EXPERIENCE ON THE PARTICIPATION OF WOMEN IN SAVING … · IN SAVING AND CREDIT COOPERATIVES IN...

31

EXPERIENCE ON THE PARTICIPATION OF WOMEN IN SAVING AND CREDIT COOPERATIVES IN DEGUA IN SAVING AND CREDIT COOPERATIVES IN DEGUA TEMBIEN WOREDA OF TIGRAY REGION, ETHIOPIA Berhane Ghebremichael (Assistant Professor) D t t f C ti St di MU Department of Cooperative Studies, MU Tel: +251938788787 1

Transcript of EXPERIENCE ON THE PARTICIPATION OF WOMEN IN SAVING … · IN SAVING AND CREDIT COOPERATIVES IN...

EXPERIENCE ON THE PARTICIPATION OF WOMEN

IN SAVING AND CREDIT COOPERATIVES IN DEGUA IN SAVING AND CREDIT COOPERATIVES IN DEGUA

TEMBIEN WOREDA OF TIGRAY REGION, ETHIOPIA

Berhane Ghebremichael (Assistant Professor) D t t f C ti St di MUDepartment of Cooperative Studies, MU

Tel: +251938788787

1

ContentContent

1. Introduction

2. Objectives

3. Methodology

4. Result and Discussion

5. Conclusions and Recommendations

2

Introduction

• Association in work as well as play is natural to manand that at a very early stage, mutual aid hady y gextended beyond the family group and taken on anorganization and fairly permanent form.

• Cooperative is a very basis of human civilization, theinterdependence of mutual help among human beingshave been the essential of social lifehave been the essential of social life.

• History tells us that man can’t successfully live byh lf d f h lf lhimself and for himself alone.

• The spirits of association are essential to human• The spirits of association are essential to humanprogress and sustainable development.

3

• In the process of economic development, women’sparticipation is importantparticipation is important.

• It would not be out of place to accept the socio-i t d d f i di t feconomic standard of women as an indicator of

development of the country because womenconstitute almost half of the population of Ethiopia.

• Women have got a number of useful contributions inthe development and advancement of cooperatives.the development and advancement of cooperatives.

• Cooperative principles state that Cooperatives ared ti i ti hi h th thdemocratic organizations which means they are theplace where people exercise their rights withoutgender discrimination.

4

Objectives:j

1. To investigate the level of participation of women inSACCOSACCO.

2 To analyze the economic gains derived by women2. To analyze the economic gains derived by womenmembers after joining the SACCO.

3. To identify the factors that affect the participationof the women in SACCO.

4. To suggest possible recommendations to enhancetheir participationtheir participation

5

Methodology

Data were gathered from primary and secondarysources..

A combination of qualitative data from FGD (a totalof 25 i e 16 from the four SACCOs and 9 expertsof 25 i.e. 16 from the four SACCOs and 9 expertsfrom woreda coop office) and quantitative data from110 respondents were elicited.

Structured interview schedule were used to identifythe economic role, decision making practice and, g pfactors affecting participation of respondents in theselected cooperative societies.

6

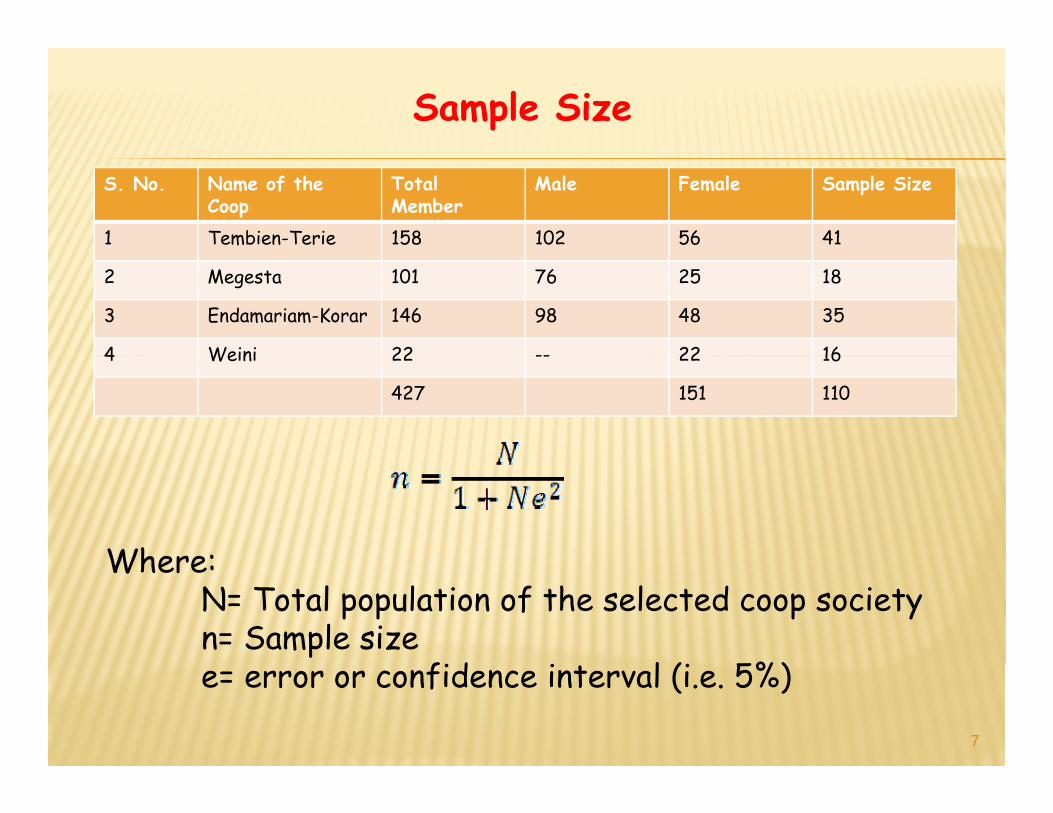

Sample Size

S. No. Name of the Coop

Total Member

Male Female Sample Size

1 Tembien-Terie 158 102 56 41

2 Megesta 101 76 25 18

3 Endamariam-Korar 146 98 48 35

4 Weini 22 -- 22 164 Weini 22 -- 22 16

427 151 110

Where:Where:N= Total population of the selected coop societyn= Sample size

f d l ( 5%)

7

e= error or confidence interval (i.e. 5%)

Data Analysis

Th d d d i i i i l h The study used descriptive statistical measures suchas mean, standard deviation, frequency, andpercentages.p g

The information is presented in graph, charts, tables,percentages and other methods on the basis of theirapplicabilityapplicability.

