marketlng board crops determines the buyer’s commwon

Cooperative

ElectIon of cooperotwe buyer Buyer of

_____ Prlmary Society

/ c

, ~~~~:~~~~“~members, lndwldual Members of the Primary Society

Fig. 4. The organisation of co-operative marketing in CCMS’s in 1973-74. This chart does not exactly correspond with the system being operated in any one state but describes the essential

features of the systems operating in the two states during 1973-74.

204 ROGER KING

their legal obligation to sell through the co-operative and receive no bonus or dividends from the marketing operation. Not surprisingly, the ordinary mem- ber does not see co-operative marketing as one of the benefits of co-operative membership.

The co-operative buyer uses the produce purchasing advances to buy from individuals or traders at the best price he can. He is usually indistinguishable from non-co-operative buyers. Sometimes the co-operative buyer can obtain a better price for the produce he buys by selling it somewhere other than the union. This is illegal, but is difficult to control in practice. Repayment records for purchasing loans are far better than for production credit, because of the smaller number of people involved.

In reality the effect of the co-operative marketing policy is to increase the money available in the existing marketing system. The average member sells to the sub- agents to whom he habitually sells and does not know whether his produce is eventually resold to the co-operative buyer or not. The elected co-operative buyer is almost certain to already be a buyer, because members recognise that only established buyers have the skills to fill the post effectively. Thus the financing is a way for some existing traders to increase their scale of operation. There may be Some indirect advantage for the co-operative in that the co-operative buyer is frequently highly motivated to support other co-operative activities and to ensure the co-operative’s continued existence.

Co-operative policy has therefore not replaced the existing marketing practices but has utilised them. As the members themselves do not receive any direct benefit the government’s justification for the policy is found in the general benefit to all farmers. If more money is made available to buy farmers’ produce, it is argued, farmers will be more willing to increase their production. Further, the co-operative buyers are elected by farmers which should mean that the more trustworthy buyers are those which receive government support.

Co-operative marketing has therefore been financed by government and used to promote its agricultural development policy. In one state this deviation from the idea of a co-operative as a business was taken further when grain purchased by the co-operatives was sold at below market price in an attempt to control urban food prices.

SUMMARY, CONCLUSIONS AND IMPLICATIONS

At the beginning of this paper co-operative policy was described in terms of an attempt to promote an institutional change which would mobilise farmers’ managerial abilities in the service of agricultural development while developing desirable social attitudes. A blueprint was designed and a Registrar appointed to head the government Co-operative Division which would administer this change.

CO-OPERATIVE CREDIT SERVICES IN NORTHERN NIGERIA 205

In practice, however, farmers have not come to run co-operatives according to the blueprint and an institution different to that envisaged has evolved.

Compared to the blueprint, actual co-operative administration involves a much higher degree of government involvement and control, and makes more use of the traditional way of doing things. There are good reasons for both of these trends.

Much of the record-keeping has been transferred from the co-operatives to the local Co-operative Office of the government. The laws requiring societies to keep fourteen types of books were unsuitable for village societies which may be dependent on a barely literate, unpaid schoolboy to keep their records. Such. records do not in any case improve farmers’ faith in an institution when they themselves cannot read. (It is possible to devise methods whereby illiterate farmers can manage co-operative affairs. Gent& 6 for example, describes a simple system of recording co-operative groundnut marketing which was successfully used by illiterate farmers in Niger.)

The necessity for the government to keep the records has been reinforced by the co-operatives’ dependence on government financial support. When ‘the source of funds essential for any co-operative activity coines from the government it is reasonable to find the government keeping a watchful eye on transactions.

The fact that the marketing societies have been unable to create their own funds probably reflects a wrong premise ois. that it is simple for co-operators to market produce more efficiently than private traders. In fact co-operative marketing policy has shelved the aim of making profit in favour of an agricultural policy affecting all farmers. In operating this policy the co-operative officials have generally made use of the skills and marketing links of private traders. That is, the Co- operative Divisions are using locally available managerial skills in their agricultural development policies, but not solely for the benefit of members, as envisaged in the blueprint.

In the operation of co-operative credit a useful institution has been built up among farmers. Although many important decisions have been removed from it, the primary society still has the important functions of vetting loan recipients and recovering loans. The managerial ability to do this is often dependent on using the existing institutions of village authority. The village unit provides the mutual knowledge and trust necessary for success. The primary society has also sometimes given the opportunity for alternative leaders to emerge when traditional authorities are unacceptable.

