Executive Remuneration Emerging Trends S H A N G H A I · TOTAL COMPENSATION FRAMEWORK TYPICAL...

23

© MERCER 2019 0 Executive Remuneration – Emerging Trends SHANGHAI MERCER GLOBAL HR CONFERENCES SEPTEMBER 18-19 Calvin Chen Head of Executive Remuneration Mercer China [email protected]

Transcript of Executive Remuneration Emerging Trends S H A N G H A I · TOTAL COMPENSATION FRAMEWORK TYPICAL...

© MERCER 2019 0

Executive Remuneration –

Emerging Trends

S H A N G H A I

M E R C E R G L O B A L H R C O N F E R E N C E S

SEPTEMBER 18-19

Calvin Chen

Head of Executive Remuneration

Mercer China

© MERCER 2019 1

Global ER Trends

© MERCER 2019 2

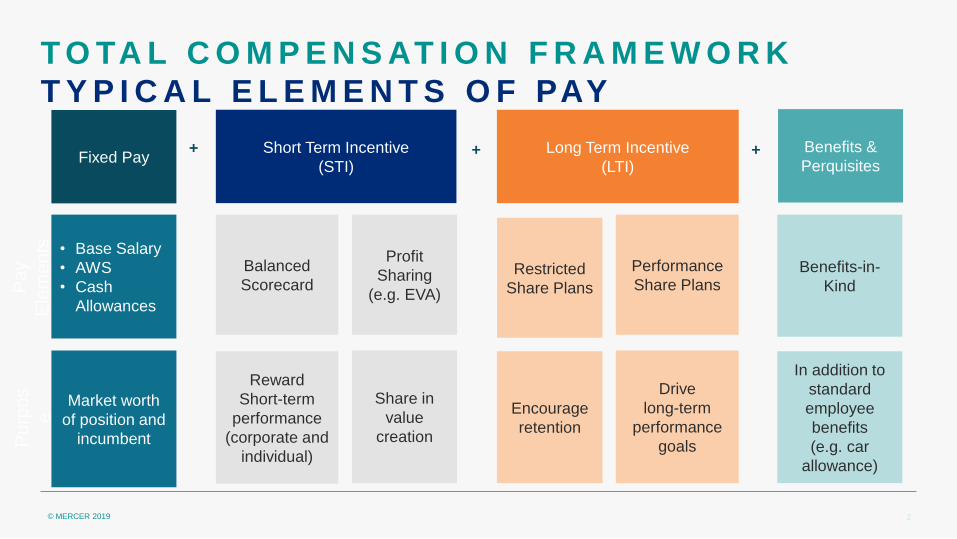

T O TA L C O M P E N S AT I O N F R A M E W O R K

T Y P I C A L E L E M E N T S O F PAY

Fixed Pay Short Term Incentive

(STI)

Long Term Incentive

(LTI)

Benefits &

Perquisites

• Base Salary

• AWS

• Cash

Allowances

Balanced

Scorecard

Profit

Sharing

(e.g. EVA)

Benefits-in-

Kind

Market worth

of position and

incumbent

Reward

Short-term

performance

(corporate and

individual)

Share in

value

creation

Encourage

retention

Drive

long-term

performance

goals

In addition to

standard

employee

benefits

(e.g. car

allowance)

Restricted

Share Plans

Performance

Share Plans

+ + +

Pa

y

Ele

me

nts

P

urp

os

e

© MERCER 2019 3

E X E C U T I V E R E M U N E R A T I O N

G L O B A L T R E N D S

Pay Opportunity Constant – The maximum earning opportunity in US

and European markets has broadly remained constant in the last 5

years but actual payouts (realized pay) have actually declined in the

past 3 years for CEO’s – broadly flat for other executives.

Strategic KPI Usage – TSR usage has flattened out and non-

GAAP metrics (e.g. FCF, adjusted EPS, EBIT) are becoming

more common – both in prevalence and weightage. ESG

measures (carbon emissions, workforce diversity, cybersecurity)

are increasingly being used as well.