8

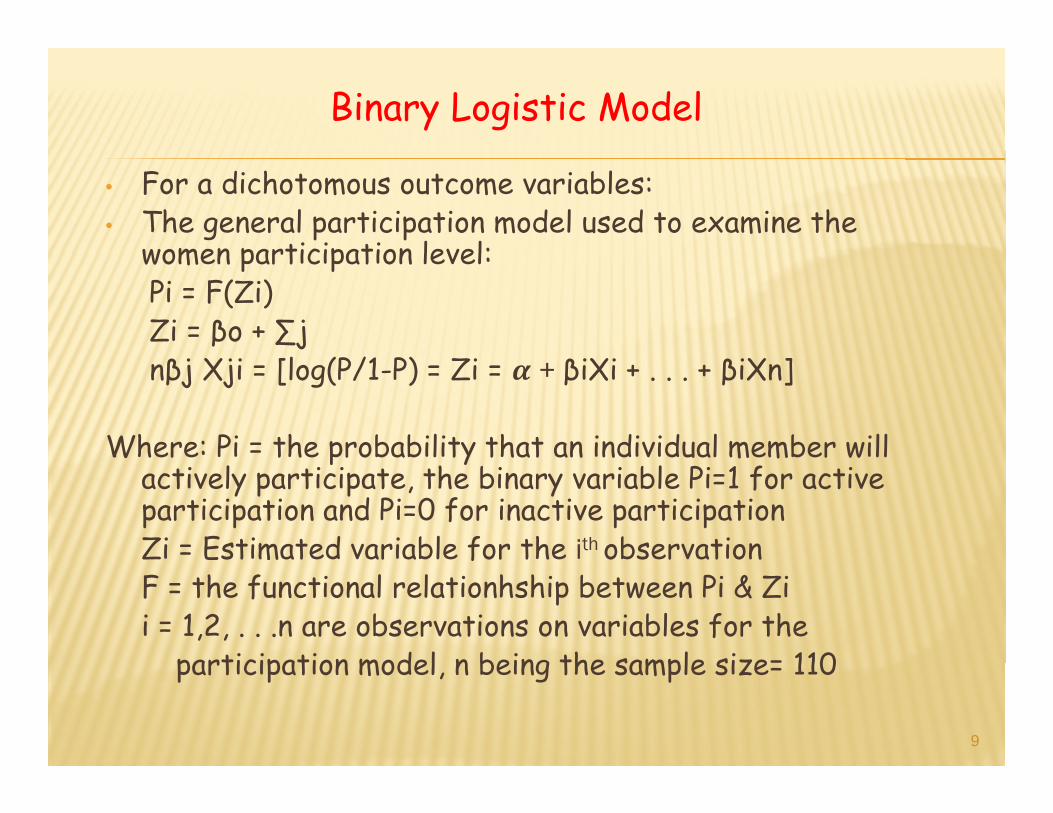

Binary Logistic Model

• For a dichotomous outcome variables: • The general participation model used to examine the

women participation level: women participation level: Pi = F(Zi) Zi = βo + ∑j nβj Xji = [log(P/1-P) = Zi = + βiXi + . . . + βiXn]

Where: Pi = the probability that an individual member will W p y m mactively participate, the binary variable Pi=1 for active participation and Pi=0 for inactive participation Zi = Estimated variable for the ith observationfF = the functional relationhship between Pi & Zii = 1,2, . . .n are observations on variables for the

participation model n being the sample size= 110 participation model, n being the sample size= 110

9

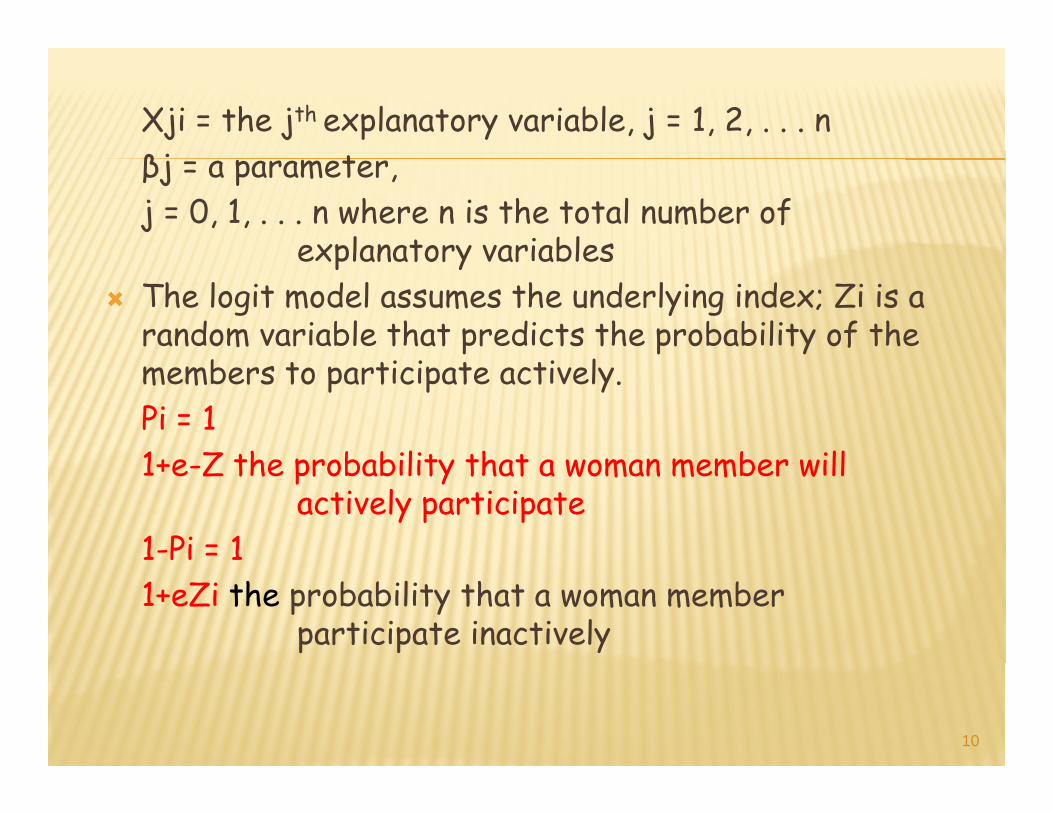

Xji = the jth explanatory variable, j = 1, 2, . . . n βj = a parameter, j = 0, 1, . . . n where n is the total number of