Many of the formalities of the blueprint are followed, although they have little substantive function. Thus money is nominally channelled through co-operative unions although its fate is, in fact, controlled by the government Co-operative Officer. Loan recipients sign application forms stating that they will use the loan for agriculture and will sell ‘their produce to the co-operative, while neither of these provisions is enforced. The farmer sensibly uses his loan and sells his produce to his own best advantage. A new member must still buy shares in the society. As

206 ROGER KING

these never yield dividends they are regarded by members not as an investment, but as a registration fee necessary before government money can be received.

The lesson to be gained from these experiences is the mundane one that develop- ment administration must be sensitive to local conditions. An attempt to introduce an institution not fully suited to existing conditions has resulted in something quite different from the original plan. A modus vivendi has evolved to accommodate the strength of established institutions and the lack of suitable skills and attitudes to operate an independent co-operative organisation.

This need not be regarded as failure if the reality is fully acknowledged and seen as the basis for more effective policies. Co-operative officials partially recognise this with their acute awareness of the need for more education among co-operative members. At the same time, perhaps as a result of the training for co-operative officials, deviation from the letter of the co-operative laws is often regarded as a failure. Thus there is a danger that practical policies which make the best use of the existing situation to promote agricultural development and self-help, may be deliberately stifled under a facade of co-operative propriety.

What is probably needed, if farmers’ managerial abilities are to be mobilised in the service of agricultural development, is encouragement to devise simple flexible institutions which farmers can operate themselves. This implies an attitude by government administrators which bears in mind the social aims co-operatives were designed to serve, rather than the myriad restrictions of the co-operative regulations. This does not necessarily mean the blueprint should be abandoned as an eventual objective, only that it is not a practical short term aim. In the short term policies of institutional change will, while trying to reform the existing structure, have to make some use of existing institutions such as the village community and adapt themselves to skills and attitudes which already exist. In the longer term new skills are gained and new leaders emerge as farmers gain experience of the new institution, a slow process which can probably be accelerated by intelligent education and propaganda policies.

1.

2.

3.

4.

5.

6.

REFERENCES

ANON., Northern Region Co-operative Societies Regulations, Co-operative Societies Law, Government Printer, Kaduna, 1956. ANON., Bye-laws of the . . . . . Co-operative Credit and Marketing Society Ltd., Government Printer, Kaduna. APTHORPE, R., Rural Co-operatives and planned change in Africa: An analytical overview, United Nations Research Institute for Sooial Development, 1972. CHARLICK. R. B., Induced participation in Nigerian Modernisation. The case of Matameye County, Rura Africana (18) (1972) pp. 5-29. CoLLIN.3, J. D., Government and groundnut marketing in rural Hausa Niger: The 1930s to the 1970s in Muzaria. Ph.D. dissertation. Johns Hopkins University, USA, 1974. GENTIL, D., The establishment of a new co-operative system in Niger. Paper repared for fJ$zd International Seminar on Change in Agriculture, Reading, England, 9-l 8 September,

CO-OPERATIVE CREDIT SERVICES IN NORTHERN NIGERIA 207

7. HUNTER, G., Agricultural administration and institutions. Paper delivered to Conference on Strategies for Agricultural Development in the IOs, Stamford University, USA, 13-16 December, 1971.

8. KING, R., The role of co-operatives in agricultural citvelopment with special reference to northern Nigeria. Paper presented at FAOINORAD West African Seminar on Agricultural Planning, Zaria, Ahmadu Bell0 University. 7th January-2nd February, 1974 (forthcoming).

9. TEXIER, J. M., The promotion of co-operatives in traditional rural societies. Paper prepared fpd;Gcond International Seminar on Change in Agriculture. Reading, England, 9-19 September,

10. ~&KXCIHNS, B. J., The co-operative movement in Nigeria. Ministry of Overseas Development, London, 1970.

![The Karnataka Co-Operative Socities Act - … Act.pdf1959: KAR. ACT 11] Co-operative Societies 1 THE KARNATAKA CO-OPERATIVE SOCIETIES ACT, 1959. ARRANGEMENT OF SECTIONS …](https://static.fdocuments.us/doc/165x107/5aa079647f8b9a8e178e0616/pdfthe-karnataka-co-operative-socities-act-actpdf1959-kar-act-11-co-operative.jpg)