Workforce Relativity – Disclosures of CEO to median

employee pay and gender pay gaps in organisations being

mandated to address public concerns around pay inequity

Shareholding Requirements – Post-vesting holding periods (typically

2 years) and higher shareholding requirements (3-5 times of salary for

CEOs) are becoming increasingly common

© MERCER 2019 4

S & P 5 0 0 : V E H I C L E U S A G E

S T O C K I S T H E M O S T P R E VA L E N T

V E H I C L E S A M O N G S & P 5 0 0 C O M PA N I E S .

16.1% 18.6% 19.9% 22.3% 25.9% 30.7% 34.6% 37.9% 34.7% 37.9% 40.9% 16.8% 13.0% 10.7% 8.1%

6.8% 5.1%

4.3% 3.3% 1.5%

1.8% 1.4%

63.5% 66.1% 66.5% 67.5% 65.5% 62.3% 59.6% 57.4% 62.9% 58.3% 55.6%

3.6% 2.3% 2.9% 2.1% 1.8% 1.9% 1.5% 1.4% 0.9% 2.0% 2.1%

0%

20%

40%

60%

80%

100%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Stock Options Both Neither

Source: Mercer, Equilar

© MERCER 2019 5

S & P 5 0 0 : K P I F O R LT I P L A N

T S R I S T H E M O S T P R E VA L E N T K P I F O R

LT I P L A N

46%

24%

18%

TSR EPS/NetIncome

Revenue

All Industry

47%

25% 21%

TSR Revenue OperatingIncome

High-tech

Source: Mercer, Equilar

37% 35%

30%

TSR Revenue EPS

Consumer

© MERCER 2019 6

A - S H A R E : V E H I C L E U S A G E

R S I S S T I L L T H E D O M I N A N T V E H I C L E • Though has its own pitfalls, RS is still a very popular vehicle in A-Share. An increasing number of

companies are buying-back shares as the source of equity to implement RS plan.

3.33%

20.00%

16.67%

60.00%

Options to RS

RS to Optioins

Keep using Options

Keep using RS

74% 74% 78% 69%

24% 24% 21% 31%

1% 1% 0% 0%

2015 2016 2017 2018

RS Options SAR

Vehicle usage for Companies implementing LTI plan

in 2017 and 2018 A-Share LTI Vehicle(2015-2018)

Source: Mercer

© MERCER 2019 7

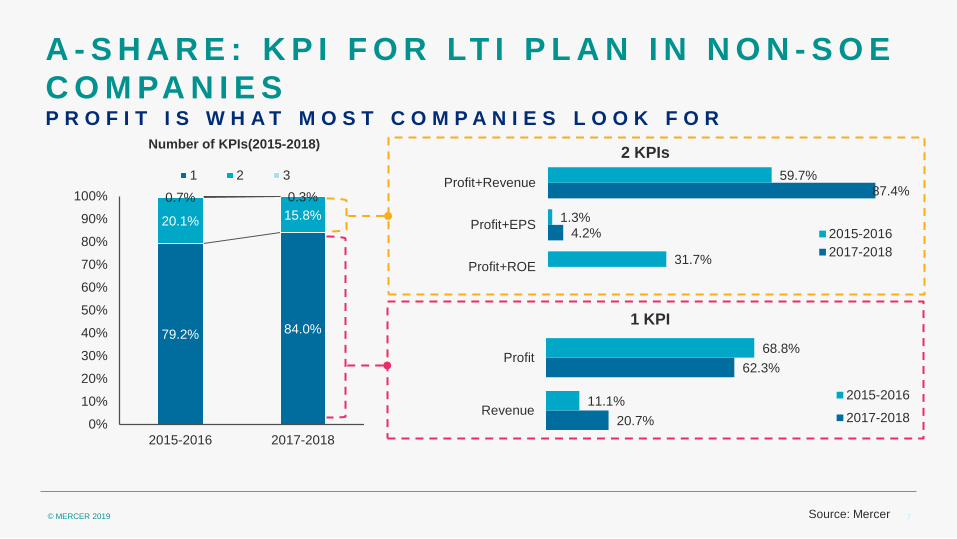

79.2% 84.0%

20.1% 15.8%

0.7% 0.3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015-2016 2017-2018

1 2 3

A - S H A R E : K P I F O R LT I P L A N I N N O N - S O E

C O M PA N I E S P R O F I T I S W H A T M O S T C O M P A N I E S L O O K F O R

Number of KPIs(2015-2018)