explanatory variables explanatory variables The logit model assumes the underlying index; Zi is a

random variable that predicts the probability of the members to participate actively. Pi = 11 Z th b bilit th t b ill 1+e-Z the probability that a woman member will

actively participate 1-Pi = 1 1+eZi the probability that a woman member

participate inactively

10

Result and Discussion

Demographic Characteristics of the Respondents

Age Distribution of the Respondents

40.00%

45.00%39.10%

44.50%

25.00%

30.00%

35.00%

10.00%

15.00%

20.00%

10.90%

5.50%

0.00%

5.00%

18-30 31-40 41-50 Above 50

5 50%

11

40.00%

Educational Status of the Respondents

30.00%

35.00%

40.00%

20.00%

25.00%

18.20% 18.20%

10.00%

15.00% 11.80% 11.80%

0.00%

5.00%

Illiterate 1 to 4 5 to 8 9 to 10 Above 10

12

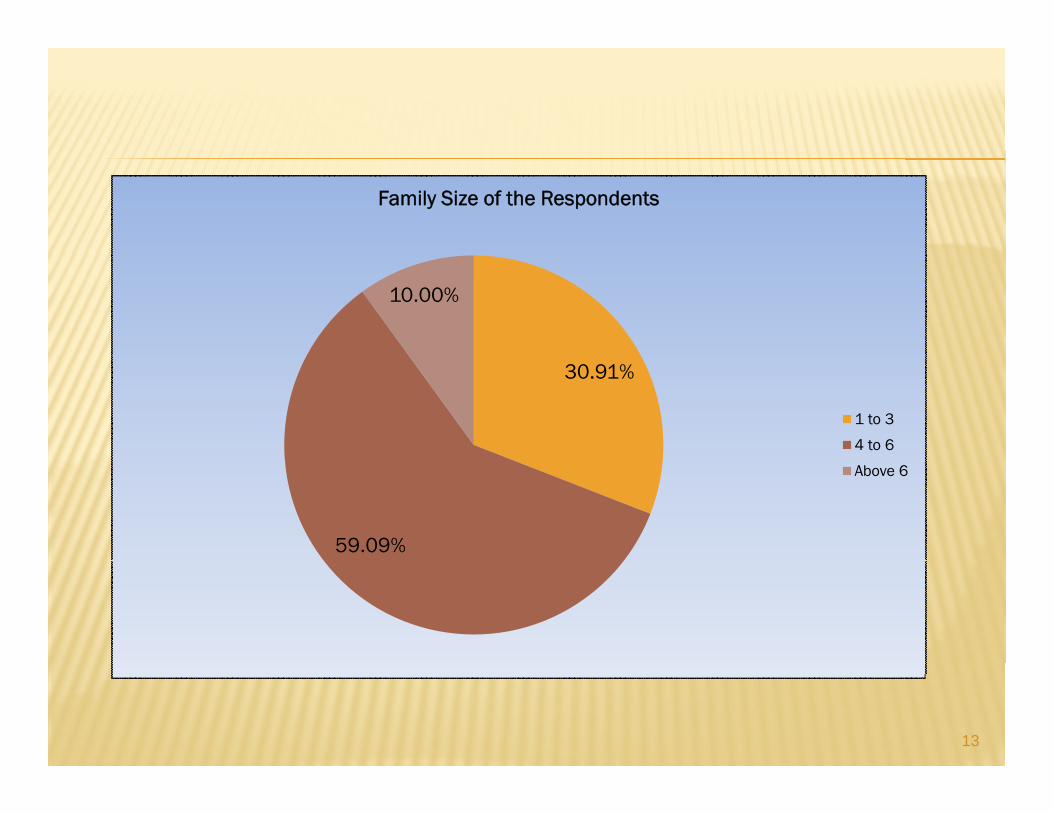

Family Size of the Respondents

10.00%

30.91%

1 to 3

4 to 6

59.09%

Above 6

13

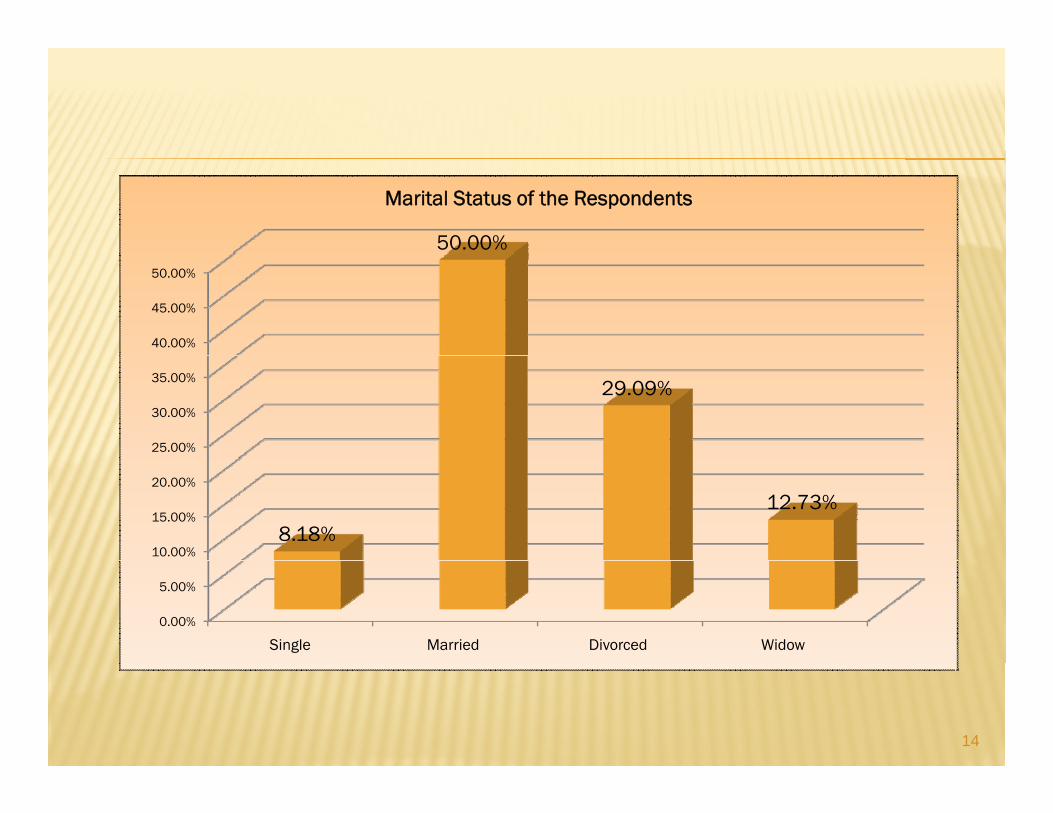

50.00%

Marital Status of the Respondents

40.00%

45.00%

50.00%

25.00%

30.00%

35.00%29.09%

10.00%

15.00%

20.00%

8.18%

12.73%

0.00%

5.00%

Single Married Divorced Widow

14

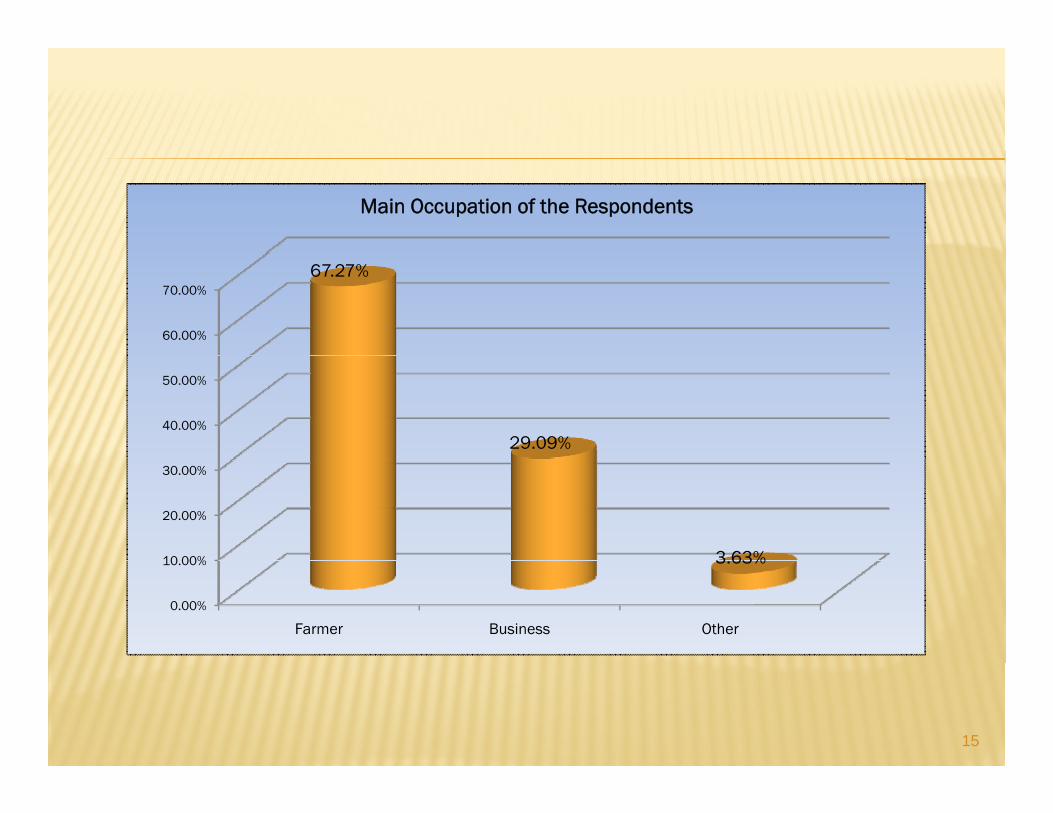

Main Occupation of the Respondents

60.00%

70.00%67.27%

40.00%

50.00%

29.09%

10 00%

20.00%

30.00%

3 63%

0.00%

10.00%

Farmer Business Other

3.63%

15

49 10%

Membership Duration of the Respondents

40 00%

45.00%

50.00%

49.10%

35 50%

30.00%

35.00%

40.00% 35.50%

15.00%

20.00%

25.00%

15.50%

0.00%

5.00%

10.00%

16

1 to 3 4 to 6 Above 6

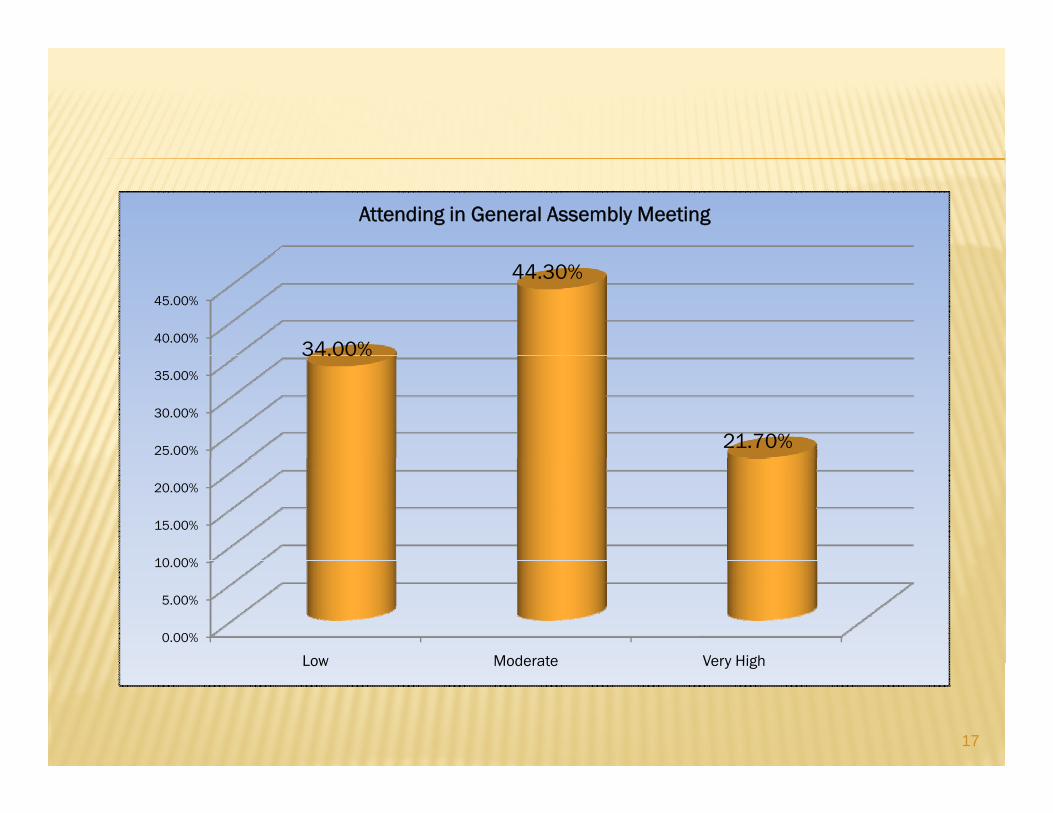

Attending in General Assembly Meeting

40.00%

45.00%

34.00%

44.30%

25.00%

30.00%

35.00%

34.00%

21.70%

10 00%

15.00%

20.00%

0.00%

5.00%

10.00%

Low Moderate Very High

17

Low Moderate Very High

Attending in Management Committee

50.00%

60.00%55.70%

30.00%

40.00%37.70%

10.00%

20.00%

6.60%

0.00%

Low Moderate Very High

18

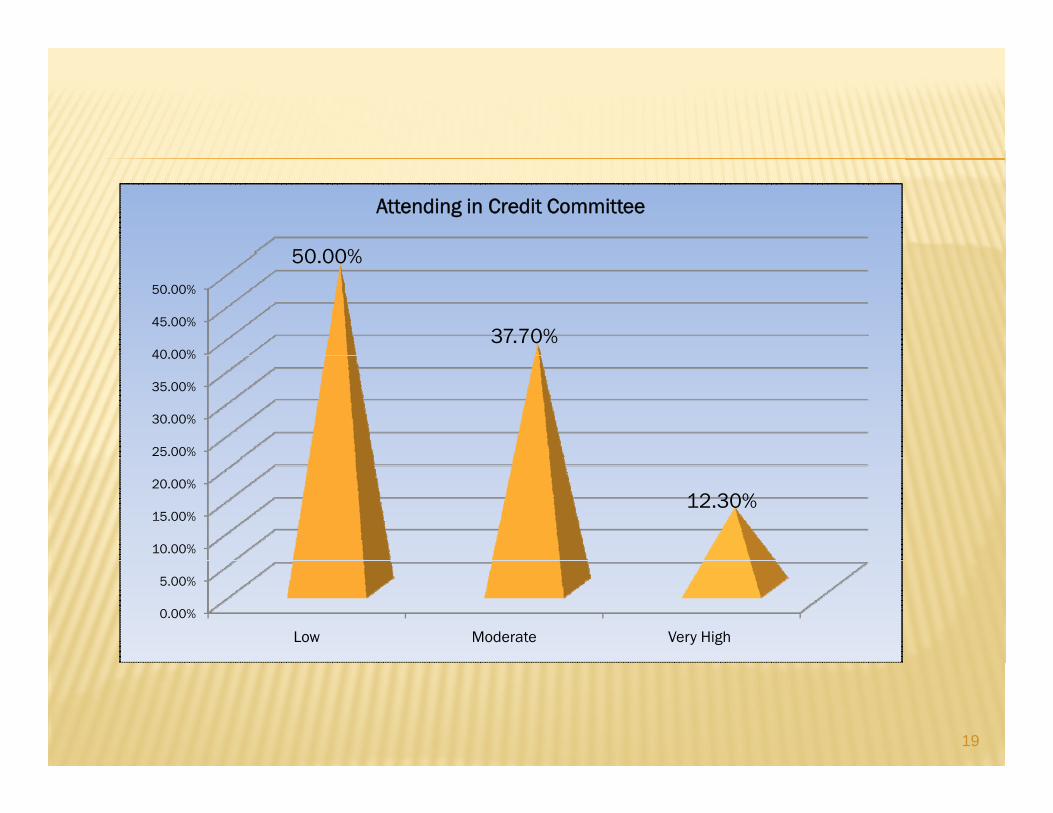

50 00%

Attending in Credit Committee

40 00%

45.00%

50.00%

50.00%

37.70%

25.00%

30.00%

35.00%

40.00%

10.00%

15.00%

20.00%12.30%

0.00%

5.00%

Low Moderate Very High

19

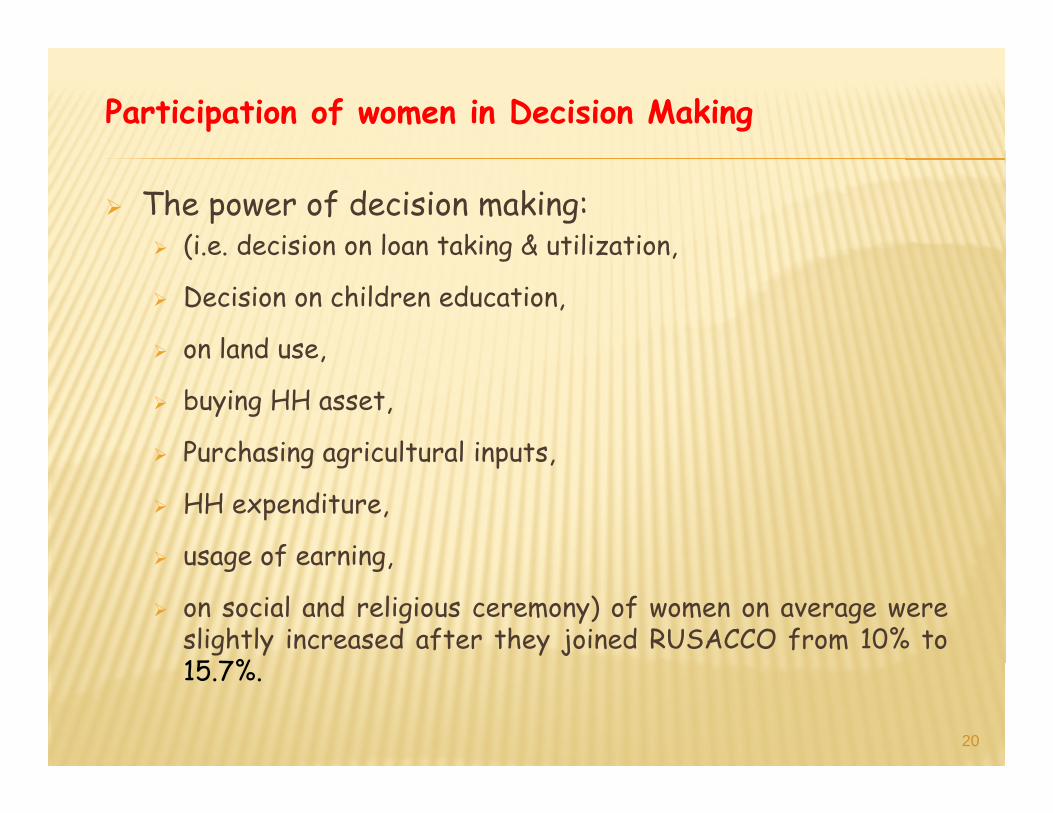

Participation of women in Decision Making

The power of decision making: (i.e. decision on loan taking & utilization, (i.e. decision on loan taking & utilization,

Decision on children education,

on land use on land use,

buying HH asset,

Purchasing agricultural inputs Purchasing agricultural inputs,

HH expenditure,

usage of earning usage of earning,

on social and religious ceremony) of women on average wereslightly increased after they joined RUSACCO from 10% to15 7%15.7%.

20

Participation of women in Training

The result revealed that 42.7% of the members ofthe RUSACCO have got different types of trainingsthe RUSACCO have got different types of trainingsbefore joining while 57.3% were not. But after joiningRUSACCO’s 62.8% have got training and still 38.2%were notwere not.

Moreover, the trainings before joining RUSACCO Moreover, the trainings before joining RUSACCOwere focused on general capacity building likeawareness creation in any development but afterjoining focused on saving and credit and all trainingsjoining, focused on saving and credit and all trainingswere given once an d less than a month.