4.2%

87.4%

31.7%

1.3%

59.7%

Profit+ROE

Profit+EPS

Profit+Revenue

2 KPIs

2015-2016

2017-2018

20.7%

62.3%

11.1%

68.8%

Revenue

Profit

1 KPI

2015-2016

2017-2018

Source: Mercer

© MERCER 2019 8

E X E C U T I V E R E M U N E R A T I O N

L O N G T E R M I N C E N T I V E S – D O T H E Y D E L I V E R ?

LTI plans allow firms to tie in organizational objectives with executive performance and then allow for sustained long term value creation and better returns for

shareholders.

GROW TH RATE NET INCOME (14-18)

Firms with LTI Plan(s) 12%

Firms without any LTI Plans 3%

(N=100)

GROW TH RATE ROCE (14-18)

Firms with LTI Plan(s) 3%

Firms without any LTI Plans -1%

Dividend Yield (14-18)

© MERCER 2019 9

What’s Different In China

© MERCER 2019 10

W H A T ’ S D I F F E R E N T I N C H I N A -

P R E - I P O E Q U I T Y I N C E N T I V E I S I N G R E A T P O P U L A R I T Y

• Founder also plays the

role as CEO.

• Family-owned

business.

• Weak board, no formal

supervision of ER.

C o r p o r a t e

G o ve r n a n c e

1 • Enthusiasitic investors

• High appetite of risks in

the private financing

rounds.

• IPO is a way to

measure fortune and

success

C a p i t a l

M a r k e t

2 • High pressure of living

in big cities.

• Lots of millionair

fairytales.

• Eager to change life.

E m p l o ye e ’s

E x p e c t a t i o n

3

© MERCER 2019 11

LT I V E H I C L E S F O R P R I VAT E C O M PA N I E S

I N C H I N A • For the 35 high-tech companies listed in U.S. 71% of them are using options as their

vehicles

71%

37%

6%

23%

Option

RS

Others

No LTI plan

Source: Company filings

© MERCER 2019 12

K E Y C O N S I D E R AT I O N S W H E N C H O O S I N G O P T I O N S

• Legal structure

• Local law compliance

Legal

• Income tax implication

• Possible tax

deduction(No. 101)

Tax

• Measure the

contribution

• Fair and easy to

manage.

Business

• Don’t have to make

No.37 registration.