21

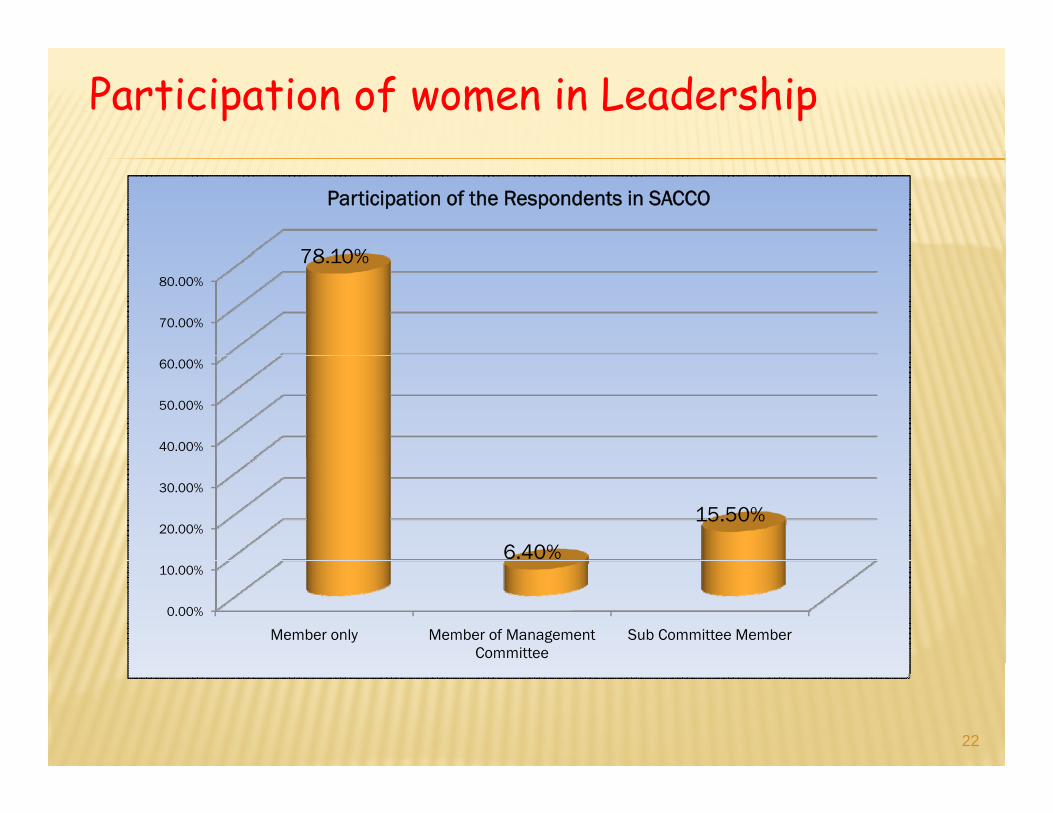

Participation of women in Leadership

78 10%

Participation of the Respondents in SACCO

70.00%

80.00%

78.10%

40.00%

50.00%

60.00%

20.00%

30.00%

6.40%

15.50%

0.00%

10.00%

Member only Member of Management Committee

Sub Committee Member

22

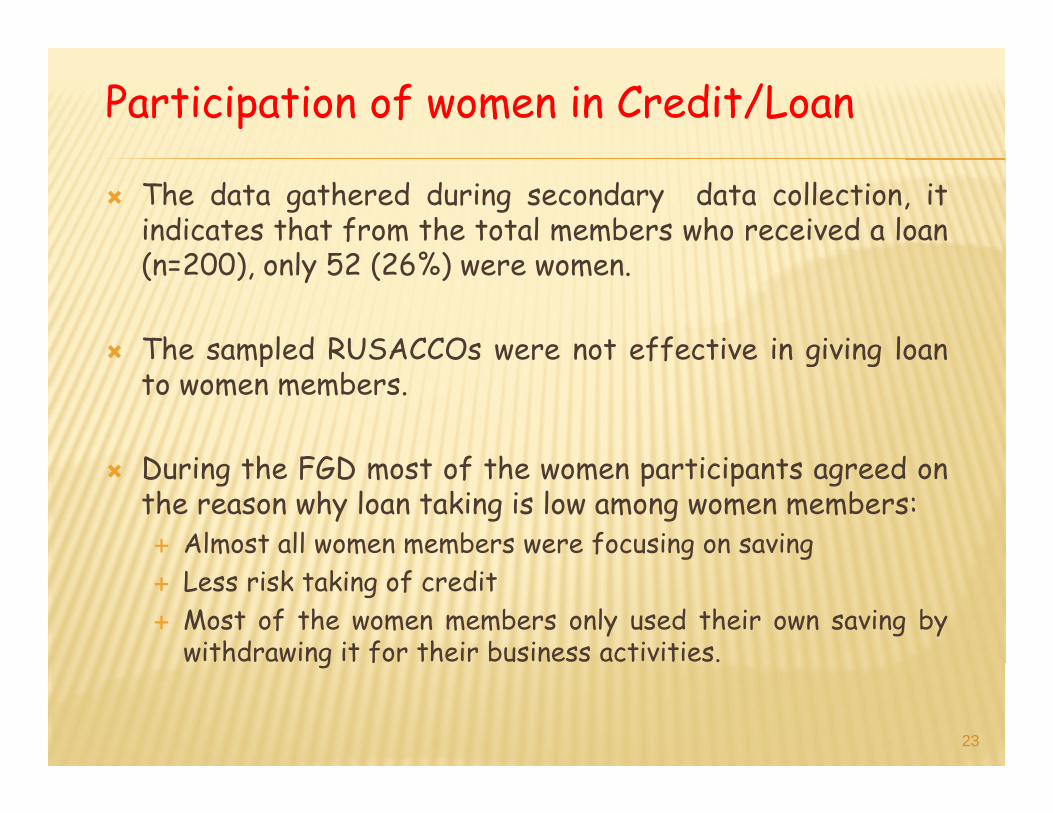

Participation of women in Credit/Loan

The data gathered during secondary data collection, itindicates that from the total members who received a loan( 200) l 52 (26%)(n=200), only 52 (26%) were women.

The sampled RUSACCOs were not effective in giving loan The sampled RUSACCOs were not effective in giving loanto women members.

D i h FGD f h i i d During the FGD most of the women participants agreed onthe reason why loan taking is low among women members: Almost all women members were focusing on saving Less risk taking of credit Most of the women members only used their own saving by

withdrawing it for their business activities.g f

23

Reason for Credit

Reasons for Credit

35.00%

40.00%

45.00% 42.00%

20.00%

25.00%

30.00% 24.70%

14 80%18.50%

Percent

5.00%

10.00%

15.00%

14.80%

0.00%

5.00%

To Buy Agricultural Inputs

To Start Income Generating Activities

For Consumption Other

24

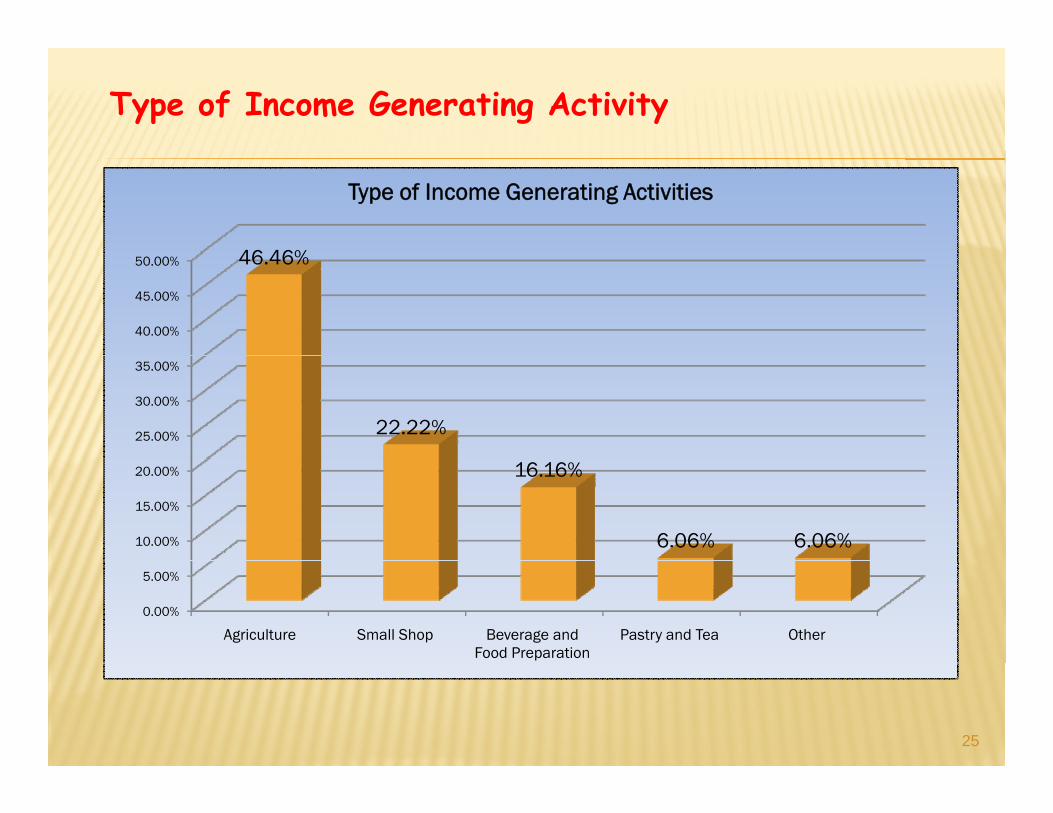

Type of Income Generating Activity

46 46%

Type of Income Generating Activities

40.00%

45.00%

50.00% 46.46%

25.00%

30.00%

35.00%

22.22%

10.00%

15.00%

20.00% 16.16%

6.06% 6.06%

0.00%

5.00%

Agriculture Small Shop Beverage and Food Preparation

Pastry and Tea Other

25

I d p d t β S E W ld Si

Econometric AnalysisIndependent Variable

β S.E. Wald Sig

Age -.210 .365 .331 .565Education -.040 .199 .040 .842Membership .216 .507 5.763 .016**Training .136 .693 2.237 .035**n ng . 6 .69 . .Saving .786 .594 9.025 .003***Income .737 .302 5.952 .015**Credit/Loan 338 664 259 611Credit/Loan -.338 .664 .259 .611Family Size .913 .647 1.993 .158Main

ti5.164 4.769 1.173 .279

occupationShare .484 4.705 .011 .918Dividend 1.686 1.374 1.507 .220Constant 5.302 2.598 4.165 .041

26*** Significant at the 0.01 level (2-tailed)** Significant at the 0.05 level (2-tailed)

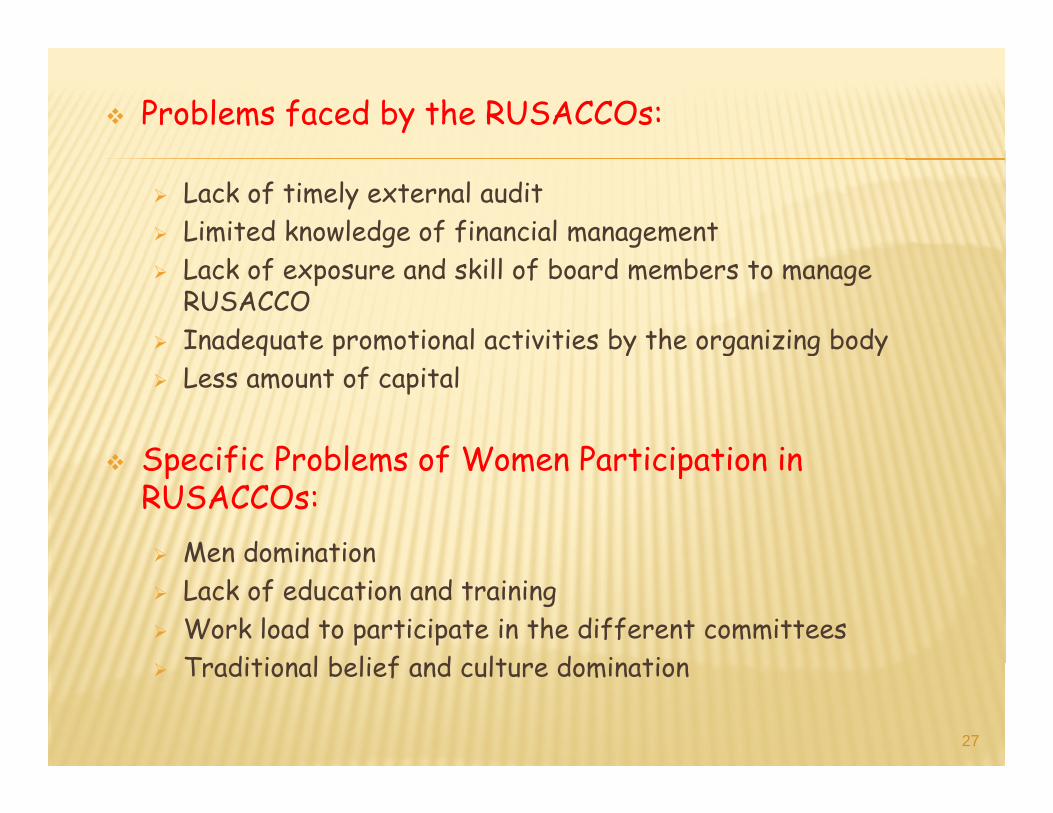

Problems faced by the RUSACCOs:

Lack of timely external audit Limited knowledge of financial management Lack of exposure and skill of board members to manage

RUSACCO Inadequate promotional activities by the organizing body q p y g g y Less amount of capital

Specific Problems of Women Participation in Specific Problems of Women Participation in RUSACCOs: Men domination Men domination Lack of education and training Work load to participate in the different committees Traditional belief and culture domination Traditional belief and culture domination

27

Conclusion