FX

© MERCER 2019 13

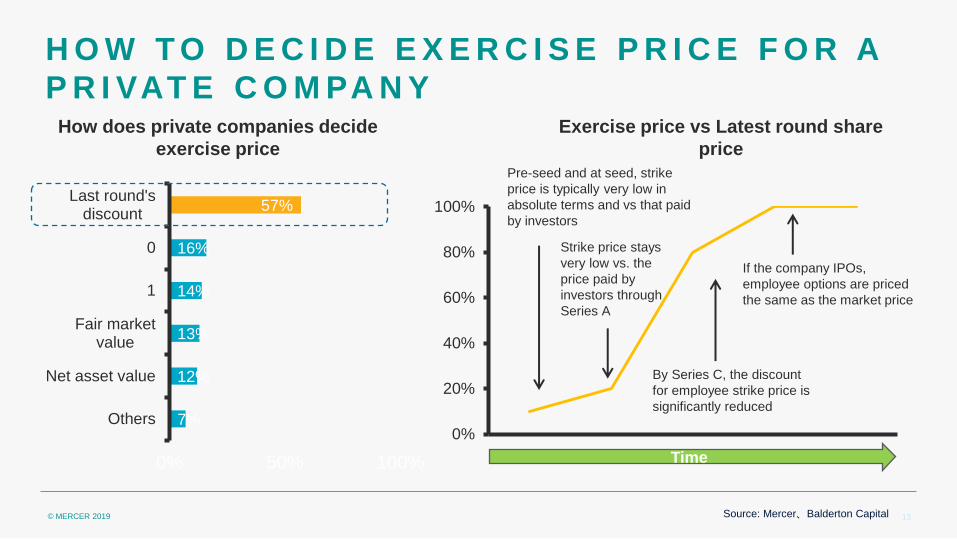

H O W T O D E C I D E E X E R C I S E P R I C E F O R A

P R I VAT E C O M PA N Y

7%

12%

13%

14%

16%

57%

0% 50% 100%

Others

Net asset value

Fair marketvalue

1

0

Last round'sdiscount

Source: Mercer、Balderton Capital

0%

20%

40%

60%

80%

100%

How does private companies decide

exercise price

Exercise price vs Latest round share

price

Pre-seed and at seed, strike

price is typically very low in

absolute terms and vs that paid

by investors

Strike price stays

very low vs. the

price paid by

investors through

Series A

By Series C, the discount

for employee strike price is

significantly reduced

If the company IPOs,

employee options are priced

the same as the market price

Time

© MERCER 2019 14

34.9%

100.0%

85.2%

71.6% 66.0%

43.3%

0%

20%

40%

60%

80%

100%

PA R T I C I PAT I O N R AT E

3 5 % O F T H E T O TA L E M P L O Y E E W I L L

PA R T I C I PAT E I N T H E P R E - I P O I N C E N T I V E

P L A N

Source: Mercer

COMPANY OVERALL CEO VP MID MANAGEMENT PROFESSIONALS

(TECH)

PROFESSIONALS

(NON-TECH)

75%ile

50%ile

25%ile

© MERCER 2019 15

Effective Long Term

Incentive (LTI) Design

Considerations

© MERCER 2019 16

L O N G T E R M I N C E N T I V E P L A N O B J E C T I V E S

A D I F F I C U L T B A L A N C I N G A C T

Organisation Perspective Employee Perspective

EFFECTIVE INCENTIVE PLAN

Performance Linkage

Retention

Shareholder Alignment

Affordability

Achievability

Sizeable Award

Ability to Influence

Fair & Simple

© MERCER 2019 17

K E Y L T I P L A N D E S I G N C O N S I D E R A T I O N S

T H O U S A N D S O F D E S I G N C O M B I N A T I O N S

Objectives Performance

Eligibility

Award Size

Plan Type

Performance

Measurement

Plan Mechanics

Grant Frequency

Exercising

Accounting/ Tax

Retention Market

Competitiveness

Shareholder

Alignment

Top Executives only Top Executives &

Mid Management All Employees Key Talent

Market Aligned Desired Pay-Mix Internally Consistent

Performance Shares Restricted Shares Stock Options Cash Plan

KPI Targets Peer Comparison Share Price Movement

High/Low Leverage Wide/Narrow Performance

Range Capped/ Uncapped

Annually Discretionary Periodically One-time Only

Shares Cash All at once Deferred over time

Total Cost Company/ Individual

Tax Accrual Time Adjustment Provisions

© MERCER 2019 18

A W A R D S I Z E D E T E R M I N A T I O N - M A R K E T B E N C H M A R K I N G

K E Y D E C I S I O N C R I T E R I A

Business Size

Industry

Geography

Disclosure

Proposed Peer Group

Financials (i.e. Revenue, Market Cap) between 50% - 200% of that of your company

Companies operating in a similar or related sector

Companies that have a similar regional/global presence and scope

Organisations with sufficient details of executive pay in public disclosures

Select between 10-15 Companies that meet these criteria to compose the peer group

No peer group is perfect as no two businesses are the same. But using the filters below, select a peer group that resembles your talent market as closely as

possible

Outcome? Pay-mix compared to Market Target Total Compensation Position

© MERCER 2019 19

T Y P E S O F L O N G - T E R M I N C E N T I V E P L A N S

Business objectives Stock Options/SARs Restricted Shares Performance Shares Long-term Cash/ Bonus

Deferral

Align employees’ and

shareholders’ interest

Staff retention

Increase Shareholders’ Value

Minimize share dilution Good Average Poor

High Upside Retention key Performance led No Shares

No Dilution Concern Dilution concern Direct Linkage b/w

Performance & Reward

Managed Cost (budget

set aside)

Difficulty in KPI Selection/

Target Setting

Difficulty in KPI Selection/

Target Setting

Clarity in Key Business

Drivers & Forecasts

Can be performance

related or retention led

Shareholder Aligned Simplicity desired Shareholder Aligned

Plan Suitability

© MERCER 2019 20

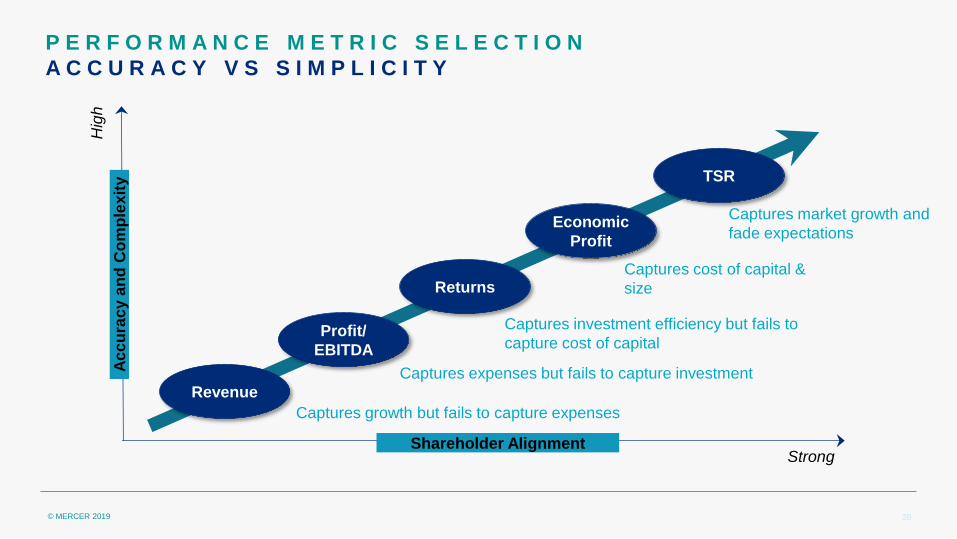

P E R F O R M A N C E M E T R I C S E L E C T I O N

A C C U R A C Y V S S I M P L I C I T Y

Strong Shareholder Alignment

Ac

cu

rac

y a

nd

Co

mp

lex

ity

Revenue

Economic

Profit

TSR

Profit/

EBITDA

Returns

Captures growth but fails to capture expenses

Captures expenses but fails to capture investment

Captures investment efficiency but fails to

capture cost of capital

Captures cost of capital &

size

Captures market growth and

fade expectations

Hig

h

© MERCER 2019 21

D E T E R M I N I N G R I G H T K P I S ’ A N D T A R G E T S

E V I D E N C E B A S E D D E C I S I O N M A K I N G

KPI SELECTION – KEY TESTS

L E A D V S L A G

I N D I C A T O R

B U S I N E S S S T R A T E G Y

A L I G N M E N T

V A L U E D R I V E R

A N A L Y S I S

P E R F O R M A N C E

S E N S I T I V I T Y A N A L Y S I S

TARGET SETTING – KEY TESTS

H I S T O R I C

P E R F O R M A N C E

M A N A G E M E N T

F O R E C A S T S

H I S T O R I C P E E R

P E R F O R M A N C E A N A L Y S T S F O R E C A S T S

© MERCER 2019 22

![TZ PUBLIC SERVICE PAY AND INCENTIVE POLICY.[1] · PDF filePUBLIC SERVICE PAY AND INCENTIVE POLICY ... 1.3 The Medium Term Pay Policy ... To adopt a compensation structure where allowances](https://static.fdocuments.us/doc/165x107/5ab933e67f8b9ac10d8de8de/tz-public-service-pay-and-incentive-policy1-service-pay-and-incentive-policy.jpg)