Women in Ethiopia encounter several problems that are multi faceted. Cooperatives have been considered as means of pempowering resource poor women who have no access to formal financial facilities economically.

They promote the provision of saving, loan, training, and information services to the members.

Women represent greater than 50% of the total population in the study area. SACCOs have a great potential to become a stronger economic and more influential force if more women are stronger economic and more influential force if more women are actively involved in cooperative movement.

In the study; it was clearly observed that the level of women In the study; it was clearly observed that the level of women participation in all activities was very low.

28

Recommendations

Thorough and continuous awareness creation, training, andeducation program which are sensitive to women need.

Cooperatives should review their saving policiesperiodically for sustainability and benefit of their womenmembersmembers.

The cooperative should introduce gender related trainingt th i b s t i i i th bl f ltto their members to minimize the problem of cultureinfluence.

h f d l d l The federal cooperative agency and regional cooperativebureaus should encourage of establishing more number ofwomen SACCOs to minimize thinking that men dominate inall casesall cases.

29

The federal cooperative agency and regional cooperativebureaus should encourage in advocating and increasing thebureaus should encourage n advocat ng and ncreas ng thesaving and thrift culture of the people at large and greatemphasis to women.

Continuous and sustainable radio and television programs arealso needed to upgrade the know how about SACCO to bring

th ti i ti fup the participation of women.

Special saving and credit package for women in collaboration Special saving and credit package for women in collaborationto governmental and NGOs.

30